Loyal Dems were over the moon with reports from California that the costs provided by insurers of various levels of plans on state exchanges were coming in under CBO estimates, as well as below prices on the current small-group market. The early huzzahs survived an effort to claim otherwise by Avik Roy at Forbes; his creative footwork with numbers was shredded in the blogosphere (although still curiously repeated by Reuters).

A bit more serious challenge to claims of early success on the cost front comes from Ohio, where Republican officials brayed that premium increases next year would average 88%. The analysis appears a bit sus, since it included some pretty crappy plans in the baseline. But while more detached commentators weren’t happy with how Ohio officials ran the numbers, they didn’t appear able to debunk the idea that costs would be higher for most people than before, even though the higher costs might indeed result from plans providing more comprehensive coverage.

One big issue is that the Republican-led states are doing a good job of throwing sand in the gears of implementation, which means it’s likely that consumers there will indeed have reason to be less satisfied. These states have refused to implement state health exchanges, throwing the task on the Federal government, and also nixing Medicaid program expansion, which will leave a lot of low-income people out in the cold.

But reader martha r has been poking around the information in her state, Vermont, which is now being touted for coming in with lower-than-anticipated cost forecasts, like California. But the plans don’t strike her as affordable for locals. She writes:

Newly up on the website for the Vermont implementation of ACA:

http://healthconnect.vermont.gov/tax_credit_calculatorI’ve queried them on whether one should enter one’s gross or net income. But you can play with different numbers and see how it comes out.

A not at all uncommon salary among my neighbors–I live in a condo community with many single women living alone, social workers, teachers, nonprofit directors, and the like– in this area is $35K.

That may seem shockingly low, and for many it is not tenable, so after they try to make a go of it in Vermont they decide to leave and seek better paying work elsewhere.

But for the hard core who get Vermont into their blood and can’t bring themselves to leave, this low a salary is not at all unusual. Hopefully, one also has benefits–but not always.

So you might try entering $35 or $40 or $45K and see what these lower-middle income people are going to get.

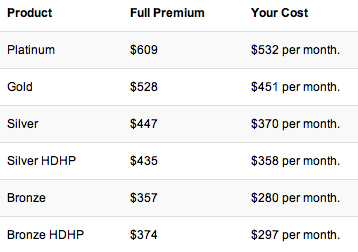

For a single person, the cutoff seems to be $46K–at $46.1K, you get zero subsidy. at $46K you get $77 per month–the minimum subsidy. Here’s how that plays out:

For a single person, at S46K gross on a salary (not self-employed with a home office deduction and the like), or $3833 per month before taxes, who can afford $370 per month? Perhaps those who have paid off their mortgages or nearly so?

I admittedly only have a personal datapoint, but in New York, which has to be a higher cost state, my current plan is a bit better than silver (plus I have some very valuable features, like coverage anywhere in the world, plus no network or primary physician gatekeeping, and external appeal to New York State) and my costs are markedly lower than the silver plan cost in Vermont. And I’m over 50.

A new article by Karen Higgens at Alternet gives some other reasons why the cheerleading is overdone. For instance:

Wellness” programs that enable businesses to transfer more healthcare costs to workers with “unhealthy” factors like smoking or high blood pressure or cholesterol levels are rapidly spreading, actively encouraged by the ACA which offers premium discounts to participating employees. However, health disorders are as likely to derive from chronic or genetic conditions as “life style choices” and economic factors which have a disproportionate impact on the poor. The cost reductions also fall far short of the hype. The federal government apparently buried a report it mandated for the ACA from the Rand Corporation on wellness programs which showed the overall savings are, at best, modest. The programs make insurance unaffordable for some workers, and “keep the sickest workers from affording the care they need,” said Alan Balch, vice president of the Preventive Health Partnership, an alliance of the American Cancer Society, the American Diabetes Association, and the American Heart Association.

And we warned earlier of the growing corporatization of health care:

If Massachusetts is the political model of the ACA, the industry model is Kaiser Permanente by combining the roles of insurance company and medical provider with its network of hospitals and clinics. As ACA implementation nears, Kaiser has stepped up practices once associated with the worst abuses of HMOs. These include delaying medical appointments, restricting hospital admissions, and rapid discharge of patients from the hospital care to other settings. These include sending people home where the care burden is placed entirely on family members, or to outpatient facilities or nursing homes that have fewer regulations and fewer, typically lesser skilled, lesser paid staff where the patients receive less care than in hospitals. Other industry giants hope to follow this path, enrolling new members who are required to buy insurance, while they are more directly able to control their expenditures for care and can more easily slash spending. The ACA encourages care cutting practices through several mechanisms, including financial penalties for hospital re-admissions, an incentive to keep people out of the hospital, and rewarding providers who divert patients to outpatient clinics.

And of course, Obama will be gone from office before all these corporate-enriching chickens will have come home to roost. Nicely played.

There was an article in Mother Jones a while back that said under the ACA, employers that currently provide family coverage will no longer be required to provide coverage for spouses. In other words, only the employee and any kids would be covered.

The uncovered spouse would then have to go out and find his or her own insurance. And that’s likely to be a huge burden (and headache) for families in which the second income often doesn’t qualify for assistance under ACA.

If true, this planet-sized “loophole” would seem to be rather larger in effect than the rest of the ACA. Dems say it was an oversight in the law that they’re trying to fix, but I doubt that on both counts. Its too convenient as a way to pump money into the exchanges. And besides, how could those who wrote the law just “forget” spouses? Come on.

Of course, now the Dems blame Republicans for blocking a fix. But isn’t that rather convenient for the Dems too, who clearly never wanted spousal coverage in the first place? Now the Dems can portray themselves as heroes valiantly trying to remedy this problem and the GOP as villains. Again, come on.

One possible, slight mitigating factor: All those employers no longer funding the health coverage of spouses could hand the savings over to their employees. But, really, how likely is that?

Another flaw in the program–

If an employer offers health insurance, the worker will be entitled to some subsidy if his income is below 400% of the poverty level and if the cost of the policy exceeds 9.5% of his income.

However, this 9.5% figure is based solely on the worker’s individual health insurance premium costs.

It does not include the costs of a family plan.

Below, the costs of an employee sponsored family plan is $24,000–50% of the worker’s income. The worker can get subsidies for his individual policy, but none are available at all for his family which will also be excluded from the exchanges.

In particular:

“Under the Affordable Care Act, companies with 50 or more workers must offer health insurance coverage that is both affordable and adequate; otherwise, their workers may be eligible for subsidized coverage on the online health insurance exchanges if their income is less than 400 percent of the federal poverty level ($94,200 for a family of four in 2013).

A plan is considered adequate if it covers at least 60 percent of an employee’s covered medical expenses and affordable if the cost for employee-only coverage doesn’t exceed 9.5 percent of a worker’s income.

Some consumer advocates argued that the 9.5 percent test should also apply to the cost of family coverage, which is generally much more expensive than employee-only coverage. But in a final rule issued in February, the Internal Revenue Service said that it would not consider the premium for family coverage in determining affordability.

“If the premium for employee-only coverage at your company is less than 9.5 percent of your income, your family may be out of luck.

The whole family could be barred from premium tax credits on the exchange,” says Edwin Park, vice president for health policy at the Center on Budget and Policy Priorities.”

http://www.elpasotimes.com/ci_23410297/will-my-family-be-eligible-subsidized-coverage-under

Excellent points – also the commenter above you.

Employers must offer coverage to employees and their children.

If their children make cthe employee’s premium higher than 9.5 % of his income, his coverage is affordable – even if the employee-only coverage is less than 9.5% of his income.

Don Levit

‘For a single person, at S46K gross on a salary, who can afford $370 per month?’

One thing’s for sure: the $95 penalty in 2014 for going uncovered is a hell of a lot more affordable than $370/month.

Over the next four months, a clearer picture will emerge of pricing in each state. But what’s nothing more than a WAG is the sign-up rate. After all, since ACA is mandatory, no market research was conducted.

A previous trial run occurred in the late Nineties with CHIP, the Child Health Insurance Program. Being part of Medicaid, CHIP coverage is free for those who qualify. Sign-up rates for CHIP were well below expectations in the early years of the program. CHIP took to putting up posters in the post office: Don’t you want free health care for your kids … PLEASE?!

CBO has projected that 57% of those eligible will enroll in Obamacare. Without knowing pricing (which won’t be fully available till 4Q 2013), such projections are meaningless.

Taking account of known hurdles — high prices; limited disposable income; poor marketing; complex forms and instructions; people’s aversion to paperwork — I suppose ACA sign-up rates by the end of 2014 might be in the 25 to 35% range.

Which may well prove fatal: if the sickest are the most motivated to sign up, while the youngest and healthiest (who serve as the cash cows) are put off by the cost, ACA coverage will be pushed into a cost spiral that will cause even some existing participants to drop out.

The wonderful thing about boycotting ACA is that you don’t have to run petition drives, man phone banks, or go knocking on doors. Simple lethargy — not signing up — will keep participation low and sabotage the program. Let’s hear it for apathy!

I have read that the fine – oops I mean the tax! – for not having health insurance quickly goes up to over $1,000 after the Year One of the ACA. (Sorry I don’t have a source for this) That’s still much less than lower income people will be squeezed for by their “subsidized” substandard plans. But when Democrats chirp that any problems with the ACA, or with its phase in, will be fixed later, I am thinking this may be one of the first areas to receive a patch – by making the penalty for not complying with their Beautiful Vision even steeper.

Found a source on the penalty. WOW! they are a lot steeper than I was ever led to believe by my fellow Democrats (I am in recovery, thank you. Three and half years now, clean and Green)

http://money.usnews.com/money/blogs/the-best-life/2012/07/13/how-the-health-insurance-mandate-penalty-will-work

The Penalties

The actual individual mandate penalties under the ACA are perhaps the easiest part of the program to understand:

In 2014, the annual penalty will be $95 per adult and $47.50 per child, up to a family maximum of $285 or 1 percent of family income, whichever is greater.

In 2015, the penalty will be $325 per adult and $162.50 per child, up to a family maximum of $975 or 2 percent of family income, whichever is greater.

In 2016, the penalty will be $695 per adult and $347.50 per child, up to a family maximum of $2,085 or 2.5 percent of family income, whichever is greater.

“Most people think of it as an annual penalty,” notes Larry Levitt, a senior vice president at Kaiser. “But it is in fact a monthly thing, and you would pay a penalty for any month that you are uncovered.” However, a person may be without coverage for up to three months without triggering the penalty.

I followed the whole sickening pageant of Democratic wheeling and dealing with the insurance and pharmaceutical and hospital rackets. Or I tried to. I listened, as far as I was able to stomach, the explanations and apologies for the auctioning of our lives to the corporate bidders. Not once in the whole drawn out abortive birth of the ACA did I hear that the allegedly oh so light penalties would in fact be levied against hold outs and delinquent citizens monthly.

Will there be interest then? I’m guessing yes, given that it’s an IRS penalty, and based on a hitherto well-founded realism that the worse outcome will prevail.

About interest on penalties, I don’t know. I imagine the only way you could avoid paying the penalties, though, is to simply stop paying your income taxes altogether. The interest on that penalty is sometimes paid in a different currency.

It occurred to me afterwards, that the “monthly” penalty I referred to above might be a pro-rated portion of the set penalty figure. As in, the penalty for non compliance might be $695, but that will be pro-rated over how many months out of the year in question you went uninsured. But I didn’t want to reply to myself yet again – so thanks for giving me the opportunity to qualify my statement without looking like the guy who stands on the corner of the Internet arguing with himself.

Although I am confident that generally speaking Obamacare will be a “trainwreck”, as its main author has predicted, I must admit that am underinformed about the details. But I think most people are, too, and I am pretty sure that was 100% intentional on the part of Democrats writing law under the direction of their corporate sponsors.

@Barnitt I looked at the statute, after the anxiety attack, and indeed the penalty is pro-rated. The penalty applies by month, and it’s 1/12 the greater of the flat dollar amount (e.g. $95 in 2014) or percentage of income (1% in 2014).

LS

” … it’s 1/12 the greater of the flat dollar amount (e.g. $95 in 2014) or percentage of income (1% in 2014).”

Wow, hadn’t heard anywhere about the “or percentage of income … whichever is *greater*. They’re not just picking out pockets; this is bloody grand larceny. And it’s crickets out there beyond the narrow shores of Awake Land.

I’m going to have a really tough time being able to afford not having health care.

That yearly tax is far less than the inflated cost which will be charged for health insurance.

Result: people will pay the penalty and be angry at the goddamn government for charging them the Obamacare tax.

The ACA (and most other federal programs) now use the Modified Adjusted Gross Income (MAGI) (a rough equivelent of the IRS’s Adjusted Gross Income). See here:

http://aspe.hhs.gov/health/reports/2013/MAGIConversions/rb_magicon.cfm

And that the VT website doesn’t make that clear is a user experience disaster. They’re simply begging for the wrong income figure to be entered — and ObamaCare forms are filled out under penalty of perjury, let us remember.

The Gulag creates jobs too, comrade.

Not to mention that you get free health care in the joint.

So be creative!

what is MAGI–simple explanation:

http://collegesavings.about.com/od/glossarydefinitions/g/magi.htm

So called Wellness programs or ‘healthy living’ plans are not well thought out; their intent by design is supposedly to motivate members of health insurance plans to practice putatively healthy living styles. supposedly, by following good dietary practices, participating in regualar physical exercises and following the dictums of a healthy live style, medical costs will go down as keeping up with a healthy life style is equated with less need for health care from provders. Those goals are laudable but these programs, in the long run, punish folks for a medical condition that may, at its root causes, be out of the member’s control. More evidence accumulates every day that there are fetal origins to the adult onset of diabetes, obesity cardiovascular conditions and poor mental health.

Just a brief quote from one of many studies:

http://www.jacn.org/content/23/suppl_6/588S.full

The Developmental Origins of Adult Disease

Key teaching points:

• Studies have shown an association between low birthweight and risk for cardiovascular diseases and other chronic conditions later in life.

• Developmental plasticity describes the fetuses ability to respond to their mother’s diet in utero.

• Low birthweight and inadequate nutrition early in life may lead to lifelong alterations in the body’s setting of metabolism and hormones as well as the number of cells in key organs.

• Low birthweight followed by rapid weight gain during infancy has been shown to further increase risk for disease.

The main point to the above discussion is that pre and post natal care should be available for all women and children. We are so far from that as to make discussion about ‘healthy living’ a cruel joke. Until real health care reform aligns all of the paramaters of good health care wilth healthy living so called wellnes programs are just another stick used by the folks in charge to beat up those who are less fortunate. Less fortunate here could mean having a medical condition that can be ‘blamed’ on the patient.

Not really trying to to the troll thing but this topic is so vast I can really only skim the surface and the research is so well written that I hesitate to mangle the material by a too hasty rewording.

Developmental Exposure to Endocrine Disruptors and the Obesity Epidemic

Reprod Toxicol. 2007 ; 23(3): 290–296.

Retha R. Newbold

Abstract

Xenobiotic and dietary compounds with hormone-like activity can disrupt endocrine signaling

pathways that play important roles during perinatal differentiation and result in alterations that are

not apparent until later in life. Evidence implicates developmental exposure to environmental

hormone-mimics with a growing list of health problems. Obesity is currently receiving needed

attention since it has potential to overwhelm health systems worldwide with associated illnesses such

as diabetes and cardiovascular disease. Here, we review the literature that proposes an association

of exposure to environmental endocrine disrupting chemicals with the development of obesity. We

describe an animal model of developmental exposure to diethylstilbestrol (DES), a potent perinatal

endocrine disruptor with estrogenic activity, to study mechanisms involved in programming an

organism for obesity. This experimental animal model provides an example of the growing scientific

field termed “the developmental origins of adult disease” and suggests new targets of abnormal

programming by endocrine disrupting chemicals.

Much appreciated. It’s sad that pre- and post-natal care are considered investments without an immediate payoff. That’s not true. What’s true is that this is a reform not ripe for commercial exploitation.

Thank you. Very interesting. Paying for endocrine disruptors poisoning our environment, food, water, and air should not be done by people and businesses buying their most cost effective insurance policies. There is a huge disconnect here. These known hazards should be paid for by chemical and plastics manufacturers and other polluters. Otherwise is just one more subsidy to corporations gone wild.

How about those with stress-related conditions caused by the need to stay in a crappy job?

Plus a lot of this “wellness” stuff is actually an excuse to make you consume services or drugs.

For instance, I have high cholesterol. None of my doctors has ever been worried. I exercise, don’t eat meat, don’t eat a lot of fat, and am trim. I have extremely high HDL and normal LDL. One cardiologist said I’d be immortal based on my heart. But a lot of health plans would pressure me to take statins based on my gross cholesterol #s or the new idea that getting your LDL down to 100 is good. One of my old yoga teachers, who had LOW cholesterol, was concerned re that, because it increased her stroke risk. But the medical industry is really keen to get everyone on statins. I’ve even seen some doctors in all seriousness advocate adding it to the water supply.

Well, you should be. I don’t know your age, but if your 50 or older, get an angiogram (3% risk factor) to be certain that your heart arteries are not resticted.

Most of the cholesterol in your blood comes from your liver, not from the things you eat (read meat, etc.) Reducing carbohydrates (pasta, bread, tortilla) will help reduce bad cholesterol. The current upper limit for bad cholesterol is 100. (10 years ago it was 130.)

I’m not a doctor. I just have one of the top Cardiologist in the state (CA).

Yves:

I didn’t notice that you were author of the comment I reponded to. Liptor (atorvastatin calcium) can now be purchased at reasonable cost ($20/mo.) Believe me, many people have heart attacks (and other health issues) because of restricted coronary arteries. You’re alive until your not!

Getting your cholesterol below 100 is essential. Statins is the easist way to do it. A high quality diet was insufficient, in my case. (At age 60 I was considered to be in the top 3 percentile for physical fitness, but now have a Cardiologist for a reason.)

I hate to sound harsh when you mean to help, but that’s utter nonsense.

First, “LDL” isn’t the cholesterol you need to be worried about. It is specifically lipoprotein A, which BTW no one bothers checking on a routine basis. So much for science in medicine.

Second, if cholesterol were simply clogging arteries, you’d expect to see the smallest arteries get clogged, not the largest. Cholesterol is essential to tissue repair. Arterial constriction is likely due to an effort to repair stressed arteries. The more advanced thinking on this topic looks to homocysteine, triglycerides, and other factors as much better markers for heart disease risk than cholesterol.

Third, I have the hormone levels of someone ten years younger than my age, so I’m not at the usual age based risks (I get full hormonal workups every year). And I have always had, and continue to have, low blood pressure.

And a reader wrote:

I was talking to my brother (PhD in biochemistry as was my father) not too long ago about another PhD in biochemistry, Dr. Ray Peat. Peat did his dissertation on progesterone and had spent 40 years researching it. Progesterone is made from cholesterol and is the precursor of the hormones testosterone, estrogen and hydrocortisone. In other words, four of the body’s six major hormones are derived from cholesterol.

Peat did some extensive research on the deaths of women, to find out what was the optimal cholesterol level for longevity. His conclusion was the number women needed for longevity was 270 (very high according to the AMA which wants it under 200). Peat found that low cholesterol did in fact decrease a woman’s chances of dying from a heart attack but caused a woman to die sooner from something else.

My brother couldn’t believe what I was telling him about Peat’s research, but after checking out Peat’s articles and references, he concluded Peat was right. In fact, one of the things my brother found in his research was that LDL is very good at killing bacteria. My brother jokingly commented to me that in lowering one’s LDL that you don’t die of heart disease, you die of MRSA much sooner.

So both my brother and I who were on statins got off of them. Plus my brother found a new meta study of 62,000 people showing they did no good for those who didn’t have cardiovascular disease, making the decision even easier.

My dad, who taught medical students biochemstry for 40 years, found very few MD’s that knew enough biochemistry to give him any confidence in their ability to decide whether medications were justified. So I have always been very skeptical of what they recommend.

As for your Atkins comment, I have been an Atkins dieter for about 18 years. My dad thought Atkins’ ideas made sense from a metabolic point of view which is why I started doing it and still do. Atkins was a cardiologist and he wasn’t nearling as concerned about cholesterol as he was about triglicerides and blood pressure.

The other thing that is getting attention as a possible marker for heart disease is C reactive protein, which measures inflamation. Progesterone is great at reducing inflamation (remember it is the precursor of hydrocortisone) which is why I take it and I am a man.

Oh, thank God that I’m exempt from this mess. Otherwise I’d reduce my working hours and cut my on-the-table income enough to qualify for medicaid. There is no way in hell I could pay for even the cheapest of their “affordable” plans, plans that would still bankrupt me if I ever tried to use one.

Anyway I don’t like posting things that people will generally agree with (echo chambers tend to make me ill), but I’ll make an exception this time: Obamacare is a disaster. The first hints of the mandate is what turned me against Obama and the Democrats in 2009 my opinion of it (and them) has only gotten steadily worse with time.

And didn’t I read that rates in California were going to increase between 68% and 134%?

I am bemused by people’s inability to see that not only will costs go up, but they will continue to rise. The direct transfer payments from government to insurer that masquerade as “tax credits” are such a nice source of earnings that are guaranteed to rise, and not at the “official” inflation rate.

Just as with student loans, FHA insured mortgages, medicare, or any other subsidy offered by the government, this subsidy will increase the “price” of medical care.

The only solution is cash basis medicine and a personal priority on health.

Under Obamacare, employer sponsored health insurance must be “adequate” and “affordable”.

“Adequate” is defined as a policy that covers 60% of the employee’s health expenses.

How many folks can afford to pay 40% out of pocket for any signficant medical treatment?

Answer: Obama (cough, the Insurance Companies and the Pharmas).

“Affordable” seems to mean “how much do you think we can suck from the customer before he/she realizes he/she won’t be able to make rent/mortgage a few months down.”

The mandate forces you to enter a market* and purchase a defective product**. What could go wrong?

* This is the right’s critique. I agree with it.

** This is the left’s critique.

The mandate is a direct result of trying to pay for health care with an insurance system. Health is too predictable for a voluntary insurance system to work. Single-payer is also “mandatory” in the sense that you are taxed for it, but at least there the cost to the individual has some connection with ability to pay.

The disconnect on salaries is pretty amazing. The majority of workers actually make less than $35K. And workers without employer provided health insurance are disproportionately lower-income.

This basic economic truth keeps getting in the way of the hope and change rainbows, not to mention the inflation-denying print-money-to-the-platinium-moon wing of MMT.

http://www.ssa.gov/cgi-bin/netcomp.cgi?year=2011

Right, just look at all the inflation we’ve had since the government printed all that money in 2008-09.

Yeah, medical care and tuition and transportation and housing and vacations have been really affordable over the past six years.

I mean, somebody living on $30K a year is basically living the Good Life!

They only have themselves to blame by not getting into the market several years ago.

Platinum with that straw?

Um, this is far from a strawman. Go back and read the articles about high value platinum coins being game changers. Here is a link to a Joe Firestone piece:

http://neweconomicperspectives.org/2013/01/wake-up-progressives-the-trillion-dollar-coin-can-be-game-changing.html

“I concluded that inflation due to PCS per se wouldn’t be an issue, because the $6.4 T in intragovernmental and Fed-held debt wasn’t going to get into the economy. The repayment of other debt, gradually, and when it fell due, would have a similar impact on the economy as quantitative easing, already shown not to be inflationary”

I’m not sure whether to be sarcastic here or play this straight, because this notion that we spend money but the money doesn’t go into the economy is absurd. It’s academic gobbledygook that has no relation to the actual world where USFG marginal dollars go overwhelmingly to healthcare, national security, and financial bailouts.

If the Fed stopped buying the emissions of Treasury and Mortgage-Backed Securities, prices would fall. If the government stopped paying hospital administrators million dollar salaries, prices would fall. If the government stopped contracting defense work to connected insiders who deliver inferior products, prices would fall. If the government put criminal firms through bankruptcy, prices would fall. If the government stopped backing student loans, prices would fall. If the government stopped the ridiculous changes in IP law protecting drugs and other items, prices would fall.

I’m open to whatever monetary or price definitions of inflation anyone wants to throw out. However defined, it is patently obvious that prices are higher than they otherwise would be due to public policy.

Except that Firestone’s post explains exactly why your scenario isn’t grounded.

Seriously, I shouldn’t have fallen for the off-topic flame-bait, in the midst of a health care thread. My bad.

The notion that economics is off topic to healthcare policy is exactly what’s wrong with the crowd that says how money is spent is irrelevant.

For posterity’s sake, I’m going to link this post here.

http://www.nakedcapitalism.com/2013/06/joe-firestone-what-social-securitymedicare-solvency-problem.html

If the platinum-wing of MMTers would answer the basic questions instead of repeating the same blather about net deficit spending, we could actually resolve some issues.

What the article soesn’t state is that the Silver Plan @ $370 per month is a 70/30 plan whic includes a high deductible. The deductibles for the plan are somewhere in the range of $2,000 if I recall. So not only can you not afford the 370 per month but you will have to pay that deductible first out of pocket before the insurance even kicks in. What a ripoff!!

At this point, ObamaCare’s defenders will start talking about the caps, which admittedly do exist. However, one can drown in a shallow pool as well as the ocean. RomneyCare reduced bankruptcies claimed for medical care from 57% of the total to 52%, IIRC (link on request, I don’t have it to hand).

And when it kicks in — assuming you haven’t expired — all that means is that you’ll get to “cost-share” 30-40% of [unspecified] costs if you get sick and need to *use* the policy.

This is why the Obama ACA Propaganda machine *never* talks about hard numbers (i.e., dollars) or, in any even, in any meaningful way — e.g., here’s the “all in” burden on you if you buy one of these Credit Card Policies (the “metals”): XX in premiums, YY in deductibles, ZZ in co-pays, A, B, C not covered, etc. But there’s a CAP!!

The exchanges will collapse within 2-3 years unless the penalty for non-compliance is greatly raised and enforced. The Oregon Medicaid study tells you everything you need to know about what compliance is going to look like- there, they couldn’t even give away Medicaid to most of the people who won the lottery for the new slots. The mandate, with the present penalty will almost surely result in 50% compliance or less for those who are required by law to buy insurance in the individual market, and you can bet the ranch that the people who do buy in the market are going to be sicklier and more expensive to treat than the group that refuses the product. And I think the percentage that purchases the product will be well under 50% and thus skew even more towards those who are sicker and more expensive to treat.

The IRS FAQ on the fines/fees/penalties — I believe they are now called “Shared Responsibility Payments,” a phrase Orwell would be proud of — and their enforcement:

“individual responsibility provision”

And, I will note that no one really eviscerated Roy’s analysis of the California claims. His analysis still stands.

I hate linking to Ezra, but you are dead wrong on that:

http://www.washingtonpost.com/blogs/wonkblog/wp/2013/06/01/the-shocking-truth-about-obamacares-rate-shock/

See this too:

http://krugman.blogs.nytimes.com/2013/06/01/we-are-not-having-a-serious-discussion-obamacare-edition/

Sorry, Yves, you are still wrong. Roy dealt with Klein’s points, and they still show premiums will go up significantly the healthy and the young, even with subsidies.

Link

Anyone who gives any credence to Romney and GOP propagandist Roy has swallowed all of the Republican kool-aid and is marching toward the white tent.

The “wellness initiatives” are a joke. As pointed out they punish many patients for factors that are out of their control. And, the president likes to tout how they prevent more expensive care down the line. But someone with borderline cholesterol or “prediabetes” is not the same as someone with COPD and heart failure. You are not preventing a tsunami of ER visits by putting everyone and their cousin on a statin.

Every time you start a new medication, you open yourself up to all the side effects. It’s even worse if it is the newest and latest drug.

To think that insurers or even employers would pass along 50% discpounts off the traditional premium, for adhering to a wellness program is a bit ludicrous.

Even the regulations note that most employers and insurers, who even have wellness programs, provide nowhere near the 50% discount.

Don Levit

Of course Ohio will be more expensive than CA.

http://www.cdc.gov/healthyyouth/obesity/obesity-youth.htm

http://smilesforalifetime.com/index.php/2011/08/american-obesity-rates-remain-higher-than-20-in-all-states/

OH is fatter than CA. A federal program would have been much better than a state programs since cost of say a MRI is relativity the same in both states, but the % of obese and smokers is higher in some states.

West Virginia and Mississippi are in trouble. They’ll probably have the highest cost and are least able to afford them.

Here’s a smoking map by state:

http://freemarketmojo.wordpress.com/2009/11/19/the-georgaphy-of-smoking/

OH much worse than CA. WV = toast.

Nice what you did there. Blame higher costs on the individual.

That’s the point.

A huge portion of medical costs are driven by individually identifiable factors and preferences, not unpredictable bad luck. DC Dems denying this basic fact were a big part of squashing actual debate about healthcare in 2007-2009.

Yeah, I mean it’s not like all-pervasive corporate marketing actually works or anything. Just ask Big Tobacco! Or more to the point, Big Food.

Right, smoking is a great example of an activity where individual behavior can be identified. Combine that with obesity and age, and just those three variables can predict large disparities in health costs between two people.

Add in more sophisticated medical underwriting plus preferences about healthcare treatment, and you get massive disparities in costs that have nothing to do with the subset of healthcare costs that are truly random and unpredictable.

No, a huge portion of costs are driven by rapacious health care cartels.

No argument there. The waste in the healthcare system is a huge problem in our economy (and no argument about full employment nonsense will change my mind on that; waste is waste).

But that’s not mutually exclusive with the observation that medical underwriting and personal preferences can predict a significant portion of individual costs.

In fact, the massive waste of our healthcare system makes the problem worse, because it exaggerates the cost of outlier cases. We have drugs and hospital stays that literally cost hundreds of thousands of dollars due to intellectual property laws and paying for million dollar hospital salaries and granting exceptions to anti-trust laws and so forth.

Exactly. Because “people” are just too *extravagant* in their use of health care. I mean, haven’t you heard about all those “folks” in their sixties running around to get multiple by-passes just for the heck of it and “because they don’t know how much it really costs”?

The few of us who have been awake the past 5-8 years have started noticing a pattern in how the Legacy Parties, Political Class, and the FIRE industries they service, justify the imposition of artificially high prices (looting) on the backs of “folks” (Obama’s favorite warm ‘n fuzzy nickname for citizens) or (with the Democratic Rich People’s Party) passage of legislation that strips citizens (“folks”) of all assets, income, now jobs, and now access to health care. IT’S YOUR FAULT — YOU SHOULD HAVE [Fill in the blank with, e.g. (1) Made your senator do x, (2) Made your house rep do Y, (3) Made *me* (Obama), (4) been more disciplined about your shopping binges in the health care services sector!.

Short Answer: “No, it’s not [our fault]. Now get out and get lost.”

Actually, I wasn’t trying to blame individuals. (That’s a different discussion.) I just wanted to point out the fact that obesity and smoking account for a large amount of required healthcare. I also wanted to point out rates for both of these are not distributed evenly.

I was actually kinda waiting for someone to put of a map smoking bans or state tobacco taxes:

http://taxfoundation.org/blog/monday-map-state-cigarette-excise-tax-rates

It makes since that since these are problem vary regionally, that maybe regional policies affect them. (Why is OH more obese than CA?)

The problem is patients and medical providers are still dealing with insurance companies and all the shanigans they pull to not pay claims. Those bureauocracies, especially insurance companies, don’t handle change well.

My preimums went from 168 to 293 in two years. Under ACA, my premium will go down to around 200 for basically the same plan. But the premiums are always going up, which rises my subsity or my premium? I figure within a couple of years using the exchange, I’ll be back to 300 per month.

Unless you go into the details of the plan it is difficult to determine whether or not you getting a deal. From my reading of the Forbes article the author compares a quote from Esurance which is the teaser rate to get one to apply, so its a BS analysis.

He also goes into detail about the percentages who get the quoted rate. While not all do, in the end, about 3/4 got that rate, so the analysis is still good.

eSururance is sketchy, but the 30,000 foot view is that the CA public relations campaign did in fact compare apples to oranges. On that point, Roy is correct, even if Demoratic campaign operatives managed to obscure the main issue by beating up Roy on what he got wrong.*

NOTE * I say “campaign operatives” because IMNSHO the best way to think about the California rollout is as the opening battle of the 2014 and 2016 Campaigns. That’s why Enroll America, for example, is stuffed with politicos; it’s not just a slush fund for loyalists, there’s an actual strategic purpose involved.

I hate to break it to you Lambert, but the view from 30,000 feet is that any policy with a premium below $1,500 is pretty much a scam and useless for a self-insured person not under 45 and without a “sterling health record” (snark).

The latest revelation was the Freelancers Union plans, all of which appear to have semi-affordable premiums until you look at the deductibles, what’s not covered, what is subject to “coinsurance,” the co-pays for this that and the other. Ergo: too expensive to use. So why the heck bother paying the premiums if it’s going to bankrupt you to use the thing?!

i suspect the freelancers union is basically a “creative enterprise” being set up to eventually market insurance, and whatever other stuff they can “create”, to the gullible. sort of like AARP. they’re already selling a self-termed “freelancer’s bible” that offers no advice to freelancers starting out that they cannot get from many other sources for free.

yes, the population of temp and part-time workers keeps growing, and the freelancers’ “union” when promoting themselves includes such workers in the total number of “freelancers” they claim the u.s now has. why claim that all these unwilling contractual workers with no salary or benefits are part of the new, cool, growing “freelancers” “phenomenon”? and what does the freelancers union offer them?

we need to keep an eye on the show over at the “freelancers” “union” as its “membership” grows apace, as it is not a real union and does not offer real, self-employed freelancers anything real.

Social epidemiology shows that unequal income distribution in a society is highly correlated with health outcomes (the poor do worst – Richard Wilkinson). This research looks incontrovertible to me.

“Economics” seems to start upside down in the cult of the self-sufficient individual and prevent sensible social solutions. Private solutions everywhere rely on massive tax payer subsidies – so-called successful corporations export jobs (and consequently technology and know-how) abroad, steal tax, turn computers and shoes into neat toys and advertise to us as perpetual children. A Manchester report on British Rail privatisation and after tells much of the story – http://www.tuc.org.uk/tucfiles/603/The_Great_Train_Robbery_7June2013.pdf

aligning the UK Trades Union Congress with regular government cronyism reports on, say, Zerohedge.

The horrible truth may be that the private sector is no good at everything and we have the way we use it completely wrong – the tail is wagging the dog. I’m less concerned that lies about the cost of Obamacare are being told than the way the mythical wonders of the private sector are maintained generally. Of course, State Capitalism isn’t much of a way either.

We create major costs in health care and other professions through scarcity and professional restrictive practices – does anyone see any major business process analysis that challenges this?

Lebensunwertes Leben. Yeah, somebody could throw a Godwin flag, but I don’t know what else to call the morality involved.

“More detached commentators” like Cohn at the New Republic??? So he’s the type who will provide a non-biased viewpoint, accurate numbers and apples to apples comparisons? (Unlike Avik Roy?) Now that’s funny stuff!