Yves here. We’ve written that the sudden decline in the price of oil has the potential to deliver some nasty financial shocks, given that shale companies and even the majors have been financing exploration and development with debt.

But while concerns about fragility are well warranted, we wanted to make sure a mention made in this article is not treated with undue alarm. It points out that the BIS is concerned that an unprecedented portion of CDOs are now made of leveraged loans.

The problem is that the term “CDO” has been used inconsistently in the financial media. The CDO that you learned to hate in the wake of the crisis and blew up AIG, monoline insurers, and did a lot of damage to big banks were more formally called “asset backed securities CDOs” or “ABS CDOs” But that was too much of a mouthful, so they were referred to as “CDOs” in the press. There were two periods when that type of CDO existed, the late 1990s, and from the mid 2000 to mid-2007. Ina both cases, that market was a Ponzi, used to make the unwanted parts of subprime securitizatons saleable by making them into financial sausage, with some better assets thrown in, and then re-tranched again. The Ponzi part came about from the fact that these CDOs also had unsaleable parts, which were either put into first generation CDO sausage (CDOs allowed a certain portion of CDOs to be included) or sold into CDO squareds (which were hard to sell).

But the more mainstream type of CDO was one made of credit defaults swaps on corporate credits. That was the original CDO done in the famed JP Morgan Bisto deal in the mid-1990s. Indeed, when I first started researching subprime (ABS) CDOs, and just called them “CDOs” some experts assumed I meant the corporate loan type, since that was prevalent. During the crisis, possibly to make sure no one confused these CDOs with the ones that were blowing up, they were increasingly called CLOs, or “collatearlized loan obligations.” They were also legitimately less risky than the subprime CDOs, since their value didn’t suddenly collapse when a certain level of loan losses was breached.

The cause for pause is that CLOs, which are indeed a type of CDOs have traditionally been made mainly or entirely of investment grade credits. It now appears that junk credits predominate. While their structures and diversification will keep ABS CDO-type total wipeouts from happening, they could still deliver some nasty surprises.

By Raúl Ilargi Meijer, editor-in-chief of The Automatic Earth. Originally published at http://www.theautomaticearth.com/the-broken-model-of-the-eurozone/” rel=”nofollow”>Automatic Earth

The wider impact of plummeting oil prices is just now starting to be considered. Just about all ‘experts’ are way behind the curve. There’s still people insisting it’s all be a big boon to all of our economies. Not here, as you know if you follow TheAutomaticEarth.com, or as you can find out by retracing us over the past 1-2 months. I said from the get go that this cannot end well. Oil is too large a part of the economy to let a 40% price drop be reason to party.

And now both the Federal Reserve and the Bank for International Settlements have clued in, with urgency, to leveraged loans, their role in CDOs, AND their link to the energy industry. And whatever we may think of either institution, when both hoot the red alarm horn at the same time, we should pay attention.

Two articles from very different sources paint the – essentially same – picture. One is from Wolf Richter, easily one of my favorite writers at the moment in this narrow financial niche of ours, and his article today does a lot to confirm that. The other is from my ‘friend’ against all odds (we never met nor communicated), Ambrose Evans-Pritchard, who proves once more what makes him, despite all else, an interesting journalist to read.

What connects the two articles is leveraged loans, which in turn are strongly linked to collateralized debt obligations (CDOs). Ambrose quotes the BIS as saying 55% of CDOs are issued based on leveraged loans, an “unprecedented level”. Which is another way of saying we’re not in Kansas anymore. While Wolf confirms that leveraged loans play a major role in the oil (re:shale) industry.

Obviously, so do junk bonds, but those don’t bother the Fed and BIS as much; they get sold to investors, mutual funds, pension funds and the like. Leveraged loans on the other hand directly impact major banks. And that gives grandma Yellen the ‘Janet Jitters’ (let’s remember that term). For good reason: the Fed can’t buy oil, but its owner banks are hugely exposed to it.

This is what makes the falling oil prices so dangerous. As I must have said a million times in just the past few weeks, it’s not about the energy, it’s about the money. And this time around, I don’t have to do much writing, I laid plenty groundwork recently, and now the story tells itself. Apologies for the long quotes, I deleted what I thought was suitable. So first, here’s Wolf:

Oil, Gas Bloodbath Spreads to Junk Bonds, Leveraged Loans. Defaults Next

The price of oil has plunged nearly 40% since June to $65.63, and junk bonds in the US energy sector are getting hammered, after a phenomenal boom that peaked this year. Energy companies sold $50 billion in junk bonds through October, 14% of all junk bonds issued! But junk-rated energy companies trying to raise new money to service old debt or to fund costly fracking or off-shore drilling operations are suddenly hitting resistance.

And the erstwhile booming leveraged loans, the ugly sisters of junk bonds, are causing the Fed to have conniptions. Even Fed Chair Yellen singled them out because they involve banks and represent risks to the financial system. Regulators are investigating them and are trying to curtail them through “macroprudential” means, such as cracking down on banks, rather than through monetary means, such as raising rates. And what the Fed has been worrying about is already happening in the energy sector: leveraged loans are getting mauled. And it’s just the beginning.

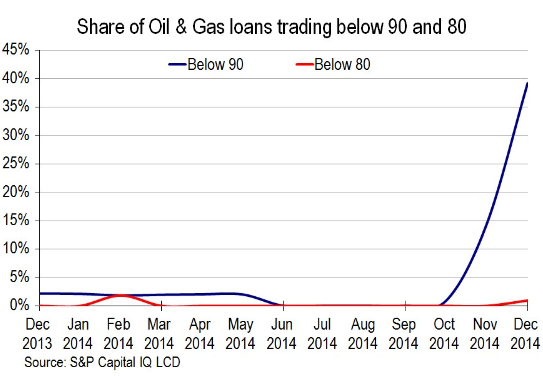

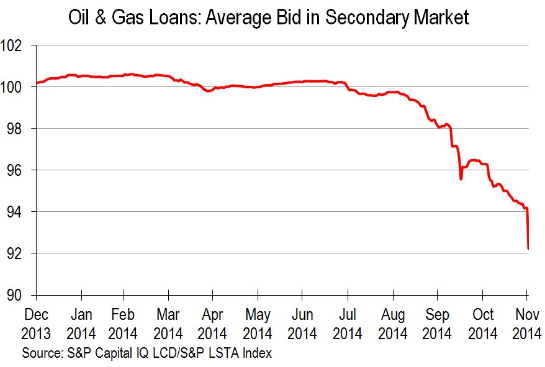

This monthly chart by S&P Capital IQ’s LeveragedLoan.com shows the leveraged loan index for the oil and gas sector. Earlier this year, when optimism about the US shale revolution was still defying gravity, these loans were trading at over 100 cents on the dollar. In July, when oil began to swoon, these loans fell below 100 cents on the dollar. The trend accelerated during the fall. And in November, these loans dropped to around 92 cents on the dollar.

How bad is it? The number of leveraged loans in the oil and gas sector trading between 80 and 90 cents on the dollar (blue line in the chart below) has soared parabolically from 0% in September to 40% now. These loans are now between 10% and 20% in the hole! And some leveraged loans are now trading below 80 cents on the dollar:

“If oil can stabilize, the scope for contagion is limited,” Edward Marrinan, macro credit strategist at RBS Securities, told Bloomberg. “But if we see a further fall in prices, there will have to be a reaction in the broader market as problems will spill out and more segments of the high-yield space will feel the pain.”

Oil and gas stocks are bleeding: the Energy Select Sector ETF is down 21% from June; S&P International Energy Sector ETF down 29% and the Oil & Gas Equipment & Services ETF down 42% from early July. Smaller drillers are in trouble. All of them had horrific single-day plunges, some over 30%, on “Black Friday” after OPEC’s Thanksgiving decision [..] Traders who tried to catch these stocks have gotten their fingers sliced off since then:

Goodrich Petroleum -88% since June. Energy XXI -86% since June. Sanchez Energy -78% since June. Oasis Petroleum -75% since July. Etc.

These are the very companies that benefited during the crazy good times from yield-desperate investors who’d been driven to obvious insanity by the Fed’s interest rate repression. These investors – such as your bond mutual fund or your pension fund – loaded up on energy junk bonds and leveraged loans. And now the Fed-inspired financial house, where all risks have been eliminated by QE Infinity and ZIRP, is rediscovering risk. Turns out, the Fed, so ingeniously prolific in buying financial assets to inflate their prices, can’t buy oil.

Unless a miracle happens that will goose the price of oil pronto, there will be defaults, and they will reverberate beyond the oil patch. [..] even the 43 largest, most diversified players in the energy sector that are part of the S&P 500 are grappling with the new reality: analysts chopped earnings estimates by 20.5% since September 30, according to FactSet.

As of Friday, analysts expected the energy sector to report a 13.7% drop in revenues. At the beginning of the quarter, they’d expected a decline of only 1.7%, though oil prices had been plunging for three months. And they now expect a 14.6% swoon in earnings, as opposed to the 6.6% gain they still saw at the beginning of the quarter.

All of the energy companies in the S&P 500 got their EPS estimates decimated, even the biggest ones: Exxon Mobil by 20%, Chevron by 25%, Hess by 47%, Murphy Oil by 50%, and Marathon Oil by 63%.

And then Ambrose comes in from a completely different angle, to tell basically the exact same story. The overlords of finance are nervous and worried, and limited in the scope of their possible remedies. But I bet you, the Fed will still raise rates. With ‘official’ US jobless rates at 5.8%, they must, or they lose all credibility. And besides, don’t forget that Wall Street banks need higher rates now more than ever, never mind the real economy, exactly because of leveraged loans. Hey, amigo, everybody’s in oil!

Dollar Surge Endangers Global Debt Edifice, Warns BIS

Off-shore lending in US dollars has soared to $9 trillion and poses a growing risk to both emerging markets and the world’s financial stability, the Bank for International Settlements has warned. The Swiss-based global watchdog said dollar loans to Chinese banks and companies are rising at an annual rate of 47%. They have jumped to $1.1 trillion from almost nothing five years ago. Cross-border dollar credit has ballooned to $456bn in Brazil, and $381bn in Mexico. External debt has reached $715bn in Russia, mostly in dollars.

A chunk of China’s borrowing is disguised as intra-firm financing. This replicates practices by German industrial companies in the 1920s [..]“To the extent that these flows are driven by financial operations rather than real activities, they could give rise to financial stability concerns,” said the BIS in its quarterly report. “More than a quantum of fragility underlies the current elevated mood in financial markets,” it warned.

[..] Some of the violent moves lately go beyond stress seen in earlier crises, a sign that markets may be dangerously stretched and that many fund managers do not really believe their own Goldilocks narrative. “Mid-October’s extreme intraday price movements underscore how sensitive markets have become to even small surprises. On 15 October, the yield on 10-year US Treasury bonds fell almost 37 basis points, more than the drop on 15 September 2008 when Lehman Brothers filed for bankruptcy.”

The BIS said 55% of collateralised debt obligations (CDOs) now being issued are based on leveraged loans, an “unprecedented level”. This raises eyebrows because CDOs were pivotal in the 2008 crash. “Activity in the leveraged loan markets even surpassed the levels recorded before the crisis: average quarterly announcements during the year to end-September 2014 were $250bn,” it said.

BIS officials are worried that tightening by the US Federal Reserve will transmit a credit shock through East Asia and the emerging world, both by raising the cost of borrowing and by pushing up the dollar.

The role of the US dollar is crucial in all this. If and when you see that “cross-border lending in dollars has tripled to $9 trillion in a decade“, you must recognize that you might as well forget about the demise of the greenback for the time being.

The dollar index (DXY) has surged 12% since late June to 89.36, smashing through its 30-year downtrend line. [..] Hyun Song Shin, the BIS’s head of research, said the world’s central banks still hold over 60% of their reserves in dollars. This ratio has changed remarkably little in 40 years, but the overall level has soared – from $1 trillion to $12 trillion just since 2000.

Cross-border lending in dollars has tripled to $9 trillion in a decade. Some $7 trillion of this is entirely outside the American regulatory sphere. “Neither a borrower nor a lender is a US resident. The role that the US dollar plays in debt contracts is very important. It is a global currency, and no other currency has this role,” he said.

The implication is that there is no lender-of-last resort standing behind trillions of off-shore dollar bank transactions. This increases the risks of a chain-reaction if it ever goes wrong. China’s central bank has ample dollar reserves to bail out its companies – should it wish to do so – but the jury is out on Brazil, Russia, and other countries. This flaw in the global system may be tested as the Fed prepares to raise interest rates for the first time in seven years. [..] The Fed’s new “optimal control” model suggests that rates may rise sooner and faster than markets expect. This has the makings of a global shock.

The great unknown is whether the current cycle of Fed tightening will lead to the same sort of stress seen in the Latin American debt crisis in the early 1980s or the East Asia/Russia crisis in the late 1990s. This time governments have far less dollar debt, but corporate dollar debt has replaced it, with mounting excesses in the non-bank bond markets. Emerging market bond issuance in dollars has jumped by $550bn since 2009. [..].. the weak links may not be where we think they are [..] the new threat may lie in non-leveraged investments by asset managers and pension funds funnelling vast sums of excess capital around the world, especially into emerging markets.

They engage in clustering and crowd behaviours, and are apt to pull-out en masse, risking a bad feedback-loop. This could prove to be today’s systemic danger. [..] [The BIS] now warns that the world is in many ways even more stretched today than it was in 2008 [..]

This is the story of today. Oil is everywhere. In all aspects of our lives. If oil prices suddenly move up a lot, people driving cars get hit, bad for the economy. If they move down much, the industry gets hit, jobs are lost, also bad for the economy. And everyone’s invested in that industry, whether they know it or not. We simply can’t afford $40 oil anymore than we can $200 oil; that is, in the short term. Our pensions funds, mutual funds and especially our banks are too heavily invested in it. Let alone our governments.

Falling oil prices are not just set to create future mayhem, they’re doing it now, you ain’t seen nothing yet. Much of the industry itself is scrambling to stay alive, many parties won’t make it if prices stay low or go lower, and the financial world, including your pension funds and mutual funds, will go south with it.

My wife and I are looking at my half of the family retirement savings (in CREF funds, largely tied to stocks) and wondering about cashing it in, taking the hit (as I am currently unemployed and so our income is unusually low) and knocking the hell out of our mortgage with the money. With the DOW hovering around 18,000 I can’t see it staying there for long, and I think the next big collapse is going to be permanent (or at least last a generation or until population falls and a new stage for what one can hope is smarter growth takes place). We feel that one asset (our home and the land around it) is just vastly more valuable than any retirement earnings tied to the financial sector. “Losing” money via penalties and taxes is rough, but it will save us a bundle over time in interest payments on the mortgage and allow us to pay off the mortgage well in advance of retirement. It’s a scary plan, but this article and so many others convinces me that a crash is inevitable and my instinct is that the “good times” will not be returning in the foreseeable future. Perhaps they can successfully artificially pump up the price of stocks one more time, but I don’t want to bet my future on it.

James, we did something like that this past summer…. moved out of the big house, into something much smaller and are now mortgage free. You may also want to consider keeping some of that money in good old fashioned currency. If things blow apart big time, having some cash in hand may not be a bad idea.

Underlying the financial decision is a pretty straightforward amortization. While accepting large uncertainty variables (ultimate stock market value versus ultimate house value, plus expected tax rate in retirement). There is of course the psychological aspect of opting out and of being debt & payment free now.

Don’t forget the risk of putting all your eggs in one basket (your house) it’s value may drop or it may be illiquid, and you may have time sensitive cash needs. Having no savings and an albatross house could be tough for a retiree.

The amortization is basically comparing the time value of mortgage interest saved over the remainder of the loan, versus tax impact of cashing out today. Don’t forget state taxes too.

Does your fund have money market/short bond funds. These should theoretically be safer from a major value swoon. Maybe a 10% or 20% hit, versus 50% or 60%.

But yeah, if you are going to get out, try and get out on top.

That said, everyone who got out in 2009/2010 at the bottom discovered that it is foolish to bet against Wall Street.

This is overwrought. While there is a relatively high chance of major correction, pension funds are not going to implode, nor is the domestic energy sector going to be allowed to go bankrupt. Despite the headline numbers exposure is not sufficiently large to kill off institutional investors, and even if it were Congress would move with all speed for a fiscal bailout.

Well that’s just dandy – another huge round of bailouts like 2008 only this time it’s junk bond investors. Remind me to order extra hemlock with that gin and tonic.

“While they were preparing the hemlock Socrates was learning how to play a new tune on his flute”. Make mine a double.

But I don’t get why any of this is surprising, when you have a massive thumb holding down the scales on the price of money of course it gives wildly false readings like this. It’s just the sheer size of the capital mis-allocations this time around that boggles the mind. Read: everything, from the cost of that puppy in the window to the $100’s of billions in environmental destruction in Nicaragua so some Chinese investor can have his own Panama Canal. 200 million for a house in Mayfair, sure, that’s normal, if you were paying in confetti…

TCTF: Too Crony to Fail. or Too Connected to Fail if you prefer.

That about sums it up.

Only mystery is the details of how they do it. End-consumer gas buyer bail-ins perhaps.

No, it isn’t. The fundamental reason the global economy is tanking is the abject failure of the US to respond appropriately to the GFC. Every aspect of US policy since, from Fed carpet bombing with cheap money to failure to re-regulate markets to the naked pursuit of inherently destabilizing policies re a dozen countries around the globe have in toto smashed business confidence to invest in real productive activity rather than the perceived ‘no-risk; follow the Fed’ road to a bust. Is the US still stronger? Of course. But is it good for the US to pursue policies that beggar Japan, Europe, China, Brazil, Turkey, Canada, Australia and many more? No. The US can no longer throw its weight around without smashing something in its own living room when it lands. Doofus moves by Congress to ‘bail out’ the situation only makes it worse. The last G20 was a total flop. The next one had better not be, and it had better be because the US is finally willing to listen to what other nations have been saying for at least the last 5 years re its monetary policy, immense regulatory failures, and escalating hostility towards all the important countries of the world.

This is the story of today. Oil is everywhere. In all aspects of our lives. If oil prices suddenly move up a lot, people driving cars get hit, bad for the economy. If they move down much, the industry gets hit, jobs are lost, also bad for the economy. And everyone’s invested in that industry, whether they know it or not. We simply can’t afford $40 oil anymore than we can $200 oil; that is, in the short term. Our pensions funds, mutual funds and especially our banks are too heavily invested in it. Let alone our governments.

Throw in the climate change aspects and it’s fair to say we’ve truly made a deal with the devil. Can’t live with the stuff, can’t live without it either. Interesting times ahead for sure. 2008’s about to be fondly remembered as “the good old days.”

What’s this “we” Kemosabe? So if I have this right, the Fed allows the banks to speculate in commodities which helps artificially drive up the oil price through speculation and now that their casino bets have gone bad that’s suddenly our problem as well. How long before recognition that the world is facing a political, not economic crisis? Crooks and gangsters are running everything.

Agree with this. Propping up pension funds and mutual funds sounds like the same scare tactics used for the original bail-outs. Shouldn’t the real question be whether these funds are invested in cotton candy? I think we need a twelve step program. http://neweconomicperspectives.org/2014/12/twelve-step-program-restore-prosperity-bernie-sanders-plan.html

As recently as ten years ago (mid-2004), $40 a barrel was the record high for crude oil. Adjust for inflation since then, and $50 represents the former record high (through mid 2004). Here’s the chart:

http://www.mrci.com/pdf/cl.pdf

Of course we can live with $40 or $50 oil. We did for all of human history, until the past decade. If some thought $100 oil was permanent, well, they seem to have miscalculated.

This is a story of long-only commodities funds becoming popular as an alternative asset class, the usual institutional victims blindly piling in, and then getting the rug rudely jerked out from under them. My tears fall like rain … think of the children!

“We” may be able to live with $40 a barrel oil, but frackers and tar sands producers can’t. And the whole thing is being manufactured by the Saudis, if you haven’t noticed, for political ends. It is unsustainable. Global oil production (conventional light sweet crude) hasn’t risen in several years, and there is good reason to believe it can’t. What oil at $80 a barrel did was instantly make unconventional oil a going proposition. What oil at $40 a barrel does is make that proposition moot.

Agree with you about the Saudis having a hand in it. As for whether $40 or $100 crude oil is more sustainable, if you draw an average through the real price of crude for the past 150 years (expressed in 2011 dollars), it comes out around $40:

http://transportblog.co.nz/wp-content/uploads/2013/07/Oil-Prices-1861-2012.png

Generically, commodity prices spike, then crash, then tread water for years. Usually the ‘treading water’ price represents the sustainable equilibrium, while the spike high proves to be a transient event.

*cranks up the V8 to hear the dual exhausts rumble*

Technically, CLOs are linked to the acutal loans, not CDS (which does make a difference). You could call CDOs “synthetic” CLOs.. But the terminology is hopelessly confused here.. (not to mention that all of the stuff is really ABS…).

Anyways, on more important note. The performance of the securitization is almost entirely linked to the correlation of the underlying. What kills any ABS is a high correlation. ABS works if, and only if, the correlation between the assets (be it loans, mortgages, CDSes, credit cards, student loans or what have you) securitised is relatively low. Which is why (linked to the inability to observe the correlation until after the fact), incidentally, new B3 regime doesn’t allow any capital relief on tranched/multiple underlying credit instruments (although there’s some ambiguity whetehr tranched single-entity is ok or not…)

If you have a high correlation – say a CLO/CDO of junk energy assets – the result is dreck, and if you’re a buyer, you’re a stuffee by definition.

This was known before the crisis (although buyers ignored it, because they trusted their trusted advisors – and the ignorant raters), and is known even more now. Unfortunately, it also means there’s less chance of pleading ignorance if you buy a leveraged CDO of junk energy.

Yes, sorry I was too behind schedule to go into the cash v. synthetics issue, which was remiss on my part…and the CLOs that everyone was worried about during the crisis were actually the leveraged loan CLOs, thanks to the takeover music stopping very abruptly and banks having a lot of inventory left.

The subprime ABS CDOs weren’t just killed by high correlation. They were deadly by being resecuritizations. They wound up being highly concentrated BBB/BBB- subprime bond risk, when those bonds had thin loss exposures. IIRC (I could look this up but I need to turn in) typical overcollateralization + excess spread was about 8%. The BBB tranche was only about 3% of loss exposure. So if you got to 11% losses, the tranche was a zero. So you had high correlation PLUS cliff risk.

The old (pre-crisis into crisis) CLOs were adequately diversified. This batch looks to be less well diversified. The leverage will mean they’ll probably decay more rapidly than a synthetic CDS on a higher-grade credit, but I’d doubt they fall over like the subprime CDOs. But you can still have serious losses short of a total train wreck.

entirely agree on diversification of the new lot of the CLO

I think the resecuritization would still work okish under low correlation environment – although it does increase the leverage massively (somethign again people are at a loss, since they feel they put in real money so how come they are leveraged?)

Say when you look at the UK RMBS market, if you had an AAA tranche of a second-order CDO made of M notes of Granite (Northern Rock vehicle, one of the two worst performers in the UK with Aire Valey) and B notes on just about everything else there was that wasn’t A tranche (not much), your actual lossses to date would be still nil. IIRC, even if you were Z notes holder in Granite, you’d not be wiped out just yet, as the total losses (so far) on Granite are running at about 4-5% of the total pool.

But then, the UK master trust structures were always much more robust than US (or any) standalones, and the lending practices less lose (even at Northern Rock). IIRC, the US credit card master trusts performed okish compared to the junk standalone RMBSes but I don’t know that market, so may be wrong.

The Fed can’t buy oil? But it can buy financial instruments dealing in all sorts of other commodities. Including the newly commoditized product (housing) we all love to hate. So this means the Fed is very short sighted. In fact, extremely stupid. It has spread trillions globally trying to save a banking system that it allows to deal in stuff it can’t be a buyer of last resort for. I think this is a terrible oversight. The obvious thing to do now is nationalize American oil and gas. Because Russia will clean our bankrupt clock if we don’t. And the Saudis don’t care, they are likewise secure. Or alternatively the Fed can just say “Well, it’s OK this time” and buy up all those CLOs and just let them run off the books, providing of course that the price of oil does not go so high that all other industries come to a screeching halt. And what’s the best choice here for a sane person? Either raise interest rates to save the banks (how’s zat work?) or keep them at zirp-nirp and save the US Treasury? Either way we are in a depression and have created so many financial contradictions that martial law is the only thing that will work. But don’t tell anyone. We can blame it on the market!

The Fed can’t buy anything under its “unusual and exigent” powers. It can LEND against anything, even a dead dog.

So, the banks helicopter money into the global cities, creating RE inflation and migration, income inequality (V1-RB) from the get-go to seed the ponzi. If you chase the money, natural resources can only follow (I1-IB). To ensure the outcome, G closes the community circuit behind you (R1-VB). Accounting is all about natural resource exploitation, and Civil Law rewards compliance, throwing symptomatic individual scapegoats into prison, imprisoning all in a closed system.

Labor doesn’t enroll its children in public education to learn, but to see why the majority repeats its past every time. At some distance from the city, you will find a town that fairly represents event horizon resonance in the city. That is where you practice the discounting function, deflation, so it’s automatic when you enter the city, so you can focus on whatever it is you want to do. You will always find that a perceived lack of resources is the problemsolution. Don’t waste your time in bipolar economic activity agendaism.

Preparing your children to be productive, which can only be done in private, is far more effective than State welfare, which is inflation articulation between public, private and non-profit corporations, the counterweight incorporation. Labor creates the rhyme from the repeat. Whether it is chaos or order depends upon perspective.

In any case, you can’t eat paper or gold, so you might want to learn to generate nutrition. Any specialty will do to keep the empire occupied, but there is always a shortage of farmers, nurses and electricians, and a surplus of bankers, because the empire pays you to be stupid, in an increasingly complex (arbitrary) social artifice (edifice).

You want your quantum backlash time element to resonate, with the circuit you want to enter, which will provide the propulsion you need, and if you want to return, you might want to build it first, and then set your distance to spacetime. It’s the artificial intersections that slow you down. The brake is circuit supply. You don’t want a shield; you want a collector.

All the ruckus, and what has changed, in the empire, except nothing, natural resource exploitation, always on the wrong side of the bubble?

About 3 months back a commentator who went only by initials (in capitals – there are several, but I can’t remember who it was) suggested, during a discussion about the US dollar, the BRICS, Japan and related goings-on, that the US response to emerging upstarts was going to be to smack them all very hard with a high dollar. Well, that person was bang on, and I think we have to view this as a tightly coordinated, massive move by the US State and Wall Street and the Saudis to reverse global capital flows and effectively squeeze the rest of the globe like a great big lemon, the pits being Iran, Russia, Brazil and Venezuela. And from the perspective of the Fed and White House, an out-of-control shale boom has its nails clipped, not its wings, on the way to a global feast for disaster capital.

This entire episode demonstrates, though, that the previous run-ups from oil for $10 a barrel in the late ’90’s to nearly $150 by 2008, and from the 2009 lows through to the 2014 high, positively required that production from some countries’ production be suppressed. What would the price of oil be if all nations with oil had equal and fair and unimpeded (by war, sanctions, ideological hostility) access to capital, technology and markets? Why should Americans (and Canadians) subsidize directly and indirectly (‘free’ money) their essentially joint oil industries at prices far, far above what a peaceful marketplace would deliver? I think the clear answer is ‘They wouldn’t.’, that is, if they knew what was really going on.

I don’t expect this will go more than several months before the US has to act to raise prices. We’ll see if Obama has the heads he needs plated by then.

Fiver gets to the heart of the matter as always. But what if what if Obama does NOT have “the heads he needs?” If the hairs on the back of your neck are not already standing up, then see this comment from 2 months ago.

=

=

=

HOP