This is Naked Capitalism fundraising week. 1051 donors have already invested in our efforts to combat corruption and predatory conduct, particularly in the financial realm. Please join us and participate via our donation page, which shows how to give via check, credit card, debit card, or PayPal. Read about why we’re doing this fundraiser, what we’ve accomplished in the last year, and our current goal, expanding our reach.

John here. This post assesses the IRA as both an inflation reduction tool and as a response to climate change. Unsurprisingly, the IRA does almost nothing to address inflation. Storm’s assessment that the climate response elements of the IRA are doomed to fail in achieving an energy transition because of their reliance on positive price incentives and minor fiscal stimulus shows the IRA has little to offer. A minor step in support of renewable energy isn’t much of a result for Biden’s flagship economic package.

By Servaas Storm, a Dutch economist, author, and Senior Lecturer at Delft University of Technology. Originally published at the Institute for New Economic Thinking.

Servaas Storm’s Commentary for an Inet Symposium on the Inflation Reduction Act

The IRA has received mixed reviews, which is not surprising given the current polarised political, social, and economic conditions existing in the US. However, what strikes even more is that reactions by economic pundits, both from the center-left and the center-right, have been inflated, often relying on dramatic hyperbole and invoking sweeping vistas of (climate) disaster averted and ‘civilization saved’. The (sad) truth is that ‘serious’ establishment macroeconomists are once again having a breathless debate over very little. Let me quickly run through the debate.

Observers on the ‘liberal’ center-left, including Paul Krugman, Joseph Stiglitz, and the AFL-CIO, have hailed IRA as a ‘very big deal,’ ‘historic,’ and a ‘victory for working people’, because the Act will reduce CO2 emissions (supposedly by 40% in 2030, compared to emissions in 2005), likely create more than 1 million green and relatively well-paying jobs per year over the next decade (according to the BlueGreen Alliance), and catalyse domestic production of batteries, electric vehicles (EVs), solar panels, and wind turbines, (finally) setting the US up to compete in the global renewable energy market. Using tax credits and direct consumer rebates for solar panels, EVs and heat pumps to speed up the clean-energy transition, IRA will lower energy costs for many US households by hundreds of dollars per year. IRA also offers an important ‘side helping’ of health-care reform which will benefit American working- and middle-class households by cutting the costs of prescription drugs and lowering health insurance premiums, while expanding health insurance coverage (White House 2022).

All this is done in a fiscally conservative way which should please all deficit hawks and balanced-budget fetishists—in fact, according to estimates by the Penn Wharton Budget Model (PWBM) and the Congressional Budget Office (CBO), IRA will lower accumulated fiscal deficits of the US government over the next 10 years by $248 billion and $305 billion, respectively. The lower deficit is also supposed to contribute to lower inflation: “126 leading economists—including 7 Nobel Laureates, 2 former Treasury Secretaries, 2 former Fed Vice Chairs and 2 former CEA Chairs—have said reducing the deficit will help fight inflation and support strong, stable economic growth” (White House 2022).

On the other side, observers on the centre-right are pointing out that IRA, despite its name, doesn’t do anything to reduce US inflation. This is confirmed by analysts using the Penn Wharton Budget Model, who conclude that the impact of IRA on inflation is statistically indistinguishable from zero, as well as by CBO Director Philip L. Swagel, who concludes that the bill will have a negligible impact on inflation in 2022 and 2023. This is not surprising. Any impact on US inflation of the average annual reduction in the fiscal deficit caused by IRA (which amounts to around 0.1 percentage point of US GDP) is simply too small to be detectable in the inflation estimates of the Bureau of Economic Analysis. In other words, the mentioned 126 leading economists—including 7 Nobel Laureates, 2 former Treasury Secretaries, 2 former Fed Vice Chairs and 2 former CEA Chairs—are wrong in believing that reducing the deficit does help fight inflation. (It is true, clearly, that some of the IRA measures will lower energy bills and healthcare costs for US households. But not aggregate inflation.)

Centre-right observers further worry that IRA will lead to an increase in tax rates for the US middle class, contrary to President Biden’s pledge to not raise taxes on households making $400,000 or less annually. Estimates by the Tax Policy Center (2022) show that this worry is evidently wrong: average taxes of middle-income households remain unaffected by IRA, while the after-tax incomes of low-income households may go up a bit and the average after-tax incomes of high-income people would decline somewhat. The point is, of course, that IRA is funded by highly targeted tax increases on highly profitable corporations: a minimum tax on the financial statement income of a few very large companies which currently pay little or no corporate income tax, and a tax on companies that buy back stock from their shareholders. Some centre-right and corporate observers (including the Business Roundtable) strongly oppose IRA, claiming that these extra corporate taxes will ultimately be paid by workers (whose wages will arguably rise less) and shareholders (robbed of the precious gains provided by their stock buybacks), also because they (mistakenly) argue that higher corporate taxes must hurt US economic growth. These pontifications about the impacts on growth of the proposed corporate tax increases make little empirical sense, however.

Estimates by the PWBM and CBO indicate that IRA will increase corporate taxes by around $30 billion per year in the next decade, or by just around 1% of corporate profits (in 2021); it must be further noted that corporate profits rose by around $120 billion on average per year during 2017-2021, and that there is ample evidence of corporate profiteering during 2021-22 (Storm 2022). Given the macroeconomically small hike in corporate taxation, it is unrealistic to expect any detectable effects on workers’ wages, business investment and growth. As Lance Taylor was wont to point out, policy changes involving billions of US dollars may look large from the point of view of an individual household or firm, but represent inconsequential droplets (‘peanuts’) at the macro level where variables are measured in trillions of dollars.

Cutting out the hyperbole and eschatological drama, both on the left and the right, what is the real significance of the IRA, if any? Clearly, IRA does nothing to bring down inflation (in the foreseeable future), but it does help lower-income US households to better manage price increases, especially as far as healthcare, medicines and energy are concerned. This is certainly important. However, IRA is best considered as a climate bill, meant to lower US CO2 emissions, promote clean energy, and improve resilience to global warming and reduce the risk of ‘fossilflation’ (Storm 2022).

As such, IRA constitutes an important—albeit limited—step in the right direction. Using ‘pecuniary rewards’ (such as tax credits and rebates on renewable energy), funded by additional taxation of socially unproductive monopoly profits of corporations, IRA aims to provide a boost to the renewable energy transition—and thus help to cut US carbon emissions over time. Within the polarised stalemate of US (climate and energy) politics, IRA definitely constitutes a major break with the past—but, alas, one which falls rather short of ‘saving civilisation’, as Krugman is suggesting.

IRA falls short of what is needed because of two reasons: the fiscal stimulus to the renewable energy transition is far too small compared to what is needed in view of the steadily building climate crisis; and the positive price incentives, loved by establishment economists, will not work, failing to bring about the required structural transformation of the US economy, addicted to fossil fuels, to a net-zero-carbon system. Let me consider these two points in somewhat greater detail.

First, most climate macro-economists agree that a strategy to reduce carbon emissions so as to keep global warming below 1.5°C degrees (with a reasonable degree of probability) would require an annual increase (or reallocation) of investment by around 2 to 2.5% of GDP (for instance, see Taylor, Semieniuk, Foley and Rezai 2021). For the US, this would mean an increase in investment in renewable energy generation and infrastructure of around $500 billion per year. IRA is budgeting an annual increase in such investment of $37 billion, which is less than one-tenth of what is needed. It is difficult to see how the limited stimulus provided by IRA is going to lower US emissions by (the expected) forty per cent compared to levels in 2005.

I must add here, on this point, that per capita greenhouse gas emissions are much higher in the US than in the European Union (EU) or the United Kingdom (UK). In fact, in 2019, consumption-based CO2 emissions are 17.1 tonnes per person in the US compared to 7.74 tonnes per capita in the EU-27 and 7.71 tonnes per person in the UK. This implies that even if IRA manages to lower per capita carbon emissions in the US by 40% over the next 10 years, CO2 emissions by the average American continue to remain much higher than average per capita emissions in Western Europe. In other words, US climate action remains relatively unambitious. As Lance Taylor (2021) pointed out a year ago, “the USA is far behind the rest of the world in attacking global warming. A gallon of gasoline costs around $2.50 here vs. at least $7.00 in Western Europe.” It is important to keep sight of the relatively limited ambition level of US climate policy—especially in view of the political hyperbole and climate eschatology characterising US macroeconomic discussions on IRA.

Second, IRA wants to have the cake and eat it. It wants to promote clean energy using positive price incentives, but at the same time is protecting the vested interests of fossil fuel capital, allowing it to continue its stranglehold on the US political system. Gone are earlier ideas of taxing carbon or pricing carbon by setting up a CO2 trading regime. Instead, IRA provides mainly positive pecuniary inducements, which (paraphrasing Martin Weitzman 2007) are meant to unleash the decentralised power of capitalist inventive genius on the problem of researching, developing, and finally investing in economically efficient carbon-avoiding alternative technologies. More specifically, as is lucidly explained by Jeff Goodell (2022), “In theory, it works like this: subsidies and rebates will give home heat pumps the little push they need to replace gas furnaces, which in turn will reduce demand for natural gas, which will close down the fracking operations that leak methane into the atmosphere. Subsidies and rebates will also give electric vehicles the extra shove they need to replace internal combustion engines, which will cut the demand for oil and that will in turn push companies like ExxonMobil and Shell and BP to accelerate their investments in clean energy. The faster this happens, the bigger it snowballs, and the faster the world is transformed.” I have put ‘in theory’ in italics because this is the crux: it won’t happen like this is reality. Sorry.

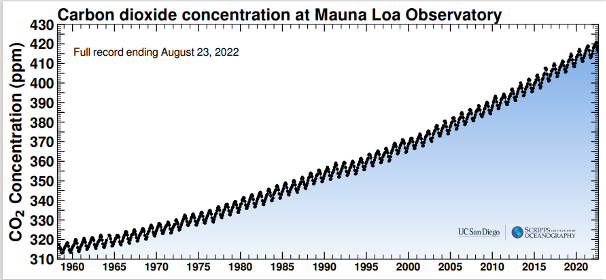

According to many energy modelers, the potential for CO2 reductions from the IRA rebates and tax credits may be around 40% by 2030 (compared to 2005). But the assumptions concerning price-induced technological progress in energy and carbon efficiency on which most climate-economy models are built, are merely educated ‘guesses’—after all, data on past performance do not provide any guidance for the structural economic transformation and the required degree of decoupling of economic growth and CO2 emissions that lies ahead (Storm 2009; Schröder and Storm 2020). Many modelers are techno-optimists, downplaying the stylized fact that labor and energy productivity levels have increased at close to equal rates for centuries (Semieniuk et. al., 2021). Rebates, subsidies, and tax credits falling within a politically acceptable range may be capable of inducing macroeconomically small changes in the structure of the economy and level of emissions. But given technical and structural constraints, the proposed incentives will not be effective, as Lance Taylor (2021) showed, in bringing about the structural change necessary to stabilize warming below 1.5°C. To argue otherwise is a conscious act of self-deception in the spirit of Wilkins Micawber’s stubborn and unfounded optimism that, in the face of adversity, “something will turn up.” Meanwhile, the Keeling Curve (Figure 1), the chart of CO2 concentration in the atmosphere (measured at Mauna Loa Observatory), continues to rise steadily and relentlessly.

Figure 1: The Keeling Curve

A final reason why IRA will not achieve its ‘expected’ CO2 reduction in the future is that it does almost nothing to reign in the fossil fuel industry. Could this be related to massive campaign contributions that the oil and gas industry routinely makes in elections? As argued by Aaron Regunberg (2022), by reframing the political discourse on climate around the additive potential of a green industrial policy and, at the same time, deprioritizing efforts to radically decarbonize the economy, the Biden administration succeeded in building a coalition (including senators Manchin and Sinema) in support of IRA. But IRA could turn into a Pyrrhic victory, coming at great costs, because, built into IRA, is a failure to do anything to directly and quickly scale back fossil fuels.

Even worse, in return for Manchin’s support, IRA comes with a side agreement, permitting changes that will help fast-track fossil fuel infrastructure—including a long-delayed pipeline in Manchin’s home state of West Virginia. Concerned environmentalists warn that the bill contains two ‘poison pills’—in sections 50264 and 50265—which mandate oil and gas leasing in the Gulf of Mexico and Alaska and bar the federal government from authorizing new wind or solar energy development “unless an onshore [oil and gas] lease sale has been held during the 120-day period ending on the date of the issuance of the right-of-way for wind or solar” (Jake Johnson 2022). Tying renewable energy development in the US to massive new oil and gas extraction guarantees that IRA will not achieve its ‘expected’ CO2 reduction in the future. Climate researchers rightly call it a climate suicide pact.

So, what is my bottom line? IRA is a first historic, but nevertheless modest step in the right direction of building a zero-carbon renewable energy US economy. Its impact in terms of reductions in CO2 emissions will be considerably smaller than ‘predicted’, and its transformative power will be limited. Much more will be needed—both in terms of public investment in clean energy and sustainable technology and in terms of direct interventions to scale back fossil fuels. There is no getting around it: direct measures including phasing out coal (power plants), taking climate liability litigation seriously, public investment in renewable energy generation and RD&D, and banning drilling, fracking, and (oil and gas) pipeline provisions, will be needed.

A coworker in the gas/ oil transport industry found a cheap house, where GE Imaging (Kraütkramer) and wind-turbine service industry has work. Any number of NOAA, National Weather Service & OUR type all began moving up there, decades ago. In the Poconos, ice storms & hurricanes replaced blizzards & NY “skiing” tourists/ anglers. We knew, when Katrina took out Shell’s TLPs that the fracking pyramid made NO sense and likely set off run-away AGW within our remaining years (and that this would simply be ignored, as NYC switched scores-of-thousands of ancient fuel oil boilers to gas). Now, that we’ve actually exceeded Exxon’s best 1982 guess as to atmospheric carbon, folks neglect this still? I’d chosen, Zion Grove, as unfrackable; anthracite mines all closed & SCARY armed locals, to fend off city folks fleeing the megalopolis. 22 deer in the yard, beryllium flavored fish, Hometown Amish Farm Market & best smoked pork in the USA. But, yeah… We’re all VERY BUSY, buying totally unnecessary fracked methane/ ethane lines; so, I’d head up there pretty SOON?

An excellent synopsis of the bill with two minor comments and one major one.

First, although the author tries to be objective by “Cutting out the hyperbole and eschatological drama” he still occasionally succumbs linguistically: “deficit hawks and balanced-budget fetishists”; “shareholders robbed of the precious gains”; “These pontifications about the impacts on growth”; “ample evidence of corporate profiteering during 2021-22”. Did rural homeowners who sold for top dollar “Profiteer”? But in his defense, he does much better than most writers on the subject.

Second, environmentally advanced Canada looks like the US. The article says: “per capita greenhouse gas emissions are much higher in the US than in the European Union (EU) or the United Kingdom (UK). In fact, in 2019, consumption-based CO2 emissions are 17.1 tonnes per person in the US compared to 7.74 tonnes per capita in the EU-27 and 7.71 tonnes per person in the UK.” Canadian numbers are at: https://www150.statcan.gc.ca/n1/daily-quotidien/211213/dq211213c-eng.htm. Not an exact comparison because these are household numbers but they give an EU comparison.

Third, world CO2 will keep going up at about the present rate regardless of what the US does. Google “World and US CO2 emissions” and you get: “The U.S. Energy Information Administration estimates that in 2019, the United States emitted 5,130 million metric tons of energy-related carbon dioxide, while the global emissions of energy-related carbon dioxide totaled 33,621.5 million metric tons.” If the US cuts emissions in half it will delay the inevitable by 3-4 years because of Third World growth.

A passenger on the Titanic who grabs a bucket and begins to bail water may feel better because he is “Doing something”, but the ship will still sink. So getting a seat in a lifeboat may be a better investment than using a bucket, a morally unpalatable truth but a truth nevertheless.

because we live in a globalised economy… one country starting to bail actually incentivizes others. the less fossil fuel infrastructure there is the less money is made in oil. since the us is both a customer and producer. and while we are inevitably fucked, there is a big difference in HOW fucked that depends on reducing emissions as fast as possible. We have choices between extinction, 90% of ppl dying, total civ collapse, and merely a couple billion dead. That’s a lot of lives riding on even small bucket solutions, though we obvoiusly need large ones like revolution since capitalism is incapable of solving the problems it causes.

Or because it’s just monopolistic bullshit to begin with.

This IRA act will neither control/reduce inflation nor have any effect on AGW. It’s another giveaway to fossil fuel companies and the elite who’ll take the tax credits for purchase of EV’s. It well past the time to triple or quadruple taxes on transportation fuels and earmark the revenues for building mass transportation system with a rebate to poorer people so they can afford to get to work in the interim. The crooked politicians we have are in the pocket of the fossil fuel companies, especially the giant oil companies which need to broken into a number of small corps.

Didn’t Biden pledge nothing will really change?

Great synopsis and I largely agree. However, to defend the tying of fossil fuel investment with green energy, we should learn from the EU situation that investment in both will need to continue. Industry will need NatGas for decades to come, and WV has lots of chemical industry needing NatGas.