Yves here. With an active US effort to isolate Russia, which Russia is seeking to undermine (with only limited success so far) in strengthening ties with China and other emerging economies, most analysts have seen the geopolitical struggle in terms of short-term effects, such as on Russia’s and Europe’s growth rates over the next year. At the same time, the Chinese initiative to create a development bank, meant to rival the World Bank, is seen by many as an important step in breaking the dollar hegemony, along with moves by China and Japan to enter into oil contracts denominated in currencies other than the greenback.

As we’ve discussed in previous posts, we believe the frisson over the demise of the dollar as the world’s reserve currency is greatly overdone. As much as the US is abusing its role, particularly in its aggressive use of its influence over the dollar payments system as a weapon, there are simply no viable candidates for replacement on the horizon.

However, this post examines a consequence of US economic aggression against Russia that has not rceived the attention that it merits: that of reducing the amount of international trade, something economists see as a driver of growth. Note that per the Lipsey Lancaster theorem, there is ample reason to doubt the near-religious belief that more open trade is always a good thing. However, sudden restrictions in trade, which is what is taking place with US/European sanctions on Russia and Russia implementing counter-sanctions, is certain to cause short-term dislocations. And as we noted in a recent post, the cordon sanitaire being placed around Russia will led it to operate more as an autarky, which may not necessarily be a negative in the medium to long term.

This post seeks to identify the impact of reduced trade between Russia and Europe. This sort of analysis could become more germane going forward. While a currency rival to the dollar any time soon looks to be far-fetched, ever-more obvious US economic imperialism may lead other countries to strengthen trade ties among themselves to the detriment of the US, or like Russia, to move to greater self-sufficiency as a defensive measure. While economists assume that our current open trade system could never be rolled back, that was the tacit assumption during the last great era of open trade, the period right before World War I. The Great War put that all in rapid reverse gear. While no one expects a violent rupture, we may be in the early stages of seeing fractures developing in the trade system.

By Peter A.G. van Bergeijk, Professor of International Economics and Macroeconomics, Institute of Social Studies, Erasmus University. Originally published at VoxEU

A quarter of a century ago, the Iron Curtain and Berlin Wall were demolished. This was one of the most visible consequences of the fall of communism. In the decades before 1989 political conflict had shaped the world trade pattern. Against the background of political tensions in the Ukraine, this column investigates the vulnerability of the world trade system.

Sanctions and counter sanctions currently taint trade developments between Russia and the EU and US (van Bergeijk 2014). This evokes memories of the Cold War that had a very substantial impact on East West trade in the 1950s and up to the 1990s. The East’s Council for Mutual Economical Assistance (COMECON) was created in response to US and UK economic sanctions against the Soviet Union and comprised the Soviet Union and the then satellite states Bulgaria, Czechoslovakia, Hungary, Poland and Romania. During the Cold War, trade at the European continent was substantially distorted both by the COMECON’s reliance on self-sufficiency, by the difficulties imposed by the East’s lack of hard and convertible currency and by the West imposing embargoes especially on dual use goods, technologically advanced goods and food. The impact of political frictions on openness (defined as world exports to Gross Planet Product (GPP) was substantial and for the year 1985 has been estimated 3.5% of GPP (van Bergeijk en Oldersma 1990; see also Wolf and Nitsch 2009 on trade between former East and West Germany). We know from observation that Détente led to an enormous surge in intra-European, and indeed global, trade (Afmann and Maurel 2010). Will increasing tensions with Russia now lead to contraction?

Potential Impact

Of course the findings for the 1990s cannot be used directly to infer what the impact of a new superpower conflict would mean. After the fall of the Iron Curtain and Berlin Wall, Germany united, formerly planned Central European countries became EU member states and many countries, in particular China, became important players in the world trade system offering alternative supply and export markets. Still the potential impact of the Crimean crisis and the chilling of relation between Russia and the West are substantial. A recent study by the CPB Netherlands Bureau for Economic Analysis (Veenendaal 2014), for example, reports short-term decreases of industrial production due to increased political uncertainty of about half a percentage point for the major EU countries and North America. New walls in Europe – even invisible walls – are still much more difficult to conceive than before 1961 when the Berlin Wall was erected, but at the same time one is aware that it is in the present geopolitical context that a political conflict could recreate significant look-alikes in the form of a Cold War trade scenario. This column illustrates the economic costs that would follow in such a scenario.

Political Trade Resistance

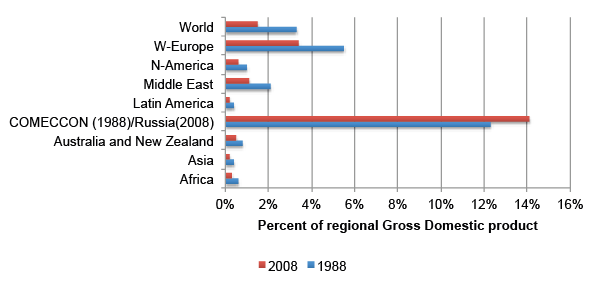

In order to estimate the potential impact of the return of a cold trade war, I perform a thought experiment, so to say re-introducing the visible and invisible walls between East and West in a gravity simulation model for the world trade system in 2008 (van Bergeijk 2012). The first step is to estimate the gravity model, in particular the political trade resistance, for the year 1988 when the political tensions between East and West were still very strong. Based on the gravity parameter estimates, for political trade resistance in 1988, I simulate a world trade patter with and without political trade resistance using 2008 population and GDP data and taking account of the breaking up of a number of former Communist countries, shifts in capital cities in Nigeria and Germany and the German unification. According to this simulation, a hypothetical re-erection of the Iron Curtain (on the borders of the Russian Federation) would reduce trade openness by about 1.5% of GPP (Figure 1).

Figure 1. Estimated Iron Curtain impact on trade openness (percent of GDP) in 1988 and 2008

Obviously, political trade resistance factors are not mirrors as illustrated by the different consequences for Western Europe and COMECON (1988)/Russian Federation (2008). The costs and benefits of political trade resistance are distributed quite unevenly between East and West. Second, the two simulations clarify that the impact of walls depends on local conditions on both sides of the wall, but also on the opportunities that exist for economic interaction with and between entities in wall-free locations. Third, although the impact of walls is obviously the strongest the closest one is to the wall, their impact beyond the local level will often be not negligible as shown by the impact of the Berlin Wall and Iron curtain in Australia and New Zealand.

Broader Implications

These results should not be seen as accurate predictions (Breuss and Egger 1999), but rather as a serious attempt to uncover the size of the potential impact of a wall that played a major role in recent history. The potential costs of politically inspired trade distortions cannot be neglected although its impact in the current context is much lower. It could therefore be argued that the political defence and safety aspects would appear to be relatively more important. From this perspective it is important to note that the history of European integration is testimony to the idea that increasing mutual economic benefits has an important instrument to appease the former belligerents Germany and France and in more recent times the integration process is credited for supporting and establishing democracy and reducing political tensions with the East European countries, if not the prevention of the Afghanistanisation of Central Europe. Reducing these mutual benefits may lead to decreasing international safety.

See original post for references

Anything that ends the so called free trade and damages the Federal Reserve is great.

For in truth free trade with the rest of the world has only created deficits of trade in the USA since 1980, which makes a country poorer, and depletes its natural resources. The only groups that has benefited is the onepercenters and wall street.

Huh? Our trade deficit entails other countries shipping us their goods (and natural resources) in exchange for green slips of paper. If anyone’s natural resources are being depleted by free-trade, I would say it’s probably the Chinese and other net exporters.

In keeping with the basic presumption that the West is and continues to be the centre of the Universe, this piece presumes it (the west) is and will continue to be the primary locus of global economic activity/growth/wealth. Take this presumption away, and the picture begins to look very different.

As for Russia’s move to “autarky” … really? This seems to be something like a given, repeated over and over; but for instance, oddly enough, its trade surplus increased despite the sanctions: http://www.bloomberg.com/news/2014-10-07/russian-trade-surplus-increases-as-putin-food-ban-curbs-imports.html

And for an “alternative” general picture, see for example here: http://russia-insider.com/en/china_germany_politics_opinion/2014/11/05/04-47-05pm/time_new_world_order_no_its_already_here

The increase in exports is likely the result of the fall of the ruble with Russia exporting energy in the similar volumes as before. Even the headline tells you the trade balance improved as a result of restricting IMPORTS. Exports barely improved in dollar terms and were below meager global growth levels. Plus the data is for Jan-August, so only a small portion of the time period includes when the sanctions were put into effect, and many analysts said their impact was slower to kick in than they’d anticipated. And the sanctions were in multiple phases. The initial ones were almost meaningless. It was the last round, the Tier Three sanctions, that had some bite, and they were imposed only as of August 1. http://europeansanctions.com/2014/08/01/details-of-tier-3-eu-russia-sanctions-published/

If Russia becomes less dependent on imports to supply itself, whatever it gets from exporting energy is gravy.

The “autarky” is more important in terms of internal security.

Also worth noting is that Japan has been given permission (… maybe actually it doesn’t bother to ask the U.S. for approval any more and just went ahead and did it) to use whatever methods it sees fit to trash its currency to have another go at mercantilism.

Now, I’m sceptical about how successful this will be. It’s pretty tricky to devalue your own currency when everyone is either playing the same game or else doing nothing proactive in supporting a currency and subjecting it to benign neglect. But if it is successful, then that would be a spur to calls to “do something” about any low-Yen policy, mainly in the U.S. But if the U.S. did take action (that action probably being limited to making noises rather than anything useful) then it would be a bit two-faced for the U.S. to not also have to look at China, who is the poster child for currency manipulators. Even though the U.S. refuses for political reasons to label them as such.

Trying, and failing, to make sense of both this and the issues brought out in the above feature, I’m left to wonder, who thought it would be a good idea to let the children play with the matches ?

Regarding the role of the dollar as the world reserve currency, I have two thougths. First, economic aggression occurs independently on the status of reserve currency. As I see it the dollar is not the weapon. The weapons are the goods or services that are no longer traded. Second, the days of the dollar as reserve currency migth be numbered but the reason is not that some countries are seeking alternatives. It migth well be that the US decides that letting the dollar be the international reserve currency is too much of a burden given how many countries have learned how to game the system. A new Bretton Woods-like agreement to change the international monetary system migth be closer than anyone thinks.

When it comes to the effects of the dollar as reserve, I think it’s inaccurate to speak of “the US” as if it were some unified thing, like, say, the State, which in practical terms is beholden to specific interests (i.e. Wall Street, business conglomerates, etc.), the whole neoliberal coalition, if you will. As we saw with the whole Argentina debt mediation debacle, the dollar as the primary medium of international monetary exchange means transfers are by and large cleared through US banks, meaning Wall Street banks, which makes it so that one particular court in New York is responsible for making decisions that affect monetary policy throughout the world, and that court is clearly beholden to banksters. In that light, the dollar as reserve appears to be an extremely potent weapon.

Now, if by “US” you mean the people of this country who might have benefited from the 24 trillion we put into banks the past few years in the form of, say, debt relief or infrastructure projects, then I would have to disagree that its will has any impact whatsoever on the policy decisions being made, so I don’t see much reason for supposing that there will be a major shift away from the status quo, seeing as those for whom the dollar reserve is a useful weapon have the power and influence, whereas those for whom the dollar reserve is a burden do not.

Maybe we will drive Russia back into communism. That would be rich irony.

If we are heading for change it does not appear that it will be an orderly change. Therefore can the US dollar as reserve currency not simply collapse, without any replacement? I see the break with Russia(and ultimately China) as the first major step towards the demise of the global economy. Doesn’t less international trade mean less need for the US dollar? Yes the dollar will still rule the roost in the Anglo-American sphere. After all US allies are all being run by quisling governments subservient to the 1% global elite. However the rest of the world – especially Asia – has the population and the natural resources.

Of course the British Empire ruled the world with only one major asset: the Royal Navy. Can the Amerikaner Reich turn the same trick? I doubt it. The sun did set on the British Empire and it’s beginning to set on Anglo-American world dominance.

The Gross Planet Product. The GPP is another new term to me. The total of all the GDPs? I like the analysis of the entire planet and think it could be beneficial for the environment, especially in view of recent statements coming from both the IMF and our FED (Fischer’s Stability Committee) that no economy (aka GDP) should be stimulated “beyond its capacity”. Not sure how this relates to arbitrary political trade sanctions based on fictitious accusations. It seems a reverse rule should also be in order that no economy should be capriciously sanctioned and driven to the opposite distress. And this thought in turn makes me think about our new secret trade agreements, the TTIP and the TPP, which have the ability to override domestic laws and sanctions. How exactly will such trade agreements which favor return on investment above all else ever be controlled and prevented from “overstimulating beyond their capacity” various industries within countries which must then compensate with some perpetual austerity. And etc.