By Lambert Strether of Corrente.

Let’s start with the voters, in particular Trump voters who are enrolled in ObamaCare. Sarah Kliff did a series of interviews[1] for Vox, summarized here:

I spent last week in southeastern Kentucky talking to Obamacare enrollees, all of whom supported Trump in the election, trying to understand how the health care law factored into their decisions.

Many expressed frustration that Obamacare plans cost way too much, that premiums and deductibles had spiraled out of control….

There was a persistent belief that Trump would fix these problems and make Obamacare work better. I kept hearing informed voters, who had watched the election closely, say they did hear the promise of repeal but simply felt Trump couldn’t repeal a law that had done so much good for them.

For example, Debbie Mills:

“I guess I thought that, you know, he would not do this, he would not take health insurance away knowing it would affect so many peoples lives,” says Debbie Mills, an Obamacare enrollee who supported Trump. “I mean, what are you to do then if you cannot pay for insurance?”[2]

Mills’s expectation that Trump would keep the Affordable Care Act, on the one hand, feel unrealistic [to Kliff]: Of course Republicans would dismantle the law they spent six years campaigning against.

But it is also understandable: Legislators typically don’t dismantle large health coverage programs that serve millions. Since their creation in 1965, Medicare and Medicaid have certainly faced some opposition but never threats of outright repeal.

It’s early days yet, and things can always get worse, but as of today, Mills seems to be holding her own with Kliff on calling her shot. AP summarizes the current state of play:

While insisting they’ve not abandoned their goal of repealing President Barack Obama’s health care overhaul, Republicans are increasingly talking about “repairing” it as they grapple with disunity, drooping momentum and uneasy voters. The GOP triumphantly shoved a budget through Congress three weeks ago that gave committees until Jan. 27 to write bills dismantling the law and substituting a Republican plan. Everyone knew that deadline was soft, but now leaders are talking instead about moving initial legislation by early spring.

(The quote is from a fine wrap-up by Kaiser Heatlth News). Mic amplifies:

Congressional Republicans seamlessly rolled out a pivot on Thursday that could signal a major shift in how they will approach health care reform. The longtime GOP mantra for the Affordable Care Act was “repeal and replace.” Now, the same Republican leaders are using the term “repair” to describe their approach to the health care law.

The shift happened for a few reasons: Because Republicans do not have 60 votes in the Senate, they cannot repeal every word of the health care law. It also recognizes, from a policy standpoint, that a wholesale repeal may not be possible. Republicans have struggled to present a plan to preserve access to coverage for millions of Americans who gained it under the ACA, especially those with lower incomes.

Now, “repair” doesn’t mean that the administration, whether from malevolence or chaotic policy-making, won’t end up “affecting people’s lives” adversely. Enrollment has dropped:

Enrollment in Obamacare health plans sagged markedly after President Trump‘s inauguration, according to new federal data that show sign-ups slowed in the final two weeks of the 2017 open enrollment period as Trump stepped up attacks on the healthcare law.

The slowdown is particularly noteworthy as enrollment was running slightly ahead of last year’s pace until Trump took office Jan. 20 amid renewed promises to scrap the 2010 Affordable Care Act.

Altogether this year, slightly more than 9.2 million people signed up for coverage in the 39 states that use the HealthCare.gov marketplace operated by the federal government.

That is down from more than 9.6 million who signed up last year.

The enrollment tally — which doesn’t include sign-ups from 11 states, including California, that operate their own marketplaces — is still substantial, undercutting claims by Republicans that the healthcare law is collapsing.

But the dramatic drop-off in the last two weeks fed rising criticism that the Trump administration is sabotaging the marketplaces to strengthen its political argument that the law must be scrapped…..

Trump also issued an executive order in which he suggested his administration wouldn’t implement rules crucial to sustaining markets.

And over the last two weeks, Trump and many GOP lawmakers have stepped up their criticism of the marketplaces, even as insurance industry officials warned that Republicans risked destabilizing the markets.

Only about 376,000 people selected a health plan through HealthCare.gov in the two weeks leading up to the Tuesday deadline, according to the recently released data.

By comparison, nearly 687,000 people chose plans through HealthCare.gov in the final one week of the open enrollment period last year.

So, Trump stopped ObamaCare’s marketing, and enrollment dropped off. (It’s worth noting that universal benefits sell themselves; they don’t need to be marketed in the first place[3]. So, from the 30,000 foot level, the enrollment drop-off is due to ObamaCare’s horrid program design.) Presumably, only the healthy wait ’til the very last minute to enroll, and so Trump’s executive order increased adverse selection in ObamaCare’s risk pool, accelerating ObamaCare’s death spiral. (On the death spiral, see here, here, and here.) Is 687,000 – 376,000 = 311,000 a big enough number to “sabotage” the program entirely? I doubt it.

Nevertheless, the mere prospect of “repair” could accelerate the death spiral, in itself. Bob Laszewski gives possible repairs and explains why:

These could include:

- Refusing to enforce the very unpopular individual mandate’s penalty for not purchasing health insurance.

- Leaving the mandate and its penalty in place but dramatically increasing the Obama administration’s “hardship” exemptions in the face of the expensive high deductible plans people now face.

- Enabling health insurers to offer limited duration health insurance plans that they are still allowed to medically underwrite. The Obama administration had intended to eliminate these policies that provided more than three months of coverage. By bringing these policies back to the market, a parallel market of cheaper plans attractive to the healthy could be created thereby pulling healthy consumers out of the Obamacare pool.

The short of it is that the Trump administration, by trying to bring relief to some consumers, could just as easily further undermine the already shaky Obamacare risk pool.

If the pool were to be made worse than it is now, health plans would be challenged to figure out how they could remain in a market already intended for demolition once the new replacement plan was ready in 2019.

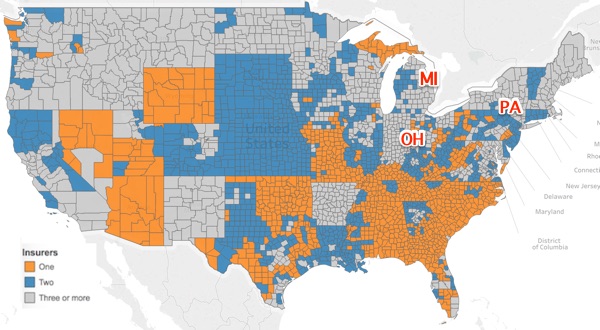

In 2017, 31% of counties have only one insurer and 62% of counties have two or fewer insurers in the Obamacare insurance exchanges.

Republicans need to be careful. Making an already fragile insurance exchange market even worse could easily lead to some markets having only one or no health plans selling individual health insurance in 2018. Even if a health plan chooses to stay, a less stable market could lead to even higher prices and deductibles and even narrower provider networks for consumers.

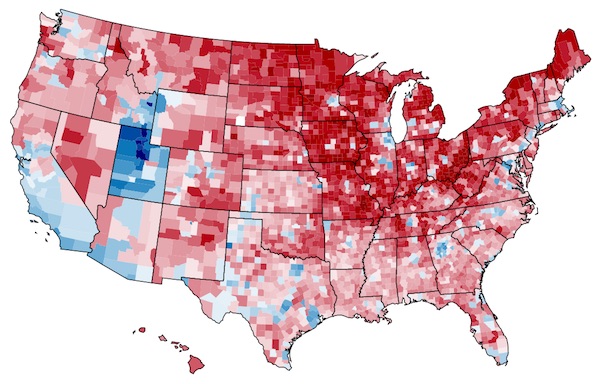

Back to the voters! Let’s look at those counties. First, here’s a chart (for completeness, since most readers are probably familiar with it) of the counties Trump won. From Time:

And now let’s look at those 31% of counties that have only one insurer and 62% of counties that have two. (On the map, grey counties have three or more insurers, blue counties have two, and orange counties have one). Pay attention to the blue counties. From Kaiser Health News:

I’ll take it as read that counties with a monopoly supplier have insurance that’s (even) more crapified than those with several suppliers. So, where are the counties that are on the bubble between two and one suppliers? That is, the counties that will turn from blue to orange? Why, many of them are in the swing states that Trump very unexpectedly won in 2016: Michigan, Ohio, and Pennsylvania. So, if Trump wants to unswing those states in 2020 by pissing off Debbie Mills in her hundreds of thousands, then he should crapify her health insurance (even more) with “repairs” that make sure she’s sending her checks to a monopoly supplier.

Tomorrow I’ll look at TrumpCare and policy.

NOTES

[1] I like Kliff, but this piece is another “road trip” piece, where anthropologists from the metropolis visit the exotic primitives of the colonies. Kliff also encountered volatility voters:

The Kentucky voters I spoke with constantly mentioned “change” as a reason they supported Trump.

“That man has a head for business,” one enrollee said. “He will absolutely do his best to change things.”

Still, Oller acknowledged she took a leap of faith with Trump.

“It was Russian roulette,” Oller said of her vote. “But I felt that we needed change.”

[2] Mills’ question is answered by Rule #2 of Neoliberalism.

[3] ObamaCare, among other things, is a welfare make-work program for 10%er symbol manipulators: Marketers, web designers, trainers, video producers, pollsters, and so on.

If anyone is interested, and Lambert, this may be worth adding, the Obamacare rise per state in premiums:

From Business Insider (not sure why some states are greyed out):

http://www.businessinsider.com/obamacare-price-change-for-every-state-in-us-2016-5

Anyways, there’s another map from the USA Today:

http://www.usatoday.com/story/news/politics/2016/10/18/regulators-approve-higher-health-premiums-strengthen-obamacare-insurers/92286590/

I’d be very interested to know if anyone here has seen their premiums double. The US desperately needs universal healthcare.

This system is going to collapse under its own weight. I think that if Trump wanted to do something popular, it would be to remove the penalty for opting out.

In Minnesota, the state passed a special rebate bill of $300 million to cover the increases for those who don’t qualify for federal subsidies.

http://www.twincities.com/2017/01/26/minnesota-senate-health-insurance-premium-relief-bill-heads-to-house/

too bad minnesota doesn’t have a sovereign currency, where is that money coming from? Great for the insurers, though, money they might not have otherwise gotten…

It’s coming from the State income. Do you have a problem with that?

how does the state get income?

The point of the question is to clarify if the same people being “helped” here will end up paying higher taxes to cover the costs of getting the “help”… or will they pay in the form of closed schools and libraries or some other crapification of public amenities, or will some other social group (those lower in the social hierarchy end up paying higher taxes to fund this slice of the population’s health insurance? Or—god forbid—will taxes be raised on the wealthy to cover the cost? The state has limited funds and this payment either represents some other, possibly vital, state service that will not get funded, or taxes being raised on at least some individuals or corporations within the state. Getting some clarification on where the money is going to come from is a great idea. Do you have a problem with that?

In 2014 I got a silver BCBS Illinois HMO policy with $450 premiums and $1800 deductible.

In 2017 I got a comparable silver BCBS North Carolina HMO policy with $1000 premiums and $3500 deductible.

The cost has effectively doubled over three years. Unlike Illinois, NC has only a single insurer in the ACA, but it is a better network, including the UNC system while in Chicago the top hospitals (University of Chicago, Northwestern, Rush) were not included.

But the maximum out-of-pocket including deductible is $7500 and I am having a knee replacement next month, for which everything — pre- and post-op appts, surgery, specialists, meds, hospitalization for two nights, outpatient physical therapy — will cost me only the unspent portion of my out-of-pocket. Guessing it may be around $5000 since I already paid for an initial visit to new PCP, appt with ortho including knee injections and x-rays, and have a colonoscopy scheduled for this week.

And any other care I get this year while still on Ocare will be at no cost to me beyond the premium, which I hope not to have to continue to pay once I have recovered and can get a job here (if the dueling bureaucracies of Illinois and North Carolina can ever get it together to get my professional license transferred).

Never knew it was that hard to get a license transferred in the US.

If you don’t mind me asking, what profession are you?

I myself am studying to be an accountant and get the Canadian equal to the CPA. Job market in Canada is awful though.

It depends on the State. I’m a licensed Geologist. Transferring between AZ and MN was merely a mild hassle. NV is too easy IMO, basically if you are licensed somewhere you’re good enough for them. Going from AZ+MN to WI wasn’t worth the hassle- apparently Walker doesn’t want any more.

CA has their own test and doesn’t take transfers at all.

Now going one step further, being a “qualified person” for mining documents requires a license, but not every State PG counts even though it did a few years ago. You have to get the particular state PG (I think CA or a few others) or a CPG from a professional organization like AIPG.

There’s my experience in licensing. I’m 100% sure that every other profession will have different results.

I am a licensed clinical social worker. I am certain that the current underfunding of everything contributes. Both bureaucracies have simplified their processes, in Illinois you can’t actually speak to the parties responsible for processing or even email them, and for both states everything has to be sent by snail mail.

And they won’t talk to each other. NC has received the verification of my current, valid Illinois license with state seal but they have a two-page questionnaire they request Illinois to fill out in addition, which Illinois WILL NOT DO. The other option would be to provide NC with a copy of the regulatory statutes governing licensing requirements AT THE TIME I WAS LICENSED – in 2000.

Well, after an internet search failed to find anything archived, I called the Illinois Board of Professional and Financial Regulation and they claim not to keep old copies of anything, and to be able only to access what is current, which was updated in 2007.

It has been a ridiculous nightmare. And turns out, others have had this problem. Alabama gave a friend of my mother’s – a teacher – such a hard time when she tried to transfer her license from Cali (legendary for higher standards for most professions than the rest of the country) that she gave up and became a school librarian instead.

so I’m trying to understand the actual numbers, you pay 12.000 in premiums, plus 3500 deductible, then another 4000 to cover your out of pocket then you don’t have to pay any more, is that correct? or am I including something that doesn’t count?

that is correct – total outlay 19.5k – not cheap, but my strategy is to have everything done (a second knee awaits) while covered – and i MAY qualify for a subsidy for the premiums but didn’t take one cuz dunno what job or when I will get here in NC

this only works if you really load up on procedures that would otherwise be quite expensive, and if you are fortunate enough to have assets (I liquidated 10k from an inherited retirement account or I couldn’t be doing this)

this is a case of sometimes if you can, other things besides $ matter. the whole reason I relocated (temporarily – am renting out my place in Chicago) is due to my mother’s declining health.

My non-ACA grandfathered plan went up 29% this year. It was still better (by 40%) than the cheapest Bronze plan in my area (which is blue). Double digit increases are a yearly event. Alas, the insurer has informed me that my plan cannot be continued, so options are limited now.

Altandmain

February 5, 2017 at 12:41 pm

Thanks for that – those are some good links Altandmain

“We conclude that a national average rate of premium increase is a fairly meaningless*** statistic since different markets are having very different experiences,” the report said.

“The focus of attention should be on understanding the wide variability by identifying the characteristics of markets that have experienced high premiums or high growth in premiums and of markets with lower premiums or lower growth in premiums.”

Only five states saw a decrease in premium cost this year, while 12 states had increases of more than 20%** ** on average. The states with the biggest changes are predominantly in the Midwest, but almost every region got hit with price jumps.

…

The paper also found that there was one player that had more of an effect on prices than any other provider.

“Those rating areas with a Medicaid insurer competing in the marketplace also have lower premiums and lower rates of increase than those regions without a Medicaid insurer competing,” Blumberg, Holahan, and Wengle said.

This is an issue as insurance companies evaluate the profitability of the state exchanges. With considerable political pushback against expanding Medicaid, private insurers will have to carry most of the load and provide competition.

2nd LINK

In eight states, regulators approved premiums that were a percentage point or more higher than carriers wanted, said Charles Gaba, a health data expert at ACASignups.net who analyzed the rates for USA TODAY. As of Tuesday, those states are Arizona, Pennsylvania, Colorado, Florida, Georgia, Kansas, Minnesota and Utah.

Pennsylvania regulators approved individual plan rate increases Monday of 33%, which is eight points higher than requested. Two insurers — Keystone Health Plan and Geisinger Quality Option — will also no longer offer plans on the ACA exchange for the state.

==============================================================

“The states with the biggest changes are predominantly in the Midwest, but almost every region got hit with price jumps.”

AND

“Pennsylvania regulators approved individual plan rate increases Monday of 33%, which is eight points higher than requested.”

I’m sure glad there were so many stories about rising health care premiums in the midwest and how that might affect the electoral college and hence the election…

AND

No wonder PA, a state I thought was the walliest of the blue wall, went for Trump…

*** Kudos for the authors understanding “aggregation” disease, the malady where economists smooth, average, and mediate problems away

** ** I’m so glad there is no inflation….

Basically people are not just more, they are paying for higher deductibles.

At this rate, only catastrophic coverage will be covered. Any other doctor appointments will be 100% out of pocket.

This it the 2017 BI article.

http://www.businessinsider.com/heres-how-much-obamacare-premiums-are-going-up-in-every-state-2016-10

Apparently Arizona has more than doubled its premiums this year.

Our premiums have doubled and deductibles have quadrupled since ACA.

. . . system is going to collapse under its own weight.

A Trump tweet some time ago—all remember.

Doubtless, he and his allies are doing more than thinking it be so.

[emphasis added]

Another variable to consider when looking at the reduction in enrollment: Insurers announced premium increases averaging about 25% in late October through November. The ACA enrollment period ended January 31. Could be as the deadline neared and people took a hard look at the premium increases, a large number of them simply said, “No more, I’m out.”

That was my calculation. My premium jumped from $410 to $505 in 2017 and I opted out of ACA. No can do. (Especially with no subsidy)

$800 for a well-woman visit. Something is wrong with this picture

Is that even accurate? I don’t think so.

It’s entirely possible if you don’t have negotiated rates. List price for my Quest tests are 6-8x my negotiated rates.

And that is the problem with not being on a plan: There is no discount from top-line billing rates. Never before have I had a plan that cost so much, yet didn’t pay ANYTHING until the (high) deductible was met. However, at least the doctor fees I have to pay now are not entirely unreasonable. And Labcorp, wow, how is Labcorp making any money at all doing complex tests for $9, or $0.51, etc as shown on my invoice while without my plan they would have cost hundreds. And the GI doc, ouch, they wanted a grand total of $14k for an upper and lower endoscopy. With the plan it was around $5k out of my pocket even though the insurance company didn’t pay a cent, let’s see, plus the $6k per year for the coverage, yep, it was worth having. Sick, sick system.

Hey, always good to read nakedcapitalism, thank you. I have a third principle of neoliberalism to add to Lamberts, works well:

1 You have money and I WANT it.

Original 2 Because markets

Original 3 Die faster

Paddlingwithoutboats

February 5, 2017 at 1:07 pm

Minor edit to improve accuracy

You have money and I TAKE it

‘FORWARD with the GOLLUM PLAN !!’

” I TAKES IT !!! ” …..” MY PRECIOUS “

Insurers to Congress: Stabilize Obamacare in next 30 days

Pity the poor insurers.

Just scroll down to the graphic of ins. co. CEOs’ increasing compensation.

https://www.peakprosperity.com/blog/106107/mad-hell

Even more galling when you consider the companies they run have, in essence, an administered income. They are an oligopoly and market a product most don’t have any alternative to buying. Hardly, then, demanding of cutting edge sales skills, commercial expertise, risk management or financial acumen. My mother in law’s cat could do the job, for the most part.

I went over to the Obamacare website, just checking out what they’ve done. Went to the “See Topics” page. There are five subheadings, each with four topics. There is another button there for “Browse All Topics”. There, it’s more like fifty individual topics, including demographics and other info specific to groups.

The website has all the character of filing taxes, an exercise that is frustrating, confusing, and dense. We know that the majority do not do their own taxes, in part because of complexity, with even less itemizing deductions, probably also due to complexity.

If Obamacare gets any more complicated, or gets more complicated as it inevitably becomes TrumpCare, and then 2020PresidentCare, and then who knows what, I expect “enrollment specialists” to crop up (if they haven’t already) who charge a premium to “help you maximize your healthcare enrollment”. Anyone else looking forward to the 2017th level of Bureaucratic Hell?

My guess is that Repubs will try to bury issue from public eye by emphasizing some national security threat in the headlines.

Let things fall apart, or break things a little more, and then say the disaster was a damn shame, but Obama’s fault, and we tried to warn you.

This will work.

No way will Repubs be held accountable, though many Bluedogs would love to sit back, watch disaster and TRY to blame Repubs.

The only way forward is a true Progressive plan to do something, and Dem primary challengers to carry that message.

That means campaigning in areas where the people disagree with Progressives on guns and other issues.

Who has the stomach to carry the flag and dare to be impure?

Rep. DeFazio (OR/D) has done that for many years, with minimal pushback. If the Dems were serious, they’d have him teaching workshops all around the country.

Why bother? Let people who vote for politicians who don’t want to have health care for poor people, not have health care for poor people.

It seems more sensible to have locally focused programs anyway.

If there was an ever a era of modern political endeavor where the maxim about roads to hell and good intentions fits, health care seems to be one.

Good intentions?

That’s a double edged sword with no handle. The “locally focused system” results in what we have now, red states and blue states both controlled by the corporate state. Besides you probably want to win the electoral college before deciding the losers get nothing and the rust belt gets less. Right now there’s someone somewhere thinking the same thing about you. You didn’t vote for the right guy, so who cares if you and yours suffer. Its just deserts.

Its amazing that the one, two, or multiple insurer coverage by county seem to largely follow state lines. It is almost as if the details of insurance issuance is regulated by the states, not the federal government. But that can’t be since all of the Affordable Care Act issues are because the federal government became all-powerful. If only states like Mississippi, Alabama, the Carolinas, Oklahoma, Arizona, etc. could exert more control over health insurance, then they too could get the power of healthy insurance markets.

The GOP really has a big problem on its hands, trying to figure out how to eliminate health insurance coverage either without people knowing about it or by blaming Obama for Executive Orders that got rid of their health insurance next year.

Rates ARE regulated by the states. But the ACA insurers are bleeding and the states can’t force them to lower their rates or the states will have NO insurers.

The problem with ACA is the pools have too many sick people. The best health insurance plan would have 320 million people in the pool.

In this world of belief in “free markets,” I would suspect the rate setting power hasn’t been used in decades, or has only been used to tell insurers to raise rates (I know personally of a case where that happened).

Rate approval and disapproval is sometimes a problem with the regulations and statues on the books for each individual state insurance regulator and not always a problem with political will and guts on the part of the regulator.

At the particular state insurance regulator I used to work as a financial regulator for, an increase was only able to be denied if actuarial review found that the proposed rates risked a financial problem to the insurer – and the guarantee fund. For the most part, rate denials were only able to be used when filed rates were too low. The state regulators could voice concerns and try to talk insurers down a bit, but were largely toothless. Regulatory power existed for little purpose other than to keep insurers solvent and use of guarantee funds low.

If only we could get rid of the too many sick people and “decrease the surplus population.”

Oh, then things would be groovy.

Yes, America, there is an effective, practical alternative: Medicare for All.

http://thehill.com/blogs/pundits-blog/healthcare/313407-medicare-for-all-use-formula-to-replace-aca

https://berniesanders.com/medicareforall/

Thanks, the Hill article is perfect calling out demodogs on why they aren’t pushing this hard. I guess they don’t want to upset their pay masters.

Nap time for me.

More cynical than that.

All they care about is getting re-elected.

They think they can use “blame the Repubs” to good advantage in the next election.

Until COSTS are contained, no amount of legislation will make a difference.

This. One free lunch per person at no more than X dollars is … a bribe to voters. Unlimited free lunches per person, with an ever increasing amount of money per lunch, paid for by somebody else (the Pool, the Pool) is … what? Lord Acton is right, democracy has self destructed perhaps.

Ahh, yes, the light appears…I’ve often wondered why only corporations are subject to monopoly codes. How about landlords, who in my city are able to raise the rent by any amount desired? As often as they wish, in month to month agreements. Prices tied to wages, perhaps…

The county level map doesn’t make sense to me. Clinton won every county but Essex County in Vermont but the map shows a sea of red for most of the state. What am I missing here?

Yes, the map shows the increase/decrease in repub vote, not who carried what counties. E.g,, the swing in my county from Obama to Trump was something on the order of 20%, so it’s darker red even though Trump only carried the county by 9%, Obama by 11%–equals 20%.

There are some ominous implications of maps of US Diabetes (and pre diabetes) rates with maps of Trump voters. https://gis.cdc.gov/grasp/diabetes/DiabetesAtlas.html

This CDC diabetes map represents a whole lot of people with chronic conditions. If ACA goes away, we’ll see (the lucky) half of the nation go Paleo, and the other half of the nation will be increasingly sick, and far less productive than they would be if their chronic conditions were managed.

ACA is far from perfect, but it did start to move toward paying for patient outcomes (rather than pay-for-service), and the implications of that have yet to play out.

You don’t have to go Paleo to prevent Type II diabetes, just keep your sugar intake reasonable.

And, Type 2 Diabetes can be reversed with a low carb high fat diet with intermittent fasting. A Toronto nephrologist, Jason Fung, MD, uses this protocol to treat his diabetic patients.

The Dems and their captive neoliberal writers keep talking to the wrong voters.

10 million people have exchange coverage. They’re not the ones who did or didn’t put Trump into office. It matters if they think their coverage sucks — nobody’s coverage should suck. But they’re not what’s driving the politics of health care.

The majority of all Americans — at least 156 million people — still get their coverage through their jobs. Their deductibles have increased six times faster than wages since Obamacare passed. The average deductible for single coverage is now more than $1,500 a year, in a country where the majority of people do not have $1,000 set aside to deal with a short term financial emergency. 31% of all Americans delayed or skipped needed care last year because of cost. Of course they’re not upset because a President and his party told them they’d be able to keep their health plan or doctor if they liked them, and then their out of pocket costs went through the roof, they probably changed carriers, and if they didn’t, their benefits have been cut and their network now excludes their doctors. Not angry at all. Wait. What?

KFF did a poll and found that people want Washington to do something about health care, but they don’t give a crap about “repeal.” They want their out of pocket costs controlled.

And in Washington, both parties are…….trying to tax the health benefits of people with employer-sponsored health insurance so that their out of pocket costs will continue to spiral upward. You know, “consumers” need “more skin in the game.” Dems = “Cadillac Tax”; Republicans = “cap on tax exclusion for health benefits (same thing)”.

All of it based on the idiotic belief that US costs are driven by overutilization. They’re not. It’s the prices.

This!

Best thing i’ve read all day.

Costs are ridiculous but overutilization is the big driver. No one ever gets much pushback when they recommend more testing or more surgery or more of something. I mean if the patient has a problem they must need more of something…….but if someone recommends less of something a lot of people are not happy…..including the patient and their family. Articles suggesting more care is not helping don’t get published. Articles pointing out that a particular surgery is useless in terms of outcome don’t get published. I don’t really understand the rationale that you use to determine that it is idiotic to believe that overutilization if the problem with US costs.

That might be your case, but I’ve had the unfortunate experience of not having the proper tests done- four times!

I have considerable, quite painful, and life threatening experience for underutilization that led or will lead to higher cost stuff required later. If you’ve ever walked around on a broken ankle, do it for three years and then tell me about overutilization.

Oh dear god would I like to see this overutilization you speak of.

Sorry, but that’s pure speculation based on kinda sorta feelings. Here’s actual data:

1. The US has the highest health care costs per capita in the entire developed world by far — two times the average, and 150% of the runner up.

2. The US already has the second highest out of pocket costs in the world after Switzerland, and again, the Swiss and us are both outliers with extreme out of pocket costs.

3. Americans see their doctors and go to the hospital LESS OFTEN than the average in the OECD — even if you eliminate the OECD’s poorer members.

4. Cooper et al studied 4 billion private sector claims from 88 million individual patients and found that hospital prices, not utilization drive cost differences between and within regions for privately insured patients. And the most powerful determinant of provider prices? Market power.

All of the vague cultural trends about the relationship between patients and providers that you cite are just that — vague feelings that this somehow can’t be right because patients aren’t acting as well-informed, ruggedly individualistic homo consumeris. But those cultural attitudes are common across the health care systems of all industrialized countries. Economists love to cite them because after all, if you draw the conclusion that our cost spiral is driven by hospital and pharmaceutical prices passed on to us by a private insurance industry that does absolutely nothing that the government can’t do better except extract rent, well, how in the hell are you going to get a corporate-funded think tank job or a grant for the institute at your University?

It’s idiotic to believe that overutilization is driving American health care costs because there aren’t any facts to substantiate the idea. Historically, there has been some evidence in Medicare data, but that’s a problem increasingly under control, and in the past few years research like the Cooper study has radically altered the analytic framework.

We really don’t use all that much health care. We just pay a ton of money for what we do use.

Most don’t know that health – along with life, liberty and property – was a fundamental human right for John Locke in the Second Treatise on Government:

“Being all equal and independent, no one ought to harm another in his life, health, liberty, or possessions.”

Numbers help?

Are these reasonable assumptions?

– Of the 92m 75% get premium support.

-Those getting support have 75% of the premium paid.

-Everybody gets a “Silver” plan. The average cost is $400/month.

-The premium support cost is $25b.

That is a small number. Trump could cover that cost by eliminating the carried interest shelter that hedge funds get. Trump said he was going to end the break.

Would you be okay with that outcome?

The average deductible on a Silver plan is $3,177.

That’s before you get to the issues of narrow networks, the exclusion of many specialists (by design, as a form of underwriting) and the fact that if you have an emergency, even if you are in a position to speak, just about no one will have the presence of mind to tell the driver: Take me only to XYZ Hospital, because I have insurance there. Indeed, I suspect many ambulances would refuse to go to a further away hospital, even if only marginally further away, for liability reasons.

And on top of that, even if you have a scheduled procedure, it is impossible to assure that your operating team will consist only of people covered by your plan, no matter how much of a stink you make.

Your numbers don’t get at those issues.

And, of course, even if you are conscious enough and persuasive enough to get your EMT to drive you to a network hospital, there’s no guarantee that the doctor/PA/APRN/physical therapist/subbed out lab, or other provider who treats you will be in network.

Patients are getting clobbered by “surprise bills” in the thousands and tens of thousands of dollars from out-of-network providers who treat them at nominally in-network facilities. The patients get billed for whatever their (increasingly lousy) insurance covers for out of network care (50% instead of 80%, for example, along with a much higher out of pocket maximum, if any max at all).

A number of states, CT, CA, NY and others have legislated against this practice, but it’s still devastating families.

Also, too, old data. 2017 average Silver deductible for individuals is now $3,572, with an out of pocket max of $6,449. For family coverage it’s $7,474 and $12,952,

Those are absurd numbers. And knocking them down through subsidies will not cut it. If you’re below 250% fpl, even with the subsidies you face bankruptcy, or at least falling way behind on rent/mortgage/utilities or incurring huge credit card debt to keep up with expenses if you get sick or hurt.

And again, the Silver plans are something of a distraction. Yes, the individual market is messed up, and Obamacare isn’t covering the small number of people who enroll each year — but the same dynamics are destroying coverage for people with job-based coverage.

The amount of ink (physical and digital) devoted to the stability of the exchanges is unforgivable from the perspective of accountable journalism, and politically suicidal for a party that claims the progressive mantle. The sometimes-stated assumption is that people with employer-sponsored coverage are more or less ok, and that we must focus maniacally on the potentially uninsured people now covered on the exchanges and through expanded Medicaid. Yes, they are important, and we should find a way to stop the rollback of that coverage.

But coverage is eroding for the majority at a breathtaking rate, and the entire cost-control theory behind both Obamacare and the GOP “replacements” has been constructed by the 21st-century equivalent of geocentric astronomers.

And the Paul Ryan solution is?

crickets?

I’m sorry, Yves, the Democrats just got defeated.

Can you bring your intelligence to bear on the non-existent Republican “alternatives.”

I admit it is fiction, since they have proposed no alternatives, but still, they will be bringing up the “reforms” such as they are.

I admit, expanding Medicare is the obvious option, but I would give that. . . . .

oh, about a 1% chance. Otherwise, what should the Republicans do–and what is your sense of the chance that they will actually do it?

Just to keep the conversation semi-real.

Although pointing out that the Republicans now own Obamacare after campaigning against it for 6 years may seem a radical proposition for blog commentary.

I know–they’ll expand Medicare! (Or, better, health savings account to pay for those ambulances!)

Ok – I’ll up it. I said that 75% of the 9.2m get subsidies on premiums of 75%. Now I will add an additional $2,000 per year as rebates on deductibles. That brings the max deductible to $100 a month. You have to be happy with that outcome.

I just added $14b to the annual cost. Now the fix is /- $40b. Still small beer. It is equal to what SS pays out ever two weeks.

You can respond about qualitative things like networks etc. I don’t care. The fact is one can “fix” the insurance problem for the 9.2m people with a manageable cost.

-WhiteyLockmandoubled

“All of it based on the idiotic belief that US costs are driven by overutilization. They’re not. It’s the prices”

During the run up to the ACA rollout, I said this to the University of Chicago geniuses, likely on pharma / health industry payrolls, at a conference downtown at the Raddison:

“You can’t lower health care costs without lowering prices, which Obamacare doesn’t do.”

He mumbled something about bending cost curves and outcome-based payments, and “improving” ACA, blah, blah, blah.

Having already gamed ACA, the health industry thugs were there to hijack the state’s Medicaid programs, converting into HMO and ACO’s (Accountable Care Organizations), slashing coverage, bloating admin staff and accountable to no one.

The entire goddamn purpose of the “health” industry is to take as much patient and taxpayer money as they can grab, straight out of the pockets of the sick and not-yet-sick.

It’s what they do

I think you are right about the pharma industry and the instrumentation industry but overall it is driven by overutilization and that is triggered by patient satisfaction demands and lawyers. Every patient wants an MRI scan for various aches and pains, most of which are either untreatable or self limited. Every patient with a headache is convinced they have a brain tumor. A doctor who orders more tests and referrals is never going to be criticized. A doctor who tries to order less will always be at risk. A lawyer with a back ached case after a car accident might be looking at 30,000 if there is no surgery. If he can get one of his doctors to do an instrumented spine fusion at astronomical cost he could be looking at a 500,000 settlement. I have more than once gotten calls from attorneys asking that I put in instrumentation so they can show the X-Rays at court. Coronary stents…….same story. Peripheral vascular stents…..on and on. End Stage oncology. Hepatitis C……we treat them for hundreds of thousands of dollars (pharma rip off) and then they shoot up and get infected again…..on the taxpayers dime. We know a lot of this stuff does not improve outcomes but the patients demand it. The patients are complicit. They know they will get SSI as well as a large cash settlement from worker’s comp or personal injury. It makes sense because the age group with degenerative conditions is the one that is getting hammered by our economy. When you have a choice between homeless on the street and income maintenance for life with Medicare you are going to go with the spine fusion, for example. The only solution would be to put doctors on salary and eliminate patient satisfaction. They should get the treatment the people that went to medical school think is effective and no more. Not going to happen no matter how much you rail at the industry which is complicit…….no doubt.

No it’s not. All of this is “might be” inferences about what “patients want” drawn from your anecdotes. Actual data in reply upthread. Respond with actual facts, please.

So are the Republicans going for Medicare for all as a solution to prices?

Nope. I didn’t think so.

I get a little tired about the fixation on Democrats as the problem, when the Repuglicans are going to reform Obamacare. Aren’t they? If not, why aren’t they all listening to you?

Hmmmm. What’s wrong with this picture on the blog commentary here?

I know—Healthcare accounts that are deductible! We’re all good with that, aren’t we? That will fix health care costs!

mumble, mumble, mumble, mumble.

Have I missed something about the Paul Ryan plan that is 6 years in ingestion and still to be born?

No, I don’t think I missed anything.

By the way, I’m fine with the Medicare for all, since all y’all think the Repuglicans are going to pass it, somehow and for some reason. What is the smoke of choice? I’d like some.

wow. Boy, really burned me there.

No, the Republicans aren’t going to pass Medicare for All, but then again neither are the corporate Democrats. What the corporate Democrats did was get the Urban Institute to put out an “analysis” of Medicare for All that was phonier than the Bowling Green massacre. Urban claimed that it would cost pretty much all the money in the entire country forever to implement, and probably eat your grandmother too, because they were in the tank for Clinton. Which will, in turn, allow the defenders of the left boundary of acceptable discourse at WaPo and NYT to ignore it as a policy option for another decade, and allow the national Democrats to continue collecting health care industry cash while posing as defenders of the middle class.

In the meantime, both parties want to tax employer-sponsored health care, which will radically increase the crisis of underinsurance among the majority of the US population. At a certain point, underinsurance is largely indistinguishable from uninsurance — if you have a $12,000 deductible and $10,000 in additional health care debt will drive you into bankruptcy, the line between uninsurance and underinsurance gets pretty thin.

Simply put, both parties will only deliver “reforms” that either hold harmless the three pillars of the system — insurance, hospitals, drugs — or allow them to expand profits . The Democratic approach was to tax (lower) middle class Americans disproportionately, shovel a trillion and a quarter dollars into the insurance industry’s maw and hope that they’d cover a few million people, all while standing by and doing zilch to make it possible for current job-based beneficiaries to afford health care.

The GOP wants to transition health care to a defined contribution system with high deductibles, which, not coincidentally, will allow the industry to collect premiums from people who will almost never use enough health care for the insurers to ever have to pay a claim. (and, no doubt, allow the hospitals to cash in on “value-based” payments that depend on low readmission rates, too).

They’re not the same. They’re not even equally bad. But they’re both pretty bad, and will continue to be so until there’s enough organizing to force the Democrats much further to the left.

“The entire goddamn purpose of the “health” industry is to take as much patient and taxpayer money as they can grab, straight out of the pockets of the sick and not-yet-sick.”

The entire purpose of the insurance industry is to take in the largest premiums possible and pay out the least benefits possible. Just ask the Oracle from Omaha.

Stanford professor of surgery Dr Robert Pearl writes in a recent column that US health care needs a wake up call from India:

In Bangalore, India, heart surgeons perform daily state-of-the-art heart surgery on adults and children at an average cost of $1,800. For the record, that’s about 2% of the $90,000 that the average heart surgery costs in the United States. And when it comes to the quality of the heart surgery, the patient outcomes are among the best in the world……

http://www.usatoday.com/story/opinion/2017/01/29/health-care-surgery-india-america-disruption-column/97056938/

As Karl Denninger writes so often, break the price fixing cartels of the entire healthcare-industrial complex and watch medical costs deflate.