Yves here. This is a terrific takedown of the loanable funds theory, on which a ton of bad policy rests.

By Servaas Storm, Senior Lecturer at Delft University of Technology, who works on macroeconomics, technological progress, income distribution & economic growth, finance, development and structural change, and climate change. Originally published at the Institute for New Economic Thinking website

Forget the myth of a savings glut causing near-zero interest rates. We have a shortage of aggregate demand, and only public spending and raising wages will change that.

Introduction

Nine years after the Great Financial Crisis, U.S. output growth has not returned to its pre-recession trend, even after interest rates hit the ‘zero lower bound’ (ZLB) and the unconventional monetary policy arsenal of the Federal Reserve has been all but exhausted. It is widely feared that this insipid recovery reflects a ‘new normal’, characterized by “secular stagnation” which set in already well before the global banking crisis of 2008 (Summers 2013, 2015).

This ‘new normal’ is characterized not just by this slowdown of aggregate economic growth, but also by greater income and wealth inequalities and a growing polarization of employment and earnings into high-skill, high-wage and low-skill, low-wage jobs—at the expense of middle-class jobs (Temin 2017; Storm 2017). The slow recovery, heightened job insecurity and economic anxiety have fueled a groundswell of popular discontent with the political establishment and made voters captive to Donald Trump’s siren song promising jobs and growth (Ferguson and Page 2017).

What are the causes of secular stagnation? What are the solutions to revive growth and get the U.S. economy out of the doldrums?

If we go by four of the papers commissioned by the Institute for New Economic Thinking (INET) at its recent symposium to explore these questions, one headline conclusion stands out: the secular stagnation is caused by a heavy overdose of savings (relative to investment), which is caused by higher retirement savings due to declining population growth and an ageing labour force (Eggertson, Mehotra & Robbins 2017; Lu & Teulings 2017; Eggertson, Lancastre and Summers 2017), higher income inequality (Rachel & Smith 2017), and an inflow of precautionary Asian savings (Rachel & Smith 2017). All these savings end up as deposits, or ‘loanable funds’ (LF), in commercial banks. In earlier times, so the argument goes, banks would successfully channel these ‘loanable funds’ into productive firm investment — by lowering the nominal interest rate and thus inducing additional demand for investment loans.

But this time is different: the glut in savings supply is so large that banks cannot get rid of all the loanable funds even when they offer firms free loans—that is, even after they reduce the interest rate to zero, firms are not willing to borrow more in order to invest. The result is inadequate investment and a shortage of aggregate demand in the short run, which lead to long-term stagnation as long as the savings-investment imbalance persists. Summers (2015) regards a “chronic excess of saving over investment” as “the essence of secular stagnation”. Monetary policymakers at the Federal Reserve are in a fix, because they cannot lower the interest rate further as it is stuck at the ZLB. Hence, forces of demography and ageing, higher inequality and thrifty Chinese savers are putting the U.S. economy on a slow-moving turtle — and not much can be done, it seems, to halt the resulting secular stagnation.

This is clearly a depressing conclusion, but it is also wrong.

To see this, we have to understand why there is a misplaced focus on the market for loanable funds that ignores the role of fiscal policy that is plainly in front of us. In other words, we need to step back from the trees of dated models and see the whole forest of our economy.

The Market for Loanable Funds

In the papers mentioned, commercial banks must first mobilise savings in order to have the loanable funds (LF) to originate new (investment) loans or credit. Banks are therefore intermediaries between “savers” (those who provide the LF-supply) and “investors” (firms which demand the LF). Banks, in this narrative, do not create money themselves and hence cannot pre-finance investment by new money. They only move it between savers and investors.

We apparently live in a non-monetary (corn) economy—one that just exchanges a real good that everybody uses, like corn. Savings (or LF-supply) are assumed to rise when the interest rate R goes up, whereas investment (or LF-demand) must decline when R increases. This is the stuff of textbooks, as is illustrated by Greg Mankiw’s (1997, p. 63) explanation:

In fact, saving and investment can be interpreted in terms of supply an demand. In this case, the ‘good’ is loanable funds, and its ‘price’ is the interest rate. Saving is the supply of loans—individuals lend their savings to investors, or they deposit their saving in a bank that makes the loan for them. Investment is the demand for loanable funds—investors borrow from the public directly by selling bonds or indirectly by borrowing from banks. [….] At the equilibrium interest rate, saving equals investment and the supply of loans equals the demand.

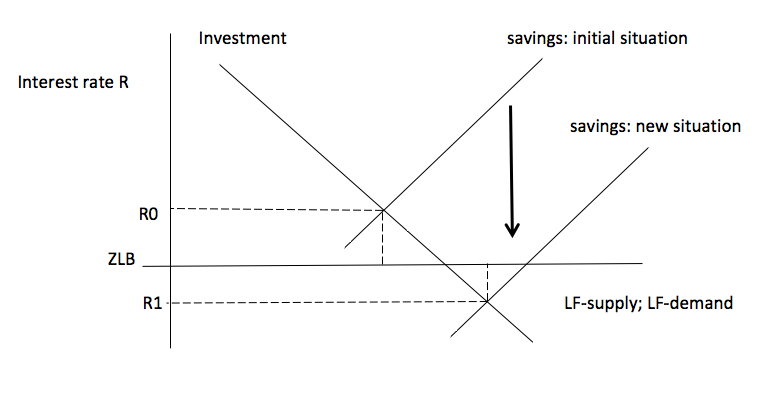

But the loanable funds market also forms the heart of complicated dynamic stochastic general equilibrium (DSGE) models, beloved by ‘freshwater’ and ‘saltwater’ economists alike (Woodford 2010), as should be clear from the commissioned INET papers as well. Figure 1 illustrates the loanable funds market in this scheme. The upward-sloping curve tells us that savings (or LF-supply) goes up as the interest rate R increases. The downward-sloping curve shows us that investment (or LF-demand) declines if the cost of capital (R) goes up. In the initial situation, the LF-market clears at a positive interest rate R0 > 0. Savings equal investment, which implies that LF-supply matches LF-demand, and in this—happy—equilibrium outcome, the economy can grow along some steady-state path.

To see how we can get secular stagnation in such a loanable-funds world, we introduce a shock, say, an ageing population (a demographic imbalance), a rise in (extreme) inequality, or an Asian savings glut, due to which the savings schedule shifts down. Equilibrium in the new situation should occur at R1 which is negative. But this can’t happen because of the ZLB: the nominal interest cannot decline below zero. Hence R is stuck at the ZLB and savings exceed investment, or LF-supply > LF-demand. This is a disequilibrium outcome which involves an over-supply of savings (relative to investment), in turn leading to depressed growth.

Ever since Knut Wicksell’s (1898) restatement of the doctrine, the loanable funds approach has exerted a surprisingly strong influence upon some of the best minds in the profession. Its appeal lies in the fact that it can be presented in digestible form in a simple diagram (as Figure 1), while its micro-economic logic matches the neoclassical belief in the ‘virtue of thrift’ and Max Weber’s Protestant Ethic, which emphasize austerity, savings (before spending!) and delayed gratification as the path to bliss.

The problem with this model is that it is wrong (see Lindner 2015; Taylor 2016). Wrong in its conceptualisation of banks (which are not just intermediaries pushing around existing money, but which can create new money ex nihilo), wrong in thinking that savings or LF-supply have anything to do with “loans” or “credit,” wrong because the empirical evidence in support of a “chronic excess of savings over investment” is weak or lacking, wrong in its utter neglect of finance, financialization and financial markets, wrong in its assumption that the interest rate is some “market-clearing” price (the interest rate, as all central bankers will acknowledge, is the principal instrument of monetary policy), and wrong in the assumption that the two schedules—the LF-supply curve and the LF-demand curve—are independent of one another (they are not, as Keynes already pointed out).

Figure 1: The Loanable Funds Market: A Savings Glut Causing Secular Stagnation

I wish to briefly elaborate these six points. I understand that each of these criticisms is known and I entertain little hope that that any of this will make people reconsider their approach, analysis, diagnosis and conclusions. Nevertheless, it is important that these criticisms are raised and not shoveled under the carpet. The problem of secular stagnation is simply too important to be left mis-diagnosed.

First Problem: Loanable Funds Supply and Demand Are Not Independent Functions

Let me start with the point that the LF-supply and LF-demand curve are not two independent schedules. Figure 1 presents savings and investment as functions of only the interest rate R, while keeping all other variables unchanged. The problem is that the ceteris paribus assumption does not hold in this case. The reason is that savings and investment are both affected by, and at the same time determined by, changes in income and (changes in) income distribution. To see how this works, let us assume that the average propensity to save rises in response to the demographic imbalance and ageing. As a result, consumption and aggregate demand go down. Rational firms, expecting future income to decline, will postpone or cancel planned investment projects and investment declines (due to the negative income effect and for a given interest rate R0). This means that LF-demand curve in Figure 1 must shift downward in response to the increased savings. The exact point was made by Keynes (1936, p. 179):

The classical theory of the rate of interest [the loanable funds theory] seems to suppose that, if the demand curve for capital shifts or if the curve relating the rate of interest to the amounts saved out of a given income shifts or if both these curves shift, the new rate of interest will be given by the point of intersection of the new positions of the two curves. But this is a nonsense theory. For the assumption that income is constant is inconsistent with the assumption that these two curves can shift independently of one another. If either of them shift, then, in general, income will change; with the result that the whole schematism based on the assumption of a given income breaks down … In truth, the classical theory has not been alive to the relevance of changes in the level of income or to the possibility of the level of income being actually a function of the rate of the investment.

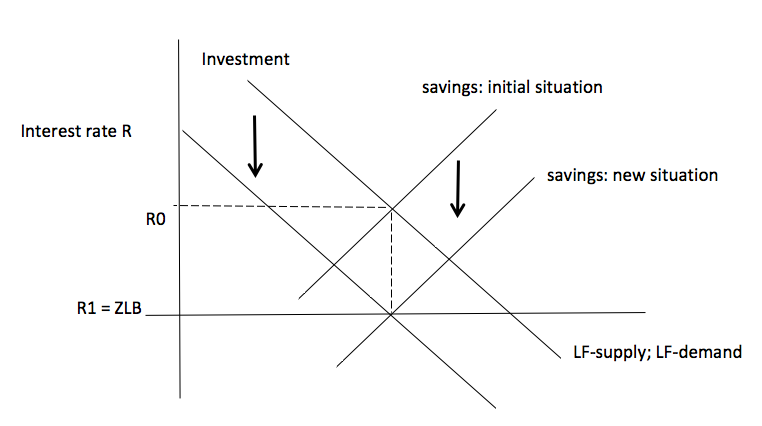

Let me try to illustrate this using Figure 2. Suppose there is an exogenous (unexplained) rise in the average propensity to save. In reponse, the LF-supply curve shifts down, but because (expected) income declines, the LF-demand schedule shifts downward as well. The outcome could well be that there is no change in equilibrium savings and equilibrium investment. The only change is that the ‘natural’ interest is now R1 and equal to the ZLB. Figure 2 is, in fact, consistent with the empirical analysis (and their Figure of global savings and investment) of Rachel & Smith. Let me be clear: Figure 2 is not intended to suggest that the loanable funds market is useful and theoretically correct. The point I am trying to make is that income changes and autonomous demand changes are much bigger drivers of both investment and saving decisions than the interest rate. Market clearing happens here—as Keynes was arguing—because the level of economic activity and income adjust, not because of interest-rate adjustment.

Figure 2: The Loanable Funds Market: Shifts in Both Schedules

Second Problem: Savings Do Not Fund Investment, Credit Does…

The loanable funds doctrine wrongly assumes that commercial bank lending is constrained by the prior availability of loanable funds or savings. The simple point in response is that, in real life, modern banks are not just intermediaries between ‘savers’ and ‘investors’, pushing around already-existing money, but are money creating institutions. Banks create new money ex nihilo, i.e. without prior mobilisation of savings. This is illustrated by Werner’s (2014) case study of the money creation process by one individual commercial bank. What this means is that banks do pre-finance investment, as was noted by Schumpeter early on and later by Keynes (1939), Kaldor (1989), Kalecki, and numerous other economists. It is for this reason that Joseph Schumpeter (1934, p. 74) called the money-creating banker ‘the ephor of the exchange economy’—someone who by creating credit (ex nihilo) is pre-financing new investments and innovation and enables “the carrying out of new combinations, authorizes people, in the name of society as it were, to form them.” Nicholas Kaldor (1989, p. 179) hit the nail on its head when he wrote that “[C]redit money has no ‘supply function’ in the production sense (since its costs of production are insignificant if not actually zero); it comes into existence as a result of bank lending and is extinguished through the repayment of bank loans. At any one time the volume of bank lending or its rate of expansion is limited only by the availability of credit-worthy borrowers.” Kaldor had earlier expressed his views on the endogeneity of money in his evidence to the Radcliffe Committee on the Workings of the Monetary System, whose report (1959) was strongly influenced by Kaldor’s argumentation. Or take Lord Adair Turner (2016, pp. 57) to whom the loanable-funds approach is 98% fictional, as he writes:

Read an undergraduate textbook of economics, or advanced academic papers on financial intermediation, and if they describe banks at all, it is usually as follows: “banks take deposits from households and lend money to businesses, allocating capital between alternative capital investment possibilities.” But as a description of what modern banks do, this account is largely fictional, and it fails to capture their essential role and implications. […] Banks create credit, money, and thus purchasing power. […] The vast majority of what we count as “money’ in modern economies is created in this fashion: in the United Kingdom 98% of money takes this form ….

We therefore don’t need savings to make possible investment—or, in contrast to the Protestant Ethic, banks allow us to have ‘gratification’ even if we have not been ‘thrifty’ and austere, as long as there are slack resources in the economy.

It is by no means a secret that commercial banks create new money. As the Bank of England (2007) writes, “When bank make loans they create additional deposits for those that have borrowed” (Berry et al. 2007, p. 377). Or consider the following statement from the Deutsche Bundesbank (2009): “The commercial banks can create money themselves ….” Across the board, central bank economists, including economists working at the Bank for International Settlements (Borio and Disyatat 2011), have rejected the loanable funds model as a wrong description of how the financial system actually works (see McLeay et al. 2014a, 2014b; Jakab and Kumhof 2015). And the Deutsche Bundesbank (2017) leaves no doubt as to how the banking system works and money is created in actually-existing capitalism, stating that the ability of banks to originate loans does not depend on the prior availability of saving deposits. Bank of England economists Zoltan Jakab and Michael Kumhoff (2015) reject the loanable-funds approach in favour of a model with money-creating banks. In their model (as in reality), banks pre-finance investment; investment creates incomes; people save out of their incomes; and at the end of the day, ex-post savings equal investment. This is what Jakab and Kumhoff (2015) conclude:

“…. if the loan is for physical investment purposes, this new lending and money is what triggers investment and therefore, by the national accounts identity of saving and investment (for closed economies), saving. Saving is therefore a consequence, not a cause, of such lending. Saving does not finance investment, financing does. To argue otherwise confuses the respective macroeconomic roles of resources (saving) and debt-based money (financing).”

Savings are a consequence of credit-financed investment (rather than a priorcondition) — and we cannot draw a savings-investment cross as in Figure 1, as ifthe two curves are independent. They are not. There exists therefore no ‘loanable funds market’ in which scarce savings constrain (through interest rate adjustments) the demand for investment loans. Highlighting the loanable funds fallacy, Keynes wrote in “The Process of Capital Formation” (1939):

“Increased investment will always be accompanied by increased saving, but it can never be preceded by it. Dishoarding and credit expansion provides not an alternative to increased saving, but a necessary preparation for it. It is the parent, not the twin, of increased saving.”

This makes it all the more remarkable that some of the authors of the commissioned conference papers continue to frame their analysis in terms of the discredited loanable funds market which wrongly assumes that savings have an existence of their own—separate from investment, the level of economic activity and the distribution of incomes.

Third Problem: The Interest Rate Is a Monetary Policy Instrument, Not a Market-Clearing Price

In loanable funds theory, the interest rate is a market price, determined by LF-supply and LF-demand (as in Figure 1). In reality, central bankers use the interest rate as their principal policy instrument (Storm and Naastepad 2012). It takes effort and a considerable amount of sophistry to match the loanable funds theory and the usage of the interest rate as a policy instrument. However, once one acknowledges the empirical fact that commercial banks create money ex nihilo, which means money supply is endogenous, the model of an interest-rate clearing loanable funds market becomes untenable. Or as Bank of England economists Jakab and Kumhof (2015) argue:

…modern central banks target interest rates, and are committed to supplying as many reserves (and cash) as banks demand at that rate, in order to safeguard financial stability. The quantity of reserves is therefore a consequence, not a cause, of lending and money creation. This view concerning central bank reserves […] has been repeatedly described in publications of the world’s leading central banks.

What this means is that the interest rate may well be at the ZLB, but this is not caused by a savings glut in the loanable funds market, but the result of a deliberate policy decision by the Federal Reserve—in an attempt to revive sluggish demand in a context of stagnation, subdued wage growth, weak or no inflation, substantial hidden un- and underemployment, and actual recorded unemployment being (much) higher than the NAIRU (see Storm and Naastepad 2012). Seen this way, the savings glut is the symptom (or consequence) of an aggregate demand shortage which has its roots in the permanent suppression of wage growth (relative to labour productivity growth), the falling share of wages in income, the rising inequalities of income and wealth (Taylor 2017) as well as the financialization of corporations (Lazonick 2017) and the economy as a whole (Storm 2018). It is not the cause of the secular stagnation—unlike in the loanable funds models.

Fourth Problem: The Manifest Absence of Finance and Financial Markets

What the various commissioned conference papers do not acknowledge is that the increase in savings (mostly due to heightened inequality and financialization) is not channeled into higher real-economy investment, but is actually channeled into more lucrative financial (derivative) markets. Big corporations like Alphabet, Facebook and Microsoft are holding enormous amounts of liquidity and IMF economists have documented the growth of global institutional cash pools, now worth $5 to 6 trillion and managed by asset or money managers in the shadow banking system (Pozsar 2011; Pozsar and Singh 2011; Pozsar 2015). Today’s global economy is suffering from an unprecedented “liquidity preference”—with the cash safely “parked” in short-term (over-collateralized lending deals in the repo-market. The liquidity is used to earn a quick buck in all kinds of OTC derivatives trading, including forex swaps, options and interest rate swaps. The global savings glut is the same thing as the global overabundance of liquidity (partying around in financial markets) and also the same thing as the global demand shortage—that is: the lack of investment in real economic activity, R&D and innovation.

The low interest rate is important in this context, because it has dramatically lowered the opportunity cost of holding cash—thus encouraging (financial) firms, the rentiers and the super-rich to hold on to their liquidity and make (quick and relatively safe and high) returns in financial markets and exotic financial instruments. Added to this, we have to acknowledge the fact that highly-leveraged firms are paying out most of their profits to shareholders as dividends or using it to buy back shares (Lazonick 2017). This has turned out to be damaging to real investment and innovation, and it has added further fuel to financialization (Epstein 2018; Storm 2018). If anything, firms have stopped using their savings (or retained profits) to finance their investments which are now financed by bank loans and higher leverage. If we acknowledge these roles of finance and financial markets, then we can begin to understand why investment is depressed and why there is an aggregate demand shortage. More than two decades of financial deregulation have created a rentiers’ delight, a capitalism without ‘compulsions’ on financial investors, banks, and the property-owning class which in practice has led to ‘capitalism for the 99%’ and ‘socialism for the 1%’ (Palma 2009; Epstein 2018) For authentic Keynesians, this financialized system is the exact opposite of Keynes’ advice to go for the euthanasia of the rentiers (i.e. design policies to reduce the excess liquidity).

Fifth Problem: Confusing Savings with “Loans,” or Stocks with Flows

“I have found out what economics is,’ Michał Kalecki once told Joan Robinson, “it is the science of confusing stocks with flows.” If anything, Kalecki’s comment applies to the loanable funds model. In the loanable fund universe, as Mankiw writes and as most commissioned conference papers argue, saving equals investment and the supply of loans equals the demand at some equilibrium interest rate. But savings and investment are flow variables, whereas the supply of loans and the demand for loans are stock variables. Simply equating these flows to the corresponding stocks is not considered good practice in stock-flow-consistent macro-economic modelling. It is incongruous, because even if we assume that the interest rate does clear “the stock of loan supply” and “the stock of loan demand”, there is no reason why the same interest rate would simultaneously balance savings (i.e. the increase in loan supply) and investment (i.e. the increase in loan demand). So what is the theoretical rationale of assuming that some interest rate is clearing the loanable funds market (which is defined in terms of flows)?

To illustrate the difference between stocks and flows: the stock of U.S. loans equals around 350% of U.S. GDP (if one includes debts of financial firms), while gross savings amount to 17% of U.S. GDP. Lance Taylor (2016) presents the basic macroeconomic flows and stocks for the U.S. economy to show how and why loanable funds macro models do not fit the data—by a big margin. No interest rate adjustment mechanism is strong enough to bring about this (ex-post) balance in terms of flows, because the interest rate determination is overwhelmed by changes in loan supply and demand stocks. What is more, and as stated before, we don’t actually use ‘savings’ to fund ‘investment’. Firms do not use retained profits (or corporate savings) to finance their investment, but in actual fact disgorge the cash to shareholders (Lazonick 2017). They finance their investment by bank loans (which is newly minted money). Households use their (accumulated) savings to buy bonds in the secondary market or any other existing asset. In that case, the savings do not go to funding new investment — but are merely used to re-arrange the composition of the financial portfolio of the savers.

Final Problem: The Evidence of a Chronic Excess of Savings Over Investment is Missing

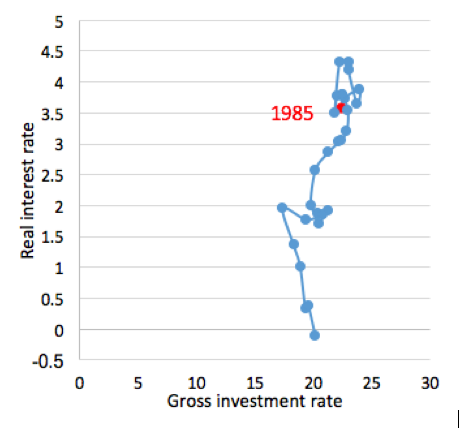

If Summers claims that there is a “chronic excess of savings over investment,” what he means is that ex-ante savings are larger than ex-ante investment. This is a difficult proposition to empirically falsify, because we only have ex-post (national accounting) data on savings and investment which presume the two variables are equal. However, what we can do is consider data on (global) gross and net savings rates (as a proportion of GDP) to see if the propensity to save has increased. This is what Bofinger and Ries (2017) did and they find that global saving rates of private households have declined dramatically since the 1980s. This means, they write, that one can rule out ‘excess savings’ due to demographic factors (as per Eggertson, Mehotra & Robbins 2017; Eggertsson, Lancastre & Summers 2017; Rachel & Smith 2017; and Lu & Teulings 2017). While the average saving propensity of household has declined, the aggregate propensity to save has basically stayed the same during the period 1985-2014. This is shown in Figure 3 (reproduced from Bofinger and Reis 2017) which plots the ratio of global gross savings (or global gross investment) to GDP against the world real interest rate during 1985-2014. A similar figure can be found in the paper by Rachel and Smith (2017). What can be seen is that while there has been no secular rise in the average global propensity to save, there has been a secular decline in interest rates. This drop in interest rates to the ZLB is not caused by a savings glut, nor by a financing glut, but is the outcome of the deliberate decisions of central banks to lower the policy rate in the face of stagnating economies, put on a ‘slow-moving turtle’ by a structural lack of aggregate demand which—as argued by Storm and Naastepad (2012) and Storm (2017)—is largely due to misconceived macro and labour-market policies centered on suppressing wage growth, fiscal austerity, and labour market deregulation.

Saving/Investment Equilibria and World Real Interest Rate, 1985-2014 Source: Bofinger and Reis (2017), Figure 1(a).

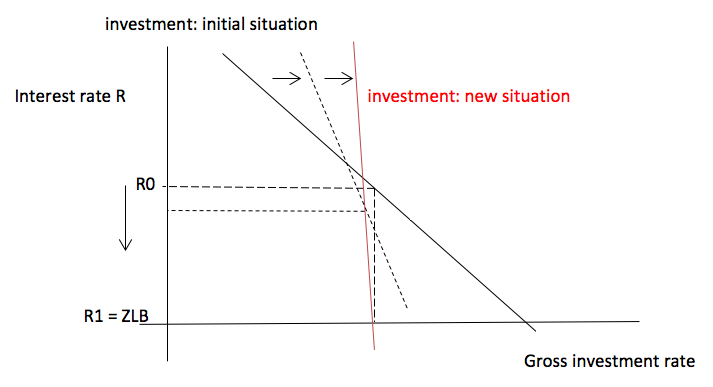

To understand the mechanisms underlying Figure 3, let us consider Figure 4 which plots investment demand as a negative function of the interest rate. In the ‘old situation’, investment demand is high at a (relatively) high rate of interest (R0); this corresponds to the data points for the period 1985-1995 in Figure 3. But then misconceived macro and labour-market policies centered on suppressing wage growth, fiscal austerity, and labour market deregulation began to depress aggregate demand and investment—and as a result, the investment demand schedule starts to shift down and to become more steeply downward-sloping at the same time. In response to the growth slowdown (and weakening inflationary pressure), central banks reduce R—but without any success in raising the gross investment rate. This process continues until the interest rate hits the ZLB while investment has become practically interest-rate insensitive, as investment is now overwhelmingly determined by pessimistic profit expectations; this is indicated by the new investment schedule (in red). That the economy is now stuck at the ZLB is not caused by a “chronic excess of savings” but rather by a chronic shortage of aggregate demand—a shortage created by decades of wage growth moderation, labour market flexibilization, and heightened job insecurity as well as the financialization of corporations and the economy at large (Storm 2018).

Figure 4: Secular Stagnation As a Crisis of Weak Investment Demand

Conclusions

The consensus in the literature and in the commissioned conference papers that the global decline in real interest rates is caused by a higher propensity to save, above all due to demographic reasons, is wrong in terms of underlying theory and evidence base. The decline in interest rates is the monetary policy response to stalling investment and growth, both caused by a shortage of global demand. However, the low interest rates are unable to revive growth and halt the secular stagnation, because there is little reason for firms to expand productive capacity in the face of the persistent aggregate demand shortage. Unless we revive demand, for example through debt-financed fiscal stimulus or a drastic and permanent progressive redistribution of income and wealth in favour of lower-income groups (Taylor 2017), there is no escape from secular stagnation. The narrow focus on the ZLB and powerless monetary policy within the framing of a loanable-funds financial system blocks out serious macroeconomic policy debate on how to revive aggregate demand in a sustainable manner. It will keep the U.S. economy on the slow-moving turtle — not because policymakers cannot do anything about it, but we choose to do so. The economic, social and political damage, fully self-inflicted, is going to be of historic proportions.

It is not a secret that the loanable funds approach is fallacious (Lindner 2015; Taylor 2016; Jakab and Kumhof 2015). While academic economists continue to refine their Ptolemaic model of a loanable-funds market, central bank economists have moved on—and are now exploring the scope of and limitations to monetary policymaking in a monetary economy. Keynes famously wrote that “Practical men who believe themselves to be quite exempt from any intellectual influence, are usually the slaves of some defunct economist. Madmen in authority, who hear voices in the air, are distilling their frenzy from some academic scribbler of a few years back.” In 2017, things seem to happen the other way around: academic economists who believe themselves to be free thinkers are caught in the stale theorizing of a century past. The puzzle is, as Lance Taylor (2016, p. 15) concludes “why [New Keynesian economists] revert to Wicksell on loanable funds and the natural rate while ignoring Keynes’s innovations. Maybe, as [Keynes] said in the preface to the General Theory, “‘The difficulty lies not in the new ideas, but in escaping from the old ones …..’ (p. viii)”

Due to our inability to free ourselves from the discredited loanable funds doctrine, we have lost the forest for the trees. We cannot see that the solution to the real problem underlying secular stagnation (a structural shortage of aggregate demand) is by no means difficult: use fiscal policy—a package of spending on infrastructure, green energy systems, public transportation and public services, and progressive income taxation—and raise (median) wages. The stagnation will soon be over, relegating all the scholastic talk about the ZLB to the dustbin of a Christmas past.

See original post for references

“Forget the myth of a savings glut causing near-zero interest rates. We have a shortage of aggregate demand, and only public spending and raising wages will change that.”

But isn’t “a savings glut” just the same as “a shortage of aggregate demand”? Or is Keynes so out of favor that this is outre thinking?

I mean, I just have this image of economists going, “It’s the chicken! It’s the chicken, I say!” “No! It’s the egg, dammit!”

I second this.

The point is that the “saving glut” is caused bi unequal distribution of income, so it’s a good thing that the “shortage of aggregate demand” is stressed, but still it’s just two names for the same thing.

In the end the “money creation” is needed because there is not a “money circulation”, IMO.

Putting money into the broadest possible distribution and circulation is the key. It could be done with existing money through taxation or with new money through the federal fiscal lever.

Given the “Tax Reform” just passed, odds on the first option look vanishingly long. The second option is what the elites do whenever they want something, normally a war or tax cut. If they want a robust economy, eventually they will pull the fiscal lever.

Feudalism, however, may look better to our depraved current elite crop than any kind of broadly robust economy.

There was a link to an article yesterday called “I write because I hate” that described how incorrect and even dangerous metaphors can be when it comes to understanding the world. Yours is a case in point.

I’m not sure I entirely understand your complaint, but at a first glance a savings glut is one kind of demand shortage, but not every kind of demand shortage can reasonably be called a savings glut. In one situation you have plenty of resource but no use for it other than possible future use (savings glut—you have everything you need so cease purchasing) and in another situation you have insufficient resource (demand shortage—you cease purchasing because you can’t afford to purchase) but no savings glut. You don’t even have the resources you need for today, never mind saving for tomorrow.

Aye, that’s exactly how I understand it, so it is not exactly a chicken-or-the-egg conflation to try to distinguish a savings glut from a lack of demand.

You seem to have missed the point. The problem is wealth distribution. Mainstream economists don’t distinguish who has the savings in their simplistic models. When the rich already have a widget in every room of their mansion, they are not going to buy more widgets no matter how low the price of widgets sink. And when the poor have no money, they will not be able to buy the widgets no matter how much they want them. Demand is not just a function of price. To increase demand, we need a more equitable form of wealth distribution.

One major difference, according to the author, is that the lack of aggregate demand exists, while the savings glut does not. The fact of companies sitting on liquidity, is detached from investment, for which they borrow. That investment is lacking because they do not see good investments, because of a lack of aggregate demand. if they did invest, it would not be constrained by their ‘savings’.

“But this time is different: the glut in savings supply is so large that banks cannot get rid of all the loanable funds even when they offer firms free loans — that is, even after they reduce the interest rate to zero, firms are not willing to borrow more in order to invest.”

That needs some explanation. Banks are not offering US businesses free money (excerpt briefly during the Crash). BBB bonds yields are aprox 4.3% — and most businesses cannot borrow at that rate (excerpt when posting collateral).

For comparison over long time horizons, the real (ex-CPI) BBB corporate bond rate is 2.5% to 3% — in the middle of its range from 1952-1980.

https://fred.stlouisfed.org/series/BAA

Banks are enjoying the privilege of loaning excess deposits to a risk free client, the Federal Reserve.

https://fred.stlouisfed.org/series/EXCSRESNS

This is at 1.5% per https://www.federalreserve.gov/monetarypolicy/reqresbalances.htm as of 12-14-2017

Why should banks risk lending money to entities who might not pay it back?

Loan it to the Fed at 1.5%

The real reason why the political system won’t make any effort to address aggregate demand is because it would help the people.

I suspect that the elite know the truth. They just want to pretend to be ignorant to prevent the system from helping the people who need it.

Let’s bring up Michal Kalecki again:

https://mronline.org/2010/05/22/political-aspects-of-full-employment/

In other words, one potential reason for business to oppose any efforts at addressing the problem is that the people would have more bargaining power. The elite are not after absolute wealth or power, but relative power over the rest of us.

Imagine for example if the alternative was passed say some form of social democracy with full employment and MMT policy.

This would undermine in their view their ability to dominate over the rest of us. Now they may arguably be richer (ex: we might see more money for productive parts of society like say, disease research), but they are willing to give that up for dominating us. That is what we are up against.

If what you say is true (re social democracy + MMT policies), how then to consider for even one second the further existence of a business cadre dedicated to upending such an agreement? We always theorize as if an actual resistance to “our” policies will melt away with the displacement of elite political control. I remember Chile and the “strikes” called to bring down Allende.

The innocence of our imaginations is not only disturbing, but dangerous. Once power is gained and capital has been put in its place, the fight begins right there, anew. Unless we wish to fall into Stalinist methods of “resolution”, consideration for alternate methods of economic control, and an anticipation of backlash, are in demand if the “people” are to prevail.

In my experience as a union organizer and negotiator the opposition by many employers to unions is not particularily because of money, but because of power and the erosion of the employer’s grip of it by the collective action of workers. Many times in my experience employers have spent a boatload more money on fighting workers and hiring union-busting attorneys than whatever wage and benefit increase is being proposed. These employers are acting from their political self-interest rather than the narrow economic self-interest that is commonly assumed.

Great comments — the motivation behind the ideas is a need for power and control.

You can look at the first 20 years of the Cold War as a domestic experiment in social control: incomes were allowed to rise for most people, and inequality was moderated in the interest of politically consolidating the country to support arming and fighting the war.

By the early 70s our handlers — as shown in the Powell Memo, say — had tired of the experiment. With more income, free time, and education, women, students, non-white people, and the newly prosperous working class were entering into contention on every terrain imaginable — and that had to reduced to a manageable level. So they “leaned-out the mix”, reduced income for most people, and bumped up the level of indebtedness and indoctrination.

Now the fuel-air mix is so lean that the engine is starting to miss (for example, the Trump election and the Sanders challenge to the Dem elite). But it looks like they have no other idea but to double-down on austerity. I guess they assume they can maintain global financial and military hegemony on the backs of a sick, unfit, indebted, and politically fractious population — an iffy proposition. No wonder they seem desperate.

That is both the long and short of it.

To engineer the scarcity of the ability to sustain is the the greatest sin

The Trump/Republican tax law tells us (if we needed another message) that the link between economic policy and economic theory is so weak as the bring into question the point of theorizing in the first place, apart, of course, from convincing (semi)-smart but fearful people to remain timid in the face of powerful lunacy. Government spending to replace worn out capital, to satisfy basic material needs of the population, and to underwrite investment in an environmental and educational future worth creating is, OBVIOUSLY, a no-no to Wall Street, war profiteers, and the large population of yes-men and women who promote fear among the middle class. We should spend less time contesting economic thinking that is nonsense. Instead why not spend time proposing and explaining fairly obvious fiscal strategies that will promote a better society, as well as the time that will be needed to defend these life-affirming proposals against the scholastic nonsense that our saltwater and freshwater scaredy-cat friends will put out every day to explain why what we propose will wreck Civilization. Let’s go on the offense for a change.

let’s go on the offensive for a change

precisely, but for the forementioned scholastic nonsense of our salty and fresh feline friends, one would need a salient and orchestrated defense, as to why such meddling with traditional economic trajectories, will mean that: by foregoing my ‘short sided 2018 increase in my personal deduction’, will I actually allow myself to feel benign about the sagging state of civilization, that those ‘cats of all breeds’, have so eloquently perpetuated upon a ‘generation of our peers’.

calling ‘message central’, the ‘greater good awaits’. Yes

I still can’t get my head around the fact that these models can persist in the economics literature whilst everyone knows they are based on flawed assumptions. In science these would quickly end up as part of some distant history. Someone would publish another model, and slowly everyone would start working with it if it had strong explanatory power. Imagine the grief that climate modellers would get if theirs models were so poorly grounded.

You could almost think it was ideology trumping evidence.

Thank you for this post. It was as good as Michael Hudson and all the clear thinkers you post for us. Since we got rid of Greenspan (who admitted that interest rates had no effect on the economy but still freaked out about inflaltion), Bernanke and then Yellen have had better instincts – not straightforward, but better. If central banks know the loanable funds theory to be nonsense, the battle is mostly won. MMT will be the logical next step. Public spending/infrastructure is just good grassroots policy that serve everyone. Even dithering goofballs like Larry Summers. And, as implied above, public spending takes care of the always ignored problem of private debt levels which suck productive spending and investment out of the economy, because unemployment. It’s hard to believe that academics have been so wrong-headed for so long without any evidence for their claims. Steve Keen’s premise, that these academics ignore both the existence of private debt and the importance of dwindling energy sources is also addressed above. Storm’s point – also made by both old hands and new MMT – that there is not a problem with inflation (too much) if there are slack resources seems to have morphed into an ossified rule whereby some inflexible academics see slack resources as scarce resources. What is slack is always a political definition. What is slack today is a filthy environment; there is a great surplus of it. Enormously slack. That’s the good news.

What are the causes of secular stagnation?

Globalization is a disaster wherever you care to look.

Big corporations like Alphabet, Facebook and Microsoft are holding enormous amounts of liquidity . . .

A better example is Apple, with it’s roughly 1/4 trillion dollar cash hoard, beaten out of their Chinese work force in collusion of the Chinese elite. With wages crushed here and there, because they don’t want to pay anyone anything anywhere, where will demand come from? The Chinese peasant slaving away on an Apple farm has a few square feet of living space, like a broiler chicken in a Tyson cage so where is she going to put the new furniture she can’t afford?

Banks create credit, money, and thus purchasing power. […] The vast majority of what we count as “money’ in modern economies is created in this fashion: in the United Kingdom 98% of money takes this form ….

The banks are the MMT practicing intermediary between the federal government and the peasants.

Was the Tax Cut a Hail Mary to get more aggregate demand? Perhaps the Administration is practicing anti-loanable funds on the sly.

So much goodness, don’t know where to start. It’s a long post. It’s my day (singular) off. I’m going long. Deacon Blues* applies.

This:

Now we’re talking. This puts the doctrine in the context of its parent beliefs.

The way I see it, beliefs:economics as operating system:application as mythology:religion. So shorter Storm: The LFF is a BS application for a BS OS.

Been dawning on me lately how neoliberalism is the spawn of a degenerate parent belief system, too. I was even thinking of Weber just the other day.

By speaking in apparently objective, pragmatic, “realistic” terms, public figures are notorious for “dog-whistling” their occult beliefs in terms their congregations hear loud and clear. When Her Royal Clinton’s even more notoriously damned to hell half the population as “deplorables,” she tipped her hand. The obscure term, ephors, is very instructive here.

To refesh the readers memory, “Schumpeter (1934, p. 74) called the money-creating banker ‘the ephor of the exchange economy’—someone who by creating credit (ex nihilo) is pre-financing new investments and innovation and enables “the carrying out of new combinations, authorizes people, in the name of society as it were, to form them.”

Not so fast, though. Who were the original ephors?

Ain’t that something. We don’t call it “class war” for nothing. More on the crypteia:

So Schumpeter’s metaphor is way too apt for comfort. Gets right under my skin.

For a modern equivalent of the pro forma declaration of civil war, I’m thinking “election cycle.” Hippie-punching and all that goes a long way back, eh?

Let’s cut to the chase: what’s all this talk of econ as religion telling us? ISTM arguing with neoliberals as they frame the debate is like arguing with theologians in their terms. My learning psych professor, Robert Bolles, regarding the dismantling of ascendant BS models, always said, you don’t take down an enormous tree leaf by leaf, you go where it meets the ground. Where does neoliberalism meet the ground? And its parent belief system?

Neoliberalism is so poorly grounded, it’s shorting out all over the place. This could be easier than it looks. Storm’s argument is compelling (at least to this newbie). What are its other weakest links? (Not being rhetorical here. I really don’t know. A little help?)

Speaking of Weber, one of the major factors in the Reformation was the utter failure of the Catholic church to be able to produce a valid calendar. The trouble is of course, in their mythos, you have to perform the proper rituals at the proper time and often in the proper place, or you will fry in hell forever and ever amen.

A functioning mythology tells one how to be human right now. The Catholic church couldn’t even tell people what date it was, putting not just ephemeral souls in peril should one die, even more of a daily dread in those days, but lives and property were increasingly at risk.

ISTM we’re in an analogous situation. Our two high holies, Wall Street and Washington, DC, are increasingly irrelevant to us helots. They’re of no use to us in ordering our daily lives. In fact, they’ve becoming openly hostile, dropping any pretense of governing for the common good, and I’m not referring only to Trump, eg, whatever happened to habeas corpus? “If you like your health plan, you can keep it.” The betrayals come fast and furious, too fast to keep up.

Others are rejecting science. A schism here, a schism there, pretty soon it all cracks up one day “outta nowhere.” And I do mean “one day.”

Moving right along, let’s look at “the virtue of thrift.”

Like the “virtues” of the LF fallacy, it arises from a parent belief system. This is from Some Call for Reclaiming the Virtue of Thrift (emphasis added).

That’s what I’m saying: secular institutions are the operationalizations, the applications, of belief systems, and further, we can study them instead of just saying “religion = bad = no further analysis required” and then dismissing it all out of hand.

As with LF-supply and LF-demand, secular and sectarian are not the independent variables they’re made out to be, as argued so well by Cook & Ferguson right here on NC in The Real Economic Consequences of Martin Luther, eg, “[Henry VIII] did not abolish the papacy so much as take the pope’s place.” Same goes for today, IMNSHO: Our “secular” leaders are sectarian high priests in mufti.

The Baptist article also goes on to say what the flock people should do: ignore Wall St. and DC. Unsuprisingly, it’s also chock full of punching downwards and victim-blaming. Payday lending and lotteries are to blame, they say. People just need to be more thrifty, which apparently means, impoverish yourself for the betterment of your betters. Or else.

When HRC damned half of us to Hell, she was dog-whistling loud and clear in a tradition going at least as far back as the wars of the ephors on the helots. When the high priests of our high holy temples of finance tell us we need more austerity, although they speak in terms apparently objective and especially dispassionate, it’s nothing but the failed preachings of the failed priests of a failed church.

Looked at as comparative mythology, and speaking empirically as well (much obliged to the present author and our hosts, sincerely) neoliberalism is no way of being human.

Sure, us nerds get that. But wonky discussions don’t move people. The execrable Mario Cuomo is credited with saying, “You campaign in poetry, you govern in prose,” and I think it’s profoundly true. Telling my friends we’ve debunked the Loanable Funds Fallacy will get me nowhere.

Oy vey. The immense satisfaction I had been feeling, of seeing through neoliberalism all the way to its core, sure was short lived. Now I need to know what MMT says about being human. This is what happens when you start thinking in words, you know. It never ends!

I’ve heard Steve Keen’s writing won’t be much help in popularizing MMT in time. Who’s a witty MMTer? Who can express its way of being human in one-liners? Who’s punchy?

(Administrivia: “Suppose there is an exogenous (unexplained) *rise* in the average propensity to save. In reponse, the LF-supply curve shifts down….” Shouldn’t that be “drop”?)

*This is the night of the expanding man

I take one last drag as I approach the stand

I cried when I wrote this song

Sue me if I play too long

This brother is free

I’ll be what I want to be

Oops left out two links https://en.wikipedia.org/wiki/Ephor

And https://en.wikipedia.org/wiki/Crypteia

Very interesting rant, Knowbuddhau. Imo all we have to do is get over gold. It made sense before the days of sovereign fiat that you saved your coins before you spent them. How else? But fiat is the essential spirit of money while gold was/is a craze. And the Neoliberals are unenlightened just like the Neocons against whom they pretend to react. But they are reactionaries regardless. That’s their problem. All reaction, no action. When Storm refers to Kalecki above saying the original sin of economics was confusing stocks with flows, I take it to mean confusing fiat with gold in a sense. Once upon a time a store of value (a pouch full of gold coins) was the same thing as a medium of exchange. Not any more. Fiat is the only mechanism, spent in advance to promote social well being, that can create an “economy” in this world of zillions of people.

All good points, with a small error: gold coins were also fiat. Their value as coins was bigger than their value as gold. And the residual value of gold is bigger than the residual value of paper in today’s money… But the principle is the same.

Isn’t a bit of an irony that the academic papers being debunked here were commissioned by the Institute for *New* Economic Thinking ? Sad to see its also been corrupted by the neoliberal virus (political Ebola).

The author writes about the fuctional LF paradigm: “Banks, in this narrative, do not create money themselves and hence cannot pre-finance investment by new money. They only move it between savers and investors.” — Note that that narrative doesn’t even make sense *within* the loanable-funds model, because with fractional reserve banking, even if banks were required to loan against pre-existing deposits, they could amplify each dollar of same into multiple units of newly-created credit money. The fact that what really happens goes even further and entirely omits the need for pre-existing funds from the banks’ monetary legerdemain is the reason for my pet term for the “loans create deposits” reality: “fictional reserve banking.”

Aggregate demand increases investment only to the extant that it increases profitable opportunities. If costs remain constant, then obviously an increase in demand increases profitability. But an increase in wages doesn’t merely increase aggregate demand, it also increases aggregate costs because that’s what a wage is to a firm. If aggregate wages were boosted by $1 trillion, consumption will be boosted by less than 100% of that (workers will save some of their increased income) while firms will have to pay the full $1 trillion in increased wages if they are to employ the workers. So how is increasing wages supposed to increase profitability and investment? It seems like it would do the opposite.

We really need to look more at profit. The aggregate profit rate is determined by the cost of the total capital employed in relation to the output. If the costs rise faster than productivity growth, then profitability falls. How do aggregate costs rise? By capital accumulation, by an increase in savings and investment. Thus, it would seem that stagnation can only be reached if too much capital has been accumulated without a corresponding increase in productivity. This hypothesis doesn’t rely on the loanable funds theory (it doesn’t matter whether the money exists before it is spent), but it is more similar to the savings glut explanation because it is the accumulation of capital that leads to the fall in profitability. The suppression of wages is an effect, an attempt to create profitable opportunities when there are none.

Your model is correct when you limit yourself to the variables in your model. Real life economies are complex, dynamic interactions of many variables. At different times some variable become more important than others.

I think your variable, capital accumulation, is itself a complicated mix of many variables. Sometimes the cost of “capital accumulation” may be controlling, and sometimes not. It also depends on which variables within capital accumulation are having the most impact.

I think one of the major problems of the theory of supply and demand is that it may be true as a static model (all other things being equal), but the economy (and life) are not static. Unless you can take dynamic effects into account, then this static or even quasi-static model will just not represent what actually happens. This is just another way of saying what this article says. Over time, the supply curve and the demand curve interact. There is hardly, if any, point in time when all other things aren’t changing.

In my world of simulating the behavior of integrated circuits, the problem involves non-linear differential equations, not just non-linear algebraic equations.

Here is another problem. “… by the national accounts[,] identity of saving and investment (for closed economies),”

Accounting is also a static snapshot of a dynamic system. A bank creates a loan payable in let’s say 30 years. The spending occurs immediately. In accounting terms these two items balance. However, on impact on the economy, they do not balance. Why else would capitalism have noticed the value of buy now, pay later?

Mr. Greenberg:

Savings flowing through the non-banks, increases the supply of loan-funds, but not the supply of money. It simply results in the transfer of title to existing commercial bank liabilities. So savings never equals investment. And all savings originate within the framework of the payment’s system. Savings are never put to work in the payment’s system. Commercial banks always pay for their new earning assets with new money. So all 10 trillion bank-held savings are un-used and un-spent. It is axiomatic. Unless savings are transferred outside the banks by their owners, and invested directly or indirectly, a dampening economic impact causes a drag and decay. This is the source of secular strangulation.

This is no longer a chicken and egg problem of which came first, the chicken or the egg. In real life, there are lots of chickens and lots of eggs. Which came first is irrelevant. Chickens create eggs and eggs create chickens.

Models are a simplification of reality. They apply best when the things that were simplified away don’t matter much. They fail when the things that were simplified away become important. So, when does the loanable funds model apply?

IMHO, the loanable funds model applies when there is a run on the bank. When the fractional reserve banking system is running smoothly, the loanable funds model is irrelevant. That’s why banks have reserves and monetary systems have central reserve banks. These reserve systems let us ignore loanable funds models.

These are great comments! You put the whole process in time.

What I don’t understand is the claim that all those loanable or equity investible funds in banks are dwarfed by the the funds that the corporations have sitting in their overseas accounts that could be put into investments and which the current US tax legislation claims will be released.

It is not clear where any of this capital could be deployed any more than where the banks could deploy their funds.

LOL. The expiration of the FDIC’s unlimited transaction deposit insurance is prima facie evidence, viz., the resultant “taper tantrum”, which I forecast, in my “market zinger”.

That’s the problem with morons, they can’t see the forest thru the trees, viz., they have empirical mindsets.