Yves here. This sort of orthodoxy-reinforing narrative is deeply frustrating, particularly since the research side of the IMF, unlike the program side, often does very good work.

One of the big problem of reports like this is they never consider the question that income distribution is a function of political and social arrangements, and in particular, the rights of capital versus labor. It is hardly an accident that labor stopped sharing in the benefits of productivity gains in the mid 1970s, well before globalization and technology would have played much of a role. The big culprit was loss of labor bargaining power, which become official policy due to Volcker committing the Fed to creating more labor slack to keep inflation as close to his preferred target of zero as possible, and the Reagan/Thatcher “free market” fetish.

Now in fairness, some of the problems with a report like this are the difficulty of unpacking critical issues. For instance, as we’ve discussed regularly, the amount of offshoring of jobs that took place was considerably more than was justified by profit concerns. Direct factory labor is a small percentage of wholesale product cost; savings there are offset by greater managerial, finance, and transport costs, plus higher risks. In others words, offshoring and outsourcing are often, if not mainly, a transfer from low level workers to management rather than a bona-fide plus to the business. So while it is narrowly correct to say that globalization has been a big driver of middle class losses, analyses like that are misleading because they focus on proximate causes, not ultimate causes.

This report also misses another increasingly recognized driver of inequality, which is the lack of anti-trust enforcement which in turns leads to monopoly and oligopoly rent extraction. And it ignores a huge transfer from ordinary citizens to the capital-owning classes via subsidies. The banking industry is a huge example, where as we’ve written repeatedly, its operations are purely extractive (the cost of periodic crises greatly exceeds the value of the enterprises) and it enjoys such large subsidies that it should not be regarded as private enterprise. Banks should be regulated as utilities.

Similarly, an op ed in Links today describes the magnitude of subsidies extracted by WalMart: roughly $50 per American household per year. That is equivalent to 1/4 of its 2014 pre-tax profits, and an even higher percentage of its US pretax profits.

By Leith van Onselen. Originally published at MacroBusiness

From the IMF Direct blog comes an interesting analysis of the declining share of income going to workers, which is being driven by automation and globalisation:

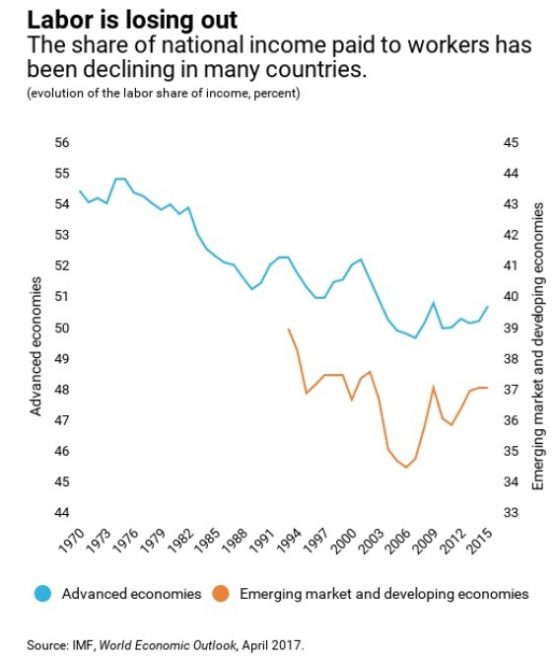

After being largely stable in many countries for decades, the share of national income paid to workers has been falling since the 1980s. Chapter 3 of the April 2017 World Economic Outlook finds that this trend is driven by rapid progress in technology and global integration.

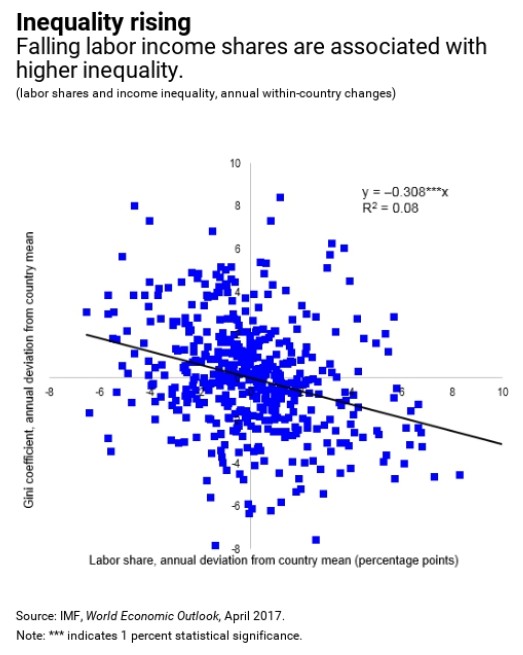

Labor’s share of income declines when wages grow more slowly than productivity, or the amount of output per hour of work. The result is that a growing fraction of productivity gains has been going to capital. And since capital tends to be concentrated in the upper ends of the income distribution, falling labor income shares are likely to raise income inequality…

In advanced economies, labor income shares began trending down in the 1980s. They reached their lowest level of the past half century just prior to the global financial crisis of 2008, and have not recovered materially since. Labor income shares now are almost 4 percentage points lower than they were in 1970…

Indeed, as growth remains subpar in many countries, an increasing recognition that the gains from growth have not been broadly shared has strengthened a backlash against economic integration and bolstered support in favor of inward-looking policies. This is especially the case in several advanced economies…

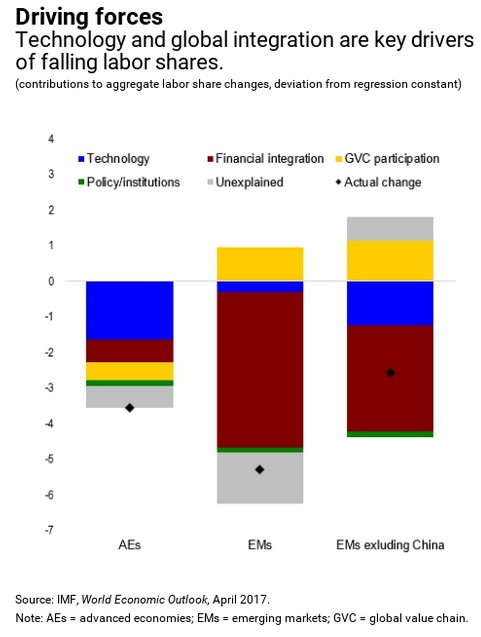

In advanced economies, about half of the decline in labor shares can be traced to the impact of technology. The decline was driven by a combination of rapid progress in information and telecommunication technology, and a high share of occupations that could be easily be automated.

Global integration—as captured by trends in final goods trade, participation in global value chains, and foreign direct investment—also played a role. Its contribution is estimated at about half that of technology. Because participation in global value chains typically implies offshoring of labor-intensive tasks, the effect of integration is to lower labor shares in tradable sectors… Taken together, technology and global integration explain close to 75 percent of the decline in labor shares in Germany and Italy, and close to 50 percent in the United States…

Another key finding of our research is that the decline in labor shares in advanced economies has been particularly sharp for middle-skilled labor. Routine-biased technology has taken over many of the tasks performed by these workers, contributing to job polarization toward high-skilled and low-skilled occupations.

This “hollowing-out” phenomenon has been reinforced by global integration, as firms in advanced economies increasingly have access to a global labor supply through cross-border value chains…

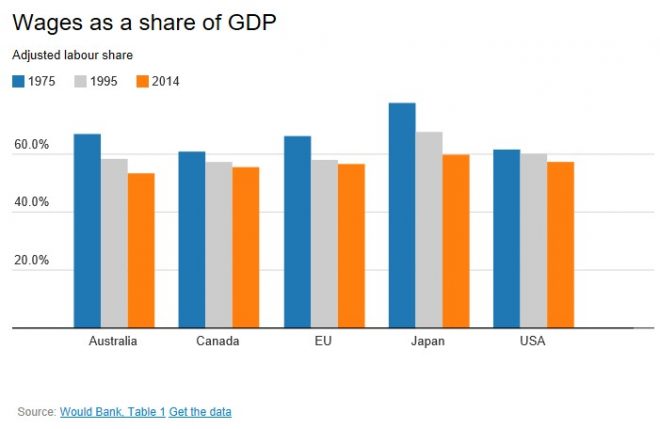

Sadly, Australian workers has fared badly against their Advanced Nation counterparts. As shown recently by Greg Jericho, Australia’s decline in wages’ share of GDP has been particularly steep:

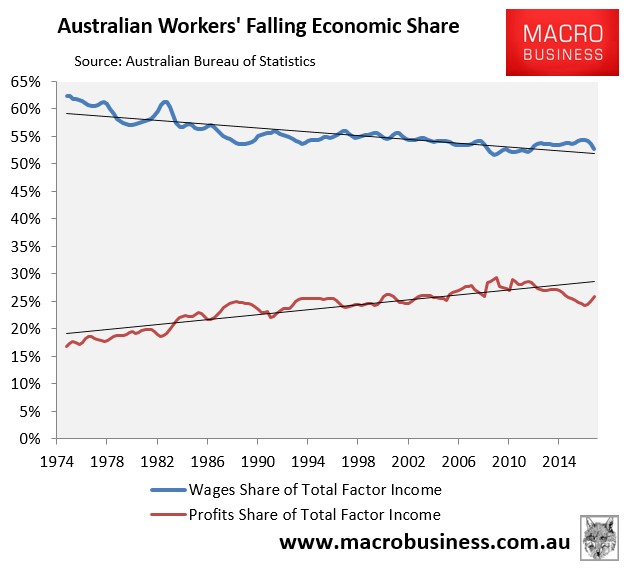

In 1975, two thirds of Australia’s GDP was in the form of wages, whereas in 2014 it was just 53%.

The below charts, which come from the ABS National Accounts, illustrates the decline in Australian workers’ shares.

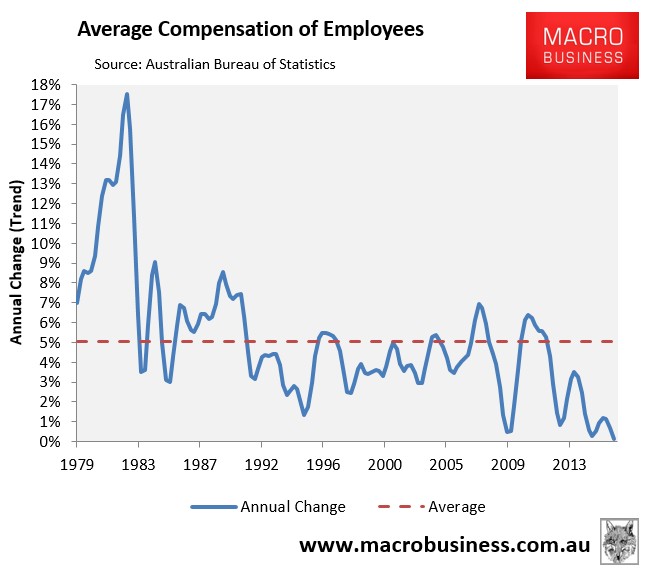

First, the growth in average employee earnings is the lowest on record:

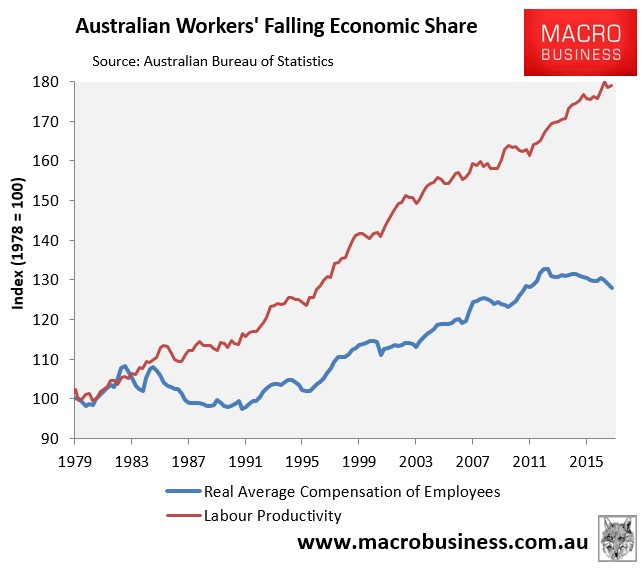

And has failed dismally to keep pace with growing labour productivity:

Meanwhile, the share of total factor income going to workers (as opposed to business owners) has been falling for decades:

While the elites continue to sell us the economic virtues of globalisation and mass immigration, the gains are flowing primarily to the wealthy owners of land and capital, who get to privatisation the gains and socialise the losses.

Ordinary workers, by contrast, have been largely left behind, experiencing weak income growth, rising debt levels, deteriorating housing affordability, worsening congestion, and overall declining livability.

These factors, above all others, help to explain the rise of fringe political movements like Brexit, Donald Trump, and One Nation at home. It’s a class war.

Bravo … thanks for paying attention to something that has been on-going since before the last quarterly report. You will never make it to executive management ;-)

Do you think that the IMF is celebrating this? Things have been going just fine for the 1% for my whole adult life. We don’t need a middle class, now that the Cold War kabuki is over … (cough, cough). Well maybe now that it is restarting (just another business-as-usual cycle?) it will be necessary to dangle a few carrots to keep the peasants happy.

readerOfTeaLeaves

Reread:

One of the big problem of reports like this is they never consider the question that income distribution is a function of political and social arrangements, and in particular, the rights of capital versus labor.

Once upon a time, I worked P/T in a bookstore. An old-fashioned, brick-and-mortar store with extremely knowledgeable employees, each of whom received a payment + (for F/T employees) modest medical and retirement benefits. None of us had ownership shares in the bookstore, which was fine as we were only there to earn some supplemental income.

When a customer bought a book, no information about them, their cash or cards, or other information was stored or kept. The value lay in the savvy of the bookstore owner in book selection, and the knowledge of the employees. No additional ‘capital’ — other than social and intellectual capital — was created from the transaction of the purchase of a book.

Along came the digital economy, which ‘informates’: it creates information about information.

Later, I worked at an online bookstore. Each digital transaction, arguably, creates capital — it ‘informates’ — by ‘creating information and storing details about the transaction of each book sale. In that economic model, I was given an infinestimal shard of ‘ownership’ in the store as an incentive to work hard. As things played out, my ‘capital’ was infinitely more valuable than my ‘labor’ in this scenario — not because it needed to be, but because as Yves as pointed out — the rules favor capital over labor, and even the IMF can’t seem to get their heads around how backward this is in a digital economy.

Capital was favored when people needed to build huge factories and mine ores – because those were the source of wealth.

Today, newer, potentially endless sources of wealth lie in creating ‘information about information’.

This process creates a new form of capital: databases of spending patterns, data tracking health parameters, data of weather patterns… all of that is ‘information about information’. This information is NOT constrained by scarcity; it is in fact the complete opposite — in this economy, wealth creation is created by the transactions themselves, which means that the actual consumers are the creators of new resources and wealth.

While it is true that you can’t eat data in the same way that you can eat fish, or grains, or eggs, when you apply outdated, early 19th century rules to an informating economy, you get what we see — an over reliance on debt, labor kicked to the curb and left in the gutter, and capital increasing astronomically in value by the day.

How does this IMF report explain the incredible valuations of LinkedIn or Uber?

It doesn’t.

It can’t, because it is not taking on the central problem of capital increasing astronomically in value over labor/consumer value that diverges exponentially by the month.

The inability of these economists to think through something as obvious or simple as ordering a book online, and the economic implications of that activity (who wins? who loses? who is taking risk?) is simply maddening after two decades of their inability to look at what lies in front of their noses, whether it is in a grocery store checkout that scans the bar codes to tally up their purchases, or a mobile app that tracks their steps each day.

And just to wrap up this rant, can the IMF explain to any of us why it is okay for Comcast to ‘own’ our data?!

Apparently not.

Comcast claims that its value lies in its network; it’s network is ‘capital’.

Some value lies there.

But a lot of new value lies in the data that network enables — however, Comcast is claiming that because their network created the conditions for new data to be created and moved, they therefore have an ownership claim on all that data. That’s either greed, or desperation, or pathology, or all three.

Comcast became so stupid and greedy that they think that they have the right to sell the data that their own customers created (!).

Comcast just became the Poster Company for Idiotic Economics — because they have destroyed trust, and in an informating economy, trust is a critical factor in wealth creation.

Anyone around here may hate Amazon, but no one can say that they sell their customer’s data.

Ditto Apple.

Why? They know that without trust, they have no business model as the world continues to informate.

Apparently, like Comcast, the IMF is also unable to decipher why or how trust is such a critical economic driver. They are documenting the destruction of trust, the fraying of social cohesion, and the implosion of economies, but they can’t seem to factor in the elemental problem of capital being exalted above labor, how bogus claims to capital are destroying value creation and feeding greed, and why that fundamental inequity is making things worse at an alarming rate.

Sorry for the rant, but this level of stupidity from such an exalted institution as the IMF really sets my hair on fire…

Anon

Love the rant. But what makes you think Amazon doesn’t sell (monetize) its customer database?

I imagine it likely uses the database to lure the secondary sellers to it’s website, or as an inducement to using its “cloud” services. Hell, user buying data is infinitely better than a statistical survey in assessing the psychology of the masses.

PKMKII

This process creates a new form of capital: databases of spending patterns, data tracking health parameters, data of weather patterns… all of that is ‘information about information’. This information is NOT constrained by scarcity; it is in fact the complete opposite — in this economy, wealth creation is created by the transactions themselves, which means that the actual consumers are the creators of new resources and wealth.

Here’s the giant begged (from the techlord PTB standpoint) question about this new, digital, “information about information” capital: Is it actually worth much of anything? Great, we can track exactly what time and what cash register Johnny Consumer bought his Vente-Frappa-Something at exactly which Starbucks because he used his smartphone to pay for it and the GPS logged the information when he did, but what good is that? Sure, it produces slightly better marketing information than if you just combined raw purchase data with focus group, but not enough to justify some of these crazy market values. And as more and more of this data gets dumped on the market, the less valuable it’s going to get and less worth it to pick through the garbage for anything useful.

readerOfTeaLeaves

You are asking the $64,000,000,000 question.

The quality of the data, including relevance at any given moment, is a key factor.

With that said, the IoT (Internet of Things) economy should shift plenty of things, and is directly relevant to today’s post on The Silver Economy IMVHO.

As for the ‘crazy’ market values, I completely agree.

But we all know that Wall Street seems to gush and preen over the pig with the most lipstick.

Cosmetics rule.

JTFaraday

Not if nobody has any money

sgt_doom

Yup, that almost last paragraph defines the entire picture:

“While the elites continue to sell us the economic virtues of globalisation and mass immigration, the gains are flowing primarily to the wealthy owners of land and capital, who get to privatisation the gains and socialise the losses.”

They globalize the wages downward (with the endless supply of labor: offshoring jobs and creating jobs offshore, insourcing foreign visa workers, refugees and undocumented workers; and, they globalize the cost of housing upwards, since there now exists all those foreigners who chose to buy housing in foreign lands of America, Canada, Germany, etc.

Last Protectionist Patriot

By the 1970s NIC imports were flooding into the US from Japan and its former colonial empire (S. Korea and Taiwan) not enough to turn the ENTIRE US into a smoking hellscape a la Youngstown, but enough to destroy numerous cities (Camden, Detroit, Cleveland). If you look at imports as a % of GDP and manufactured imports in particular, the 1970s is really when “globalization” takes off. Not enough to send wages plummeting downward a la 2000-2017, but certainly enough of a headwind to begin reversing fortunes for the least fortunate. Remember, American males with a HS diploma had their income peak in 1969, around the time of the moon landing….

The US and the West more generally held onto a reasonably high tariff regime (+20-30% import tax averages with a lot of variation) until the early 1970s. Then the US decided to throw away 200 years of protectionist prosperity so that the financial sector could gorge itself on giant capital surpluses (the flip side of current account deficits).

While I agree with your general point but it didn’t happen quite as quickly as you depict.

Japanese manufacturing was a joke in the 1960s but their big export push did start then and it si correct to say there were making good headway by the 1970s. There was a lot of handwringing in the US about Japan and Germany, particularly because their factories and infrastructure were newer than ours, and Detroit management was seen as particularly sclerotic. This paper, for instance, clearly states that Japan was not running large trade surpluses the US until the early 1980s:

But if you look at data, the big gains for the Japanese automakers was after Volcker killed inflation, in 1982. The US dollar shot to the moon, to the degree that even free market Ronald Reagan pushed through the Plaza Accord in 1985, which was a then IIRC G6 intervention to drive the yen up.

The US automakers lost enormous market share in 24 months and never got it back. The 1980s were also the era of the big Japanese electronics-makers incursion into the US.

And S Korea was nowhere in the 1970s. It was only running a trade surplus with the US of $1 billion as of 1979.

The 1980s were also the era of the big Japanese {Insert Industry Here}………

————————————-

Also everything in the capital equipment industry – electrical, mechanical, machine tool…you name it.

One that sat on my face back then was Mitsubishi Heavy Industries – The corporate parent, Mitsubishi, Inc. was at that time 8 times the size of General Electric!

Left in Wisconsin

Two things happened at the same time in the late 70s and early 80s:

1. US Dollar went way up, making Japanese imports less expensive

2. Quality AND productivity of Japanese manufactured goods/production went way up (Toyota Production System).

Ford commissioned a study in early 80s and determined that Toyota had a cost advantage of $2000 on at $12000 car, partly in productivity, partly in overvalued currency. From that point on, all new auto construction, and most manufacturing, globally (Korea, China) has been based on TPS principles. But US has had surplus capacity for the last 35 years, and retrofitting old plants for an entirely different organization of production can be problematic.

sgt_doom

Thanks, and that is a most important point: Japanese quality and ease of use, and GE couldn’t even begin to compete with Japan (compare the Sony Walkman to the GE knockoff in the last 1990s, early 2000s, etc.) similarly with autos, etc., and GE’s response was simply to offshore as many jobs as possible, and morph into a private equity firm/hedge funds, with some manufacturing — they still only now exist due to those TARP bailout funds they accessed.

Meanwhile, today we are treated to the cheaply made, low quality Chinese goods, of a different nature altogether.

Disturbed Voter

The move from the international gold standard in 1971 to the international petroleum standard changed everything. The US had already internally devalued in 1933 and 1965, with the loss of the internal gold standard and the internal silver standard. Under conditions of 1971 … the Cold War meant that the ends justified the means (very convenient for tyrants of all sorts). Politically the failure of the LBJ administration left the door open to systematically reverse every US rule since 1933, and return us to the paleo-conservativism of the 1920s. And that is exactly what proceeded. That is why market valuations now resemble 1929 much more than 1969. So a matter of Cold War economics (US vs Vietnam and vs France) and deliberate reactionary elitism. Given the context and the political ideology of the Nixon and post-Nixon administrations … could we have done anything different?

Left in Wisconsin

My two cents is that corporate elites are always looking for ways to change the equation/increase the advantage over working people, and take their opportunities when they get them. The divisions among working people in the late 60s and 70s (in many respects children vs their parents) were a big problem. (The failure of labor law reform in 78 was a big tell that labor power had waned.) But is wasn’t until the Japanese “made” big unionized US industry hopelessly uncompetitive in the early 80s that the die was cast. (That’s a manufacturing pun.)

There were real serious calls on the labor/left for the development of a US ‘industrial policy’ to redevelop US industry in the mid 80s. But by then any power was already lost.

sgt_doom

I think you summed it up most excellently!

BeliTsari

Maybe, a MONSTER ate them! At least, it’s being hotly debated in retrospect? While, somehow… magically, media, governments, academic sociology & economics mavens seem to have totally misplaced the “working class,” right around that period where we deplorables went from making, inventing, building… if not actually selling too much; to flipping burgers, guarding abandoned factories, and selling each other child-slave-shop junk, crack, crank & diacetylmorphine, imported from romantic, far off lands. http://www.zerohedge.com/news/2017-01-24/protected-privileged-establishment-versus-working-class well, we smelled kinda funny, anyhow?

Gman

Great, succinct, erudite piece.

After all these years I STILL find it extraordinary and depressing in equal measure how so many people still have brass neck to try and explain away and justify the way things are as though there is some Darwinian inevitability about it all.

Labour has been purposefully and systematically devalued in favour of Capital by those uniquely placed to do so.

This this could not have been achieved so completely without the institutional abuse of the debt based, fractional reserve banking system, complicit, venal, self-serving financial and political elites and the increasingly globalised, financialised system that some still persist on referring to as ‘the free market.’

John Wright

Yet another influence is the USA’s military and State Department that help remove risk for private companies when they move manufacturing operations and conduct business overseas.

The entire “fighting to defend our way of life” seems to always result in another military action, a military action that may make some nations (Japan, South Korea) crave military support from the USA or keep others swapping oil for military hardware/support (Saudi Arabia).

We had many “liberal” Americans falling in behind and supporting a deeply flawed Presidential candidate who pushed for destabilizing Honduras, LIbya and Syria, advocated stirring up more trouble in other parts of the Middle East (Iran) and eastern Europe AND even provided cover for the financial industry.

Both the Republican and Democrat elite are with the program as it has worked well for them, but not for the 40% of USA citizens now registered independent.

The median lifestyle in the USA could be improved if the MIC were downsized by 50% and a peace dividend paid to the American worker..

As you assert, the system is designed to function this way, there is no Darwinian inevitability about it.

Gman

Agreed.

We should be hearing a helluva a lot more about attempts to improve median incomes, rather than the mostly meaningless house price, stock market and GDP growth hype that is so often deployed only to flatter to deceive.

‘40% registered as independent’

At least that represents a glimmer of hope.

readerOfTeaLeaves

+1

Katharine

+

Globalization=Oz (pay no attention to the man behind the curtain)

Moneta

At the end of the 60s early 70s, we got the signal that the developed world was consuming too much energy per capita vs. the rest of the world and we needed to change. Great imbalances do not last forever.

But the general population did not see any of this. It wanted to believe there was always more.

So our choices were:

1. cut our consumption

2. or keep on going plus getting the entire world to consume like us.

Believing in the powers of technology and eternal planetary bounty we opted for the second choice.

But if there are indeed physical limits on this planet, the second option is bound to fail us.

To fight this global redistribution of energy and resources, the developed world used debt. And now it wants to default on it so as to keep its current share of resources and energy. However, if it does this, we can expect a lot more anger from the developing world as well as developed countries fighting to all keep their undeserved share.

So if energy and resource consumption needed to start coming down in the 70s and never did, the rising wealth discrepancy is to be expected. It just becomes a game of musical chairs.

jefemt

Musical chairs on the deck of the Titanic….

Thanks for sharing the article, and your insightful introduction. These are frustrating times.

craazyman

Social Science presses forward like a personal pleasure item into the dark recesses of global reality — headlights on and camera recording Harried Reams (no pun intended) of data.

When you’ve got two dimensions, you have to use both of them!

Eustache de Saint Pierre

I do agree that in the UK at least some of the outsourcing was almost just for the hell of it, & I do know of cases where products sold with a quality label lost business, as consumers became aware of the fact that they were paying premium prices for often inferior items manufactured in the Far East.

I once worked as a trainee manager for a fairly large manufacturing company & as part of this I was involved in cost accounting as it was then called. The obsession it appeared to me was with direct labour costs, whereas the overhead which was continually rising was completely ignored.

The company a few years after I left despite outsourcing eventually went bust, with it’s products being bought for basically nothing by a competitor which for various reasons including design investment is still going strong to this day.

A friend of mine was involved in a stock take of their patterns before it actually closed. He remarked that the place was empty of all workers except for the still virtually intact management & a few others kept on to serve their needs. One of the biggest assets that had to cleared was around seventy fleet cars, many being top of the range models.

I have since then come across similar examples.

Left in Wisconsin

In my experience, much internal cost accounting is biased against in-house work. Labor hours were always the denominator, so as soon as outsourcing begins, costs/labor hour climb because the denominator shrinks. Here in the US, it can get really bad because employers like to lump all labor costs, including pensions, into the numerator. So the first bit of outsourcing starts the inevitable downward slide. Back when I did this kind of thing, I tried to get employers to understand that there were fixed and variable components to labor costs (past pension costs are sunk costs) just like with other costs, but they invariably said the labor costs were by definition variable so that was that.

But, of course, management is (fixed) overhead, not labor cost.

Eustache de Saint Pierre

If I remember correctly there were around 4,000 shop floor workers, mainly women on piece work. The outsourcing & the lay-offs were a gradual process which ended up with nothing other than middle & top management, who it appeared to me were stuck in the 1930’s – 50’s.

They invested next to nothing in R&D or design, but jumped at the new marketing craze by employing a so called whizz kid who had been successful in a totally different industry. This was during a time when this company & others had ” Investing in People ” emblazoned on every possible piece of company literature.

They eventually went down the pan with many others like them, swallowed up by larger outsourcers. I think marketing has it’s place but not as a replacement for a well designed product & to be honest I lean towards Bill Hicks on the subject.

This once thriving industrial area where this occurred was a major supporter of Brexit, which is probably of no surprise.

Henry

Maybe we need to entertain the idea that the IMF has now started engaging in active befuddlement of the causes of current inequality just like the tobacco industry did. After all it has been documented that economists did do this just after 2008

Susan the other

Agnotology at the IMF. Sounds right. The IMF is us. And we are a military empire. Still – even though the TPP failed. The TPP was a contract for the Pacific Rim to accept our protection. Buy our weapons. And all we asked was for certain patent protections. The IMF can’t be this vacuous. Gee, duh IMF. Here’s the real thought experiment: Is the solution to fatuous economic analysis to simply automate everything including analysts and then, using automation create an economy that supplies us all with “money” to keep the system going? Or?

Jonathan

This is why capitalism is getting a bad rep. But, to that I say, “What capitalism?” Capitalism doesn’t exist in the US anymore, it hasn’t for a while now. We have a huge social welfare state and safety net along with countless government guarantees and subsides (lets not mention bailouts). And because of that, we all see a reduction in our standards of living. Along with an over-sized government, we have a Federal Reserve destroying the value of our currency. When Ben Bernanke launched the first QE what did he say was its intended purposes? To raise asset prices. I ask you this, who owns the majority of stocks, real estate, and other securities? It’s not your local mom and pop, it’s the wealthy individuals. So thanks, in large part, to the Fed we have the value of our currency being wiped out and thus, increasing the price of assets. This is why we have a disintegrating middle class. If we wish to restore prosperity we must resurrect capitalism and let it reign.

Uwotm8

Sorry, I just checked the IMF report, and it appears that in your 3rd graph (“Driving Forces”) you switched Value Chain Participation with financial integration – the red block is value chain participation, yellow is finance (original report Fig. 3.13/2). Which funnily enough has a positive impact on the wage share in developing countries (as stated in the IMF Report), the danger being that this might be used to actually exculpate finance from being resposible for inequality – which it appears to be if you don’t look at the wage share but at income distribution. Which the IMF obviously doesn’t.

This is not “my third graph”. That graph is from the IMF Direct blog.

Uwotm8

Well, then the IMF can’t keep its graphs straight. In the PDF version these two components are switched, and the accompanying text confirms the positive effect of financial integration (chapter 3, p. 16, see http://www.imf.org/~/media/Files/Publications/WEO/2017/April/pdf/c3.ashx). I only noticed because I was actually interested in the role of finance specifically, and it doesn’t change the story about globalisation overall.

salmo trutta

Not so. Secular strangulation is a late 1950’s theory. And it’s universally mis-interpreted. Economics is a science. Everything has been predicted. Everything happened exactly as outlined. And it’s both simple – but also confusing and contradictory.

Ask yourself: If banks create new money [loans + investments = deposits], then how do they, as public enemy #1, the ABA says: simultaneously loan out the non-bank public’s pooled savings placed with them?

Fractional reserve (or prudential reserve), banking is a function of the velocity of centralized bank deposits (based on payments, clearings, & settlements). From the standpoint of the commercial banks and the entire macro-economy, the monetary savings practices of the public are reflected in the velocity of their deposits and not in their volume. Whether the public saves or dissaves, chooses to hold their savings in the commercial banks or to transfer them to non-bank conduits, will not, per se, alter the total assets or liabilities of the commercial banks, nor alter the forms of these assets and liabilities.

Any institution whose liabilities can be transferred on demand, without notice, & without income penalty, via negotiable credit instruments (or data pathways), & whose deposits are regarded by the public as money, can create new money, provided that the institution is not encountering a negative cash flow.

From the accounting of the system, commercial banks (DFIs), as contrasted to financial intermediaries (non-banks, NBFIs): never loan out, & can’t loan out, existing funds in any deposit classification (saved or otherwise), or the owner’s equity, or any liability item.

When DFIs grant loans to, or purchase securities from, the non-bank public, they acquire title to earning assets by initially, the creation of an equal volume of new money (demand deposits) – somewhere in the banking system. I.e., the DFI’s bank deposits are the result of lending, not the other way around.

From a System’s standpoint, time deposits represent savings that have a payment’s velocity of zero. Commercial bank held savings are un-used and un-spent. Bank-held savings are lost to both consumption and investment, indeed to any type of payment or expenditure.

As long as savings are impounded and ensconced within the confines of the commercial banking system, they are idled. The savings held in the commercial banks, in whatever deposit classification, can only be spent by their owners; they are not, & cannot, be spent by the banks.

It couldn’t be clearer. From a system standpoint, TDs constitute an alteration of bank liabilities, their growth does not per se add to the “footings” of the consolidated balance sheet for the system. They obviously therefore are not a source of loan-funds for the banking system as a whole, & indeed their growth has no effect on the size or gross earnings of the banking system, except as their growth affects are transmitted through monetary policy.

Bravo … thanks for paying attention to something that has been on-going since before the last quarterly report. You will never make it to executive management ;-)

Do you think that the IMF is celebrating this? Things have been going just fine for the 1% for my whole adult life. We don’t need a middle class, now that the Cold War kabuki is over … (cough, cough). Well maybe now that it is restarting (just another business-as-usual cycle?) it will be necessary to dangle a few carrots to keep the peasants happy.

Reread:

Once upon a time, I worked P/T in a bookstore. An old-fashioned, brick-and-mortar store with extremely knowledgeable employees, each of whom received a payment + (for F/T employees) modest medical and retirement benefits. None of us had ownership shares in the bookstore, which was fine as we were only there to earn some supplemental income.

When a customer bought a book, no information about them, their cash or cards, or other information was stored or kept. The value lay in the savvy of the bookstore owner in book selection, and the knowledge of the employees. No additional ‘capital’ — other than social and intellectual capital — was created from the transaction of the purchase of a book.

Along came the digital economy, which ‘informates’: it creates information about information.

Later, I worked at an online bookstore. Each digital transaction, arguably, creates capital — it ‘informates’ — by ‘creating information and storing details about the transaction of each book sale. In that economic model, I was given an infinestimal shard of ‘ownership’ in the store as an incentive to work hard. As things played out, my ‘capital’ was infinitely more valuable than my ‘labor’ in this scenario — not because it needed to be, but because as Yves as pointed out — the rules favor capital over labor, and even the IMF can’t seem to get their heads around how backward this is in a digital economy.

Capital was favored when people needed to build huge factories and mine ores – because those were the source of wealth.

Today, newer, potentially endless sources of wealth lie in creating ‘information about information’.

This process creates a new form of capital: databases of spending patterns, data tracking health parameters, data of weather patterns… all of that is ‘information about information’. This information is NOT constrained by scarcity; it is in fact the complete opposite — in this economy, wealth creation is created by the transactions themselves, which means that the actual consumers are the creators of new resources and wealth.

While it is true that you can’t eat data in the same way that you can eat fish, or grains, or eggs, when you apply outdated, early 19th century rules to an informating economy, you get what we see — an over reliance on debt, labor kicked to the curb and left in the gutter, and capital increasing astronomically in value by the day.

How does this IMF report explain the incredible valuations of LinkedIn or Uber?

It doesn’t.

It can’t, because it is not taking on the central problem of capital increasing astronomically in value over labor/consumer value that diverges exponentially by the month.

The inability of these economists to think through something as obvious or simple as ordering a book online, and the economic implications of that activity (who wins? who loses? who is taking risk?) is simply maddening after two decades of their inability to look at what lies in front of their noses, whether it is in a grocery store checkout that scans the bar codes to tally up their purchases, or a mobile app that tracks their steps each day.

And just to wrap up this rant, can the IMF explain to any of us why it is okay for Comcast to ‘own’ our data?!

Apparently not.

Comcast claims that its value lies in its network; it’s network is ‘capital’.

Some value lies there.

But a lot of new value lies in the data that network enables — however, Comcast is claiming that because their network created the conditions for new data to be created and moved, they therefore have an ownership claim on all that data. That’s either greed, or desperation, or pathology, or all three.

Comcast became so stupid and greedy that they think that they have the right to sell the data that their own customers created (!).

Comcast just became the Poster Company for Idiotic Economics — because they have destroyed trust, and in an informating economy, trust is a critical factor in wealth creation.

Anyone around here may hate Amazon, but no one can say that they sell their customer’s data.

Ditto Apple.

Why? They know that without trust, they have no business model as the world continues to informate.

Apparently, like Comcast, the IMF is also unable to decipher why or how trust is such a critical economic driver. They are documenting the destruction of trust, the fraying of social cohesion, and the implosion of economies, but they can’t seem to factor in the elemental problem of capital being exalted above labor, how bogus claims to capital are destroying value creation and feeding greed, and why that fundamental inequity is making things worse at an alarming rate.

Sorry for the rant, but this level of stupidity from such an exalted institution as the IMF really sets my hair on fire…

Love the rant. But what makes you think Amazon doesn’t sell (monetize) its customer database?

I imagine it likely uses the database to lure the secondary sellers to it’s website, or as an inducement to using its “cloud” services. Hell, user buying data is infinitely better than a statistical survey in assessing the psychology of the masses.

Here’s the giant begged (from the techlord PTB standpoint) question about this new, digital, “information about information” capital: Is it actually worth much of anything? Great, we can track exactly what time and what cash register Johnny Consumer bought his Vente-Frappa-Something at exactly which Starbucks because he used his smartphone to pay for it and the GPS logged the information when he did, but what good is that? Sure, it produces slightly better marketing information than if you just combined raw purchase data with focus group, but not enough to justify some of these crazy market values. And as more and more of this data gets dumped on the market, the less valuable it’s going to get and less worth it to pick through the garbage for anything useful.

You are asking the $64,000,000,000 question.

The quality of the data, including relevance at any given moment, is a key factor.

With that said, the IoT (Internet of Things) economy should shift plenty of things, and is directly relevant to today’s post on The Silver Economy IMVHO.

As for the ‘crazy’ market values, I completely agree.

But we all know that Wall Street seems to gush and preen over the pig with the most lipstick.

Cosmetics rule.

Not if nobody has any money

Yup, that almost last paragraph defines the entire picture:

“While the elites continue to sell us the economic virtues of globalisation and mass immigration, the gains are flowing primarily to the wealthy owners of land and capital, who get to privatisation the gains and socialise the losses.”

They globalize the wages downward (with the endless supply of labor: offshoring jobs and creating jobs offshore, insourcing foreign visa workers, refugees and undocumented workers; and, they globalize the cost of housing upwards, since there now exists all those foreigners who chose to buy housing in foreign lands of America, Canada, Germany, etc.

By the 1970s NIC imports were flooding into the US from Japan and its former colonial empire (S. Korea and Taiwan) not enough to turn the ENTIRE US into a smoking hellscape a la Youngstown, but enough to destroy numerous cities (Camden, Detroit, Cleveland). If you look at imports as a % of GDP and manufactured imports in particular, the 1970s is really when “globalization” takes off. Not enough to send wages plummeting downward a la 2000-2017, but certainly enough of a headwind to begin reversing fortunes for the least fortunate. Remember, American males with a HS diploma had their income peak in 1969, around the time of the moon landing….

The US and the West more generally held onto a reasonably high tariff regime (+20-30% import tax averages with a lot of variation) until the early 1970s. Then the US decided to throw away 200 years of protectionist prosperity so that the financial sector could gorge itself on giant capital surpluses (the flip side of current account deficits).

And so the US destroyed itself in one generation!

While I agree with your general point but it didn’t happen quite as quickly as you depict.

Japanese manufacturing was a joke in the 1960s but their big export push did start then and it si correct to say there were making good headway by the 1970s. There was a lot of handwringing in the US about Japan and Germany, particularly because their factories and infrastructure were newer than ours, and Detroit management was seen as particularly sclerotic. This paper, for instance, clearly states that Japan was not running large trade surpluses the US until the early 1980s:

http://www.repository.law.indiana.edu/cgi/viewcontent.cgi?article=1007&context=ijgls

But if you look at data, the big gains for the Japanese automakers was after Volcker killed inflation, in 1982. The US dollar shot to the moon, to the degree that even free market Ronald Reagan pushed through the Plaza Accord in 1985, which was a then IIRC G6 intervention to drive the yen up.

The US automakers lost enormous market share in 24 months and never got it back. The 1980s were also the era of the big Japanese electronics-makers incursion into the US.

And S Korea was nowhere in the 1970s. It was only running a trade surplus with the US of $1 billion as of 1979.

http://www.nytimes.com/1979/07/02/archives/seoul-aims-to-increase-us-trade-exports-to-us-restricted-seoul.html

The 1980s were also the era of the big Japanese {Insert Industry Here}………

————————————-

Also everything in the capital equipment industry – electrical, mechanical, machine tool…you name it.

One that sat on my face back then was Mitsubishi Heavy Industries – The corporate parent, Mitsubishi, Inc. was at that time 8 times the size of General Electric!

Two things happened at the same time in the late 70s and early 80s:

1. US Dollar went way up, making Japanese imports less expensive

2. Quality AND productivity of Japanese manufactured goods/production went way up (Toyota Production System).

Ford commissioned a study in early 80s and determined that Toyota had a cost advantage of $2000 on at $12000 car, partly in productivity, partly in overvalued currency. From that point on, all new auto construction, and most manufacturing, globally (Korea, China) has been based on TPS principles. But US has had surplus capacity for the last 35 years, and retrofitting old plants for an entirely different organization of production can be problematic.

Thanks, and that is a most important point: Japanese quality and ease of use, and GE couldn’t even begin to compete with Japan (compare the Sony Walkman to the GE knockoff in the last 1990s, early 2000s, etc.) similarly with autos, etc., and GE’s response was simply to offshore as many jobs as possible, and morph into a private equity firm/hedge funds, with some manufacturing — they still only now exist due to those TARP bailout funds they accessed.

Meanwhile, today we are treated to the cheaply made, low quality Chinese goods, of a different nature altogether.

The move from the international gold standard in 1971 to the international petroleum standard changed everything. The US had already internally devalued in 1933 and 1965, with the loss of the internal gold standard and the internal silver standard. Under conditions of 1971 … the Cold War meant that the ends justified the means (very convenient for tyrants of all sorts). Politically the failure of the LBJ administration left the door open to systematically reverse every US rule since 1933, and return us to the paleo-conservativism of the 1920s. And that is exactly what proceeded. That is why market valuations now resemble 1929 much more than 1969. So a matter of Cold War economics (US vs Vietnam and vs France) and deliberate reactionary elitism. Given the context and the political ideology of the Nixon and post-Nixon administrations … could we have done anything different?

My two cents is that corporate elites are always looking for ways to change the equation/increase the advantage over working people, and take their opportunities when they get them. The divisions among working people in the late 60s and 70s (in many respects children vs their parents) were a big problem. (The failure of labor law reform in 78 was a big tell that labor power had waned.) But is wasn’t until the Japanese “made” big unionized US industry hopelessly uncompetitive in the early 80s that the die was cast. (That’s a manufacturing pun.)

There were real serious calls on the labor/left for the development of a US ‘industrial policy’ to redevelop US industry in the mid 80s. But by then any power was already lost.

I think you summed it up most excellently!

Maybe, a MONSTER ate them! At least, it’s being hotly debated in retrospect? While, somehow… magically, media, governments, academic sociology & economics mavens seem to have totally misplaced the “working class,” right around that period where we deplorables went from making, inventing, building… if not actually selling too much; to flipping burgers, guarding abandoned factories, and selling each other child-slave-shop junk, crack, crank & diacetylmorphine, imported from romantic, far off lands. http://www.zerohedge.com/news/2017-01-24/protected-privileged-establishment-versus-working-class well, we smelled kinda funny, anyhow?

Great, succinct, erudite piece.

After all these years I STILL find it extraordinary and depressing in equal measure how so many people still have brass neck to try and explain away and justify the way things are as though there is some Darwinian inevitability about it all.

Labour has been purposefully and systematically devalued in favour of Capital by those uniquely placed to do so.

This this could not have been achieved so completely without the institutional abuse of the debt based, fractional reserve banking system, complicit, venal, self-serving financial and political elites and the increasingly globalised, financialised system that some still persist on referring to as ‘the free market.’

Yet another influence is the USA’s military and State Department that help remove risk for private companies when they move manufacturing operations and conduct business overseas.

The entire “fighting to defend our way of life” seems to always result in another military action, a military action that may make some nations (Japan, South Korea) crave military support from the USA or keep others swapping oil for military hardware/support (Saudi Arabia).

We had many “liberal” Americans falling in behind and supporting a deeply flawed Presidential candidate who pushed for destabilizing Honduras, LIbya and Syria, advocated stirring up more trouble in other parts of the Middle East (Iran) and eastern Europe AND even provided cover for the financial industry.

Both the Republican and Democrat elite are with the program as it has worked well for them, but not for the 40% of USA citizens now registered independent.

The median lifestyle in the USA could be improved if the MIC were downsized by 50% and a peace dividend paid to the American worker..

As you assert, the system is designed to function this way, there is no Darwinian inevitability about it.

Agreed.

We should be hearing a helluva a lot more about attempts to improve median incomes, rather than the mostly meaningless house price, stock market and GDP growth hype that is so often deployed only to flatter to deceive.

‘40% registered as independent’

At least that represents a glimmer of hope.

+1

+

Globalization=Oz (pay no attention to the man behind the curtain)

At the end of the 60s early 70s, we got the signal that the developed world was consuming too much energy per capita vs. the rest of the world and we needed to change. Great imbalances do not last forever.

But the general population did not see any of this. It wanted to believe there was always more.

So our choices were:

1. cut our consumption

2. or keep on going plus getting the entire world to consume like us.

Believing in the powers of technology and eternal planetary bounty we opted for the second choice.

But if there are indeed physical limits on this planet, the second option is bound to fail us.

To fight this global redistribution of energy and resources, the developed world used debt. And now it wants to default on it so as to keep its current share of resources and energy. However, if it does this, we can expect a lot more anger from the developing world as well as developed countries fighting to all keep their undeserved share.

So if energy and resource consumption needed to start coming down in the 70s and never did, the rising wealth discrepancy is to be expected. It just becomes a game of musical chairs.

Musical chairs on the deck of the Titanic….

Thanks for sharing the article, and your insightful introduction. These are frustrating times.

Social Science presses forward like a personal pleasure item into the dark recesses of global reality — headlights on and camera recording Harried Reams (no pun intended) of data.

When you’ve got two dimensions, you have to use both of them!

I do agree that in the UK at least some of the outsourcing was almost just for the hell of it, & I do know of cases where products sold with a quality label lost business, as consumers became aware of the fact that they were paying premium prices for often inferior items manufactured in the Far East.

I once worked as a trainee manager for a fairly large manufacturing company & as part of this I was involved in cost accounting as it was then called. The obsession it appeared to me was with direct labour costs, whereas the overhead which was continually rising was completely ignored.

The company a few years after I left despite outsourcing eventually went bust, with it’s products being bought for basically nothing by a competitor which for various reasons including design investment is still going strong to this day.

A friend of mine was involved in a stock take of their patterns before it actually closed. He remarked that the place was empty of all workers except for the still virtually intact management & a few others kept on to serve their needs. One of the biggest assets that had to cleared was around seventy fleet cars, many being top of the range models.

I have since then come across similar examples.

In my experience, much internal cost accounting is biased against in-house work. Labor hours were always the denominator, so as soon as outsourcing begins, costs/labor hour climb because the denominator shrinks. Here in the US, it can get really bad because employers like to lump all labor costs, including pensions, into the numerator. So the first bit of outsourcing starts the inevitable downward slide. Back when I did this kind of thing, I tried to get employers to understand that there were fixed and variable components to labor costs (past pension costs are sunk costs) just like with other costs, but they invariably said the labor costs were by definition variable so that was that.

But, of course, management is (fixed) overhead, not labor cost.

If I remember correctly there were around 4,000 shop floor workers, mainly women on piece work. The outsourcing & the lay-offs were a gradual process which ended up with nothing other than middle & top management, who it appeared to me were stuck in the 1930’s – 50’s.

They invested next to nothing in R&D or design, but jumped at the new marketing craze by employing a so called whizz kid who had been successful in a totally different industry. This was during a time when this company & others had ” Investing in People ” emblazoned on every possible piece of company literature.

They eventually went down the pan with many others like them, swallowed up by larger outsourcers. I think marketing has it’s place but not as a replacement for a well designed product & to be honest I lean towards Bill Hicks on the subject.

This once thriving industrial area where this occurred was a major supporter of Brexit, which is probably of no surprise.

Maybe we need to entertain the idea that the IMF has now started engaging in active befuddlement of the causes of current inequality just like the tobacco industry did. After all it has been documented that economists did do this just after 2008

Agnotology at the IMF. Sounds right. The IMF is us. And we are a military empire. Still – even though the TPP failed. The TPP was a contract for the Pacific Rim to accept our protection. Buy our weapons. And all we asked was for certain patent protections. The IMF can’t be this vacuous. Gee, duh IMF. Here’s the real thought experiment: Is the solution to fatuous economic analysis to simply automate everything including analysts and then, using automation create an economy that supplies us all with “money” to keep the system going? Or?

This is why capitalism is getting a bad rep. But, to that I say, “What capitalism?” Capitalism doesn’t exist in the US anymore, it hasn’t for a while now. We have a huge social welfare state and safety net along with countless government guarantees and subsides (lets not mention bailouts). And because of that, we all see a reduction in our standards of living. Along with an over-sized government, we have a Federal Reserve destroying the value of our currency. When Ben Bernanke launched the first QE what did he say was its intended purposes? To raise asset prices. I ask you this, who owns the majority of stocks, real estate, and other securities? It’s not your local mom and pop, it’s the wealthy individuals. So thanks, in large part, to the Fed we have the value of our currency being wiped out and thus, increasing the price of assets. This is why we have a disintegrating middle class. If we wish to restore prosperity we must resurrect capitalism and let it reign.

Sorry, I just checked the IMF report, and it appears that in your 3rd graph (“Driving Forces”) you switched Value Chain Participation with financial integration – the red block is value chain participation, yellow is finance (original report Fig. 3.13/2). Which funnily enough has a positive impact on the wage share in developing countries (as stated in the IMF Report), the danger being that this might be used to actually exculpate finance from being resposible for inequality – which it appears to be if you don’t look at the wage share but at income distribution. Which the IMF obviously doesn’t.

This is not “my third graph”. That graph is from the IMF Direct blog.

Well, then the IMF can’t keep its graphs straight. In the PDF version these two components are switched, and the accompanying text confirms the positive effect of financial integration (chapter 3, p. 16, see http://www.imf.org/~/media/Files/Publications/WEO/2017/April/pdf/c3.ashx). I only noticed because I was actually interested in the role of finance specifically, and it doesn’t change the story about globalisation overall.

Not so. Secular strangulation is a late 1950’s theory. And it’s universally mis-interpreted. Economics is a science. Everything has been predicted. Everything happened exactly as outlined. And it’s both simple – but also confusing and contradictory.

Ask yourself: If banks create new money [loans + investments = deposits], then how do they, as public enemy #1, the ABA says: simultaneously loan out the non-bank public’s pooled savings placed with them?

Fractional reserve (or prudential reserve), banking is a function of the velocity of centralized bank deposits (based on payments, clearings, & settlements). From the standpoint of the commercial banks and the entire macro-economy, the monetary savings practices of the public are reflected in the velocity of their deposits and not in their volume. Whether the public saves or dissaves, chooses to hold their savings in the commercial banks or to transfer them to non-bank conduits, will not, per se, alter the total assets or liabilities of the commercial banks, nor alter the forms of these assets and liabilities.

Any institution whose liabilities can be transferred on demand, without notice, & without income penalty, via negotiable credit instruments (or data pathways), & whose deposits are regarded by the public as money, can create new money, provided that the institution is not encountering a negative cash flow.

From the accounting of the system, commercial banks (DFIs), as contrasted to financial intermediaries (non-banks, NBFIs): never loan out, & can’t loan out, existing funds in any deposit classification (saved or otherwise), or the owner’s equity, or any liability item.

When DFIs grant loans to, or purchase securities from, the non-bank public, they acquire title to earning assets by initially, the creation of an equal volume of new money (demand deposits) – somewhere in the banking system. I.e., the DFI’s bank deposits are the result of lending, not the other way around.

From a System’s standpoint, time deposits represent savings that have a payment’s velocity of zero. Commercial bank held savings are un-used and un-spent. Bank-held savings are lost to both consumption and investment, indeed to any type of payment or expenditure.

As long as savings are impounded and ensconced within the confines of the commercial banking system, they are idled. The savings held in the commercial banks, in whatever deposit classification, can only be spent by their owners; they are not, & cannot, be spent by the banks.

It couldn’t be clearer. From a system standpoint, TDs constitute an alteration of bank liabilities, their growth does not per se add to the “footings” of the consolidated balance sheet for the system. They obviously therefore are not a source of loan-funds for the banking system as a whole, & indeed their growth has no effect on the size or gross earnings of the banking system, except as their growth affects are transmitted through monetary policy.