By Peter Claeys, Visiting Professor at the Department of Economics of the College of Europe, and the Universiteit Gent, Béatrice Dumont, Professor of economics at Sorbonne University Paris and Director of the Department of Economics at the College of Europe, Martin Larch, Head of Secretariat at European Fiscal Board, and Wouter van der Wielen, Economist at European Investment Bank. Originally published at VoxEU.

Major economic downturns have left important scars in the path of economic expansion, despite forceful and regular attempts to support aggregate demand. This column summarises discussions at a recent workshop on scarring effects and strategies to avert or minimise them. Fiscal policy can play an important role in limiting hysteresis – a term coined in the 1980s – particularly by promoting government and private investment. However, the political economy of fiscal policymaking typically trades off long-term benefits for short-term gains.

The Global Crisis rekindled a discussion that has absorbed macroeconomists and policymakers for decades. In the aftermath of major economic downturns, economic activity does not return to its pre-crisis trend. In other words, major downturns leave ‘scars’ – a catchy expression for negative supply-side effects. Blanchard et al. (2015), Ball (2014), Martin et al. (2015) and Cerra et al. (2021) are particularly prominent examples of recent studies documenting the entrenched pattern. The foundations of their work were laid a long time ago, in the early 1980s, when Nelson and Plosser (1982) showed that cycles were not taking place around stable but rather variable trends.

Apart from dealing with lasting effects on economic output, the most bothering part of scarring is the (un)effectiveness of economic policies. Scarring effects seem to materialise even in the face of forceful reactions both on the monetary and the fiscal side. Things may not be so clear in the wake of smaller cyclical swings when policymakers may not always agree about the opportunity to lean against the wind. When large shocks hit, however, there is usually a sufficient sense of urgency in the political system of any democratic country to design, deliberate, and dispense important fiscal support packages. And still, scarring effects persist, and the one-million-dollar question is why.

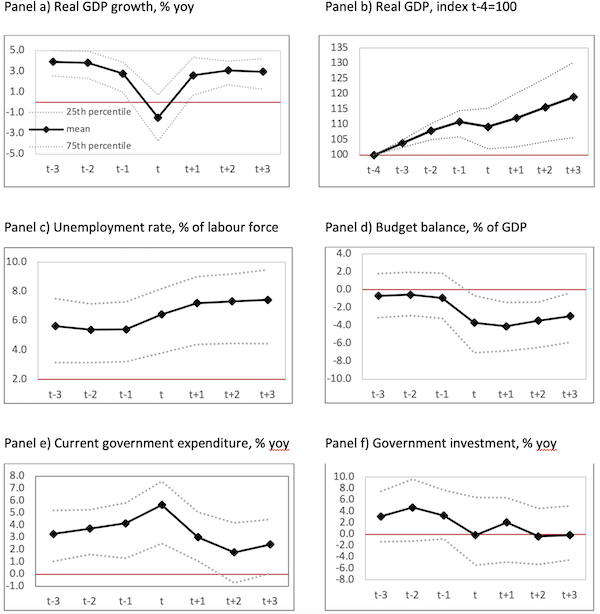

While there may be several forces at play, one seemed to be of particular importance and was at the centre of a workshop held at the College of Europe in Bruges on 23-24 November 2022, namely, investment, and public investment in particular.[1] The idea for the workshop was born after three of the four authors of this column took a closer look at the role of fiscal policy after major economic downturns in 20+ OECD countries since the 1970s (Larch et al. 2022). Our empirical analysis provided clear evidence that although fiscal policy can mitigate scarring effects, policymakers did not give enough attention to government investment; they favoured fiscal support with short-lived effects on output (see Figure 1). Over time, the sequence of forceful fiscal responses with short-lived output effects followed by scarring effects gave rise to sustainability issues.

Figure 1 Stylised facts of major economic downturns in 26 OCED countries, including 14 EU Member States, 1970–2020

Note: Behaviour of real GDP and fiscal variables in the three years before and after major economic downturns.

Source: Larch et al. (2022)

Scarring Effects Are Pervasive and Sizeable, Especially After Major Economic Downturns

Quantifying the scarring effects of major economic downturns is not a straightforward exercise, as there is no observable counterfactual. On top of our work (Larch et al. 2022), which broadly followed the approach by Blanchard et al. (2015), the workshop at the College of Europe featured a second paper assessing the importance and size of scarring effects. Applying a novel method focusing on the distribution of growth rates before, during and after recessions, Drehmann et al. (2022) convincingly corroborated the fact that severe contractions led to highly persistent negative growth effects. Smaller contractions did not have such an impact. Of particular note, Drehmann et al. (2022) did not find support for positive hysteresis, i.e. strong expansions do not seem to cause persistent above-trend growth.

The pervasiveness of scarring effects would and should attract limited attention if the effects were small in size, but the opposite was true. In line with the broader literature in the field, the evidence presented at the workshop showed that the lasting shortfall of economic activity and/or growth after major downturns could be surprisingly big. In the OECD sample we used, the average annual scarring effect three to seven years after a major economic downturn amounted to 1 ½ – 2% of the pre-recession trend. Using a very similar sample, Drehmann et al. (2022) found that for the 20% most severe contractions, the drop in GDP is, on average, 4.25% in ten years.

On top of confirming the empirical importance of scarring after major economic downturns, the workshop also offered insights into the specific mechanisms that generate lasting effects on economic activity or growth. Two invited keynote speakers – Andrea Roventini of Scuola Superiore Sant’Anna in Pisa and Valerie Cerra, Assistant Director at the IMF – offered important insights. Focusing on state-of-the-art general equilibrium models, Andrea Roventini showcased a series of channels that can generate prolonged recessions by connecting growth and business cycle theory as in Dosi et al. (2010), Dosi et al. (2017) and Dosi et al. (2018). These models couple endogenous growth (driven by innovation) with aggregate demand (driven by consumption and investment) so policies that support investment can mitigate or even avert scarring effects.

Based on a comprehensive overview of the empirical literature on how economies and economic policies behave after recessions – a literature to which she has made important contributions –Valerie Cerra underscored the importance for policymakers to act quickly and aggressively in response to a recession, especially by addressing the supply-side damages that might otherwise ensue.

The Policy Response to Scarring

The scarring effects revealed by the empirical literature and confirmed by the papers presented at the workshop beg important questions for policymakers, most importantly: how can scarring effects be mitigated?

In the early days, the prevailing idea was that any fiscal expansion supporting aggregate demand would diminish or prevent scarring effects. However, the persistence of scarring in the face of major fiscal expansions cast serious doubts over this politically appealing notion. We found limited evidence that conventional fiscal demand stimuli centred on current expenditure mitigate scarring. While estimates of short-run fiscal multipliers were sizeable, especially in bad economic times, they tended to reverse fairly quickly and even became negative in the medium term. Hence, handing out income support through higher current spending or simply keeping previously adopted expenditure plans on track when the economy tanked did not help address structural or supply-side issues triggered by severe economic downturns. By contrast, we showed that government investment could mitigate scarring effects, but in the vast majority of cases, the focus of fiscal policymakers in the wake of major downturns remained on the short term, i.e. public investment programmes were not the typical response.

Tervala and Watson (2022) corroborated the importance of public investment by taking a very careful look at a specific and highly successful policy intervention. A local schooling investment program combined with a labour market intervention in Australia between 2009-12 was found to produce very high multipliers weighing against any potentially lasting effects the fallout of the Great Crisis had on GDP in different parts of the country. In the context of European regions, Brasili et al. (2022) found that local public investment correlated positively with private investment, in particular in economic downturns. This highlighted the role of local public investment in stimulating private investment and, in turn, economic activity more generally. According to Brasili et al. (2022), the investment with the highest return was to be found in education and training, R&D, but also infrastructure.

In his opening speech, Maarten Verwey, Director-General of Economic and Financial Affairs at the European Commission, stressed how the European policy response to the Covid-19 pandemic marked a significant change compared to previous crises by banking on the potential benefits of government investment and structural reforms. In post-WWII history, the Recovery and Resilience Facility was indeed a rare and commendable example of a major policy initiative taken in the wake of a major downturn that aimed to strengthen medium and long-term growth prospects rather than producing a sugar rush of aggregate demand.

The credibility of the policy framework may also play a role in addressing supply-side effects. In particular, if fiscal rules become more credible, this might produce a wave of optimism that supports increases in aggregate demand, including investment. A paper by Betti et al. (2022) showed that periods of hysteresis could be dodged by the adoption of fiscal rules that reinstate the sustainability of public debt.

In the Economic and Monetary Union, where monetary policy cannot always stabilise idiosyncratic shocks, fiscal risk sharing can mitigate the tendency for economic divergence by offsetting prolonged recessions at the regional level, as Hauptmeier et al. (2022) argue. Following a similar line of reasoning and the more general reasoning by Obstfeld (2016), Cimadomo et al. (2022) found that fiscal risk-sharing supported growth mostly over the longer term, in particular in poorer regions.

Conclusions

Long criticised as slow and ill-timed, the policy responses to the Global Crisis and the Covid-19 pandemic initiated a reassessment of fiscal policy as a stabilisation tool. At the same time, there is ample evidence that major economic downturns produce lasting effects on real GDP in spite of active fiscal policy intervention. As a result, quite a few advanced economies ended up accumulating high public debt without fostering long-term growth prospects.

The workshop held end November last year at the College of Europe in Bruges brought together experts and policymakers to take a fresh look at the lasting effects of major economic downturns and how to address them. The papers presented at the event clearly show that policy responses can mitigate scarring effects but need to be more targeted towards supply side channels. In particular, there was growing evidence that government investment can dampen or avert lasting output effects. In contrast, higher current expenditure – the favoured policy response in practice – would support demand in the short term while heightening sustainability issues in the long run.

In sum, fiscal policymakers face an essential trade-off between short-term stabilisation and long-term sustainability: favouring the former will exacerbate the latter, while focusing on sustainability through higher investment may cost popular support. The trade-off is fraught with political economy issues but can be overcome as evidenced by the EU’s Recovery and Resilience Facility.

Footnotes

[1] The workshop was jointly organised by the Economics Department of the College of Europe, the European Investment Bank and the Secretariat of the European Fiscal Board.

References available at the original.

‘Major economic downturns have left important scars in the path of economic expansion’

Yeah, about that. That is entirely misleading that if not an outright lie. There were no scars. What happened after 2008 is that the same people and the same factors that led to that crash were left in place and bailed out by their governments – as their own people were thrown under a bus or in the case of the US, were used to foam the runways with. The prisons weren’t filled with criminal CEOs. Laws enacted to “solve’ some of those problems were soon watered down until they were basically gone. Which means sooner or later we will have another 2008 crisis but squared. So this talk of “scars” is just a deliberate distraction.

Thank you, TRK, for that analysis. I’m glad I didn’t bother to read the whole article.

Yah Rev. I’m curious about the, “[f]ocusing on state-of-the-art general equilibrium models…” Do state-of-the-art general equilibrium models include debt and debt servicing? Isn’t the giant pile of debt and the rentiers a drain on investment and even aggregate demand? The researchers view growth driven by innovation as mitigating or avoiding scarring. How do you get widespread innovation when monopolies and oligopolies are widespread and typically function to suppress innovation? How do you get public investment to favor long term sustainability when the Austerians are in control everywhere? Economists? Maybe they mean onanists…uh,oh…did I speak out of turn?

“State of the art general equilibrium models” are the same DSGE crap that got us the GFC (“Global Financial Crisis) in 2007-9. Ditto for IS/LM, which the “liberal” Krugman cites repeatedly, while claiming to be a “Keynesian.” There are certainly limits to even Keynes, but even the inventor of IS/LM (Hicks) admitted it was a non-Keynesian model.

Economics is bunk.

The S class isn’t scarred, they do the scarring.

Self s – elected narcissists, the supposed overseers of the “policymakers” only care about reelection so it is short term thinking all the way down. Besides, the E class is very comfortable dictating to the H class.

At this point in time, projecting into the future, one guy will own it all and the rest will own nothing and be servicing that guy perpetually. TINA. Capitalism rules. Socialism is a swear word.

Which one person will get to own it all? Perhaps the Lords of Davos will have to lock themselves in a room with one axe in the center of the room. And the Surviving One Lord of Davos who comes back out is the Lord of Davos who owns it all.

Color me sceptical when they being out those good old dynamic general equilibrium models, which cannot really generate complex behaviour of an economic system, which is what I am pretty sure we are looking at here. See also CR’s comment above ;-)

I would love to hear Prof. Keen’s view on this.

Btw: In comparison, the original economics concept of hysteresis applied to the labor market and the mechanism was fairly simple: loss of skills leads to long-term unemployment.

If one of the cultural-behavioral scars left behind turned out to be the mass-dachafication of EUropean society and peoples, that might well be a scar worth having and nurturing.

After all, post-USSR Russia retained the social mass-dachafication of tens of millions of Russians as a legacy from Soviet days, and that level of dachafication allowed the Russians to keep themselves and eachother from running even shorter of food than they did in the worst of the post-Soviet times. ( To the best of my totally layman’s impression, to be sure).

These research papers are (almost entirely) theoretical; depend totally on the rigour of the original data collection and are clearly intended to generate funds for yet more theoretical research papers.

Why is no-one in Brussels tracking the ‘result multipliers’ by the EU countries most successful using EU funds? Likewise penalising those EU member states that most misuse the funds.

Here is news from Portugal on the state of their Bazooka recovery Innovation planning ….

President of National Innovation Agency gives up – 7th February 2023

<Joana Mendonça cites absence of support by key ministries

Another resignation by a senior State official with management functions in the application of EU community and ‘bazooka’ (PRR) funding.

…….

Ms Mendonça has told Expresso that it was “an honour” to work with the “spectacular team” at the agency, but she has not received “any guidance” from either the ministry of science, technology and higher education, or economy on issues “as relevant as the PRR (plan for recovery and resilience), the new framework of community funds Portugal 2030 or the system of tax incentives for research and business development (SIFIDE)”.

She describes “great unease” created in Brussels regarding Portugal’s indefinite participation in another European programme, says Expresso.

https://www.portugalresident.com/president-of-national-innovation-agency-gives-up/