Given the weekend, there was not much in the way of news on the Bear Stearns front, save further clarification of how perilous its state is.

From CNBC:

Department heads at Bear Stearns met with officials at J.C. Flowers and JPMorgan Chase Saturday afternoon to give an overview of their business divisions, including headcount and profit and loss positions, CNBC has learned….

On Friday… S&P lowered its long-term counterparty credit rating on Bear to “BBB” from “A,” and it placed long-and short term ratings on credit watch with negative implications.

Because of that S&P downgrade, bankers have now come to the conclusion that a deal must be done by Monday morning because no one on the street will trade or lend to Bear Stearns, which is rated a notch above junk bond levels. If the downgrade hadn’t happened, Bear management would have had more time to work the Street for a deal, sources said.

CNBC failed to note that Moody’s had cut Bear’s long-term counterparty rating to Baa1 and Fitch to BBB.

The irony is rich. Moody’s and S&P were arm-twisted into not lowering the ratings of the monolline insurers because it would Cause the End of the World of Finance as We Know It. But their diligent, speedy response on Bear might set off a nasty chain reaction.

The significance of the downgrade goes beyond taking the firm out and shooting it in the head (as if that isn’t bad enough). Some readers did an astute job of addressing these issues, so I’ll turn the mike over to them. From Steve on the immediate impact:

I doubt anyone wants to pick up Bear’s level 3 book and pending lawsuits. As for piecing out prime brokerage and wealth management, the first question is how big a hole has been blown into them by the run, and whether there’s a buyer who wants to `rebuild’ those businesses for a price that management can stomach. Bear is dead in the water. They can’t trade their positions and the client run isn’t going to stop. If there isn’t some (partial) resolution by Monday morning, I expect they’ll be filing by Monday afternoon. The Fed’s liquidity support means nothing if no one wants to do business with their brokers and desks.

Let’s consider that unpleasant scenario by itself: Bear files for Chapter 11. This is not an area of expertise of mine, but I imagine anyone who didn’t start the process of moving their accounts out would now find it difficult and protracted. And the last time you want to have access to your accounts restricted is when markets are haywire, which they certainly will be next week.

But worse, if you were trading on margin, your collateral will be seized and will become part of the bankruptcy. Eeek. If any sizable hedge funds get caught, God only knows how nasty the knock-on effects might be.

A further, and potentially disastrous development is that a Bear bankruptcy could trigger the unravelling of the credit default swaps market. Reader reality-based lawyer worked through the narrower issue of the impact of a downgrade big enough to trip collateral triggers:

Bear wrote credit-default swaps in large volume. All/most of the swaps probably require Bear to post collateral in the event it’s downgraded below a specified level (a rating trigger), typically “A-.” Do you know whether S&P’s downgrade to “BBB” trips the rating trigger, or does it require two rating agencies, or is it set at “BBB”? If the last, the trigger wouldn’t be pulled unless/until Bear is downgraded below “BBB-“, at which point it very likely wouldn’t be able to meet the resulting collateral posting requirements (depending on the market value of its net exposures) and would simply go directly to somewhere in the “C” or “D” range. If the first, meaning the trigger’s already been pulled, the question is how S&P could give Bear a “BBB” rating – how much funding do they think the Fed will provide?

Bankruptcy would lead to ratings downgrades beyond BBB- and probably independently lead to the collateral trigger being tripped.

Now RBL assumes the Fed can step up to fill the gap. But can it? It has about $400 billion of firepower left under current balance sheet constraints (one reader argued that the Fed could expand its balance sheet much more; I’m not clear in practical terms how that could happen and other analysts have taken the opposite view). I suspect in dollar terms this is more than enough, but I wonder whether the Fed/JPM tag team will be able to deploy it successfully, given the constraints of operating in bankruptcy.

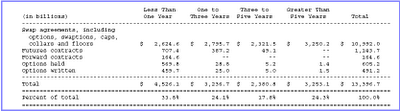

Let’s look at this unenlightening-by-design chart (click to enlarge) and related disclosure from Bear’s November 2007 10-K (hat tip Prudent Bear via Michael Shedlock):

As of November 30, 2007 and 2006, the Company had notional/contract amounts of approximately $13.40 trillion and $8.74 trillion, respectively, of derivative financial instruments, of which $1.85 trillion and $1.25 trillion, respectively, were listed futures and option contracts.

The aggregate notional/contract value of derivative contracts is a reflection of the level of activity and does not represent the amounts that are recorded in the Consolidated Statements of Financial Condition. The Company’s derivative financial instruments outstanding, which either are used to offset trading positions, modify the interest rate characteristics of its long- and short-term debt, or are part of its derivative dealer activities, are marked to fair value.

The Company’s derivatives had a notional weighted average maturity of approximately 4.2 years at November 30, 2007 and 4.1 years at November 30, 2006. The maturities of notional/contract amounts outstanding for derivative financial instruments as of November 30, 2007 were as follows:

Now it isn’t evident that the rather scary looking $10 trillion line (yes, that’s $10 trillion, but remember that is notional amount; the economic exposure is a teeny fraction of that) is credit default swaps. Given the “swaptions, caps, collars, floors” this looks to be in large measure interest rate swaps.

However, the interest rate swaps market is the bread and butter of short-and-intermediate term interest rate management. Disruption in that market would be nasty. It would almost certainly have a serious, adverse impact on interbank funding rates, and they were looking rocky before the events of last week. Similarly, one of the trades that brought LTCM down was being on the wrong side of rising swaps spreads. Anyone (and it really could be anyone, hedge fund, securities firm, bank) who had similarly placed the wrong bet could be badly impaired.

Now that is pretty bad, but if reality-based lawyer is right and Bear wrote a lot of credit default swaps, the downside is probably even worse. Remember, the protection writer is the one who has to pay up if there is a credit event. So if they get downgraded or go bankrupt, suddenly that guarantee looks pretty unreliable.

Further, many users and writers of CDS hedge their exposures with other CDS. So if one piece looks like it might fail, that hedged position suddenly looks unhedged. This would cause a scramble for more protection writing when hardly anyone is writing protection and spreads are already at extremely elevated levels.

To reiterate: the issue is probably not the magnitude of the Fed commitment, but operational difficulties due to bankruptcy rules that impede the Fed in delivering on its backup.

So that means it is imperative that someone buy Bear by Monday (perhaps this can miraculously be strung out another day, but I defer to the experts). I’m not clear if mechanically that can happen. Even getting to a letter of intent by Monday would be heroic (and for sports fans, letters of intent unless someone screws up have language that makes them not legally binding and subject to due diligence). And Bear is a regulated entity, which means additional hocus-pocus has to happen before a deal is done.

So we appear to have two outcomes: that somehow the clever folks at Lazard get something signed that looks enough like a deal (even though it can’t possibly be a deal) that between it and the Fed bailout Bear does not have to file for bankruptcy. Or it files.

Now let’s go one step further. Unless someone leaks a very very positive update to the Financial Times (best because it closes its online edition much earlier than the Wall Street Journal), anyone who has an operating brain cell and can trade in Tokyo time is going to be unwinding carry trades as fast as possible. No one who is reliant on yen funding wants to be exposed to what might happen if Bear goes BK. And a sharp move in the yen will feed on itself. You could see the yen move to 98 or 97 if the recognition that Bear could go bankrupt fast and what that might mean takes hold.

And all bets are off if we see further unwinding of the carry trade. The markets are already panicked, rumors will swirl as to who is at risk, and per Bear, those rumors of trouble can become self-fulfilling. And that could redound to the stressed credit default swaps market.

We had this typically cheery view from Nouriel Roubini:

And Bear is only the first broker dealer to go belly up. Rumors had been circulating in the market for days that the exposure of Lehman to toxic ABS/MBS securities is as bad as that of Bear: according to Fitch at the beginning of the turmoil Bear Stearns had the highest toxic waste (“residual balance”) exposure as percent of adjusted equity on balance sheet; the exposure of Bear was 54.5% while that of Lehman was only marginally smaller at 53.3%; that of Goldman Sachs was only 21%. And guess what? Today Lehman received a $2 billion unsecured credit line from 40 lenders. Here is another massively leveraged broker dealer that mismanaged its liquidity risk, had massive amount of toxic waste on its books and is now in trouble. Again here we have not only a situation of illiquidity but serious credit problems and losses given the reckless exposure of this second broker dealer to toxic investments.

His gleeful tone that his prediction that “one or two systemically important broker-dealers will go belly up” has come to pass is troubling, I don’t particularly enjoy seeing the financial equivalent of broken bodies.

I’m in no position to comment on Lehman. On the one hand, the Wall Street Journal went to some length to indicate that Lehman had much better liquidity buffers than Bear had, and perhaps more important, the advisors to hedge funds who told them to pull back from Bear are not worried about Lehman. On the other hand, that $2 billion in new facilities doesn’t buy much. Recall that Bears’ $17 billion cash and equivalents hoard went poof in a mere three days.

But consider what other lessons have been learned in this saga;

Investment banks can go under with remarkable speed. The last time we had an investment bank failure was Drexel Burnham Lambert, but everyone on the Street hated Drexel, it was in a niche business that its competitors coveted, so everyone stood aside and the firm was gone in no time flat (I dimly recall that crisis to failure was maybe three business days). But here, even with the Fed and another major bank putting their muscle behind a rescue operation, the outcome will probably be much the same. That isn’t just sobering, it’s a reality that many haven’t witnessed. It will elevate the prevailing level of nervousness.

Efforts to reduce risk can have the opposite effect. This was a point made in Richard Bookstaber’s A Demon of Our Own Design, that in what he called tightly coupled systems, insurance measures can make things worse (witness: everyone running to buy credit default swaps to contain their risks is making prices skyrocket, which is increasing prices considerably for anyone who want to finance, which hurts the real economy, which increases fundamental risk). And that specifically means that the Fed’s moves may well backfire. As we noted yesterday (this obsrevation came from a reader):

The TSLF probably had the perverse effect of killing Carlyle Capital, the exact opposite of what was intended (Robert Peston @ BBC, via Alea). The TSLF gave creditors every incentive to seize Carlyle Capital’s collateral in order to present it at the Fed window in exchange for “lovely liquid Treasuries”, something which Carlyle Capital itself couldn’t do. Bear, on the other hand, is allowed to use the TSLF… but the TSLF doesn’t go live until March 27.

Specifically, if the yen rallies to 98 or higher on Monday and Tuesday trading in Tokyo, a 100 or even 75 basis point cut by the Fed Tuesday could be disastrous.

The Fed is badly out of its depth. Not that this is a surprise, since its actions have looked desperate for a while (was it Barry Ritholtz who said “75 is the new 25”?). This confirmation comes from a hedgie reader:

A last note on the Fed. A friend who’s got very good contacts told me today that they’re completely at sea here, not understanding what’s going on, flying by the seat of their pants, and making policy completely on an ad hoc basis. Not precisely what one would hope for in this situation.

Let’s all hope next week is not as exciting as I fear it could be.

Congrats, best piece on the web on Bear.

On the Fed ‘at sea’ — everyone should re-read Yves post about Gaither’s speech in, I think, spring of 2007. Gaither admitted/described/acknowledged that the Fed — the people who work at the Fed — do not understand these sophisticated, and toxic, financial instruments.

If that was the spring of 07, then the Fed has had nearly a year to go to school. If Yves’ friend at the Fed is accurate, they didn’t learn much.

And, by the way, that might not be too surprising because, IMHO, there aren’t even five people on the planet who understand these ‘wonders of financial innovation’.

I don’t think Roubini is a “glee” as you suggest. His writing style can be boring, and he’s just trying to make the material more palatable. Give the guy a break – he’s taken a lot of abuse over the years and was woefully early on his recession call. It’s his time in the spotlight, and we should be grateful that we have someone that presents this worse case scenerio with such intelligence and rigor.

God help us.

I don’t see Roubini’s writing as gleeful. He always seems pretty objective to me, particularly given the amount of vilification he and other longtime bears have received for sticking to their guns. He has so far been absolutely right.

Regarding the “broken bodies”, the other side of that coin is the statement that (paraphrasing) if you can see all the hands at the poker table and you STILL manage to lose money, sympathy is likely to be in short supply. All of these big IBs have been printing money for several years now at the (ongoing) expense of taxpayers, home renters and clients who were not “in the loop” in that way. Why should we feel sorry for them now the house of cards is collapsing? We are too busy dealing with the consequences to ourselves – rocketing prices, housing crash, job market recession. Bear’s bodies are not the only ones being broken here.

I’m curious as to how much of an investment bank’s daily cash flow typically derives from the trading of securities.

Can anyone answer this?

The question arises after reading that other firms no longer wanting to trade with Bear helped cause their liquidity collapse.

Since it has now become very evident as to how incredibly fast an investment bank can unravel, it stands to reason that the “risk premium” embedded in the stock price of all investment banks should be permanently elevated (implying a lower PE multiple). The same goes for the credit spreads on their debt.

Let’s call this for what it is: this was a bank run.

The same dynamics are at work.

It’s funny because our regulatory system was geared since the last Great Depression to prevent runs on commercial banks.

There was no system set up to prevent runs on investment banks.

And yet it is the investment banks that are now at the heart of our securities-based credit system.

The housing market still at least has to drop another 20% nationwide before this is over. This implies further massive hemhorraging in the credit market. That will destroy the balance sheet of the investment banks and hedge funds.

It’s hard to see how “bank runs” won’t eventually occur with ALL FIVE of the major investment banks.

An argument could be made that the bankruptcy of Drexel Burnham contributed in a large part to the failure of several large savings and loans and helped trigger a crisis that eventually cost the taxpayers close to $1 trilion.

Many owners of S&Ls derived substantial personal income from side deals with Drexel. In return, for these lucrative deals for their personal accounts they loaded up the S&L balance sheets with toxic waste.

For example, I knew of several law firms that had large equity stakes in S&Ls. Drexel paid substantial legal fess to these firms. Their S&Ls, in turn, purchased large volumes of junk bonds that Drexel happened to be underwriting.

Without Drexel, the owners could no longer afford their S&Ls and promptly ‘put’ them to the government.

Also, as an aside,Kidder Peabody was the last big investment bank to go under (in 1994). But they were backed by GE, so the market disrupton, while significant, wasn’t as consequential as that of Drexel.

per the derivatives table, Bear has written $491 billion in options. what happens to those options if they go BK? is this the beginning of extreme counterparty risk in the options market, or am i missing something? i (and probably others here) have PUT options. i guess the easy answer is don’t hold them at the expiration date to see who is holding the bag.

but if we start seeing counterparty failures in the options market at expiration next week, is that going to blow up the whole options market, both for CALLs and PUTS?

inquiring minds want to know.

thanks.

It’s not surprising that the Fed doesn’t know how to handle these massive problems. I believe they should revisit their policy of allowing asset bubbles to inflate, because of course you cannot recognize one, and then deal with the consequences of it’s subsequent popping. Raiding the taxpayers’ largesse to bail out wall street investment banks, so early in the crisis, is a mistake. TRANSPARENCY is the only way to restore confidence. Bailout by acronym is not a policy.

I am really curious as to how much in the way of cds has been written not BY BSC but ON BSC, and where that exposure lies. I would guess that, regardless of what happens later today and tomorrow, the downgrade would trigger a payment obligation.

Who has the exposure here and what is the chain reaction likely to be?

A primary root cause of the “bank run” on Bear Stearns was indeed the LACK OF TRANSPARENCY.

Fear of the unknown causes the bank run.

Hello Bernanke, is anybody home?

Should we wait under the whole system is burned to the ground before you mandate this much-vaunted transparency?

A securities market-based credit system must be founded on transparency (in the absence of the direct borrower-lender relationship that banks used to have).

“I don’t particularly enjoy seeing the financial equivalent of broken bodies.”

I love it, personally. Especially these.

You scare me. Good Piece.

naked

Nice piece. Nj the Fed knows exactly what it needs to do to fix this problem IMO. the problem is they don’t have the capital to do it. they have about 800 billion to throw at this disaster and this is a multi-trillion dollar issue.

If it comes down to the Fed going BK or Wall St., then the Fed will stand on the sidelines and do what they cab which won’t be much.

Their mantra will be to make this meltdown orderly and try to keep the financial system in tact.

The Fed simply doesn’t have the resources to fix this problem. the weak banks will go down and the good ones like JP Morgan will survive. Its going to take a lot of pain to get there sadly.

“A friend who’s got very good contacts told me today that they’re completely at sea here, not understanding what’s going on, flying by the seat of their pants, and making policy completely on an ad hoc basis. Not precisely what one would hope for in this situation.”

“There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.”

Human Action: A Treatise on Economics

Ludwig von Mises (1881-1973)

What we are witnessing is the death of keynesianism economics and like Roubini the Austrians will be proven correct.

It seems to me that we are in for a pretty good ride.

Here’s what I think is happening:

Banks are holding a gun to their own heads and threatening to shoot if they are not bailed out, the FED terrified bails them out efectively devaluing the currency, creating run away inflation leading to greater over extension by consumers at which point the FED realizing that inflation is a real problem raises rates which freezes the credit market and the economy thus causing a general collapse.

And I’m like a deer in the headlights – no habor seems safe, not real estate, not stocks, not cash, not commodities.

I only hope that the investment crowd feels at least a little of the pinch.

ok as a quant and also a tax lawyer but NOT a BK lawyer…

(a) as a member of various exchanges, bsc is going to have its ability to book or clear driven down to zero dam fast unless theres an undisclosed guarantor

(b) as to what happens to their puts and calls…if they are the counterparty on those puts and calls then the other side is screwed; however, assuming theyre not completely stupid (uh…) and were running a delta neutral book and it was also fairly gamma neutral (english: it would be immune to both small and larger price moves of the underlying) then if the markets didnt go nuts (oh sure…) it would be technically possible to operate in some kind of quasi runoff where a credible entity came in and at least mathematically “matched” those on each side of the trades (in other words, if some guy sold calls to bsc and some guy bought calls from bsc they ought to meet each other fast) and for some extra money from each or concessions etc work something out…actually for plain vanilla stuff it would be in the overall interests of an exchange to come in and facilitate this because if the new stuff crossed on an exchange then it would quiet down the counterparties (you do NOT want to imagine a scenario where no one trusts a trade crossing on an exchange)

(c) normal cds dont trigger payout on a downgrade to bbb alone (ie if you own protection on bsc normally this wouldnt be an event of default) however default of many other unrelated obligations of bsc would be

(d) the bigger issue imo is this (as to the derivatives): you have to think of a derivative as both a “current” instrument and a “terminal” one. suppose you have a call on something with a certain exercise date (assume european). you can think of it in terms of its value at exercise or in terms of its intrinsic value minute by minute. for those whose exercise dates are far enough out they probably can ride through this if they’re long and have no collateral requirements as i imagine some new people will take over their book. but for anyone else, and for all people who would normally trade their position not just hold to expiration, they’re sol.

Re: And all bets are off if we see further unwinding of the carry trade. The markets are already panicked, rumors will swirl as to who is at risk, and per Bear, those rumors of trouble can become self-fulfilling. And that could redound to the stressed credit default swaps market.

>> One issue to remember in this event, is that Bear was being watched by SEC and FBI, thus the following “old” reminder is worth noting IMHO:

Morgan Stanley, Goldman Sachs Group Inc. and Bear Stearns Cos. all disclosed in regulatory filings Tuesday that they are cooperating with requests for information from various, but unspecified, regulatory and government agencies. Officials at the companies either declined to comment, or could not immediately be reached.

FBI officials also highlighted what they called a growing pattern of suspected mortgage loan fraud potentially committed when loans were made to shaky borrowers. They cited a surge in “suspicious activity reports” that banks are required to file with the government.

The number of those reports is projected to rise to 60,000 this year after hitting 48,000 last year, up from about 7,000 in 2003. “We’re going to have to take a hard look at these things,” said Assistant FBI Director Ken Kaiser.

to the tax lawyer and quant:

The guy who sold the option to BS doens’t give a damn what happens to BS. He has not risk to them. Why on earth would he even want to meet someone who bought calls from BS?

if reality-based lawyer is right and Bear wrote a lot of credit default swaps, the downside is probably even worse. Remember, the protection writer is the one who has to pay up if there is a credit event.

no offence, but this is garbage. Bear’s CDS books will basically be fully hedged, or fairly close to it. That is, they bought protection just as much as they sold protection.

Bear’s problem is liquidity, ie. they can’t borrow money any more. And also they probably have some sh*t assets on their balance sheet. CDS doesn’t seem to be an issue for anyone except the monolines, who only sold protection and hence will be taking large losses when defaults occur. The derivatives books at investment banks do not have this problem. Yes they have counterparty credit risk exposure, but that can be minimised with good credit control procedures in place, which believe it or not most places do have.

Re: Rating agencies and the speed involved here (for Bear), may be related to the following nudge to get them out of the collusion/asleep-at-the-wheel mode and to attempt to save what microscopic reputations that might remain for them; the rating agencies are obviously being looked at very close now, so they needed to appear to be in the business of valuation ratings:

The advisory group also recommended that credit-rating agencies differentiate between ratings on complex investment products and conventional bonds. The ratings agencies also should disclose conflicts of interest, Paulson said.

SEC Chairman Christopher Cox said Congress recently gave the SEC the power to address issues including conflicts of interest involving credit-rating agencies. “We will use that authority to help restore investor confidence,” he said.

Great article even if it is depressing! It’s really great to get a little thoughtful perspective over the weekend. Your blog does this routinely & I appreciate it (although I don’t always enjoy it).

As for Nouriel Roubini, I find his work highly thoughtful and rigorous, but I don’t always agree with him. I too often find errors in his assumptions (usually “worst case”) that make his analysis faulty–and even more pessimistic than it need be.

Roubini validates that economics is “the dismal science.”

probably because he’s not a moron and if he sold an option to bsc does not want to get a call from the person running the debtor in possession or the us trustee or bankruptcy trustee telling him there is no way to trade out of it and he should expect to be slammed at expiration if its in the money.

people who sell options kind of, you know, like to be able to roll them or close them out before expiration and they would be gosh awful upset to find out that theyre shut out of that.

see, let’s pretend we all think first before we write, admittedly a stretch, and let’s assume we sold puts on, say, spx strike 1100 on 9/4/01 and these were sold on cboe and the exercise date was 9/21/01. now theres an attack and the markets are closed. so you’re sitting there all week long, 9/11, 9/12, etc tick tick tick

friday morning 9/21 you may owe someone a s–tload of money. you can’t trade out of this. you can’t take an offsetting position because no one will trade with you because they don’t know what price to put on it or it will be murderously expensive.

now sit there and imagine what its like to be in that position (and fyi if the markets had never opened till october 01 i assure you the contract language would have used the first available after-rotation price to come looking for you).

you don’t want to be short an option to a counterparty who is a debtor in possession or being run by a bk trustee.

ever.

ps

unless you have RUN a book, dont pontificate on what it means to be balanced, because is very unusual to be matched. matched and balanced are not the same. matched means for every guy you’re short to there’s a guy you’re long from and all terms are identical, tenor, strike, etc. balanced on the other hands means that for a small range or price movement in the underlying the value of your shorts and longs offset each other.

it means you’re dynamically hedging to neutrality, not that you’re statically hedged.

in the case of cds, most of these guys are NOT matched, they use correlation models and consider themselves balanced but when shock to the system occurs as, you know, is going to happen if theres a bk or two soon, then the price gyrations of the underlying make it impossible to hedge dynamically.

now you imagine doing this when you’re a debtor in possession or a bk trustee and no one wants to play with you.

thats why you don’t want to be short to these guys.

This is too rich! A option seller is at risk if if his in-the-money counterparty goes bankrupt!

If I sold an option to BSC and its in the money, I owe BSC or its sucessor the money. If BSC doesn’t want to roll over, so what?

And I’m sure a bankruptcy judge is going to sit there and net long and short options positions.

Which ratings days are you working at these days? Or are you at one of the monolines.

to underdog worried about his put option:

the option you bought or wrote are most probably traded on an exchange and not over the counter unless you are some institution. With exchange traded options there are daily margin requirements that help prevent counterparty risk. If you buy/sell options you better know how it works.

yeah i figured you’re a moron.

all option sellers are at risk if their counterparty refuses to retrade, reprice, or roll. option sellers with brains (presumably leaving you out of the set as a definitional matter) don’t expect to hold through expiration. now they have to.

and as i probably earn several dozen times what you do being hired by us trustees or bk trustees unraveling matched books of busted funds, yeah, thats exactly what they will do if they have time.

With regards to the back-and-forth about options, assuming the options are routine puts/calls traded on an exchange, wouldn’t the OCC step in and guarantee the contracts? They won’t make a market for them, so you might have problems closing them before expiration, but if you hold in-the-money options at the time of expiration and BSC doesn’t have the money to pay, or they’re frozen by the BK process, wouldn’t the OCC step in?

Gosh, I never thought we’d get to the point where we all have to bone up on OCC guarantees…

The fact that this discussion about options is even taking place only serves to underline in general just how much fear has run rampant in the investment community after the Bear Stearns bailout.

Great stuff, thanks. A few random addiitions:

Anon of 9:09 AM,

Great point. That aspect of the Drexel failure is not widely known and should get more coverage.

But Kidder was a different case. Remember, they were sold after the Joe Jett incident. Jett did not cause losses, he merely created very large phantom profits that then had to be reversed, much to GE’s consternation and embarrassment. It was more of a shut-down than a failure (yes, they were way overgeared, but I think GE was waiting for any excuse at that point to shut them down).

A general comment:

I ran out of steam, but one thing that has bothered me about this entire affair is the Fed’s lack of preparedness. IBs do fail upon occasion. They’ve known since LTCM that a failure of anyone large has systemic consequences. They’ve also known that investment banks have become even more significant since then it terms of total credit intermediation.

Why was there no disaster planning? There was a comment in something on Bear (I’m not motivated enough to track it down) how Geither polled various firms in 2006 about risk sceanarios. Huh? First, that’s way too passive for that sort of exercise, and it shouldn’t be a “gee let’s have a look now” process, it should be done regularly and rigorously. The Bank of England publishes a Financial Stability Report every six months, and it has tons of coverage of credit markets generally, not simply the UK or banking. And I would hope they have more in depth discussions in private.

The Fed was a prisoner of free market ideology, and we are all going to pay dearly for that.

Yves,

Awesome work – top quality analysis.

Keep it up. You and Felix do such a good job of not just posting news to your blog, but actually giving us useful analysis.

Thanks!

–Q

Yves: I’m not sure that polling is as passive as all that. I remember (or misremembering?) a demand at our across-the-pond firm about what would happen if the Agencies went belly up. I think that was a pretty solid indication that we were supposed to consider it as a legitimate scenario and if we were expecting Agencies to be backed by the full faith and credit of the U.S. government, then our regulators wanted us to think again.

For people who are talking about calls and puts. Actually, it usually doesn’t matter who wrote the call or who wrote the put. In this age the major firms have collateral agreements. They tote up the mark-to-market value of all the book and they post margin if they owe and receive margin if they are owed. So a counterpart could have sold calls to Bear and still be at risk, if the market tanks, because it might have paid x in margin and now needs to collect some of that x back.

Yves,

To the following post, why not have the fed step aside let the market correct itself even if quick and very painful. Then step in with a governement program of recapitalization witha series of bond issues (akin to the special class of jumcos for mortgages from Fannie and Freddie) along with stricter regs. Serieous leadership would stand up and tell the americans and the democrats who were asking several years ago why no american was asked to sacrifice for the warwell it has finally come home only in a slightly different hue. I think americans are up to the task. Not to mention you want to seea wall of capital flow into the USA this is the recipe. Not only would it break the commodity trade but it would slingshot the dollar as the US has repeatedly shown that it is the most resiliant economy. Such a plan would require pain all around, but the message that we may be the ultimate consumer but we are not above taking our beating would be a message to the world that we may be down but we are for sure not about to fold. The only thing we lack today is leadership. We need pattonesque no holds barred approach.

to the tax quant/lawyer

I was unaware that so many dealers with matched books had gone bankrupt over the years that you could make money advising the bankruptcy trustees.

So if you are long an in-the-money option sold by a bankrupt company you don’t have to worry becuae a judge will find an offsetting option bought by that bankrupt company to make your whole!

I was not aware that in any G10 country that ‘in-the-money’ option holders were senior to all other creditors!

No wonder there is no risk in the financial system!

Let me guess, you helped draw up the strategic plan that told AMBA and MBIA that there was big money and little risk in insuring CDOs.

There is real risk on exchange traded options.

If you bought a put that is in the money and that money is with your brokerage firm.

If your brokerage firm goes belly up you are just an unsecured creditor of that firm.

Now, the OCC will try to step in to make sure that you are made whole.

However, the OCC does not have unlimited resources. If the losses reach sevearl billion, not even the OCC can guarantee all lossss, IMHO.

The number of failures over the past twenty years covered by the OCC can be counted on one hand.

But, as they always tell you in the fine print, past experience is not any guarantee for future performance.

By the way I think this is a pretty plausible historic of Bear’s troubles. It was using Agencies as collateral. The blow-up in Agencies meant that according to cross-collateral agreements, counterparts could refuse them as collateral. Certain European banks decided to refuse them, so Bears had to post cash or Treasuries, which began the downward spiral. The Fed tried to help with its new TSLF facility, but it was too late.

a,

To your point re the polling of dealers by the Fed not being passive, I was not sufficiently clear what I meant.

If a regulator comes calling and says, “Gee are you prepared for Y” the answer is “Yes!” You may scramble around to shore up a few things to make sure your affirmation will stand whatever inspection they perform.

Similarly, if a regulator asks more generally, “Gee what bad things could happen?” you are not going to dream up any awful scenarios. Some of that is, per above, you don’t want to alarm them, God knows what rules they might impose, and some of it is hubris or lack of historical memory. Recall that some accounts of the subprime mess had senior people dismissing downside scenarios as implausible, impossible, when we’ve blown through them all.

So the result is the Fed is dependent on the Street for its understanding of systemic risk and appears not to have done enough independent fact-gathering to have its own point of view. Given the dim opinoin that many people in the industry have of its reliance on VAR as a risk management measure, it doesn’t understand the products or operational issues in sufficient depth to challenge members of the securities industry either.

See this speech as an example.

The Bank of England, in its April 2007 Financial Stability Report, identified 16 “large complex financial institutions.” They deemed that if any of them got in serious trouble, it could constitute a systemic event. At least the Bank of England had figured out that the big players were vital to the functioning of the international capital markets. But note further: Bear was not on that list.

From what I can tell, the Fed hadn’t even gotten as far as the Bank of England in its thinking. If it had, just based on the discussion of derivatives in the comments above, they ought to have realized that the Street was now sufficiently enmeshed via trades that no meaningful player could fail without it having very serious consequences.

To a’s second comment, about Bear’s woes resulting from the deterioration in Agencies: that fits the known facts, since it was apparently European banks, nine days ago, that started refusing to trade with Bear. But then you have to widen the frame of reference: Agency spreads were widening, at least as far as I could tell, because the market was reacting badly to various measures and further proposals to have Freddie and Fannie effectively refinance stressed borrowers. So again, measures to ameliorate the problem are making it worse.

Check out yahoo’s finance page:

http://finance.yahoo.com/

[From near the bottom of the middle column]

—-

* Community Sentiment

Stocks everyone is talking about.

Bullish

The Bear Stearns Companies, Inc. (BSC)

Alvarion Ltd. (ALVR)

Boyd Gaming Corp. (BYD)

Bearish

General Motors Corporation (GM)

Washington Mutual Inc. (WM)

Hemispherx Biopharma, Inc. (HEB)

—-

Apparently we’re Bullish as a community on BSC :)

–Q

“WHAT are the consequences of a world in which regulators rescue even the financial institutions whose recklessness and greed helped create the titanic credit mess we are in?”…NY Times Sun March 16th.

Smartest guys on the street… You boneheads created the instruments that were too complex for even you to understand once you shuffled them all over the world’s markets as CDOs. Now the American taxpayer has to bail you stupid f*&cks out. It is immaterial that Bear “can’t fail” because it manages backroom admin for major hedgefunds etc. Who cares? I suppose next you’ll want the average joe to buy your elephant suits and ridiculous ties…

Anon of 5:18 PM,

Personally, I’d love to let Bear fail and I’ve said so in earlier posts. However, Bear and its ilk have made themselves indispensable to the operations of our economy.

Remember how much municipalities lost when the auction rate securities market failed last month? Multiply that sort of damage by 20, maybe 100, if we see big Wall Street firms go belly up. The public at large is going to wind up paying for this under any scenario.

Great Article. It clarified several points for me. From the news being released it looks like JPM will buy Bear this evening — even if only in principle — for the value of the buildings.

I’m not sure what that will really do for things as it isn’t clear from what’s being reported as to who is going to assume the liabilities for the toxic stuff.