By Jérémie Cohen-Setton, a PhD candidate in Economics at U.C. Berkeley and previously and economist at HM Treasury. Originally published at Bruegel

What’s at stake: As the recovery takes hold in the US, Europe appears stuck in a never-ending slump. With the ECB systematically undershooting its inflation target and recent signs that inflation expectations could become de-anchored, the bulk of commentators in the blogosphere are again calling for more monetary actions. Noticeably, some have completely lost hope in the ability of the European institutions to turn this situation around and are now calling for countries to simply break away from the EMU trap.

The Greater Depression

The Economist writes that this week’s figures for the euro-zone economy were dispiriting by any measure. An already feeble and faltering recovery has stumbled. Output across the euro area was flat in the second quarter. The new GDP figures are yet more evidence that the euro-zone economy is in a bad way. It is not only that growth is evaporating; inflation is also extraordinarily low.

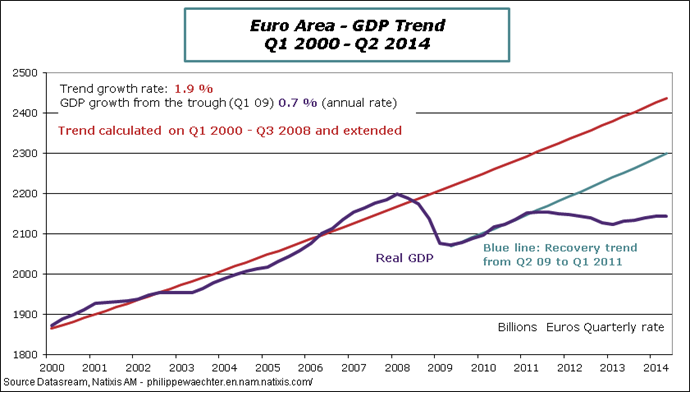

Matt O’Brien writes that it’s been six-and-a-half years, and eurozone GDP is still 1.9 percent lower than it was before the Great Recession began. It “only” took the U.S. economy seven years to get back to where it’d been before the Great Depression hit. Eurointelligence writes that until earlier this year, the eurozone’s macroeconomic development was a core vs. periphery story. If that had continued, the eurozone would have gone through a somewhat painful adjustment. But with core economies growth and inflation also low and falling, this is not happening. Brad DeLong writes that in the middle of 2011 it was possible to say that Germany had recovered from the crisis, that the remaining problems of southern Europe were the result of their own fecklessness, and that German growth was about to resume–it was wrong to say that, but it was possible. But we will soon have three years of no industrial production growth in Germany.

Source: Philippe Waechter

Ambrose Evans-Pritchard writes that it takes spectacular policy errors to bring about such an outcome in a modern economy. Eurointelligence writes that this is a recession caused by policy failure. It was not a financial crisis that has damaged the eurozone as much as the policy response to it: obsessive deficit cutting in a poisonous conjunction with obsessive central bankers (who obsess about everything, except meeting their own inflation target).

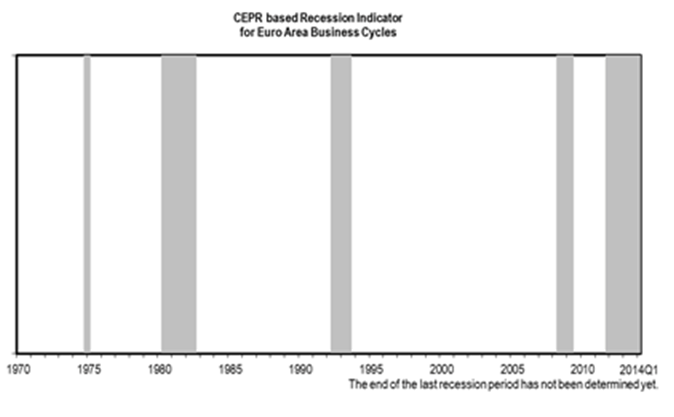

Jeffrey Frankel writes that the peculiar way individual European economies define a recession makes it harder for the public to see that the same wrong policies have been followed throughout the crisis. Under U.S. standards (where the start and the end of a recession is determined by a cycle dating committee) Italy would, for example, probably be treated as having been in the same horrific six-year recession ever since the shock of the global financial crisis in 2008. Citizens in Italy have now been given the impression that they have entered a new recession. Voters may draw the conclusion that their new political leaders must have done something wrong. But the picture is different if Italy has been in the same recession for six years. The implication may be that the leaders have been doing the same wrong things throughout that period.

Structural Reforms, the ECB and the EMU Trap

Antonio Fatas writes the central bank should, as in the US, communicate its view on how close the economy is to potential output, how much slack there is in the economy and how they plan to use their economic tools to address that gap. Otherwise, by always invoking structural reforms, the ECB sounds defensive as if they feel too much pressure to lift growth rates and they want to explain to the public at large that the low economic performance is not really their fault but the fault of governments’ failure to reform.

Wolfgang Munchau writes that if the ECB continues blaming eurozone governments for not implementing structural reforms and continues missing its own targets, the eurozone will end up looking like Japan, but with one difference. Countries whose policy goes off track have nowhere to go. The member states of a monetary union have alternatives. By failing to deliver on its inflation target, the ECB could give member countries a good reason to leave the eurozone: they could have a better central bank.

Ambrose Evans-Pritchard writes that there is no point negotiating. The European institutions have failed to ensure a symmetric adjustment that compels both North and South to take equal steps to close the intra-EMU divide from both ends, befitting their equal responsibility for mismanaging the EMU joint venture in its early years. Italy must look after itself. It can recover only if it breaks free from the EMU trap, retakes control of its sovereign policy instruments and redominates its debts into lira, with capital controls until the dust settles.

Matt O’Brien writes that the euro is the gold standard with moral authority. And that last part is a problem. Both are fixed exchange rate systems that can turn a recession into a depression, because they make countercyclical policy impossible. But people are even more attached to the euro today than they were to the gold standard then. Now, in the 1930s, people equated the gold standard with civilization itself, and were willing to sacrifice their economies for it. The euro doesn’t just represent civilization, but the defense of it, too. After all, the past 60 years of civilization have all been about making sure it never happens again. Europe’s leaders aren’t going to give that up because of a little thing like a never-ending slum.

Economist regularly miss some of the underlying phycology of what is going on here in Europe. One of them is the idea governments must balance their budgets, kinda like the household checkbook. Incredidably, this mindset is instilled in politicians and in the general population. What is also some times missed by economists is the recent efforts of Righties to dismantle the long standing social programs that were put in place by socialists after the War. With grinning teeth,, our anti-socialist friends are using the recession to slash these programs.

Case in point, Belgium. We had our national, local and EP elections at the end of May. The national government is still not in place, but appears to be ready to go in September. Nationalist righties (they call themselves center-right) won a majority and are poised, with Christian Dems, Lib Dems and MR help to ax 17B euros (yep, with a B) out of the budget. In small, tiny Belgium. Every social program looks like it will get a thorough going over to stop all that evil spending. Keep in mind Belgium did reasonably well economically throughout the recession thus far because — socialists held the line on program cuts. Now that the nationalist Righties are firmly in control they openly mock the socialists for all that wild “spending.” Pain is definitely on the horizon for many folks, especially for civil servants.

Spending within your means is the mantra being pertuated by folks who abhor social programs even if it means hurting those who can least afford cuts. Even grannies are not exempt from this. No longer will they be able to travel for free on the partially used public transportation system. We all must tighten our belts is what we are told.

I’ve seen a number of economists explain our situation in Europe as shooting ourselves in the foot. That is very true.

In theory, I agree that we need deficits and government spending to get out of the funk. However, in the real world before spending we need a change of paradigm which has not happened yet.

If government spends more now it is just going to double down on what is already failing us. That’s why I believe we need austerity even if it stinks. This austerity will bring the needed change in paradigm.

If a party is not opposed to the EU, then it is not ‘nationalist’. It may well be right-wing in some sense, but it is not nationalist if it supports the EU regime.

I have a problem with “trend growth” extrapolations to tell us how big the economy ‘should’ be — especially when the time period of the extrapolation includes asset / credit bubbles. Seems like begging a pretty important question.

Such analyses often feed into the narrative that all we need is more GROAF and everything will be just ducky. I have a big problem with that, as it is a ‘solution’ that leaves oligarchy and kleptocracy comfortably in the catbird seat.

I strongly agree, MikeNY. Keynesianism was invented to lure people away from socialism. Instead of an equitable distribution of wealth and power in society, which is what socialism advocates, Keynesianism pushes the idea of infinite growth as a balm that will heal all wounds. But it typically leaves the same corporate/financial oligarchy in charge, even if it temporarily regulates them a bit more. The first great depression was a missed opportunity in the west, so now we have a second one.

Perhaps–but when it was implemented during the post-WWII period in the West it worked fairly well for some time. It is interesting that it has been, in the main, abandoned by the global elites.

The main problem with socialism is that it requires some degree of national unity and communitarian sentiments as well as a cadre of public officials that are rarely corrupt. Those two conditions, at least in the US context is not even remotely possible. Since Europeans seem to want to become American subjects I suspect things are not much different there.

Let’s not forget the ‘Golden Years’ of US capital post-WWII featured a permanent underclass comprising roughly 20% of the population at the zenith, now blown out to nearly double – when you look at job quality, income, debt loads, savings, etc., it’s evident absent major change that half the people in the US will be dependent poor or working poor inside a decade.

Anyway you can find a very telling graph in the Real-World Economics Review blog that compares growth in the US and the eurozone that says a lot about the eurozone failure:

http://rwer.wordpress.com/2014/08/15/how-the-goldman-sachs-guys-and-die-goldman-sachs-frau-2013-wrecked-europe/

In the wars of Banksters vs Labour the former won the battle by all means. With the help of the “independent” ECB, and the bond vigilantes, banksters have managed to charge the costs of bad debt in the shoulders of households. The ECB was blind before the crisis (debt did not matter) and now they declare that it is the fault of governments for not implementing the so called structural reforms. Implicitily, government share they guilt with “spendthrift” households that wanted to live beyond their possibilities.

It is so amazing to realise how miserably the ECB failed and yet they have the guts to lecture the rest of the society. This behaviour can be acomplished only if the ECB is not an autonomous institution but, on the contrary, their hypocresy serves very well the interests of their masters (Banksters all around the world).

The problem is that the EU is politically stunted and lacks the ability to respond correctly to the crisis. Germans feel relatively happy with their goverment just because, by comparison with others, they enjoy low unemployment rates. This gves ground to the bankster-friendly Merkel to impose their rule. Meanwhile, in debt afflicted periphery countries, governments repeatedly fail to aknowledge that a symmetric adjustment (as Ambrose-Pritchard writes) or an eurobreakup are the only solutions.

We are in a slump with numbers where we are trying to meet targets that were blown up by bubbles. Scrap off the numbers created by bubbles in inflation, dot.Com, Debt, Housing and Finance and face a realistic economic market and we would be fine. Stop fleecing the middle class and poor and return the interest rates and home prices back to normal and let the chips fall where need be with deflation. Quit stimulating the supper rich and create opportunity for anyone who is willing to work for it and give back commerce to the independents who want to have their own business. Stop the rectal Cranial Inversions of Politicians and create a long term plan that both parties can follow and stick to it.

This gets all so boring. Europeans don’t have enough money to keep their economies running. So print more money, or sit around making excuses for not printing more money until the people bring out the guillotines. Personally, I favor the second. It’s the only way the excuse makers will learn a lesson.

Yes but I wouldn’t remove the oxide from the guillotines to increase the pain.

I know very little about the Italian economy, so I don’t understand this:

Interesting. According to the U.S. National Bureau of Economic Research, the U.S. recession ended in June, 2009. Most people outside the economics profession (and a few economists, perhaps) consider this to be absurd. The recession in the U.S. definitely did not end in June, 2009, unless one accepts a very narrow, pedantic definition of the word “recession”. I wonder what’s different about Italy, in that the U.S. standards would show that the Italian recession never ended?

http://en.wikipedia.org/wiki/National_Bureau_of_Economic_Research#Announcement_of_end_of_2007.E2.80.932009_recession

http://www.nber.org/cycles/sept2010.html

Up to a point. I fully agree that an honest US national economic data would paint a far worse picture than that sprayed around by MSM. Further, that anything approaching an honest telling of the story of the financial crisis and its ‘resolution’ in the US has to weigh mainstream economists’ views of purported US banks’ strength against the scope and scale of corruption involved in the stabilization and ‘recovery’. Is a system strong by virtue of how many regulations, standards, laws, norms, practices are abandoned in the face of epochal extortion?

Yet I have no trouble believing Italy is in a mess. And Europe. But the chief cause of the problem is the US-based global corporate globalization project itself. First it destroyed European labour. Then it destroyed Europe’s financial system. No amount of Draghi QE will make a Greek or Spanish or Italian worker productive enough to offset the race-to-the-bottom wages inherent when you double, treble, quadruple the labour force he/she now competes in.

Can EU maintain trendline when demographic indicators are going negative?

How much of the “trend” was due to one-time efficiency gains from EU integration?

The focus must be on redistribution, not growth.

There is something about the permanently superior air of Ambrose Evans-Pritchard and other Anglosphere critics of the EU that just doesn’t sit well with me given the UK’s response has been to blow yet another stupendous bubble on the back of the Fed, itself ultimately backed by the US Navy, which controls the world’s trade routes, and that London would shrivel up and blow away if it could not continue in its role as Global Financial Parasite.

Let’s not confuse smarts with power. As noted above, Europe’s problems cannot be resolved if God Himself made policy absent a radical overhaul of the entire framework within which corporate globalization operates. The longer the real threat that is this giant process goes unattended, or worse, ‘pooh-poohed’ as irreversible, inevitable, etc., the worse this is going to get. I guarantee it.

+1

“Global Financial Parasite” is exact. Should be used in their tourist ads!