I am frequently mystified at what goes on in the markets. I am even more mystified when people who ought to know better make pronouncements that appear to be profoundly counter-factual. Even if they are talking their own book, the high odds of being revealed as bald-faced liars proven wrong ought to make them worry about damaging their credibility.

Is this wishful thinking? Delusion? A hope that that a united front can change perceptions and therefore reality? (see this as Tinkerbell behavior: if we all clap together, the markets won’t die).

In the last week, we’ve had the CEOs of Goldman, Morgan Stanley and JP Morgan say that they see an end in the not-too-distant future to the credit crunch. Similarly, Mark Mobius of Templeton argues that all the bad news is already priced into stocks, while private equity investor Wilbur Ross plans to spend $4 billion buying banks (although he professes to be picky)

Mind you, the optimism among the financial services leadership is far from universal. Lehman thinks recovery won’t come till 2009; Paul Calello, CEO of the investment bank Credit Suisse expressed considerable uncertainty as to when the crisis might be over. And the industry’s own analysts, who have strong incentives to argue the bull case, have been far more downbeat than industry executives. Goldman has forecast an “awful” earnings season across the board; Meredith Whitney of Oppenheimer is calling for continued large losses at banks.

I could go through a litany readers know well (and can no doubt improve upon): the housing market is continuing to deteriorate and based on precedents here and abroad, there is no reason to think it will bottom before 2010 or 2011; we are some distance from a typical bear market low of a 30% fall in the S&P (and with the severity of this crisis, we may overshoot); the US has to wean itself off its credit habit, and none of the ways out are pretty; non-government guaranteed securiization has fallen off a cliff and appears unlikely to come back any time soon, yet banks lack the equity to fill the gap with on-balance-sheet intermediation; counterparty risk in the credit default swaps market hangs over the financial services industry like a sword of Damocles.

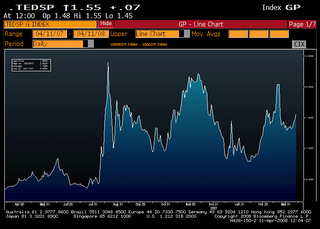

But let’s put these long-term considerations aside. It’s bizarre to see this upsurge of cheery chatter given the counterevidence in the money markets. Widening TED spreads suggest we are on the verge of another crisis:

The overnight index swap rate has also indicated bank reluctance to lend to each other. Jeff Frankels provided an update yesterday, with a chart from the Institute of International Finance:

And the report yesterday that banks were fudging on their reporting of Libor is making maters worse. From Across the Curve:

I have related the thoughts of a money market trader at a large shop who has been modestly constructive on his market. The story in the Wall Street Journal this morning which suggetst that banks have been understating the true cost of funding and the true Libor rate has turned this veteran trader less optimisitic. My source believes that this story and the subsequent report that the British Bankers Association will mete out harsh punishment to those found dealing in untruths will lead to an excess of caution over the near term. My trader source reports that inquiry further out on the money market curve has dried up this morning and the only business he has printed is in overnight sector. He thinks the imbroglio could add 5 basis points to 10 basis points to Libor in the near term

Separately, the 5year swap spread is currrently at 92.5 basis points. It has essentially retraced the entire post Bear Stearns rally. On the Friday evening of March 14 the 5 year swap spread finished trading at the 93.75 level. In the rally which followed it reached 77 basis points. It has slowly moved wider so that it currently sits just a basis point from the pre Bear level.

Central bankers have thrown a lot of firepower at the problem of a money market seize-up, yet illiquidity persists. What more can they possibly do if we move into another acute phase?

Update 11:30 AM: Reader Scott sent this chart, showing two year US swaps, with the comments. “The concept that the Fed has stabilized the system is fantasy…..queue the Ride of the Valkyries.”

What more can they possibly do if we move into another acute phase?

Don’t worry, they’ll think of something. TSLF, PDCF, etc — there are plenty of letter combinations left. And they don’t have to end in ‘F’.

WTF? A “trader source” became less optimistic after the story in the WSJ? What the WSJ reported was well known for 6 months. Either the trader has had his head in his ass, or he has become “less optimistic” because he belongs to one of the BBA-polled banks who have been lying on the LIBOR poll in order to save money on their derivatives positions. (This is from someone who is just a little incensed because we have been losing money on same. Lending at LIBOR because of contracts signed years ago and borrowing at what turns out to be LIBOR + x is pretty f*cking annoying.)

You want a “trader source”? Here’s one. Libor improved its accuracy by 10 – 12 bips today; it is still about double that off. When I see it north of 3% on the USD 3Months I will begin to believe it.

There’s a simple reason for the money-market seize-up: pretty much every bank knows they are in bad shape, and they naturally surmise that every other bank is probably in the same shape. So why would you lend? Banks don’t normally think of themselves as charities…

One other comment: central banks think that by taking toxic waste “temporarily” off the banks’ books will do some good. Not likely. Why lend to a bank which is on life support, where that support can be removed at any moment? This is, by the way, not a plea for central banks to start buying the toxic waste. That solves the banks’ problems but won’t solve society’s or the economy’s. Society’s best solution is to ring-fence the commerical side of the commerical banks and let the IBs fail.

Very confused; on the one hand, commentators of every sort have claimed that all the $ investors pulled has been ploughed back to money markets (and equity from the looks of it. If money markets have been seizing up, where hasthe $ gone? all in commodities and equity?

Another reason why banks may be reluctant to lend, if I read this a-right, is that with present rates _and_ present cost inflation, real rates are negative, even over month long terms. Banks don’t lend money to get less back. Lending on a time frame of a week finishes in the black, so there’s a nickle to be made—which is all most of these guys have to risk anyway. That’s the problem with driving rates DOWN: where’s the money to be made lending at pissant rates? Another reason why the power dive in the Fed funds was ill-conceived, and why the ECB holding the line where banks can still make some money lending is the better policy. We made money cheap; they made money good. Who did good?

“Society’s best solution is to ring-fence the commerical side of the commerical banks and let the IBs fail.” a, I am with you 200%. Don’t ring-off the questionable; fort up the necessary, and let the devil take the rest. Or to revive my preferred metaphor of awhile back, throw the plutocrats out of the life boat, and split up their lunch among the rest.

“Central bankers have thrown a lot of firepower at the problem of a money market seize-up, yet illiquidity persists. What more can they possibly do if we move into another acute phase?”

Nothing. It’s a solvency problem for the banks, pure and simple…. they’re out of good collateral. Measures undertaken to date are largely aimed at liquidity so they’re missing their target.

These people have been lying and cheating for so long I think it is impossible for them to tell or even comprehend the truth. Also lying does seem the way to go.

while private equity investor Wilbur Ross plans to spend $4 billion buying banks (although he professes to be picky, after his investment in MBIA, is this doubling down?)

Uh, Ross bought a stake in Assured Guaranty, not MBIA. He *is* picky, and bought a stake in one that presently has no likelihood of downgrade.

An aside: It almost never pays to put money into financial guarantors where the credit quality is in question… the future dilution will eat you… unless you put in enough to right the ship, and you get a discounted price sufficient to give you a good return on equity — which means a very bad return on equity for existing equityholders.

I would also not be so sanguine. The reason why we had a systematic issue was because the normal clearing mechanism for asset price booms was rerouted through the banking system.

The only reason we have some semblance of stability is because interest rates have been lowered and central banks have been supporting liquidity and temporarily accomodating the stress of asset price revaluation.

Unfortunately the excess broad money supply growth of the last 10 to 15 years is still more or less in situ and much of this has to go through the banking system if debt/asset prices continue to revalue.

The only way we can be assuaged is if debt/asset prices stabilise and the imbalance between nominal returns on debt/assets and debt/asset prices is allowed to balance via higher wage, consumer and producer price inflation.

This means higher interest rates down the road if indeed the credit crunch is now over. The terrible shape of US and other consumers suggests that the debt market has still some way to correct and hence the systematic risks have much more room to widen.

We need to remember just how we got into this mess before we can sound the all clear.

Andrew Teasdale

The TAMRIS Consultancy

a,

Excellent points, all.

“the high odds of being revealed as *****proven wrong ought to make them worry about damaging their credibility. “

I ask this in all seriousness. Is their credibility really an issue, after all this? Shouldn’t they be genuinely, thoroughly discredited?

Galbraith’s book on the 1929 crash has plenty of analogous examples of happytalk from government and industry. Even as late as 1931 Keynes had to remind his readers that the collapse wasn’t going to fix itself magically (the stock market was steadily rising in 1931, btw). Today I think gov’t and industry are even more convinced that perception is reality; that proposition seems almost axiomatic to them. The calculus seems to be that there’s a 10% chance that all of this will blow over if negative sentiment is contained. The happytalk does seem orchestrated–safety in numbers, so no single CEO looks like a fool later.

Steve,

You don’t believe perception is reality? Reality is a construct of your intellectual capacity. Some of us have more and can discern fact from perception. Most don’t. Simple bell curves, so perception IS reality.

The very top of cnn.com’s business page right this minute –> ” Wall Street firm’s (Merrill) quarterly loss is even wider than expected “

Expected BY WHOM? Not Yves. Not Mish. Not CalculatedRisk. Not Minyanville. Not Krugman. Not Roubini.

Et cetera, et cetera, and so forth. America is a banana republic right now. Not “like” a banana republic.. IS.

Thank your Republican lawmakers for making America into a footnote. McCain will continue the stupidity if you vote for him.

Sorry to deviate slightly into politics, but we stand no chance of turning this around until regulation is returned.. and Republicans don’t have the guts to pass the appropriate measures.

Note that ML resulots included $2B gain on credit spreads widening. IE credit profile gets worse take a gain. Lehman apaprently worried about this on the flip side. So I guess when those write ups that everyone is waiting for will be fully offset by the imprioving credit spreads ats the two would appear to be highly correlated. A natural hedge perhaps. Nevertheless, disturbing

ML Press Release: di ytou think an analyst asked about thisor even brought up what happens on the flip side? no chance

“To a lesser

extent, net revenues were also impacted by net write-downs related to leveraged finance

and residential mortgage exposures, which were offset by a net benefit of $2.1 billion due

to the impact of the widening of Merrill Lynch’s credit spreads on the carrying value of

certain of our long-term debt liabilities.”

Yves,

It’s all about pumping up the value of collateral and helping the poor banks make things better… , however, this new game of hot potato and or musical derivatives is sorta like the subprime game we just played, but now that recess, I mean the recession is over we can soon go back out and play! It’s nice we have a substitute Congress, Senate, DOJ, Fed, SEC…

http://www.gillygaloo.net/docs/07_lyrics.htm

Re: The more we get together, together, together,

The more we get together, the happier we’ll be,

For your friends are my friends, and my friends are yours,

The more we get together, the happier we’ll be…

The more we sing together, together, together,

The more we sing together, the happier we’ll be,

For your songs are my songs, and my songs are yours,

The more we sing together, the happier we’ll be…

The more we clap together, together, together,

The more we clap together, the happier we’ll be,

For your beat is my beat, and my beat is yours,

The more we clap together, the happier we’ll be….

I’m so sorry for song above … many bows, here is better song:

Money Moves

Given a lack of visibility into counterparty risk, many CFOs are scrutinizing how they are investing precious excess cash. Investor focus has shifted from yield to risk, says Sarah Jones, co-head of liquidity and investment products at JP Morgan Treasury and Securities Services.

Driving this is the discovery that short-term cash funds and even some money-market funds — an investment heretofore thought highly liquid — are exposed to structured investment vehicles (SIVs) that purchased toxic mortgage-backed securities and collateralized debt obligations. CFOs are shedding investments in funds with SIV exposure that don’t offer complete transparency or daily liquidity.

In August 2007, Ethan Manuel, treasurer at $800 million Mentor Graphics, had migrated the company’s short-term investments from asset-backed paper to money-market funds to maintain liquidity while gaining a bit on the return. He switched back to treasuries and commercial paper last November. “We went away from money-market funds, because we weren’t sure if there would be write-downs or liquidity concerns,” says Manuel. “Right now, we’re being very careful.” — K.M.K.

Taking the Measure of Your Banks

Given the rockiness in the financial sector, CFOs would be remiss if they didn’t question the stability of their banking partners. However, determining just how strong a specific bank is can take some doing.

To evaluate large banks’ capital adequacy, many analysts look at “tangible common equity,” a measure of net worth relative to assets, says Brent Christ, an analyst with Fox-Pitt Kelton. Tangible common equity, a non-GAAP measure, is common shareholders’ equity, less intangibles and goodwill. The ratio of TCE to assets (less goodwill and intangibles) is generally considered more healthy if it is at least 6 percent for smaller banks and 4 percent for larger ones, Christ says.

http://paradigmshiftpr.com/pedal…/ pedalingas.htm

OCC’s Quarterly Report on Bank Derivatives Activities

Third Quarter 2007

http://www.occ.treas.gov/ftp/rel…e/2007- 137a.pdf

Derivatives activity in the U.S. banking system is dominated by a small group of large financial institutions. Five

large commercial banks represent 97% of the total industry notional amount, 78% of total trading revenues and

87% of industry net current credit exposure.

The first step in measuring credit exposure in derivative contracts involves identifying those contracts where a

bank would lose value if the counterparty to a contract defaulted today. The total of all contracts with positive

value (i.e., derivatives receivables) to the bank is the gross positive fair value (GPFV) and represents an initial

measurement of credit exposure. The total of all contracts with negative value (i.e., derivatives payables) to

the bank is the gross negative fair value (GNFV) and represents a measurement of the exposure the bank poses

to its counterparties.

A bank’s net current credit exposure across all counterparties will therefore be the sum of the gross positive fair

values for counterparties lacking legally certain bilateral netting arrangements (this may be due to the use of

non-standardized documentation or jurisdiction considerations) and the bilaterally netted current credit

exposure for counterparties with legal certainty regarding the enforceability of netting agreements.

This “net” current credit exposure is the primary metric used by the OCC to evaluate credit risk in bank

derivatives activities. A more risk sensitive measure of credit exposure would also consider the value of

collateral held against counterparty exposures. While banks are not required to report collateral held against

their derivatives positions in their Call Reports, they do report collateral in their published financial statements.

Notably, large trading banks tend to have collateral coverage of 30-40% of their net current credit exposures

from derivatives contracts.

Net current credit exposure for U.S. commercial banks increased $53 billion in the third quarter to $252 billion.

At the end of the third quarter, legally enforceable netting agreements allowed banks to reduce the gross credit

exposure (GPFV) of $1.6 trillion by 84% to $252 billion in net current credit exposure

thefinancedude,

Yes, magicians really do saw their assistants in half.

So why is the gross negative thing such a big deal?

Re: The first step in measuring credit exposure in derivative contracts involves identifying those contracts where a

bank would lose value if the counterparty to a contract defaulted today. The total of all contracts with positive

value (i.e., derivatives receivables) to the bank is the gross positive fair value (GPFV) and represents an initial

measurement of credit exposure. The total of all contracts with negative value (i.e., derivatives payables) to

the bank is the gross negative fair value (GNFV) and represents a measurement of the exposure the bank poses

to its counterparties.

Re: During the fiscal third quarter, the Firm is expected to incur negative gross mark-to-market adjustments on assets of ($7.8) billion, including gross negative mark-to-market adjustments of

($5.3) billion on residential mortgage-related positions, ($1.7) billion on commercial real estate positions, ($600) million on other asset-backed positions and ($200) million on acquisition finance positions.