Yves here. The post revisits a favorite topic. Back in runup to the crisis, the financial blogopshere was a vibrant place and Serious Economists interacted with finance experts to try to figure out what was going on. One hot topic was the first half 2008 runup of commodity prices, most of all oil. Your truly got in a big row with Paul Krugman, who insisted the levitation (the peak was $147 a barrel) was due to fundamentals. And he went even further, basically insisting financial speculators could not elevate prices without it showing up in excess inventories, when there were none to be found.

Yours truly will not belabor the key counterarguments, since the pre-crisis price reversal showed Krugman to be wrong. We reviewed this debate in ECONNED.

By Carlotta Breman, MSc. Student, Management of Technology, Faculty of Technology, Policy and Management, Delft University of Technology and Servaas Storm, Senior Lecturer of Economics, Delft University of Technology. Originally published at the Institute for New Economic Thinking website

The surge in U.S. inflation has been attributed to a number of supply-side causes, namely: (1) higher import prices; (2) higher energy prices; (3) higher corporate profit margins (leading to ‘greedflation’); and (4) the impact of COVID19 on wages in (mostly) low-wage occupations that had previously been considered safe (see Ferguson and Storm 2023 for a review). In addition, as documented by Ferguson and Storm (2023), U.S. inflation has increased in response to the recovery of aggregate U.S. consumption expenditure during mid-2021 and end-2022, caused by unprecedented gains in household wealth, particularly for the richest 10% of American households.

These supply-side and demand-side drivers of U.S. inflation have been widely analyzed, scrutinized, and discussed — but we nevertheless think that an important piece of the U.S. inflation puzzle is still missing. The missing piece of the puzzle concerns the rise in energy and oil prices, or, more precisely, the causes of the drastic increase in the price of crude oil, from around $40 per barrel in the second half of 2020 to a peak of $115 in June 2022.

A number of observers have pointed fingers at the excessive flow of money into financial instruments tied to oil (Meyer 2018; Verleger 2022). These money flows, they argue, have pushed the oil price up and away from its ‘fundamental’ value. It is well known that hedge funds are very active in the oil market and their activity, along with other speculators, has raised the volume of oil transactions far above the volume warranted by ordinary commercial transactions. However, other observers are skeptical that the oil price spike during 2020-2022 was speculative, arguing that the underlying (geopolitical) fundamentals of oil supply and demand changed significantly during this period (EIA 2023). Hence, and specifically focusing on the U.S. oil market, in our new INET Working Paper, we ask the question of whether the sharp increases in prices during 2020-2022 were due to fundamental shifts in supply and demand or whether they must be attributed (at least partly) to excessive market speculation.

Oil Prices, Oil Profits, and Inflation

From January 2020 to February 2023, the U.S. PCE price index rose by 13.8%, while the PCE price index for energy goods & services increased by 43.1%. Since energy is a major item of consumer expenditure, the sharp increase in energy prices did raise the PCE inflation rate. In fact, during March 2021 – June 2022, higher energy prices accounted for an average of 16% of the accelerating PCE inflation rate; and in June 2022, energy inflation alone was responsible for more than 21% of PCE inflation.

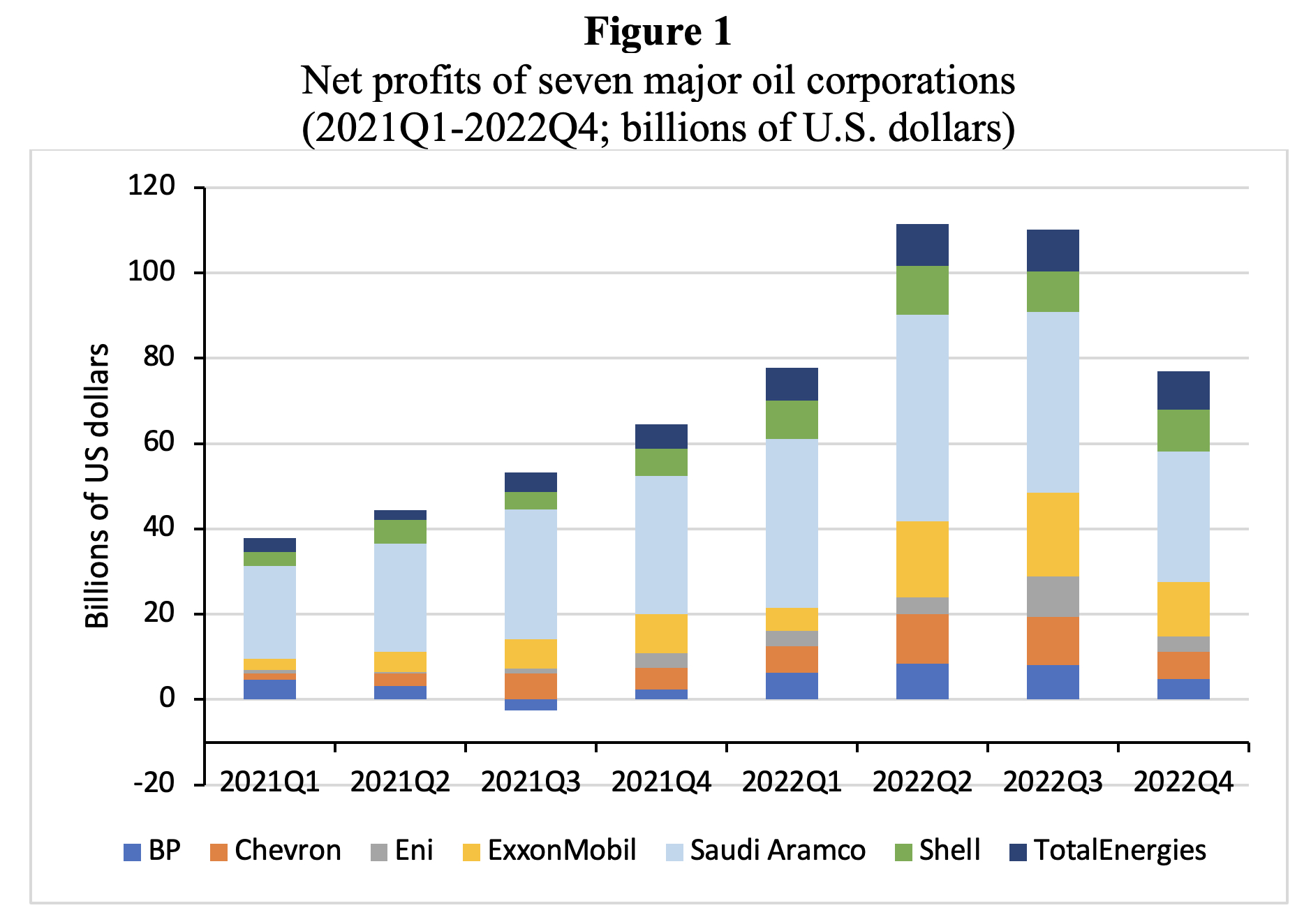

As consumers faced soaring oil (and energy) prices and struggled with fuel, heating, and electricity bills, the world’s biggest oil corporations broke company records for (annual) profits (Figure 1). Seven of the largest energy firms—ExxonMobil, Chevron, BP, Shell, Total Energies, Eni, and Saudi Aramco—made almost $200 billion in 2021 and $376 billion in 2022. These windfall profits are good news for the shareholders of these corporations. To illustrate, under pressure from shareholders, led by Wall Street firms such as BlackRock, ExxonMobil is planning to spend $30 billion on share repurchases in 2023 and another $50 billion in 2024. Chevron pledged a massive $75 billion share buyback in the coming years and is raising its dividend.

Source: Annual reports

As a result, the share prices of the oil majors have increased considerably during the period October 2020 – June 2022 (and beyond). In fact, the stock price of ExxonMobil and Chevron increased by 168% and 107%, respectively, while the share price of Shell plc rose by 142% during this period. The resulting wealth gains for shareholders did reinforce the wealth impact on personal consumption spending and demand, which contributed to rising inflation from the demand side (Ferguson and Storm 2023). From the cost side, rising (oil) profit margins have played a significant role in the acceleration of consumer price inflation, as is explicitly recognized, for the European Union, by economists from the European Central Bank (Arce, Hahn, and Koester 2023).

However, our aim is not to explain the exact pass-through effect of higher oil prices and profit margins on U.S. inflation but rather to determine whether financial speculation was a significant driver of the sharp increase in oil prices during 2020-2022.

Oil Price Speculation During 2020-2022

To answer this question, we use the supply and demand model in the spot market for oil, the storage market, and the futures-spot price spread, developed by Knittel and Pindyck (2016) and published in the American Economic Journal: Macroeconomics. The model allows for a clever decomposition of actual changes in the crude oil spot price into a contribution of supply and demand fundamentals and a contribution of (excessive) speculation; details of the decomposition can be found in the paper.

We have updated the model by Knittel and Pindyck, using recent data for the years 2020-22. The numerical outcomes of the model hinge critically on the choice of plausible values for the price elasticities of oil supply and oil demand. We take great care to properly contextualize the recent econometric evidence on these price elasticities within recent macroeconomic developments (i.e., rising interest rates), pressures to wean the economy off of oil (i.e., the ‘green’ transition), and geopolitical reality (e.g., turbulence in global oil markets following the Ukraine war and sanctions imposed on Russian oil).

We note that institutional investors, led by BlackRock, have convinced virtually every oil executive to keep spending to increase oil supply under control. Javier Blas (2022) adds that “today, the pressure from shareholders to remain frugal is so strong and uniform across the industry that from the outside it almost looks like a cartel. And the result is cartel-like: Big Oil is collectively underinvesting by a lot.” The oil majors prefer to continue to maximize revenues for shareholders from their decaying, sun-setting assets. Or, as Blas (2023) writes,

“No matter how high oil prices go above that level—say $100 a barrel—the industry will no longer add rigs to sop up market share. Rather, it will stay put and go into harvest mode with existing wells—that’s exactly what happened in 2022, much to the consternation of the White House, which urged shale companies to drill more.”

Oil companies, in harvesting mode, are holding back new drilling. The go-slow is a business reality, and the drastic curtailment of rig utilization—and capital destruction in the oil shale industry in earlier years—have been key factors constraining the already low price-responsiveness of oil supply during 2020-2022.

However, given the uncertainty surrounding the price elasticities of oil supply and demand, we have used the model to evaluate three empirically plausible scenarios. The numerical assumptions underlying our analysis and detailed results of the model analysis appear in the Working Paper. According to the model analysis, excessive speculation in the crude oil market has been responsible for 24%-48% of the increase in the WTI crude price during October 2020-June 2022.

Industry observers will not be surprised. “Fundamentals do not matter to a new breed of oil speculator”, writes Gregory Meyer (2018). A new class of prominent ‘macro speculators’, mostly Wall Street money managers, is not necessarily reacting to news about supply and demand but instead may be buying and selling oil futures based on moves in currencies, interest rates, or the price of oil itself. Veteran oil analyst Philip K. Verleger (2022) agrees, arguing that “oil prices in 2022 are being driven not by fundamentals but by those betting that prices will soon exceed $125, $150, or $200/bbl”.

Our estimates would translate into an oil price increase of around $18-$36 per barrel and an increase in the U.S. PCE inflation rate by circa 0.75 to 1.5 percentage points during October 2020-June 2022. Oil speculation thus has been a significant systemic factor contributing to the recent surge in the U.S. inflation rate.

Further Evidence of Speculation in Oil Markets

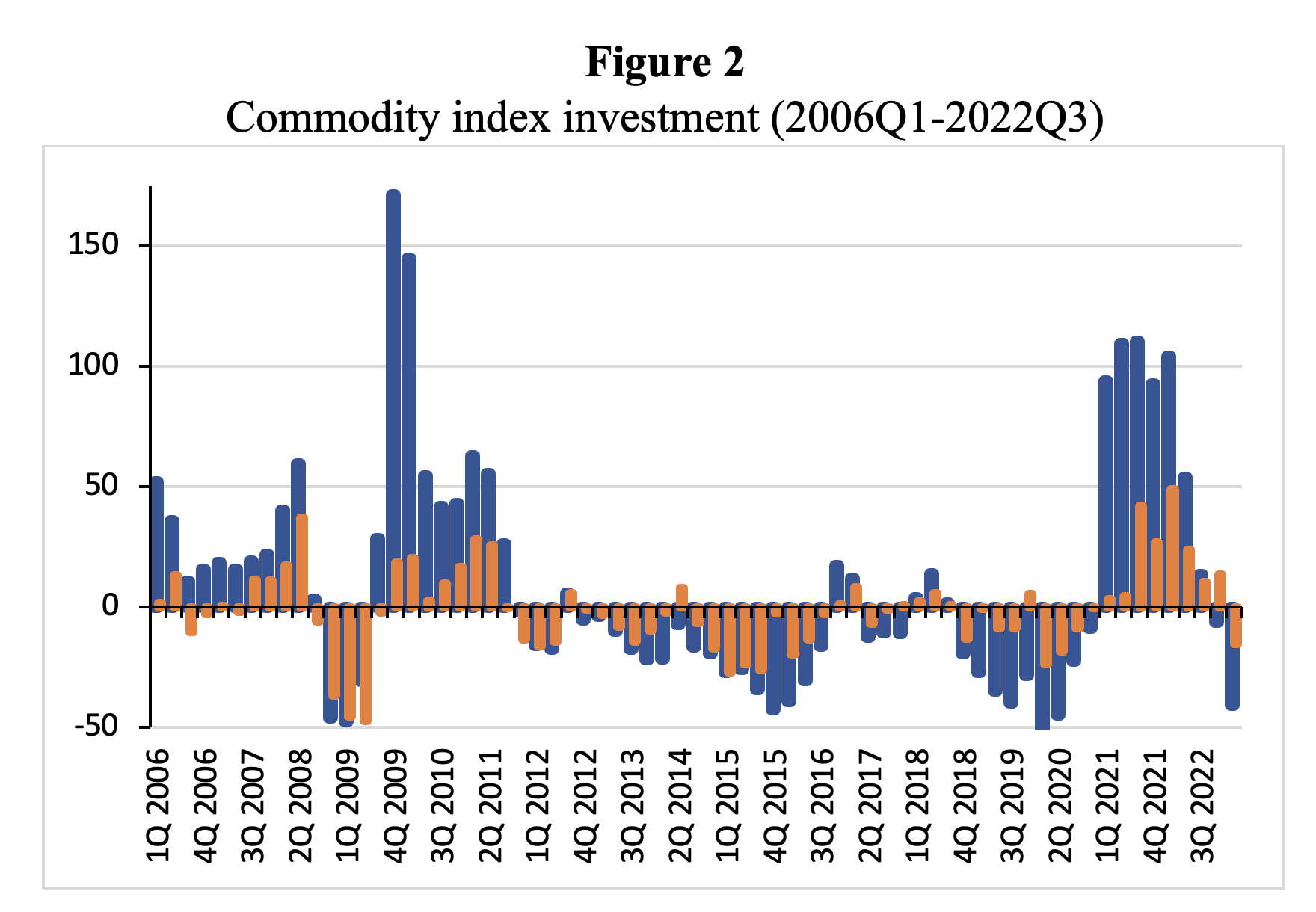

We complement our model analysis by an empirical investigation, based on monthly data for the period January 2004-January 2023. We show that (speculative) long non-commercial open-interest positions in oil futures have increased considerably relative to short non-commercial positions, signaling a sustained and significant increase in speculative pressure in the oil market. This strong growth of long non-commercial positions is related to the growing importance of ‘long only’ index funds. Commodity index investors, as Masters and White (2008) explain, “lean only in one direction—long—and they lean with all their weight.” Investors in such instruments expect commodity prices to rise; money is lost if the values of the underlying commodities in the index decrease.

Money flows to commodity index funds increased sharply during 2021Q1 and 2022Q2 (Figure 2); in cumulative terms, the value of assets under the management of commodity index funds grew by more than 300% on a year-to-year basis during these six quarters. (We note that energy commodities comprise around one-third of most commodity index funds, with crude oil comprising around 15 percent.) As a result, the oil market has become more financialized and, arguably, more speculative.

We find that merchants/producers of oil are outnumbered by Wall Street traders. We calculate Working’s T-index and find that a considerable degree of excess speculation is a persistent characteristic of the crude oil market. Another widely used measure for ‘speculative pressure’ shows a clear upward trend. And employing linear Granger causality testing, we find that there is a unidirectional effect of futures oil prices on spot oil prices (during 2004-2023). This result falsifies the ‘fundamentalist’ claim concerning the oil market that spot oil prices are fully determined by economic fundamentals, and, hence, there is no way in which futures prices—and excessive speculation—can affect spot prices.

Note: Year-on-year percentage change in commodity index assets under management (4 largest public U.S. commodity index funds). These changes are compared to year-on-year percentage changes in the Bloomberg commodity price index level. When the growth rate of assets under management (blue bars) is greater (resp. more negative) than the growth rate of the price index (orange bars), this indicates a net inflow (resp. outflow) of index investment. Source: EIA

In addition, and again using Granger causality tests, we explore the potential impacts of higher prices for crude oil on the futures prices of corn and soybeans (which are major food commodities) and the price of fertilizers (a major agricultural input). Our econometric results show that oil speculators have to be held accountable for driving up fertilizer and (indirectly) food commodity prices as well—and by doing so, oil speculators have further fuelled U.S. consumer price inflation, while increasing food insecurity and food poverty in the U.S. and abroad.

Conclusions

Higher energy prices have been a major driver of the surge in the U.S. PCE inflation, accounting for 21% of PCE inflation in June 2022. Under reasonable empirical assumptions and using the model of Knittel and Pindyck (2016), our analysis shows that speculative activity in the crude oil market has been responsible for 24%-48% of the increase in the WTI crude price during October 2020-June 2022. A back-of-the-envelope calculation suggests that these estimates translate into an oil price increase of around $18-$36 per barrel and an increase in the U.S. PCE inflation rate by circa 0.75 to 1.5 percentage points during October 2020-June 2022.

Our estimations of the extent by which speculative activity in the oil market has driven up oil prices, are supplemented by direct evidence of the degree of speculative activity in the WTI crude oil market.

The higher oil prices are also found to have raised the price of fertilizers, thereby raising the prices of major food commodities (corn and soybeans). Oil speculators have been indirectly responsible, therefore, for driving up food commodity prices as well. Higher oil prices squeeze real incomes, and disproportionately hit lower- and middle-income households (as these are spending a larger proportion of their budgets on energy and food than the richer households).

If all this speculation is pushing oil prices higher and leading to higher PCE inflation, with adverse societal consequences, then what can be done to eliminate excessive oil speculation?

For one, the Commodity Futures Trading Commission (CFTC) can establish speculative oil position limits equal to the position accountability levels that have been in place at the New York Mercantile Exchange since 2001. Second, the CFTC can raise the margin requirements on speculative oil trading so that non-commercial traders (often Wall Street investment banks and hedge funds) back their bets with real capital. And finally, financial firms including Goldman Sachs, Morgan Stanley, and other Wall Street investment banks engaged in proprietary oil (swap) trading should be classified as speculators, instead of bona-fide hedgers.

There is a catch, unfortunately: when these remedies are taken only by the U.S., they will not work, because oil speculators will move offshore. Remedies need to be internationally coordinated. Growing geopolitical tensions in a belligerent multipolar world further sadly complicate the matter (Ferguson and Storm 2023).

See original post for references

Interesting Krugman’s position. I read long ago some post from him talking about different “equilibrium prices” regarding oil markets. If I remember correctly he didn’t specify if those different equilibriums were driven by speculation and profit searching.

Imagine if commodity speculators had to take physical delivery of their ‘game piece’.

Imagine of commodity markets were only open to trade to producers.

The parasitic disruptive Big Boys and Girls in Chicago and New York wouldn’t know what to do with themselves!

I remember some time back reading about huge tank farms that were being rented (possibly owned?) by Wall Street oil speculators. I think the gist of the article was they do take delivery in order to reduce supply in the market and to drive the price up. Once the price is suitably high, they sell their reserves back into to the market. Manufactured arbitrage I suppose. That is what I remember. It would be interesting to know if the scheme is still being used.

That isn’t arbitrage, which is (ab)use of difference in pricing in markets to strike a series of matching deals. In the old days of telex machines and poor telecom coverage it was what drove physical trading giants like Phibro or Helm (information inequality). Now a days it’s what computer trader robots set about. In general due to improved communications the margin on arbitrade is too thin to support much if any overhead. The only risk in arbitrage is if one of the buyers or sellers default on delivery (of money or goods).

What you describe is speculation possibly combined with manipulation, which Phibro and Helm also did, but due to the high risk it often finished off firms who bet too big and lost, like ASOMA or PLEXCHEM. Now-a-days with too big to fail, I guess it’s the US citizen who provides insurance on the new breed of bank owned traders.

I think the activity Someguy describes is referred to as cornering the market.

Cornering the market is one tactic in speculation, It requires either a (nearly) unitary market with precisely known quantities to manipulate and sufficient bank to carry it off together with demand, or it has to have artificial barriers (ie: governmental regulations) which limit access. It’s extremely difficult to pull off even in exotics like silver, ask the Hunt Brothers (decedents?), I doubt even the Saudis and Russians together have that kind of heft. This is a mix of speculation and manipulation, but not at anywhere near cornering a market with so many mechanisms like the US salt dome deposits that dwarf tank farms (which mostly store down stream derivatives for far better profit).

Oil needs processing to become a useful product for nearly all needs. My expectation, based on Al Dunlap style caprification, Bain Capital financialization, Shell Oil style loss of skills, etc; that it is restrictions in refining and other value adding processes which at as gate keepers, ie: targets for profiteers, which are primary inputs into inflation. The Saudis and Russians are not cutting output to raise prices but to stave off a collapse, but even if oil fell through the floor I would not expect much difference in the behavior of the profit seeking gate keepers.

Yeah, but it’s more than profit seeking, it’s monopoly/oligopoly rent extraction and financial parasitism.

Monopoly/oligopoly rent extraction and financial parasitism are means to greater profit. Society, or some part of it, decides what restraints are placed on the pursuit of profit.

….which act as gate keepers…

IMF Confirms that Profits Are Driving Inflation

Krugman’s record is pretty dismal. Although I haven’t read or listened to him in years, he always seems to defend the status-quo, and the D team of the political duopoly (D/R dictatorship). He has been proven wrong so many times, it’s a wonder he has any credibility left. He doesn’t have to – as long as he does his job as apologist for oligarchy. He still adheres to mainstream neoclassical “theory” (ideology) even now.

“It is difficult to get a man to understand something, when his salary depends upon his not understanding it.” (U. Sinclair)

It is refreshing to see a thorough study of what appears pretty straightforward to some of us. But folks like Kruggie will bend over backwards to deny the obvious – that’s his job. I wonder if he really believes in his own claims?

Conclusion: “Higher energy prices have been a major driver of the surge in the U.S. PCE inflation, accounting for 21% of PCE inflation in June 2022…”

If I understand the paper correctly, the financial speculators are betting on driving a near future oil price of $125 – $200/barrel. This implies either bankruptcy of the long betters if prices stay relatively low (stock market crash), or collapse of the economy when consumers can’t afford the sky high prices (recession/depression), all of this leading into the election. One of the experts here on energy/finance, please correct me on this.

Depends on how they covered the futures price, long or short; what options (insurance) they purchased, etc. They may have even already bankrupted the firm by theft, and like main characters in “The Producers” or Marc Rich, they may be vehicles that need to go bust. Perhaps they engaged in sanctions busting, and periodically need to be busted like a piñata , so the party on the other side of the trade now gets (reasonably) arms length clean funds. Naturally, as was the case with many firms that did business with Marc Rich, the beneficiary is just another arm of the owner of the vehicle. Consulting engineers have to be aware and very careful about with whom they do business, or they may accidentally find an inconvenient fact and wind up slipping on their hotel balcony, even if the hotel doesn’t have balconies. Apparently that happened more than once to ship surveyors who inspected vessels chartered to Mr. Rich.

Is this why the major producers are cutting production even with rising prices? There isn’t real demand, and the inflated price means the same revenue for less product so why not? Is the speculative position that oil will go up in some way supported by global production cuts?

I was listening to Duncan’s Russian revolution(s) ep 62 the other day “Inflation and Scarcity”. It was discomforting, not the exact details but the broad outlines. And now I’m starting to wonder if the US could experience inflation and scarcity when it comes to oil.

100 times more electronic oil is traded in New York each day than the amount of physical oil traded in the rest of the country; that should tell you who’s setting the price..

Sounds like Vegas vs. the rest of Arizona/

Reminds me that back when the Syrian civil war kicked off, and Saudis leaned in by opening the spigot, quite a few full full oil tankers sat idle in the Irish Sea as traders were trying to stall delivery on their now worthless contracts.

On a related note, Ann Pettifor discussed this briefly in a recent Geopolitical Economy Report episode. There’s a bit of a preamble starting at 43:00 which ends at 47:20. Pettifor’s narrative account made this really clear to me in a way it hadn’t been before, especially her discussion of a town which bought it’s own windmills only to find that doing so did not affect what they pay for power because the price is already determined by trading and a good deal of that trading is speculative.

https://www.youtube.com/watch?v=-uxyjIFqi4o