In 2017, INSEAD published a study by Robert Ayres, an INSEAD Emeritus Professor of Economics and Political Science and Technology Management, and Michael Olenick, an Institute Executive Fellow which looked at all buybacks for US companies over the prior 20 years, discarding firms not in business when the study was done, not in business five years before, too small (<$100M market cap), or trading OTC. The study showed statistically that the higher the buyback ratio –the more firms engage in excessive buybacks – the less likely they are to grow in market cap.

Even though the study got some predictable pushback, an updated version of the analysis shows the findings still hold, that buybacks do not enhance shareholder value.

From the 2017 write-up at Knowledge at INSEAD:

When share repurchases increase debt and reduce spending on innovation and R&D it directly affects a firm’s long-term ability to survive and grow in a disruptive and uncertain business environment. Meanwhile, the question arises: What happens to the money that is “returned” to shareholders by share buybacks? Economic theorists suppose that this money will be re-invested in more promising opportunities. What seems certain is that much of the money will be ploughed into ever-riskier investments in the search for even higher returns. We suspect that much of the money spent on buybacks by established “mature” companies has created a stock market bubble in FAANG stocks (and others) where conventional PE ratios no longer restrain investors in search of growth.

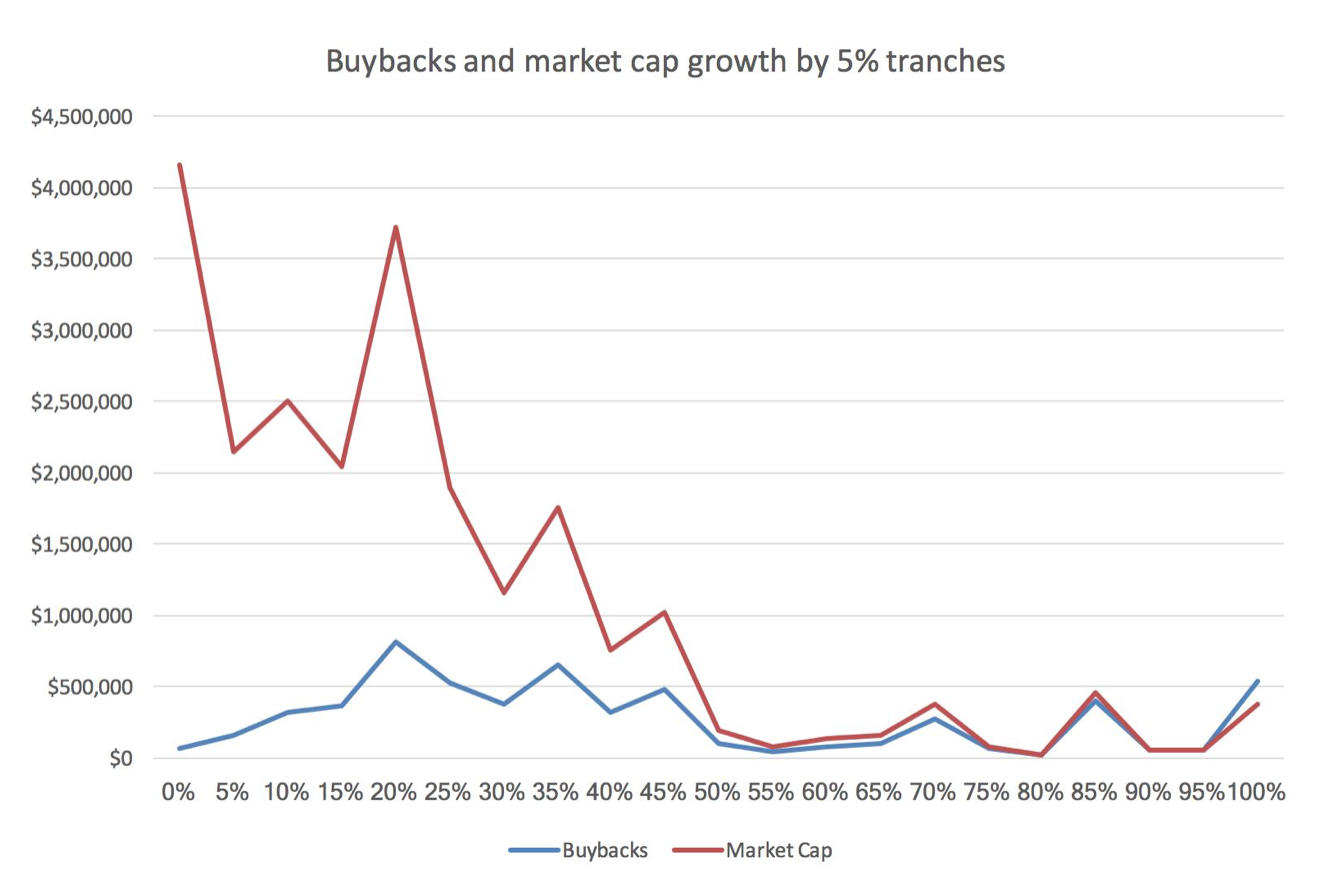

To get a better understanding of the impact of buybacks, we set out to compare the performance of companies that rely heavily on repurchasing shares with those that do not. Our study, “Secular Stagnation”, examined 1,839 public companies in the United States over a five-year time‐scale. We found that the more money a firm spends on buybacks, the less likely it is to grow over the long-term. In fact, as the chart below makes clear, we discovered that not only do buybacks not lead to growth in a company’s market value, they are strongly correlated to a declining market value.

Last month, Steven Pearlstein of the Washington Post cited the Ayers/Olenick study and raised additional concerns about buybacks:

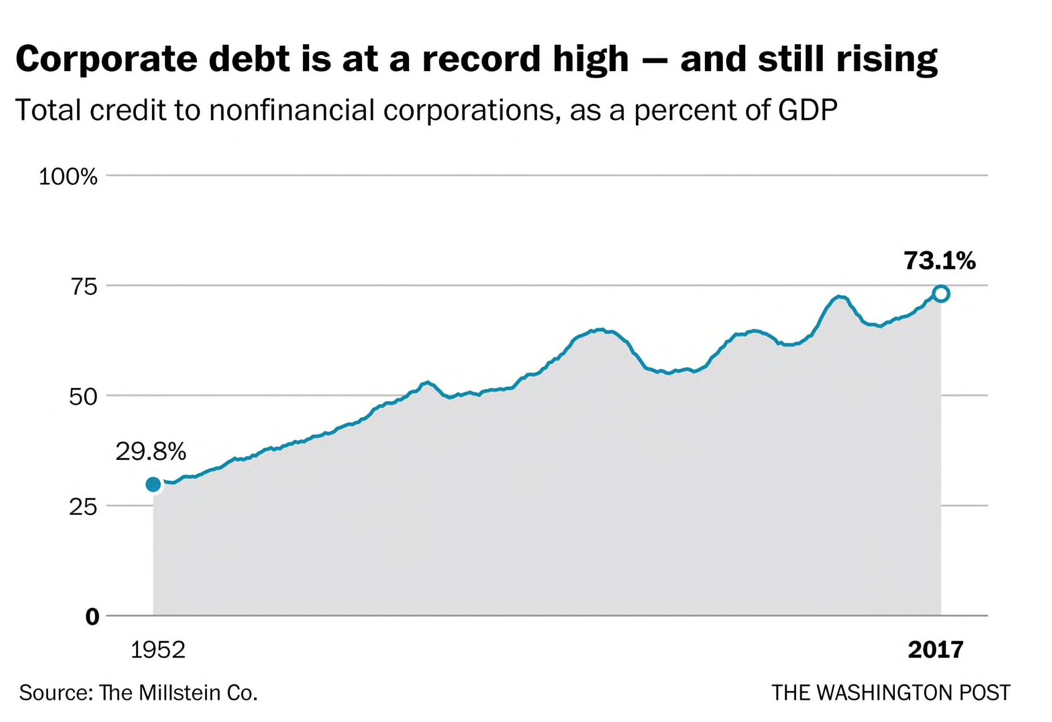

Corporate executives and directors are apparently bereft of ideas and the confidence to make long-term investments. Rather than using record profits, and record amounts of borrowed money, to invest in new plants and equipment, develop new products, improve service, lower prices or raise the wages and skills of their employees, they are “returning” that money to shareholders. Corporate America, in effect, has transformed itself into one giant leveraged buyout….

The best recent research on the folly of buybacks is by two professors at Europe’s top business school, INSEAD. Looking at the 60 percent of companies that have bought back their stock between 2010 and 2015, Robert Ayres and Michael Olenick calculated that the firms, as a group, spent more than 100 percent of their net profits on dividends and share repurchases. They also found that the more a company spent on buybacks, relatively speaking, the less good it did for the stock price….

Corporate buybacks don’t just affect individual companies, however. At this scale, buybacks are also a factor in the performance of the overall economy.

Consider that $1.2 trillion is the equivalent of more than 6 percent of the annual output — or gross domestic product — of the United States, the world’s largest economy. It is larger than the GDP of all but the 15 largest countries in the world. And it is a sum that will likely far exceed the amount of money raised by the corporate sector’s issuing new stock, meaning that for another year, more equity capital is flowing out of publicly traded corporations than flowing in….

The most significant and troubling aspect of this buyback boom, however, is that despite record corporate profits and cash flow, at least a third of the shares are being repurchased with borrowed money, bringing the corporate debt to an all-time high, not only in an absolute sense but also in relation to profits, assets and the overall size of the economy.

Now to the update.

By Michael Olenick, a research fellow at INSEAD who writes regularly at Olen on Economics

In April, 2017, I pulled and analyzed stock buyback data, looking for a correlation between excessive buybacks and five-year market cap change.

I pulled a list of firms that had repurchased their own stock in the prior 20 years. Then excluded companies that were trading over the counter, were no longer trading (usually because they went private), were not public five years before the study, or that had a market cap less than $100 million. In other words, I was trying to compare menschkeit firms performance over a longish-term horizon. To eliminate bias by different legal frameworks, I limited my study to US firms.

Feeling like Edison, trying different lightbulb filaments, I kept querying the S&P Capital IQ database and finally had a list of 1,063 companies that matched the criteria. I adjusted the value of the buybacks for inflation then computed the ratio of buybacks to the then current market cap. Finally, I put them into 10% tranches based on the buyback ratio.

There was a statistical correlation: the more that a firm engaged in excessive buybacks – the higher their ratio – the overall worse their five-year market cap performance. The findings were widely published.

Buyback fans weren’t pleased. They argued I didn’t know what I was talking about. The figures are what they are: it’s just data. They asked why I care: I’m not a finance person. Guilty as charged: I focus on innovation. But if a firm is spending free capital on buybacks – and even borrowing money for buybacks – they’re not investing in innovation. Well, R&D spending is up, or at least flat, argued some. Funds spent on blue sky R&D invention, aimlessly poking around the lab, is still funded but that’s different than innovation.

In any event, the study blew over, Trump and his Republicans passed their mega tax-cut, and businesses predictably went on a stock repurchase binge. Even before that, the Trump Bump drove up stock prices. Maybe they were right; maybe I didn’t know what I was talking about, I thought, watching the market reach dizzying new heights.

A few weeks ago, the Washington Post wrote about the study. It’s been more than a year, and I wondered how well that list acted as a forward-predictor. On a hot night, in my French cottage, I realized it’d be easy enough to find out. With a glass of wine and my French bulldog as an assistant, I returned to S&P Capital IQ, pulling in the current stock price and market cap for those firms in the original study, and compared.

When Edison’s bulb turned on and didn’t burn out he realized he had a business (well, he still had to build electricity plants, fuses, meters, a power grid, and find customers but close enough for our purposes here). When I saw the results from the follow-up, I realized a low buyback ratio basket fund would’ve produced happy investors with trading fees more akin to index funds than hedge funds.

Before the big reveal, an important digression. Stock buyback enthusiasts argue that repurchases are a signal, by management, that they believe their stock is trading abnormally low, that it’s a good deal. The Securities & Exchange Commission commissioned a studyall but using the word bullshit. It showed that managers are more likely to sell their shares after a stock-price bump influenced by a buyback announcement. Obviously, if they’re selling their own stock then they don’t believe the shares are underpriced.

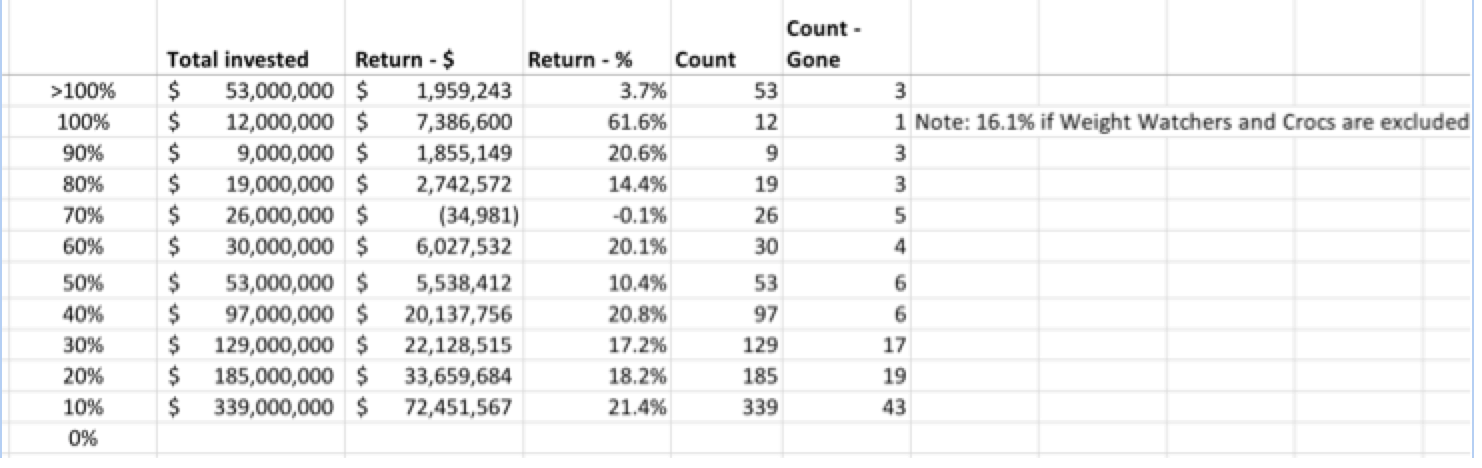

Except, in a small number of firms, this might be the case; some really were, in hindsight, good buys. Comtech Telecom (+130%), Myriad Genetics (+104%), Tailored Brands (+104%), Weight Watchers (+384%), and Crocs (+177%) are all standouts that had buyback to market cap ratios over 90%. That is, when I did my initial analysis, they had all repurchased at least 90-percent of what the market thought their firms were worth.

Weight Watchers. Crocks. I struggled, trying to find the correlation. Maybe it had something to do with the fall of Mario Batali?

Finally, I realized it didn’t matter because – except for the 90-100 percent tier (where both Weight Watchers and Crocs sat) my high ratio companies far underperformed my low ratio companies overall. Choosing the right tranche, except maybe the >100% one, is probably impossible except for stock picking savants … unicorns. Instead, investors would have been better simply avoiding the companies with ratios above 50% and buying companies under 20%. Here is the list, by tranche:

Aha – 62%, say the buyback mavens. Well, yes. If you buy exactly the right tranche. Of 12 stocks. And two of those go gangbusters. If you’d bought stocks with a ratio >90% the overall return would have been 14%. If you bought ratios >50% it’d be 13%. If you bought a basket with ratios <50% you’d have a 19% return. Finally, if you bought firms with a ratio <10% – company’s buying small amounts of stock, probably for employee compensation – you’d have a 21.4% return.

In essence, this proves – looking forward, using results previously published – that even in a bull market the original study was correct. There may be a small number of anomalies but, overall, excessive buybacks stink. Besides lower returns, they’re also harmful to employees, suppliers (who get squeezed), and the overall economy.

Buyback proponents cite Milton Friedman, and follow-up articles, that argue a firm’s sole responsibility is to shareholders and management should do nothing but increase share price by any legal means. These theories (and, no doubt, the revolving door to better post-government jobs) were what inspired regulators to legalize share buybacks in 1982.

Except that Friedman was famously wrong in his seminal article that inspired everything else. The responsibility of your firm, he told GM directors in 1970 – in a lengthy New York Times article – must ignore calls to build cars that are safer, cleaner, and have better fuel mileage. “Businessmen who talk this way are unwitting puppets of the intellectual forces that have been undermining the basis of a free society these past decades,” ranted Friedman, urging GM to Galt’s Gulch.

They listened and watched a long, slow, and painful decline as car buyers changed to companies offering safer, cleaner, more fuel-efficient automobiles. How’d shareholders do? The stock was flat or down for decades. The share price recovered, thanks largely to reckless lending in subprime mortgages, then imploded into bankruptcy. Great work, Milton.

Excluding firms with buyback ratios above 50% – firms that use buybacks responsibly – investors would have realized better returns. The S&P 500 was up 13.58% for that timeframe. My <10% tranche was up 21.4%. My high-ratio firms underperformed by so much that if I had funds and motivation I could’ve shorted the whole batch, putting stop-losses in for the gainers, and done well.

I did a very quick read of this and the quoted paragraph just hit me; I might have missed the answer to this question. Maybe I’m stupid, but I thought that investment in one’s business is how you make a profit. The little enough of economy thought since the Industrial Revolution that I have read kinda stress this. It’s supposed to be bedrock. It is also common sense. So what caused the change? Why the rampaging stupidity? Yes, I know the herds of MBAs poisoning our economy might have something to do with this, but wouldn’t they have been taught about investment in the company itself? If not, why not?

Investment in new products and processes often fails, is inherently uncertain and has long payback times when it works. Often involves listening to the engineers and technical people too.

Engaging in financial engineering of one sort or another is a fairly sure-fire way to short term profits and means dealing with the ‘right sort’ of people. It might ruin the company in the long term, or even medium term, but who cares about that?

I believe share buy backs used to be illegal, considered fraudulent. Once deregulation allowed the fraud, fraud became the unbeatable business model it is now.

So what if it liquidates the business, it makes a few liquidators rich.

it sounds like “share buy-backs” should be re-outlawed back to how it was before 1982, as part of a New Deal 2.0 agenda.

Many particular items on a New Deal 2.0 agenda would be very technical and boring, just like this one. But since boring is the best cover evil ever had, perhaps a Reformationist Movement will have to cultivate a very high tolerance for boredom and picky-poo attention to niggling details among all its members if such a movement wishes to disarm and dispose of all the hidden mines and bombs and booby traps which the Overclass enemy has been planting all around us for lo these fifty years now.

LOL! See Adam Smith, Wealth of Nations, Book III, Chapter 2, paragraph 10, “The pride of man makes him love to domineer, and nothing mortifies him so much as to be obliged to condescend to persuade his inferiors. Wherever the law allows it, and the nature of the work can afford it, therefore, he will generally prefer the service of slaves to that of freemen.” There’s so much in Adam Smith the kakistocracy does not want you to read. He’s sometimes called the first economist (he wasn’t), and he certainly understood the capitalism that was forming in his time.

The C Suite often receives equity as part of their compensation. Buying back shares and paying dividends directly impacts management’s material wealth. And it’s far easier than actually managing the company to do anything productive.

Perhaps we should outlaw the use of any form of “equity” as payment to employees from the CEO to the janitor. That would get rid of the incentive-conflict pollution we see all around us.

But the people making the buyback decisions are not paid based upon their company’s profits, They are paid, primarily, in stock options. So, who benefits from these buybacks? The CEOs, the largest constituency of the 0.1%.

I suspect the answer lies with Bill Black’s theory of looting through control fraud. The CEOs who make the decision to spend capital or even borrow money for stock buybacks most likely have large stock options as part of their compensation package. The have no desire to grow the company because they’re going to be gone in two years. Their best interest is to get as much out of the company as possible in that short time span. If the stock price is high they can sell the stock. If the price is low, then pay out large dividends. Anyway, take the money and run.

Bingo Andrew !!!!!!!!!!!!!

When money is easy…. it’s easier to play games with finance

Making “stuff” is hard and inherently risky……

Buybacks, leverage are easy and almost riskless*

* (you just have to know when to move on before the implosion)

Further to corporate suicide, my TBTF employer has just appointed one its shareholders, Cerberus, as adviser to the management. The TBTF was stuffed anyway. The appointment has caused much consternation and merriment, but as many colleagues wonder what the fuss, mainly in the FT, is about. I have forwarded links to NC for their enlightenment.

Colonel;

Get your ‘Golden Parachute’ ready! I’d say, get any ‘parachute’ you can. The Foxes are now officially running the henhouse.

I worked for a short time at AutoZone corporate headquarters. AZ buys spends heavily on buying back stock. I was in store placement. AZ was rushing to place new stores. After it hit the target of 8,000 or 9,000, it would go back to the oldests stores and re-evaluate their locations. AZ also was all about expanding to Brazil and Mexico. It would never go to any country with chances of having unions formed. Forget Canada.

90% of AZ is do it yourself small repairs. AZ wanted to do more with autorepair shops. Advance, Napa, and O’Reilly’s had most of that market. AZ thought their problem with real mechanics was logistics. Didn’t have the right parts at the right time. My family owns a repair shop. They said it wasn’t logistics problem, it was AZ sold junk. Aside from brake pads, their parts had high failure rates. A mechanic gets burned a couple times have to do work twice, they remember where those faulty parts come from. AZ could spent some money on quality parts suppliers and expanded their business, but they still get crap and sell DIYers who don’t know better.

Thanks for the information about AZ. I do all my auto repairs. If I can afford it at the time, I go to NAPA.

Autozone batteries used to be the best. And the quality of its competitors’ parts is not a given – I will never buy another O’Reilly hub assembly after one I installed lasted less than 60k miles after the original equipment lasted 170k.

Here’s a useful tip – always buy the lifetime guarantee item where it is offered.

And it’s always better to buy from a franchise store – where the owner is right there it is less likely they will sell you crap, especially if you are local.

Napa is more likely to meet both criteria – like AMbrit, it’s where I buy parts mostly.

Not sure why Olenick arbitrarily excluded over the counter stocks. Over 3,000 issues are listed on the Nasdaq, including many giant tech firms such as Apple which are prominent in buying back their own shares.

That said, Bubble III is topping out with an orgy of buybacks like none other ever:

Ramping up leverage just before a recession — they always find a way to do it, as regulatory chaperones such the Fed and SEC snooze soundly in their beds. “No one could have seen this coming,” etc

At S&P’s site, one can compare the S&P Buyback Index to the broader S&P 500 by clicking the “Compare an index” button in red below the chart.

For the past 12 months the Buyback Index still beat the the S&P 500 benchmark by 0.43%. But year to date, it fell 1.28% short of the broad index.

S&P uses a 12-month index for 100 companies where we used a 20-year one, adjusting for inflation, with 1300+ companies. The gains makes sense; they’re index is based on short-term jumps whereas our study is based on long-term value creation. So my buyback index beat theirs, and I didn’t even mean to make an index (well, mine is more like an anti-buyback index). Their buyback index is almost identical to the S&P500 which makes sense; in the past year so many company’s are buying back stock it may as well be the same basket as the whole S&P500.

Just to clarify, S&P’s methodology selects the 100 companies with the highest buyback ratios in the S&P 500 index. Its backfilled history begins on Jan 21, 1994, making 24 years of data.

Twelve months is the default setting in S&P’s chart, but the time scale can be expanded to up to ten years. Here is the 10-year comparison chart, in which the Buyback index beat the S&P 500 index by 14.41% vs 10.70% annually compounded.

From this longer-term perspective, the past 12 months have seen an uncharacteristically poor performance by the Buyback Index. It’s quite different from the broader S&P 500, both in its equal-weighting scheme and its much higher performance.

In their definitions, S&P said inclusion in the index is for buyback ratios for the past year; that’s how they decide what’s in and what’s out. My study has 13x as many companies and looks at their long-term buyback history. The S&P index goes back further but inclusion each year is based, by their definition, on the buyback ratio from just the prior year. I’m looking at a much longer-term buyback ratio.

Answering the earlier question, I omitted OTC pink sheet stocks, not regular stocks. You can see from the list in the prior study, and I think I highlighted in this article, I’m only looking at real companies, not microcap or pink sheet stocks that can be easily manipulated. I don’t know if S&P includes those in their index or not (I’d assume not, for the same reason I took them out).

By definition, the S&P 500 membership from which the Buyback 100 are drawn does not include microcaps or pink sheet stocks.

Presumably, the effect of buybacks should be relatively short-term. Buybacks leave companies more leveraged, but Modigliani-Miller said capital structure shouldn’t affect their valuation.

Since your buyback index and S&P’s buyback index show opposite results, it would be interesting to attribute where the difference lies. Logically, buybacks should boost stock prices; otherwise self-interested corporate managers wouldn’t authorize them.

If the 1,063 companies in your sample are included only during the 12 months following buybacks, do they outperform rather than underperform?

The difference is an excessive number of buybacks. I’m looking at buybacks compared to market cap over a long time period. Many (well, 56, to be exact) of the companies at the top of my list have repurchased at least as much as their market cap over time.

My initial study didn’t look at stock price changes; only market cap. It was more recently (last week, to be exact) that I thought to see what happened to the stock price of the highest ratio companies and found that, as a group, they underperformed from the time of the study to now (though there were a few individual standouts).

I didn’t check if buybacks affected short-term stock price but there are many studies that say they do, and I’d assume they’re true. I know some of the people who have done those studies and think highly of them but the studies typically check only short-term change after a buyback. My theory, and it’s still just that (though the data seem to suggest it’s right) is the buybacks are like a sugar-high. Eat a lot and you’ll bounce off the walls with a lot of energy for awhile. But eventually you’ll find yourself diabetic, overweight, and with bad teeth. That’s where I think many of these companies are.

I agree it would be interesting to look at the difference in my list, and the S&P buyback index, and figure out why mine over-performed while theirs just matched the market.

Driving home (I’m in Europe) I thought of something. I wonder what would happen if my list of excessive long-term buyback companies was removed from the S&P short-term list? Would their one-year returns perk back up?

Stock buybacks with borrowed money are an obviously stupid plan. But even when a company has profits that it can’t put to productive use, I can’t see any real reason for buybacks. If you want to return money to shareholders, why not a special dividend? That would give money back and also, presumably, increase the stock price in anticipation of future dividends.

The goal is to increase earnings per share (EPS) which makes it look like the company is growing which makes the share price go up. The executives then cash out their stock options and everybody is happy.

@Jim A.

July 11, 2018 at 8:04 am

——

Dividends and capital gains have different tax treatments. For dividends to be “Qualified” and taxed as capital gains the stock must be held for a certain time period. Capital gains from the sale of stock are always taxed at a lower rate than ordinary income.

This means that active traders may not meet the holding period and thus lose the benefit of lower tax rates on Qualified Dividends.

Another reason is that dividends increase shareholder wealth dollar-for-dollar, while buying back stock may increase the price by more than the dollars per share actually expended, providing a potentially greater gain on sale.

At the risk of stating the obvious, share buybacks provide a counterbalance to insiders exercising options (and selling the resulting stock). They either drive the share price up, making the options more valuable, or they provide market support to allow large volumes of selling to occur without depressing the price.

They were especially popular during the tech boom in the early 2000s, when stock options weren’t required to be expensed. NVR was one example. They were massively profitable and generated lots of cash, but it all went into stock buyback programs, which were roughly matched by option selling to the point where the number of shares outstanding didn’t drop appreciably.

It would be interesting to see whether there was any correlation between the use of option grants as compensation and magnitude of share buyback programs as described in the OP. That could help support or disprove the theory that it’s all about boosting executive compensation.

IBM and GE committed corporate suicide through share buybacks a long time ago. And their stock has gone nowhere but south since then.

And I’m trying to think of the last innovative product that came out of either company. Believe me, I am really trying.

IBM had enormously creative people who wrote hundreds if not thousands of programs for the PC, in their space time. The programs were considered “not strategic” and only a few were offered to IBM’s customers.

One of them was a GML (HTML) based word processor. IBM wrote all its’ internal documents in GML, but DisplayWriter was the “Strategic Product.”

IBM had worldwide email in the late ’70s.

A Virtual machine Operating System running multiple copies of DOS on i286 PCs in the early ’80s.

Management picked winner and losers, and did not let their customers choose.

You should read the chapter on Gary Kildall in “They Made America” by Harold Evans. IBM comes across, at best, as clueless. His takedown was bad enough he and his publisher were sued for libel, and they won.

This gets much closer to what I do in my day job but that’s a pattern we see repeatedly in “well run” companies.

In the late 60’s and 70’s, Xerox was at the height of its glory and fame, managed by the best and brightest MBA’s, and they entirely botched commercializing everything invented at Xerox PARC (besides the laser printer, and they didn’t even do well on that one).

IBM in the 80’s the computer company — you can’t go wrong with IBM — and their MBA’s flushed it down the toilet.

GE was an original Dow component. They’d been briefly dropped but had been there continuously since the beginning of the 1900’s. The best managed company ever .. brilliant. Until they suffered a cash crunch so severe they needed an emergency loan from the US government to make payroll. They were ingloriously dumped from the Dow just a few weeks ago not because they were poorly managed (which they were), but — almost worse — because they performed so poorly they became insignificant in the index.

Microsoft was da’ bomb but operating systems and office software will soon (finally) run better in browsers, then they won’t matter much.

Ford was once the car company. Then they weren’t and GM was. Then they weren’t and Toyota was. Then they weren’t and now there isn’t really a market leader.

Over and over, in every company and through every industry, managers eventually blow it, focusing on games like pumping up the stock price through buybacks rather than focusing on new customers, new products, new markets, and organic long-term growth. Why? They assume there’s “nothing better to do with the money” than buyback stock. Any manager who says that should be immediately shown the door.

Don’t forget the role that “activist investors” have in this. They buy a portion of the company (but still own less than index funds) and then demand that it start buying back stock instead of other uses of capital. One recent example is Elliot Management taking on Sempra Energy. Once of Elliot’s biggest criticisms is that management isn’t doing enough stock manipulation (of course, they didn’t put it that way, couching it as management is not fully aligned with shareholders).

A question from a (very non-expert) reader of all these interesting comments:

What tax law change would it take to make the stock-buyback scam a memory? Has any member of Congress ever proposed such a legislative measure? [Guffaws of amusement at my expense are hereby forgiven.] But whatever organization eventually supersedes the D Party will need a platform. Perhaps some easy-to-understand gordian-knot-cutting proposals might be included.

One reason firms say they favor buybacks over dividends is that buybacks then increase stock prices but aren’t taxed until the stock is sold, and then they’re taxed as capital gains. I’m about the worst person to ask for tax information – we pick and chose our knowledge fights and that’s a field I’m lost in – but somebody who knows can surely innovate a change so that buybacks are, at best, treated no better than dividends.

@Michael Olenick

July 11, 2018 at 10:07 am

——-

Stock buybacks by companies were considered illegal stock manipulation until about 1982, IIRC. I’m not sure which agency changed its rules but it was probably the SEC. If that’s the case, it would only take a new rule-making to change things back to the way they were. Of course, there would be such a huge outcry that such a change may not be possible short of legislation.

Also, see my comment above about the tax treatment of dividends and capital gains (I’m a tax accountant):

https://www.nakedcapitalism.com/2018/07/michael-olenick-update-confirms-that-share-buybacks-are-still-corporate-suicide.html#comment-2995022

Simply require that a corporate insider can’t exercise options or sell shares at the post buyback value until 12 months have passed from the last stock buyback or announcement of an upcoming stock buyback. Otherwise, the shares would have to be sold at the market price from 12 months previously if it is lower than the market price at the time of sale. That would require multi-year planning to have organic growth.

In addition to increased debt and diversion of cash flows from operations, an under-reported aspect of these massive corporate stock buybacks is that they are also being indirectly funded by employees of many of these corporations as their pension plans are hugely underfunded.

The latest: https://www.marketwatch.com/story/another-company-just-cut-its-pension-plan-what-to-do-if-it-happens-to-you-2018-07-11

Contemplating the stock buybacks, it seems as if our Corporate Elite is working hard to cash out the last little bit of value left in the firms they control.

Close the shades, snuff the lights, and lock the doors.

They took all our machines and all our jobs.

They took all our savings, and all our future’s dreams.

So unlike in that older story …

“… when she looked into the box the only thing that had remained was …”

It too was gone.

They took even that.

Basically this plan is about maximizing executive compensation. It is horrible for long term shareholders, society as a whole, and every other stakeholder.

The executives buy back stocks with either existing money or even borrow money. They get Earnings Per Share up and get a bigger bonus and/or cash in their stock.

The problem is that the company becomes more vulnerable to shocks. They have less cash reserves as they have used them to buy shares back or worse, they have borrowed money. This also means less money and less room for more leverage for future investments that are actually productive.

Stock buybacks should probably be banned. The only legitimate reason to buy a stock back is to make a publicly traded company private again. At the very least, executives should be banned from trading in stock for several months after the buyback. There should also be restrictions on so called activist shareholders from pressuring firms into buying back.

This whole share buyback is a con to make the executives richer and to hurt the common citizen. When companies die, it will be the employees, customers, suppliers, and long term investors who are hurt.

It appears the executives lack any ideas of how to grow the business, and have to do something, so voila “share buyback.”

This whole article seems flawed. Since buybacks are effectively equivalent to dividends, measuring the market cap of companies buying back stocks as opposed to the stock price is as problematic as failing to include dividends in total shareholder return.

It’s very likely that both companies paying dividends and those buying back stock are more mature than those companies not returning capital, and do returns come not through a growing market cap but through cash payouts or a rising share price through buybacks, even if the market cap stays constant.

I suspect if measured correctly, the results would either be inconclusive or in fact tilted the other way, since buybacks are a sign that a company is being managed in a shareholder friendly way (returning capital to shareholders, and doing so in a tax efficient manner).

There are a lot of assumptions here.

Going backwards, you assume the results are not “measured correctly.” The basket of high ratio stocks far underperformed the basket of low ratio stocks in the time period (about 14 months) between the study and now. Before that, the high ratio stocks had worse five-year market cap performance. Is there a different measure you suggest is more accurate? All these companies have been public for over five years, they’re all traded on US exchanges (they’re all US companies), and all have a market cap of at least $100M. They’re all “mature.”

There is the assertion that buybacks are “effectively equivalent” to dividends. They’re not. Dividends release 100% of the funds paid to shareholders; buybacks do not. Sometimes they return more, sometimes less. Dividends do not artificially change the stock price; buybacks do.

Your assertion that buybacks should somehow be measured in addition to stock price or market cap makes no sense. Buybacks are not dividends: the value of buybacks is supposed to be included in the stock price and market cap, unlike dividends which are separate. Adding the buyback to the stock price or market cap would therefore be double counting, unlike dividends which are separate and different.

There is an underlying assertion in your piece that buybacks are positive and that I’m claiming they’re negative without foundation. The numbers are what they are; the higher the long-term buyback ratio, the less likely a firm is to grow. I proved that with firm stats in the first study. In this follow-up I’ve shown the basket of low-ratio firms far outperformed the basket of high-ratio firms over the fourteen months since I first ran the figures.

Asserting that shouldn’t have happened, which I think is the crux of your argument, isn’t especially helpful except maybe in the questioning whether buybacks are always positive for shareholders. That question entirely ignores whether buybacks are good for a firm, whether they result in less innovation and organic growth, and whether they encourage managers to game the finances rather than grow the business.

The two obvious questions here:

(1) Are buybacks any different than dividends in this respect?

(2) Is there any difference between unlevered and levered companies in respect of post-buyback returns?

In some countries, buy backs capital gains are taxed at a lower rate than dividends. But the bigger question remains: what should company’s do when they have cash and no new projects to go after? It is easy to say focus on Rd and things like that but doing it is another matter.

This article is really weak. Stock buybacks should increase stock returns and stock price…But they 100% should not lead to higher market capitalization.

Think about it a company is sending money out of the corporation while getting nothing of value in return. That should lead to a lower market cap. And the article highlights exactly what buyback proponents say should happen – buybacks return cash to shareholders who then reinvest that cash into growing companies like FAANG stock. A buyback is designed to accomplish that. Its like a boring mature company that generates cash like say an electric utility. They should grow slowly. They then return cash to shareholders who reinvest into something with better growth plans. If you disagree with this logic then you are basically advocating for the management of a boring mature company like an electric utility should be reinvesting their earnings into what? Innovative things..do you think that company has management that is good at venture capital? No an electric utility should have management that is trained to management a boring company efficiently not guys who can see new growth opportunities.