CalPERS is having trouble getting anyone reputable to endorse its unorthodox, risky private equity scheme. the centerpiece of which is to create and fund two new large fund managers that would be completely unaccountable to CalPERS.

The idea should have died a long time ago, but CEO Marcie Frost is still desperate to get it done, despite staff members admitting in a November board meeting that CalPERS’ newfangled companies would have higher costs in the early years and would also generate lower returns than conventional private equity funds. This is tantamount to an admission that CalPERS board members, executives, and consultants would be violating their fiduciary duty to CalPERS if they were to let this plan go forward.

As we’ll show below, one of the experts that CalPERS has now had in twice, with the apparent aim of helping to persuade the board to approve this obviously bad idea, has taken the unusual step of publishing a long tweetstorm shortly after a presentation at CalPERS last week that makes clear that he is opposed to CalPERS’ plans. Mind you, Dr. Ashby Monk is too polite to say, “CalPERS needs its head examined,” but if you look at his forceful and clear recommendation, it is the polar opposite of Marcie Frost’s private equity plans.

Even though Dr. Monk has made clear his general position on private equity for a long time, it seems noteworthy that he felt compelled to give a one-stop-shopping version on Twitter later in the very same week that he spoke at CalPERS. Recall that this was the second time Dr. Monk has spoken to CalPERS board. We pointed out that CalPERS had snookered Dr. Monk the first time he presented:

CalPERS has even gone so far as to mislead its own cheerleaders. The pension fund invited Dr. Ashby Monk of Stanford to speak at a public board meeting in August, and Frost quotes Dr. Monk in her promotional article. Dr. Monk took a generally positive tone but pointed out that what CalPERS was planning to do was not direct investing, which means having CalPERS staff make private equity investments itself, but was forming its own general partners. Dr. Monk then described how some large investors had used “pick the pickers” methods to assure that the board was loyal to the organization that provided the money.

I spoke with Dr. Monk for a half-hour after his CalPERS presentation. He acknowledged in our conversation that CalPERS had not disclosed to him that the board of the new entity would be chosen by its management and CalPERS would have no say in the board’s selection. Thus he cannot be deemed to have approved what CalPERS is doing, since he was misinformed.

We pointed out in this same October post that CalPERS has featured Dr. Monk prominently in a brochure to CalPERS beneficiaries as if he were supportive of CalPERS’ plans. Reader Brooklyn Bridge pointed out that even with CalPERS’ cherry-picking, Dr. Monk’s support had actually been so heavily qualified as to be empty:

“But as Dr. Monk said, “I’m encouraged that if you can get the governance right, if you can evolve this into a platform that can recruit the right talent, you can succeed.”

Even as a total know nothing, I would see pure bunk in this line alone (never mind, “We’ve listened to our Stakeholders”… and they want dumb, dumber and dumbest). It might as well read, “I’m encouraged that if you succeed, and succeed well, you are well on your way to success!”

The title should be, “Taking aim. Exploring a new Private Equity Mark“

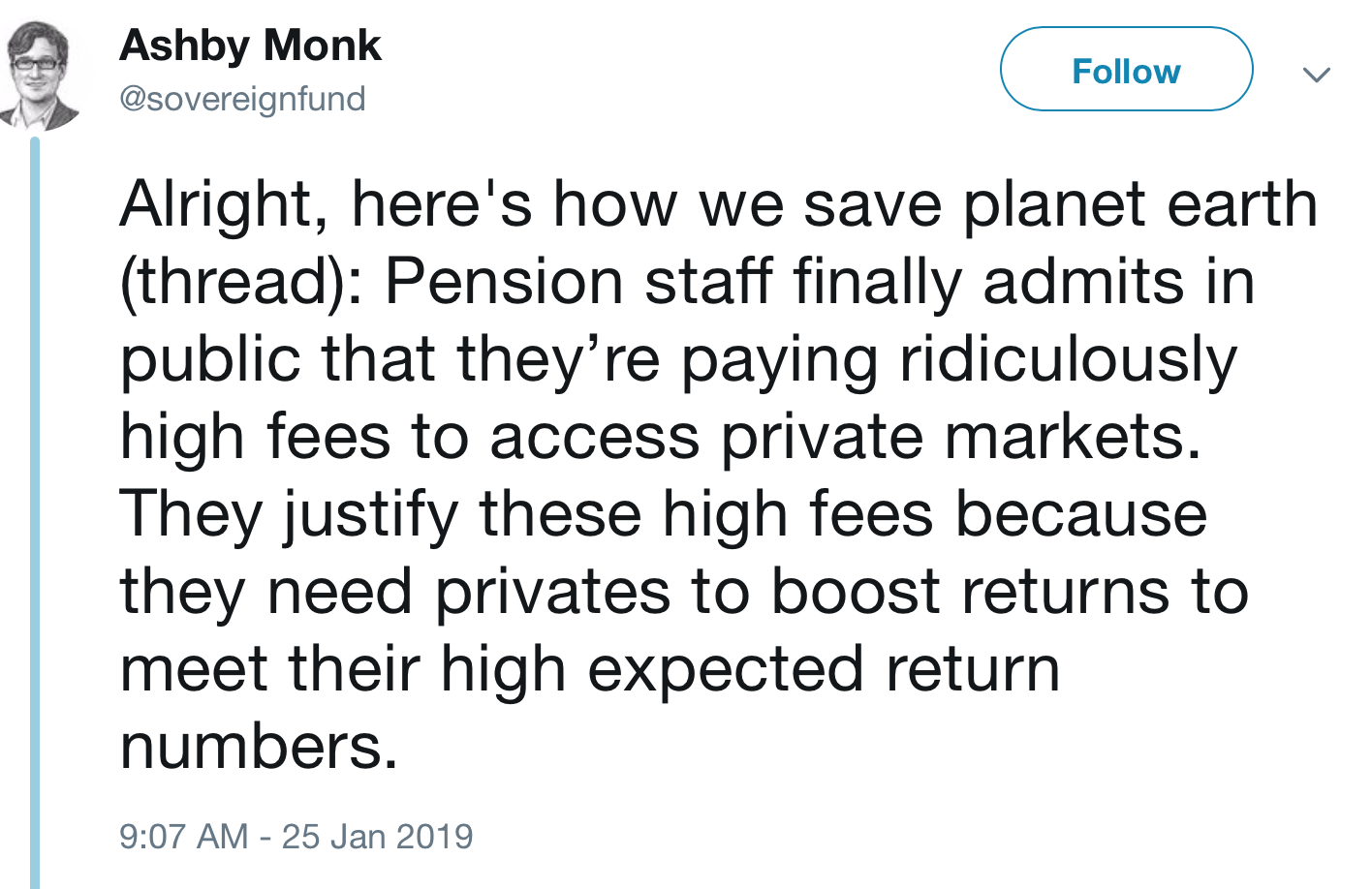

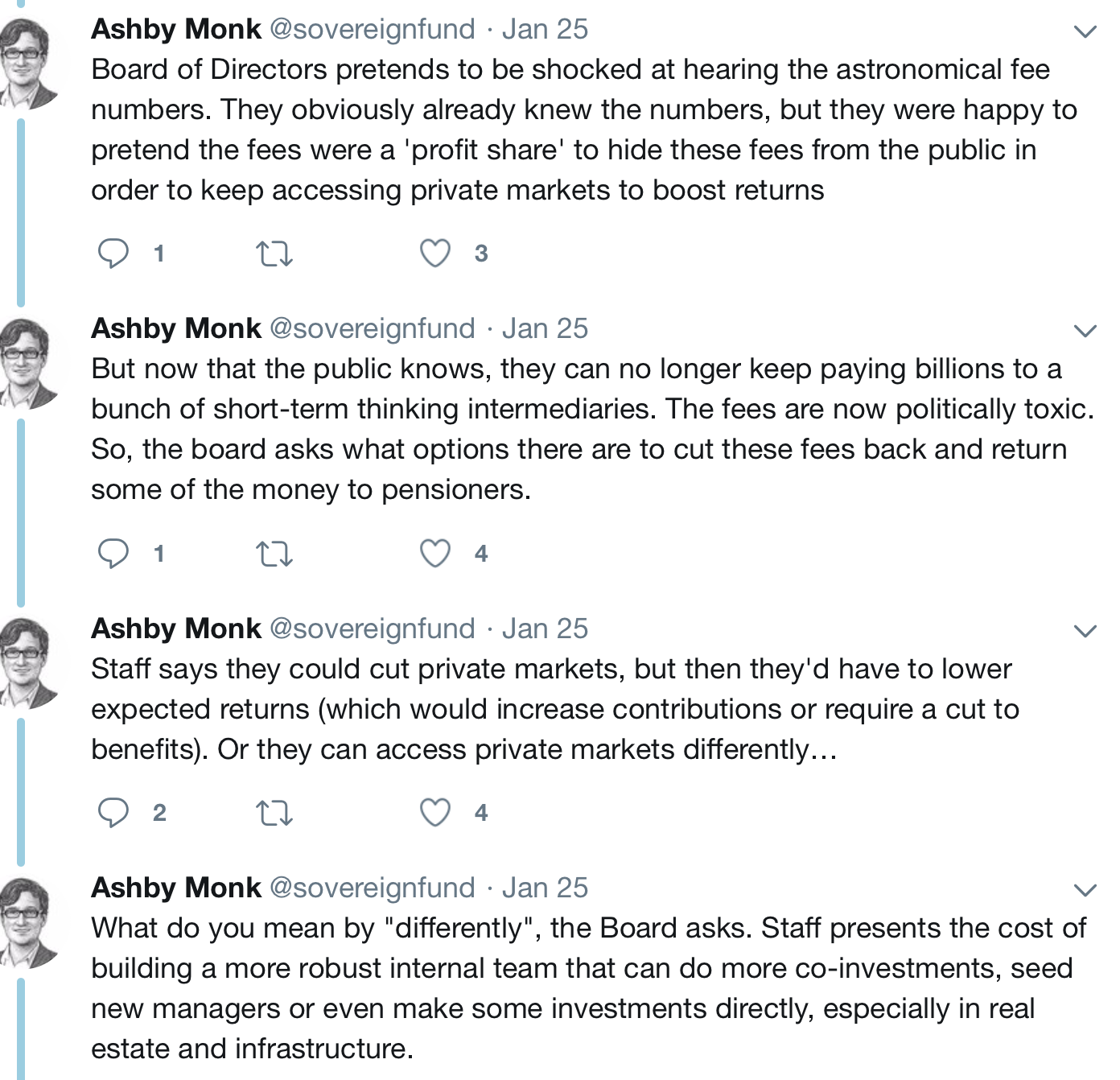

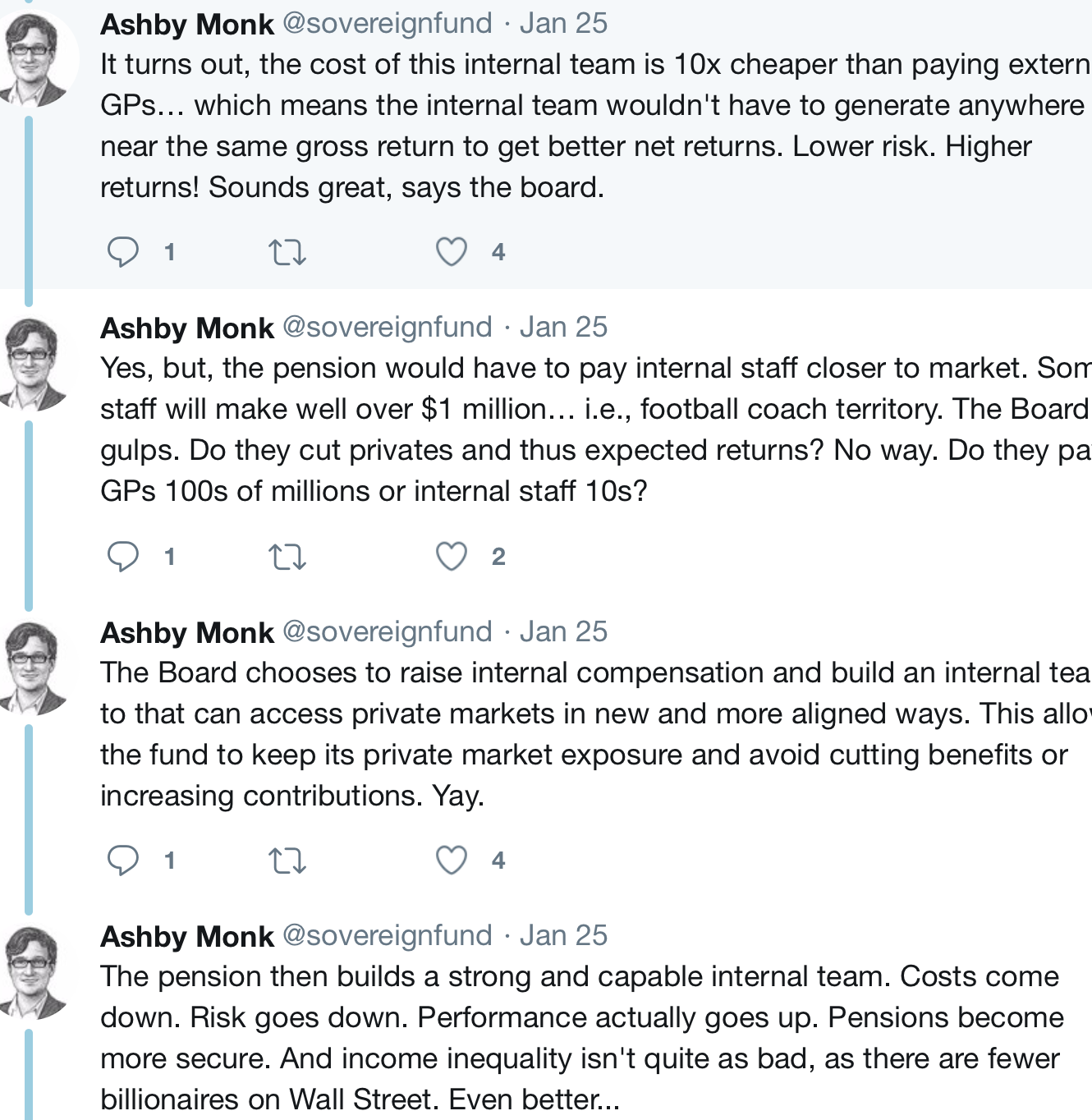

Below is Dr. Monk laying out his recommended private equity to public pension funds…and this recommendation is the polar opposite of what CalPERS has been trying to get its board to approve. It’s unlikely to be a coincidence that he posted this tweetstorm within days of visiting CalPERS:

This is a recommendation to bring private equity in house, period. As we have said repeatedly, that is the polar opposite to what CalPERS is trying to do, CalPeRS wants to create new investment vehicles which will be even riskier and less accountable than inventing through private equity fund managers.

Dr. Monk also points out that if your are serious about ESG (emphasizing environmental, social, and governance investing), you need to run your private equity investing in-house. Recall that CalSTRS had a long and uphill to get fund manager Cerberus to sell its stake in a firearms maker. That’s only one holding. Consider this part of a clearly unhappy 2015 press release:

Although Cerberus committed to sell its holdings in Remington Outdoor, thus far that pledge has not been fulfilled. As we continue to push them on this front, we have also worked to exercise patience and give them time to execute what is a complicated transaction.

But we understand the patience of our membership wears thin. Unfortunately, as a limited partner in a private equity investment pool controlled by Cerberus, CalSTRS has very limited rights. Contractual obligations and legal constraints severely limit our options to exit this investment.

More importantly, we cannot take unilateral action, in this case, to remove a specific company from an investment pool. Nor can we expose the fund by prematurely or imprudently selling about $375 million worth of holdings at a loss without thoroughly exhausting all other options first. While we cannot share the details, we want to make it clear that all potential options are being fully considered and have been for some time.

Even though we don’t have the same level of enthusiasm for ESG investing that CalPERS does, the point is that CalPERS pretends to be serious about it, and it can’t be if it is investing through third-party managers. It can only have very limited firm prohibitions; otherwise, it constrains the investment universe and becomes an unattractive funds source.1

Dr. Monk’s tweetstorm came after he repudiated another central element of CalPERS’ scheme, that of its lack of transparency. Recall that CalPERS now provides limited information about all of its private equity investments every quarter, such at the commitment amount, the total funds invested, and the returns, expressed as IRR and investment multiple. That disclosure came about as the result of a settlement with the Mercury News in 2002. Many other public pension funds now provide similar fund-by-fund information. One of the important aims of Marcie Frost’s private equity plans are to end this and other disclosures.

Recall that at last December’s board meeting, General Counsel Matt Jacobs stated that the purpose of the new private equity scheme was secrecy (see 3:36:58):

Board Member Margaret Brown: Mr. Cole, you know that this Board has a fiduciary responsibility to 1.9 million members and thousands of employers. And so with that in mind, I wanted to let you know that I have a lot of concerns that we are putting this program together, I think, in part to avoid transparency, Bagley-Keene, the 700s, and the Public Records Act request.

And so what I’m wondering is since CalPERS is drafting the agreements we could, in fact, make them — at

least due to a Public Records Act we request, we could, in fact, require that of our partners in these companies could we not, since we’re drafting that agreement? Oh, good. Mr. Jacobs, we’ll have him come up and answer.Investment Director John Cole: That’s a legal question.

Board Member Brown: Yeah.

Investment Director Cole: I don’t want to get out of my lane

General Counsel Matt Jacobs: Well, at a high level, I suppose we could. I think that would defeat the entire purpose of the endeavor that the Investment Office is undertaking, which is that these are private investments, and they’re private for a reason, which is that the — the financial information needs to be private. And the people running them have these types of preferences.

A little more than a month later, at the board’s offsite meeting on January 22, one of the private equity experts invited to speak, Dr. Ashby Monk, blew up the CalPERS’ claim that secrecy is necessary and desirable at 1:31:10: “I’ll offer some bit of extreme views. I think there is no balance. 100% should have ESG and transparency.”

And CalPERS has also used as a defense that private equity funds don’t like transparency. Mind you, we’ve had the limited partnership agreements of many of the biggest fund managers posted on our site for years and none of them appear to have suffered as a result of these supposed trade secrets getting out in the wild.

One of the amusing spectacles at the offsite was Jonathan Coslet of TPG trying to pretend that the over-the-top secrecy requirements for private equity limited partnership agreements was somehow the doing of investors and TPG was perfectly fine with everything being out in the open. Starting at 1:06:30:

Board Member Margaret Brown:: As you may know, we have been having open discussions about the secrecy of private equity agreements. And I understand that the Pennsylvania state legislature has recommended substantial narrowing of the laws that exempt from FOIA the entire contracts between private equity funds and investors like public pension funds. I am curious in TPG’s case investors or TPG was harmed by the release of what I understand was one of your agreements by the Pennsylvania state Treasurer. Just wondering. Several years ago that happened, it was out in the public domain and I’m just wondering if there was any harm to investors or to TPG when that happened.

TPG Chief Investment Officer Jonathan Coslet: I can’t really comment specifically, but my sense is that our perspective would be that we want to respect the confidentiality that you would like and if you our clients would like confidentiality, confidentiality with what is essentially a private contract, we would like to respect that. Different organizations have different feelings about that. We have sovereign wealth funds, insurance companies, endowments, pension funds, individuals. So we just want to respect the confidentiality our clients would like.

As Dr. Monk said to an audience member later, this claim was completely false. Private equity fund managers have fought fiercely to keep their limited partnership agreements secret, absurdly claiming the entire agreement to be a trade secret. This systematic shielding of these agreements started, ironically, in the wake of the 2002 Mercury News settlement with CalPERS that we mentioned earlier. Private equity firms went to every state and got either legislation or state attorney general opinions shielding private equity agreements in full from disclosure. Even now, these alternative investment agreements are the only contracts that state and city governments enter into that are secret.

We gave a long-form debunking of the idea that anything in private equity agreements could be considered a trade secret in 2014, when we published a set of private equity agreements that the Pennsylvania Treasurer had on its website with no password protection. That includes the TPG contract that Margaret Brown mentioned. A key section of that post:

For decades, private equity (PE) firms have asserted that limited partnership agreements (LPAs), the contracts between themselves and investors, should be treated in their entirety as trade secrets, and therefore not subject to disclosure under Freedom of Information Act laws in any jurisdiction. These private equity general partners argued that the information in their contracts was so sensitive that it needed to be shielded from competitors’ eyes, otherwise their unique, critically important know-how would be appropriated and used against them. In particular, PE firms have made frequent, forceful claims that their limited partnership agreements provide valuable insight into their investment strategies. The industry took the position that these documents were as valuable to them as the formula for Coca-Cola or the schematics for Intel’s next microprocessor chip.

You can see why Dr. Monk was unable to contain himself when Coslet served up such nonsense with a straight face. But the flip side is that this revisionist history is the new party line in private equity, that the general partners know they don’t have a leg to stand on in trying to continue the pretense that they have a legitimate business need for their secrecy regime. It may be that general partners recognize that the Pennsylvania disclosure recommendations have breached the levee, and there’s no standing against the wave of changes that will follow.2

So if CalPERS can’t even get supposedly supportive experts to back its plan, pray tell how can its board go forward without putting a huge “Sue me” target on their backs? I bet Bill Lerach is quietly hoping they don’t figure that one out.

______

1 As much as we applaud some of what Dr. Monk says, we also have to note that he goes to considerable lengths to cater to the needs of investors that are his prospective clients, unlike academics who focus on private equity like Oxford’s Ludovic Phalippou, or Eileen Appelbaum and Rosemary Batt.

Specifically, Dr. Monk notably sidesteps the real reason for bringing private equity in house. It isn’t that public pensions funds all over America have suddenly become camp followers of Alexandria Ocasio-Cortez and have decided to get out of the billionaire-creation business. No, it is that private equity net returns are falling and investing via private equity funds no longer earning enough on a risk-adjusted basis to justify investing in the strategy. It’s truly disturbing to see Dr. Monk effectively support the public pensions funds’ “absolute return” fallacy, when no intellectually honest finance professional would indulge it. The only way to have private equity deliver adequate net returns is to considerably reduce the fees and costs of private equity investing by doing it in house. And those charges are so ginormous that doing it yourself, even though it will take time to get there, ought to be seen as a no-brainer.

It is also bogus to depict equities of any sort a long-term investments that better fit the long-term liabilities of pension funds. In the hoary days of my childhood, equities were recognized as highly speculative. Bonds were the preferred investments for pension funds because bonds, with their fixed payments of interest and principal, could be laddered to meet the projected liabilities of pension funds.

The reason for higher equity allocations has nada to do with them not having fixed maturities. Equities were added because they have higher returns and provide diversification by asset class, which before risky assets became so highly correlated, also offered some additional downside protection.

Moreover, had Dr. Monk familiarized himself with public markets investing, he would know that one of the reasons academic studies back index investing is that the rebalancing to replicate the index forces selling of winners, as in realization of gains. Similarly, the reason private equity as currently practiced has provided high returns is the discipline of requiring realization of profit. While there are cases where PE funds buy a “growth-y” company and wind up selling it to another private equity fund who is also able to get good returns (meaning the sale from one fund to the second just resulted in paying extra transaction fees, if you look at total returns from owning that company), CalPERS has effectively admitted that this isn’t a widespread phenomenon, and that longer holding periods = lower returns. Why engage in this long-dated fund fad at all if it undermines the whole rationale for private equity, higher returns?

2 Key section from the executive summary:

Well, this should put paid to any pretenses it’s about “returns” or “other asset class” or whatever.

This leaves two possibilities open – incompetence and pigheadedness accompaniying it, or looting. If I was a CA taxpayer, I’d almost go for the other, as that would allow some (small) chance on being able to get the perps in jail. Unfortunately, incompetence of this level is still not criminal.

I’m a layman on these issues, but it sure looks to me like Dr. Monk has left the Board wide open for legal action if they go ahead with this and it turns out (as it surely will) to be a bad investment. Although of course maybe they are hoping they’ll be long gone and retired before this becomes apparent.

CalPERS staff are still, incredibly, asking the Board to put themselves in a completely needless position of being a prisoner in PE’s game of prisoners’ dilemma. If the Board demand more transparency and accountability from PE then they get told their demands cut them off from the supposedly “best” PE deals and funds.

So they have to, apparently, sign up to Frost’s cockamamy twice-removed management structure lest PE, like Miss Muffet being spooked by a troublesome spider threatening to come and sit down beside them, runs away terrorised by anyone lifting the lid on their high-fee low-return (or high risk low liquidity) vehicles.

Fiduciary duty isn’t difficult to understand. As a trust manager in my TBTF’s trust team once said, it’s just a case of being able to ask — and being able to answer — a basic question: “where’s the money gone, where’s it going and why?”

Q: Where’s the money?

A: In CalPERS’ account.

Q: Where’s it going?

A: To PE managers’ accounts.

Q: Why?

A: Because the CalPERS board members aren’t afraid of going to prison…(ol’ Fred could use some company, after all).

I like the cut of Ashby Monk’s jib here and I am glad that Yves put the original thread in this article. He makes his recommendations which are based on his conclusions and his conclusions are grounded solidly in facts. After his first visit, I am sure that he approached attending his second CalPERS meeting with all the caution of Sammy Davis jr. at a Ku Klux Klan meeting. Being blind-sided like he was the first time must have left a bad taste in his mouth and made him wonder what exactly he had gotten himself into.

After losing so many high-profile execs recently with the possibility of a pending employment lawsuit must be making some people at CalPERS nervous. I suppose that CalPERS wants some high profile people and firms to sign off their approval but after all the bad publicity that is starting to stack up, who wants to be the one to throw themselves on this double-set of financial hand grenades in order to make some other people in CalPERS rich?

I can see it now. Frost and some other Board members gather all the people that could sign off their cluster-f*** of a scheme to a meeting. They give their presentations and then starts the question.

Audience: How much will this scheme cost to fully set up and have running.

Frost: I can’t tell you that.

Audience: Who will you have as managers to set up and run these entities?

Frost: I can’t tell you that.

Audience: Will CalPERS have any influence on them, especially in light of the Remington fiasco?

Frost: I can’t tell you that.

Audience: Will returns be higher than if they were instead done inside CalPERS

Frost: I can’t tell you that.

Audience: Aren’t you worried about being fired based on your inability to answer any questions at all?

Frost: No!

Audience: Why?

Frost: I know too much.

Also known as purchasing…

A pig in a poke.

A cat in a bag.

A little pup.

Reminds me of the tax “planning” heyday a few years back, when tax departments started to become profit centers rather than cost centers.

Big sellers of such services, usually accounting and audit firms, would sell a big company CFO a blind bag full of such tricks for a million bucks. (I’m not kidding about the upfront fee.) No looking inside until the check clears, because the ideas were proprietary and ultra-ultra-secret.

Pro-tip for institutional investors (and everyone else): never ever make an investment with a company that takes its name from a literal hell hound.

(can’t believe I even have to say this…what a bunch of noobs).

Monk’s tweets are saying there is a sea change coming. Maybe he once approved of private equity investments. But it will become obvious to everyone that short term investing for high returns is a strange creature. It’s not capitalism anymore, it’s just finance and skimming. What other secret can there be? It’s like a long term business plan for PE – hook a prize like CalPERS into being your insurance policy – your limited partner with unlimited funds. If CalPERS decides to go into the insurance business it should cut out the PE parasite and set up its own insurance corporation for the economic needs of the future but with certain express exceptions like the CalPERS fund cannot ever insure an enterprise that is only a financial scheme for short term profits, aka a scam.

Mr. Meng gets 120 days to evaluate his new digs. Why would the board approve anything prior to the evaluation report?

Many thanks for this persistent, sterling work. Without exaggerations, millions of people might benefit from it if it helps someone (apparently not Ms. Frost) turn around the wreck that is the SS CalPERS not-PE scheme.

Regarding Dr. Monk’s tweetstorm, I wonder if he was concerned that CalPERS would again spin his comments and recommendations to mean the opposite of what he said. To coin a phrase Ms. Frost has apparently never heard, once bitten, twice shy.

An observation that Ms. Frost seems incapable of hearing is that for PE, CalPERS is a cash cow it wants to milk through exhaustion and into the knacker’s yard. Reducing transparency and accountability would be key, hence the not-PE that CalPERS is pushing, a move that should be anathema to any CEO of CalPERS.

Not so with Ms. Frost, who can only hear the PE whispers in her ear, not the drumbeats from outside.

Are some of these people on the board on the take in some way, perhaps kickbacks from PE down the road? What else can explain this behavior?

Yves, yet again my breakfast table is sprayed with coffee.

After reading Dr. Monk’s full tweet-storm I think that you managed, against all odds, to under-state how dripping with sarcasm his words really are! That Frost and her minions have quoted him in their pitch materials is truly rich, as Dr. Monk supports their hare-brained scheme in no way, shape, or form. He appears to have sufficient gumption that he’s making it quite clear that he has no intention of joining them as a defendant when the members and beneficiaries sue the living snot out of the CalPERS Board and staff for breach of fiduciary duty, à-la-Kentucky.

Pigheadedness is the handmaiden of incompetence, as vlade points out. Including video of the quote from Matt Jacobs is particularly rich — I really think that this white-collar criminal defense lawyer may actually be so ignorant of investing that he actually thinks that “privacy” is the distinction between “public” and “private” equity — although I fear that he’s so used to defending quasi-mobsters that maintaining “secrecy” at all costs has become one of his values. “…these are private investments, and they’re private for a reason, which is that the — the financial information needs to be private. And the people running them have these types of preferences.” Please. Go defend Roger Stone. Investing public pension monies in confidence schemes is never, ever, appropriate for a fiduciary.

Instead, Frost and Jacobs appear to have forced-out the one person at CalPERS who actually has experience in running the sort of in-house investment scheme recommended by Dr. Monk. They are the ones who need to be run out of Sacramento, tarred and feathered on a rail.

No one in the previous administration or the current administration has a problem with the way CalPers is run, it’s BAU.

John Chiang’s call for an investigation was pure butt covering, or he would have continued to bring these problems to the public’s attention.

Other than a few columns by Tony Butka and Mike Hiltzik of the LA Times these issues have recieved no coverage in the MSM.

This is BAU in California and when it blows up ( Within a year is my guess) it will be Hoocoodanode?, there will be a fall guy or gal and it will be deja vu all over again.

On my to-do list is read up on what’s happened to CA. I remember as a kid it was held up the world over, certainly news reached my young ears in England, of what a liberal, forward-thinking, enlightened and tolerant place it was. If I recall correctly, CA used its clout as a market for autos to mandate that manufacturers built cleaner emissions vehicles, the gasoline supply chain made widely available the unleaded fuel they needed and if the Big Three carped on about how it was “impossible” to do so, they could just jolly well kiss California’s fat ass.

Now, we have CalPERS and PG&E.

Something must have happened, I’m determined to try to educate myself on what. Probably it’s the bleedin’ obvious to the natives, but in the Rest of The World, we don’t get taught anything about it.

Clive, as the native son of two natives (my grandparents all immigrated here circa 1907), I can tell you that California is the victim of having been founded and sustained by a series of manias — Gold, Railroad Agriculture, Garden-Suburb Real Estate, the Great Depression Diaspora, Post-war Real Estate, Aerospace, Tech, Sub-Prime Real Estate — to enumerate just a few of our recurring infestations of hucksters and gold-diggers looking to make a quick buck.

Every time that the culture seems about to settle, a new rush of carpet-baggers and credulous newcomers arrive on the scene to turn the consensus topsy-turvy. As my friend likes to say, “People around here love to be lied-to.”

ahhh, got it. it’s the Wild West.

Yes, because then she has the position, with no accountability. She can lay off the blame on the Board or the independent fund managers.

And then live happily ever after. She must have a great deal of charisma and intelligence, all apparently directed to her personal goals, with little or no concept of duty. Possibly complete Psychopathy.

No one has mentioned the P/E portfolio companies in which they take an active management role vs companies in which they simply purchase stock and watch from the sidelines.

The opportunity to manipulate a company’s earnings and profitability, upon which a PE firm’s fees are in part based presents many conflicts of interest. Apart from cutting costs by firing employees and eliminating positions, questionable dealings with other portfolio companies may exist.

All to boost fees. Is the actual ROI the actual ROI? Who knows?