We will soon go through some of the elements of the rap sheet of former Fed chairman Alan Greenspan, who just died at age 100, that may not be as well known as other misdeeds, the biggest being the Greenspan put, which then became the Bernanke/Yellen/Powell put. But to prove that he was not as well respected even in his heyday as the press then would have you believe, a story from a finance professional prominent enough to be regularly invited to Economics Club of New York talks:

One time, when I was on the last shuttle flight from Washington DC to New York, Greenspan was on the same plane. I debated whether I would be willing to die in a crash if it killed Greenspan too. I quickly concluded “yes”.

In other words, during Peak Greenspan, many skeptics held their tongues rather than fight the tape of the media cheerleading.

Reagan replaced Volcker as Fed chairman with Greenspan despite Volcker having implemented Friedmanite (as in neoliberal) monetary policies and explicitly seeking to weaken labor bargaining power during his super-high interest rate experiment attributed with breaking the back of 1970s/early 1980s inflation. In his book on the Federal Reserve, The Secrets of the Temple, Bill Greider recounted that Volcker kept an index card of weekly average construction wages and was looking for them to start falling as proof that his punishment was working. IIRC, Volcker said, “I want unions to get the message.”

Even though Volcker was tough on labor, he was also tough on big finance. He believed banks should stay largely simple and stupid, as in focus on their core role of payments processing, and correctly saw fancy finance as rentierism. Volcker said the only real innovation he had seen in banking was the ATM.1

Volcker was ousted due to his refusal to support bank deregulation. From a 2020 paper by Thomas Ferguson, Paul Jorgensen, and Jie Chen:

For months the suspense built up. By the late Spring of 1987, the initial trickle of anxious conjectures had swollen into a raging torrent of speculation and suspicion. On June 2, 1987, the worldwide guessing game came at last to an end: the White House announced that President Reagan would nominate Alan Greenspan to replace Paul Volcker as Chair of the Federal Reserve Board. Markets reacted with shock: “the news stunned the financial markets, which had come to regard a third term for Mr. Volcker as highly probable. Bonds finished with one of the biggest losses on record, and the dollar tumbled” (Hershey 1987).

At the time, the official story was that Volcker had indicated in a letter that “he did not wish to be reappointed after eight years in the job.” Even then many doubted that was the whole truth: “It appeared that White House efforts to persuade Mr. Volcker to remain were minimal. It is understood that Mr. Volcker would have accepted a reappointment to the post if the President himself had urged

him to do so. But no such effort was made.”In fact this gloss was an epic understatement, linked closely to a second – and far more profound – misjudgment: “Economists and other analysts said Mr. Greenspan, in taking a job that is sometimes described as the second most

influential in the nation, was unlikely to pursue a policy markedly different from

Mr. Volcker’s.”The truth, as a few insiders knew, was very different. At a crucial White House meeting of top Republicans convened to discuss Volcker’s fate, the hostility of Treasury Secretary James A. Baker and his Deputy, Richard Darman to the six foot, seven inch cigar chomping Fed Chair spilled out into the open. GOP Senate Leader Robert Dole and Senate Budget Committee Chair Pete Domenici, who came suspecting that Baker and Darman wanted to substitute Greenspan, pressed a case for reappointing Volcker. They questioned whether his experience and knowledge of international economic issues did not make him irreplaceable. Baker flatly rejected this, saying that he and Darman now knew enough to deal with the G7 issues.

Eventually the discussion worked around to the reasons for Baker’s opposition. The Treasury Secretary responded by naming two issues: Volcker’s skepticism about financial deregulation and, in particular, his opposition to repeal of the Glass-Steagall Act, the New Deal measure that severed investment from commercial banking. Asked why that issue was so important, Baker’s answer was startling direct: Possible repeal of Glass-Steagall was the signature issue used by investment bankers, led by Robert Rubin, then of Goldman, Sachs, to raise money from their cohorts on Wall Street for the Democratic Party. Getting rid of Glass- Steagall, Baker explained, would alter the balance of power between the two major parties by depriving the Democrats of a central revenue stream.

Readers might say, that plan did not wark as intended. After all, Glass-Steagall was not repealed until 1999.2

But as we have said, by then Glass-Steagall was so shot full of holes that its repeal was a mere formality, passed mainly to tidy up the legalities of Citigroup acquisition of insurance giant Travelers.3 Glass-Steagall came to an end in a very big way in 1988 (no typo) when very early in Greenspan’s tenure, the European commercial bank Credit Suisse merged with bulge bracket firm and fixed income powerhouse First Boston to rescue First Boston in the wake of the 1987 crash (First Boston had badly wrong-footed some high-risk bond exposures). Both Citibank and JP Morgan were pushing the envelope as hard as they could in the late 1980s and through the 1990s in their investment bank adventurism. Similarly, the Fed allowed an “affiliation” between Citibank and Salomon Smith Barney in 1998 that was effectively a merger.

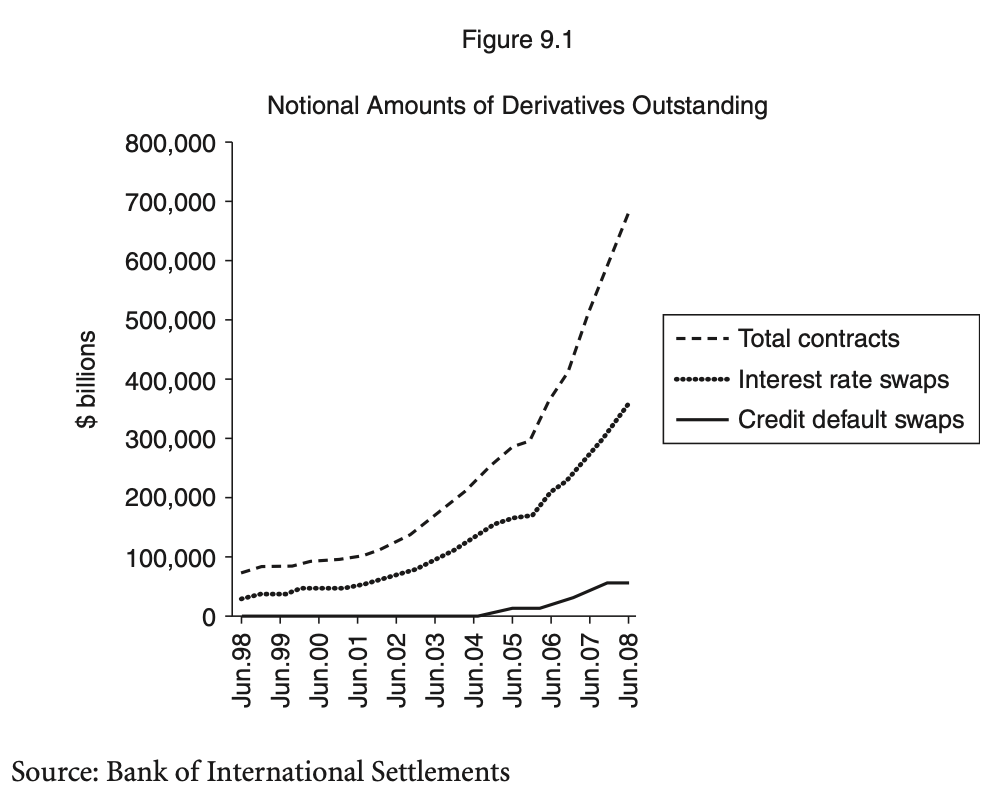

But an even bigger and less well known Greenspan sin was allowing unregulated derivatives trading. As we explained long form in ECONNED, the 2008 crisis was not a housing crisis but a derivatives crisis of instruments that referenced particularly risky subprime exposures. The entire subprime market was not big enough to produce more than at worst something a big nastier than the saving & loan crisis, nor a near failure of the global financial system. But credit default swaps and CDO composed heavily of CDS referencing BBB-subprime tranches created exposures of 4 to 6 times the real economy value and concentrated them at systemically important, overleveraged financial institutions.

And Greenspan’s pathological neglect and the systemic effects greatly predate the famed row of Greenspan and Treasury Secretary Bob Rubin against CFTC chair Brooksley Born over regulation of credit default swaps, with Born lost. Greenspan ushered in the widespread use of derivatives which are used almost entirely for speculation, thus diverting resources and “talent” into socially destructive activity. And as we will soon explain, the explosive growth of over-the-counter derivatives markets was a major driver of demand for securitized products.

In the early 1990s, your humble blogger had one of the two top derivatives trading firms, O’Connor & Associates, as a client. Their big competitor was Bankers Trust. My time with O’Connor showed me that it took an extremely high level of sophistication, in staff training, risk modeling, internal organization (as in trader/position management) and IT (where O’Connor was bleeding edge, running the biggest UNIX network in the world ex DARPAnet itself). It was way too easy for mere mortals to blow themselves up; O’Connor did some advising to Fortune 500 companies who had done just that. The idea that a sophisticated multinational like Proctor & Gamble could claim to have been victimized when they should have damned well known what they were doing is a further testament to the high skill level needed to manage derivates operations properly.

I recall gasping out loud, I believe in 1996, when I read in Institutional Investor that Greenspan was adopting a “Let a thousand flowers bloom” approach to regulatory oversight of derivatives risk at banks, as in doing nothing. But Greenspan believe that reputational risk would keep industry participants on good behavior.

In reality, I later learned that JP Morgan was in a big push to get its version of Value at Risk models adopted. I won’t belabor as to how, but JP Morgan clearly thought this would give them competitive advantages.

The result was that regulators came to operate in a close to blind manner, much like a doctor treating blood pressure as a reliable indictor of patient health, when it needs to be included with other measures. And we will skip over how badly VaR models peformed in the crisis.

Forgive us for the deep dive, but ECONNED explained how the free markets approach to derivatives was a, if not the, major driver of the 2008 crisis, to create more AAA rated paper to secure derivatives positions. The AAA tranches in most securitizations account for 70% to 80% of face value. From ECONNED:

Some have argued that the parabolic increase in demand for repos was due in large measure to borrowing by hedge funds. Indeed, Alan Greenspan reportedly used repos as a proxy for the leverage used by hedge funds. Others believe that the greater need for repos resulted from the growth in derivatives. But since hedge funds are also significant derivatives counterparties, the two uses are related.

Brokers and traders often need to post collateral for derivatives as a way of assuring performance on derivatives contracts. Hedge funds must typically put up an amount equal to the current market value of the contract, while large dealers generally have to post collateral only above a threshold level. Con- tracts may also call for extra collateral to be provided if specified events occur, like a downgrade to their own ratings. (Recall that it was ratings downgrades that led AIG to have to post collateral, which was the proximate cause of its bailout.) Cash is the most important form of collateral. Repos can be used to raise cash. Many counterparties also allow securities eligible for repo to serve as collateral.

Due to the strength of this demand, as early as 2001, there was evidence of a shortage of collateral. The Bank for International Settlements warned that the scarcity was likely to result in “appreciable substitution into collateral having relatively higher issuer and liquidity risk.”

That is code for “dealers will probably start accepting lower-quality collateral for repos.” And they did, with that collateral including complex securitized products that banks were obligingly creating.

We were too polite in ECONNED. Another way to tell the story is “Greenspan’s ‘Let a thousand flowers bloom’ approach to derivatives led to a kudzu-like proliferation and excessive risk-taking.”

Unnecessary complexity, since it enables structurers to pull out more fees than for plain vanilla products, can support the general tendency towards overdiversification as a bizarre counter to a fondness for unduly tailored exposures (basically fund manager busywork which again adds to false perceptions of value added and too many fees), and is often useful in getting chumps to eat too much risk for too little return.

But press commentary seldom addresses the big system-wide drag of fostering yet more unproductive financialization. Instead they focus on the public’s hot buttons and in the process, often help perpetuate financial services industry information fogging.

As much as readers might not like hearing it, most of the structured credit products in the chart above were tested in the crisis and got through unscathed, such as collateralized loan obligations (a pretty conservative structure) and commercial real estate MBS (which unlike subprime, have loans big enough that services can work out if they go back, and thus servicers are paid to do modifications).

By contrast, subprime mortgage backed securities had always been trouble. There had been a much smaller subprime market in the 1990s which hit the wall for essentially the same reasons as the 2000s versions. The structured paper didn’t pay enough to cover the risks and provide enough in fees to the intermediaries for putting them together to sell them. The “solution” had been to shortchange the lowest rated tranche, the BBB/BBB- tranche, in terms of yield and other protections. That was only a small part of the total face value, 3% to 4%. But there weren’t enough stuffees for this paper. So like making sausage out of less desired pig bits, they were rolled into CDOs, with enough better-looking assets to make them minimally appetizing. Again, the top tranche of CDOs was rated AAA but traded at more like AA yields (as in investors recognized the AAA ratings were a stretch).

So to truncate a much fuller telling of this tale, the problem was not asset backed securities per se but picking assets to securitize in bulk that were really not well suited to the exercise, and then “solving” that problem with a leverage-on-leverage scheme, the asset-backed-securities CDO, colloquially called the subprime CDO. Leverage on leverage on any scale is a ticking time bomb. Similarly highly leveraged trust of trusts (and trusts of trusts of trust) precipitated the Great Crash of 1929.

But Greenspan was far too much a free markets true believer to even consider that markets have a propensity to generate bubbles and manias since they are highly profitable to the intermediaries as they build up, plus the insiders often manage to escape losses when they implode, or at least believe they can.

We could go on and on and on, but expending too many pixels on Greenspan gives him more dignity than he deserves.

____

1 After the crisis, Bank of England governor Mervyn King pushed hard for what was called ring-fencing, as in a rollback to the separation of investment banking, with the intent of also subjecting traditional banks to stricter regulation. King and his allies lost to Treasury.

2 I hate to pull rank, but this is terrain I know particularly well. When I joined McKinsey in 1983, I was assigned almost entirely to studies to help commercial banks get into investment banking. For instance in the early 1980s, I was in the room when a Citibank manager proudly told us how Citi had moved an entire commercial company on and off their books, almost as a financial engineering stunt. We were quietly aghast since this was clearly illegal under the rules at that time.

3 We will skip over how Greenspan largely got the Fed out of taking its job as the regulatory supervisor seriously, although the Fed fiercely insisted on keeping that role when Gramm–Leach–Bliley Act was being finalized.

Thanks for the deep dive. We are here to learn.

And is it not well past time for Bob Woodward, author of Maestro, to have his own reputation slashed? It says it all that bigfoot journalism, after pretending to save the republic during Nixon, so comfortably got down “on bended knee” for Reagan and figures like Greenspan. Those now mourning The Washington Post don’t want to talk about how genuinely horrible it has been since their big triumph. Just the other night PBS did a rerun of a show praising Katharine Graham as some kind of truth and justice hero. It’s this sort of fakery that gave us Obama and his new mecca for the fakees.

re: WaPo – I like this embarrassing detail via Taibbi:

Who Helped Overturn the “Pentagon Papers Principle”? The Washington Post and New York Times

https://www.racket.news/p/who-helped-overturn-the-pentagon?utm_source=publication-search

“(…)

Three steps later, the two authors posited that reporters “Break the ‘Pentagon Papers Principle.’” What’s fascinating about this ambitious change proposal is who signed off on it. In addition to onetime New York Times figures like Taubman and Corbett, and current and former Washington Post representatives like R.B. Brenner (a consultant on the movie The Post, lionizing the Pentagon Papers decision!), Glenn Kessler, David Cho, and Tracy Grant, the Stanford authors cited Terence Samuel and “roughly 20” other editors and reporters at National Public Radio:

(…)”

p.s. It´s also rumoured that Graham´s “heroic” senior editor Bradlee played by above Tom Hanks in real life threatened NYT´s Sheehan when latter intended to publish an honest account of Katherine Graham´s life and work where Sheehan apparently wanted to disclose affiliations to the CIA etc.

—copy of letter to NYT

https://www.nytimes.com/1991/06/23/opinion/l-did-the-pentagon-papers-change-anything-624891.html

“But an even bigger and less well known Volcker sin was allowing unregulated derivatives trading.”

Do you mean Greenspan here allowing or Volcker disallowing?

Thanks for the catch. Fixing. Volcker would be spinning in his grave at the idea that he approved of any sort of deregulated trading at banks, ex Treasuries and high quality public debt instruments.

The title alone has me cheering for this one!!!

Me too.

Ditto! And awesome footnotes.

Double ditto — and the whole shebang is awesome! Many thanks and kudos to Yves. Read ECONNED several years ago: time for a re-read : -)

Just a reminder what Clinton said about getting rid of Glass-Steagall with Greenspan’s connivance-

‘In 1999, on signing Gramm-Leach-Bliley into law, Clinton said, ‘This is a day we can celebrate as an American day’ and that ‘the Glass-Steagall law is no longer appropriate for the economy in which we live’ and ‘today what we are doing is modernizing the financial services industry, tearing down these antiquated laws and granting banks significant new authority’ and ‘This is a very good day for the United States.’

Columbia Journalism Review, Bill Clinton on Deregulation

https://archives.cjr.org/the_audit/bill_clinton_the_republicans_m.php

So, how did that end up working out? /sarc

The Clinton/Gingerich era pols were the first group of move-fast-and-break-things. The tech bros came later.

I wonder if Greenspan, Clinton, et al have been able to grasp the scale of destruction they unleashed on the US and the world. The tech bros are unabashed vandals, taking joy in destruction as an expression of power like toddlers knocking down a block tower or juvenile delinquents breaking glass to hear the smash (see Elon “I am not an incel” Musk). I can slot Clinton, the consummate over-compensator, in with the delinquents; probably Gingrich also. But Greenspan? Did he believe what he said? Did he want to smash the world? Was he just evil?

Re: “Destruction”

The Death Toll of Western Sanctions 1971 – 2021

28 Million dead. Just from Sanctions (bombing not included)

564 258 deaths X 50 years

https://www.thelancet.com/journals/langlo/article/PIIS2214-109X(25)00189-5/fulltext

Clinton was taking credit for letting a horse out of the barn when it had already gotten to the next county.

Thank you, Yves.

Love your “no holds barred’ approach to the Greenspan legacy.

I am ordering a copy of your “ECONned” today.

Appreciated,

Alan

And I’m long overdue in re-reading the book.

Greenspan’s magician’s act speaking to Congress was gobbledygook* given in a thoughtful and measured voice designed to obfuscate, imo.

Congress and the press thought it must be very wise and hard to understand since they couldn’t understand it. No. It was not hard to understand. But, like the emperor’s new clothes, none of them dared say it was bunk.

One of the three men who saved the world? Rubin, Summers and Greenspan? Oh please….

https://content.time.com/time/magazine/archive/covers/1999/1101990215_400.jpg

*gobbledygook: wordy and generally unintelligible jargon.

Greenspan was selling Congress and the press a financial encabulator-

https://www.youtube.com/watch?v=MXW0bx_Ooq4 (3:53 mins)

It amazed me at the time how when Greenspan was giving a speech, that he would be treated like Moses coming back with the stone tablets.

Stone Tablets 1.0 or Stone Tablets 2.0?

If you mean Stone Tablets 1.0, I can agree since what came next if I remember correctly, were the Golden Idols.

It’s a little know fact that originally there were three tablets-

https://www.youtube.com/watch?v=-8ihcq4hzR4 (1:15 mins)

As I recall, Greenspan’s speaking style was described by listeners as causing MEGO.

My Eyes Gloss Over.

Hahaha. I had just made a similar comment, looking over comments to make sure I wasn’t repeating anyone else’s. Still time to remove mine.

“…over regulation of credit default swamps,…”

I see what you did there… :)

I started on Wall Street in 1988, when most trading firms were still partnerships (partly because exchange memberships were only held by individuals, not corporations), and was at Swiss Bank (now UBS) just after they acquired O’Connor. Earlier, the O’Connors had founded First Options, which went in and out of bank ownership in the late 80s / early 90s, as brokerages, clearing firms, and specialists sought non-loan ways to tap pools of bank capital, and banks saw the fortunes that trading firms were making (which they had previously looked down upon, equity trading being a job not suited to college graduates). Foreign banks in particular were early to, and good at, the job of hammering away at the Glass-Steagall walls. My view is that the Fed was happy to turn a deaf ear to the hammering, as foreign banks acting as Treasury primary dealers were a significant force in pushing offshore Treasury sales.

Haha Freudian typo! Fixing.

I love breaking the taboo against speaking ill of the dead. When Franco died, I offered my condolences to a fellow grad student. He set me straight. I read Martin Mayer’s three volumes done over a period of years, The Bankers books. It’s been I while, but my recollection is that they will continue to push the limits with more and more systemic risk until one of these days, they will do the ultimate crash.

They came close in 2008. O bailed out the bankers and let Main Street fail. This 2009 Atlantic Magazine article by Simon Johnson is very good:

The Quiet Coup

https://www.theatlantic.com/magazine/archive/2009/05/the-quiet-coup/307364/

The same unpaywalled article in pdf form here:

https://fcic-static.law.stanford.edu/cdn_media/fcic-testimony/2009-1020-Johnson-article.pdf

In these 2 paras he talks about the difficulties the IMF had in righting a small country’s teetering economic situation.

“No, the real concern of the fund’s senior staff, and the biggest obstacle to recovery, is almost invariably the politics of countries in crisis.

“Typically, these countries are in a desperate economic situation for one simple reason—the

powerful elites within them overreached in good times and took too many risks. Emerging-

market governments and their private-sector allies commonly form a tight-knit—and, most of the

time, genteel—oligarchy, running the country rather like a profit-seeking company in which they

are the controlling shareholders. “

Thanks for the links to Johnson, Flora.

Replace country with party and you have the Democratic Party.

I disagree. I think the taboo is well worth observing. To spit on a grave is to show a contemptible weakness. You owe it to your own self-respect, to never do such a thing.

It takes nothing away from my opposition to a man, to bid him farewell from this world. What quarrel should I have with a corpse?

If you regret that you did not harm him while he was here, that blame falls on you, not him. If you never meant him harm, then you should be glad that the temptation is gone. Either way, why speak ill of the dead?

For my part, I think that every day a man is alive, is a day when he might do better. Now you might object that every day, he could also do worse. But is that any less true of you or I?

The moral peril of being alive is something shared by us all, no less than the mortal certainty. Respect for the enemy, therefore, is respect for myself. Respect for the dead is respect for the living. Respect for the man, is respect for mankind.

In my opinion, that forms the proper socialistic ethos.

Couple of things.

1. Literally the first “modern political memoir” I’d ever read was the 2004 book by Ron Suskind on Paul O’Neill – Bush Jr.’s first Treasury Secretary, and former CEO of Alcoa – about 90% of which was basically O’Neill talking to Suskind, and the latter acting as the court stenographer.

Naturally, a big chunk of the book dealt with the Bush Tax Cuts, the first tranche of which came through in 2001. The way O’Neill spun the story (through Suskind), the first tax cut bill “needed” Greenspan’s support, which the latter only agreed to provide if triggers were included to roll the tax cuts back at the first sign of a deficit. Bush then perfidiously didn’t include any triggers, and Greenspan was a sad panda as a result, but could obviously do absolutely nothing whatever to kill the bill or its 2003 sequel. [Some quotes and additional critique from a random 2007 CBS News story, https://www.cbsnews.com/news/greenspan-and-the-triggers/%5D

What the whole – long – description of the episode told a very young me at the time was that a) Greenspan was a spineless political operative who, notwithstanding his own druthers, would bend with whichever wind was blowing through the White House and Congress, while blaming others for any bad after-effects; and b) Greenspan at his core was – or represented those who were – an adherent of the Church of Austerity, even when supporting deficit-driving policies (i.e. tax cuts for the wealthy). Which was clearly not the impression Suskind and O’Neill had wanted to convey, by the way.

Separately, both from this book and from listening to the man himself during the back end of his Federal Reserve tenure, I formed the impression that the man was not especially bright nor his ideas especially deep, but that he deliberately used obtuse language and complex sentence construction to provide the impression of oracular wisdom – a sort of a different twist on William Buckley’s gimmick. But in any case, I wanted to share the O’Neill book here as sort of another side to what Greenspan was doing whilst in office.

2. In a broader sense, I always wondered whether Greenspan genuinely believed at least some of the stuff he was spewing or advocating while at the Fed, or whether he simply defined his role at the Fed as being the empty vessel into which Wall Street poured its interests and wishes. At first, at least, I mean, if you keep saying something for 20 years straight you eventually come to believe it by mere virtue of human psychology.

But I remember listening to him in the hearings in the aftermath of the 2007-2008 financial crisis voice, in his obtuse and grammatically complex way, his dismay that Wall Street firms did not self-regulate after all, and thinking to myself – you can’t be this dumb. It’s a very politically convenient position to pretend this is the case, which would fit very well with his entire career, but literally every Wall Street guy standing next to me listening to that same testimony was laughing (!), out loud, at the very notion.

So was Greenspan a spineless operator pretending to have believed in self-regulation? Or was he a genuine adherent whom Wall Street types employed as a useful idiot? Not sure either way, myself…

On what Greenspan believed: I think Alan Greenspan, perhaps the deepest believer among those who believed in free markets, finally admitted his entire career was built on a mistake. Greenspan testified in Congress on the 2008 financial crisis and to Congressman Henry Waxman Greenspan said, “I made a mistake in presuming that the self interests of organizations, specifically banks were such that they were best capable for protecting their shareholders and equity.”

Waxman: “In other words, you found that your free market ideology was not working.”

Greenspan: “That’s precisely the reason I was shocked, because I have been going for forty years with very considerable evidence that it was working.”

Let’s not forget that while the deficit triggers may not have made it into law, the Bush tax cuts were scheduled to sunset in 2010, as a gimmick to make the CBO scoring “revenue neutral” or something like that.

And then, in 2010, right around Christmas if my memory serves me, Nancy Pelosi, who was House Speaker at the time corralled all her minions back to DC during the holidays to make sure that provision got struck and the tax cuts were extended. In an appropriations rider of some “must pass” legislation. I still remember where I was – at the airport, watching the spectacle unfold on CNN on the monitors at the gate.

Of course, Barack Obama was President at the time and could have vetoed it, as well.

I’m pointing out that perfidy does not limit itself to one party.

Found this on Wikipedia:

Also, found this:

Let’s not forget the Greenspan Comission changes to Social Security under Reagan and passed by the democratic congress. Raising retirement age, making benefits taxable, cutting benefits, constructing the charade of a locked trust fund, etc, etc. From Wikipedia:

Alan Greenspan was a grown-ass man who nevertheless fell in love with Ayn Rand’s nonsense, which was way more than enough reason to pay absolutely no attention to him.

He had lots of company on that one.

NPR had an aw shucks gee whiz piece yesterday about Greenspan’s connection with Rand,

https://www.npr.org/2026/06/22/nx-s1-5866558/alan-greenspan-dead-ayn-rand

In 2000, Christopher Hitchens (maybe there were signs) wrote a piece for Vanity Fair the entire subtext of which is that Greenspan’s enthusiasm for Rand made him interesting and intellectually serious, kind of like his love of jazz:

https://www.vanityfair.com/culture/2000/12/hitchens-200012?srsltid=AfmBOor767_0T4o2ZrcFoc3yTXYbGGLrWBWNjQW3a1wolW4FAR86x50R

The ultimate reason why people can get away with this shit is that the cause of Ayn Rand, philosopher is (surprise) extremely well-funded:

https://www.counterpunch.org/2012/02/27/ayn-rand-the-tea-partys-miscast-matriarch/

Rand actually wrote the screenplay for King Vidor’s The Fountainhead (1949), with Patricia Neal and Gary Cooper.

So ridiculous and overwrought, it’s hard to watch it without laughing. Beyond bad taste, Rand clearly had a “kitschy brain” as Thomas Bernhard would say.

I saw it in a large screening for architecture students, who jeered in derision and most decidedly did NOT find inspiration in Howard Roark.

Indeed, anybody who is persuaded by “Objectivist philosophy” is unworthy of further attention.

It had been rumored that F.L Wright thought The Fountainhead was junk but a recent book about Wright and his apprentices says that he actually liked it– although his wife thought it was junk. Wright had been approached to design the buildings for the movie backgrounds but that fell through.

The Wrights were high culture people and anything but “kitschy.”

Which wife? The first one, who lived with Wright’s and her two children in the house in Oak Park that Wright designed, was left behind for Mamah. the wife of a neighbor and friend. Before Wright could get a divorce and marry Mamah, she and her children by her first husband, were killed in a massacre at Taliesin when Wright was away. He did finally get a divorce and married another woman, Miriam, but she was addicted to morphine, and the marriage didn’t last. Finally, he hooked up with Olga, a Montenegrin by way of Russia. This relationship stuck, and Olga managed Wright and Taliesin until Wright’s death.

One of the pluses of living in Chicago is the access to all the Wright houses in Oak Park, Hyde Park and River Forest. The Wright Oak Park residence, with its huge playroom for the kids and dining room with the high-backed chairs that created an intimate setting, is open to visitors, as is the Prairie-style Robie House next to the U. of Chicago campus. A few hours drive to the north is Spring Green, WI, home of the God Almighty Lloyd-Joneses, Wright’s mother’s family, Taliesin and the Wright complex that includes a Prairie-style hotel designed by Wright students.

I would like to add that I gained some attention for being the person delegated by David Rockefeller and my immediate boss John Deaver to be the messenger telling Greenspan that he was fired from the project on the oil industry’s balance of payments back in 1965-66.

Deaver told me that he was sure that “the little bastard” had simply faked some numbers or used them incorrectly. It took me a day and a half to trace down what his problem was (depreciation of U.S. oil affiliates in Europe, applied wrongly to the U.S. parent companies).

But Deaver said that Greenspan was known for having such vindictiveness that he would take it out on Chase Manhattan Bank. Since I was low man on the totem pole (doing the actual statistics), I was told to go down the street to his office and explain. His assistant Lucille Wu kept saying, “It’s all implicit.’ But the comparison was like with unlike.

The end result was that on the day that Greenspan left, the BBC called me and asked me to come down to their studio to comment on Greenspan. At the top of their story for that day, they quoted me: “After me, the deluge.”

Bravo!

HUDSON HAWK STRIKES AGAIN!

IN THE BELLY OF THE ECONOMIC BEAST WITH THE EPSTEIN CLASS!

Amusingly, the partners at LTCM didn’t believe they could be wrong, so fiercely did they trust their models. Talk about blind faith.

Greenspan put six feet under. Take a number and join the micturition queue.

This is really mean but will dissevered.

it was way too easy for mere mortals to blow themselves up

thanks for the look behind the tranches….2008 jumped the us debt ledger on its way to oblivion

This is another good entry in a list of what I call “dipstick tests”: Quick but high reliability thought experiments that let you access a deep truth.

This sounds like an interesting story. In fact, banking IT in general seems to be littered with horror stories of one kind or another. The combination of 24/7 operations, frequently antiquated technology base, high stakes mission, and unforgiving customers, together with a rapidly changing and widespread organizational setting, makes me think of the class of power tools that frequently cut unwary operators’ body parts off. Stand clear!

I wonder if anyone has compiled a litany of banking IT disasters. Almost as entertaining sounding as a book of aircraft disasters.

File under AI and potential endless bank hacks. / ;)

From Breaking Points:

Mythos AI HACKED ENTIRE NSA In Hours, Top Intel Sen Says

https://www.youtube.com/watch?v=hD-UM8QzxV4

The NSA computer servers/files are maybe the most highly secured IT systems in the country.

The only maybe good bit of news is Malwarebytes flagged a lot of Mythos claims of security holes in computer systems as incorrect.

Oh, no no no. The O’Connor IT department was SUPER competent.

Thanks for posting this.

In the world I worked in for much of my career, large commercial aviation, the whole concept of “self-regulating” would work, but it would result in a world where poorly designed, built, and maintained aircraft would fall out of the air, unmanaged air routes and airports with daily collisions, and who knows what other havoc. Commercial aviation in America would pretty quickly fall apart. I’m not denying too much regulation can be a burden, but no regulation is pretty much insane.

I’m not a finance person, or a banker, but it would seem to to me that throwing out the hard learned wisdom on banking and finance from the Great Depression was not a wise action. Watching Greenspan and others deregulate and defend “self regulation” always struck me as a profound idiocy.

That is the implicit argument of libertarianism, if one is honest about what market signals will end up encompassing. If enough people get food poisoning, word gets out, and it’s more efficient than restaurant licensing and inspection. If enough planes fall out of the sky, if enough botched or unnecessary amputations occur–

The kernel of truth in this is that, in practice, regulations do serve entrenched interests, which is why those in power only ever push this very selectively.

If only he had stuck to jazz. He attended Juilliard, played clarinet and sax, and also with Stan Getz (among others).

Quincy Jones talked about it in a bio.

Greenspan was also a very good baseball player. He was the slugging first baseman on the Uptown Titans teenage sandlot team in NYC in the late 1930s. My father was the leadoff shortstop on the same team. Greenspan was a Dodgers fan and a cultured scholarly snob headed for the Ivy League, while my father was a Giants fan and a pool hall street thug who would have wound up in the Jewish mafia if WW2 hadn’t come along. Two very different kids, but they were friends from each end of the neighborhood double-play combination. My father said he was good enough to play pro.

A little over two decades later, Greenspan visited my family in Los Angeles when I was in utero. He was trying to recruit my father, then a young hustling businessman, into what my father could only describe as a cult, and which I figured out later must have been Objectivism. My father, an FDR Democrat, thought he was nuts and according to family legend, threw Greenspan out of our house and they never spoke again.

re: From the 2020 paper by Ferguson et al.

“On June 2, 1987, the worldwide guessing game came at last to an end: the White House announced that President Reagan would nominate Alan Greenspan to replace Paul Volcker as Chair of the Federal Reserve Board. Markets reacted with shock:”

And after that:

Springtime for Milken and junk bond kings.

Winter for Drexel Burnham Lambert ….. /;)

(Milken was pardoned by President Donald Trump in February 2020. )

One might say that Yves “wrote the book” in this area . . . but she did much more than that: she blogged about it with insight, wit, and authority. She made arcane material accessible and cut-through deliberate obfuscations to show how things really worked.

And she’s still at it!!

While Greenspan’s death is a reminder of how the financial system went off the rails, its a good time to remember the brave and dedicated people that had tried to prevent that train wreck and/or explain how it happened.

Note: Greenspan was warned about the housing bubble in June 2005.

I am familiar with all of this topic. It changed our entire world for the worst. Me personally also. I want to barf now.

Thank you Yves for the sacrifices you have made. Perhaps this learning will be used to rebuild or at least slow down losses into our final descent into hell.

For Greenspan and his ilk, this excerpt from Dorothy Parker’s Tombstones in Starlight

“III. The Very Rich Man

He’d have the best, and that was none too good;

No barrier could hold, before his terms.

He lies below, correct in cypress wood,

And entertains the most exclusive worms.”

A contemporary of Alan Greenspan was Pierre Rinfret.

This was pulled from the internet archive of Rinfret’s website of 2002:

https://web.archive.org/web/20021218051044/http://www.parida.com/ag.html

“One of the absolute lies about him is that he retired from his consulting business a wealthy man. Absolutely and totally untrue. When he closed down his economic consulting business to go on the Board of the Federal Reserve he did so because he had no clients left and the business was going under. We even went so far as to try and hire some of his former employees only to find out he had none for the 6 months prior to his closing. When he closed down he did not have a single client left on a retainer basis. His only source of income was his speech making. As a speaker he had to be the ultimate bore exceeded only by Paul McCracken about who Richard Nixon told me on many an occasion “When he talks MEDGO” meaning “my eyes doth glaze over”.”

So perhaps Greenspan entered the Federal Reserve job in poor financial shape. This could have influenced him to be reluctant to irritate the financial industry via regulation.

I had no idea. This is important. Thanks.

Another Greenspan fraud: he was criticized for not having a PhD in economics or anything adjacent, merely having been a highfalutin’ data analyst. Then suddenly there were claims he had actually gotten one, from NYU. But no one was allowed to see his dissertation!

Barrons did a piece on the Greenspan thesis, apparently the thesis WAS viewed by at least one person and there were/are two copies.

Here is a link: https://www.barrons.com/articles/SB120917419049046805

archive,ph found a full article snapshot for me.

The Barrons piece closes with

“Wachtel came to us after we reviewed Deception and Abuse at the Fed, a book in which Robert Auerbach, a University of Texas professor, asserts that the Greenspan Ph.D. is, de facto, an honorary degree. Wachtel says that the book wrongly impugns New York University’s reputation and that Auerbach’s accusations are “a flight of fancy.””

Here is Barry Ritholz’ take on the Barrons article:

https://ritholtz.com/2008/04/greenspans-long-lost-thesis/

“Barron’s Jim McTague had a chance to review one of only two existing copies of Greenspan’s 1977 NYU Doctoral thesis. Astonishingly, it focuses on Housing booms and busts.”

“Some highlights:

• A discussion of soaring housing prices and their effect on consumer spending;

• An anticipation of a bursting housing bubble. Greenspan even wrote: “There is no perpetual motion machine which generates an ever-rising path for the prices of homes.”

• A failure to anticipate a broader housing mania spilling into the general economy;

• Its doubtful anyone in 1977 could forsee the securitization process of subprime loans, including Greenspan. He did write, however, “a sharp break in prices of existing homes would pull down the prices of new homes to the level of construction costs or below, inducing a sharp contraction in building.”

• The thesis shows the future Fed boss was focused on housing early in his career. Barron’s notes this casts doubt on his assertions about being surprised by the impact of this decade’s housing mania.

• In the introduction to Greenspan’s thesis, he noted that homeowners were refinancing for larger amounts than their original mortgage, in essence monetizing increases in their home’s market value and spending the excess cash on goods and services. This broke new ground in 1977, as the economic models at the time were not tracking this source of income.”

Possibly the thesis contents were quietly suppressed by Greenspan, not because they were faulty, incorrect or indefensible, but because they demonstrated that Greenspan anticipated housing market problems in 1977, watched them unfold and did little in response when he was in a powerful position to do something.

Better to have a “who couda known?” public position.