Yves here. Some savvy investors were warning the single family home rental market was overheated nearly a year ago. Carrington, one of the early entrants, said it had pulled back last May, largely because “stupid money” had flooded the market.

In a recent post, readers confirmed that private equity investors are, not surprisingly, taking a very short-sighted posture towards their investments in single-family homes. It’s not uncommon for them to list well above-market rent rates and include unrealistically low levels of reinvestment in their projections. But sweating an asset works only if you’ve got an exit strategy. As we indicated, the cleanest and simplest one, that of doing an IPO of the operating company, appears to no longer be viable, thanks to the Fed’s taper. A few deals got launched, then one was pulled, as it seems the PE landlords can’t get the pricing they want via this route. Another that Wall Street was very keen to establish was that of securtizing the rental stream (a prospect your truly regards with horror, since if mortgage servicers were terrible, I shudder to think what the property management will be like in these deals). But with Blackstone’s first rental securitization showing a nearly 8% fall in rental income shortly after it was launched, the bloom may be off that rose as well.

By Wolf Richter, a San Francisco based executive, entrepreneur, start up specialist, and author, with extensive international work experience. Originally published at Testosterone Pit.

In real estate, national averages paper over the gritty details on the ground and are a crummy, often contradictory indicator as to what is happening in specific metro areas. When a new trend starts or when a reversal takes place in some locations, it’s watered down by data from other unaffected locations to form the overall averages. But even with this caveat, a national average suddenly sounded an alarm for the housing market: the smart money has started to bail out.

The smart money entered the housing market gingerly in 2011 then piled in helter-skelter over the next two years, gobbling up vacant single-family homes out of foreclosure. The forays were funded by Wall Street, awash in the Fed’s crazy-money. The smart-money operators trained their guns on specific markets, such as Phoenix and Las Vegas, and bought homes by the thousands that they tried to rent out. Then they spread their campaigns to other cities.

The tally has reached 200,000 single-family vacant homes for which they’re now trying to find tenants. In the process, mega-landlords have emerged. On top of the heap: Invitation Homes, a unit of private-equity giant Blackstone Group, and American Homes 4 Rent, a highly leveraged REIT that went public last August.

As in the heyday before the financial crisis, their smartest minds are now feverishly at work trying to figure out how to shuffle risks and future losses off to yield-desperate investors who’ve been driven to near-insanity by the Fed’s relentless repression of interest rates. So Blackstone and American Homes 4 Rent have started selling synthetic structured securities that are backed, not by mortgages, like the toxic waste before the financial crisis, but by something even classier, rental payments – based on the rickety hope that these single-family homes will stay rented out. Wall Street is already jubilating: the market for this type of synthetic monster is estimated to be $1.5 trillion [read…. The Exquisitely Reengineered Frankenstein Housing Monster].

But now the party appears to be running out of booze. This frantic institutional buying has driven up home prices – in some areas above the levels of the prior bubble. Trying to make money by buying these homes at inflated prices and renting them out into a tough job market where strung-out consumers with declining real wages have trouble making ends meet has become a precarious business model.

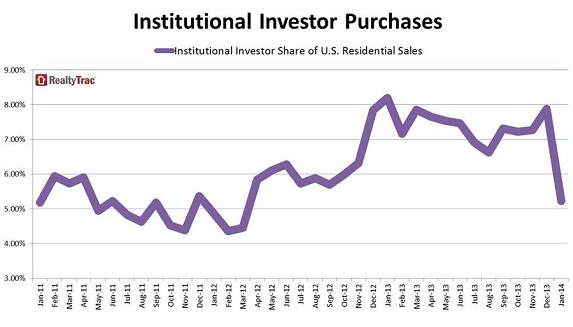

In some of the formerly hottest metro areas, purchases by large institutional investors – those having bought at least 10 properties over the past 12 months – plunged in January from a year ago, according to RealtyTrac’s Residential & Foreclosure Sales Report: in Jacksonville, Florida, by 21%; in Tampa, by 48%; in Tucson, 59%; Memphis, 64%; in Cape Coral-Fort Myers, Florida, by 70%!

Institutional purchases hit the skids in over three-quarters of the 101 metro areas that RealtyTrac analyzed, their share dropping to 5.2% overall, from 7.9% in December, and from 8.2% in January 2013. It was the lowest monthly share since March 2012, at the infancy of this whole bonanza.

But 23 of the 101 metro areas had year-over-year gains, some of them late starters. In Atlanta, institutional purchases rose 9% to where a quarter of all homes were purchased by institutional investors. That’s how the Fed has “fixed” the housing market. In Austin, the institutional share soared by a mind-boggling 162% to reach nearly a fifth of all purchases. In Denver, their share rose 21%, in Dallas 30%.

And in Cincinnati 83%. “Big hedge fund investors,” explained Michael Mahon, Executive Vice President at HER Realtors, which covers the area. “I think that’s contributing to the lower levels of inventory available on the market,” he added, seeing how these vacant homes have been pushed from the much scrutinized for-sale listings to the ignored for-rent listings.

“Many have anticipated that the large institutional investors backed by private equity would start winding down their purchases of homes to rent, and the January sales numbers provide early evidence this is happening,” said RealtyTrac VP Daren Blomquist. “It’s unlikely that this pullback in purchasing is weather-related given that there were increases in the institutional investor share of purchases in colder-weather markets such as Denver and Cincinnati, even while many warmer-weather markets in Florida and Arizona saw substantial decreases in the share of institutional investors from a year ago.”

So forget the by now ubiquitous all-encompassing polar-vortex explanation. Which begs the question: if not institutional investors, who the heck is going to buy these homes at these prices?

Existing homeowners who buy a home and sell their old home don’t count. They’re just swapping homes, not creating demand. But foreigners are buying in certain cities – Chinese and Argentine buyers and others who want to deposit their wealth while they still can in a reasonably safe place. So they’re creating demand.

But the most powerful economic force in the housing market, first-time buyers? Normally, they’d swarm all over these homes and create real and lasting demand and make the housing market grow. But prices have soared, and mortgage rates have crept up, and young people are teetering under piles of student loans, and so that economic force has collapsed to record low levels. Read…. Without Them, The Housing ‘Recovery’ Remains A Sham

These guys aren’t stupid. They realize that the easy money has already been made. Now that they’ve re-inflated the bubble in those previously busted markets, they’re looking for more stable returns in better areas, where they can find them of course. Explains why one PE firm was looking to buy 60 homes in Houston for rent-to-own and do the same in Dallas. I can only assume they are looking at Austin as well.

Two houses on my street that were empty for 3 years were bought by “investors” a month ago. Not only did they pay double what I thought the houses were worth, the new owner is putting $50K into each one to make them livable. I hope he can find another sucker to sell them to. Actually, I don’t, because if he gets what he wants for them, my property taxes will double (the Dallas County appraisal district must love this).

Keep an eye on the TX appraisal districts this year. My guess is they are going to jump on the mantra of higher (inflated) property values to generate revenue and put the screws to homeowners, while we continue to look for an equitable method to finance schools and corporate landowners lobby for more breaks on their high-value property.

I’ll be shocked if I don’t have to go to binding arbitration this year to get a fair assessment. Did it a few years ago and it was certainly an educational experience. Formulas for our local CAD were seriously flawed, and likely still are. Comparing recently built homes to 7-8 year old properties with higher depreciation, also failing to account for different utility value when homes don’t have the same number of bedrooms or bathrooms. Panel hearings with the review board are a joke because even if their data and comps are flawed it’s up to their discretion as to whether they want to consider your argument. You don’t get to ask questions of the board members because it’s all about speed and efficiency (i.e revenue generation). Accuracy is apparently an afterthought.

http://aaronlayman.com/2012/04/a-letter-to-the-fort-bend-central-appraisal-district-your-assessment-formulas-still-suck/

How dare you get up in arms over the prospect of higher valuations on homes owned by people who are not new buyers?! Don’t you know that here in CA the evil and despised Prop 13, which all good liberals know is responsible for all the ills of the universe, prevents such bubble-driven oppressive increases?

No, we must do away with Prop 13 so that Wall Street types can buy up homes at inflated prices, sell them at even more inflated prices, and dump the profits in their Credit Suisse offshore tax haven bank accounts while the average schmuck — who thinks his home is a place to live, raise a family, and retire — is stuck with the inflated property tax bills.

Yet it’s ok for me as a prospective first-time homebuyer to pay $15,000/year in property taxes while the people next door in the same size/quality of house pay $1,600/year? Prop 13 is evil and should be eliminated on both residential and commercial property. And don’t give me any crap about tossing grannies out of their homes. Even states like Oklahoma have systems to freeze property tax hikes when the owners turn 65 and such.

itheir smartest minds are now feverishly at work trying to figure out how to shuffle risks and future losses off to yield-desperate investors who’ve been driven to near-insanity by the Fed’s relentless repression of interest rates

I do not feel any kind of empathy for those “yield-desperate investors” and would argue whether the insanity relies on the Fed or on those thristy rent-seekers. I believe that Investing incentives haven’t been diverted to those finantial instruments by an insane Fed but, almost certainly, by the more insane Treasury Dpt. fiscal policy.

ZIRP is NOT your friend. It certainly is not my friend.

I own 35 units. I would like to own more because I have cash that I refuse to invest in the manipulated stock market. But, because property is now higher than my calculated economic value, I’ve not.

BTW … property management is not a way to get rich. It will cause the big guys big time problems.

Speaking of the hassles of property management, my guess is, if you own 35 units, and even if you have your own cadre of tradesmen, you are probably working about 75 hours a week! Something always needs to be handled, and handled now.

Those desperate investors can be pension plans…. if pension plans get a raw deal, then pensions get cut.

Or individual savers who used to be able to put a few dollars away each month and earn compounding interest.

You know, that making money with money thing. The individual’s ability to use their own money to make a little “unearned” income was the first thing to get squashed.

Of course. Can’t have the sheeple saving when they should be spending.

My impression is that many of the investors in the past few years are looking for long-term investments in RE rather than bonds and, as someone said upstream, the manipulated stock market. RE may go up and down over the next few years but, long-term, it should rise according to this thinking. The international oligarchs believe that RE may well be the only safe investment there is at this time. Money has to go somewhere.

“Money has to go somewhere.” Unless it was never real in the first place. Hence deflation in the market. Pensions, 401k’s, all of these things aren’t real. It’s not like you have tangible things to hold onto unless you cash out early in the game. All ponzi schemes under another name.

Single family real estate is a speculation, not an investment. You need reliable tenants, one at a time, and they are very difficult to identify, harder to replace and harder still to evict if that becomes necessary. Meanwhile, taxes and maintenance hammer you, and you risk adverse changes in the surrounding houses, employment conditions in the community, all of which is impossible to control or even to predict.

Good summary! Add “insurance and major expenses” to taxes and maintenance. If you have just 10 houses, you have to replace a roof on average every three years.

Regardless of the sanity (or not) of current pension fund imperatives, it was chasing after yield that brought us all down. It wasn’t Condi Rice’s mushroom cloud of atomic radiation – it was a mushroom cloud of ever expanding profits seeking ever expanding yields. I haven’t read anything about real estate as an asset for some time, but it’s pretty clear that no asset is safe these days; nor is saved money, nor is a job. So in this environment, speculating on real estate for a return based on rents is nuts. The only thing it will yield is a lot of tax deductions and losses, so maybe that is the goal. And in the meantime it does seem that decisions have been made to prevent our recent “financialism” from happening again and it looks like keeping interest rates ultra low is the way they plan to achieve a new stability. Which is a relief. Since money is a political invention and should never have anything but a very low interest rate attached to it. Pension funds could always change their charters and allow pension money to be used in productive social ways, student loans, cheap mortgages, various projects without middle money management taking a cut. And the pension funds could then also benefit from all those great tax subsidies, credits, write-offs. What a big tax-mess monster. I wonder how much pension money has been diverted to the military over the last two decades.

You can’t have the entire population making more than GDP growth on their retirement portfolio.

The biggest delusion was that pensions can be funded when you have a bulge in the population and the living standards of that bulge are higher than that of their parents.

If we had stuck to pay-as-you-go pensions and the funding had come from taxes, people wold have stayed lucid. Instead, we opted for money printing, lower taxes, deficits and now we have no idea who is worth what.

Bravo!

I don’t think you would approve of “ultra low interest rates” if you were seventy years old, had worked a lifetime and saved your money, expecting to enjoy a reasonable, safe return on it. I think you would feel you are being robbed, and you would be right.

ZIRP hasn’t stabilized anything. It has simply disguised a legion of insolvent banks and allowed those controlling them to continue looting them. It has prevented the liquidation of debt that is required for the economy to restart. It continues to enforce perpetual servitude on credit card and student loan debtors, and to prop up all the scoundrels responsible for the economic mess we are in. And it is destroying the lives of millions of small savers long past possibility of reemployment.

Bottom line: ZIRP is class warfare and nothing else.

Thank you! Right on target!

From a retired 84 year old……..

It begs the question, why should one expect a good return on their money without working for it? Doesn’t that just fall into the rentier mentality? A few can get a free lunch but not an entire nation of 300M.

Why should treasuries get you good returns if the whole population is expecting others to work and make them rich and no one wants to pay taxes? Why should treasuries offer good returns if the government is not investing properly? After decades of malinvestment, how can one even expect good returns on government securities? We are reaping what was sowed!

While one is working, one should be preparing for old age. That means making sure one has a roof over one’s head until the day one dies… one could make sure their house is paid off and well maintained for retirement. In a perfect world, during working years, one could stockpile stuff that will be needed to maintain that home over 20-30 years. One could stock up on food and medicine. The perfect hedge would be to stock up on everything one will need one’s old age.

But for obvious, that is not possible so one invests. You’d think that logically, one would at least invest in institutions that offer services and stuff one will need in one’s old age. But that is not what happened…

Too much money was spent on the military so American materialism and consumerism could continue. Too much money was invested in real estate which depreciates and needs maintenance. Too much money was invested in cars that end up in the dump. Too much money was spent on making the system bigger instead of maintaining it properly.

One of the problem is that people have become completely disconnected from the true value of money. The discrepancy between what boomers invested in and where their money was spent is proof of that disconnect. What is telling is the number of older people who believe they are entitled to good returns when we are surrounded by gross mismanagement whihc was not created by the under 18 crowd.

Over the last few decades, people in the Western World have become completely disconnected from the natural laws on this planet. The truth is that if you need food, you don’t bake bricks

People need to think about what investing truly means.

It’s a delusion to think that higher rates would save retirees. Decades of malinvestment and the boomer bulge guarantee that if rates on treasuries go up, some other benefit will get cut.

Rien ne se perd, rien ne se crée.

Most articles on this issue have the flavor that the big Private Equity outfits that are buying up these houses are out there on their own. Nothing could be farther from the truth. It is clear that this is all part of the Fed’s/Treasuries/POTUS plan to re-inflate the housing sector; PARTICULARLY in cities/areas that saw huge price drops. So PEs were brought in; given assurances of bailout, etc. if things don’t quite work out. Right now, I loos like their ability to offload this stuff into securitized products isn’t finding the appropriate number of suckers…..but that doesn’t mean they won’t get bailed out. Likewise, we know the big holders of troubled properties were told/and agreed to hold those off the market sometime around 2011. That was actually a smart move by Geithner (assumed) because all those properties were the cause of the big price drops.

So the plan is/was to re-inflate to get many other folks out from being underwater. It was done by shutting off inventory and getting PEs to buy up under the “framework” of owning to rent. These PEs aren’t that stupid!! I own rental property and folks, it’s real work And you don’t get rich. Just a nice cash flow with ups and downs.

It will however, be interesting to see what happens next in all this mess. The PEs can and will sit on this stuff but as QE continues to wind down the real economy will reappear as we know and we’ll be back in recession or worse.

Mike – “It is clear that this is all part of the Fed’s/Treasuries/POTUS plan to re-inflate the housing sector; PARTICULARLY in cities/areas that saw huge price drops. So PEs were brought in…”

Totally agree with your synopsis. That’s exactly what’s happened. PE’s were brought in to snap up cheap properties, which increased demand, raising home prices. A ton of inventory was held off market (decreased supply), keeping prices from falling. Interest rates were hammered down. It’s all been a concerted effort.

More free market (ha) engineering by the Finazis!

Mike, you see it all but the therefore. There isn’t going to be any wind down of QE. Not now, not ever. What there will be, ultimately, is a stock market crash, because sooner or later something will happen to frighten the lenders and stop renewal of those overnight loans on which speculators rely. Nobody knows what will happen or when, but this fantasy market cannot last forever, QE or no QE.r

Duh-uh! What else is new?! When any bubble bursts, “because ‘stupid money’ had flooded the market” the smart money buys low. Then they sell high when the money floods the market again. This worm has turned at least half a dozen times in my lifetime. I’m sure it’s more. The smart money sold high twice: once at the beginning and once at the end of the Bush Administration alone.

Moses saw that making money from money or from real estate was tantamount to perpetual motion. That’s why he banned usury, rent and selling land forever. . . . When will we catch on that the FIRE must concentrate wealth and burn out the economy, because it is a mathematical certainty that one can’t make something from nothing. No work. No gain. Non productive activity produces nothing but a drain on real material economy.

There is a very big issue with investing in RE for the long term. The methods, materials and workmanship on many homes built since the 80’s are not equal to much of the housing stock built before then. After spending a couple decades in the construction business my guess is that a significant number of newer homes will experience failure that can not be cost effectively repaired. The result of poor quality housing is the projected useful life of a newer house will be much shorter than that of former housing stock.

In much of the country I would agree with you. Here in CA it’s a little different, mainly (entirely?) due to the constant improvement of our state building codes in an effort to minimize the loss of life and property damage from our inevitable periodic earthquakes. My current home was built in 1971. The newer ones which have been built over the ensuing years are far superior in every respect except one: mine was one of the last built with real plaster walls instead of drywall. (Real plaster is a personal aesthetic favorite of mine but probably doesn’t matter to most other people.)

But everything else? Much better.

Foundation footings are deeper and wider, with steel I-beam posts required on all four corners (and sometimes at strategic locations in between) on all multi-story homes. Steel I-beams are also used across the garage opening, the wall separating the garage from the main area of the house, and on the back wall of the living area. Sides and ends of the homes are sheathed in 5/8″ or 3/4″ MDSB shear panels and then those panels are connected to each other laterally and vertically by nailed-on 4′ lengths of steel strapping. Roofs are also sheathed with MDSB. Before the exterior wall covering (stucco, siding, masonry, whatever) is applied all the surfaces are covered with TyVek waterproof membrane to keep out moisture.

A few things that I don’t like (again, personal preference) and which might lead to the problems you suggest, are the use of PVC and ABS plastic pipes as well as Romex with plastic electrical boxes instead of traditional electrical conduit and metal boxes. However, even I believe that this stuff will continue to function as intended for 40-50 years.

But in much of the rest of the country, including AZ, NV, FL and similar areas, new construction does not have the quality of stuff built “back when”.

Here in North Carolina, the houses are worse than the cars coming out of Detroit. Everything falls apart in twenty years, in houses selling for $500,000!

Code proliferation is a mixed bag (perhaps less so in CA). It ensures more energy efficient houses, as well as any number of other benefits that come when the house is built. But it can do so at the expense of long lasting materials, or at the level of cost per square foot or both. Home buyers that are well off end up getting most of the benefits and those that are average or right on the margin end up paying for it.

Moreover, homeowners and smaller contractors who want to “legally” work on their own or others homes (renovations, additions, moderate to large repairs) – old or new – end up paying due to exploding complexity in meeting and understanding code requirements. Many renovations are simply going beyond the scope of the average homeowner to do and are becoming harder and harder to make a living on for the small contractor. This is, of course, not an accident or unintended casualty of the proliferation process.

That said, many of these code changes and additions are real improvements and do add lasting value to the buildings somewhat regardless of price category. I’m frankly amazed, for instance, that some of the “matchbox” houses built in the 50’s have lasted as long as they did. They might not last a whole lot longer today than then, if you could get them, but they would remain tighter, more comfortable and safer for a much longer period.

This is just going to create a new round of underwater “homeowners” when the property market resumes its date with reality. Another round of bailouts, then good bye any semblance of the last 40 years.

Which begs the question: if not institutional investors, who the heck is going to buy these homes at these prices?

No one with any common sense. For potential buyers in those markets, sitting it out and watching as the local real estate market gets crapified would be a smart money move.

When manufacturing was being outsourced, lowering prices of imported goods, no less a light than Bernanke crowed about how this was keeping inflation down and was a good thing. A lot of people suffered for that good thing.

Apparently Bernanke is schizophrenic, because according to him and a whole host of economists, lower house prices are a bad thing.

Economists might think differently if they lost their jobs to outsourcing or were fired for no reason at all, and tried to make their living producing something a willing customer wanted to buy.

I fail to see how applying a torque wrench to the financial system so things get “better” by boosting asset prices and destroying little people is beneficial to anyone, including the plutocrats. Eventually there will be a snap back.

I do mapping of foreclosures in Memphis. Please take a look and see what has happened to my community.

http://polardonkey.blogspot.com/2013/07/in-memphis-foreclosurewealth.html

Also take a look at this post. It shows the assessed value of every single family residential home in Memphis & Shelby County. http://polardonkey.blogspot.com/2013/09/take-drive-around-county-judge-mays.html

White people in Memphis & Shelby County complain about political polarization, but how can you not have political polarization when you have such levels of racial and economic polarization? Memphis is a testing lab for neoliberal policies. Massive government giveaways to corporations, Blue Crush law enforcement tactics (we exported it to LA. Have fun with that), privatizing the schools in poor black areas but creating separate “public” school systems in white, wealthier areas, and a general belief that government really shouldn’t do much for the community. The government has become predatory. We have a police force with one of the highest rates of indictment of officers. Code Enforcement, which is supposed to help mitigate some of the problems associated with foreclosures, actually was running schemes to enrich themselves. (Kickbacks to managers for contracts to demolish houses. Using code officers to find empty houses to strip or seize themselves and sell. Plus, several other money making schemes. The only reason these schemes got discovered is because the foreclosure crisis reached such a scale that they couldn’t keep a low profile on their activities and clean code officers felt uncomfortable with the level of corruption.

The foreclosure crisis in cities like Memphis, create a whole eco-system unto themselves. It is like the jungle. At the top of the food chain are lions, which are banks. Next you have servicers who are the hyenas. Then come your code enforcement jackals followed by the government contractor vultures. If code enforcement corruption was happening in Memphis at this large a scale, it is happening in other cities. Too much money is to made off the scraps from lions and hyenas. The local government bureaucrats see all these outside forces stripping their community of wealth, may as well get in the game before it is all gone. This is what government devolution looks like in America. Pay attention to the backwater areas like Memphis because our problems will soon become your problems.

Memphis- Where the government goal of keeping the shit at shoe level is just too high a standard.

Great comment! This is really helpful to those of us interested in the lay of the land. The USA is the land of the hustle but at this time it has no limit. This mentality has become international in scope and will reach your community fairly quickly. This is all a feature of globalization. i.e., there is only one value that trumps all others–money!

Thanks for the Memphis comment. Here in California in the last week the respect for police has collapsed (that happens eons ago in L.A. and I was in an uneasy alliance with them to get rid of the gangs in a neighborhood. Horrifying experience.) We’ve got cops seizing cars of undocumented people and selling them in t the San Joaquin Valley, in San Diego the police chief just resigned due to his officers forcing sex on arresstees (or non-arrestees, as that played out.) Of course the beating to death of a compliant homeless man in Fullerton. Today in San Francisco five officers arresting for stealing, selling drugs. 20 deputies Los Angeles Country beating the hell out of inmates, etc, and all having been hired with police records. L.A. cops shooting up two old ladies and a white surfer in L.A. while the cops lived in white terror of a burly black police officer who had gone nuts.. (I always say – their experience for those three days while they sought Dorner is what the rest of us experience and fear at their hands every day. That they will go apeshit over something and kill you or stomp you to death while you are in handcuffs (as a female officer did to a restrained woman suspect. She stomped on the woman’s private parts, the woman died of her injuries, and the cop was exonerated..

All this reminds me of the great Onion headline, i paraphrase ” Los Angeles citizens terrified as LAPD resumes normal patrols” after going crazy over the rogue cop.

Our Planning Department and Code enforcement is absolutely criminal – I lost a building because they “didn’t like” my licensed engineer architect. Another friend of mine, same situation, the same plan check “did not like” the same licensed engineer. He lost his building too. Oddly, another code enforcement worker owned a contiguous property and had been trying to buy my friend’s property at a distress discount. Probably just a coincidence.

I stay off the local community boards (like Yahoo Community) because after I repeatedly warned the new yuppies in our neighborhood who kept mistaking code enforcement for a friend (as in, I’ll call them to find out code on my planned project) I got seriously hacked from an email from someone in the group that unleashed holy hell on my email, which meant I could never enter it again. (Sadly, the last email from friend who died suddenly was in there. Lost to history.)

As everyone knows here I have been fighting with banks for years. I even got cited for criminal neglect by the City while the bank had a receiver on the building – and thus I was barred from the property. I had to go to criminal court to face charges that should have been filed against the bank. But, of course, were not, and never were going to be.

Yes, it’s a brave new world out there. It takes the constitution of an ox to face down these fuckers, but one must try.

I have always thought of corruption as the fish rotting from the head, but I’ve assumed that in the United States, the rot has not reached the tail. I see I am wrong.

Speculation is just casino gambling without the cocktail waitresses.

The Case Schiller Index was 100 in 1897 and 110 in 1997. There were a lot of wobbles, bumps and crashes in the interim, but the long game gave 0.1% annually. I would wager that from its high of 220 it will go back to 110 or something near that.

Some historians did a study of home prices in the Netherlands over 400 years (great record keeping!) and found a similar 0.1% return.

So it’s all about timing the stupid money. Soros did that in the currency markets. Looks as if the big firms have too much hysteresis in their feedback loops to do it effectively, but then they have our tax dollars to make them whole. Up to a point.

And yes, most of these homes are fast-depreciating crap, made worse by absentee landlords milking the asset. That’s aside from the fact that most of these homes are in car-commute suburbs, adding what might be called “balloon depreciation” when oil pops up again.

Between stories from my parents and grandparents and a time living in Detroit, I pieced together the following, all in current (not real) dollars:

My grandparents bought their house in NW Detroit in 1930 or 31 out of foreclosure from the person who either built it or bought it new for about 25K. They sold it when they retired to CA in 1960 (more retirement than early white flight but timing is the same) for about 30K. I noticed it was sold sometime when I lived there in the early 90s for about 30K. And if you go on Zillow right now, homes in the hood (that appear lived in) are going for … 30K.

On the other hand, if you are looking for quality-built, willing to do a little digging and willing to live on a block that is 50-75% inhabited, Detroit is your place.

Help!

I need assistance in understanding something and feedback as to whether or not this is also part of what is going on.

It’s well-documented that I am no Ocwen fan. But I’ve been wondering if Ocwen and its Ocwiterations were sorta “chumps” for the banks who needed to offload these NPLs in order to comply with Basel–which in turn would have left them not clearing the hurdle for the new Fed stress testing under Dodd-Frank.

Deutsche via OneWest off-loaded their IndyMac dreck on to Ocwen in Q-4 of last year. I want to know if Deutsche financed the deal for Ocwen. (“I will gladly pay you $500 today to eat this e-coli-ridden hamburger that the health inspectors are coming to look at on Tuesday….”) (?)

http://stream.wsj.com/story/markets/SS-2-5/SS-2-463708/

“….Under the Fed’s new rules, foreign banks with U.S. assets greater than $50 billion will have to maintain more loss-absorbing capital and hold a minimum 4% of total assets in equity capital. Analysts have said that Deutsche Bank is the foreign bank most affected by the rule. According to Citigroup analysts, Deutsche Bank could face a capital shortfall of roughly $7 billion under the new rules…..”

So….does anyone here think that Deutsche Bank will have trouble passing the stress tests? And when are the stress tests, btw? Does the FED have to wait for a stress to take any action–e.g. if the FED saw trouble ahead, could the FED swoop in and stress test it earlier than scheduled?

Anyone? :-)

The question that interests me is: how will the inevitable bailout play out?

How does this buy low/sell lower play parlay into a net wealth transfer into PE firms?

I do find it hard to believe these firms were caught unawares out on a limb by a change in policy and predictable default rates which killed their chances at IPOs and securitization, which leads me to believe I am not watching the correct hand during the magic trick.

And I have to start wondering if Ocwen should be considered a SIFI (A Systemically Important Financial Institution.) It’s apparently not, as of now, on the SIFI list, but should it be?

And if it is a SIFI and if it were to go under–how in the world would that work?

http://www.sfgate.com/business/bloomberg/article/Billionaire-Erbey-Fails-to-Halt-Ocwen-Slide-on-5273073.php

CEO Erbey is physically domiciled in St. Croix now. How do we get the fleet of black Suburbans and men in dark suits and sunglasses over to The Virgin Islands on a Friday afternoon?

I’m not suggesting that Ocwen would truly fail–but being that it is so interwoven with such a huge portion of our real estate now, which is definitely tied to our economy–shouldn’t we have a plan in place in case it does go “erp-rattle-klonk”?

I sorta understand why we might not have such a plan–I don’t think anyone really expected them to be such big players so suddenly. But–maybe it’s time that we–the regular ole people–start asking if there is such a plan. Maybe?

Banking [usury] is pure evil.

What these financial wizards have done to housing in the Western world should earn them a trip back to the Hell that hatched these despicable vermin.

Did anyone catch this snippet in the Bloomberg article today about foreclosures in NY/NJ? http://www.bloomberg.com/news/2014-02-26/foreclosures-climaxing-in-new-york-new-jersey-market-mortgages.html

“Newark, the state’s most populous city, and nearby Irvington are considering plans to use government power to seize underwater mortgages to help homeowners reduce debt and avoid foreclosure. The cities are researching a program that would offer fair-market value for the loans and reissue them to homeowners who can afford to keep making payments at the lowered amount. Many largely black and Hispanic communities in New Jersey and elsewhere were targeted for predatory loans during the boom, said Linda E. Fisher, law professor at Seton Hall University, who is helping the cities research the eminent domain proposal.”

I’m not well-versed in these issues, but this seems shockingly unethical to me. Being underwater doesn’t mean you’re going to default on your mortgage or that you can’t afford it–just means you owe more than it’s worth currently. You could very well be making enough money to support it….but this proposal would mean that even if that’s the case, the city can seize your house and “reissue” it to someone else.

This reminds me of that scene from Upton Sinclair’s classic novel “The Jungle” where the family can’t pay their mortgage to the bank and comes home one day to find that their precious home had been repainted and rented out to another family, already living there, who could make the payment.

Are they seizing the mortgages or seizing the houses?

The devil, of course, is in the details, but it could be something like this plan in Richmond CA, which looks like a good thing for homeowners. http://www.thenation.com/article/175244/rescue-local-economies-cities-seize-underwater-mortgages-through-eminent-domain

This could be the only sensible solution to these underwater mortgages. You can bet the bankers will do everything possible to prevent it, calling in favors from the stooge legislators on their payroll. And the local governments need financing, which will undermine more than token gestures in this direction. They are utterly dependent on Wall Street. Will they be selling tax exempt bonds door to door? I don’t think so.

Why? These people were not going to socialize the gains on their houses if they kept going up so why do they get to socialize the losses? The houses should be foreclosed upon and sold to those of us who have been patiently waiting and saving money to buy our first house. The foreclosed-upon family could rent for 7 years and then buy again. That is the sensible and fair thing to do.

I’ll believe it when I see it. A lot of similar schemes were proposed one year, two and then three after the bubble burst and I never heard of a single one coming to anything. The banks are indeed powerful.

What I don’t understand is how investors get sucked into these things. I mean didn’t they just loose their shirts with the securitized mortgage fiasco? Is this some sort of abuse syndrome?

Like more and better dems?

The radical plan on property would be to put it into public management at low rent related to earnings and maintenance costs in a plan similar to bail-in. We could do this to prevent people losing homes. This would bring down prices. Those affected by this could have some fair proportion of their mortgages written-off.

We need some really different thinking, based on how Europe and Japan rose from the ashes left after WW2. Why can’t we do something similar from a higher base start? The above might stiff the investment weasels, but who should care? It’s time to modularise the economy, get hot money out of basics and start allocating capital where we think it might matter.

Let’s not forget the ever increasing property taxes, in PA, many vacant homes will remain vacant…who can afford property taxes that eclipse your mortgage payment. 2300 sf home $6,500/yr. 1200 sf shoebox home $3,700/yr.

When will it end?