By Lambert Strether of Corrente.

And we are here as on a darkling plain

Swept with confused alarms of struggle and flight,

Where ignorant armies clash by night. –Matthew Arnold, Dover Beach

Another Obama Open Enrollment period has closed, and of course you know that if the results were good, there’d be parades, dancing in the streets, happy enrollees brought to the White House, etc. None of that. What actually happened: Exchange enrollment remained more or less flat and the exchanges are still not actuarially sound. Medicaid, however, is a success story, at least by the side of the exchanges. On the bright side many reports were generated, by consultants, pollsters, marketers, IT people, strategists, and think tanks, so you can see that ObamaCare — by world standards, the F-35 of health care systems — is doing some people some good. In fact, a lot of good. Ya know, for years I’ve deployed the old saw that “You can’t buff a turd.” What ObamaCare proves is that you can; it’s just very lucrative expensive to do so. And if you’re looking for a picture of what Clintonian pragmatism would look and feel like in practice — “you change the way systems operate” — then slowly and expensively buffing a turd is as good an image as any.

So first I’ll look at the Open Enrollment outcome on the exchanges and take a quick detour through the largest state exchange, Covered California. Then I’ll look at Medicaid, and conclude.

The Exchanges’ Slow Death Spiral

The first thing to realize is that the administration and the CBO together lowered the baseline for ObamaCare enrollment, not modestly, but drastically. The New York Times:

When the Affordable Care Act was drafted, the Congressional Budget Office expected people to sign up quickly for new health insurance.

Now, two years into the law, it’s clear that progress is going to be slower. The Obama administration acknowledged as much in late 2014, and again in October, when it presented its own modest predictions. Monday, the budget office also agreed, slashing its 2016 estimate by close to 40 percent.

The Obamacare marketplaces have helped millions of Americans get health insurance, but they have not caused the kind of immediate and drastic plunge in the ranks of the uninsured that analysts had hoped for before the law was passed. It has proved harder to spread the word about new health insurance, and harder yet to persuade people to shell out money for new health insurance they hadn’t had in their household budgets.

(Oh, my. “Harder to shell out money.” Class privilege at the Times? Could it be?) Anyhow, you’d think that slashing projections by 40% would be worth a bit more notice from our somnolent press, and even some murmurs about accountability and performance from those in charge of the program, but these are Democrats. There will no more be accountability for this debacle then there was for ObamaCare website launch debacle.

Anyhow, given slashed projections with some heavy-duty expectations management larded on top, the administration is now claiming success, nothing to worry about, gotta keep pluggin’ away, gotta keep buffin’ the turd…. Anyhow, I can’t bear to quote them, so I’ll just give you the numbers. USA Today:

In 2010, the non-partisan

Rand Corporation estimated 27 million people would have exchange policies this year and theCongressional Budget Office at that time was estimating 21 million for 2016. CBO even said last June that 20 million people would have plans purchased on the exchanges this year. Just 12.7 million signed up for plans, however, by the end of open enrollment Jan. 31 and about 1 million people are expected to drop their plans — or be dropped when they don’t pay their premiums.

Worse, enrollment growth seems to be levelling off. Gallup (ka-ching):

The sharp drop in the uninsured rate seen in the first year after the insurance exchanges opened has leveled off in the second year, with smaller declines seen in 2015 compared with 2014. This validates concerns that similarly large reductions may not be possible in the future because the remaining uninsured are harder to reach or less inclined to become insured more generally. Future reductions will likely require significant outreach and expanded programs targeting those who have not yet taken advantage of the health insurance marketplace.[1]

Even worse — and why I quoted Arnold on “ignorant armies” — we don’t really know why enrollment is so bad[2]. From USA Today once more:

Reasons why supporters say enrollment is lower than the original projections include:

• The process hasn’t completely recovered from the disastrous rollout of the federal Healthcare.gov website in the fall of 2013, says Matthew Buettgens, a senior research associate with the Urban Institute.

Let me break out my calculator…. 2016 – 2013… Three years on? Really? Can I get that research associate job?

• CBO expected a lot more employers to drop their plans and send workers to the exchanges for their coverage, notes Katherine Hempstead, director of the insurance coverage team at the Robert Wood Johnson Foundation. That hasn’t happened, however.

So maybe employer-based health insurance, bad though it is, is still a competive advantage over “sending” workers to ObamaCare?

• CBO also thought more people who didn’t get subsidies would still buy on the exchanges, but several million are believed to buy direct from insurers or brokers. While that affects the overall enrollment numbers for the exchanges, Hempstead says, it also means these people are still getting better plans with ACA’s protections, including a prohibition against discriminating with preexisting conditions.

I’m glad these people have health insurance, but we’re still in ignorant armies territory. “Are believed to”? We don’t know?[3]

Of course, for many, ObamaCare is a bad deal, but that simple fact doesn’t figure at all on the supporters’ list of reasons. Odd.

So, who are the eligible potential enrollees who are not buying ObamaCare? As it turns out, those who get smaller subsidies, or none. From the Robert Wood Johnson Foundation (ka-ching):

We find that across all states using HealthCare.gov, plan selection rates among the tax credit eligible population declined with higher incomes, ranging from a median rate of 62 percent for incomes below 200 percent of the federal poverty line (FPL), 29 percent for those with incomes between 200 and 300 percent FPL, to only 13 percent for those with incomes between 300 and 400 percent FPL. The consistency across states in the estimated plan selection rates within these income groups indicates much lower willingness of eligible people to pay for health coverage with the ACA’s tax credits among those with incomes above 200 percent and particularly above 300 percent of the FPL. The limits of this willingness to pay could make increases in future enrollment difficult to achieve without policy changes to improve affordability. .

This may pose challenges for efforts to increase marketplace enrollment in the future, though the rising penalties may make more uninsured willing to pay the going prices for marketplace coverage

(The mandate screws will tighten until morale improves.) The RWJF foundation cheerfully allows us to remain ignorant of why these less impoverished people behave as they do, but I’m guessing that a little margin makes it easier to gut it out and avoid being forced into a bad deal. That’s if they can afford a plan at all. From Health Care Policy and Marketplace Review:

But if you are solidly in the working and middle-class in this country individual health insurance on the state and federal exchanges is anything but affordable.

That is why the Urban Institute found that more than 80% of those earning between 100% and 150% of the federal poverty level (FPL)–the poor–signed up for Obamacare coverage in 2015 but only about 30% of those earning between 200% and 300% of the FPL signed up. Even worse, only about 14% of those earning between 300% and 400% of the FPL signed up in 2015.

According to HealthCare.gov, a family of four living in Roanoke Virginia, with mom and dad age-40, and making $60,000 a year would have to pay $415 a month, or $4,980 a year for the second lowest cost Silver plan, a plan from Optima Health. That plan has a $5,000 deductible:

But, if this family bought the lowest cost Silver Plan available to them in Roanoke Virginia the premium would be $394 a year and they’d have a $4,400 deductible. The lowest cost Bronze plan would have a premium of only $186 a month for the family of four––but would have a deductible of $12,900 for both the individual and the family.

So, just where is a family making this kind of income supposed to find an extra $5,000 a year in income to buy a plan with a $5,000 deductible on top of that. Or, why would they even pay $186 a month for a plan with a $12,900 deductible?

Note finally that this failure — for whatever reason — to enroll the unsubsidized has very bad actuarial effects. From Health Care Policy and Marketplace Review again:

Way too much emphasis is put on this age 18-to-35 statistic. Yes, they are more often healthy but under Obamacare the youngest pay one-third the premium of the oldest. We really need the healthy to sign up in much bigger numbers, that have so far been holding out, more than we need the young.

This is the great untold-story. About half of the individual market doesn’t qualify for a subsidy. We already know the take-up rate for subsidized population in the 300% of the federal poverty level to 400% of the federal poverty level is dismal. Those who get no subsidy are really taking these higher premiums and deductibles on the chin.

In other words, poverty is bad for you. The subsidy-eligible, then, are more likely, on the whole and on the average, to require insurance company payouts. If there were more people in the risk pool at three or four times the FPL, the insurance companies would be more likely to make a profit. But that’s not happening. Ergo, actuarial death spiral (absent more subsidies, of course. Ka-ching.)

Jeffrey Young of HuffPo sums up the darkling plain of ignorance of policy-making elites quite well:

Year three of Obamacare enrollment promises to bring only incremental changes from year two, and little in the way of firm answers to lingering questions. The uninsured rate is about the same, the sign-up numbers are about the same, the polling numbers are about the same, and the worries about this new market are about the same.

In a sense, all of these numbers do little more than confirm the unsatisfying truth that the health insurance exchanges will be works in progress for years.

The fundamental questions are the same as they were in the fall of 2013 (except that the websites work now). Will the premiums be affordable? Will people sign up? Will enough of them be healthy to offset to costs of the sick and create a stable system? Will the uninsured learn that subsidies are available to make coverage more affordable and take advantage of them? Will health insurance companies make enough profit to keep them in the market?

When the current open enrollment period winds down, don’t expect the final results to tell you much more than you already know. Sign-ups start again in the fall.

[Gag. Spew.] Then again, it’s not like there are people suffering and dying for lack of heatlh care. Oh, wait…

The Covered California Exchange

I want to take this pleasant little side trip through Covered California, primarily to show this User Experience video, which shows that after three years of work and half a billion dollars, the Covered California website still s— is still farcically bad:

This video was part of a larger report (ka-ching) by the California Health Care Foundation. Here’s their conclussion:

User experience research findings suggest that many consumers seeking to enroll or renew their coverage online with Covered California may have experienced similar problems. In general, study participants were experienced website users and did not have complex enrollment or renewal circumstances. The study outcomes were, in large part, the result of problems with the website and online application. Many of the difficulties that participants experienced have fairly straightforward and simple solutions. While consumers can enroll in Covered California offline, in person, by phone, or by mail, providing consumers with a user-friendly and efficient online experience should be a top priority. In fact, for millenials, one of Covered California’s key target populations, it is crucial. However, after three years, consumer user testing continues to show that consumers are experiencing significant difficulty enrolling or renewing Covered California health insurance online. This report points to improvements Covered California should make so that consumers can have the first-rate online experience they expect and deserve when purchasing health insurance.

(Remember, it’s the Democrats running the show here; they’re supposed to be competent at governing.) Oh, and California enrollment numbers are plateauing too. San Jose Mercury News:

With Covered California’s announcement Wednesday that 1.57 million Californians selected health plans during its third open enrollment period, at least one health care expert believes that the nation’s bellwether state in implementing the Affordable Care Act is now essentially running in place.

Although the latest numbers don’t say how many people have paid for their plan to complete their enrollment — the only figure that really counts and which will be available in a few months — some experts say that the net gain from last year’s 1.3 million total could be minimal.

Roughly one of 10 people who sign up for an exchange plan don’t complete their enrollment. So Covered California’s projected total for the latest enrollment period could easily wind up around 1.4 million — about 100,000 more than last year.

Medicaid’s Partial Success

From the failures of the ObamaCare exchanges, we turn to the relative success of ObamaCare’s Medicaid expansion, both in terms of enrollment and in health insurance company profit. From Health Affairs:

CMS released its November 2015 Medicaid and CHIP enrollment report. Medicaid and CHIP enrollment as of the last day of the November 2015 reporting period stood at 70.8 million, including 29.3 million children. Medicaid enrollment has increased by 14.1 million since October 2013 for the 48 states reporting both 2013 and 2015 data. Enrollment has increased by 34 percent in states that had implemented Medicaid expansion as of that date, and by 10.1 percent in states that had not.

Recall that Medicaid suffers from a neoliberal infestation, and so Medicaid services are contracted out to private health insurance companies. They’re happy too (ka-ching). From Forbes:

A snapshot of health insurers’ Medicaid windfall under the ACA could be seen in the earnings reports of Wellcare Health Plans and Centene, which both beat Wall Street’s fourth-quarter 2015 earnings expectations. These companies are an important measure of whether health insurers can find financial success providing Medicaid coverage to poor Americans under the health law President Obama signed six years ago even as the other key part of the legislation has growing paid.

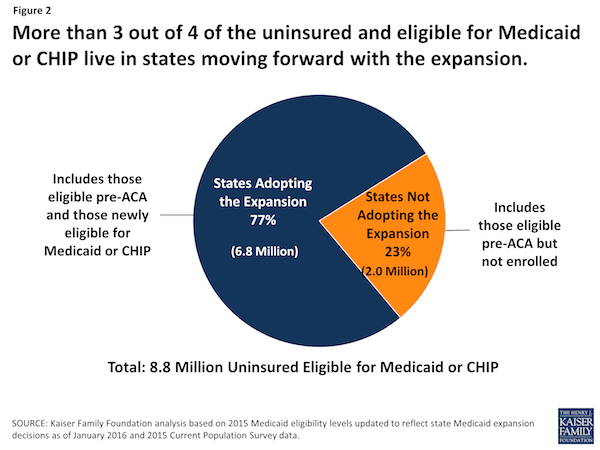

However, not everybody eligible for Medicaid has enrolled. Kaiser:

Most of the 8.8 million uninsured and eligible (77%, or 6.8 million people) reside in states that are expanding their Medicaid programs for adults, as these states have higher income eligibility for adults than non-expansion states (Figure 2). The other quarter (23%, or 2.0 million people) are in states that have not expanded Medicaid, but are eligible for Medicaid or CHIP under pathways in place before the ACA.

Here’s the same information in chart form:

So interestingly, and despite the Democrat “Those mean Republican!” talking points, the failure concentrates in Medicaid expansion states. But why? Why doesn’t everybody eligible for Medicaid sign up? It’s “free stuff”! Well, we’re in darkling plain territory again. We are ignorant. Nobody knows. The Wall Street Journal:

Among the 30 million people still without health insurance despite gains made under the 2010 health law, there is one surprising and poorly understood group: as many as six million people, like Ms. Collier, who are eligible to get near-free care through Medicaid but don’t sign up.

The biggest hurdle for those who want to sign up the Medicaid holdouts might be that not a lot is known about their motivations for staying out of the system.

So, ObamaCare was passed in 2009. Let me break out my calculator again… 2016 – 2009… That’s seven years into the program, and the people running the program, who think of citizens as “consumers,” and have built an entire “marketplace” to hawk their product, and are thorough-going neo-liberal “Because markets!” believers in every way, don’t know their market at all. They are ignorant. Let’s do a study! Ka-ching.

Conclusion

I envision the top echelon of health wonks in the political class being very much like the liberal upper crotte so wonderfully described by Thomas Frank in his recent essay in Harpers:

Everyone strode with polished informality about the stage, reading their lines from an invisible teleprompter. And back and forth, the presenters called out to one another in tones of supportiveness and sweet flattery. …. This is modern liberalism in action: an unregulated virtue exchange in which representatives of one class of humanity ritually forgive the sins[4] of another class, all of it convened and facilitated by a vast army of well-credentialed American technocrats, while the objects of their high and noble compassion sink slowly back into a preindustrial state.

Such ignorance. No need for any of these people to struggle with Covered California’s miserable P.O.S. website. They have people for that. I bet their teeth are all in good shape, too.

NOTES

[1] More from Gallup:

The uninsured rate among Hispanics was 30.9% in the fourth quarter of 2015, down 7.8 points from the fourth quarter of 2013. Similarly, the uninsured rate has declined 7.4 points among blacks over this same period. The sharper declines among these groups in part reflect that they had much higher uninsured rates to begin with. Even with the declines over the past two years, blacks and Hispanics still have relatively higher uninsured rates than the rest of the population.

The Democrats can’t even successfully target their own putative constituencies for basic, bottom-of-Maslow’s heirarchy services!

[2] So sign some crony up for that contract!

[3] Recall that insurance companies can still game ObamaCare to deny coverage to pre-existing conditions, for example with narrow networks, narrow formularies, leaving speciality hospitals out of their networks, etc.

[4] Not having “skin in the game.”

My Obamacare premium increased by 100% this year. I asked why and the response? It’s based on an algorithm. Also, it took 4 phone calls, including a conference call with myself, Covered CA & Healthnet to straighten out the billing. It’s a freaking disaster!

I’ll just comment that we recently had a meme where Hilary told Bernie what a bad idea it would be to start over with ACA, whereas she wanted to “build on all of the success”.

Maybe they can arrange something with human biology where your eyes turn flashing yellow or something when the b*llshit fills up and overflows your entire being?

Regarding Medicaid – I was under the impression there is a clawback provision. Speaking for myself, just that alone would prevent me from ever considering Medicaid as an option as I would never want to leave that burden to my family.

Plus there’s the open-ended telephone research project of finding a doctor who will take Medicaid:

Ostensibly, quality of care is unrelated to payment. But only a very naive individual would believe such a thing. Just as only a very altruistic physician would spend the same time with a Medicaid patient as with one who is paying three or five times more.

In blunt terms, Medicaid sucks, unless you have no other option.

Well the clawback is only on inheritance as far as I know. If they aren’t going to inherit much anyway, then I don’t think they have any obligations to pay it out of their own personal finances or anything (this could change, and that would very bad).

I’m not really defending the clawback provision, it punishes the poor and middle class, just it’s hard for me to see not inheriting as a burden exactly.. A loved one not having health care is a burden as well.

Well, the family home is oftentimes the only thing left to pass on to the children. So why shouldn’t there be a homestead exemption?

Well, even though corporations are legal ‘people,’ dead people are not. Why isn’t an estate not included in with corporations here? Hmmm…

people with financial planners and the capacity to do so place their home in a trust I hear, the clawback just preys on the weak.

Yep, irrevocable trusts. As you point out though, how many people on Medicaid will have the means to hire an attorney to prepare one, even if they had heard of such a trust?

If you are between 55 and 65, there is no longer any asset test for Medicaid. In other words, if a 56 yr. old goes to purchase health insurance on the exchanges–and his/her income is at a certain low level, that person will be directed automatically to Medicaid, even if that person has $50,000 in savings–if that person’s income is too low to qualify for subsidies and private insurance.

To comply with the mandate, that person will be forced into a system that essentially is a loan secured by his estate. In other words, it’s a reverse mortgage. But if that very same person earned a few dollars more, the person would qualify for subsidies and private insurance without any estate clawback.

Yes, so if you’re on the bubble, you are urged to lie. How one becomes complicit in this wretched system.

– In other words, it’s a reverse mortgage.

Well put.

We have a time honored tradition of stripping poor people of everything they own, its just they used to be elsewhere- now we’re turning on our own people-

and gutting the world’s safety net, with our negative list US style trade deals, just as the bulk of the working folks jobs are vanishing for good faster than one can say “cross border data flows”.

This document explains an important piece of why they do what they do.. http://www.iatp.org/files/GATS_and_Public_Service_Systems.htm

Also read the Nicholas Skala paper I linked in my other post- thats an eye opener –

Depends on which state you’re in, but yes that is ultimately very mean spirited and cynical. The Medicaid part of the ACA is a big money maker for insurers, so there are no cost controls making the system extremely expensive, that way lots of gov’t dough goes to insurers, then when you die your heirs get nothing and your assets get handed to wall st for a song, which they then sell high back into the eCONomy! What was that noise the old cash registers used to make?

People have to understand the constraints on government to not do anything that adversely effects the profits of multinationals, banks, insurance companies, etc. because international capital.. mobility and all.

We can spare a few hundred thousand sick poor people a year, to help make the point that we aren’t giving our own people any sweetheart deals..

Note that 60% of the states containing 60% of the population didn’t expand anything. So we didn’t break the WTO Understanding on Commitments in Financial Services standstill clause..

We ARE dismantling public health care! Slick, huh?

Also, get this- people have to be impoverished before they qualify, making millions of exits from the workforce just to get a drug that costs $0.11 a year to manufacture, no buyouts, they are are voluntary.

It also helps keep older people out of the job market – older people never demonstrate-

Obamacare is a work of genius. but we have to say we hate it..

Lambert,

I know you mean well, but “Ka-ching” is really getting stale. It reminds me of that phase in grammar school when “that’s what she said” was all the rage.

I disagree. “Ka-ching” sums it up pretty well.

That’s what she said.

Ka-ching.

Well, writing the post I was amazed at how many opportunities there were to use it. Can you suggest one or more alternatives?

Or perhaps I should add a sound effect?

Try this one

https://www.youtube.com/watch?v=1ytCEuuW2_A

For example:

“Liberal economists correct Sanders’s fuzzy math” https://www.youtube.com/watch?v=1ytCEuuW2_A

ka-ching says it all, maybe too clearly for some people…

perhaps after a few repeated uses say something like “man this register might jam with all the ka-ching’s happening. and then the obama administration will contract out servicing the register. I’ll ka-ching if/when it comes back”

But then again the only possible alternative I can come up with is “Unexpected item in the bagging area” so can’t we just carry on using what works?

Ha! A couple of months ago, I wished for the day when it would no longer be necessary to say something like “ka-ching”. Needless to say, that day will be far in the future…

“Bada Bing, Bada Boom!” ?

“Cash talks, bullshit walks” ?

“BAM, there it is!” ?

Nah..stick with Seth Green, the ka-ching guy.

From the Illinois S-CHIP website (the Illinois program is called “All Kids”):

This, in my opinion, is an example of the reason families aren’t signing up for Obamacare. Compare the costs in the Illinois program to the quote above:

My guess is that families are making sure their kids are insured but the parents are going without. Using Illinois as an example, the doctors and hospitals available under All Kids are great, and parents don’t have to qualify for Medicaid in order to have their kids covered. On the other hand, adults on Medicaid have a tough time finding doctors. For people working low wage jobs, with unpredictable annual earnings and no benefits, why wouldn’t you opt for inexpensive protection for your children and just use home remedies for yourself? It’s a dangerous gamble, but the economics are pretty straightforward.

Excellent insight. Thanks.

All these numeric contingencies make for really grinding reading and difficult understanding. 13% of the 200-300% FPL prefer product A but only 7% of the 300-400% signed up while the 100-200% FPL saw a 59% increase to 40%.

The deductibles, incomes, subsidies, etc make an impossibly complex maze of BS. I know Lambert’s discussed this. It just gets so hard to make a mental model in which I can place myself to make sense of what the heck’s going on.

Then I remember all the extraction and BS and how that’s the actual point, and it all makes sense again.

Thanks for the article Lambert. Only shortcoming: I think every article you write on health care should note, at least in a footnote, that the whole thing is a scam which could be fixed by single-payer; that is, all of this discussion and wondering and suffering and tweaking and surveys could be insta-nixed with a simple policy change.

During the hearings for the ACA the thing that I took away from days of watching them beginning to end on CSPAN was that the insurance companies were making the dismantling of SCHIP a mandatory requirement if the government wanted their participation, and from what I know now its my understanding that it comes down to a particular and little known area of our state ideology called competition policy..

Also, you can learn a bit about this issue by Googling the following lines..and drilling down deeper- especially the third one.

“For the purposes of this Agreement…

(b) ‘services’ includes any service in any sector except services supplied in the exercise of governmental authority;

(c) ‘a service supplied in the exercise of governmental authority’ means any service which is supplied neither on a commercial basis, nor in competition with one or more service suppliers.”

They are the lines from a 1995 trade agreement that form the official definition of what services are covered by a newer “plurilateral” trade deal that is almost completed in Geneva after ten years of negotiations.

One that forces big chunks of the public sector to gradually privatize, globally, so the jobs can be put into the big game – giving us more leverage, with the Global South, where they expect growth to continue a few years longer before automation hits there like it has here, but they are underestimating the rate of change..

Those jobs once they are in play, likely will be put up for e-tendering system and procurement of those services will become a legal right of the winning lowest bidder. That will push wages down for skilled work by making the whole world one market.. In other words, its not immigration, its tempoary, so they can be traded internationally.

Since we’re the country pushing these things, we cannot give our own people any kind of better deal, on principle.

By the way, not a peep during those hearings did I hear about the fact, which I am sure everybody there was aware of, that decades of research shows that even small copays are too high for SCHIP families and they result in kids not getting care. oftentimes its a bad mistake because small amounts of money spent then often results in much less money spent later..

All that was thrown out the window.

Hypersensitivity; The Rear View Mirror Problem

GIGO – “the behavior of the mirror system is the reflection of the information processing streams that plug into it.”

Mr. & Mrs. Clinton were at the center of noise, and reflect that noise; they are now tone deaf, like the majority they represented always is, and now a new majority is forming, same as the old, hiring a scapegoat for their own behavior, to identify a bogeyman, as they move deeper into the cave. Life takes all kinds, and each position has its trade-offs.

Humanity moves forward, nevertheless. As we do, we are becoming hypersensitive relative to the past, adding sensory perception with artificial intelligence, and the good doctors are studying the majority, analyzing the past and predicting nothing, as a means of ‘treating’ the population advancing, which wants nothing to do with the draconian methods of witch doctors. Inferential deduction built on a foundation of sand doesn’t get you very far, except in the wrong direction. You are looking for discernment, which can only be found in yourself.

When a baby is born, from a world of parents, highly specified nutrition and nearly pure oxygen, the last thing you want to do is give it shots of immunodepressants, deprive it of oxygen and confine it to a completely artificial world, relative to its parents. Nevertheless, that is the prescription of Obamacare, because the majority fears the future, anything entering its shrinking box that may challenge its assumptions. Blinded themselves, the good doctors assume that everyone else is so-afflicted.

If you and your spouse are hypersensitive, the last thing you want is modern medicine, which has always been the solution for ignorance, by those waiting to pounce on it, and breed more of the same. You are not going to ‘beat’ nature with a derivative of nature designed by a derivative of nature. The short cut is always the long way, in time.

My wife had to learn the hard way, that her own family, community and government were aligned against her, long before she contemplated a baby, all bitching and moaning about someone else, collecting a check in one way or the other to participate. Everyone involved was told not to give those shots to Grace, Grace blew up, and they were frightened, immediately turning to find that bogeyman, someone, anyone other than themselves. Emotionally, it’s devastating, because you see the train wreck coming long before it happens, in slow motion, but they do you the favor of shuffling your children into the deck, better than you could.

DNA really doesn’t care about your emotional response, because you are the past and it knew you before you were you, with eggs for the next already installed. Money and property are but illusions of artificial differentiation, pretending otherwise. The distance you are interested in is mental, the distance from the noise of ignorance.

I’m not saying don’t go to Rome; it’s a nice place to visit, but the longer you stay there, the more you drift into its particular brand of ignorance, feedback in event horizon time. Besides being the anti-Christ, an illusion combating an illusion, the Pope may very well be a very nice guy, or not. Regardless, it is what comes out of your own mouth that matters most, in terms of the path you travel, because your self-obsessed brain is always listening.

Don’t curse yourself by cursing others in a house of mirrors.

Generally, my method is to give each a unique piece of information contrary to my character and time its return and path. As you can see, my ‘language’ is highly distributed. Now, the RE bank is placing signs in every corner of the city and calling social security recipients offering zero down liar loans, which tells me everything I need to know.

I am not going to waste my time getting even with a hospital full of mental midgets, and neither should you. Have some faith, and act accordingly, to set your distance. I’m ancient, but houses for young people are about to be a dime a dozen; don’t waste your time building anything but a home.

Don’t stand in a soup line, a bank line or a drug line, with those who chose to ignore the obvious, with the latest and greatest gossip. Go to where you are welcome for who your are, instead of competing for debt to be who you are not. And don’t be surprised in your own home town, by enemies who are not really your enemies, and friends who are not really your friends.

There are always opportunities wherever you are and wherever you go, if you have the courage to look, beyond the mythology of empire. Funny, people are people, including you, and it isn’t the bully on the corner, TV or Internet that determines your future. Technology is an inferential illusion, which may or may not have its uses at the time.

The History of gossip and voyeurism merely serves to place you in a line to get in a line to go nowhere. The fact of the matter is that the majority couldn’t raise children if their life depended upon it, and it does. Expert is just another way of saying specialist in ignorance.

There is no such thing as an expert parent, only experience with your own, which is why healthcare in America is such a colossal failure, and everything else is a derivative.

So much gnashing of teeth to cover ~5% of the population. This is Obama’s signature achievement?

Yes. This is Obama’s signature achievement. The obfuscation and the dysfunctionality and the lack of accountability and the self-righteousness are all part of Obama’s signature. Along with the looting, of course. And the excess deaths.

Don’t forget the unintended (intended more likely) consequences of the 30 hour work week which has been as inimical to the middle class as all the job outsourcing.

Our family has been helped by Obamacare but I am beginning to concede that far too many people are not being helped which is why I think single payer is the only option. Since I was a personal injury attorney for 35 years before I retired I can navigate through the morass of insurance and governmental crap without any real problem other than wasting lots of my time.

But my experience has taught me that many people would probably not have the skills or knowledge or time to navigate the maze even if it made good economic sense. And it is easy for me to figure out that if you don’t qualify for a subsidy, these plans are probably way too expensive for most people to afford. And even for those who do qualify for a subsidy, many of the plans are too expensive and getting more so. A plan that cost my adult daughter $40 per month the first two years with a full 94% subsidy now cost $71 per month with the full 94% subsidy.

So much for curtailing costs.

So this is a topic I can speak about with first hand knowledge. I have been in the so called “individual insurance market’ since 2009. When I first bought insurance for our family of two adults and one child in 2009 our premiums were $410 per month with a $5k deductible. The insurer was Anthem and the coverage and benefits were excellent and the network was extensive. The premiums increased steadily each year and by 2013 we were paying about $600 per month in premiums for the same plan. That was a pretty healthy increase in premiums over 5 years but nothing compared to what happened when the ACA kicked in. At the end of 2013 we received notice that our old plan was being terminated and offered a new plan at the cost of $1,675 per month with a $5k deductible. Needless to say I was stupefied to see our premiums nearly tripled!!! I called the Connecticut State Insurance Commissioner’s office to ask how this was possible and was told that rates had indeed gone up dramatically in the state as a result of the ACA and it had absolutely noting to do with enhanced benefits since CT had long mandated comprehensive coverage for all plans sold in the state. Rather, our rates increased astronomically because we were no longer “under written” meaning our policy was no longer priced according to our age, health, etc. The insurance commissioner’s office explained that rates were so much higher because of the expected cost of insuring people with pre-existing conditions and that the state had thereby authorized dramatic rate increases.

One can argue that this is good public policy but form our perspective it destroyed the individual insurance market and took $13k in after tax dollars directly out of our pockets. The story gets even worse. Prior to the ACA all of the expenses associated with my annual physical exam were covered but under the ACA I have had to pay about 35% of the total bill because a couple of the routine screening tests that were covered under the old plan aren’t covered any longer.

In addition shopping for insurance has become a complicated nightmare with scores plans with endless permutations that are nearly impossible to decipher. And that is before you even begin to try and understand the network issues which are a nightmare.

The ACA is a sick joke as far as I am concerned. As for all the poor people who can now supposedly afford insurance, well that is a load of BS propaganda. There is no way most families can afford these plans even if they get a “subsidy”. And with $5k deductible most people avoid going to the doctor under these plans.

So the issues you discuss are a reflection of this warped and predatory system that has been forced on us. The worst part of all this for me personally is that I supported heath care reform for multiple reasons but I should have known that once the world’s most disreputable and skanky whorehouse got involved nothing good was going to happen.

Thank you so very much for sharing your personal story. It is so helpful to have real-life examples, and I am sick at heart for all of my fellow citizens suffering under the Not-So-Affordable Care Act. We need single payer. Period.

From someone who departed the US for Australia when Bush II was re-appointed, in large part because I saw these kinds of train wrecks coming…believe me you do want single payer. It’s a dream.

Now if we could just get enough people angry and fed up enough to get off their couches and pull the lever for Bernie instead of the Wicked Witch of Arkansas.

I had a similar experience. I’m glad to see somebody talking about the devastation Obamacare wreaked in the individual market because it seems hardly anyone is aware of it.

Thanks, I have been shocked at how distorted the coverage has been on this issue. I find the whole thing Orwellian with all the double speak and lies starting with the very name, “The Affordable Care Act”.

I voted for Obama with a great deal of belief and enthusiasm in 2008, I now think he is a disgrace for a whole host of reasons.

I think my local insurance monopoly was ahead of the curve.

From 2008 to 2009 my single person costly coverage went from about 700 a month to over 1,000,

I called the insurance company- “name one single cost that has gone up in 2008, just one”….nothing.

State AG was in no luck, they are federally exempt from anti-trust statues. I even called the state police to ask what would be required for them to be charged with extortion. We ended up agreeing that, by the letter, and intent of the law, they were guilty, but they couldn’t do anything without the AG.

Then this cherry on top, after my original very expensive 700 went to over 1500, and I said fuck it-

http://www.rbj.net/print_article.asp?aID=207198

Ex-CEO Klein to collect some $29.8M

Originally reported at ONLY 12.9 million.

His picture should be in every dictionary under “non-profiteer”. BCBS is non-profit, remember. For whom, they never say….

Adding, very profitable non-profit, also-

http://www.syracuse.com/news/index.ssf/2013/03/excellus_reports_106_million_p.html

“Excellus BlueCross BlueShield made a $106 million profit in 2012 and paid its former chief executive officer David Klein $3.8 million, the health insurer reported today.

The profit was less than half the $223 million it made in 2011.”

This has been the exact same experience I’ve had with my mother’s insurance travails on the individual “market over the past decade +. Increasing premiums, increasing deductibles, shrinking networks. All of these trends have picked up speed since Obamacare went into effect. It is a sick joke indeed.

“[F]rom our perspective it destroyed the individual insurance market and took $13k in after tax dollars directly out of our pockets.”

But remember you’re doing your little bit to bend the cost curve.

Holy Heck! You people are getting robbed blind!!

Here in Socialist Sweden, I make the equivalent of 6,574 USD per month and I pay about 2,191 USD in taxes per month – this amount includes medical care (with 352 USD “self-pay”/deductible) and of course everything else – school, university. The property tax is 800 USD annually and there is a car tax for 160 or so.

Did I mention the 40 hour work week and 6 weeks (working days, of course so 8 calendar weeks) of vacation???

oh shutup

Ah. Sweden the socialist paradise where refugees have instant rape privileges for women and children. not to forget subsidies while destroying the very society that enables them.

Just paid our monthly premiums for myself (64) and my mate (57). We have the cheapest policy available in our state (WA). It is $985/mo. w/of course, a $6k deductible…ea. So…we pay almost $12,000.00/ year for a policy that never covers anything until we are hit by a bus. Luckily for the insurance co. we live on an island w/o roads.

Since I work as a contractor, before Obamacare I was using Freelancer’s Union for my insurance and was paying around $600/month for a very solid plan with no deductible (in network). The network was robust and I had relatively few complaints. Now Freelancer’s Union doesn’t have a plan anymore, just directs us to the NY health exchange. I couldn’t find a plan that included any of our doctors for less than $1,000/month with a $4k deductible, and lord knows how rotten the narrow network really is. All of which means we haven’t been insured for years and don’t see any light at the end of Obama’s awful tunnel of garbage “insurance”. Sickening, and we’re supposed to vote for Hillary who is now apparently “for” (*TM) a “public option”. Why am I not excited? Of course we’re feeling the Bern. How can we not?

* The word ‘for’, in this context means something Hillary nominally ‘supports’ but will do absolutely nothing to pass once elected, or if she does bother at all, it will be to push for a proposal that will be so hollow and non-competitive as to be unworthy of the already weak concept. Neoliberalism at work!

Count me as a former member of the FU, aka the Freelancers Union. Being an AZ resident, their insurance did me no good. (It only covered residents of NY State.)

The rest of the organization seemed like a buyer’s club, rather than a union.

And, IMHO, unions for independent workers are very much needed. If employees were treated the way freelancers routinely are, this world would be on general strike.

Or perhaps we could end the monopoly that jobs have on the necessities of life…

The real solution isn’t better employer-based healthcare, but rather, having some form of universal health insurance independent of employment that drives down the prices charged by hospital franchises, drug dealers, equipment peddlers, medical schools, and so forth.

“The biggest hurdle for those who want to sign up the Medicaid holdouts might be that not a lot is known about their motivations for staying out of the system.”

How did that get published anywhere?

“The biggest hurdle for those who want to sign up”

Oh wow, it seems an answer might be afoot-

“the Medicaid holdouts”

Nope, unless the medicare holdouts are the hurdle?

“not a lot is known about their motivations for staying out of the system”

Asked and NOT answered. But, then, wait, how did this sentence start?

Hurdles got in the way? Millions of hurdles, on the internets. Why are there hurdles on the Internets? Because medicare, motivations and morons trying to type.

Wow, I missed that “Medicaid holdouts” framing. It’s like they think their “customers” are the enemy, or something.

MERC 1: Over there! Medicaid holdouts!

MERC 2: Confirmed eyes on, target is designated.

RADIO VOICE: Roger, target acquired…

Together my husband and I curently pay $1,300. premiums monthly which reflects a BCBSAZ grandfathered plan that increased around 20% this year and his ACA premium plan that incresed 38%. Both with no significant claims $4,500. deductables, $50. co-pays for office visits etc.

It’s incredible and mind boggling but we can’t risk being w/o insurance.

I can’t imagine the young or healthy, likely already burdoned with crushing student loans will suscribe to this and the majority living paycheck to can begin to afford it.

The sophistry of the system is preposterous. Imagine the Canadian health care system was created on 3 pages.

And even in lawyer-riven USA, HR 676 was all of what, thirty pages? Methinks Rep. Conyers needs to answer for his pledge to Hillary.

If you’re having trouble understanding why people at 300% FPL aren’t spending a mortgage payment every month for a plan that will bankrupt them if they actually try to use it, your problem may be not a lack of information, but a lack of insight.

It does seem obvious. What is amazing to me, or not, is that none of the many polling and consulting organizations paying good money to highly Credentialled experts for studies aren’t even asking questions about that very problem.

Here’s a product that people are actually mandated to buy, and they’re still not buying it. Could it be that the product is defective in some way? That “affordable” and “worth the money” are not the same thing?

Nah, science fiction stuff. Can’t be that. Let’s not waste our valuable panel space on wild speculations.

Hey, those experts are paid good money not to understand that!

Sure the “affordable” is a scam, but so too is the “care”.

Those offensive premiums buy not a penny of care. All you bought was an insurance “policy”.

That contract just lets you, an ordinary Joe, have an argument with a giant corporation about whether this complex contract means they must cover some of the money that you already owe to those who delivered whatever care you actually got.

Orwellian. We need to stop using the enemy’s language.

And let us not forget that the postponed-until-after-the-elections but NOT eliminated “cadillac” (ie decent plan) tax continues to lurk in the background.

If that comes into play, the upper stratum of the working class and public sector workers are going to fairly rapidly discover that this was not a good deal for them at all. I love the theory that the reason I didn’t competitively shop my wrist surgery is because my deductible was too low, so I wasn’t motivated to pitch in and help bend the ol’ cost curve. On what planet am I assumed to be competent to compare “products” and “vendors” when the “product” is a wickedly complex surgery involving that many tendons and muscles?

Even if you were competent to “product shop,” every time you visit a new doctor, you are going to be charged a “new patient” fee, whether or not you decide to continue seeing that doctor. Around here, the standard “new patient” fee is $125 and, at least in the case of Medicare, it is not picked up as an allowable expense.

Wait, what? You’re telling me there’s friction in the health care market?

Why aren’t people rushing to sign up for Medicaid? As I have 15 years of experience dealing with the program in New York State, I can tell you the reasons are many.

If a Medicaid enrollee calls a hospital ‘referral line’ to get the name of a doctor, your are steered to a Medicaid clinic (although it is not required) because federal reimbursement rates for clinic visits are at least 20% higher than that for in-hospital doctor office visits.The waiting times in Medicaid clinics are appalling, an average of 1.5 to 3 hours past your appointment – so if you have the temerity to be poor but working, you would have to take the day off, which would jeapordize your income, and perhaps your job. The Medicaid clinics are, of course, training grounds for interns and resident doctors, who rotate through every 6-8 weeks. This means anyone with chronic conditions (CVD, diabetes, hypertension – classic diseases of poverty), never have the same doctor for any real length of time, with a gross lack of continuity of care – a breeding ground for medical errors and neglect

On top of all this, NY has joined 17 other states in the Obamacare ‘FIDA’ pilot. This crapification maneuver forces anyone with Medicaid, even if they have Medicare as their primary insurance, into HMOs or ‘managed care plans’. These naturally have narrow networks, few specialists in any particular catchment area, and those specialists are overbooked and of mediocre quality. God forbid you have a neurological condition, autoimmune disease, or other ‘exotic’ illness – specialists do not exist.

The only current exceptions to FIDA in NYS are Medicare/Medicaid patients who do not need homecare, or Medicaid enrollees in one of 2 ‘waiver’ programs (there used to 5). The Medicaid waiver programs cover either developmentally disabled children, or traumatic brain injury patients. I fled to the TBI waiver program to avoid FIDA, as it was supposed to provide more targeted services. However, I discovered that the TBI program was thoroughly corrupt – there was no state oversight of contractors; indeed, the state director of the program was aiding and abetting them. My local program provider was being paid about $4k/month to provide services to me, including 40 hrs/week homecare, but for 9 months I had no assistance whatsoever. After a 1 1/2 years of struggle (with help from 2 public interest attorneys, no less), the problems were still not repaired, so I had to return to FIDA.

Cuomo and Obama are hard at work turning Medicaid into a complete sump.

Every time I write an ObamaCare post, I get multiple detailed, knowledgeable, and credible comments on clusterf*cks like this, and from different commenters, all across the country. (This one is from the People’s Republic of New York, where government is still supposed to work.)

I can’t imagine why reports like this aren’t being aggregated and studied. Why, it’s almost as if there’s a news blackout being imposed, or something.

In a 2008 paper entitled State Health Reform Flatlines America’s previous attempts to enact health reform that was compatible with the state ideology were detailed.

Like Obamacare, they all collapsed in a few years, for the same reasons.

The problem is really a system that wastes a third to a half of every health care dollar, which is still being pushed as a success, due to somewhat delusional thinking that hopes to lock it in place globally using bad trade policy , basically “future proofing” the future. By deceptive means. of course, Americans themselves cannot be given a sweetheart deal, when profits must be maximized globally. So we have to get the worst deal of all. Mr Friedman broke the rules by telling the truth as it is, and the implicit back story is that we are a nation abused that wil recover strongly after the abuse is ended.

The real problem behind the scenes is something almost nobody is aware of. Really bad trade policy.

A very good 2009 paper by the late Mr. Nicholas Skala lays out the problem quite articulately.

We need to see this issue for what it is soon. Approval of any one of the three pending trade deals, especially the plurilateral agreement on services that is now almost completed in Geneva, will make the problem much much worse, basically hijacking the election and severely constraining choices to ones that conform with the trade deals implicit ideological framing, which basically forbids the entire New Deal as well as Senator Sanders entire platform. This fact can be extracted from an intelligent reading of the so called mandate document here..

The body of the “mandate document” consists of garbage characters in my view. Can you provide another link, or tell me what character set to use?

Incidentally, the plurilateral link was an outcome of Maine’s Dirigo health care program. Dirigo and health care policy generally was one reason I felt comfortable moving to Maine in 2006, and leaving my corporate health insurance behind. I felt the Democrats couldn’t possible fuck it up. Hahahaha. What a simp.

Apparently Content-Type: headers are “liberalised” in the EU. Try saving as a PDF file.

Thank you for telling me that, that would explain a lot.

My guess is that the URL- which is sort of nonstandard, is not triggering the right mimetype behavior in your browser. So your browser likely thinks its HTML. its not, its a PDF..

What you should do is try to save it as a file with a PDF extension. Like notamandate dot pdf or something shorter.. Dont edit it in anything, just let it stream like its gibberish text and save it with the right extension..

Then open it in a PDF viewer.

Also, if you have a bit of curiosity left in you after that, this is for the investigative journalist in you. I don’t know what to make of it. Its not encouraging.

The document here may be helpful for sorting out the differences between the two deals.

Who wrote “this document here”? I can’t tell from the website. Thanks!

The dual Canadian nationality I inherited from my mother was the best inheritance I got. I’m happy north of the boundary at age 63.

I don’t suppose that works as far back as grandparents…

Certainly seems designed to fail, doesn’t it?

A doctor on a competing financial blog said (in the comments section) that Obamacare is the TARP program for the insurance companies. After bailing out the banks with enough money to pay off everyone’s mortgage, there was no will to do the same thing for the insurance companies, although they were next in line. So the insurance companies were allowed to write this program of graduated extortion where you pay them the protection money until you go broke in order not to go broke when you need doctor/hospital care. Except now you’re too broke to afford the deductible. Win/win, insurance company, lose/lose you. The only way to win is not to play, but most people are too scared to go without coverage that doesn’t really cover anything.

That is solid gold, fantastic observation. Can we finally point the finger to the center of all of our woes: the Federal Reserve and their Keynesian delusions of debt-based money. The temptation is ALWAYS too great to print too much and the society is told they need to bail out the casino gamblers.

Well they have the “solution” ready, just in time!

What a coincidence.. cough…

A manufactured crisis that “forces” us to sacrifice our doctors and nurses and our minimum wage and our current way of handling permission to work on the one way street / sacrificial altar of *”progressive liberalisation”* is what is in the pipeline..

They have been planning it for 20 years, literally, no less..

But its a sensitive subject, because it involves millions of jobs, you see!

Shhh or they may hear us!

Developing countries know more about this than we do of course and are already gearing up for the challenge.

I know two people who are dropping their “exchange” coverage, because they were misled concerning subsidies. One has a decently-employed husband; she was told by a navigator that she was eligible for hefty subsidies. Then when her tax bill came due, it turned out she wasn’t, and she had a very big (I don’t know the exact number) tax bill because the family income was higher than predicted. They can afford to pay it, but she is very disgusted. Another is a close family friend who has a small business (she used to clean houses; now she does online sales) who didn’t have health insurance for years. She signed onto the exchanges and got a hefty subsidy. Then, her tax bill came due and voila, she owes $6,000 because her income was “higher than predicted.” She can in no way pay this (she is trying to work out a deal with the IRS) and also pay premiums; she is now dropping her insurance coverage and will be back to no insurance again.

I don’t have a big social set but if I know two people who had this happen to them I doubt it’s rare. I think that the “navigators” misled people about eligibility for subsidies to get them to sign on to boost enrollment numbers. Only when their tax bill arrives do they find out they are screwed. And it is very complicated; our family friend’s CPA can’t figure out exactly what is up.

Re medicaid avoiders: I would bet that some of them have become aware of the “clawback” rules, and that in some circumstances the cost of their medicaid benefits will be clawed back from their estates. I would like to find some updates on this issue.

I was recently retained to search for possible interests purportedly held by a recently deceased Medicaid recipient. The correspondence specifically mentioned that the decedents Medicaid application listed no assets, but her probate file mentioned possible interests in Minerals in two counties. As I understand it, I was NOT working for the heirs, but for the govmint, who paid me well.

I think the clawbacks are for real, and it seems to me that most families who are on the ball are very resolute and effective at dissipating the assets of the person contemplating (and frankly in need) of care, prior to ever applying for the Medicaid program.

Just like much of what goes on in Wall Street, all perfectly legal… difference being the Medicaid customer probably has no meaningful assets to start, and really needs a hand.

I encourage anyone here to visit the Physicians for a National Health Plan web site, try to get a screening of their 1 hr movie, “Fix It!!” at your local chamber of commerce, Rotary, business clubs, and local libraries.

Finally, I am embarrassed by and ashamed of our former Senator Baucus for ramming through this insane plan, and specifically for having two single payer advocate nurses escorted from hearings by the po-leece. For Shame. Poop rises: he’s now an Ambassador to China?!

“most families who are on the ball are very resolute and effective at dissipating the assets of the person contemplating (and frankly in need) of care, prior to ever applying for the Medicaid program. ”

Very much so, but it’s not just being “on the ball.” You’ve got to interact with the medical system, the legal system, and have the money to pay professionals to paper up the situation, so as usual it’s a case where those at the edge get kicked over it.

“State Medicaid programs must recover certain Medicaid benefits paid on behalf of a Medicaid enrollee. “For individuals age 55 or older, states are required to seek recovery of payments from the individual’s estate for nursing facility services, home and community-based services, and related hospital and prescription drug services. States have the option to recover payments for all other Medicaid services provided to these individuals, except Medicare cost-sharing paid on behalf of Medicare Savings Program beneficiaries.”

From medicaid.gov. They keep pointing out how “rare” it is in all the articles about it, though. lol

Wonder how long it will stay “rare?”

I ALSO am in the same situation, my husb and i last year first enrolled with obamacare and deemed within income levels…we were so glad to have ins ,im retired and husb works part time job so we have limted income but we qualified around the 33,ooo income level, …i had no idea ever that if in mid year due to blown water heater and other home repairs i had to do if i took money out of a retirement IRA it would ever affect any subsidies,,,when i enrolled i was never asked about my retirement acct, i dont have muuch but the money if there for emergencies, well obamacare sasy the money i took out of an ira mid year took me ovr income and now they want 10,000 back ,when my taxes got done is when i got this shocking news, never did i ever dream taking funds from an ira would result in this, they need to be more vocal about subsidies when you enroll, i read its obamacares dirty little secret they dont go out of their way to tell you about…now im going to be in debt with the irs,dont have all that money to pay and we didnt even hardly use any coverage all year…im still numb

Is there a typo in the original source for this quote about the price, one is per moth the other per annum?

Yes, it has to be an error in the source.

There is no way a plan has an annual premium. Premiums are paid monthly. The subsidies are set up around monthly income estimates and payments. And $394 a year is impossibly low.

Lambert asked “Why doesn’t everybody eligible for Medicaid sign up.”

I can’t speak for others but my even if my red state someday does expand Medicaid so that I become eligible, I will refuse to sign up (if given a choice) because of the Democrat-passed law that encourages states to put a lien on your property and on your financial assets to recover your health care expenses.

If you are over 55, Medicaid is not a gift, it is a loan that has to be paid by your children.

No problem! You can just do without insurance for 10 years, and then Medicare kicks in. So kwitcherbellyachin’. This is America!

There used to be a public health blogger called Revere. One of the things I remember them passing along was how much over-65s health status improved, or slowed in decline, post-Medicare enrollment.

Revere pointed out that if one were concerned with controlling costs, it would make sense to expand Medicare downward to 60-year-olds (at least), because costs are so much lower if many health conditions are found and treated early: heart disease and diabetes in particular. Never mind the death, disease, and suffering burden that could be prevented: it would save the U.S. government a ton of money.

It was evidence point 1(or 56,884,212) that neither saving money nor saving lives is the priority.

Here’s the article; it was actually calling for Medicare For All.

Another personal story of clusterfuck in the ACA, Covered California style: Due to increasing penalties this year, finally signed up! Picked a plan and everything, and was even happily surprised that coverage areas and available plans had mightily improved this time around. Not that hard to get an affordable plan with doctors in our area, unlike previous years.

So we get an email telling us if we haven’t gotten a bill yet, check online. I double check the unopened mail, and in fact I have one thing from blue cross anthem or something like that telling us how to go online and see more info about our plan, and another thing from covered california that has our income estimate completely wrong telling us we need to hurry up and pick a plan or coverage will be delayed, but no bill. So I go online to check out my plan. Anthem or whoever it is says they have no record of us! Covered California has no record either, and does have our income estimate way too low, so low it would entitle us for medicaid. While saying our income is too high for medicaid and we have to choose something else, even tho we never tried to choose medicaid. We tried for hours to get something going and finally gave up. Eventually one of us will probably do something again to check on it. Probably. Would think this was the kind of typically weird thing that happens to us but in this case it seems to be happening to lots and lots of people and be closer to the norm than to weirdness. I dunno who set this up but competence is not their strong suit.

You’d think that IT people given half a billion dollars could develop a website that successfully registered people for a service.

I wonder where the money went?

Political contributions, of course.

I think in effort to make more people enroll in healthcare. We seem to have created more mess. It would be good if we just a single payer system with everyone paying 5-10% of your income in your pay check. So that way if someone loses their job, their health doesn’t suffers. I am going to pay the fine because i can’t afford the cost of actually buy one which is close to 11K/year for two.