Philip Pilkington is a London-based economist and member of the Political Economy Research Group at Kingston University. Originally published at his website, Fixing the Economists

Monetarism is a hoary old myth that does its damage in two distinct ways. The first is that, piggybacking on Milton Friedman’s personality, basically an entire generation of economists are actually monetarist in their practical thinking. Greg Mankiw once remarked that New Keynesianism should more accurately be called New Monetarism and a glance at the actual pronouncements of even the more self-critical the New Keynesians shows this beyond a shadow of a doubt.

The second way in which monetarism does its damage is what might be called ‘man-in-the-street-monetarism’. Man-in-the-street-monetarism is the knee-jerk reaction you get from people who have no training in economics (and some people who actually do but obviously weren’t paying close attention!) but who nevertheless read about economic matters and so forth. When they hear ‘money printing’ they instantly think ‘inflation’. This can interfere with conversations at dinner parties but it also infects the journalistic media. In its more extreme forms it leads people into economic cults like the neo-Austrian school that has become so popular on the internet after the financial crisis. These poor suckers are then sold gold and other dodgy investment vehicles by industry frontmen.

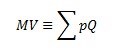

The essence of monetarism is in the transformation of an identity put forward in Irving Fisher’s classic 1911 work The Purchasing Power of Money into a supposed causal relationship. In that work Fisher laid out the following identity:

That equation reads: “The amount of money, M, multiplied by its velocity, V, is equal by identity to the sum of the quantity of goods and services purchased, Q, times the sum of their prices, p.” Note the clause “equal by identity”. The equals sign with an extra bar indicates that this is a tautological statement. It simply must be true. In the book Fisher discusses a number of ways in which this identity might hold. I think that while Fisher’s discussion was far more nuanced than the monetarists that grew out of the 1960s and 1970s it is nevertheless quite misleading. I lay out this argument in the chapter on money in my forthcoming book.

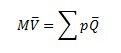

The monetarists proper converted this identity into a behavioral equation. This equation ran as follows and should be read running from left to right:

Note two things. First, the fact that we have converted the “equal by identity” sign into a standard equals sign. This implies causality running from left to right. So, the left-hand side of the equation causes the right-hand side. Secondly, we have placed ‘hats’ on the velocity and quantity variables. This implies that they are to be thought of as fixed. Thus the equation reads: “The sum of prices is equal to the quantity of money”. We understand the sum of prices here to be the Consumer Price Index (CPI).

Even when Friedman first came out with these statements they were showed to be empirically vacuous in the classic empiricist, anti-monetarist text The Scourge of Monetarism by Nicholas Kaldor. But today we have easy access to these statistics and can quickly run the relevant regressions. So, let’s see how monetarism fairs when confronted with the facts today.

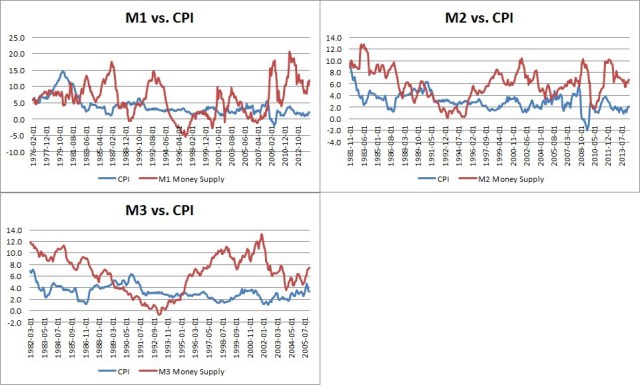

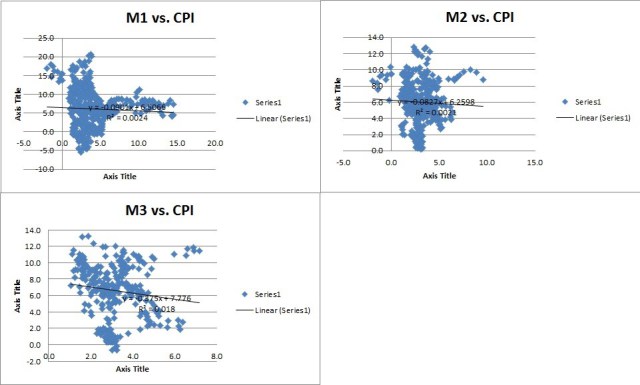

First it should be noted that one peculiar feature of monetarism is its vagueness. When monetarist policies were implemented in the late-1970s and early-1980s and did not have the intended effects, monetarist economists began to cast doubt on the measures being used to calculate the money supply. Any time the policy didn’t work the economists would say that the central banks were not measuring the money supply properly. This is a classic use of theoretical argument to immunise marginalist economic theories against empirical criticism and was a tendency much discussed by the neo-positivist philosopher Hans Albert. For this reason we will include three key measures of the money supply — M1, M2 and M3 — and plot them against the CPI to give the theory the best possible chance to come to empirically verifiable conclusions. All the data that follows comes from FRED and the years chosen are based on availability.

Let us first lay these out in a standard graph form to see if we can intuitively spot any correlation. All graphs measure percentage changes year-on-year of both variables mapped. The reader can click on the image to enlarge it.

Oh dear, oh dear. Typically we should be able to pick up any correlation intuitively but in the above graphs — which represent all the data that FRED provides on the various money supply measures — we really do not see much to be hopeful for. Nevertheless, let us run some simple regressions to see if there is a correlation hiding in plain view that our all-too-human faculties have missed.

Oh no! This is very bad news for our monetarist friends. First of all, we must note that if the monetarist theory is true we should see a positive correlation between the money supply and prices. That is, when the money supply rises so too should prices and vice versa. This would be indicated in the regressions by an upward-sloping trendline. But in all three regressions we see a negative correlation indicated by a downward-sloping trendline. Embarrassing!

Secondly, we should note that the correlation coefficient, annotated the R-squared, is very, very weak in all three regressions. This is reflective of the intuitive fact that the graphs we laid out previously showed no significant relationship between the variables. Thirdly, we should note that the generally favoured measure of the money supply by monetarists is the M3 and in our regressions the M3 had the lowest correlation coefficient and the most substantially negative relationship. If these regressions are anything to go by we should more so expect prices to fall when the M3 grows!

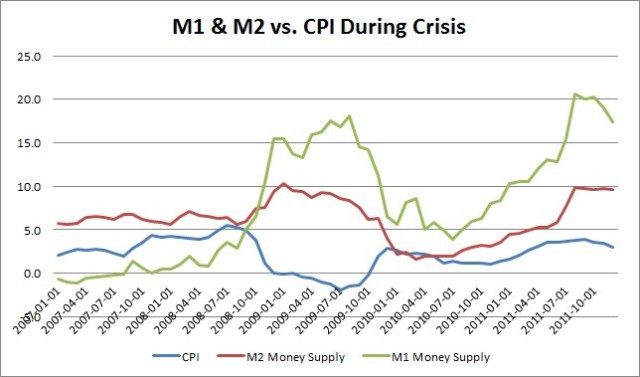

But before we take our leave from monetarist fantasyland let us zoom in on the best ‘natural experiment’ of the thesis that we find in the data: namely, the extreme events surrounding 2008. Here is the data for the M1 and the M2 plotted against the CPI for that era (data for M3 is not available as it was discontinued in 2005):

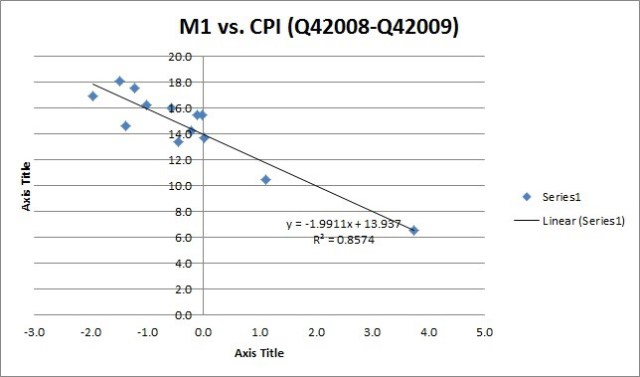

Again, the data seems to run entirely contrary to the monetarist theory. Recall that above we read the monetarist equation to say that an increase in the money supply causes a rise in prices. But here we see both money supply measures rising toward the end of the 2008 as prices fell. This runs exactly contrary to what the monetarists would have you believe. Indeed, the negative relationship between the M1 monetary base and the price level is extremely statistically significant. Here is a regression plotting that important 12 month period:

All we can conclude from this is that monetarist theory — whether in academic form or in its man-in-the-street variant — is deeply, deeply misleading. The real world facts seem to run exactly contrary to the theory. Indeed, I do not think you could hope for a stronger refutation of any theory by engaging in data analysis. And yet the theory will continue to live on, zombie-like in the minds of academic economists, the media and the general public. Why? Why did this doctrine impose itself on the minds of men, especially in the 1970s and 1980s?

This, I think, is when ideology comes to play a role. I have documented some reasons for the rise of monetarist doctrine in this era on this blog before and readers can consult that particular post. But that post mainly focused on the case of the UK. With regards to the US James Galbraith and William Darity Jr. put forward the following argument as to monetarism’s supposed adoption by the Federal Reserve in the late-1970s and early-1980s in their excellent textbook Macroeconomics:

The Federal Reserve was no more monetarist in the early 1980s than it had ever been; it merely found for a time that monetarist arguments could be used to justify a severe credit crunch, and resulting recession, when these were felt necessary to bring a rapid end to inflation. (p244)

Amen to that!

The real economy exists within a box called the world. It is physically restricted by available resources.

Money, on the other hand, is an abstraction; we can in fact make limitless amounts of it. That’s why economists are under the delusion that an economy can grow without limit: because money can, and that seems to be all they care about.

So we have limitless money chasing limited resources. Isn’t that the basic formula for inflation?

Haalp*!!!

Can’t read post past Solow quote, as it induces all the conversations this topic covers I’ve ever had, with the brunt of that one liner…. in… an all at once epic and debilitating flash back.

skippy… absurdly delirious with just the right amount of mental anguish… to make it even funnier….

PS…. yes public perception of taxes facilitated it [usual crowd beating that ideological drum], Nam, and the Tradies shot themselves in the foot by mimicking the structures they fought against as a separate identity, rather than a more European integration of the two.

Pilkington really messes up here.

He’s dealing with a globally used currency, and he’s only looking at US inflation data.

Brutal.

Pilkington must be aware that the massive monetary expansion post-2001 had serious inflation consequences around the world. e.g. Egypt had pegged to USD and was running double-digit inflation by 2010.

If your talking about the implantation of the neoliberal Washington Consensus – monetary expansion – it really needs to be unpacked much further than Egypt’s currency peg to the USD. You could include Turkey for example w/ the increase in financialisation after rapid privatization, liberalizing the capital account, credit expansion and ensuing bubbles.

skippy… repeat this template wherever they try and spread cough…. democracy… around the world.

Egypt had pegged to USD and was running double-digit inflation by 2010.

You’re making precisely the mistake Phillip just addressed by assuming that if Egypt experiences inflation it must be a monetary phenomenon due solely to U.S. policies. If you had looked more closely you would have realized that the Egyptian Pound is tightly managed, which means the exchange rate is a policy variable chosen by the Egyptian monetary authority. You would also have noticed that Egypt experiences domestic production shortages which drive up the general price level.

The argument that inflation is driven by monetary policy because monetary policy drives inflation is rather circular.

“The sum of prices is equal to the quantity of money”. We understand the sum of prices here to be the Consumer Price Index (CPI).”

CPI ?? Always a changing, 100 unit-based, price mechanism ??

Sooooo, a sum (of prices) is equal to……an index ????

S = I………..again?

Or, is it that the quantity of money is equal to the CPI ??

Is this somehow more simple than it sounds ?

Wouldn’t GDP = money supply be closer to the construct …..

as the money-value of all goods and services must approximate the exchanged money supply as this metric includes its velocity?

I got a chuckle from that statement, too. The Consumer Price Index is a model. Some humans make a judgment call about what components are important and how to include them. It is not some natural law or mathematical identity, and it certainly doesn’t sum all prices.

What confuses me is whether the proof here is that inflation is not always a monetary phenom, or that monetary phenom don’t always track ( = ) consumer price phenom.

If the monetary phenom of growth is taken in the asset owning, financing sector, then how can the cpi come into play?

There are many uses of the purchasing power of money that escape the consumer price measure. The lack of any ongoing correlation between money supply growth and consumer prices seems almost guaranteed for that reason.

The main problem with that 80s quasi-monetarism was its failure at string-pushing to control monetary policy, trying to use interest rates to control the money supply, to stabilize the economy.

That don’t work. What will?

OK, I’ll say the FAIL here in a different way.

The statement that : “Inflation is NOT always a monetary phenomena”, can only be proven by showing actual “inflation” that is not associated with any “monetary phenomena” (an increase in the money supply).

Anything like that here?

Nope.

Did you forget what you were trying to prove with all those heady-looking scatterings?

Please, present some causality of what is claimed to be proven-false.

Like, that inflation is not always money related.

Thanks.

PhilPil is looking an annual rates of change (which are quite noisy) and finding little correlation.

On the other hand, plot absolute values of M2 and CPI over a few decades, and the correlation is excellent.

http://pithocrates.com/wp-content/uploads/2012/04/M2-and-CPI.png

During the 50 years from 1959 through 2008, the M1 money stock rose by a factor of 11, while the CPI rose by a factor of 7. Why else did this explosion of prices, which distinguishes the 20th century from all other centuries in history, occur?

The burden is on those who claim expansion of the money stock didn’t cause the Great Inflation to show what DID cause it.

My data is monthly calculated at annual rate of change.

If you think plotting two increasing variables against each other measured in different terms (dollars and an index set to somewhere around 2000=100) is evidence of a correlation I cannot help you.

So to clarify, are you denying that dollar prices have increased significantly, or are you suggesting that something other than printing dollars is responsible?

Dwyer and Hafer examined IMF data for eighty countries. They found:

‘Correlations between inflation and the growth of money relative to income are 0.92 for 1987-92 and 0.84 for 1992-97. The correlation between changes in inflation and changes in the growth of money relative to income [between the two 5-year periods] is a slightly lower 0.78.’

http://www.frbatlanta.org/filelegacydocs/dwyhaf.pdf

That’s because the authors estimate changes in price level by a ratio of nominal to real income, rather than actually looking at prices. Now put your thinking cap on and ask yourself about causation in an economy with an endogenous money supply.

Whilst adjusting my cap, I kept thinking about ‘causation’ and an endogenous monied economy, but I couldn’t help also thinking about the data, and the overall correlation in the Atlanta fed data and there being nothing said about ‘causation’.

So, why exactly, should we be thinking about credit-monied causation, and what is causation there?

There is still correlation at the cumulative level.

But, certainly, the monetarists are wrong.

The data prove that.

Keep working. I’m not here to hold your hand.

Got it. You have no reason to raise ‘causation’ as an economic phenom, but, presenting it here confuses the data that correlates money supply and overall prices.

Well done.

Was not the purpose of this posting and your comment to cast broad aspersions on that ‘hoary old myth’ of ‘monetarism, by somehow disproving the Quantity Theory’s underlying, and related, equation of exchange.

Phillip provides a link to Fisher’s ‘Purchasing Power of Money’ e-edition and we can only hope all take a read of that which well informs this discussion.

There:

“”The chief object of this book is to explain the causes determining the purchasing power of money.””

And:

“The so-called “quantity theory,” (*13) i.e. that prices vary proportionately to money, has often been incorrectly formulated, but (overlooking checks) the theory is correct in the sense that the level of prices varies directly with the quantity of money in circulation, provided the velocity of circulation of that money and the volume of trade which it is obliged to perform are not changed.””

*13.

This theory, though often crudely formulated, has been accepted by Locke, Hume, Adam Smith, Ricardo, Mill, Walker, Marshall, Hadley, Fetter, Kemmerer and most writers on the subject. The Roman Julius Paulus, about 200 A.D., stated his belief that the value of money depends on its quantity. See Zuckerkandl, Theorie des Preises; Kemmerer, Money and Credit Instruments in their Relation to General Prices, New York (Holt), 1909. It is true that many writers still oppose the quantity theory. See especially, Laughlin, Principles of Money, New York (Scribner), 1903.”

Perhaps, add: Pilkington and Johannson 2014

You should probably take a peek over at Phillips blog and review – engage in the comment thread.

Skippy… Myself… assuming the mental position of a deity and laying claim to tautologies as divine dicta, wellie…. the bones man, good gawd… look at all the bones [!!!].

“Plot absolute value” can mean anything. You have a habit of linking charts without context, methodology or data source cited, which makes them not worth the paper they aren’t printed on.

Secondly your assertion that CPI increases in the 20th Century are the greatest in history is remarkably disingenuous given that A) CPI did not exist prior to that century and B) the 20th Century is the first in which comprehensive data were gathered on the subject.

Have you ever seen Global Financial Data’s series on ‘data from the United Kingdom on wheat and other agricultural [prices] back to the 1200s’?

https://www.globalfinancialdata.com/Databases/CommodityDatabase.html

Ever heard of David Hackett Fischer’s The Great Wave: Price Revolutions and the Rhythm of History?

Sixteenth century Spanish inflation caused by the import of New World gold is no myth.

When it comes to economic history, one starts by reading the syllabus.

Nothing in this comment even remotely addresses my reply.

Well, okay, but only if you didn’t say that there was no consumer sector price change data until the last century, for some reason.

Then, fine.

You would do well to pay attention.

A) CPI did not exist prior to that century and B) the 20th Century is the first in which comprehensive data were gathered on the subject.

A book on prices published in the 20th Century does not qualify as comprehensive data gathered in previous centuries. It doesn’t go back in time for source material.

Perhaps not. ( sufficiently ‘comprehensive’, given modern tools for collection and analysis).

But the good data subsequent those tools (Atlanta Fed) bear out the bad data from when hardly anybody was looking. The proof is thus in the pudding.

Maybe the question should be whether Phil’s data….reflecting an obvious lack of correlation between very short term “changes” in prices and money quantities are superior to those presented by the money economists at the Fed, with their broad cumulative ‘quantities-related’ data, or not.

Has Phil’s data indeed lain waste to that ‘hoary old myth of monetarism’.

This book is historically problematic. So, should be put forward as an implicit counterexample to Piilkington’s thesis, whatever one may feel about Phil’s thesis itself.

Not a prop for this particular data vendor, but as they point out:

Inflation data for the United Kingdom goes back to 1209, further back than any other indices available. The inflation index for France dates back to 1431 and the Netherlands back to 1450. Inflation indices for the United States stretch back to 1720 and inflation indices for most major countries go back to the 1800s.

Subscribers can measure the impact of inflation on the rest of the economy by using GFD’s long-term monetary aggregates to discover the causes of inflation.

https://www.globalfinancialdata.com/Databases/Data.html#Inflation_to_1209

Are you paying attention at all? Your records dating back to the 13th Century concern certain individual commodities. It is not possible to extrapolate changes in the general price level from such a limited data set.

Even in the 13th C. there was gross inequality. The Doge of Venice extracted the difference from the least able to defend themselves. Times that by hundreds of city states all over Europe. Capitalism always worked. For the rich, aka the merchants, aka the mercantilists. But capitalism has never worked economically or environmentally. Ergo inflation is an inherent outcome of capitalist economics. Profit is just too expensive. And at some point, like now, it cannot be balanced out.

Unless of course capitalism is atomized down to its fundamentals. So every person is a capitalist. But not a fake, absurd, idiotic capitalist.

Susan I’m not referring to inequality, only whether the records of the time can tell us about changes in price levels. They primarily relate to us how much it cost monks to eat, which doesn’t help us to reach the goal.

It’s better to use YOY percentage changes because plotting the absolute time series numbers together raises a big issue of auto-correlation that artificially increases the R-squared

I’m not a mathematician, so I’m curious about this statement. I thought autocorrelation was more a problem with repeating patterns within a range rather than with series that maintain a positive (or negative) slope basically continuously from beginning to end. Isn’t that one of the simplest forms of correlation, two series that both increase over time? I thought time was used quite frequently precisely because the passage of time is as close to an independent variable as we can get. Are you saying that the age of a child and the height of a child are not positively correlated because of autocorrelation?

Whether the correlation coefficient is .82 or .91 or .65 is largely irrelevant to the main point – indeed, the false precision of numbers is one of the primary problems in academic economics. I think that’s why the mind is repulsed by simple time series: it quite clearly demonstrates that ‘M2’ and ‘CPI’ are not independent variables. Over time in the recent past, they have both been rising.

no reply ??

I wonder if anyone will offer an explanation of why prices have risen so much, especially during a period of massive productivity growth?

* sound of crickets chirping *

Nice try smoking them out, though!

Eveeyone has but you don’t listen. What is it with you right libertarians that everything distills down to a binary explanation? Why on earth would you even consider the nonsense idea that rising prices throughout history must have only one cause? I’ve lost track of the number of times people have explained to you that prices fluctuate due to employment, exchange rate, wage changes, effective demand and resource constraints.

And yet the next time said subject comes up you will once again pretend no one has ever given you an answer. At this point I seriously question your ability to retain and internalize information that conflicts with your ideological biases, which demonstrates that I’m relatively dumb in that others gave up on engaging with you long ago.

Dwyer and Hafer at the Atlanta Fed, using a hundred years of evidence in the US and UK, and 60 to 80 years in Brazil and Chile, find a clear relationship.

‘Inflation is associated with growth of money relative to real income. This relationship holds across countries with quite different economic and political experiences. Substantial changes in inflation are associated with changes in the growth of money relative to real income.’

http://www.frbatlanta.org/filelegacydocs/dwyhaf.pdf

Please read and retain — there is going to be a pop quiz later this week. Don’t make me call your mom about your attitude problem.

Already addressed, please stop wasting others’ time.

Already addressed?

You DID get the point right?

“‘Inflation is associated with growth of money relative to real income.”

And we know where real income is going.

Inflation IS correlated with monetary ‘phenomena’.

Are we trying to confuse this reality?

It’s unfortunate we are talking past each other, but you are right on one account; I don’t comprehend the words you just wrote.

I’m not saying that prices are fluctuating up and down. They are increasing, dramatically, to the point that housing, healthy food, higher education, healthcare, and so forth are far more costly today than a few decades ago. That has happened in spite of massive productivity gains from personal computing to telecommunications, a sustained decline in the employment to population ratio, the ongoing 21st century transition of the workforce from permanent to temporary, and a general level of global geopolitical stability. It’s not like a world war or asteroid impact destroyed half our hospitals, schools, and homes.

As far as right libertarian, I hope you don’t mean that as name calling, because resorting to personal attacks is pretty much the definition of being frustrated by the available facts.

It is also hilariously inaccurate, unless by libertarian, you simply mean anyone who is fed up with the current two-party system, and by right, you mean someone who thinks the federal government shouldn’t give so much corporate welfare to highly compensated employees in defense, finance, agribusiness, healthcare, energy, academia, and so forth. Which, by the way, is a plurality of all Americans. More people identify as Independent than either the Democratic or Republican parties.

Basically, if you are suggesting that the Declaration of Independence, the Constitution, the ACLU, the Social Security Act, and so forth, are right libertarian ideas, then, well, I guess I’m guilty as charged. Yes, sorry, my ideological biases say that torture is wrong, even if reducing the military budget would result in the Unspeakable Evil of Austerity.

Right Libertarian, or Left Libertarian…..no matter.

If you don’t agree, you’re an uninformed wacko, debasing the currency of these pages.

Read Mosler’s critique of FT’s Martin Wolf’s call to end fractional-reserve banking and private money creation………..

There(Mosler)……Full-reserve banking becomes the gold standard…..when, in reality, it’s entire purpose was to replace the gold standard with a civilized “standard of stable purchasing power”.

Wolf becomes a “Gold-bugger’. And a bit of a crank.

No comments allowed by Warren.

Both of these constructs derive from Fisher…..either his 100 Percent Money proposal or his Quantity Theory and underlying “Equation of Exchange”.

Dare to disagree?

Must be a totally misinformed wacko………either Right Libertarian, or money crank……like Wolf.

the correlation you cite is consistent with inflation resulting in an increase in money supply.

Without disagreeing about monentarism (unlike some people, I can point at periods where gold currency has led to inflation), when you write “the sum of the quantity of goods and services purchased, Q, times the sum of their prices, p.” Your equation reads not (\sum_i Q_i ) (\sum_j p_j) — which is what you say — but instead the correct \sum_i Q_i p_i

If I buy two $100,000 cars and two 25 cent eggs, I pay 2 x 100,000 + 2 x 0.2, not (2+2) * (100,000+ 0.25). Your equation is fine, but the prhasing needs a little tuning.

Sorry I’ll stick with my economic cult. At least it isn’t bringing about a global economic collapse.

Which cult is that? Any economic cult that’s not leading to global economic collapse is at least worth a look…

Seems to me prices are a function of spending, not the quantity of money, so the equation seems fundamentally wrong from the get-go, but I’m not an economist so…

Still, looking at the system from the point of view of a mechanical engineer, that equation makes little sense wrt any real-world system and, as expected, is pretty much useless.

If you want to look for a correlation that may point to causation we should look at the relationship between G and GDP… those series track in a more or less linear way…but we aren’t allowed to think government plays any role in a “free-market” economy.

https://dl.dropboxusercontent.com/u/33741/FGEXPND%20to%20GDPI%20log.png

As for inflation, I see it as a natural consequence of growth with finite resources and not enough competition…we have too many monopolies…big business hates competition and has the power to do something about it.

I just love the truth in this line:-

“but we aren’t allowed to think government plays any role in a “free-market” economy”

it’s like whole nations have been forced to wear NeoCon Zombie Helmets that alter the natural functioning of brain wave activity in order that government can never be perceived as a creator of money! Scary! The horror movie that has out-grossed any previous ones in the genre!

@Schofield

I do believe we’re conditioned from birth to believe in nonsense that promotes the status quo no matter how unbelievable. We just can’t believe our lying eyes.

Some of us are more resistant to programming against reason. My so-called “liberal” friends (not to mention the conservative ones) become visibly agitated if I suggest that maybe we aren’t ever going to “run out of money” or that maybe shopping at Walmart or Amazon may not be in our own best interests. Neoliberalism has taken root to the fullest possible extent.

But but but…inflation.

Most people won’t be convinced otherwise until they’ve lost everything they hold dear…and even then it’s a toss-up.

Paul– The link doesn’t work for me. I’d be interested in seeing it. Thanks…

Dan,

Odd…it works for me when I click on it.

Try this Evernote link…

https://www.evernote.com/shard/s82/sh/0acf438f-5a29-4065-97f5-cc98ce8da9b6/b582418cdbec9399af26beda51b95c4c

Hi! Congrats on the blog.

I find the analysis could be more comprehensive if the correlation with changes a few months/years later were calculated. Maybe the expansion in monetary base causes CPI growth with a delay?

Mind you, I’m not monetarist (just the other day I was reading about the disaster they caused Chile in the 70’s) but the M2 graph looks a bit like what I’m saying.

I take this opportunity to present John Hussman’s perspective that monetary policy is just fiscal policy with another name, All the attention to the Fed is only useful because the others think it’s relevant: http://www.hussmanfunds.com/html/fedirrel.htm

I just have to ask: how is money velocity measured? Km/hr…light years…? I never figured out quite how that one got measured.

Velocity is a ratio of nominal GDP to a measure of the money supply (M1 or M2). It can be thought of as the rate of turnover in the money supply–that is, the number of times one dollar is used to purchase final goods and services included in GDP.

If, for example, in a very small economy, a farmer and a mechanic, with just $50 between them, buy new goods and services from each other in just three transactions over the course of a year

Farmer spends $50 on tractor repair from mechanic.

Mechanic buys $40 of corn from farmer.

Mechanic spends $10 on barn cats from farmer.

then $100 changed hands in the course of a year, even though there is only $50 in this little economy. That $100 level is possible because each dollar was spent on new goods and services an average of twice a year, which is to say that the velocity was 2/\text{year}. Note that if the farmer bought a used tractor from the mechanic or made a gift to the mechanic, it would not go into the numerator of velocity because that transaction would not be part of this tiny economy’s gross domestic product.

Skippy… time and space…

And if you want to see further evidence why assuming monetary velocity constant is a grievous error, check out the following…it’s FAAAAAaaalllinnnngggg…clunk

http://research.stlouisfed.org/fred2/series/M2V

“When they hear ‘money printing’ they instantly think ‘inflation’.”

This seems to be where a lot of leftist economic thought has drifted. Use a different definition of a word, and then complain that not everybody desires to use your definition. It’s semantics. If one person approaches expansion of the money supply as inflation, and another says a rise in the general price level is inflation, who cares? It’s make-work for academics and obfuscation for the actual problems we face.

The question with actual application to real people inhabiting our system of political economy is why does a decent standard of living cost so much?

Climate change and peak oil, and generalized looting due to financialization are the answers to your question about the standard of living

Interesting suggestion. Aren’t all of those caused by government spending? I’d agree with financialization, not so much climate change and peak oil. Those are primarily future risks, not historical explanations, I’d say.

Climate change is driven primarily by 1) public policy that diminished our rail system in favor of car commuting, long haul trucking, and other energy inefficient means of transport; 2) public policy that supports fossil fuel usage in electricity production over other types of electricity production that produce fewer GHG emissions (such as wind and solar); 3) public policy that under-funds investment in infrastructure that would waste less energy (like improving power grids); 4) fossil-fuel based agribusiness subsidies rather than local, small scale farming; and 5) a national security state that is the biggest user of oil on the planet, both directly and in terms of the energy it forces other countries to use to counter it and the extent to which US foreign policy in environmental action is undermined due to hard feelings about US power projection (and the fact that the US elite themselves don’t care much about climate change, as evidenced by the US federal budget itself).

Peak oil hasn’t even happened yet, but to the extent it will, it will matter precisely because public policy has created a society dependent upon oil when alternatives readily exist, particularly for transportation, real estate development, and electricity generation.

As far as generalized looting due to financialization, well, that’s pretty much where the net deficit spending that wasn’t for the national security state went, especially over the past couple decades. That’s about as direct a link as it gets from ‘money printing’ to ‘inflation’.

I thought you meant it as in, why does a decent standard cost so much right now. Climate change and peak oil, and finance have combined, in the figure of droughts, speculation in commodities markets + increased fertilizer and transport costs to drive the prices of commodity agricultural products way up.

And it cascades from there.

Yeah, I do mean right now – I disagree that peak oil and climate change are relevant factors in price increases that have happened to date precisely because I see our situation as one struggling from a distributional matter rather than one of aggregates.

In other words, I’d say that healthcare costs more because gatekeepers are skimming funds for their own personal benefit, not because those funds have been consumed by peak oil.

Hey, I thought you were a Right Libertarian.

It’s the Right Libertarians who equate growth of the money supply with the definition of “inflation”, and have so little regard for price stability.

Now I’m confused.

Ha, yes. But seriously, I think the reason I hit a nerve from time to time on this subject is that I don’t see the value in the Inflation Good/Inflation Bad pie fight (or it’s odd rabbit hole derivative: Inflation Is Happening/Inflation Isn’t Happening).

Aggregate solutions just don’t matter that much when the problems we face are distributional in nature.

What has always disturbed me about the monetarist explanation of the relation between the money supply and the CPI is the conflation of supply-demand price increases that result from external changes in factors of production and the values expressed in consumption and the monetary-driven price increases that result from “too much money chasing too few goods and services”, to use the popularized expression of monetarism.

But what is causing this reevaluation of monetarism today seems to be the fact that we have been living the past decade in a deflationary economy in fact that is still being analyzed as if it were inflationary or subject to a sudden spike in inflation just from the action of government.

In the meantime, we are allowing infrastructure to deteriorate of using military force to destroy infrastructure globally and disrupt societies, which in real terms increases the cost of doing business in those areas. And that is not incorporated into any monetary models. How money is used is as significant as how much money is used in evaluating effects on price increases and decreases.

Christ’s Empire: Placement, Discernment, & Perspective

An individual turns the consumer moneylending trade on its head, back when real risks existed, and the Eunuchs for Christ try to build an empire in his name, to eliminate their own risk. Global communication was built to jump those artificial empire borders, and the Bay Area Rockstars are employing it to build more concentration camps within concentration camps, to print more money.

And the biggest complainers are the beneficiaries, carrying around SMART technology to spy on each other, complaining about the resulting income inequality. So, Japan is the latest failure, to save America from itself, but here comes the big bad bear from the north, in yet another currency war, after yet another demographic collapse, leading to another war, which changes what?

Of course the emerging markets, copying the demographic boom/bust financing of the more mature scale economies are being crushed, with best business practice of FILO feudalism. Depleting long-term natural resources for short-term material gain, employing the planet as an ATM, is the whole point; employ the critters like bulldozers and discard them when the job is done.

“Procyclicality and Structural Trends in Investment Allocation in Insurance and Pension Funds…accountancy and regulations have been introduced that accentuate these human foibles…they have bought bucketfuls of bonds in the teeth of what might be the biggest fixed income bubble…short-termism is slowly but surely being hard-wired into the financial system.”

“[L]ongevity is the defining challenge of our age…having a seismic effect on the way we live…straining budgets and skewing markets.” “Lord Livingston, the Trade Minister, has also warned that the City should expect some pain from the ban on certain Russian companies tapping international markets.”

On one end of the feudalist spectrum, you have monopolies paying themselves to print money, living on the other end, individuals competing with billions of other individuals on a credit gradient up to 25%, and the only growth is coming from those not complying, denied access to established credit channels. Where do you suppose organic growth really comes from, and what do you suppose is going to happen in the middle?

From the perspective of labor, leadership is about taking individual initiative, ownership, and the consensus, the status quo buffer of feudalism, is always in your path, installing yet another toll booth. Engaging the consensus to get anything done is like messing with someone else’s horse, expecting it to consider your interests, given that it cannot consider its own interest, while in captivity.

Consensus at the top is not dissimilar to what you see in public education, children grouping up out of insecurity, and bullying the remainder to step in line, a copy of their parents. University simply concentrates the stupidity into specialties. The last critters you want in charge of your children’s education is the committee consensus, using each other like disposable rungs, on a ladder to nowhere.

“We tend to get so focused on size in this world. How many Facebook friends we have, how many people come to our party, how many contributed to our cause…Because whenever we label something as “big” or “small” it’s always a comparison to something else. Comparison is dangerous because it’s about more or less. It pushes us either toward pride or insecurity…Be certain that your work is beyond measure.”

All empires are clocks, operated by civil marriage, feudalism of, by and for feudalism. Relationships only follow behavior, which only follows the law, to leverage the gravity of History. The critters are always marching into History, but that’s no reason to join the crowd. How much gravity you want, of which there is never a scarcity, depends upon your development.

Have you ever poured slow-cooking oats into boiling water? That’s gravity and that’s technology. All empires are cheap imitations of life in a mirror, competing to avoid parenting themselves. Of course they are coming for your children. Prepare your children accordingly, to walk right through the war, with the necessary spirit to jump the intellectuals, trapped in their own false assumptions.

The problemsolution of technology is that the individual serves the machine, instead of the other way around, in a bait and swap, which makes those who print the money, those who establish the law, and those who follow the law irrelevant, other than as an extension of gravity. Look at the patient charts and outcomes, not the data collected for the purpose of extending fiat. The critters use each other as lab rats, assuming that the behavior is normal.

You are not going to replace the integral with a cheap derivative simulating it. No matter how many timers you try, you learn nothing, but the convention of comical constants, false assumptions embedded in public education by doctors for the purpose. Look at the history; healthcare has always been a scam, perpetrated upon those who turn to superstition, the short cut, by those taking the short cut before them.

Begin at the beginning, your own perspective, or be paid in debt to become derivatively irrelevant. Don’t attempt to impose feudalism upon labor and expect anything other than death as ROI, slow or quick, pick your poison. Silicon Valley is welcome to all the dead inventory it can carry. Build just as many “state of the art” hospitals as you like, in the face of demographic collapse.

Don’t leave us hanging! Tell us where you learnt to write exactly 3 lines and a half at a time!

Holy smokestacks! Not one false word.

Since you asked. Personally, I tried pouring oatmeal into boiling water but I didn’t like the taste or texture. Then I tried pouring into cold water and heating it all up at once. That worked! Much much better. But it’s a lot of work either way. No I get breakfast out at a food bar == French toast and berries usually.

lots of berries in bear country; no need to go to a food bar. healthcare is having a smoothie.

In trying to understand the post and it’s discussion, it’s unclear to me where debt/credit falls.

Given that all money is endogenously issued, as a debt/credit, the growth in what we call the money supply, always M-1, sometimes M-2, means that we are equating ‘money’ growth with credit/debt growth, more or less axiomatically.

How its – issued – being the key dynamic, the other is to what purpose.

My guess…..

“it”, being money, is issued as a debt (loan) by a private bank, to a borrower.

So, that’s the key dynamic….ok.

If I understand, the other dynamic is ‘to what purpose’.

On the smaller scale, the purpose of this loan is to provide whatever it is the borrower needs.

On the larger scale, the purpose of debt-based lending is to maintain the status quo.for as long as possible.

Your guess?

.

Myself when young did eagerly frequent

Doctor and Saint and heard great argument

About it and about: but evermore

Came out by that same door as in I went.

The True Monetarism

by D. Tremens, unofficial economist and analyst of things remote to the mind

Professor P. is correct. but This is all fake monetarism! It’s nonsense produced by people who are victims of a mental disorder. The disorder in this case is “The ascension of the absolute”. It take over the brain: 1-thing and it transfixes the feeble mind! It’s a hypnosis. The real monetarism is E = MC^2, where M = money and E = economic activity and c = cooperation and 2 = squared. That’s at least 3 things. Don’t worry.

when you increase M with C constant, you get more E. However, when you increase M and C declines, you get either the same or less E.

if you get more E but not as much as the rise in M, you have inflation. If you get more E than more M, you get Groaf or Growth, depending on C.

Sorry to make you guys think this hard. I know it hurts.

If you take the derivative of the equation, you get dE/dC = 2MC. That makes it easier to see the relations between M and C. Or rather, the interaction, since it’s not like M = F of (C). Don’t tempt me like that. Instead M&C interact with a slight positive correlation, estimated at 0.2., but it doesn’t always work.

Everybody should understand this is true just by channeling it.

-QED

not to nitpick but correlation coefficient = r;

r^2 = the expalantory power of the regression model

but the overall idea is right

I stopped reading after the 2nd equation, because the “math fails” had already reached critical level at that point.

[On eqn 1:]

That equation reads: “The amount of money, M, multiplied by its velocity, V, is equal by identity to the sum of the quantity of goods and services purchased, Q, times the sum of their prices, p.”

The equation clearly has the sum of products on the RHS, which is very different than the product of the sums. FAIL.

Note the clause “equal by identity”. The equals sign with an extra bar indicates that this is a tautological statement. It simply must be true. In the book Fisher discusses a number of ways in which this identity might hold.

So first it *must* be true, then hard upon it *might* be true. Which is it? FAIL.

The monetarists proper converted this identity into a behavioral equation. This equation ran as follows and should be read running from left to right:

fisher-equation2

Note two things. First, the fact that we have converted the “equal by identity” sign into a standard equals sign. This implies causality running from left to right. So, the left-hand side of the equation causes the right-hand side.

Where did you learn mathematics? There is no causality implied in a mathematical equality – the statement “A = B” is just what it purports to be: “A equals B”. Hence B = A. Once again, FAIL.

If this is in any way representative of the level of “mathematical” discourse which occurs in mainstream economics, then things are dire indeed, especially in light of the disproportionate influence economists have on real-world policymaking.

You may have gotten to the bottom of a lot of our problems – though it was obvious for other reasons that modern economics (I exempt basic market theory, which is really just applied feedback theory) is mostly horsepuckey.

You also have to keep in mind that the equations are mostly window-dressing; taking them too seriously, unless they involve real-world numbers, is a big mistake. Yves already confirmed this for me, with a LOL.

Or is it representative of PP’s level of mathematical discourse?

Business managers cause inflation, not the quantity of money. The quantity of money is not an actor in the economy. Someone has to raise prices, and they are the price-setters in the economy.

Prices on goods and services for sale are set by the business manager. She examines her estimates of future demand, the cost of operations and overhead, and sets the price. If we were to sum all these transactions across the economy we could see how prices rise. If prices are regularly adjusted higher, over several time periods, then this is referred to as inflation. Whether consumers choose to purchase is not relevant. If they decline to purchase this will harm to business prospects of the company, but will not change the price trend.

Business managers are always in control of prices. In an extremely simple model, if all business managers in a display of solidarity, never raised prices ever again, no matter the consequences to their business, then inflation would be zero, always. Only when business managers raise prices over several time periods will the consumer see inflation.

The quantity of money plays no direct part in the price setting process. Business managers will not visit the FR website, examine M1or M2, and set their prices; rather, they will look at their costs of production and the demand for their output and estimates of the future, and set prices accordingly. So prices are determined by the interaction between demand and the supply of goods and services, which is generated transaction-by-transaction at the level of individual buyers and sellers.

The quantity of money only affects prices indirectly, as it: changes the cost of financing and influences investment in new production; or changes the attractiveness of saving, and how these affect employment and consumption, and ultimately, demand within the economy.

Sincerely, Joel

Decade Year-0 Year-1 Year-2 Year-3 Year-4 Year-5 Year-6 Year-7 Year-8 Year-9

1850’s 16.00

1860’s 9.59 0.49 1.05 3.15 8.06 6.59 3.74 2.41 3.62 5.64

1870’s 3.86 4.34 3.64 1.83 1.17 1.35 2.52 2.38 1.17 0.86

1880’s 0.94 0.92 0.78 1.10 0.85 0.88 0.71 0.67 0.65 0.77

1890’s 0.77 0.56 0.51 0.60 0.72 1.09 0.96 0.68 0.80 1.13

1900’s 1.19 0.96 0.80 0.94 0.86 0.62 0.73 0.72 0.72 0.70

1910’s 0.61 0.61 0.74 0.95 0.81 0.64 1.10 1.56 1.98 2.01

1920’s 3.07 1.73 1.61 1.34 1.43 1.68 1.88 1.30 1.17 1.27

1930’s 1.19 0.65 0.87 0.67 1.00 0.97 1.09 1.18 1.13 1.02

1940’s 1.02 1.14 1.19 1.20 1.21 1.22 1.41 1.93 2.60 2.54

1950’s 2.51 2.53 2.53 2.68 2.78 2.77 2.79 3.09 3.01 2.90

1960’s 2.88 2.89 2.90 2.89 2.88 2.86 2.88 2.92 2.94 3.09

1970’s 3.18 3.39 3.39 3.89 6.87 7.67 8.19 8.57 9.00 12.64

1980’s 21.59 31.77 28.52 26.19 25.88 24.09 12.51 15.40 12.58 15.86

1990’s 20.03 16.54 15.99 14.25 13.19 14.62 18.46 17.23 10.87 15.56

2000’s 26.72 21.84 22.51 27.56 36.77 50.28 59.69 66.52 94.04 56.35

2010’s 74.71 95.73 94.52 95.99

http://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=F000000__3&f=A

Inflation caused by universally used commodity increasing in price in the 1970s from $3.18/brl to $12.64/brl

Supply of money increasing relative to wages has nothing to do with this.

In the book “BEHEMOTH” BY NEUMANN, the German economy has inflation because it was looted of nearly all industrial production which was shipped out in exchange for no hard money or foreign currencies and the lack of arable land to feed itself. The lack of arable land to produce food and the lack of any usable currency to pay for imported food left Germany in the absurd situation of creating more money to command a market economy looted by war reparations of any means to feed itself. Printing more money did make crops grow or attract the attention of foreign growers for German currency which was useless. Food sold to Germans paid in their currency could be used to buy nothing of value, because it was all claimed as war debt service. Here inflation reveals the utter uselessness of money in any amount when the market mechanism is destroyed for trade. They produced more money in the vain hopes that some economic output would rise when it simply could not.

These are two examples of political decision making dominating economic theory and practice and reducing it mere words on paper which can ripped up and thrown in the trash. You know, like treaties and contracts.

First, wish your data was in a readable table to make comprehending possible.

Second……

“” Inflation caused by universally used commodity increasing in price in the 1970s from $3.18/brl to $12.64/brl

Supply of money increasing relative to wages has nothing to do with this.””

When prices are set in a monopoly (cartel-dominated) market, then that part of the equation does become meaningless.

That the market took those wages and gave them to the monopoly producer resulted in less ‘income’ to buy other stuff. So, other stuff was reduced in the economy’s throughput, but the sum of the economy’s throughput was the amount of money in circulation……regardless. Only money’s distribution was affected, and the prices of other goods that had oil-energy-inputs.

Today, it is the financializers that monopolize the use of money…….. which is what makes Phil’s CPI data set irrelevant.