Yves here. This post on Brexit reminds me of Tom Ferguson’s district-by-district analysis of the special Senate election in 2010 after Ted Kennedy died, where the win by Republican Scott Brown meant the Democrats lost their filibuster-proof majority in the Senate, a fact the Obama Administration used for meeting the Republicans more than half way. Ferguson demonstrated that level of vote for Brown was highly correlated with foreclosures, a crisis the Obama Administration had largely ignored.

By Nicholas Crafts, Professor of Economics and Economic History at the University of Warwick. Originally published at VoxEU

Brexit in 2019 and the banking crisis in 2007 to 2009 are usually seen as unrelated events. This column argues that they are in fact closely connected. The austerity policies embarked on in response to the fiscal damage resulting from the banking crisis triggered the protest votes of left-behind voters, which at the margin allowed Leave to win the referendum vote. The implication is that the economic costs of the banking crisis are much larger than is usually supposed.

The banking crisis of ten years ago was a serious policy failure (Independent Commission on Banking 2011). Leverage increased dramatically from the late 1980s to the crisis while loss-absorbing equity capital was inadequate. Regulation that addressed these issues could have maintained financial stability at minimal cost to economic growth (Miles et al. 2013).

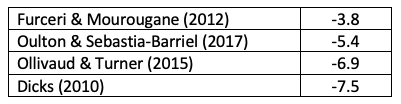

The banking crisis was damaging in many ways, most obviously through the output and fiscal costs of the recessionary shock that it imposed on the economy. The key point for the argument of this column is that it reduced the level of potential output in the economy and accordingly raised the structural budget deficit. This effect comes through decreases in capital, human capital and total factor productivity. A conventional estimate might be that the crisis of ten years ago probably reduced the level of potential output in the UK by somewhere between 3.8% and 7.5% (Table 1).

Table 1 Estimates of the impact of the banking crisis on the level of UK potential output (% GDP)

Note: the estimates in the first two rows are derived from econometric analysis of the average effects of past banking crises. The third and fourth rows are estimates for the UK in the context of the 2007-2009 crisis.

Sources: as listed above.

Plans for fiscal tightening were formulated in the context of contemporary estimates of the increase in the structural budget deficit since before the crisis (Table 2). Both the outgoing Labour government and the incoming Coalition government accepted the case for significant fiscal consolidation to restore fiscal sustainability, although the parties differed somewhat on its composition, size and timing. Austerity was a bi-partisan policy response to the fiscal implications of the banking crisis without which it would not have been instigated by either party.

Table 2 Fiscal implications of the banking crisis (% GDP)

Source: Emmerson and Tetlow (2015).

In the event, the austerity programme relied very heavily on cuts to public expenditure which comprised 89% of the fiscal consolidation. In turn, a substantial part of these cuts were implemented through reductions in grants to local authorities which fell by 36.3% on average between 2009/10 and 2015/16. Across local authorities the reductions in public spending per person ranged from 46.3% to 6.2% with the most deprived areas experiencing relatively large cuts (Innes and Tetlow 2015).

After 2010 support for UKIP in local elections surged to the extent that they became a serious electoral threat to the Conservatives who therefore promised a referendum on EU membership. In a difference-in-differences analysis, Fetzer (2018) shows that rising support for UKIP at the local level was strongly correlated over time with the impact of austerity in areas with weak socioeconomic fundamentals. The effects are sizeable: for a district experiencing the average austerity shock UKIP’s vote share would rise by 3.58 percentage points based on the pooled estimate for the post-2010 period and 11.51 percentage points based on the estimate for 2015. Given the tight relationship between the vote shares of UKIP in elections and Leave in the referendum, these results suggest that Remain would very probably have won in the absence of austerity.

Clearly, in principle, fiscal consolidation could have been designed differently; for example, increased taxation could have played a much bigger part. Also, the Conservatives winning a majority in 2015 and having to implement their referendum promise was something of a surprise especially as fiscal consolidation was still ongoing. As it turned out, however, the sequence of events seems clear – the financial crisis led to an austerity programme which boosted support for UKIP enough to make the Conservatives promise a referendum and antagonised left-behind voters whose protest votes were enough to tip the balance for Leave.

So, Brexit is a legacy of the banking crisis although it was not an inevitable consequence. With this analysis to build on, in a recent paper I calculated a total impact on potential output in which I added the indirect impact through Brexit to the direct impact of the banking crisis (Crafts 2019).

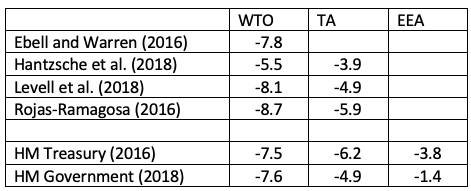

The general assumption in studies of the economic impact of Brexit is that it will entail an increase in trade costs for the UK. In turn, this will imply a reduction in trade volumes and, accordingly, an adverse impact on the level of productivity and thus on the level of GDP relative to the counterfactual of staying in the EU.1 The magnitudes of these effects depend on the details of the new trading arrangements that are assumed to supersede EU membership as well as on model specifications. A ‘soft Brexit’ – for example, the UK leaving the EU but staying in the European Economic Area – would be expected to have a smaller negative effect than a ‘hard Brexit’ – for example, leaving without a deal and trading on a WTO-rules basis – and a trade agreement with the EU would presumably have an intermediate effect.

Membership of the EEA seems unlikely under the present government. In that case, the TA and WTO columns of Table 3 can be seen as representative of mainstream estimates of the impact of Brexit on the level of UK potential output when adjustment is complete perhaps after 10 years or so. The range is from -3.9% to -8.7% of GDP.2

Table 3 Estimates of the long-term impact of Brexit on the level of UK potential output (% GDP)

Note: all estimates include long-term impact on level of productivity but do not take account of any impact from migration.

Sources: as listed above.

This implies that a new structural budget deficit would emerge even allowing for the ending of the UK’s net budgetary contribution to the EU. Based on the arithmetic in Emmerson et al. (2016) this would amount to about 5.7% of GDP if a hard (WTO) Brexit reduced potential GDP by 8.7%.3 This would bring a whole new dimension to the concept of ‘self-defeating austerity’. A quest to eliminate a structural deficit estimated by HM Treasury at around 5% of GDP in 2010 would have given rise to an even bigger one down the line.

The banking crisis and Brexit are usually seen as two unrelated setbacks. In fact, there is a close connection between them which runs through the fiscal consolidation that had to be undertaken in the wake of the financial crisis. The pain of austerity promoted the rise of UKIP, a referendum on EU membership, and a win for Leave. None of these outcomes was by any means certain ex ante but they were the realised results of the policy response to the banking crisis. If Brexit is seen as an outcome of the banking crisis, then the total loss of potential output from that debacle is approximately doubled and lies in the range 7.7% to 16.2% of GDP.

The implication is that, if the risks of unfortunate policy responses following a crisis are taken into account, there are even stronger reasons to regulate the banking system strictly, in particular to ensure that it has adequate levels of loss absorbing equity capital. Miles et al. (2013) show that the social benefit-cost ratio of reducing leverage substantially is high in any case. The events of the last ten years indicate that it is even higher than they thought.

See original post for references

If I’m reading this correctly, it is assuming that there is a correlation between the UKIP vote and the Brexit vote – I’m not sure this is true at all – far more people voted for Brexit than for UKIP, and from memory, UKIPs vote was much more heavily slanted to the south of England than the Brexit vote.

Obviously, austerity and economic decline contributed strongly to a ‘if that lot in London are in favour, I’m against it’ type vote. But I think its simplistic to see it as a response to economic conditions – the campaign for Brexit started in the immediate aftermath of the Thatcher years and grew steadily through boom cycles. I think the deeper cause is cultural – as argued by Fintan O’Toole:

Thanks for the link PK. I think Fintan O’Toole’s article is very perceptive.

Brexit IMO is a result of scapegoating foreigners for the failures of successive UK Governments. It is a classic elite diversion tactic:: – distract the poor from the real cause of their problems, the governing elite, by blaming their problems on people from other places (‘bloody foreigners’ in the English parlance).

I don’t think it is simplistic to see economic conditions as an important factor in Brexit especially if we go back to Thatcher. During Thatcher’s terms, and afterwards, the number and quality of the jobs in the North declined, drastically at times, less so at others. There were two severe recessions during Thatcher’s time in power, which did away with Industrial jobs, and the miner’s strike, and her economic policies deliberately focused on creating financial and service jobs, most of which were in the South East, especially London, while the industrial jobs and mines were in the North. During the nineties some of these services jobs moved to the North of England, especially Leeds. Meanwhile the MSM increasingly denigrated refugees and migrants to the UK, and the EU. Other factors also contributed to rise of English Nationalism (great analysis by Fintan O’Toole), but I would argue the primary cause is economic. I would like to point out that I went through secondary education and university in the ’80’s in the South of England, and lived in the North (Manchester and Leeds) throughout the 90’s.

Thanks for your sound observations and the link to O’Toole’s piece. He writes that we are exchanging 1st class seats for 2nd class – how apt! – but perhaps after the breakup of the union things will stabilize.

i don’t think it’s that, the UKIP perspective was just background for why the tories called a referendum. the real point is that those areas that suffered the most from austerity were the ones that most voted to leave.

Isn’t the ‘implication‘ that allowing the banking system to, make the rules, self-regulate, and then decide on how the government will respond to the disasters it creates, is a sure-fire recipe for the rest of us ending up starving and penniless?

And if you allow the rich and powerful to short the world economy, you can bet the world economy is going down.

Yup, truly the revolt of the ignored.

And the banks will continue to clean up on the aftermath of the crisis.

Aye! Well, shiver me timbers, secure the booty, land ahoy…

I think they are starting to realize the Hamptons may not be as defensible as they thought.

https://twitter.com/LHSummers/status/1085963444594061312

In the US the most galling part of austerity,imo, was it exempted Wall Street and gave even more tax cuts to the wealthy. So, CRISIS!, you in the 90% must take austerity to save the country, while we in the rich club get more goodies. Shared sacrifice it wasn’t.

This doesn’t make sense to me – why would austerity policies have generated feelings against the EU? Should one not be able to confirm this thesis by looking at regional variations? I see no attempt to correlate regional outcomes of the referendum with the regional effects of austerity policies. “Given the tight relationship between the vote shares of UKIP in elections and Leave in the referendum, these results suggest that Remain would very probably have won in the absence of austerity.” doesn’t help because it is not clear how this relationship is distributed regionally. Some maps would have been helpful.

When I look at unemployment levels for 2010 (https://academic.oup.com/cjres/article/4/3/289/335181 – Figure 6) I get a substantial mismatch when compared to the referendum outcomes (https://en.wikipedia.org/wiki/Results_of_the_2016_United_Kingdom_European_Union_membership_referendum#/media/File:United_Kingdom_EU_referendum_2016_area_results.svg). Furthermore, women voted to remain (https://www.ipsos.com/ipsos-mori/en-uk/how-britain-voted-2016-eu-referendum), but “have arguably been worst affected by the crisis…” (https://www.oxfam.org/sites/www.oxfam.org/files/cs-true-cost-austerity-inequality-uk-120913-en.pdf). Finally, though “The disproportionate impact of welfare reforms on young people shows that the effects of austerity have not been evenly experienced.” (http://shura.shu.ac.uk/11550/1/Crisp%20Young%20people%20and%20UK%20labour%20market%20policy.pdf), young people voted overwhelmingly to remain (https://www.ipsos.com/ipsos-mori/en-uk/how-britain-voted-2016-eu-referendum).

A ‘crossvalidation’ of the thesis shows that Brexit cannot be blamed on the banking crisis.

There are some studies IIRC (from LSE?) which show correlation between the relative income levels by region of England which as I recall showed that the poorest areas tended to vote Leave. Wouldn’t these have been the worst affected by the austerity measures, on the basis that the poorest people and areas will feel the effects of austerity more for the simple reason that they have relatively less income in the first place?

I think we are talking here in particular about cuts in public spending?

Remember that most Tory voters voted Leave while most Labour. Others votes Remain. Those Try voters are most likely Daily Mail and Express readers, nationalistic and somewhat xenophobic believers in the greatness of Britain, well England anyway. Many actually voted UKIP. They alone weren’t enough to win for Leave. Labour voters in the midlands and north who felt vaguely that the EU was responsible for austerity, cuts etc tipped the balance. Older ones probably also hold delusions in England’s greatness. A bit like Trump’s win, most Republicans voted for him but he won because some Democrat voters bought into his rhetoric about jobs, and H Clinton is odious.

I recognize that the authors need to accept this premise for the rest of their research to make sense, but it seems politically naive in the extreme:

Austerity has been the universal policy solution for years, being deployed whenever an excuse, like a bankster looting spree gone wrong, emerged. As c_heale and others above note, this is part of an ongoing neoliberal project since, at latest, Thatcher. I concede that the the GFC provided the ‘shock therapy’ that emboldened Friedman acolytes around the world to make grabs for public assets, but guessing brexit costs and adding them to guessed GFC costs seems like a bizarre exercise.

If I were to write a post at NC, I would look at how the wheels are really falling off the poster-children for the neoliberal infestation, with the US and UK being essentially ungovernable in important ways at this exact point in history, and France not looking all too stable either. I think the main result of the GFC that fed into the current popular ressentiment is the revelation of our financial elites as not only stunning corrupt, but also stunning incompetent and brazenly impervious to legal or financial consequences. The GFC and the responses to it basically collapsed the credibility of the political ruling class and damaged that of their infotainment industry fluffers. Their own panicked launch of the Fake News meme a decade later may have critically undermined their remaining credibility. But that would be another discussion I suppose.

It always seemed to me that the quickest route to re-establish serfdom was to follow the precepts of Hayek and Von Mises. Why anyone should advocate the prescriptions of two Habsburg functionaries who signally failed to preserve their Emperor in all his glory amazes me. Unless you ask the question ” Cui Bono “. Well that is obvious. The rentier, the price gauger and the monopolist-all people railed against by Adam Smith.

Then we have Ayn Rand. Pity the poor rich kid, oppressed by the majority who have none of his skill, acumen, sensibility and sensitivity. Pity the country that oppresses such delicate flowers.

Mr O’Toole in, in his excellent book ‘ Heroic Failure Brexit And The Politics Of Pain’ To paraphrase Richard Nixon he suggests that we Brits ‘ are all Ayn Randists now ‘. It is as good an explanation for the mess we are in now as any I’ve read. We are all victims!

When the leavers realise that they have not forged a revolution but only broken the wheel there will have to be a reckoning.

The rentier, the price gauger and the monopolist-all people railed against by Adam Smith.

I think the Brexit vote result was supposed to be a reckoning against neoliberalism’s economic predations, but is being turned by the neoliberal politicians and their friends in msm into a ‘reckoning’ against the people neoliberal economic policies have harmed the most.

The Brexit result was whatever any particular audience wanted it to be IMO. ‘You want less neo-liberalism – Brexit is the answer’. ‘You want more neoliberalism. Brexit is the answer’. That was the genius of the Leave campaign, promising all things to all, depending on the targeted audience. The problem is now they have to deliver on their mutually contradictory promises and cannot.

typo

please delete “To paraphrase Richard Nixon he…”

Sorry

Nick Crafts was the leading figure in Economic History when I was a kid. Interesting stuff.

So reading other things, it seems an extension pretty much has to happen now. Apparently even if they had voted Yes to May’s deal there wouldnt have been enough time to pass the bills. I read that July 1st is likely to have to happen, despite the EUs unwillingness to give open ended extensions.