Yves here. This post makes an interesting observation: that demand for traded goods is unusually high, presumably due to catchup after Covid-induced supply chain interruptions and perhaps even some stockpiling. It then works though how this pattern plays into inflation and growth.

By Luca Fornaro, Junior Researcher, CREI; Adjunct Professor, Universitat Pompeu Fabra; Research Professor, Barcelona GSE and Federica Romei, Assistant Professor, Stockholm School of Economics; CEPR Research Affiliate. Originally published at VoxEU

Since the start of the pandemic, global demand for tradable goods relative to non-tradable services has been exceptionally high. This column argues that this unusual demand pattern can push the global economy into stagflation, driven by scarcity of tradable goods. Countries running trade deficits export high inflation abroad, while policies that boost production of tradable goods and current account surpluses act as a benign disinflationary force. Due to a free riding problem, national monetary authorities may fall into a coordination trap leading to excessively high unemployment. High energy prices exacerbate all these effects.

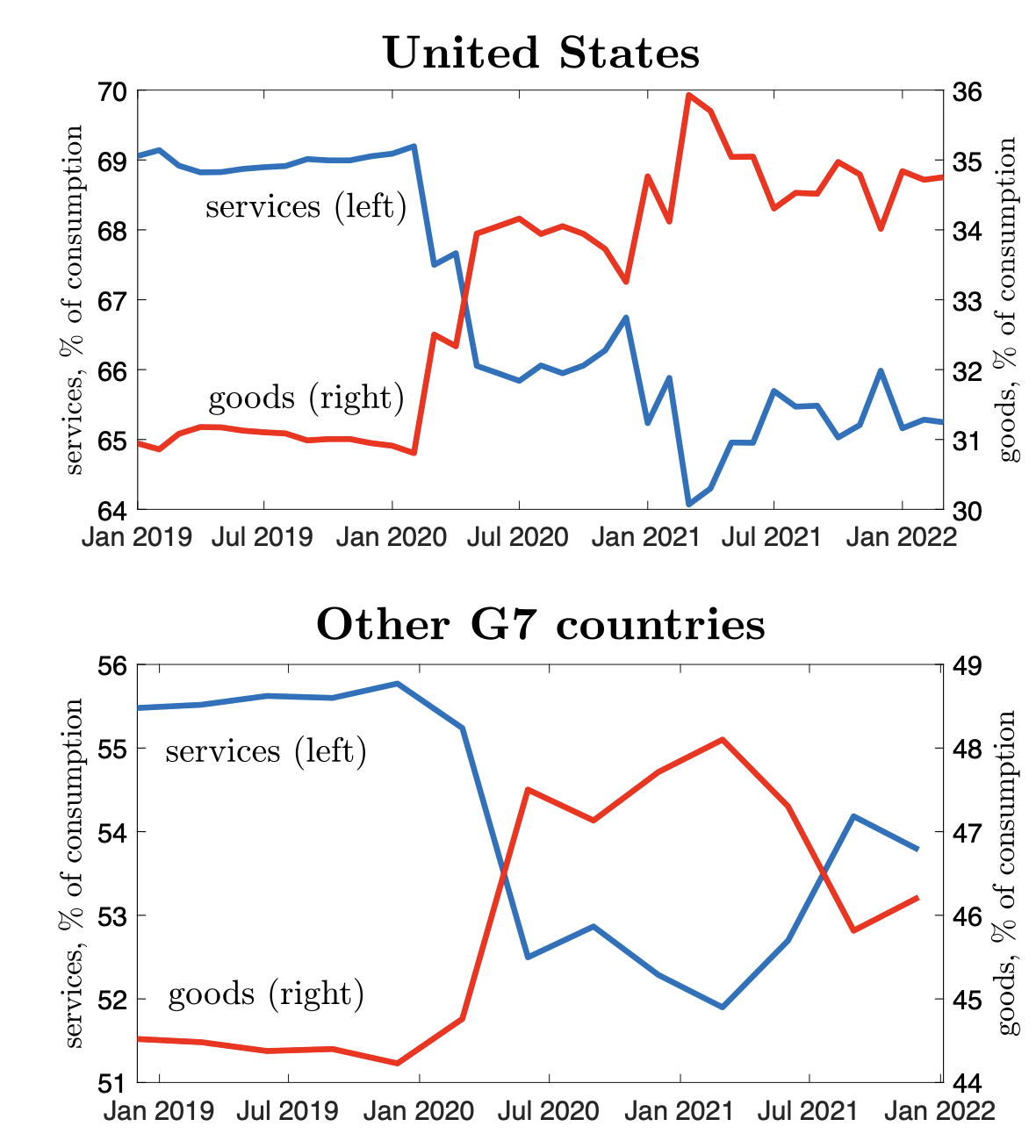

A salient feature of the ongoing recovery from the Covid-19 recession is its unbalanced nature. Throughout the world, demand for goods is buoyant, while demand for contact-intensive services is subdued (Figure 1). Considering that goods are typically traded across countries while most services are not, the global economy is effectively experiencing a large reallocation of demand away from non-tradable services and towards tradable goods. Unsurprisingly, this period of exceptionally high global demand for goods is associated with rising goods prices, and stress on the global supply chains (Eo et al. 2022).

Figure 1 Goods and services share in total consumption expenditure

Note: See Fornaro and Romei (2022a) for data sources.

n a recent paper (Fornaro and Romei 2022a), we propose a multi-country Keynesian model with multiple sectors to understand the macroeconomic implications of this unusual demand pattern. Our analysis is organised around three questions: What is the optimal monetary policy response to a reallocation of global demand from services to goods? How are international spillovers shaping the global recovery and the inflation outlook? Are there gains from international cooperation?

Monetary Policy and the Structuralist Approach to Inflation

We study a world composed of countries producing tradable goods and non-tradable services. Nominal wages are rigid, so that monetary policy has real effects, and involuntary unemployment may arise due to weak demand. We consider a global reallocation shock, that is, a temporary rise in consumers’ demand for goods relative to services, leading to an increase in the share of consumption expenditure on goods similar to the one observed during the pandemic.

Our first insight is that this reallocation of demand from services to goods can push the global economy into stagflation. Intuitively, lower demand induces firms in the service sector to reduce production and fire part of their workforce. To contain the increase in unemployment, a rise in inflation in the traded sector is needed. On the one hand, higher prices induce firms in the goods sector to hire more workers and increase production. Moreover, as workers receive more income from the tradable sector, their demand for services rises.1 Through this income effect, higher goods prices lift employment in the service sector too.

The optimal monetary policy trades off the costs arising from high inflation against the employment gains.2 A reallocation shock thus acts as a cost-push shock, leading to a contemporaneous rise in inflation and unemployment. These results are in line with the structuralist view of inflation (Olivera 1964, Tobin 1972, Guerrieri et al. 2021), which argues that some inflation is needed to reallocate smoothly workers across different sectors. This literature, however, has mainly focused on closed economies, while we are interested in its international implications.

Capital Flows, Trade Imbalances, and Inflationary Spillovers

In a financially integrated world, a country can increase its consumption of traded goods by borrowing from the rest of the world and running trade deficits. Indeed, in our model the regions experiencing the strongest increase in demand for traded goods adjust by running trade deficits toward the rest of the world. This helps explain why the US trade balance deteriorated during the recovery from the Covid-19 recession, since in the US the rise in goods consumption has been particularly pronounced.

Trade deficits, however, generate international inflationary spillovers. When a country runs a trade deficit, it exacerbates the scarcity of tradable goods on the global markets and worsens the trade-off between inflation and employment in the rest of the world. Through this channel, a country experiencing a rise in its demand for tradable goods exports high inflation abroad.

Our work thus formalises the notion that global factors are playing an important role in the recent rise in inflation, which was largely synchronised among advanced economies (Forbes et al. 2021). It also warns against the use of inflation differentials to measure the strength of relative demand, say between the US and the euro area. The reason is that high goods demand in the US, and the associated trade imbalances, lifts inflation in the euro area too. A more complete approach to understanding demand differentials should thus look at a combination of inflation and trade imbalances.

Free Riding and Gains from Monetary Policy Cooperation

We also highlight the presence of a free riding problem among national central banks, arising when global demand for tradable goods is exceptionally high. When a country implements a monetary expansion, it fosters its production of traded goods and increases its net exports toward the rest of the world, thus easing pressure on the global markets for tradables. As global consumers gain access to a greater supply of tradable goods, their demand for non-tradable services rises. Through this channel, a monetary expansion lifts aggregate demand and employment not only domestically, but in the rest of the world as well.

The presence of this international aggregate demand spillover implies that national central banks are likely to fall in a coordination trap. The reason is simple. The inflation costs associated with monetary expansions are fully borne by domestic agents. The gains in terms of higher demand and employment, instead, are partly enjoyed by the rest of the world. National monetary authorities have thus an incentive to free ride on foreign monetary expansions, meaning that lack of international cooperation may lead to excessive unemployment during periods of exceptionally high demand for tradable goods.

This result is connected to the debate on the international externalities triggered by countries running large trade surpluses. A long tradition argues that current account surpluses are detrimental when global demand is scarce, because they export abroad domestic demand weaknesses.3 But we show that things are very different when global demand for tradable goods is high, such as during the recovery from the Covid-19 recession. In this case, policies that foster the domestic production of tradable goods – and current account surpluses – alleviate the pressure on the global goods market, and act as a benign disinflationary force on the rest of the world. These considerations suggest that current account surpluses should be discouraged when global demand is weak but encouraged when the weakness is on global supply. Of course, this makes designing a system to regulate international trade imbalances a daunting task.

Energy Shocks in the Global Economy

Partly due to the Russian invasion of Ukraine, global energy prices are rising fast. In ongoing work (Fornaro and Romei 2022b), we show that a rise in energy prices exacerbates all the stagflationary forces described above. High energy prices, in fact, increase production costs for manufacturing firms, leading to a global scarcity of tradable goods. As discussed above, when traded goods are scarce, central banks face a trade-off between inflation and employment, trade deficits impose deflationary spillovers toward the rest of the world, and monetary expansions produce positive demand spillovers in foreign countries. The main difference is that in this case the euro area, due to its dependence on Russian energy, is likely to be the worst hit region, meaning that the ECB may face a particularly harsh trade-off between containing inflation and sustaining economic activity.

See original post for references

Oil prices are really being caused by the huge disinvestment in ICE vehicles and new investment in electric vehicles. It has been going on starting in 2020 and is now a full scale tidal wave. Big oil has a 5 year time frame to recover capital on land wells and 10 years on sea wells, fracking has 0 cash flow. 68% of oil goes to cars and class 8 diesel.

In five years electric cars could be 25% of vehicles sold and maybe 12% of cars on the road. This takes a huge chunk out of oil sales. They stopped investing for this reason — market discipline— it is called on wall street. We will realize later that this is a big part of Putins strategy He had to attack now because in 5 years Europe the free market will not need his oil or gas. The energy inflation will persist for about 5 years. Electric cars will get cheaper and charged on off peak power which is currently being wasted or new renewables. Energy inflation will be lower than in the past.

Gasoline comprises only 44% of oil consumption in the US, and personal vehicles account for a little more than half. So only 25% of oil production goes to the market segment where electric vehicles will have presence in the next 5 years. New Vehicle sales are ~15 million per year, but there is 280 million vehicles in the US, so even if new electric vehicle sell 15 million over the next 5 years, they will only comprise about 6% of vehicles on the road (currently 2.5 million).

So even assuming very optimistic conditions, you are looking at 1.5% decrease in oil consumption due to new electric vehicle sales. These numbers are for the US, keep in mind that the rest of the world has even less of a chance to push electric vehicle sales due to lack of production.

I think the 44% applies to cars only which means a savings of 2.6%; not great but something. A better way would be for people to cut down on miles and buy smaller more gas efficient cars, fat chance.

The more gas costs per gallon, the more that will happen.

A world of $10.00/gallon gas would be a world of smaller more gas efficient cars and less driving of them.

Many people in poorer and more rural areas like myself have no choice but to commute twenty or more minutes to work or even to the nearest grocery store…and considering the snowfall that we get in the winter where I live, all-wheel drive is almost a must.

Now, it is imperative to come up with a carbon-neutral liquid fuel and the infrastructure to produce and dispense it. I nominate dimethyl ether produced from water hydrolysis and atmospheric carbon dioxide using the “waste” heat provided by nuclear energy plants during routine operation.

How could an industry-shattering bill such as one that would introduce new, more efficient forms of energy into the economy pass through congress before the question of how that infrastructure will actually be built is answered? Some of the largest companies in the world are these oil companies that, of course, have their hands deep into the pockets of the most influential voices and faces in Washington. I think that there is also an administrative, behind the scenes piece to these sky-high oil prices and rising inflation that is currently going on worldwide.

Seeing something like this actually come into fruition would be interesting, no doubt.

Why isn’t an increase in public transportation considered to lessen the use of fossil fuels. The US used to have trolley systems in cities and surrounding areas but they were dismantled by auto and tire manufacturers. This alternative attracts little attention and would be opposed by large sectors of industry.

When you can’t spend on services, you spend on goods. When you spend more time at home, you spend more on your home. When inflationary expectations rise you bring purchases forward rather than put them off. When you expect shortages, you stock up. When you think the world is going to shite, you start to wonder if those preppers are maybe onto something. A lot of demand for goods is being brought forward and that may leave a big hole on the other side, so look out below.

Excessive climate alarmism created enormous fragility in the global fossil fuel markets, which as night follows day gave Putin the green light to make his move on The Ukraine.

What the heck is “excessive climate alarmism”? Probably what I see as a necessarily concern to move away from fossil fuels as it’s not sustainable. But I’m not sure how much “alarmism” has impacted policies or markets for fossil fuels.

Look around. Climate change is now a crowd event and crowd events never end well because crowds are manic.

Fossil fuels are not sustainable, but what matters is how we manage the transition to renewables. Trying to do it faster than resources and technology allow could make the cure worse than the disease. “Excessive climate alarmism” has resulted in fossil fuel industries being subjected to increasing regulatory hurdles and uncertainty, projects have been cancelled and the cost of equity and debt has risen. Investment hurdles have increased accordingly, so investment has fallen. The system has become increasingly fragile and pricing power has been handed back to Russia and OPEC. Enter Putin.

Just today I read that Jamie Dimon from JP Morgan recently said “oil would hit $185 a barrel within five years, given the chronic underinvestment and demand that likely will soon top 100m barrels a day.”

“Could” being the key word. You’re premise is based on an argument of ignorance fallacy. Climate change hasnt terribly effected us yet, therefor we shouldnt be alarmed.

We should be alarmed, but we should also be measured. I say “could” because nothing is certain, but my view is that it will, by a large margin. Look around. I hope you realize that the opposing view, which I presume you support, is based on an equivalent ignorance fallacy that relies on fear! The difference is that you are part of the self-reinforcing crowd and I am not.

>I presume you support, is based on an equivalent ignorance fallacy that relies on fear!

Agreed.. at least partially., But my opinion is also based on the precautionary principle. The outcome if either of us are wrong are extremely asymmetric. One could feasibly result in the end of humanity entirely. (I’d also add that oil producers do a pretty good job of self-reinforcing and whipping up good segments of the population to come to their side as well, which I imagine is part of the reason you feel the way you do)

I subscribed to the precautionary principle on climate change perhaps 15 years ago, but have been pulling back from it ever since. The precautionary principle and the asymmetric payoffs is why hell is such an awful place; who in their right mind would take that sort of risk? I have no particular loyalty to or vested interest in any industry or lobby group, I just don’t want us to create a real disaster while trying to solve a perceived or at least exaggerated disaster. I’m not saying we shouldn’t act on climate change, I’m saying we should do it in a way that gives us at least a chance of succeeding without seriously damaging our civilization from the inside in the process. The task is now exceptionally difficult, in part because the green movement ruined the development of a robust nuclear industry, again largely by promulgating fear. Also because the resources needed to do it will take decades to develop, copper being one of the better examples. Technology also has a long way to go, particularly with batteries to get the efficiency up and the cost down. Demanding action in excess of available resources and technology will increase the cost exponentially. Another important aspect of the problem is that we seem to be incredibly dangerously poised on the cusp or at the early stages of Neil Howe’s “fourth turning” and we no longer have any resources or capacity left to squander.

Climate change is not a crowd event. Climate change is a terraphysical process. The crowd’s response to climate change could be called a crowd event.

How much climate change alarmism would be the right amount? Also, what would be the right amount of alarmism over ocean acidation from runaway carbon skyflooding?

Thanks for the pedantry.

How much alarmism is the whole point and using limited resources wastefully will limit our ability to deal with the problem.

What happens to sea water’s capacity to hold carbon dioxide as it warms?

It was U.S. attempts to stop NordStream II from being brought online by training and financing the Ukies to liquidate Donbass and Crimea that gave Putin the “green light” to invade “Ukraine.”

The U.S. ability to export “traded goods” long ago collapsed to only exporting civil and military aerospace. The 737-Max debacle and the success of Russian arms in Syria was killing those exports. The only “traded goods” left for the U.S. to export are oil and gas plus agricultural products.

U.S. blob appears to have decided that a contained conflict in “Ukraine” would stop the Post-Brexit European pivot to Russian gas, oil, and ag products before there was nothing left for America to trade.

you just described a third world extract economy. some of our largest exports are dirt and scraps.

its amazing how nafta billy clintons criminal policies have reduced a first world nation, into a third world nation.

the author touches on how free trade is unworkable.

surplus nations stay surplus on purpose, such as what shroeder did in germany in the 1990’s, its still in effect today.

you export you poverty, unemployment and deflation onto others. china is a master at that game.

anyone stupid and corrupt enough to sign a free trade agreement, finds their people have their wages deflated poverty, unemployment, under employment explodes, along with debt and higher prices.

the other game they play is that we are free trading for the poor. the huckster woodrew wilson was a master at that.

they are just working stiffs, leave them alone. not exactly, they are sweatshop, forced and slave labor that parasites profit off. and were far better off evolving under their old systems.

the free traders that i argue with claim any day now the system will be fixed. when the nafta democrats said they will fix taxes to stop the corporations rampant tax avoidance under free trade, the free trade dupes were giddy, i said fat chance.

the E.U. tried it, right away four countries balked, and nothing but dead silence out of the dupes.

today no one speaks of it.

their is a reason why the french could not get rid of macron, macron represents and is backed by a world wide oligarchy brought to us be nafta billy clintons free trade.

the 90% world wide are simply ignored.

the author touched on this when he said try crafting world wide rules, fat chance of that ever happening.

Yep, pretty naked.

I don’t see how McCoy sees the future clearly, but [IMO] has ended up somewhat off on Ukraine.

Still, the US kind of more crazily flaunts its presumptions.

Lots of big words in the article. Let’s see if I can rephrase so I can understand it better.

—

Goods prices are going up world-wide because of reduced supply and increased demand.

Service demand is going down – primarily COVID related? – so service jobs are being lost.

There is self-correction: as goods prices rise, producers increase production. This lowers prices, not just in-country, but internationally. New production jobs replace lost service jobs.

Allocating resources – more and better production facilities – and reallocating resources – job shifts – are easier with loose monetary policy. Traditionally this implies in-country inflation, but as more goods are produced prices of (tradable) goods eventually fall worldwide.

There is a “tragedy of the commons” effect. Any individual country will be worse off due to domestic inflation if it has loose monetary policy, so will tighten policy. If all countries tighten policy increasing production is harder, so goods prices will not fall, and jobs lost in services are not made up for by new jobs in production.

High prices in goods together with job loss is stagflation. This is bad. Central banks should coordinate and not tighten monetary policy too much.

—

Who wudda thunk?

Is this true? If loose policy results in building “better production facilities – and reallocating resources” that could easily offset any negative from inflation, no?

Yes, it is true, because the loose monetary policy approach has been over-egged for the last 60 odd years and its effectiveness is in terminal decline. Go to YouTube and listen to any interview of Lacy Hunt given over the last few months and listen to his comments on the Law of Diminishing Returns. There’s a good one given by Danielle diMartino Booth. Loose monetary policy now just increases asset prices and worsens class and generational inequality.

Central banks create more problems than they solve.

OK — but that doesnt change the question. Just because central banks use monetary policy irresponsibly doesn’t mean monetary policies couldnt be used in a responsible and constructive manner. You dont even need the central bank to be involved. The government can just print money to do it. For example: https://www.vox.com/recode/23048906/chip-shortage-manufacturing-america-biden

The problem with central banks is that they try to reduce economic volatility. That sounds like a good plan, but reducing volatility actually creates fragility, which eventually leads to massive volatility when it finally breaks down: the so called “Minsky Moment” named after Hyman Minsky, which I believe we are now approaching. In addition to Neil Howe’s “The Fourth Turning”, which I mentioned in an early reply to you, I really recommend Nassim Taleb’s “Antifragile” (which I am reading now). The latter also gives perspective on things like floods and bushfires. We go out of our way to control rivers and put out small fires (ie reduce volatility), but in so doing we set ourselves up for the disastrous big ones, which are then of course blamed on climate change.

Printing money will have to wait for another day, but I’m not a fan. I’ll just say it only works effectively at a very limited part of the economic cycle ie at the end to alleviate a major deflationary bust. In addition to the Lacy Hunt videos I mentioned in an earlier reply, I recommend the Ray Dalio video on YouTube called “How the Economic Machine Works”, which is really good and covers this point towards the end.

“The problem with central banks is” the ideology that the administration is beholden too and not some wobbly notion about volatility in a NAIRU or 2% targeted inflation mindset.

For clarity: the parts of my comment between — — are my concise and hopefully clear paraphrase of the original article.

It investigates differential price changes in goods and services in an international trading environment, concludes that models dealing with such changes more locally – within a country – provide incomplete understanding of what is happening in the world today, and that, unless what’s happening is understood more correctly and completely, actions – particularly central bank actions – are more likely to make problems worse than better.

I more or less agree with the argument. The “wudda thunk” link covers my thoughts expressed on another occasion.

But Objective Ace and Bellatrix deserve more.

—

“Any individual country will be worse off due to domestic inflation if it has loose monetary policy” is a statement that is absolute dogma to some, more-or-less-true to others, and more-or-less-true-in-some-cases to people like me.

Let’s take the example of a chip factory, a fab. It takes four or five years to build. In loose policy times it is more likely that the money to build it can be raised; lower interest costs make it easier to see profit in the investment. In the end chip supply will increase and chip prices will fall, as Objective Ace expects. But there is a lag.

During construction money flows to people and businesses doing the construction. They are able to buy – or save – more. Buying more is the definition of increased demand. With increased demand comes inflation – unless an increased supply of those items meets the increased demand, but again, there is always likely to be some lag.

The general belief is that when monetary policy is loose inflation rises. I look at this through the eyes of experience. I lived through the inflation of the seventies. My family lived through inflation in the twenties. When, in a period of rising prices, the expectation of ever rising prices takes hold, that is what I see as inflation. That is not yet what I see today for goods and services.

—

Note, however, the “or save” above. Saving eventually means more than growing cash in the bank. For many it has been using the cash as down payment for a house, saving with investment certificates, mutual funds, stocks, bonds, land, rental properties, and so on. I agree with Bellatrix that “Loose monetary policy now just increases asset prices.” I believe that asset price inflation is a thing and has been problematic for quite a long time.

For 60 years, well, no, in my opinion not quite so long; and I also don’t think that asset price inflation only “worsens class and generational inequality.” The counterexample is that for many years home ownership – in a world of asset price inflation – has created class and generational wealth.

There are other more foundational factors worsening class and generational inequality. I’ll probably write about them some other time.

—

Actually, central banks solve many problems very successfully. It’s just that people expect them to also solve problems that they don’t have the direct tools to deal with, but doing nothing is politically not really an option. They are then forced to act. From the link, an example:

While this is very helpful, I have to strongly disagree with your premise, “More demand produces more inflation.” Whether it does or doesn’t depends on how much slack there is in the economy, which is a function of productive capacity. In WWII, the economy ran at over potential, at wartime production levels, yet did not generate inflation. That was achieved by increasing productive capacity by bringing women en masse into the work force and running extra shifts at factories.

Reading “More demand produces more inflation” as my premise means that I must have been unclear somewhere. I am much more in your camp; this statement is certainly too simplistic.

Is it that we define or interpret “demand’ differently?

In any case my comment of May 16 gives my complete definition:

Unfortunately, this is a quantitative definition, not a qualitative one. You can have generally rising (or falling) prices for supply/demand reasons without inflation (or deflation).

Yeah, sure, if you have inflation, then the price of a basket of goods increases. And sure, I know that people say, “you can’t tell if you’re doing better or worse unless you can measure it.” Defining inflation as the increase in a basket of goods seems like the right thing to do.

On the other hand, it’s been my painful experience that just because measurements can be made, they don’t necessarily measure what they are expected to measure. Failure mechanisms include having measures

Defining inflation as the increase in price of a basket of goods fails the second way. This is understood better when you look at the difficulties that the Fed, and economists in general, have in defining the basket of goods to use. They take things out and put replacements in as technology changes; they take out things like energy and rents as being too volatile and not reflecting the core rate of inflation.

This just demonstrates the measurement is flawed. I would say that if inflation is in place, measuring the rise in price indicates how bad it is, no more than that. When prices are rising, you have to look at other things to decide whether it is inflation.

—

Your comment on inflation during WWII is worth looking at more deeply. The following extract from the US Inflation Calculator shows the “inflation” for 1941 to 1949 in December of the year and the annual average.

In 1941 “inflation” was high, with December higher than the average for the year. I interpret this as price rises in the face of restricted international supply.

In 1942 prices rose even more quickly, but the December number was a bit lower – perhaps reflecting the start of war psychology?

From 1943 to 1945 “inflation” was low. This the period you reference. As you say quite correctly, the potential increase in price of military equipment and of running a war economy was made up for by the increase in production as the economy ran at over potential by bringing women into the work force and running extra shifts at factories.

The numbers reflect consumer prices, though, and there is a strong psychological component. Sure, there was rationing and price control, but but people in general bought into the notion of the war, they were willing to make sacrifices, and consumer demand fell as “everyone did their part.” This is the important psychological aspect of price changes.

Germany, on the other hand, used resources extracted from the countries it took over, and on the order of 12 million forced and slave laborers. This helped allow for increased production without uncontrolled inflation. Of course, motivated American workers were more productive and produced goods of higher quality.

With the end of the war “inflation” spiked in 1946. Self-imposed demand restriction were thrown out the window, retooling from a war to a peacetime economy was not complete, so a corresponding increase in supply could not yet meet demand. This is the period where “More demand produces more inflation” was closest to being true.

From 1947 to 1948 “inflation” fell, with December numbers lower than annual averages indicating a continuing fall with negative numbers by 1949

I actually see something like this as reasonably possible….

We had what was massively depicted as “money printing” after the crisis even though it was not money printing, as in QE. We did have lax monetary policy due to real interest rates being negative. The EU had explicit negative interest rates. Japan had extremely loose monetary policy for over two decades. Yet the US and EU did not get inflation in the years after the crisis and Japan was in borderline deflation.

What created this inflation was:

1. Supply chain breakage due to Covid and actual shortages (chips, lumber, consumer durables, meat at point)

2. Covid induced fiscal spending

Even 1 + 2 produced only acute inflation in certain sectors, notably cars and used cars, and not much in others.

Then we had

3. More fiscal spending

4. Russia commodities shock, particularly in energy, which over time propagates through everything.

Please tell me where money supply appears in this story.

I basically agree with all your points here.

The only place that money supply appears is that the fed balance sheet held proportionally more treasuries to balance the fiscal spending. Commercial banks did not increase their deposits, so there was little overall increase in money supply.

Overall prices increased exactly for the reasons you state – supply restrictions.

Since we don’t see people expecting ever increasing prices, but being hurt by existing increases, I don’t see ongoing inflation by my definition. There is clearly “inflation” by the usual definition, but we agree that this is caused more by supply problems than anything else.

I’m not so sanguine about increases in money supply, particularly because of the impact on asset prices. M2 is up over 40% since the beginning of 2020 (and its components were changed in May 2020, so the real change may be more, although I’m not sure about that). It shows up everywhere in asset prices and has increased inequality enormously, particularly because of rising property prices, where the wealth effect benefits the few at the cost of the many.

You can’t just print money to fund fiscal spending on this scale and not increase money supply. As noted above, M2 is up over 40%. Reverse repos are a direct measure of the flood of surplus funds into the banking system. There is more money sloshing around than the banks can use, so the Fed now takes it and pays the banks a few points for it. If they didn’t, the banks would probably stop taking deposits or impose negative deposit rates, which can’t be allowed to happen. Reverse repos now total over 2.25 TRILLION, which is an increase of over 2 TRILLION since the beginning of 2020. This is unprecedented and what it means and what its consequences will be is anyone’s guess, but I can’t see any good coming from it.

The issue with goods and services inflation is that although it may start because of supply disruptions, in a complex economy there are then second, third, fourth etc. order adjustments, particularly with wages, so it takes an extended period well beyond the initial cause for prices and wages to adjust. So it’s not going away any time soon, unless the Fed crushes the economy, which I don’t think it’s prepared to do. I think it will raise rates and engage in QT until it causes a major market correction and it will then go back to its old ways. I’m even less sanguine about what happens after that.

Your points are good, but consider the following:

Money is the medium of exchange. It’s also a store of value. If it’s being used to store value (“There is more money sloshing around than the banks can use”) then it’s not being used as a medium of exchange.

Or to put it another way, it seems to me that the velocity of money is lower for the time being. Monetary momentum, the amount of money times its velocity is the true measure of monetary effect and is by itself not high enough to itself push prices higher.

—

That said, the massive overhang is worrying because, in theory, it could start to be used for exchange at any time. To slightly misquote but also to agree with you, after this adjustment “there are then second, third, fourth etc. order adjustments” which make the future uncertain.

Your last paragraph is the key to the situation. You are right that money is both a medium of exchange and a store of value, but when the quantity of money keeps increasing faster than the supply of real assets, it’s value relative to real assets declines accordingly. Wiser souls then start to reduce their cash holdings and increase their holdings in real assets, which pushes up prices of real assets. We have seen this happening. These things happen slowly then quickly and the ultimate danger is that there is a general rush to get out of cash and into real assets and even general goods. That literally creates shortages and is the stuff of hyperinflations. As you say, the velocity of money does not yet show there is an immediate problem, but it is an important indicator to watch and you should keep in mind that it is only published several months after the fact.

Peak free enterprise? “This (complexity) makes designing a system to regulate international trade imbalances a daunting task.” But, since these imbalances have a tendency to counter-balance each other over time, why are we so fixated on securing payment settlements as soon as possible? To globalize trade in manufactured goods smoothly and mitigate the imbalances, which cause inflation problems, they really need to create a global revolving credit account with a grace period factored in – another big escrow in the cloud – to provide payment -settlements in a timely manner without causing price inflation. A revolving account based on the statistics of trade eventually balancing itself out, No? The first paragraphs almost say this when they talk about trade in services swinging up to match trade in goods – when one goes up the other follows, but just not fast enough. Are we really so dumb that we can’t plan for something like this? And to that end, energy-petroleum will be necessary long after electric cars have dented their profits because we need high energy petroleum for much of our industrial manufacturing (for said trade goods). So when it becomes impossible for energy producers, drillers, to make their necessary revenue and profit – “naturally” prices inflate by some invisible hand – it would be better just to nationalize oil and absorb the price fluctuations without distorting the economy. Nationalize oil and gas. And stop obsessing over settlements. Or did I miss the point entirely?

Looks like the evil Putin and his evil minions might have figured this out, while we try to eat “freedom.”

I have to wonder what part of inflation in the cost of so many things, goods AND services, is just due to good old price gouging and good old greed? The “price” of a lot of things bears only a tenuous relationship to “cost” to the seller. Like this: https://www.dailymail.co.uk/health/article-3460321/How-Big-Pharma-greed-killing-tens-thousands-world-Patients-medicated-given-profitable-drugs-little-proven-benefits-leading-doctors-warn.html

But no, it seems most of us don’t ask such questions.

Yeah, I sat through two presentations this week on the macro economy, with no mention of corporate profits. An article today on the latest data (“down 3 percent!”) had lots of handwringing about the implications for investment. LOL.

Oil and Gas corporates have been engaging in blatant profiteering since Russia attacked Ukraine, the profits are obscene. Even the conservative UK government has found they can’t ignore them. But otherwise governments are simply letting oil and gas companies get away with this, and then of course they will seek to invest all that cash in extracting more oil and gas. They don’t know any other way than to accumulate in their death cult.

And there it is, the now standard erasure/transferral of agency. How much has the invasion caused inflation in comparison to the economic sanctions chosen as a response. They were in no way inevitable or required, they were a carefully considered strategy.