By Pablo Druck and Nicolas Magud, Senior Economists at the International Monetary Fund, and Rodrigo Mariscal, Research analyst in the Western Hemisphere Department, IMF. Originally published at VoxEU

The strength of the US dollar can impact the economic activity in emerging economies in various ways. This column argues that appreciation of the dollar mitigates the impact of real GDP growth in emerging markets. The main transmission channel is through an income effect. As the dollar appreciates, commodity prices fall, depressing domestic demand via lower real income, and as a result real GDP in emerging markets decelerates. Emerging markets’ growth is expected to remain subdued, reflecting the expected persistence of the strong dollar.

US Dollar and Emerging Markets

What is the effect of a stronger or weaker US dollar on emerging markets’ economic activity? Frenkel (1986) documents that US monetary easing – usually related to a more depreciated dollar – results in higher commodity prices, and vice versa. Dornbusch (1986), Borensztein and Reinhart (1994), and Akram (2009) show that nominal and real commodity prices depend negatively on the US real exchange rate. In parallel, Engel and Hamilton (1990) have long ago documented the long swings in dollar values. However, we are not aware of any systematic evidence of the link between the strength of the US dollar and economic activity in emerging markets over the dollar cycle – less so of any study documenting the transmission channel. In a recent paper (Druck et al., 2015) we try to bridge this gap.

Using data for 1970–2014, we document that:

- During periods of US dollar appreciation, real GDP growth in emerging markets slows despite the positive impulse of US growth, and vice versa.

The main transmission channel is through an income effect owing to the impact of the dollar on global commodity prices. As the dollar appreciates, dollar commodity prices tend to fall. In turn, weaker commodity prices depress domestic demand via lower real (dollar) income. Thus, real GDP in emerging markets decelerates. Moreover, we show that these effects hold despite any potential expenditure-switching effect resulting from the relative currency depreciation of emerging market economies when the dollar appreciates. We also show that despite controlling for the effects of the US real exchange rate appreciation and real GDP growth, an increase in the US interest rate further reduces growth in emerging markets. All these effects are stronger in countries with more rigid exchange rate regimes. Finally, although net commodity exporters are affected the most, countries that rely on importing capital or inputs for domestic production will also be affected. Therefore, at the time of writing, emerging markets’ growth is likely to remain subdued reflecting, in part, the expected persistence of the strong dollar and the anticipated increase in the US interest rates.

Why the US real effective exchange rate has such an impact? For developing countries, this is essentially an exogenous variable. Most international transactions are priced in US dollars, including commodity prices. And emerging markets (excluding perhaps China) cannot affect much the weights in the multilateral exchange rate of the US. Thus, developments in the US affect emerging markets – and not vice versa. Further, the independence of US macroeconomic policy with respect to less developed countries suggests that the US real exchange rate is likely to be more relevant and even more exogenous than the terms of trade.

Historical Context: Some Stylised Facts

- Stronger US dollar, lower emerging markets’ growth.

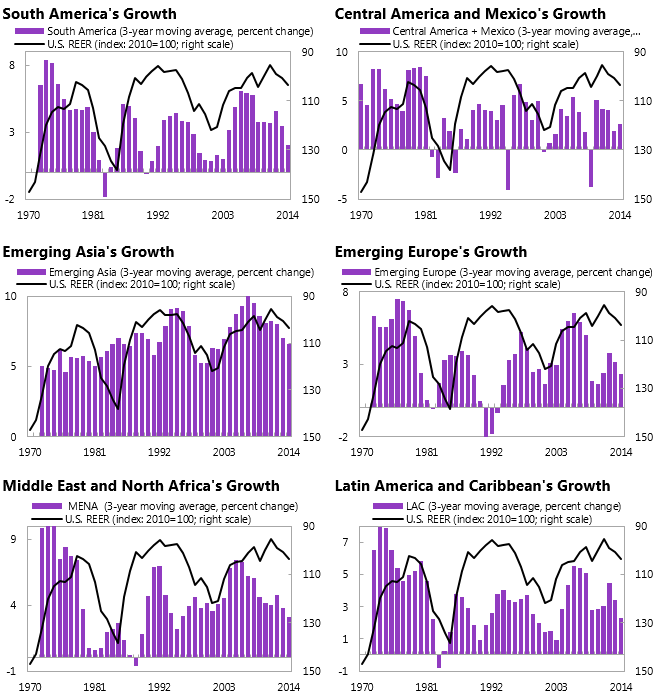

Periods of US dollar appreciation coincide with softer real GDP growth rates throughout emerging market regions (Figure 1) – and vice versa. This stylised fact is especially strong for regions that are strong net commodity exporters.

Figure 1. US dollar strength and real GDP growth in emerging markets

Sources: IMF, World Economic Outlook; and IMF, International Financial Statistics; and IMF staff calculations.

Note: REER = Real Effective Exchange Rate. Increase = depreciation.

- Stronger U.S. dollar, softer real domestic demand growth.

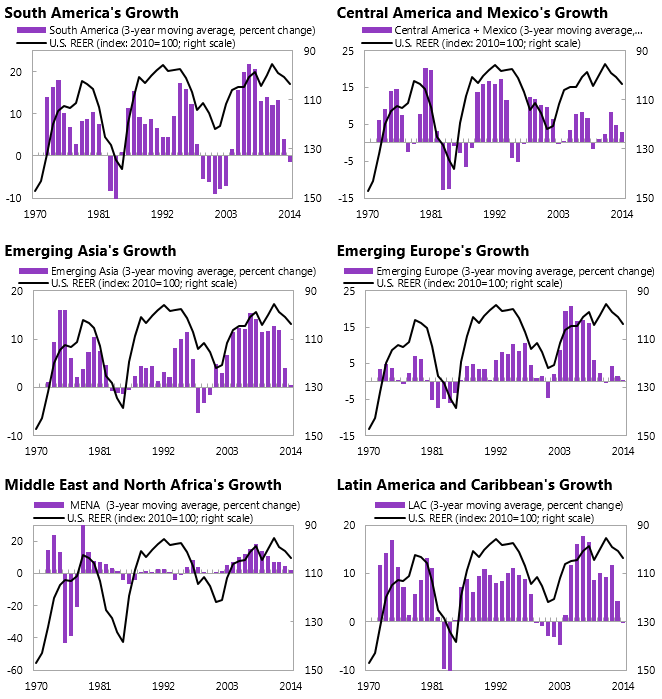

Figure 2 presents a similar picture as Figure 1, but using the growth rate of real domestic demand. It suggests that domestic demand is a strong driver of economic activity, beyond other factors that might influence domestic demand.

Figure 2. US dollar strength and real domestic demand growth in emerging markets

Sources: IMF, World Economic Outlook; and IMF, International Financial Statistics; and IMF staff calculations.

Note: REER = Real Effective Exchange Rate. Increase = depreciation.

- Higher US interest rates, a stronger US dollar.

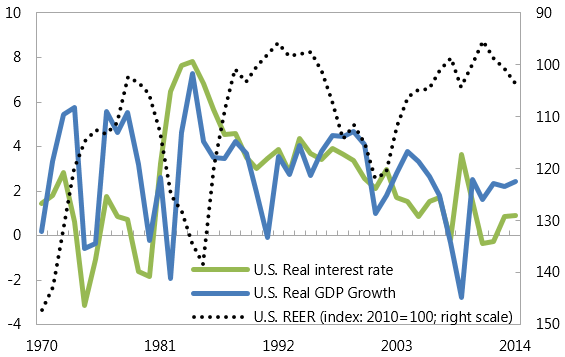

Higher interest rates in the US tend to occur alongside a stronger dollar, and vice versa (Figure 3). Higher interest rates in the US increase capital inflows to the US searching for higher yields, appreciating the currency. Often, higher interest rates are also associated with stronger growth, though not always.

Figure 3. US dollar strength, real GDP growth, and real interest rates

Sources: IMF, World Economic Outlook; and IMF, International Financial Statistics; and IMF staff calculations.

Note: REER = Real Effective Exchange Rate. Increase = depreciation.

- Though not systematically, higher US interest rates appear to be associated with stronger US growth; Interest rate-economic activity relationship: stronger growth eventually generates demand-induced inflationary pressures.

Lack of sufficient (or fast enough) supply response translates into higher prices. The latter triggers the Fed into tightening its monetary policy, increasing borrowing costs and thus mitigating inflationary pressures through slower economic activity growth.

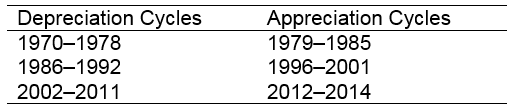

Dollar Appreciation/Depreciation Cycles

Estimating a simple Markov-switching model with appreciation/depreciation regimes for the period 1970–2014, we find that real depreciations have been, on average, stronger and lasted longer than real appreciations. The real annual average appreciation is 3.2% per year with an average duration of over 6 years; the real average annual depreciation is 3.8% with an average duration of close to 9 years.1 In addition, these regimes are very persistent. A period of real appreciation is 83% more likely to remain appreciating in the following period than to switch regimes. For real depreciation, the probability of continuation of the state of nature is about 88%.2 Thus, we identify the following cycles:

Table 1. Appreciation and depreciation cycles

Event analysis

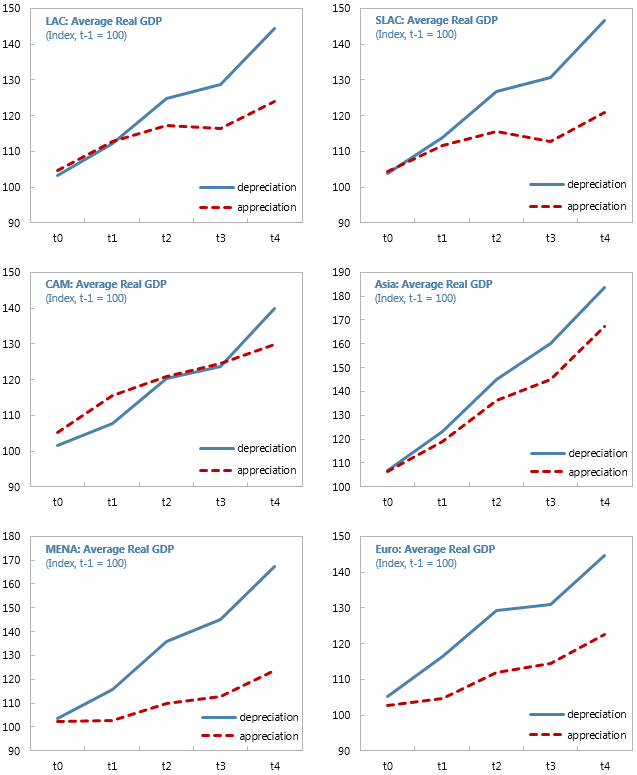

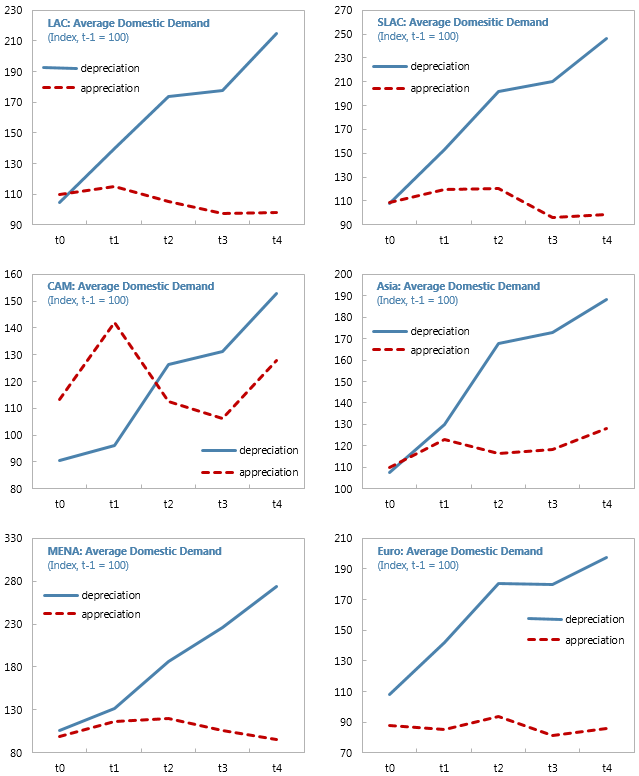

Next, we add dynamics to the average depreciation and appreciation cycles, based on event analysis using the dollar cycles identified above.3 Figure 4 shows the indices for the average real GDP during appreciation and depreciation episodes; Figure 5 shows real domestic demand.

Figure 4. Real GDP during US dollar appreciation and depreciation cycles

Source: authors’ calculation.

Except for Central America and Mexico, every other emerging region shows that real GDP is lower during periods of US dollar appreciation. We observe that this pattern holds for Latin America as an aggregate, and especially for South America. The latter is a strong commodity exporter – unlike Central America and Mexico. It also holds for emerging countries in the Middle East and North Africa Region (MENA), as well as for emerging Europe. To a lesser extent, it also true for emerging Asia. On average, Latin America’s slower growth results in real GDP being about 25 percentage points lower toward the end of the cycle during appreciation cycles than during depreciation cycles. South America’s differences are of similar order of magnitude. They are even higher in MENA countries – about 50 percentage points, while lower in emerging Asia, though still sizeable (at about 20 percentage points). There is not such a marked difference in Central America and Mexico, however. Among the possible causes of the latter, are the strong links via trade, tourism, and remittances. The trade link operates through the external demand for goods. Tourism boosts external demand for services. And remittances transfer resources from the US to Mexico, Central America, and the Caribbean. All these factors help increase domestic demand and income in the emerging and developing countries. Thus, they could offset any negative income effect owing to the stronger dollar. Countries with hard pegs or outright dollarization tend to be further synchronised with the US’ business cycle.

Figure 5. Real domestic demand during US dollar appreciation and depreciation cycles

Source: authors’ calculation.

- Regarding domestic demand, except for Central America and Mexico, all other regions and sub-regions experience much stronger real domestic demand growth when the US dollar is more depreciated.

In fact, in many of the regions domestic demand actually decreases or remains flat during appreciation phases. We take this as a powerful indication of the negative impact of a stronger dollar on the purchasing power of domestic demand. In turn, this could suggest that it might be the case that the income effect actually dominates the (expenditure-switching) substitution effect in some cases.

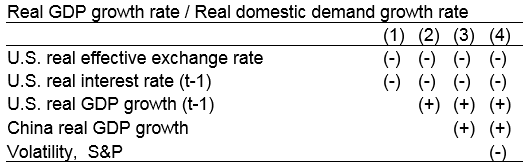

Some Simple Econometrics

After sketching a simple model to rationalise our findings, we run two sets of simple regressions to test the above stylised facts. The left-hand side variable is either the growth rate of emerging markets’ real GDP or real domestic demand, respectively. Despite controlling for US and China’s real GDP growth rates (external demand), US real interest rates (financial channel), net capital inflows (availability of external financing), volatility (uncertainty), commodity terms of trade, and several other controls, there is a strong statistically significant effect of the US real effective exchange rate on emerging markets’ growth. This effect is negative, particularly so for domestic demand. It holds across different emerging regions, with varying degrees. It is especially strong for net commodity exporters. But it is also relevant for countries that rely on importing capital or inputs to produce. For economies with more exchange rate flexibility, the effect is weaker on output, but stronger on domestic demand, as expected. Thus, a stronger US dollar lowers real GDP and domestic demand growth.

Table 2. Real GDP growth rate and demand growth rate

Going Forward

The US dollar is on an appreciating cycle since mid-2014. Based on our historical estimations, the probability of the dollar remaining appreciated in the short- and medium-term is high (above 80%), in line with appreciating cycles in the US dollar of about 68 years. In the circumstances, commodity prices would remain weak. Together, these effects point to slower domestic demand and real GDP growth in emerging markets than otherwise – across all regions.

Moreover, in the context of a lift-off in US interest rates as the Federal Reserve is expected to start unwinding the extraordinary expansionary monetary policy implemented in recent years, if anything, the US dollar is more likely to remain strong. Capital inflows to emerging markets are likely to moderate at best (even if no capital flow reversal takes place), on the back of weaker commodity prices. Unfortunately, thus, the external front for these economies is not promising.

Strong US growth is good for emerging markets, as external demand for the latter increases. Beyond that effect, however, a stronger US dollar mitigates the expansionary effect of faster growth in the US, via an income effect. The latter, in turn, is particularly strong for commodity exporters and countries with more rigid exchange rate regimes. To a lesser extent, countries that rely on importing capital and intermediate inputs in production could also experience this offsetting income effect via domestic demand. And higher US real interest rate further adds to the mitigation/amplification effect or the tighter/easier financial conditions that usually come along with a more appreciated dollar.

Disclaimer: The views expressed are those of the authors and do not necessarily represent the views of the IMF, its Executive Board of management.

Footnotes

1 Excluding the current (ongoing) appreciation cycle we find that appreciation cycles are still shorter than depreciation cycles, but less so. The average length is about 8 years. The average annual appreciation rate is 3.4%, and the average annual depreciation rate is 3.7%.

2 The results from excluding the current appreciation cycle imply a slightly higher persistence of depreciation cycles (92%), and similar expected persistence for appreciation cycles (82%).

3 Given that each event is not necessarily of the same period length, we discretize the length of each event. To this end, let us call period t0 the first observation in any appreciation or depreciation cycle and (the real GDP) observation in the last year of the appreciation or depreciation cycle as t4. Let us standardise real GDP in period t-1 equal to 100. Given the data for real GDP growth rates for each (PPP-weighted) real GDP, we reconstruct the indexed real GDP for each region. We discretize the time-space to compute the real GDP index at the half-life of each event, as well as at quarter-life and three-quarter-life. Last, we compute basic statistics across each set of appreciation and depreciation episodes at t0, ¼, ½, and ¾ and t, respectively (which we label as t0, t1, t2, t3, and t4, respectively).

See original post for references