Maybe I am getting a bit burned out. I almost took a night off because I couldn’t get worked up as I normally do about the stories du jour.

Yes, Chuck Prince is expected to resign on Sunday. I’m surprised he lasted this long. He was over when he made his now-infamous remark:

When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing.

Mind you, this wasn’t pre-March 2007, when everything looked rosy. This was in July, when the cracks had started to appear and after the Bear hedge fund crisis. That sort of comment is a hubristic death wish, a willful defiance of the warnings. And the odds most assuredly caught up with Prince.

But for my money, the juicier bit in the Wall Street Journal story on Prince’s imminent departure is that Citi may take further writedowns:

People familiar with the matter said the Securities and Exchange Commission is looking into the bank’s accounting for its off-balance sheet investment funds that have recently attracted scrutiny…..

The board is expected to discuss whether Citigroup should update the amount of write-downs that it has taken on certain securities to reflect their deteriorating value, according to people familiar with the matter.

The issue has generated intense discussion in the bank’s senior ranks in recent days and could potentially result in a significant addition to the $3.55 billion capital-markets hit to third-quarter earnings that Citigroup announced just three weeks ago. The company is expected to file a quarterly report with the SEC next week.

Citigroup is the largest player in the $350 billion SIV market, managing seven of these off-balance sheet vehicles that hold a combined $80 billion in assets. SIVs have issued short-term debt to investors such as money-market funds while buying mortgage-backed securities and other assets that carry a higher yield.

“Citi is confident that its SIV accounting is proper and in thorough accordance with all applicable rules and regulations,” said Christina Pretto, a bank spokeswoman.

The SEC’s review of Citigroup is in the early stages, people familiar with it said. The result could range from no action to a referral to the agency’s enforcement division. The SEC is also taking a broad look at how brokerage firms valued assets tied to high-risk mortgages and whether they were timely in their disclosure of losses to investors, people familiar with the matter say.

There has also been surprisingly little discussion of the lack of bench depth at Citi and Merrill. Prince was a weak choice for CEO. For example, Sallie Krawcheck, the former CFO, now head of wealth management, has been given what amount to battlefield promotions. She may be talented enough to pull it off, but she does not have a depth of managerial experience (her stint at as the head of the newly constituted Smith Barney cum research and brokerage operation was relatively brief). Similarly, Vikram Pandit, the new head of investment banking, is undeniably able, but is now supervising some important businesses that lie outside his trading-area expertise.

To Merrill. Bloomberg claims that Stan O’Neal’s exit package is one of the five largest and is stoking Congressional ire. However, the proposed measures, to give shareholders more say on pay, is certain to have no impact. Diffuse and largely disenfranchised owners are no match (save when enough team up to wage an effective proxy battle) for comp consultants and craven boards who are nominated by management and therefore beholden.

As for the bombshell that Merrill may have parked securities with hedge funds to delay the reporting of losses, the Financial Times reports that there may be nothing untoward about Merrill’s actions:

Experts said that, without further details, it was hard to determine how such a transaction would have differed from a standard commercial paper funding arrangement, other than that it involved a hedge fund. Hedge funds are not typically buyers of commercial paper.

Many banks which underwrite collateralised debt obligations use off-balance sheet vehicles in which to hold the underlying mortgage-backed securities.

The vehicles are funded by issuing commercial paper for which the banks often provide so-called liquidity back-ups. This means the banks commit to buy the paper if other purchasers cannot be found when it comes due.

“It looks just like selling commercial paper with a liquidity facility,” said an analyst at a rating agency.

Whether the Journal’s charges are borne out, we still have the other Merrill eruption, namely, the Deutshce Bank estimate that it still have losses to take of $10 billion:

Merrill Lynch & Co. fell the most in six years, leading financial stocks lower for a second day, after Deutsche Bank AG said the world’s biggest brokerage may write down an additional $10 billion for losses on subprime assets.

“We have increasingly lost confidence in the financials of Merrill,” Deutsche Bank analyst Michael Mayo said in a report today. “Merrill may have additional credit rating downgrades” should the New York-based firm be forced to write down the value of its debt holdings, Mayo said.

I assume that Bloomberg misquoted Mayo. Merrill can’t possibly have $10 billion in losses on subprimes. since it has only $5.7 billion remaining. However, it has $15.2 billion in CDOs, and having almost assuredly sold the better ones (that’s how it generally goes in a deteriorating market), the rest looks plenty vulnerable, particularly with CDO downgrades being announced by the rating agencies. We had guesstimated that next quarter losses could exceed $7 billion, and Mayo’s figures are plausible.

Other observers suggested the alleged transaction might have involved the hedge fund buying the underlying assets with a guarantee from Merrill that they would be bought back in a year’s time at a set price. One expert said that on the surface this resembled a standard “repo” funding arrangement.

Similarly, we could have written about one of our favorite topics, phony government stats, but that has been ably covered elsewhere. The 3.9% GDP release was a complete crock, and Barry Ritholtz jumped on it right away:

At the risk of sounding shrill, I am compelled to point out the quantum bogosity of this 3.9% GDP number: It is highly dependent upon a rather suspect reading of Price Increases/Indexes for Gross Domestic Product: The Price Deflator rose a much less than expected .8% vs expectations of 2%.

The increase in real GDP in the third quarter reflected positive contributions from personal consumption expenditures (PCE), exports, federal government spending, equipment and software, nonresidential structures, private inventory investment, and state and local government spending that were partly offset by a negative contribution from residential fixed investment. Imports, which are a subtraction in the calculation of GDP, increased.

The slight acceleration in real GDP growth in the third quarter primarily reflected accelerations in PCE and in exports that were partly offset by an upturn in imports, a larger decrease in residential fixed investment, and a deceleration in nonresidential structures.

Price Indexes for Gross Domestic Product was an astounding low 0.8% (Table 4). In other words, this report benefited as much from higher inflation as it did from true growth.

I obviously take issue with that (as Crude Oil crosses $94 for the first time).

To highlight the impact that this 0.8% price gain had on the reported REAL GDP: that 0.8% gain matches a level last seen in 1998; prior to that, the previous deflator gain of .8% was n 1963.

Similarly, the non-farm payrolls report Friday, which showed an increase of 186,000, was also rubbish. As Michael Shedlock tells us:

The overall numbers look OK on the surface but once again the devil is in the details.

Manufacturing shed another 21,000 jobs this month and continues to lose jobs every month.

Government added 36,000 useless workers.

Leisure and hospitality (typically very low paying jobs) added 56,000 jobs.

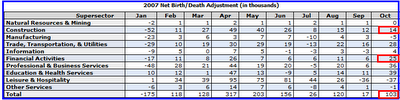

But we get back to our usual culprit, the birth-death model, which is a statistical plug to allow for job gains or losses at businesses either so newly created or folded as to not show up in the stats. It has been a source of dubious adjustments for months running. Back to Shedlock:

The BLS has shown a net gain of jobs added to new businesses in both construction and financial activities nine consecutive months from February through October.The BLS is assuming not only that jobs were added, but that new unaccounted construction businesses were created in this environment where business capex spending has been weak, housing has been horrid, and over 170 lenders have gone out of business or stopped writing loans since last December as per the Mortgage Lender Implode-O-Meter.

Clearly this is reporting from an alternate universe.

A note of caution: One cannot take the birth death adjustments and subtract them from the reported numbers because one set of numbers is seasonally adjusted and the other is not.

Finally, we have been following what so far appears to be an underrreported story, namely, the tsuris of the mortgage guarantors, which include AAA so-called monoline insurers like Ambac and MGIC (see here and here). Elaine Meinel Supkis, who is eccentric, conspiracy minded (which appeals to me even when she is wrong, although she is most often right), and obsessive in her trolling for information, has a very lengthy and very good post, “Bond Insurers Are Going Bankrupt Now.” This is going to be important, and her entire post is worth reading. Some excerpts:

Credit derivative traders are valuing bond insurers Ambac Financial Group (ABK.N: Quote, Profile , Research) and MBIA Inc (MBI.N: Quote, Profile , Research) as deep junk credits, while their stock prices have also plunged on concerns the companies may need more capital to shore up their high ratings.

Credit default swaps on Ambac have surged to around 620 basis points, or $620,000 per year for five years to insure $10 million in debt, from 185 basis points a month ago, according to data provided by CMA DataVision.Its shares have tumbled nearly 60 percent since the beginning of October, 41 percent this week alone.

Ambac and MBIA both reported third-quarter losses last week caused by their writing down the market value of their respective credit derivative portfolios, which are used to insure assets including residential mortgages against default.

This is a major failure. This is deep beneath the surface of the waters, like the Titanic ripping its hull underwater, these organizations we will visit tonight are similar: they are the hull of the banking system. They are the ones who are supposed to protect the banking system from failure and they are now failing, themselves. This is serious…..

Knowing this background, it is time to look at the effects of this major banking collapse which is bigger, I think, than the previous 3 banking collapses I have seen in the past.

href=”http://news.yahoo.com/s/ft/20071102/bs_ft/fto110120072249061435;_ylt=Ajn8QQhKv6OkXw4APDGfuFb2ULEF”>CDS traders warn of ‘blood on streets’Bond insurers, or monolines, were also hit hard.

“[These triple-A rated companies are] exposed to the crumbling housing market,” said Gavan Nolan, an analyst at derivatives data provider Markit. “Investors in monolines will be waiting for the coming months of housing data with trepidation,” Mr Nolan said. CDS on MBIA Insurance rocketed to a four-year high, of 345bp, CMA Datavision said.Last week the insurer posted $36.6m net loss and halted its share buy-back programme. Contracts on the bond insurance unit of Ambac Financial climbed to a five-year high of 310bp. Gimme Credit, an independent research term, downgraded both MBIA and Ambac this week.

When the AAA rating is dropped, this means one has to pay a higher interest rate because one looks more and more like the bastard sons of Miz Risky, that wench, that wild female who sleeps around and parties all the time and who goes to Vegas at the drop of her panties, no one trusts Risky or her children! But all speculators love her to death. Insurance groups that are supposed to be hedging banks and lenders can’t afford to look like Risky’s kiddies, they have to appear sober and clean, not drunk and staggering about the place. But who is going to replace these organizations that messed up?

First, I would suggest they never had insured these CDOs and tranches in the first place. Like Moody’s and others who also decided they wanted to play footsie with Risky, these guys threw caution to the winds and embraced an obvious old whore and kissed her and got the cooties. Yuck. Well, serves them right!

You have to love someone who has the nerve to write like that.

One day the market players are going to wake up, smell the coffee, as they say, and we will see some 1000 point down days. It will all be downhill after that.

Am I right that in this case “insurance” is repackaging with an extra bit of “enhancement”?

Yves:

Take a long weekend, get a good night’s sleep, re-read a favorite book – but then come back refreshed and keep blogging!

– Constant reader

Yves,

Can’t thank you enough for this blog. Along with CR the best on the web!

BTW, on Sally Krawcheck — she has very little mgmt experience. Her stint as head of brokerage at Sanford Bernstein lasted just a year, and she was best remembered for staffing up in tech research just before the crash. As CFO she released reserves to make Citi’s numbers, which given the credit troubles brewing at the time was irresponsible.

Amazing that such giant firms can be managed with so little depth of talent.

Yves your blog is terrific, please take care of yourself (and don’t burn out).

That said, guys, I think you’re all wet! This is what we know for sure:

Government is always the problem.

Regulation is Bad.

Lowering taxes is the best thing to do to solve any problem.

(I’m a Republican, can you tell?)

So, all we need to do is cut back on all banking and finance regulations, tell Paulson to keep his nose out of the pot (and Bernanke to stop with those pesky mortgage regulations) and then, a big round of tax cuts for the rich as chaser.

If we do all this, trust me, CDO, SIV, subprime – all these problems will be history.

Party on!

Another avid and daily reader here. Take a few days off, we can wait… I’d rather see you return refreshed and eager than get burnt out and blog along unwilling.

To David Pearson or other: Forgive me, but please provide a link to the CR blog. Thanks.

Yves: Great, great blog. Hang in there.

To all: Chuck Prince is out. Wasn’t Rubin supposed to be a guardian angel of sorts to the company? What happened? If he doesn’t take charge now, can they justify keeping him in place?

Dear anonymous:

Here’s CR – get thee hence!

http://calculatedrisk.blogspot.com/

Anon of 9:05 AM,

The problem with these bloody CDO deals is you can’t get the documents through Edgar, but I am pretty certain that the insurers don’t play a role in structuring (although they would have to be consulted as to what their price would be to make sure the deal structure works). But keep in mind that they aren’t the only game in town. Overcollateralization and credit default swaps were the other common ways to credit enhance structured finance deals.

But the impairment of the monolines in particular would be a big deal, since they also provide guarantees on municipal bond deals, and there aren’t as many alternatives there.

Anon of 11:42 AM,

Thanks for the tidbits on Krawcheck. I was going largely on instinct (her experience vs. what those big jobs entail) so appreciate the intelligence. I did see her back when she was at Bernstein as a mere Wall Street industry analyst. She was a great analyst and very charismatic. This may be a case of Peter Principle in action.

Anon of 1:26 PM,

Someone will probably do a story on the gory details of Prince’s demise. But you are right, Rubin is quite a mystery. He is a master politician, and was probably unwilling to continue to back a losing horse.

I have been told by old Citibankers that Weill destroyed the culture. It had been very entrepreneurial, with profit centers that had a lot of autonomy if you followed the rules and delivered good results (of course, Citi sometimes didn’t have enough rules, but that’s another story). Weill was a micromanager and drove a lot of talent out.

Prince clearly did not have the right background, even though that wasn’t evident on paper. Working under Weill meant he had had limited authority. And with Weill having effectively gutted the management ranks, he didn’t have enough strong subordinates to shore him up.

There is also a question as to whether Citi is too big and in too many businesses to be managed properly. A buddy who used to work at Citi at a very senior level and is an expert on board/leadership issues argues that big diversified financial firms need co-heads at the top, because there are too many businesses that require expert knowledge for one person to have enough scope.

It is so hard to make the co-head thing work that it says to me these firms are too broad (in econ-speak, they have diseconomies of scope).

Yves

1) To second Anon’s comments above: both Merrill and Citi suffered from wholesale sackings at executive levels after 2001. You don’t need talent and experience in bull markets-any ‘bright sparks’ will do nicely. Downturns call for ‘steady hands’…unfortunately, there are v few people left who fit this description

2) Pls take some time off; recharge. Apres vous, le deluge!

CrocodileChuck

Yves,

Please don’t feel a need to get worked up before you blog. Some of us don’t come for the indignation, we come for the analysis and insight emitted by that excellent mind of yours.

Truth is, we don’t really want to be edified, we just want to understand things and maybe have a clearer notion of what’s going to happen tomorrow.

Un gran abrazo Yves… y mas que gracias por su trabajo

Juan de la O

Yves:

A few comments on your comments, leaving Rubin for last.

When Travelers merged with Citicorp, the result was a giant company with two cultures.

Weill had created the Travelers culture, which was all about financial results, leading ultimately to enhanced shareholder value. Compensation too, but a lot of that compensation was in the form of shares. Weill more or less forced his people to buy as many shares as they could, and he let it be known that they were not to sell them, ever.

In the Travelers culture, you cut to the chase, did what needed to be done as quickly as possible, shook things up, innovated, and attacked inertia wherever you saw it.

At Citicorp, John Reed “controlled the logic” but let his people implement it. It was a combination of innovation and enrepreneurship on the one hand and a formal, genteel, old-fashioned banking culture on the other. Many Citibankers were downright anal in their observance of rules, procedures, and precedents.

But in exchange for your cautious and prudent devotion to the Citicorp way of doing things, you were a respected member of a club. It was a privilege that was earned. You were not only allowed to have a life, the company wanted you to have a good life. You had generous benefits, vacation time, personal time if needed, reasonable hours, comfortable surroundings, genteel colleagues.

Sandy dismantled the Citicorp culture. Whether that culture could have survived or should have is debatable, but Sandy and the Travelers guys (and gals) took charge, and their corporate culture was imposed on the whole.

Sandy had the ability to be a micromanager, but not necessarily the time, by definition. He seemed to know more about everyone’s operation than they did. But they knew he didn’t have time to do everything and that he needed them to run their businesses themselves.

Until Sandy handed the CEO title to Chuck, he had not actually driven a lot of talent out at the highest level. While Sandy was the sole CEO, the only possible example that comes to mind is Jay Fishman, but I don’t think Sandy drove him out. Fishman left to take charge of another company, and I think he knew or suspected that things would play out as they have, his company merging with the divested Travelers and him as Chairman and CEO. And Fishman probably didn’t like his odds or the timeline for succeeding Sandy.

Otherwise, Weill had a very deep bench at the top. This included Chuck Prince, Bob Willumstad, Todd Thomson, Bob Druskin, Mike Masin, Tom Jones, Mike Carpenter, Derek Maughan, Marge Magner, Victor Menezes, Sally Crawcheck, Ajay Banga, and others.

The great loss of bench strength has occurred since Prince became CEO. Those departing have included Willumstad, Thomson, Masin, Jones, Carpenter, Maughan, Magner, Menezes, and others. To an extent this was not surprising, given that some of these executives had stayed on in the hope of succeeding Weill or working closely with whoever did. But there is the appearance that some of these executives were eliminated because they were possible alternatives to Prince.

Prince had the right background to clean up the reputational mess that arose during the late nineties and after, which I honestly think occurred on Sandy’s watch without him quite realizing it was happening. But while Prince was cleaning up that mess, he did not recognize the financial reality of what Citigroup was doing in certain areas.

I think Rubin should have protected Citigroup from those things. If he warned Chuck and the board about what is now happening, then he did his job, and he’s golden as usual. But if not, why not? Did he not see it? Hard to believe.

I’m with you on the co-head idea: forget it.

Is Citigroup unmanageable? The question is only meaningful if life as we know it goes on for some time to come. If the financial system, the economy, and perhaps society in general are on the brink of disaster, then who cares?

If life goes on, I say there are only a few people who can manage Citigroup, and those people might indeed decide to break it up, or at least shed the Wall Street piece. One of those people is Bob Rubin, even if the company’s current troubles escaped his notice as they developed. After all, he doesn’t run the company, and as far as one can tell, the terms of his employment do not make him accountable for the company’s performance.

I admire Rubin and would like to see him take charge of Citigroup. I see it reported now that he is “reluctant” to take the job. That’s quite different from what he told the Times five years ago, namely that he “would not” be Citigroup’s CEO.

Maybe they’ll bring Willumstad back. They could do a lot worse. I see some news about his current company this weekend as well.

We’ll know more soon.

– Anon of 1:26 PM (yesterday)

Anon of 1:26 PM,

Thanks for the thoughtful comment. Weill was undoubtedly a smart acquirer and built a talented core team, but whether it was the right team for Citigroup is an open question.

One thing that is hard to reconcile, and to his credit, Weill was able to do it to some degree, was reconcile the commercial banking and investment banking cultures.

I had Citi as a client a long time ago, ironically in its money markets division (later some other trading ops and an investment banking unit), which was as close as it got to a securities operation and got as close to Wall Street as you could get in a bank in those days (example: to the consternation of all, Wriston gave the head of the MMD the second highest comp in the bank, which put him way out of line relative to his formal rank, which was really contrary to commercial banking practice).

The cultures of banking and securities businesses are radically different because the nature of the underlying businesses are different (we’ll for the moment exclude the trading operation of banks).

People in securities firms get/have to make decisions, some many in a day, that have bottom line impact. So who you hire and promote, MIS, risk controls, and incentives are very important. Managers typically supervise relatively few people, and supervising is less valued than producing.

Banking, by contrast, is about control repeatability, processes. Only fairly senior people make decisions that can affect the bottom line. That’s why a systems guy like Reed was so successful. And ability to manage large groups of people is prized.

It’s ironic that you call Citi clubby. Compared to Travelers, that may be true, but Ciiti was the most aggressive and innovative bank by a considerable margin. It pushed all the regulatory boundaries, invented swaps, caps, and collars, had (and may still have) one of the biggest and most successful international operations. Having worked with other banks, its staff was smarter and much harder working by a considerable margin than the norm.

In fact, Citi’s tendency to be aggressive has gotten it repeatedly in trouble. It was front and center in the sovereign debt crisis of the 1970s, nearly went under in the S&L crisis, and now has the SIV and God knows what other messes.

As for Rubin, you are right that if he was Prince’s sponsor he should have coached him better, But remember that Rubin was co-head of Goldman in a very different era. He was co-COO from 1987 to 1990, and co-chief from 1990-1992. The firm went through its first major downsizing then, which was hugely traumatic and seen as a violation of the culture. Although the firm had a solid fixed income operation, that had not become the huge business that it became in the 1990s. Even though Rubin was a risk arb, the kind of risk analysis you do in that field is vastly simpler than what you do in more complex instruments (and does not require higher math).

So that is a long-winded way of saying that Rubin might not have fully appreciated the risks either until they were already evident.

Duh, This should have occurred to me earlier:

Why is Prince leaving now? He clearly could have hung on if he wanted to. There is some speculation as to nefarious things that will come out soon, others saying that he was doing the mature thing, that the handwriting was on the wall.

Alternative theory: the powers that be want Thain if they are going to have to have a new CEO. So Prince had to go once O’Neal was toast.

Both Rubin and John Reed have close relationships with him.

There may have been fear that Merrill would succeed in getting him if they waited too long. And Thain is far and away the best candidate. He ran a substantial mortgage-backed trading at Goldman, so he knows trading and operations, and is considered to be an excellent manager, which is rare on the Street. I know him from years ago and at least then he was an unusually decent fellow.