Yves here. Our one-time frequent writer Richard Smith, who has devoted a great deal of energy over the years to pursuing international fraudsters, has been getting more and more notice as an expert on some of the tools they use. It may seem rhetorical to question whether the UK will continue to be a major money laundering hub. Nicholas Shaxson, in his classic Treasure Island, described how the US and UK had long been competing for leadership in “offshore,” as in operating financial secrecy jurisdictions. On top of that, some Brexiteers have championed the UK becoming “Singapore on Thames” which in their vision, includes even more financial buccaneering. E-monay looks like a new addition to an old toolkit.

Some readers will notice the way the article muddies the Baltic nations with Russia. That is peculiar give that there is considerable tension between these countries and Russia. For instance, in 2018, the US deployed soldiers and tanks to Latvia in a show of force. I would assume this broad brush is the result of openDemocracy editing. But some of this is also due to the analogy to the 2014 “Russian laundromat” which moved illicit funds out of some former Warsaw Pact countries.

By David Leask, a freelance journalist and Richard Smith, a researcher documenting shell company abuse. Past collaborations, credited and uncredited, with Australian Broadcasting Corporation, British Broadcasting Corporation, Canadian Broadcasting Corporation, Al-Jazeera, interest.co.nz, Glasgow Herald; blog posts at www.nakedcapitalism.com. Originally published at openDemocracy

A survey in April found four out of five Britons – many forced to do all their shopping online – were considering new digital ways to pay.

Some are turning to ‘e-money’, with a raft of new money-handling products aiming to challenge industry leader PayPal.

From a health point of view, this is safer than handling cash and visiting shops. But, anti-corruption researchers warn, the boom in e-money poses another risk: money-laundering.

There are already concerns that regulators, including British ones, failed to keep close tabs on German payments giant Wirecard, which went bust two weeks ago.

The UK’s watchdog, the Financial Conduct Authority (FCA), for a few days even froze some £500 million in customer money at the firm’s British subsidiary, while it made sure the money actually existed.

Now an investigation by openDemocracy reveals UK-regulated electronic money institutions, or EMIs, are being touted as a replacement for networks through which billions of dollars of dark money moved in and out of the former Soviet Union.

Our research follows individuals and institutions who were linked with Baltic banks that were fined for enabling – or failing to prevent – industrial-scale money-laundering. We’ve found that some are moving into the British e-money business, complete with a stamp of approval from the FCA.

And we have found an open Russian-language internet trade in UK shell companies with EMI accounts, EMI licences and even an anonymous EMI provider on offer for £1 million.

Anti-corruption group Transparency International believes the sector poses an emerging threat in the battle to stop criminals from cleaning or moving their dirty money.

The Next Russian Laundromat?

For years corrupt officials, criminals and tax-avoiding entrepreneurs used anonymously held ‘shell’ companies (often registered in the UK or its territories) to open bank accounts in the Baltic states.

This relatively simple scheme enabled some of the biggest laundering schemes ever exposed, such as the multi-billion-dollar ‘Russian laundromat’, revealed in 2014, and similar pipelines for dark or dirty money out of Azerbaijan and Ukraine.

The huge flow of money through this machinery is thought to have reduced to a trickle since a 2018 crackdown in Latvia on banking for people who do not live in the country.

But now an alternative route has been suggested: EMIs, including those registered and regulated in the UK.

There is a cottage industry advising people and business in the former Soviet Union about offshore structures. It is pretty frank about this shift to British EMIs.

Back in 2018 the Russian-language site Zapiski ob Ofshorakh (‘Notes on “offshores”’) set out the pros of various EMIs, including UK-regulated ones. And its explanation for why it was doing so could not be blunter.

It said: “In connection with the mass closures of non-resident bank accounts in Baltic states – and the growing difficulty in working with foreign banks – some entrepreneurs are looking to open corporate accounts in payment systems.”

The message: it is now harder to move money – including dirty or untaxed money – through shell firms and Baltic banks, so try EMIs instead.

The site sells shell companies, including the now-notorious Scottish limited partnerships or SLPs, dubbed Britain’s “home-grown secrecy vehicles” by Transparency International.

One of the site’s specialists even boasts in a recent video how clients can set up an SLP and then have a credit card issued by an EMI sent to the firm’s proxy address in Scotland and from there on to Russia or Ukraine.

Moreover, other sites offering offshore services to a largely Russian-speaking market are going further.

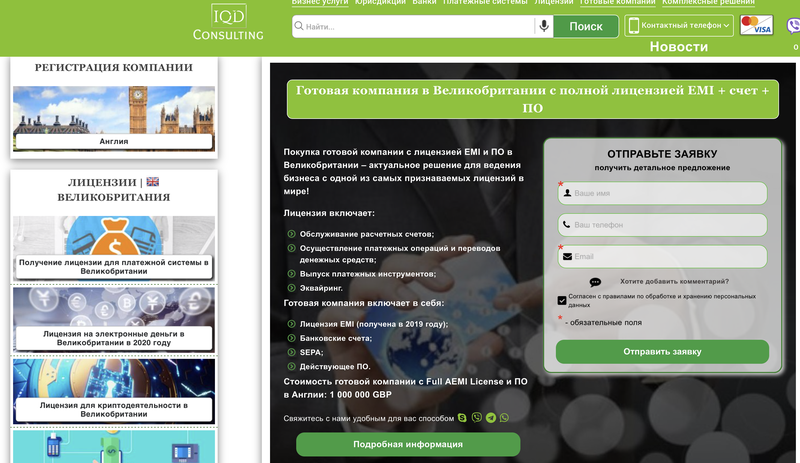

IQD Consulting has been offering to sell an unnamed British company complete with an e-money licence. The price tag? £1 million.

The vendor also markets British and international shell companies, including Scottish limited partnerships, complete with accounts at British banks or EMIs.

IQD did not respond to a request from openDemocracy for comment. It did, however, remove its English-language offer for the e-money company after we got in touch.

The website is owned by a limited partnership called Lacerna registered in Dublin. Irish limited partnerships do not need to declare a beneficiary so there is no way of knowing who owns or operates the site.

The Latvian Connection

They were the bankers who helped North Korea develop ballistic missiles: three financial institutions in Latvia were fined after an FBI probe exposed their lax controls had let the world’s most secretive state get around sanctions.

Now people who owned or worked for those banks are getting what – to outsiders at least – looks like an endorsement from the British state, a kind of financial kitemark: registration from the FCA as EMIs.

Latvian banking, specifically non-resident banking, was widely seen as a breach in international defences against money laundering. It suffered scandal after scandal until Latvia, under pressure from the EU and US, moved to stop its banks giving accounts to anonymously owned shell companies or dummy corporations, not least from the UK and its overseas possessions.

The great crackdown on Baltic non-resident banking in 2017-18 coincided with a gradual migration of some of its institutions and personalities to the UK’s e-money industry.

One Latvian bank, Rietumu Banka, already has links to the British Isles. One of its three owners is Dermot Desmond, a leading shareholder of Scottish football champions, Celtic.

The bank has been fined by Latvian regulators for failures in money-laundering controls. It is also currently appealing against a criminal conviction – and penalty of €80 million – from a French court for enabling mass tax evasion.

Now its shareholders own a British EMI, Decta, and Rietumu banka provides clearing services for it and five more.

Decta told openDemocracy that it “acts in strict accordance with the requirements of FCA”.

It added: “We regularly pass anti-money-laundering (AML), Anti-Fraud, Know Your Customer and Combating the Financing of Terrorism audits held by Visa, Mastercard and big-four auditors, proving Decta to be complying with all latest AML standards.”

Another Latvian bank repeatedly fined for money-laundering failures was Baltikums, now called BlueOrange. It was one of three Latvian institutions punished by regulators after its accounts were used to breach EU and US sanctions against North Korea. It was one of the banks used to process payments under the multi-billion-dollar Russian and Azerbaijani laundromats, according to investigations carried out by the Organised Crime and Corruption Reporting Project and its partners.

The chairman and co-owner of BlueOrange, Alexander Peshkov, is listed in British corporate filings as the person of significant control of Bilderlings Pay, a British EMI licensed by the FCA. Offshore business advice website Zapiski ob Ofshorakh, among others, recommends Bilderlings Pay as an alternative to a Baltic bank account.

Bilderlings did not respond to a request for comment. Last year accounting giant BDO announced it had reviewed the e-money provider’s anti-money-laundering procedures. BlueOrange has said it has improved such controls since 2017.

Other veterans of the Baltic non-resident banking system are also setting up British e-money firms or working for them.

British-educated Latvian Artjoms Dozorcevs, who used to work at Rietumu, set up British EMI AltPay in 2018. He hired another Latvian banker, Andris Ovsjaņņikovs, as head of his client relationship department. Ovsjaņņikovs had previously worked for ABLV, a bank stripped of its licence in 2018 after the US Treasury found that it had “institutionalized money laundering as a pillar of the bank’s business practices”. Early this year Ovsjaņņikovs was arrested as part of a €50 million laundering investigation into ABLV.

Dozorcevs believes the risk of cross-contamination of bad anti-money-laundering practices from Latvian banks to British EMIs is “minimal”.

In an email to openDemocracy, he described Ovsjaņņikovs’ arrest as a “devastating turn of events”.

He added: “As soon as I heard the news our business relationship was terminated indefinitely.

“He has now been released with charges dropped but we do not plan to renew our cooperation.”

Dozorcevs said his small EMI avoided the hurdles of traditional banking but did not compromise on anti-money-laundering checks.

Several British EMIs have appointed people who were responsible for anti-money-laundering work at Latvian banks to do the same or similar jobs.

Take Paystree. This EMI has Evija Meimane as a director. She has worked for no fewer than four of the Latvian banks fined over money-laundering, including a spell lasting from 2010 to 2014 in charge of monitoring customer payments at Trasta Komercbanka. This bank is currently challenging the 2016 revocation of its licence over alleged failure to prevent the laundering of up to $13 billion by its customers, between 2010 and 2014: the notorious ‘Russian laundromat’. Paystree did not respond to requests for comment.

Global Star Finance, another EMI, has a director and head of anti-money-laundering who held compliance posts at four banks fined for lax money-laundering controls. The official, Ingreta Jansone, told openDemocracy the EMI was “not doing active business at the moment, and wouldn’t want to comment”.

British EMI Dzing this spring appointed Iveta Kerpe as its chief financial officer after a career in Latvian banking, including jobs at two banks sanctioned for not controlling money-laundering carefully enough. In the aftermath of a banking fraud in Moldova, in which $1 billion was spirited away to accounts at ABLV and PrivatBank Latvia, Kerpe was fined and ordered to stand down from her board position at the Latvian branch of Ukraine’s controversial PrivatBank. PrivatBank was one of the three institutions fined after the North Korea probe.

A spokesman for Dzing said the business – which aims to facilitate small cash transfers between family members – was not yet in operation.

He said compliance was one of the largest teams in the firm and added: “We do not provide banking for companies – our current proposition at the moment is for retail customers only. We are regulated by [the] FCA and intend to comply with all aspects of UK and EU financial regulation, including anti-money laundering procedures.”

Policing Electronic Money

The UK’s watchdog, the FCA, has previously ranked the laundering threat from e-money as “medium”. Transparency campaigners and opposition politicians have long accused Britain and its regulator of taking a light-touch approach to financial markets. However, the UK’s image as a state with rule of law and a reputation for fair play is also a vital part of the marketing of EMIs aimed squarely at the former Soviet Union.

The FCA licenses EMIs – who have to show that their executives and owners are respectable – and can shut down those which break rules. A licence is not an endorsement, but it can be marketed that way.

The regulator does act against EMIs. This February ePayments Services Limited – which uses Rietumu Banka for clearing – suspended its accounts, around one million in total.

The company, in a statement on its website, said: “This decision was taken following a review, by the FCA, of ePayments’ anti-money-laundering systems and controls, which identified weakness that required remediation.”

Industry sources have suggested it was over-exposed to online businesses with a high risk of claims for the return of payments, such as online porn and gambling.

The business, which says it has no overall controller, offers services in English and Russian.

Last year the FCA forced the UK subsidiary of another e-money provider, Allied Wallet, into liquidation after the firm’s parent settled US charges that it had helped clients defraud consumers of $110 million in scams and pyramid schemes and illegal debt collections. Allied Wallet, which never admitted or denied the claims, was accused of helping to buy British shell companies for its clients.

The firm’s chief executive, Andy Khawaja, was last year charged in the US with alleged involvement in illegal campaign contributions to Hillary Clinton’s 2016 presidential campaign as part of an influence-peddling scheme. Khawaja, a Lebanese-American who also made a donation to Donald Trump’s inauguration, was essentially accused of providing proxies, so-called “straw” donors, to make campaign contributions on behalf of those who wished to hide dark money flowing into US politics.

He was charged alongside another Lebanese-American, George Nader, an informal diplomat with ties to the Abu Dhabi royal family who advised the Trump administration and later was a witness in Robert Mueller’s Trump-Russia investigation. Last month he was convicted in the US on child sex charges.

The FCA said it could not comment on individual cases or companies highlighted by openDemocracy. However, in a statement, it said: “We expect payment firms, including e-money institutions, to meet their regulatory responsibilities and it will act swiftly where firms fail to meet requirements.

“Financial crime continues to be an area of supervisory focus to ensure that payments firms have appropriate systems and controls in place to minimise the incidence of accounts being used for fraud, money laundering or other financial crime.”

Under FCA rules anyone running an EMI has to be a ‘fit and proper person” and that directors and managers should be of good repute and have the necessary know-how.

This, it is understood, would apply to anybody who bought an EMI-licensed company off the shelf.

Offshoring the UK

COVID does appear to be driving traffic to e-money and other cashless and digital payment systems. One Irish e-money provider has said its turnover has doubled under the lockdown.

However, some in the e-money industry are looking at what they see as another opportunity to grow: Brexit.

Late last year, the founder of e-money firm 3S Money Club – which styles itself as an “online-bank” and uses Rietumu for clearing – set out his vision for a freewheeling UK free of Brussels red tape.

According to a Russian-language report on Rambler News, Ivan Zhiznevskiy said the UK would have greater “ofshornost” (‘offshore-ness’) after it left the EU. He said: “We have been waiting impatiently for Brexit all year because – and this is good news – this island will probably become more ‘offshore’.”

And excellent expose of how not only is there no shortage of people with illicit funds they need to wash whiter, but there’s no shortage of Big Finance (or even small or medium sized finance) willing to cater to their needs.

There’s nothing to be added to the comprehensive description of the nitty-gritty of how these various schemes and products provided under them are set up and run. One point I can add is from the business side of finance. What’s been forgotten (or not really dug into — you’ll be shocked, just shocked at that) is how in the backdraft of the Global Financial Crisis, a lot of the industry — faced with huge losses to make up and not (for a short period of time) aware that TARP and the other government bailouts (including ZIRP and Extend and Pretend, mortgage services abuses… etc. etc. I could go on, that’s not a complete list but you get the picture) would come to their rescue considered how “tax services”, “investment efficiency advice” and similar sounding offers that could be sold to high or ultra high net worth customers might be a good source of fee income,

The regulators (mostly) clamped down on that, but in the event it wasn’t really needed because the industry got a bailout. But structural problems remain — a lot of finance simply isn’t profitable or barely profitable in a low yield environment. This explains why old, bad ideas (like money transmission products which, gosh, would you look at that, who’d have thought it, end up concealing sources of funds) that have side-benefits that are not necessarily particularly wholesome but nevertheless are potentially hugely profitable as the article describes are getting resurrected.

Probably the piece was written pre Wirecard — Wirecard will make an great source of additional material on this never-too-far-from-the-surface seedy side of the financial services industry when all the skeletons are finally exhumed from that.

I don’t know if this is a tall order but I am asking whether the possibilities raised here about new e-money and payment systems seeking to profit from brexit cold be seen by Barnier and Brussels as a possible source of problems if UK financial services firms reach compliance agreements in a country-by-country basis with EU countries.

An exceptionally important point. And often overlooked in the backdrop of bigger players (like the EU) which make more noise.

Even when governments try (and they don’t always try especially hard), good financial services regulation is a big ask. It is a specialist skillset. Like any specialism (as you’ll no doubt know!) you have to really “do” it to “know” it. You can learn theories, you can get consultants to give you briefings, you can read journals and you can ask colleagues for their expertise. But in order to know what really happens in finance — especially how it not only intentionally or inadvertently pulls the wool over the eyes of the regulatory authorities but how it can also end up misleading the firms’ own managements — you really have to have been there, done that and bought the t-shirt.

So, regulators have to recruit from finance to a degree to at least get a foundation in their pool of employees who know how it all works “on the inside”. But they can’t usually match salaries (except at the top, but it’s not general vanilla institutional management which is needed, it’s mid-level employees with subject matter expertise), the culture is different and the politics of these sorts of agencies can be pretty chronic. They also need good legal skills, people who can work their way around contracts and procedures, people who can sift information and analyse it and so on. But there’s a tendency to outsource legal and other specialisms, because, being government agencies, it’s just easier to buy in skills (or think you can) rather than develop them over a long period of time in-house. So there’s — as always with outside suppliers — a lot of chopping and changing.

It’s hard enough to get regulation done right in the best of circumstances. As today’s other important piece https://www.nakedcapitalism.com/2020/07/ny-department-of-financial-services-fines-deutsche-bank-over-jeffrey-epstein-abuses-where-are-the-feds.html shows, the NY Department of Financial Services is a stand-out example of how to try to. It is stand out, because as Yves noted, so few regulators really make the sorts of efforts they need to make to be successful.

Bad (or, maybe more correctly stated) “mediocre” though the UK’s regulatory authorities are in financial services, they are probably more sophisticated than those in a lot of the EU27 countries. If nothing else, they have scale. They have scale because the City of London is so vast when it comes to financial services. If a regulatory issue arises, they’ve probably seen it before. They have, at least, been doing this a long time. Plus there’s been more scandals than I’ve had slices of cake, so they know that ignorance, or misplaced trust, isn’t going to be forgiven.

Barnier is many things, but a fool isn’t one of them. And he’ll know all-too-well the risk that EU27 regulators may well not be up to the job they’re about to get landed with. He also knows that (and here is my one and only feeling sorry for the Commission that I’ll do this year) the Commission is in a bind. It lacks the competencies to fully regulate everything in financial services in the EU (it’s a bit of a patchwork between the Commission, the ECB and the national regulatory bodies spread across Member States). He also knows that, if it all gets messed up, everyone will look for someone to blame and the Commission will probably, rightly or wrongly, be in the firing line. Yet, Barnier has little sway with the national regulatory authorities. He can’t exceed his competencies. All he can do is fire off enforcement notices (which may well get ignored — and can only be within the scope of the EU’s Directives) and hope the national agencies take note and Do Something.

Even then, even if the Member States realise they need to up their game and the skillsets, actually getting those skills isn’t as I noted above especially easy. It takes time. It takes effort. Often, the only thing which motivates is failure.

Thanks a lot Clive. My foggy intuitions were going in line with your explanations but your answer makes them clearer. In Spain, I guess, the institutions implied would probably have to resort to outsourcing and the results could be messy if the consultants do not align 100% with the… let’s call it general interest.

The City has got its reputation to think of.

The place to come to, to do all that dodgy stuff you can’t do elsewhere.

Except, perhaps, Danske and Deutsche Bank, paragons of the European banking establishment https://www.msn.com/en-us/money/companies/danske-deutsche-bank-ignored-estonia-risks-in-lucrative-setup/ar-BB16ulYz (yes, not only prim and proper Germany but also those stout, sturdy stolidly responsible Danes, too! … and this is apparently the biggest money laundering scandal in European history).

You do raise a fascinating cultural aspect to all this. Anglo-Saxon capital (the US and the UK, mostly) is widely and rightly reviled for its encouragement and tolerance of gung-ho shareholder / investor miscreants and has a societal tolerance for making off with the loot by fair means or foul. Getting your hands on the dough is always implicitly redemptive.

European thinking eschews this (openDemocracy couldn’t help but get its usual digs in, we’ll forgive it this because it isn’t entirely wrong and it has its readership to please). But what that can and I’d argue does lead to is being deaf, dumb and blind to an equally problematic phenomena — management control frauds. If there is a more European cultural lauding of what is lionised as skilled and responsible management, the risk is always that management and managerialism is not subject to any critical investigations. Put management on a pedestal and worship it, and you’re not likely to go looking for any defects of character. Resolving (or, at least, giving the impression of resolving) the problems of the day through demonstrations of management skill and competence is always redemptive.

This lack of willingness to consider management as the source of wrongdoing creates a criminogenic environment for control frauds. Control frauds are just as damaging (and of course just as both morally and potentially criminally liable) as investor-sponsored wrongdoing.

Shorter, at least everyone knows London is a potential cesspool. But nice, polite, squeaky clean starchy Berlin and Copenhagen? Oh, no, it can’t be like that lot over there. Can it? If you wanted to cover your tracks and give yourself a shiny polished veneer for your nefariousness, where would you go?

“From a health point of view, this is safer than handling cash and visiting shops. But, anti-corruption researchers warn, the boom in e-money poses another risk: money-laundering.”

First: “From a health point of view, this is safer than handling cash….”

I have seen this statement many times yet I have still to see any scientific study that proves that “handling cash” is more dangerous than any other payment system. So many complaints about those who don’t listen to “science” yet this statement is made over and over again without proof or support. Any scientific study should consider multiple factors including, in this case, the danger of increasing criminality. As far as disease, how high is the actual risk if any?

Second: “and visiting shops.” So, does that mean that all shopping must be online and payment digital because it is safer?

The cash statement is part of the drive to eliminate cash and make us dependent on a single digital payment system that has no backup system and is extremely vulnerable to solar storms, EMP attack, cyber attack, war, among other dangers. If I were a War Game Planner, the first thing I would do is take out my opponent’s payment system. I would be sure that my own system had backup, like cash.

Put all your eggs in one basket and then watch it get crushed.

Will? Will? I thought that the UK – specifically the City of London – was already a hub of money laundering with the spokes going out to Shaxson’s Treasure Islands. If the authors are talking about dodgy Russians with their money, then I am sure that the Federal Tax Police Service of the Russian Federation will also be taking an interest. The Russians in this article – are they regular Russians or those trying to steal money out of Russia illegally? It gets a bit blurry this point in the article. But who am I kidding? The UK took in a cohort of Russian billionaires with the money that they stripped out of Russia and are protecting them from any possibility of extraditions. Certainly there is not much that Russian oligarchs can teach the City of London about corruption as the later has been into financial transactions since Augustus was knee high to a grasshopper.

I do find it interesting that Latvia comes up in connection with these transactions as that country has been a Neoliberal “success” story. Not so great if you actually lived there and you can ask Michael Hudson about that one. So, neoliberalism in countries lead to corrupt banking practices? Who knew? Has anybody told London or New York about that? That article also mentions a Lebanese-American – George Nader – who was convicted in the US on child sex charges. Anybody else read that and wonder about an Epstein connection? I also see that PrivatBank was mentioned. That’s Ihor Kolomoyskyi who is as corrupt as they come. Maybe they should be checking the finances of the Ukraine though I doubt that that will be allowed to happen. Anyway, electronic money will be a boon to criminals but most money these days is electronic already. Better maybe to go after the actors and get countries to clean up their banking systems but as regular billionaires take advantage of the same mechanism, I am not holding my breath.

Perhaps because I recently re-watched The Spider’s Web: Britain’s Second Empire (Financial Power Documentary) | Timeline (https://www.youtube.com/watch?v=-YgFDZNXPyg), this piece feels decidedly underwhelming. And it is hard not to see it just as an opportunity to link ‘Russian and money laundering’ in one sentence. (The frequency with which this appears in the article argues against an editing oversight – but seems more like one of the purposes.)

Yes, EMIs may be susceptible to corruption. Seems to me, anywhere there is capitalism and money, opportunities for corruption ensue. Given that there is no political will to crack down on abuses, how is this news? Wake me up, when politicians resolve once and for all to tackle money laundering and off-shoring – British, Russian, or any other.

Wait…….you mean the UK is NOT already a hub of money laundering? With Cayman, Jersey, Isle of Man, Guernsey, Mauritius, Seychelles already UK suzerains….?

There have been a number of articles in the MSM recently laying the groundwork for replacing cash with official digital money. These proposals are promoted on spurious grounds of health, convenience and national security (we must not fall behind the PRC!) but I imagine the real agenda includes solving the pesky problem of the zero bound, opening vast new frontiers for surveillance of both the capitalist and political sort and incidentally making money laundering, tax evasion and other City specialities a lot more difficult to pull off.

There is a flaw in the basic thesis of the article, by stating, “Become a hub of money laundering,” it assumes that London is not already a hub for money laundering.

It is pretty clear that the City of London is already a hub for money laundering.

London is the only real Global Financial Centre. That means it has exploited and in some cases devised every idea on the spectrum from totally legit to extremely criminal. London really just reflects the world’s appetite for tolerance or regulation. It is only regulated as far as the world wants it to be. If you say London facilitates crime in Russia and is a good place to fight the crime then fine but who is actually fighting the criminals? When the world changes London changes unless God intervenes… so far he doesn’t bother much.

The fight against all systems as e-money structures, shell companies, SLP’s or whatsoever stuff is actually directed to beat poor fellows trying to divert the money from the greed of money of the Taxman in every State where the taxation must sustain an enormous Public “apparatich”. The real money laundering and evasion are made by the big corporations, by banks, by big groups through complicated but only formally checked by the system (AML, KYC, CTA…)Everybody knows that to swift money to a friend or for business reasons when the amount is more than €1,000 (or 3,000 sometimes) is checked carefully and always seen as “suspicious”. After 35 years of experience I can bear any discussion about, also reminding to the inattentive people how many billions have been stolen by ENRON, QUALCOMM, DEUTSCHE BANK, SOCIETE’ GENERAL….and useless public expenditures