By Hugh, who is a long-time commenter at Naked Capitalism. Originally published at Corrente.

On September 24, 2012, Josh Lehner published a post comparing employment (jobs) and unemployment rates in and after various financial crises, including Sweden in 1991 and the US in 2008. Lehner concluded that the policy response to the 2008 financial crisis “compares pretty favorably” and that

While the initial path of both the global and U.S. economies in 2008 and 2009 effectively matched the early years of the Great Depression – or worse –the strong policy response employed by nearly all major economies – both monetary and fiscal – helped stop the economic free fall.

This has been used by some to argue erroneously that the Bernanke-Obama-Geithner-Bush-Paulson strategy of bank bailouts effectively proves the Swedish approach of resolving insolvent banks following the 1991 crisis was wrong. What is wrong is this assertion. It ignores Swedish economic history and the limitations of Lehner’s evidence.

I do not pretend to be an expert on Sweden, but the basic facts are not hard to come by. Sweden had a real estate bubble which burst in 1991. Rather than prop up and bailout the affected banks, the Swedish government went in guaranteed deposits (and creditors) and created a bad bank for bad debts with proceeds flowing back to the government. Banks were recapitalized either by the government (in exchange for stock) or by private investors (by issuance of new stock). By 1992, the banking sector had been restored. The rest of the Swedish economy had not. At this point, the Swedish government had options. It had a fiat currency, but instead chose to wastefully and unsuccessfully defend a currency peg, effectively imposing a gold standard on itself. This was at a time when the Swedish welfare state was in full flower. The added social costs from the bursting of the bubble, the bank recapitalizations, and the self-inflicted restraints of its monetary policy created an unsustainable situation. Rather than loosening monetary policy and increasing investment and stimulus, in 1994, the government opted for the neoliberal solution of partially dismantling the welfare state, promoting exports, and tolerating higher levels of unemployment in the name of increased “competitiveness”.

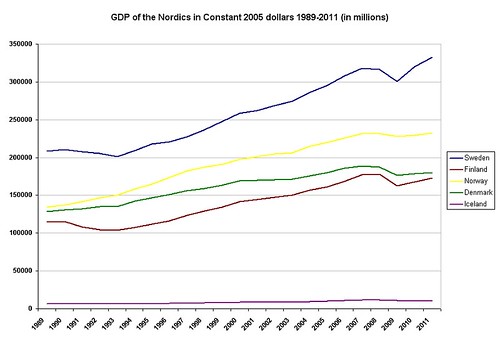

If you look at GDP, this worked out rather well with Sweden outperforming the other Nordics. Of course, GDP is not people.

But it shows the weakness of the whole line of thought of those criticizing the Swedish model. They look at only a narrow range of indicators, and those not too closely, and overread their meaning.

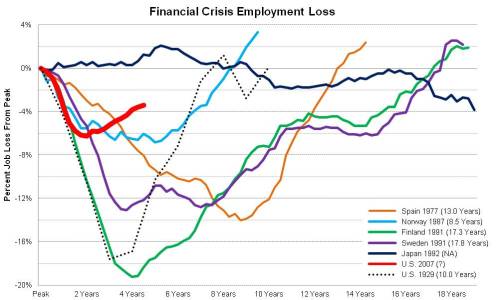

So what were these indicators? First, there is employment (jobs):

The point I wish to make here is about the red line representing the US. You will notice a quick turnaround in it, and this is supposed to demonstrate the superiority of the bailout approach. But what all comparisons of jobs to a peak leave out is population growth over the period. It is not enough for jobs to get back to January 2008 levels. As I pointed out in a recent post, the working age population grew by some 10.950 million in the interim. If we use the labor force participation rate for January 2008 (66.2), a by no means stellar rate, we come up with an extra 7.249 million jobs needed for them. This is not reflected in the chart. And needing a job and not having one is probably a more pressing concern in the US (with its high debt levels and poor safety net than it is in Sweden even with its partly dismantled welfare state). Finally and also as I have noted before, there is the issue of the deteriorating quality of American jobs. A chart like this one can not treat quality, but its analysis should.

Reading the chart, it looks like it took about 10 years for the Swedish economy to hit a new, lower jobs level consistent with the prevailing neoliberal philosophy. This was followed by a goosing in the bubble years of the mid to late 2000s. If anyone wants to say that the Swedish model, along with everything else going on at the time, played some role in those first 10 years, I really have not problem with that. I do have one in describing it as the primary driver of events for 17.8 years.

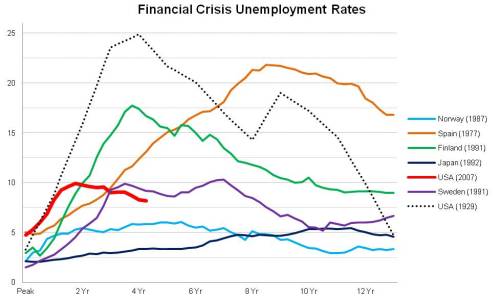

Lehner’s second chart tracks unemployment.

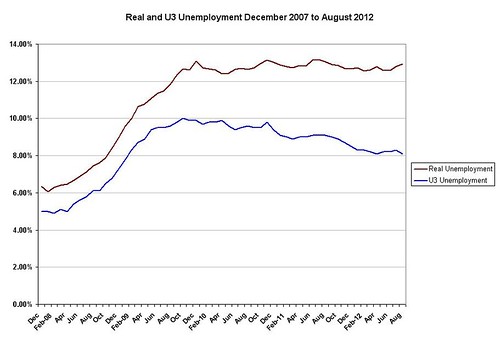

There are several things to say about this. The official U-3 rate of unemployment (people) topped out at 10% in October 2009 and gradually declined to the present level of 8.1%. However, the participation rate changed markedly from its peak in January 2008 of 66.2 to 63.5 in August 2012. As mentioned above, that change represents 7.249 million people. If these were incorporated into the stats, the unemployment rate in August 2012 would 12.2%. As it is, the decline in the unemployment rate in the US has not been because there are fewer unemployed. There are actually 4.899 million more than when the recession began in December 2007. The decrease is an artifact of a job-seeking definition of unemployment and the resulting removal of millions from the labor force. These are people who would work if jobs were available to them. We know this because from 1996 to 2000, the participation rate was .67 or higher. If we take .67 as a measure of where the labor force should be, the real vs. U-3 unemployment picture looks like this:

Real unemployment plateaued in September 2009 and has averaged 12.8% since. This is a very different from picture portrayed by the official rate. There are a few other things to consider as well. The US has large armed forces and prison populations and neither of these is counted as part of the labor age population, or non-institutional population over 16.

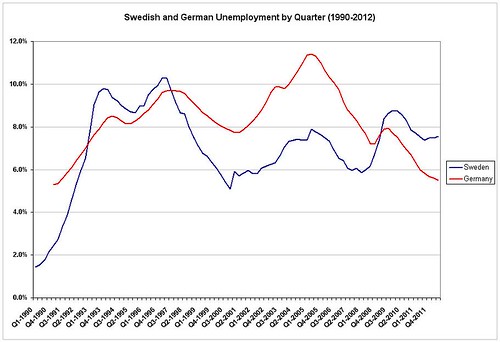

Looking at the Swedish data, the following is based on harmonized unemployment figures from OECD Stats.

I compared Sweden to Germany because I wanted to show that Sweden does not exist in isolation from its neighbors. The peaks and valleys in the Swedish data, though varying in degree, track with those in the much larger German economy. This argues against the notion that the Swedish model was the principal force behind unemployment in Sweden over a timeframe of some 10-20 years.

Put simply, Lehner’s charts are being misread and overread, and Sweden’s economic history completely ignored. The Swedish model did the job it was designed to do. It fixed the banks, which is a lot more than can be said for what bailouts have done for our banking sector. The Swedish model didn’t create years of economic turmoil in Sweden. That was done by the real estate bubble bursting and the government’s other responses to it. At the same time, Sweden was not immune from the economic ups and downs happening in the rest of Europe and the world.

As for the US, we are up to QE3. Need I say more? The banks remain predatory and broken, and unemployment is improving only because so many are being definitionally “exited” from the labor force and the counts.

* * *

Lambert here: So, the (issue (is (hardly (“settled”)))).

thanks for setting this straight

The post assumes that Sweden doesn’t separate U3 and Real Unemployment figures, or they are one and the same. On that count, the comparison is yet to be done. The point about the banks is well made. We not only have predatory, partially insolvent bank as of today, but these banks control our political system and strangle it.

The US has just started the process similar to “the [Swedish] government opted for the neoliberal solution of partially dismantling the welfare state.” The cat food Simpson/Bowels commission recommendations supported by Obama, lowering taxes through lowering FICA payments, vicious attacks on unions and all other workers and in particular the almost racist attacks on teachers fully supported by Obama and his basketball buddy Arne Duncan are all bad signs. Yet nothing, accept lower wages, much was actually completed.

[1] The U.S. and Sweden have started from such very different places, obviously, in terms of dismantling their welfare states, in that such a thing existed far more vestigially in the U.S. in the first place and, besides, Sweden never bore the enormous burden of being a host for the enormously parasitic U.S. medical-industrial complex (37th worst health outcomes in the world for twice the costs per person). It’s a slightly crazy comparison, on that score.

[2] As for Hugh’s post, it’s both an admirably thorough piece of work and a message that will need to be repeatedly hammered home through the din of official propaganda till enough people get it.

“As for Hugh’s post, …. and a message that will need to be repeatedly hammered home through the din of official propaganda till enough people get it.”

Totally in agreement. And we are very lucky at NC to have Hugh’s posts and the repeated hammering home of the points (backed by exquisitely well parsed and analyzed troves of otherwise impenetrable official data.)

Some historical info on ours and Sweden’s bank problem.

Did Sweden really nationalize its banks?

by Ed Harrison

http://www.creditwritedowns.com/2009/02/did-sweden-really-nationalize-its-banks.html

He excerpts some of this report, then recommends reading the rest. That is necessary to get the whole picture of how Sweden handled the banks. But this was a pretty “soft touch” with only setting up bad banks and it sounds like shareholders kept ownership, tho they kicked in new capital, and no mention in the report of what happened to bondholders.

http://www.piie.com/blogs/realtime/?p=504

IIRC, I think back then O said that they had considered a Swedish nationalization, but this is America.

So there you have your reason.

But then The Bernank set up what was basically bad banks with the Maiden Lanes, and now we have more MBS buying with QE3 of course. Forever, or until employment get better. So let’s call the Fed a bad bank too.

So we managed to combine the worst of everything.

Depends on what you mean by “better” Lambert. If it means better for politically connected bankers then the U.S. bailout trumps anything in history. If better for say the economy or society or small business then well the swedes got it…

This is excellent analysis and a great first step. Has anyone definitively answered Middle Seaman’s question? I suspect it is only the U.S. that defines job seekers in the way that we do, but someone would know for sure re Sweden.

At bottom, though, there is still the matter of justice. This is not a criticism of Lambert’s work, but a criticisim of the state of discourse on the bailouts: mere cost-benefit analysis leaves out the primary question, which is one of right and wrong. I would prefer a system that didn’t prop up Wall St. bonuses with my tax dollars and my monetary system. I would particularly prefer a system that didn’t involve massive bailouts coupled with editorials in the Wall St. Journal telling me the bailouts were good for me and I should be thankful for them.

Thanks to Hugh for the speaking truth to power about the abuse of US employment stats in support of unjust and unfair social policy (bailing out the banks).

I agree with Pitchfork above that this is a continuation of the control of our public narrative when we should be talking about nationalizing the Fed, reasserting just rule-of law including putting people in jail and taking our country back from the global inherited rich.

To my knowledge, both Sweden and the US use job-seeking definitions of unemployment as set out by the ILO. But they are still different societies. Sweden may have more job training programs. We have more people in prison.

I don’t think anyone calculates real unemployment except me, precisely because official entities use the job-seeking model to define unemployment and the media and most researchers tend to blindly follow them. The problem is that now the discrepancy between the two has grown so great that it is producing a kind of schizophrenia or cognitive dissonance. People know that unemployment is a big deal. All they have to do is look at where they live. Even the Fed paid lipservice to this theme when it used it as a pretext to initiate QE3.

But the truth is, and this is part of the disconnect, 8.1% while a problem is, if we accept the official line, not that big a problem. If you take the old figure of natural unemployment running around 5%, then that leaves 3.1% or about 4.5 million unemployed that need to be dealt with. If you apply some of the new arguments (i.e. propaganda lines) for structural unemployment rates as high as 7%, then excess unemployment drops to just over 1.5 million. This is simply an invitation not to believe our lying eyes.

The gravity of the jobs crisis is not reflected in the official numbers. My calculation for real unemployment for August 2012 was just over 21 million and I am sceptical about natural rates. With a jobs guarantee, I would think that turnover rates could be held below 1%. Of course, significantly higher unemployment than what is officially recognized explains only part of the popular unease toward what is going on in the economy. There is also disemployment (29 million), the sum of real unemployment and involuntary part timers. And beyond these and largely unquantifiable is the replacement of stable jobs with good wages and benefits with crap Mcjobs. We catch whiffs of this in the official stats only in which sectors are hiring, which losing, and in the general erosion of wages.

And back in the early 70’s when we had less unemployment than now our federal government was creating public service jobs to carry unemployed workers through those tough times…..I know, I helped run the CETA/PSE program for 32 of 39 counties in WA state.

We have totally lost compassion toward our fellow man since then….sad commentary on the concept of civilization.

Not to harp on the obvious, but Sweden did not have a one-plus-trillion-per-year military bill. We all know that democratic finance will never vote for that.

It is nice to read a thorough debunking of the idea that bailing out banks works better than the Swedish Model.

When the idea that bailouts are amazing and the Swedish Model is a joke first surfaced, I wrote the following post (http://tyillc.blogspot.com/2012/09/it-is-simply-not-true-that-us-bank.html).

It also debunks what is a misreading of the data. My focus was on comparing the US during the Great Depression with the US during the Great Recession.

What readers might find interesting is that during the Great Depression, the US adopted the Swedish Model shortly before the upturn shown on the Financial Crisis Employment Loss chart.

I like your last sentence:

“The only thing that bailouts achieved is the bankers were paid their bonuses and governments incurred a significant amount of debt related to the bailouts.”

Thank you for making this obvious point:

“Mr. Weisenthal makes the assumption that there is a direct connection between making banks absorb the losses on the excesses in the financial system and the unemployment rate. Advocates of the Swedish model like your humble blogger never say there is a direct connection to the unemployment rate for the simple reason that there isn’t a direct connection.”

Joe just makes a classic post-hoc-ergo-propter-hoc error. Of course, in the MSM, that passes for analysis. It is SO important to look at the discrete effects of the various bailout policies.

For example, TARP had almost nothing at all to do with credit availability in the wider economy. The Fed’s Comm Paper facility nursed the CP market, while Treasury’s blanket guarantee of MMF’s stopped the fabled “electronic run on the bank.” Moreover, the government could have “bailed out” depositors, insurance companies, the commercial paper market, MMF’s, etc. (which they did), but WITHOUT also preserving the capital structure of the Wall St. and money-center banks and also preserving Lloyd Blankfein’s and John Thain’s bonuses.

Weisenthal’s argument gets us right back to the old straw man of “Either we bail out Morgan Stanley’s and AIG’s bonus pools OR….we let the world burn and we all fight in the streets over scraps of rat meat.” Thanks, Joe.

In addition, to the GDP and unemployment numbers for Sweden, it is important to recognise that Sweden’s national debt/GDP shot up like a rocket as a consequence of the financial crisis and peaked at almost 80% in 1995. Subsequent governments, left and right, then made it central to their policies to bring down the debt levels which currently stand at ca. 30% of GDP and are projected to fall further in the coming years.

The country has thus pursued less policies that have been less expansionary than otherwise would have been possible in order to avoid a debt trap.

Sweden’s budget for 2013 is expansionary in order to counter the current economic slowdown

No disrespect intended Hugh, but the situations are radically different.

Sweden had to defend it’s currency from a massive speculative run. A spectacular dive in the kronor’s value would have negatively impacted their economy. Almost entirely due to Sweden having to import oil for at least a third of it’s energy use. That effectively tied the hands of Swedish authorities to respond to the crisis. As every modern economy simply cannot function without energy. One of the major reservations I have about MMT theorists is that they treat every fiat currency as if they functioned as a reserve currency. When they clearly do not.

The pace of recovery Sweden experienced had little to do with their bailout method and more to do with their relative economic position pre-crisis and worldwide conditions post-crisis. Pre-crisis Sweden did not need to rebuild from the second World War, while many of it’s economic competitors were left in shambles. It was this economic void that Sweden (as well as the US) benefited from. If you take a look at history from that mid 70s / early 80s a picture begins to form that shows ground being lost in both countries to their economic rivals recovered.

The irony is that both countries tried to make up for lost ground by credit expansion. The United States jumped off the gold standard to sustain this expansion. (Guns and Butter) While Sweden as a neutral country did not have to expend it’s economic energy on military expenditures and subsequently did not have to drop as deeply as quickly into debt. The dynamic of credit inflation followed by debt deflation though was startlingly similar. Post-crisis the Swedes find themselves on a relatively flat economic level in Europe.

There is no way that the last 30 years of debt based economic growth was going to end in anything but tears. Or as the Federal Reserve put it in it’s study of the Swedish economic crisis; “even well-managed financial crises don’t really have a happy ending.”.

As far as Lehner’s point goes, he ignores the reality of the Great Depression. Which is quite typical of economists who don’t read history books. It didn’t begin or end with the financial crisis. Before the ’29 crash, most major industrial countries were already in a deep recession. The United States then (like China today) was the exception. The world was just as reliant on cheap American credit pre-crisis back then as we are in the present. The yen carry trade served this functioned until late 2007.

There was a speculative run because the Swedish government had left itself open to one by pegging its currency at an unsustainable level. It then compounded its error by trying to defend the peg. It ultimately lost and the krona depreciated 20%. The depreciation then allowed Sweden to pursue a decade long export led recovery.

Debt is a major problem and it probably will all end in tears. The tragedy is that it doesn’t need to. I look at all this from a resource point of view. The resources, both people and material, are there. They are just being massively wasted and misallocated.