Yves here. Steve Keen, one of the few economists to predict the global economic crisis, has identified China as a prime candidate for Japan-style zombification, based on its rapid growth in debt from an already not-shabbly level. China has engaged in stop-and-go economic policies, tightening credit, then loosening it again when growth weakens too much. Recent reports have also had senior party members call for an end to credit growth. Note that Keen points out that a mere end to credit growth will trigger a recession or worse in countries with rapid debt growth and high overall debt levels.

And signs of strain are growing. The Financial Times reported that companies are stretching their payables. China optimists are arguing that housing inventories are clearing, which portends further growth. MacroBusiness debunked that notion yesterday:

Inventory clearance “on track”. Sure, if a barely perceptible slowing in the uptrend and more recent reversal upwards is “on track”. And this is only tiers 1&2. In the tier 3&4 cities there is no change.

Chinese realty will slow as the year runs on and floor space under construction will slow with it. I still expect new starts growth to fall away all year and gross floor space under construction to end flat.

The short answer to the question is China clearing it’s housing glut is “no”, that will only happen when prices fall enough to make property affordable.

Today, MacroBusiness gave a broader look at signs of stress in China’s shadow banking system.

By David Llewellyn-Smith, founding publisher and former editor-in-chief of The Diplomat magazine, now the Asia Pacific’s leading geo-politics website. Originally posted at MacroBusiness

Chinese loan sharks are demanding nude photos as collateral from female borrowers which can be used for blackmail if they fall behind on their repayments.

The aggressive tactics are an example of the drastic debt recovery measures that are being employed in the slowing Chinese economy.

The democratisation of finance in China via peer-to-peer lenders and the vast shadow banking system, with interest rates sometimes topping 30 per cent, have proved an inflammatory mix and fuelled a surge in souring loans.

Female college students in the southern province of Guangdong were told to hand over naked photos of themselves holding their ID cards, with lenders threatening to make them public if they failed to repay their microloans, according to the Nandu Daily, the local newspaper.

…Blackmailing with nude photos joins a long list of threats including property destruction and bodily injury committed by loan sharks attempting to collect unpaid loans.

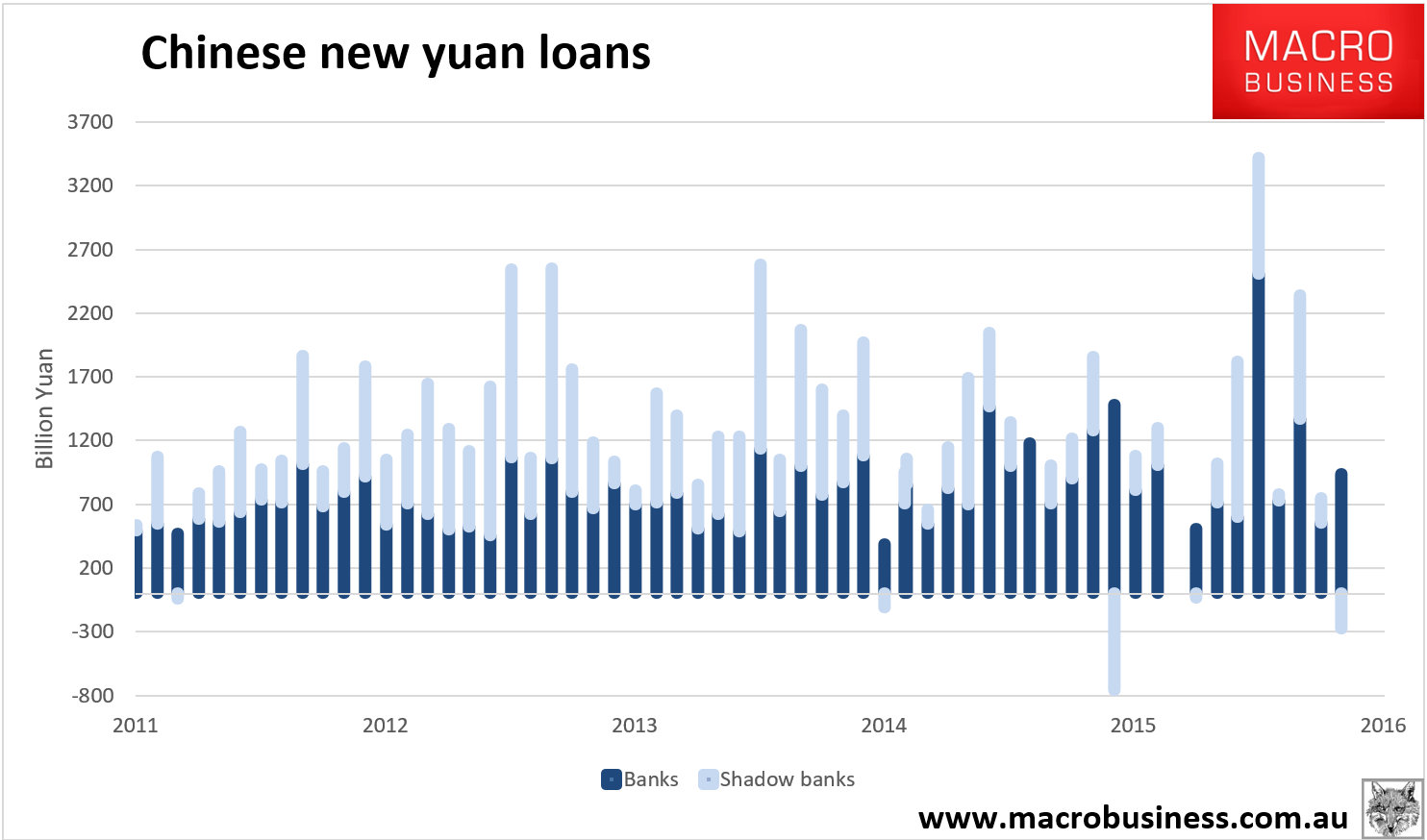

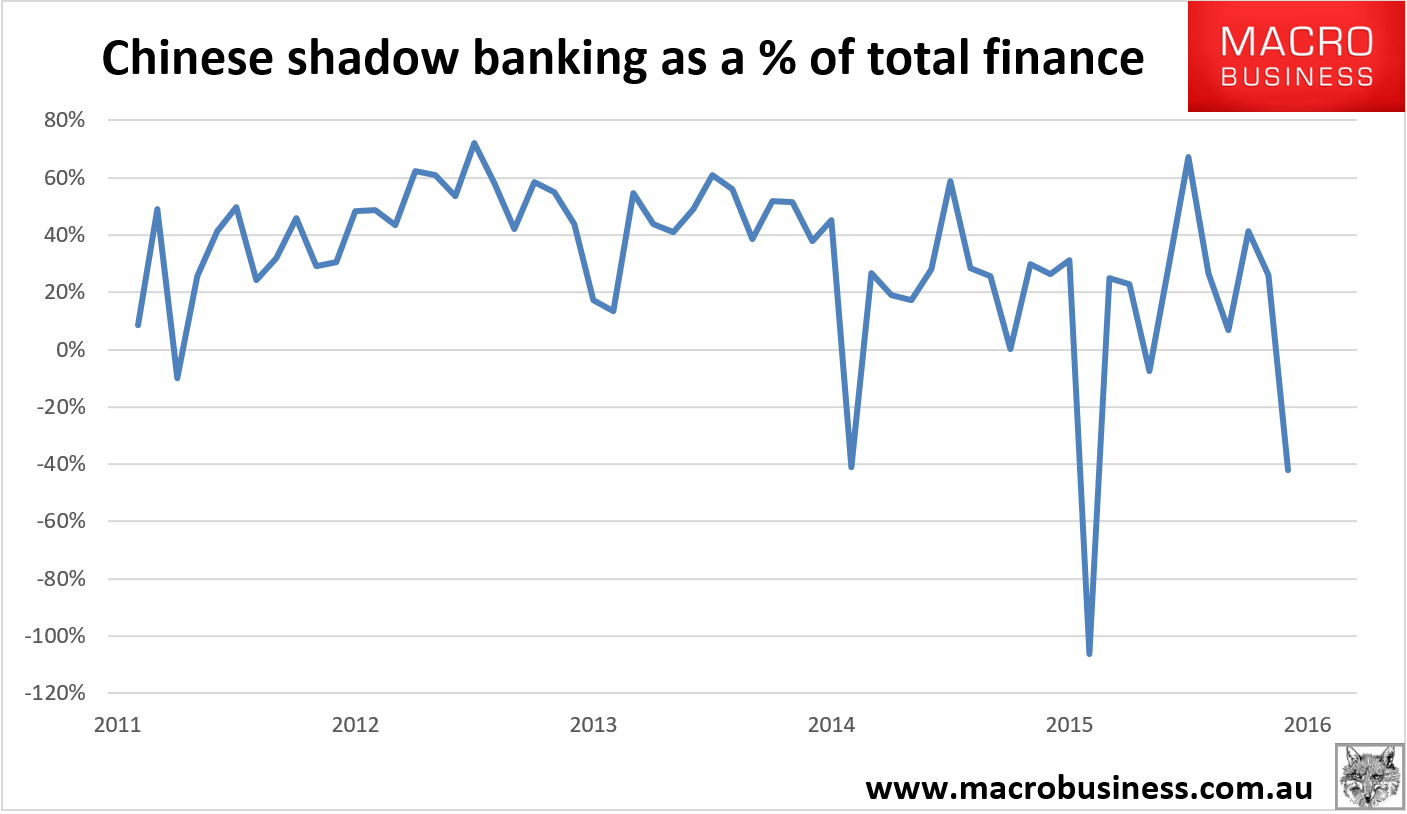

Hmm, well, although not directly related it is risk, nicely embodied in this story, that is driving the Chinese crackdown on shadow lending. And for now, it is working after a recovery in the early months of the year:

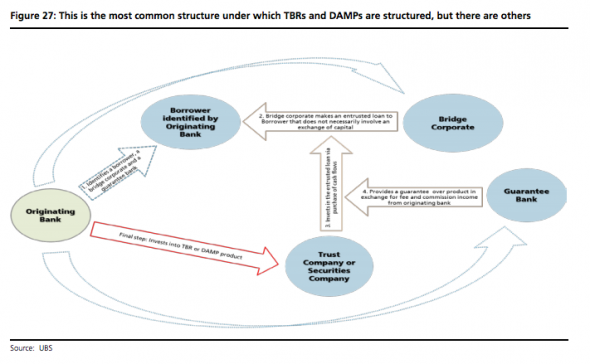

The crackdown is set to continue, from UBS:

In aggregate, these assets are roughly equivalent in size to 16% of total banking sector loans. However, they are deeply concentrated in subsets of the banking sector that account for around 43% of total banking sector assets: the joint stock banks (JSBs), city commercial banks (CCBs), rural commercial banks (RCBs) and other rural lenders (see Figure 1). Notably, foreign banks hold none of these assets, while the big five commercial banks and the policy banks hold immaterial amounts (see Figure 3).

…the fastest-growing assets in H115 for listed banks(excluding the big five commercial banks, which still continue to have immaterial holdings of these assets—see Figure 3), with shadow loan growth of Rmb1.4trn versus Rmb1.2trn loan book growth.

Q: Are the regulators closing the shadow loan loophole?

Yes. Document 82 effectively limits, and in the case of certain specified activities, completely closes a loophole that has allowed banks to build up trillions of Rmb of loans outside of their loan books as investments—all of which avoid the far stricter provisioning, asset quality disclosure and risk weightings that accompanies loans. In particular, we believe the wording of Document 82 signals a hardened resolve by the regulators to crack down on the use of these assets in understating NPL ratios. Given the size of TBR and DAMP investments (we estimate they stand at Rmb12.6tn as at end- 2015) and their concentration in weaker subsets of the banking sector, the regulation is likely to be accompanied by a grace period.

Q: Will banks need to raise capital?

Yes. Any changes whatsoever to the risk weighting and provisioning of TBRs and DAMPs will have a direct impact on capital levels. We estimate this regulation will result in capital needs of between Rmb1.1trn and Rmb1.46trn. Even in a banking sector the size of China’s, this would be material. To put those figures in context, the total equity generated by the commercial banking sector from 2014 to 2015 was Rmb1.8trn. The capital requirements could be even higher, potentially even in excess of Rmb2.8trn if banks are required to apply the same non-performing asset recognition standards to these assets as they do their loan books (something we think is highly unlikely). Given the scale of capital that could be needed (and the concentration of those capital needs in certain subsets of the banking sector), we expect the impact of the regulation to take place gradually over multiple quarters.

Q: What are the implications for the bank sector?

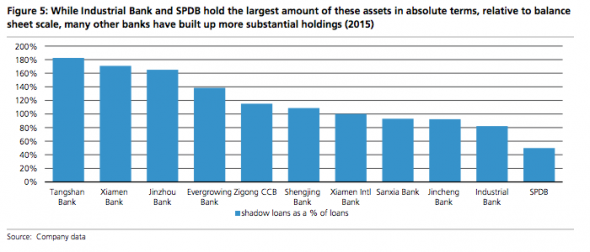

Nearly every listed (and unlisted) bank in China will be negatively impacted by this increased regulatory tightening, with the exception of the big five commercial banks, which have immaterial holdings of these assets. This supports our China Banks team’s Buy ratings on China Construction Bank (CCB) and Bank of China (BoC). However, joint stock banks (JSBs) across the board would be particularly impacted by any crackdown on their TBR and DAMP positions. China Zheshang Bank (24% of total assets), China Industrial Bank (28% of total assets) and Shanghai Pudong Development Bank (22% of total assets) should be the most impacted. The impact to city commercial and rural commercial banks would be more uneven, with Jinzhou Bank (46% of total assets), Shengjing Bank (30% of total assets) and Bank of Nanjing (30% of total assets) the most negatively affected. Only Bank of Beijing (6% of total assets) and Chongqing Rural Commercial Bank (CQRCB; 6% of total assets) are likely to avoid an overly material impact.

…we continue to believe that market concerns around bank WMPs may be excessive and we are still much more concerned about the on-balance sheet shadow loans than the off-balance sheet ones. This is not to suggest that we are not concerned by the rapid growth in WMPs in 2015 (see Figure 8 and Figure 9), and we estimate TBRs and DAMPs held in the off-balance positions could add an additional Rmb3.2trn to our Rmb12.6trn estimate of on-balance sheet exposures. Document 82 suggests that some of these assets may need to be brought back on-balance sheet, and provisioned and recognised accordingly. Subject to how big such off-balance sheet positions are, we estimate this could result in additional capital needs of up to Rmb438bn.

While Australia’s terms of trade resume their crash through the second half as China slows, we can comfort ourselves that the plight of these young women is being alleviated.

The loan sharking sounds like the sort of thing the Chinese had a revolution to stop.

ewmayer

We’ve all heard about “having skin in the game”, but this takes it to a ridiculous extreme. And for men who take out loans using this kind of collateral, just hope you’re not outed for “naked shorting”. There are stiff legal penalties for that, chaps!

bronco

Victims are tasked with providing the pictures for their own blackmail? This is another example of how those wily Chinese have lowered the barriers to entry in yet another field. The chief difficulty in being a blackmailer is all the legwork digging up dirt people would be willing to pay to keep hidden. They figured out a way to outsource all that to unpaid subcontractors.

craazyman

The Chinese are clever.

I bet they’ll find a way to make a market in fake nude photos.

The likeness will be just enough to get the money, but when it’s time to collect, friends and family will see it’s not really her after all — and there will be no shame. hahahahah.

They all look alike anyway. It should be pretty easy to scam this one. Especially for the Chinese.

craazyboy

It’s just a matter of time until they start cloning western nude model photos.

But I am disappointed to find out the Chinese are so prudish that bankers would even think this would work.

hunkerdown

I remember reading a one-act play in high school called “Do Not Spit at Random” by Fang Tzu, in which some Chinese man spits on the sidewalk instead of into a spittoon, and a girl Pioneer, after she (and an accumulating crowd) fail to cajole the man to clean up his mess by invoking public obligations, finally succeeds by threatening to circle it in chalk and write his name and employer by it.

Also, I remember reading in Graeber’s Debt that, absent official means of recourse against non-performing debtors, some lenders — ancient Greeks? — would require a borrower to take minor liberties to get the loan (such as grabbing the money out of the lender’s hand) in order that the lender had a crime to hold over the borrower.

Expect photo booths at your local cash advance parlor in 2017.

Synoia

Chinese loan sharks are demanding nude photos as collateral from female borrowers which can be used for blackmail if they fall behind on their repayments.

That’s very cheeky.

allan

And giving new meaning to being in arrears.

Anonymous

Perfect for this blog – lending with nude photos as a form of reverse-collateral is truly a form of “naked” capitalism!

TheCatSaid

What’s the incentive for the loan shark to ever get rid of the photos? Could they get rid of them, if they’ve been digitized? (Have they been added to NSA archives?) What about in-country hacking, say of loan sharks’ customer photo albums?

And what about the men? Not the same social stigma as women if theirs were posted online?

FWIW I don’t recall reading anything about cyber crime within China. Is it as common as elsewhere? Anyone else know anything?

The loan sharking sounds like the sort of thing the Chinese had a revolution to stop.

We’ve all heard about “having skin in the game”, but this takes it to a ridiculous extreme. And for men who take out loans using this kind of collateral, just hope you’re not outed for “naked shorting”. There are stiff legal penalties for that, chaps!

Victims are tasked with providing the pictures for their own blackmail? This is another example of how those wily Chinese have lowered the barriers to entry in yet another field. The chief difficulty in being a blackmailer is all the legwork digging up dirt people would be willing to pay to keep hidden. They figured out a way to outsource all that to unpaid subcontractors.

The Chinese are clever.

I bet they’ll find a way to make a market in fake nude photos.

The likeness will be just enough to get the money, but when it’s time to collect, friends and family will see it’s not really her after all — and there will be no shame. hahahahah.

They all look alike anyway. It should be pretty easy to scam this one. Especially for the Chinese.

It’s just a matter of time until they start cloning western nude model photos.

But I am disappointed to find out the Chinese are so prudish that bankers would even think this would work.

I remember reading a one-act play in high school called “Do Not Spit at Random” by Fang Tzu, in which some Chinese man spits on the sidewalk instead of into a spittoon, and a girl Pioneer, after she (and an accumulating crowd) fail to cajole the man to clean up his mess by invoking public obligations, finally succeeds by threatening to circle it in chalk and write his name and employer by it.

Also, I remember reading in Graeber’s Debt that, absent official means of recourse against non-performing debtors, some lenders — ancient Greeks? — would require a borrower to take minor liberties to get the loan (such as grabbing the money out of the lender’s hand) in order that the lender had a crime to hold over the borrower.

Expect photo booths at your local cash advance parlor in 2017.

That’s very cheeky.

And giving new meaning to being in arrears.

Perfect for this blog – lending with nude photos as a form of reverse-collateral is truly a form of “naked” capitalism!

What’s the incentive for the loan shark to ever get rid of the photos? Could they get rid of them, if they’ve been digitized? (Have they been added to NSA archives?) What about in-country hacking, say of loan sharks’ customer photo albums?

And what about the men? Not the same social stigma as women if theirs were posted online?

FWIW I don’t recall reading anything about cyber crime within China. Is it as common as elsewhere? Anyone else know anything?