Admittedly, most CalPERS board members have been working hard at imitating potted plants. The rare exceptions that attempt to perform their constitutionally-mandated jobs as fiduciaries, like JJ Jelincic and now Margaret Brown, are subjected to CalPERS-orchestrated attacks in the press and petty hazing.

However, in a brazen power grab, the staff is about to have the board sign away its remaining power, even though the board members cannot escape their legal responsibilities by saying, “Oh, those CalPERS people did it. How was I supposed to know?” Yet the board is about to go officially into head in the sand mode despite the fact that it is becoming even more clear that leaving the staff on auto-pilot leads to abuse.

Tony Butka of LA CityWatch has a good piece out on this power grab: COVID-19 or the CalPERS Board – Which is Worse?. We’ll turn to it later in the post.

The latest example is the fiasco of Chief Investment Officer Ben Meng failing to tell the board about his decision to exit two tail risk investments just as they were about to turn spectacularly profitable.

These hedges were intended to reduce the damage of a market downdraft, to the tune of over $1 billion in missed gains. The only reason CalPERS didn’t suffer from even more egg on its face was the manager of the smaller exposure begged CalPERS to delay the wind-down, with the result that CalPERS had a bit of unintended protection through the end of March.

On top of that, Nassim Nicholas Taleb alleges that Meng flagrantly misrepresented the cost and benefits of what Meng claimed were superior and lower cost alternatives to the abandoned hedges. Taleb does not dispute that the two approaches, long dated Treasuries and factor-weighted equity investing, blunted CalPERS losses by $11 billion this year. But Taleb called out Meng for fibbing about the cost, which was sacrificing roughly $30 billion in investment profits last year. That leaves CalPERS net $19 billion worse off than if Meng had left things alone.

In combination with the $1 billion in sacrificed tail risk profits, should we start calling Meng CalPERS’ $20 billion wrong way man?

The issue here isn’t simply that Meng made poor investment calls. Even storied investors make mistakes. It is that Meng looks to have exceeded his authority by firing the tail risk managers without informing the board or even CalPERS’ consultant, Wilshire Associates. He then lied about it to the board, beneficiaries, and California taxpayers when asked a direct question at the March board meeting. Meng then went further in the “cover up is worse than the crime” territory via claiming his supposedly better risk mitigation strategy made even more than the lost in the hedge fiasco. Taleb exposed that as false by showing that all in, it was a big turkey. Taleb is in a position to know that pretty well because CalPERS’ asset allocation major domo left just this month for Universa, the fund with which Taleb is affiliated, so Taleb has a good idea of how CalPERS was implementing its strategies.

So CalPERS has its top investment official defying normal requirements and sound investment practice by ignoring the advice of CalPERS’ expert, Wilshire, and ditching the hedges.1 And this defective decision process blew up with surprising speed. What other risk bombs might be about to go off?

Yet with CalPERS having even more visible management problems than ever, and at the worst possible time, when the world economy is falling off a cliff and recovery could be many years away, the board is about to go into hands off the wheels mode.

We’ll go over the details shortly, but the votes on the board’s abdication are set to take place first in the Investment Committee on Monday, April 20, and then before the full board on Wednesday. You can see how Marcie Frost orchestrated this coup. First she persuaded the board to meet fewer times a year, pushing it further out of the picture. Then she got them to agree to shrink the Investment Committee, knowing that the only board member who is vigilant and reasonably clued in, would be excluded, since the other board members are allergic to asking staff questions. Can’t harsh their mellow!

As Butka put it:

….faced with relatively low return on investments, the institution, has adopted a siege mentality, with the key executive staff manipulating a compliant Board to hide the real inner workings of CalPERS. As well as its problems and failures…

[It] raises questions as to whether the CalPERS Board members are simply toadies to the staff, instead of doing their fiduciary duty to the beneficiaries and taxpayers who fund the institution.

The Staff’s Plan to Get the Board to Resign

So let’s now look at the CalPERS board’s death warrant.

As regular readers know, the CalPERS board has been abandoning any pretense that it supervises staff. It has been handing over more and more power to the staff in the form of increasing its “delegated authority,” as in how much the staff can spend on investments without getting board approval. Committee chairmen also regularly tolerate staff insubordination by not calling staff out when they fail to report back on certain matters.

As JJ Jelinic summed it up,

Only Private Equity and Real Estate have staff delegation limits in their policy.

Other than that there are no limits on staff. However, staff cannot just overturn Board decisions on asset allocation and risk levels. At least until April when the Board will withdraw its limited control.

As Jelincic alludes, the board does have some remaining points of intervention, such as investment manager selection. That has proven to be extremely important. Remember that CalPERS was planning to hand over its entire private equity program to BlackRock, even though that would clearly increase costs with no reason to expect improved performance. The need to discuss this and other parts of the ever shape-shifting “private equity new business model” to the board provided enough transparency for the idea to become bogged down under the weight of its internal conflicts.

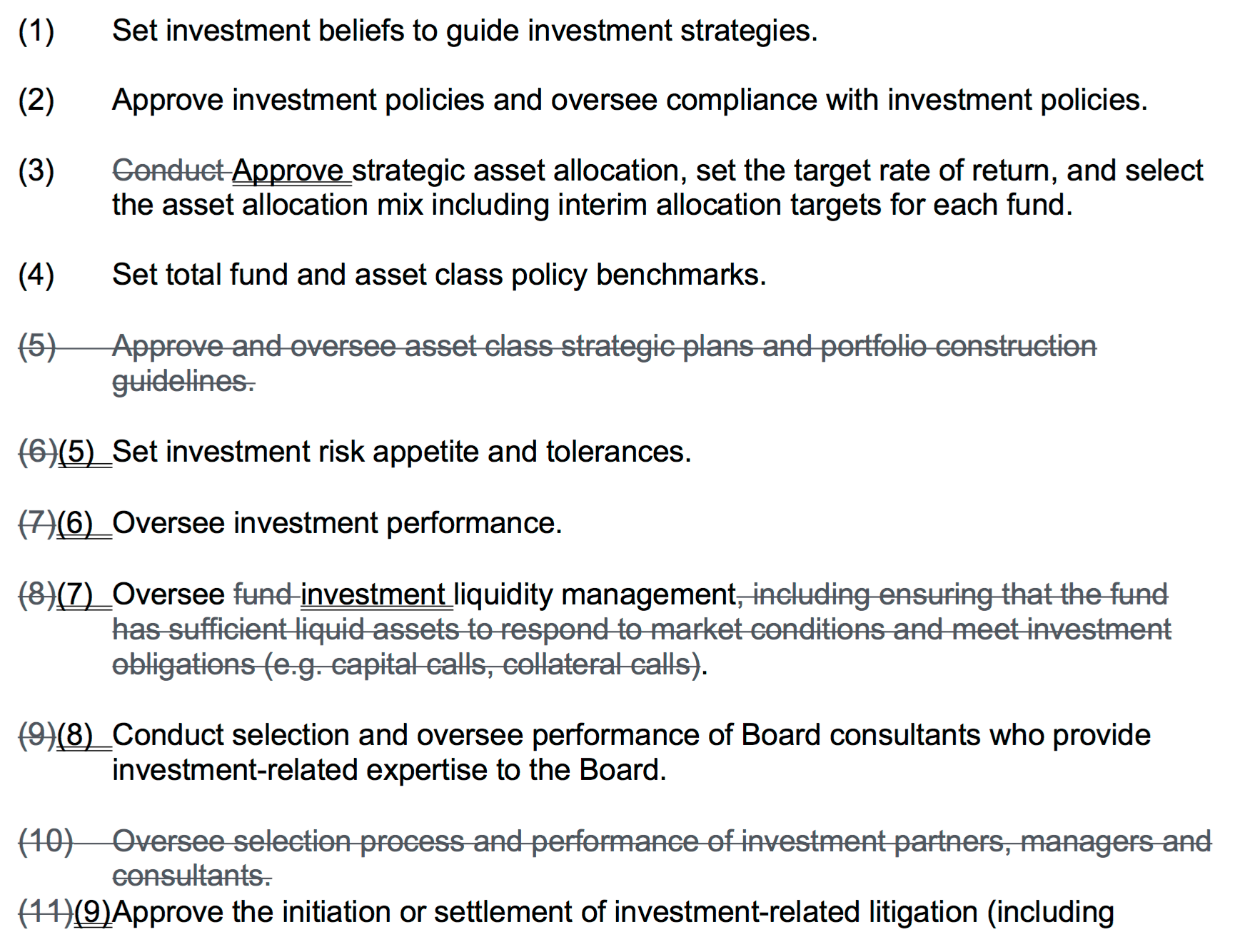

We’ve embedded the key document at the end of this post. This section shows how the Board is giving up virtually all investment supervision and setting itself up simply to hear staff pleasantries and vote in favor of them:

In all seriousness, what is there left for the board to do? It is no longer “conducting” asset allocation but merely waving through what staff wants to do. It no longer have any say over strategies within asset classes. Recall that CalPERS made a costly mistake a few years back in deciding to considerably reduce the number of private equity fund managers and concentrate on fewer and bigger managers. The board won’t have any ability to review or challenge changes like these.

Similarly, giving up the authority to “Oversee selection process and performance of investment partners, managers and consultants” makes clear the Investment Committee is just a big charade.

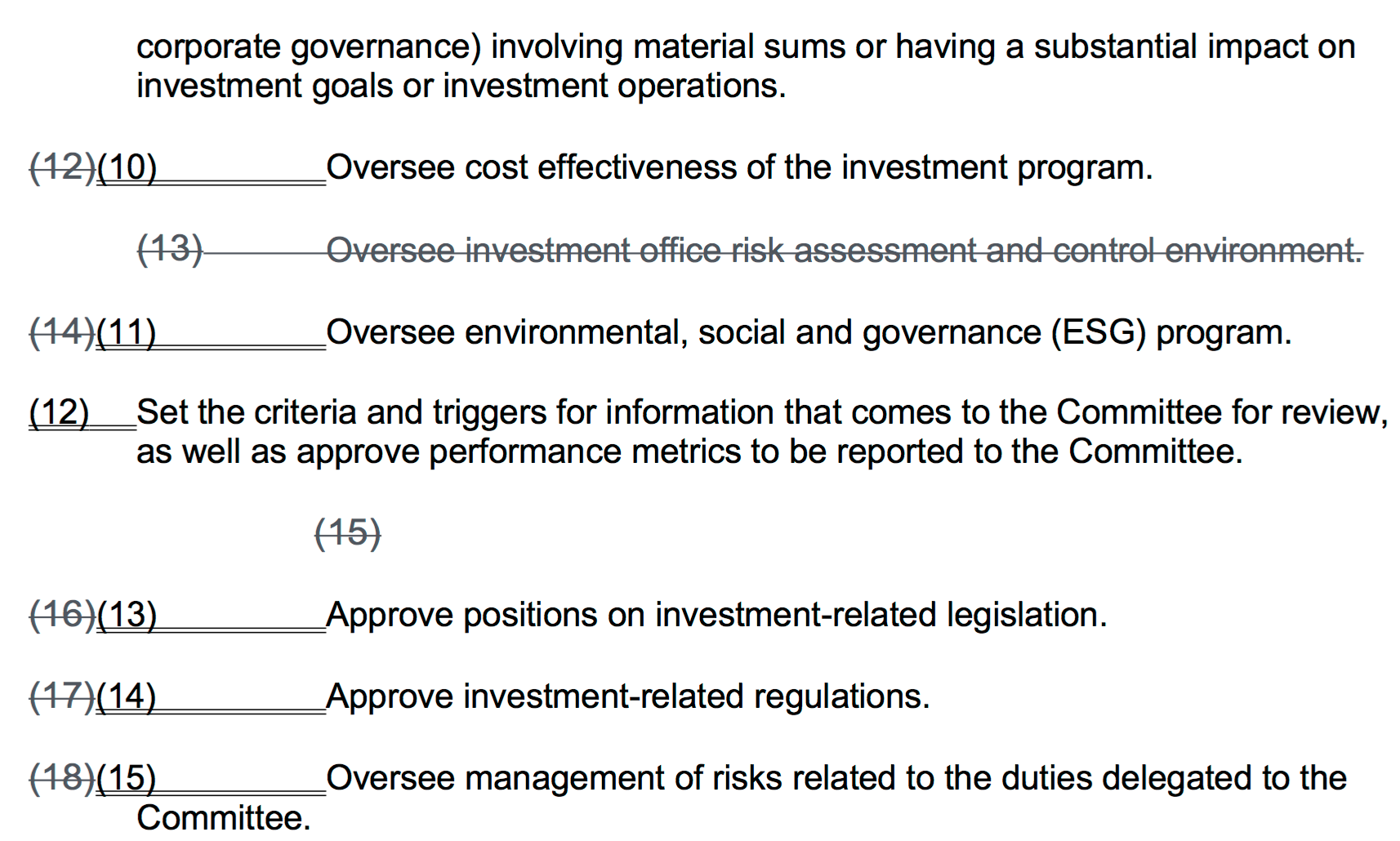

It is alarming to see the board ceding “Oversee investment office risk assessment and control environment.” As we’ve described, CalPERS already has a defective risk management structure, with risk control reporting to the Chief Investment Officer rather than the General Counsel or the CEO. This is the same bad approach that led to the JP Morgan London Whale fiasco. At least risk control now has what organizational management types like to call a dotted line relationship to the board, a limited window in. That is set to go.

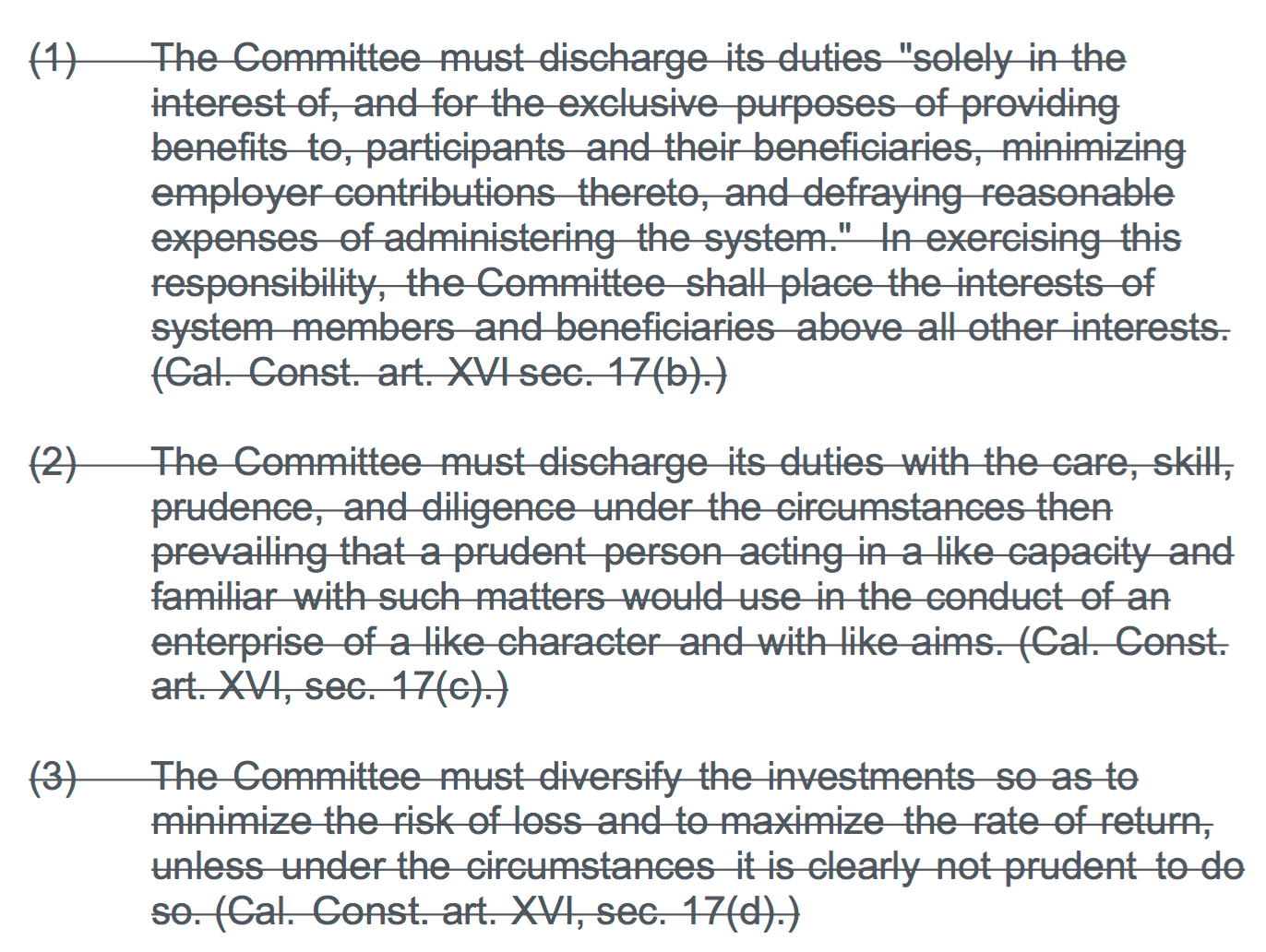

And in keeping with the wrong-headedness of this exercise, the next section, on page 3 of the embed below, strikes out all of the requirements from the California Constitution. The CalPERS board in theory cannot abandon these obligations, but putting them next to the board’s clear abandonment of its role evidently makes the contradiction too obvious:

And don’t kid yourself that the board can also delegate its duties to staff. Those responsibilities are always and ever the board’s. Per Article 16 sec. 17(a) of the California Constitution (emphasis ours):

The retirement board of a public pension or retirement system shall have the sole and exclusive fiduciary responsibility over the assets of the public pension or retirement system.

As former prosecutor, now prominent retiree David in Santa Cruz warned:

This means that when the members eventually see their contributions increased and the beneficiaries eventually have their benefits cut, and are looking for someone to sue, it is the individual board members who will be sued personally. Then Jones will also discover that the E&O “self-insurance” that the CalPERS CAFR reveals is not reserved — as required by both state and common law — provides as much coverage as the Emperor’s New Clothes.

It’s always a bad idea for a fiduciary to involve him or herself in a cover-up. It’s doubtful that a future governor or legislature tasked with bailing-out the fund will be much interested in bailing-out the current board from personal bankruptcy when they so blatantly ignore their duty to hold managers accountable.

CalPERS Elected Board Members Thumb Noses at Public by Taking Time Off Via Shedding Duties While Lying to Employers and the Public

The fact that the Investment Committee, far and away the most important and time-consuming activity of the board, is meeting less often, dumped some members and is about to dump pretty much everything it once did, begs the question as to why board members (for the ones that are current government employees) are being compensated in the form of undeserved paid vacations at CalPERS’ expense.

Six of the 13 board members are elected by beneficiaries. One seat is for a retiree. Of the rest, at least three and potentially all five of the rest are held by active employees.

These employees get “release time” from their employers to (supposedly) work on the board (it’s formally called employer reimbursement). The theory is that the board member works for CalPERS X% of the time and CalPERS reimburses them for that.

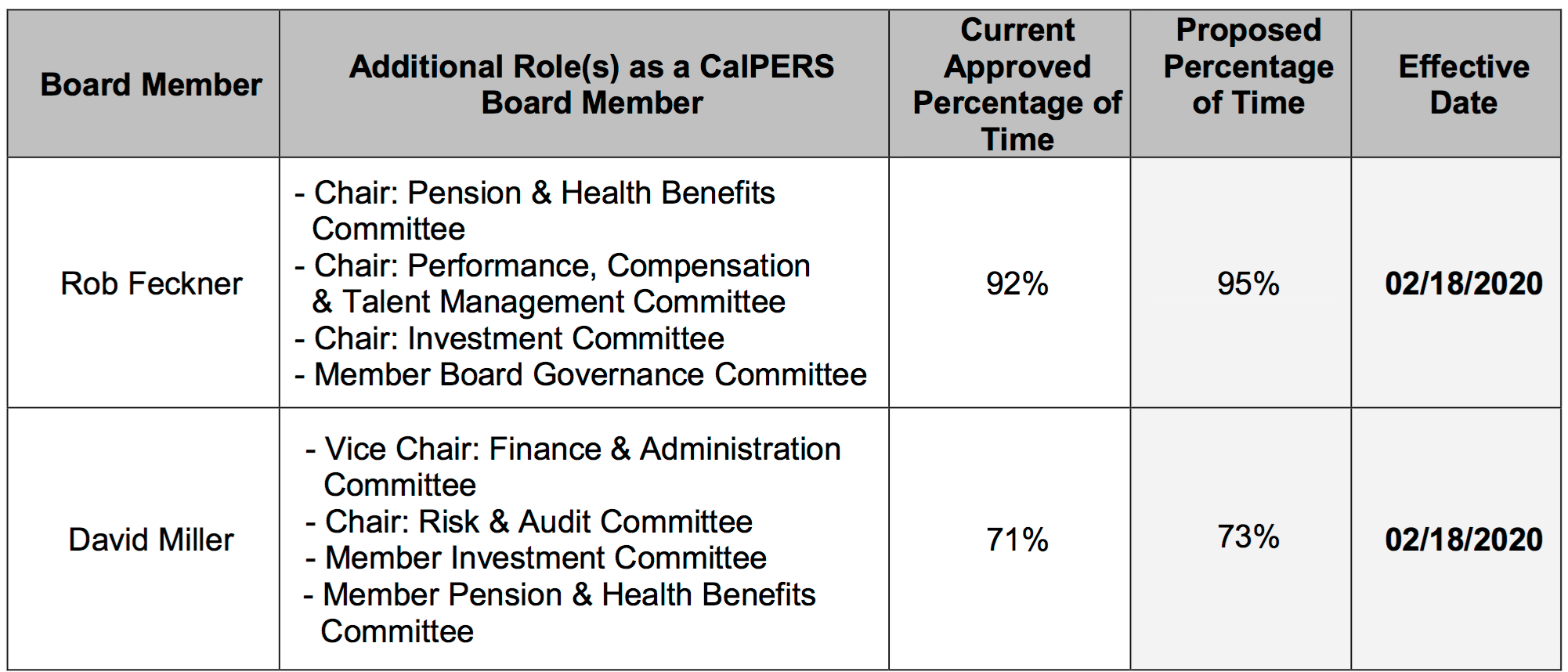

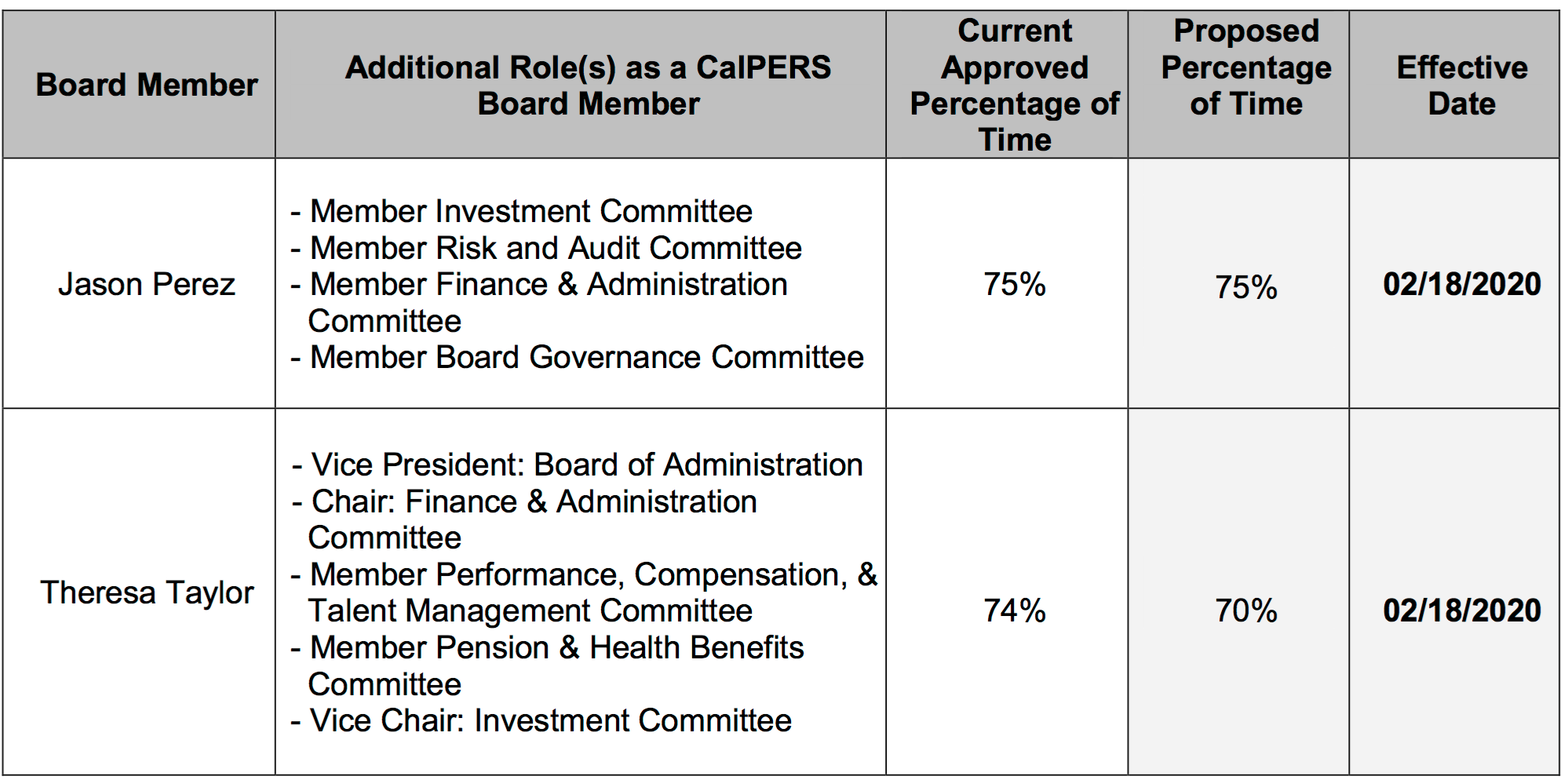

In a show of utter disrespect to the public, the requests for release time authorization are also scheduled for the board meetings next week. Yet most board members are asking for the same or increased “release time” despite the fact that they are clearly doing vastly less than they used to. Specifically:

All are vastly in excess of actual board meeting time. The “release time” presupposes that board members are carefully reviewing all the materials the staff sends prior to board meetings. From the caliber of discussions, it is evident never happens save for the board members that staff treats as dissidents and has successfully gotten the rest of the board to treat as pariahs). At Butka noted:

Just go look at the video recording of any meeting and look for any questioning of staff by Board members on anything. Good luck finding any fiduciary oversight. More like a bunch of crash test dummies.

In addition, the ability of the board to do anything between board meetings is severely circumscribed by the Bagley-Keene Open Meeting Act, which is designed to bar deliberations outside of formal meetings with stipulated notices and disclosures.

On top of that, the reality is for any desk job, it is hard for employers to make use of the remaining <30% or less time (recall that ~10% is vacation, so the remaining work time is <20% of total man days/year). So in many cases, employers don’t ask the CalPERS board member to take on meaningful work the balance of their time (this was clearly the case for long-standing board member Priya Mathur).

So it is no accident that Rob Feckner asks for far more release time than anyone else (95%). He is a glazier, meaning he fixes broken windows. That’s one of the few things an employer could readily arrange to be done on an ad hoc basis for a few days total every month.

Notice that staff provides cover for these ludicrous number in the form of “baselines” that are out of date by showing 12 months of board meetings when the board went to 10 several years ago and has now cut that further.

The matter of release time may seem trivial compared to the utter abdication of duty. But it’s the sort of thing that sticks in the craw of the beneficiaries who vote for candidates for these seats, and even more so to employers, who resent how increases in CalPERS contributions were breaking their budgets even before the coronavirus came also to crush their revenues.

There is a tiny silver lining to the coronacrisis. CalPERS will, for the first time, read e-mailed public comments into the record during the board meeting. They to be limited to roughly three minutes of speaking time.

Please, if you are a CalPERS beneficiary or a California resident, give CalPERS a piece of your mind! State that you firmly oppose the reduction of board investment oversight as a rejection of its fiduciary duty.

The more voices speak out, the better the odds of beating back these abuses. We have the rare luck of the wind of deserved bad press at our backs. From CalPERS:

Public Comment

Individuals present at the CalPERS auditorium may provide public comment on agenda items at the time each item is heard. Members of the public may also submit written public comments by email to board@calpers.ca.gov. Written public comments should note the meeting and agenda item the comments relate to and shall be read into the record at the time the corresponding agenda item is heard. All public comments shall be subject to CalPERS Pusblic Comment Regulation (Cal. Code Regs. tit. 2, § 552.1.)

https://www.calpers.ca.gov/docs/board-agendas/202004/board-notice.pdf

Be sure to check the board vote on April 20, because you have two shots at defeating these changes. Even if they are approved at the Investment Committee on April 20, they still need to be approved by the full board on April 22. So you may need to submit a second round of critical comments and perhaps enlist even more friends and colleagues to join you.

Give them a piece of your mind! And please circulate this post widely and ask everyone you know to do the same!

____

1 It may seem I am making overmuch of this point, but the key to avoiding liability as a board or executive is acting in accordance with expert advice, and papering your files very well as to why if you choose to ignore it. Meng is violating bedrock practices in blowing off Wilshire’s recommendation.

As we can see from the his talk in this post, Meng did not have independent expert advice that diverged with Wilshire’s view based on looking at the performance of the two funds and how they managed their hedges. Instead, all he could muster were two articles, neither specific to these managers, and one not rising to the level of being academic work.

00 CalPERS Board Suicide Pact

Sweet, it reminds me of my favorite Richard Nixon quote “I accept the responsibility, but not the blame”.

If I were a board member and this passed I would resign immediately, there’s something about having no authority to make any decisions while retaining all of the legal liability as a fiduciary that I would not be comfortable with.

On the positive side, we can be sure that Attorney General Becerra will be all over this!

“In all seriousness, what is there left for the board to do? ”

The prior talking relationship with BlackRock is interesting considering BlackRock is going to manage the $2-6T bailout. Which makes me speculate the govt has just become some sort of giant hedge fund that CalPERS staff hopes to profit from…. What else can they be thinking? That wouldn’t be sound business practice in the normal capitalism sense. ( PE isn’t sound business practice in the normal capitalism sense. Making money by destroying businesses is … something else than normal capitalism. imo. But now it looks like PE and its offshoots have captured the govt and the FED distributions. ) This comment is waay out there, I know. CalPERS staff is waay out there, too.

Board, what board? Ah, you mean the CalPERs DARTBoard, that Marcie has in her office and invites the staff to throw whatever comes handy at as a stress reduction strategy? Good HR move.

As part of their discussion about reducing the number of board meetings, Rob Feckner, the board president, said at one point on the record that board members could use the freed-up time to act as “CalPERS ambassadors.” Somehow, I don’t see that role listed in the California constitution as one of the components of fiduciary duty. But it is fun! Go to conferences at the Ritz Carlton in Half Moon Bay, play some golf while there. Go to conferences at the Pebble Beach Resort, play some golf while there. Being an ambassador is hard work!

I confess extreme ignorance of this entire subject. Does the state government have no role here? Yves has been writing about this for years and nothing seems to happen except perhaps it becomes worse. Second question: Who benefits from this on-going state of affairs?

When the history books are written NC’s reporting will be an important source for understanding just wth happened. imo..

Thanks for asking. CalPERS is exceptionally well bunkered, which is why it is such a governance mess.

The short and a bit oversimplified version is Governor Pete Wilson tried messing with CalPERS benefits in the early 1990s. The legislature slapped him down and removed any state control over CalPERS. It’s accountable only to the board.

Now the legislature could conceivably change that, so that is why the only thing CalPERS is afraid of is the legislature. We have been pushing for an independent Inspector General.

John’s question was “Who benefits?”

What are your thoughts about this?

“Wrong Way Meng.”

That might stick. Not that I personally would ever sink to such pettiness.

One phrase for this: Litigation Futures

Follow the money…

Yves has been hammering away at CALPERS for many years to little avail. This pension fund has become the standard of all Ponzi pension schemes which quite soon now will have to be bailed out by the USG, just like those similar schemes in too many other states like Illinois, Ct, NY, et al. The only thing that the bailouts will accomplish is that, in a few short years, the typical annual pension received might, just might be enough to buy a loaf of bread. All, of course thanks to the Marxist ideology that claimed that deficits don’t matter and made a religion of MMT.

logy

I hope you can get that knee seen to.

While you are at it, you might also get some pills for your memory.

Among the things we’ve gotten done at CalPERS:

I’m sure I’ve forgotten a few.

And Making Shit up is a violation of our written site Policies. MMT academics are not Marxists. And they don’t say deficits don’t matter: they are very clear that there is a real resources/inflation constraint.

And it’s the mainstream economists who are acting like cult members. They pillory MMT proponents as apostates.

It was Dick Cheney who famously said deficits don’t matter and we all know how that turned out in the budget fights. Funny how only a rare few “fiscal conservatives” are making even the slightest whispers (Rand Paul’s stagecraft smarm excluded) about how the present and future waves of Covid bailout funds will be paid for.

On the MMT side of things, will there be a reply to Taibbi’s response to your critique of how it could be perceived that he was describing the current bailout’s relationship to a heavily skewed MMT?

Thanks for asking. Yes, Richard Vague and John Siman are working on it. It is taking longer than I would like but Vague is deliberate.

Thanks, Yves, for the summary and your efforts. I’ve vaguely followed the CalPERS debacles over the years. Astounded at the brazenness.

Does anyone have a sense of who are the key CalPERS employees driving this proposed shift in control from the Board to staff? To what extent is Meng the lead driver (since he has always pushed for more control)?

Also, with 40+ employees in “public affairs” who spend many millions of CA taxpayer dollars annually on legal and public affairs companies to advance CalPERS’s image and pursuits, and with a compliant Board, CalPERS execs and Board together have always been able to control the narrative. But with Margaret on the Board and with Yves truth telling, perhaps some reform is possible . . .

Last I checked, it was 72 people in “Communications and Stakeholder Relations” or whatever it is called.

Marcie Frost and General Counsel Matt Jacobs look to be driving this train.

Looks like the CalpERS story is even getting press in the Wall Street Journal-

https://www.wsj.com/articles/calpers-unwound-hedges-just-before-marchs-epic-stock-selloff-11587211200

A Dec 11, 2019 Wall Street Journal article by Heather Gillers and Dawm Lim states that Meng directed a change in a CalPERS internal equity index fund so that CalPERS would buy shares in nearly 100 additional Chinese companies. A passage of the text from the article is pasted verbatim below.

[Calpers CEO Marcie Frost praised Mr. Meng for taking “a hard look at the portfolio.”

“He’s doing exactly what he was hired to do,” she said.

He has been re-examining everything from how the pension benchmarks returns to how it should borrow against pension assets to clear the way for market wagers. He told board members in May that risk was more complex than many investors thought. Building on a review already under way, Calpers revamped the algorithm dictating what goes into its stock index portfolio, which holds $130 billion. This resulted in the removal of 143 stocks, including prison stocks that Calpers had drawn heat for and the addition of 198, nearly half of them Chinese companies.]

https://www.wsj.com/articles/nothing-is-sacred-for-new-leader-of-nations-largest-pension-fund

Long time reader, first time commenter. I emailed the Board. Thank you for continuing to investigate CalPers.

I very much appreciate it! Be sure also to send the same e-mail you sent to the board to the Public Comments link in the post, if you have not already done so, so it will be read into the record of Monday’s board meeting.