Yves here. This is another tour de force from Michael Hudson, derived from a paper he presented in early January at the UPRE session during the annual ASSA meeting. This time he turns from his recent focus on the economically destructive but oligarchy-advancing practice of sanctifying debt to another favorite topic, the evolution of capitalism. Hudson looks from the early Industrial Revolution onward and demonstrates that the dominance of financial capital over industrial capital was neither the likely course of events nor desirable. A major feature of this development is the increasing weight of rentier activities and how they drain income from workers and more productive sectors.

One of his key conclusions:

The result is a “deep state” supporting a cosmopolitan financial oligarchy. That is the definition of fascism, reversing democratic government to restore control to the rentier financial and monopoly classes. The beneficiary is the corporate sector, not labor, whose resentment is turned against foreigners and against designated enemies within.

For Hudson, the deep state enforcers are the IMF and the World Bank (which pressed emerging economies to develop capital markets, making them more vulnerable to destabilizing hot money flows). He did not mention them in this article but I imagine Hudson would add domestic law neutering “investor-state dispute settlement” provisions in trade agreements.

Even with its length (get a cup of coffee!), an article that covers so much terrain is bound to simplify a bit. One small quibble: While Hudson correctly depicts China as hewing strictly and successfully to an industrial capital model, and keeping finance in check, Hudson overeggs the pudding a bit in saying, “China has kept banking in the public domain.” China’s regional governments have supported real-estate development projects, including a non-trivial proportion of ghost cities. often funded by private “wealth management products”. China’s “shadow banking sector” which officials have just estimated at nearly $13 trillion, or 86% of GDP and nearly 30% of banking assets. Chinese officials say they are about to crack down on them, after many years of looking the other way, plus the occasional bailout of particular wealth management product issuances gone sour. Similarly, the dominant mobile payment platform player, Alibaba, is private.

By Michael Hudson, a research professor of Economics at University of Missouri, Kansas City, and a research associate at the Levy Economics Institute of Bard College. His latest book is “and forgive them their debts”: Lending, Foreclosure and Redemption from Bronze Age Finance to the Jubilee Year

Marx and many of his less radical contemporary reformers saw the historical role of industrial capitalism as being to clear away the legacy of feudalism – the landlords, bankers and monopolists extracting economic rent without producing real value. But that reform movement failed. Today, the Finance, Insurance and Real Estate (FIRE) sector has regained control of government, creating neo-rentier economies.

The aim of this post-industrial finance capitalism is the oppositeof that of industrial capitalism as known to 19th-century economists: It seeks wealth primarily through the extraction of economic rent, not industrial capital formation. Tax favoritism for real estate, privatization of oil and mineral extraction, banking and infrastructure monopolies add to the cost of living and doing business. Labor is being exploited increasingly by bank debt, student debt, credit-card debt, while housing and other prices are inflated on credit, leaving less income to spend on goods and services as economies suffer debt deflation.

Today’s New Cold War is a fight to internationalize this rentier capitalism by globally privatizing and financializing transportation, education, health care, prisons and policing, the post office and communications, and other sectors that formerly were kept in the public domain of European and American economies so as to keep their costs low and minimize their cost structure.

In the Western economies such privatizations have reversed the drive of industrial capitalism to minimize socially unnecessary costs of production and distribution. In addition to monopoly prices for privatized services, financial managers are cannibalizing industry by debt leveraging and high dividend payouts to increase stock prices.

Today’s neo-rentier economies obtain wealth mainly by rent seeking, while financialization capitalizes real estate and monopoly rent into bank loans, stocks and bonds. Debt leveraging to bid up prices and create capital gains on credit for this “virtual wealth” has been fueled by central bank Quantitative Easing since 2009.

Financial engineering is replacing industrial engineering. Over 90 percent of recent U.S. corporate income has been earmarked to raise the companies’ stock prices by being paid out as dividends to stockholders or spent on stock buyback programs. Many companies even borrow to buy up their own shares, raising their debt/equity ratios.

Households and industry are becoming debt-strapped, owing rent and debt service to the Finance, Insurance and Real Estate (FIRE) sector. This rentier overhead leaves less wage and profit income available to spend on goods and services, bringing to a close the 75-year U.S. and European expansion since World War II ended in 1945.

These rentier dynamics are the opposite of what Marx described as industrial capitalism’s laws of motion. German banking was indeed financing heavy industry under Bismarck, in association with the Reichsbank and military. But elsewhere, bank lending rarely has financed new tangible means of production. What promised to be a democratic and ultimately socialist dynamic has relapsed back toward feudalism and debt peonage, with the financial class today playing the role that the landlord class did in post-medieval times.

Marx’s View of the Historical Destiny of Capitalism: to Free Economies from Feudalism

The industrial capitalism that Marx described in Volume I of Capital is being dismantled. He saw the historical destiny of capitalism to be to free economies from the legacy of feudalism: a hereditary warlord class imposing tributary land rent, and usurious banking. He thought that as industrial capitalism evolved toward more enlightened management, and indeed toward socialism, it would replace predatory “usurious” finance, cutting away the economically and socially unnecessary rentier income, land rent and financial interest and related fees for unproductive credit. Adam Smith, David Ricardo, John Stuart Mill, Joseph Proudhon and their fellow classical economists had analyzed these phenomena, and Marx summarized their discussion in Volumes II and III of Capitaland his parallel Theories of Surplus Valuedealing with economic rent and the mathematics of compound interest, which causes debt to grow exponentially at a higher rate than the rest of the economy.

However, Marx devoted Volume I of Capital to industrial capitalism’s most obvious characteristic: the drive to make profits by investing in means of production to employ wage labor to produce goods and services to sell at a markup over what labor was paid. Analyzing surplus value by adjusting profit rates to take account of outlays for plant, equipment and materials (the “organic composition of capital”), Marx described a circular flow in which capitalist employers pay wages to their workers and invest their profits in plant and equipment with the surplus not paid to employees.

Finance capitalism has eroded this core circulation between labor and industrial capital. Much of the midwestern United States has been turning into a rust belt. Instead of the financial sector evolving to fund capital investment in manufacturing, industry is being financialized. Making economic gains financially, primarily by debt leverage, far outstrips making profits by hiring employees to produce goods and services.

Capitalism’s Alliance of Banks with Industry to Promote Democratic Political Reform

The capitalism of Marx’s day still contained many survivals from feudalism, most notably a hereditary landlord class living off the land rents, most of which were spent unproductively on servants and luxuries, not to make a profit. These rents had originated in a tax. Twenty years after the Norman Conquest, William the Conquer had ordered compilation of the Domesday Book in 1086 to calculate the yield that could be extracted as taxes from the English land that he and his companions had seized. As a result of King John’s overbearing fiscal demands, the Revolt of the Barons (1215-17) and their Magna Carta enabled the leading warlords to obtain much of this rent for themselves. Marx explained that industrial capitalism was politically radical in seeking to free itself from the burden of having to support this privileged landlord class, receiving income with no basis in cost value or enterprise of its own.

Industrialists sought to win markets by cutting costs below those of their competitors. That aim required freeing the entire economy from the “faux frais” of production, socially unnecessary charges built into the cost of living and doing business. Classical economic rent was defined as the excess of price above intrinsic cost-value, the latter being ultimately reducible to labor costs. Productive labor was defined as that employed to create a profit, in contrast to the servants and retainers (coachmen, butlers, cooks, et al.) on whom landlords spent much of their rent.

The paradigmatic form of economic rent was the ground rent paid to Europe’s hereditary aristocracy. As John Stuart Mill explained, landlords reaped rents (and rising land prices) “in their sleep.” Ricardo had pointed out (in Chapter 2 of his 1817 Principles of Political Economy and Taxation) a kindred form of differential rent in natural-resource rent stemming from the ability of mines with high-quality orebodies to sell their lower-cost mineral output at prices set by high-cost mines. Finally, there was monopoly rent paid to owners at choke points in the economy where they could extract rents without a basis in any cost outlay. Such rents logically included financial interest, fees and penalties.

Marx saw the capitalist ideal as freeing economies from the landlord class that controlled the House of Lords in Britain, and similar upper houses of government in other countries. That aim required political reform of Parliament in Britain, ultimately to replace the House of Lords with the Commons, so as to prevent the landlords from protecting their special interests at the expense of Britain’s industrial economy. The first great battle in this fight against the landed interest was won in 1846 with repeal of the Corn Laws. The fight to limit landlord power over government culminated in the constitutional crisis of 1909-10, when the Lords rejected the land tax imposed by the Commons. The crisis was resolved by a ruling that the Lords never again could reject a revenue bill passed by the House of Commons.

The Banking Sector Lobbies Against the Real Estate Sector, 1815-1846

It may seem ironic today that Britain’s banking sector was whole-heartedly behind the first great fight to minimize land-rent. That alliance occurred after the Napoleonic Wars ended in 1815, which ended the French blockage against British seaborne trade and re-opened the British market to lower-priced grain imports. British landlords demanded tariff protection under the Corn Laws – to raise the price of food, so as to increase the revenue and hence the capitalized rental value of their landholdings – but that has rendered the economy high-cost. A successful capitalist economy would have to minimize these costs in order to win foreign markets and indeed, to defend its own home market. The classical idea of a free market was one free from economic rent – from rentier income in the form of land rent.

This rent – a quasi-tax paid to the heirs of the warlord bands that had conquered Britain in 1066, and the similar Viking bands that had conquered other European realms – threatened to minimize foreign trade. That was a threat to Europe’s banking classes, whose major market was the funding of commerce by bills of exchange. The banking class arose as Europe’s economy was revived by the vast looting of monetary bullion from Constantinople by the Crusaders. Bankers were permitted a loophole to avoid Christianity’s banning of the charging of interest, by taking their return in the form of agio, a fee for transferring money from one currency to another, including from one country to another.

Even domestic credit could use the loophole of “dry exchange,” charging agioon domestic transactions cloaked as a foreign-currency transfer, much as modern corporations use “offshore banking centers” today to pretend that they earn their income in tax-avoidance countries that do not charge an income tax.

If Britain was to become the industrial workshop of the world, it would prove highly beneficial to Ricardo’s banking class. (He was its Parliamentary spokesman; today we would say lobbyist.) Britain would enjoy an international division of labor in which it exported manufactures and imported food and raw materials from other countries specializing in primary commodities and depending on Britain for their industrial products. But for this to happen, Britain needed a low price of labor. That meant low food costs, which at that time were the largest items in the family budgets of wage labor. And that in turn required ending the power of the landlord class to protect its “free lunch” of land rent, and all recipients of such “unearned income.”

It is hard today to imagine industrialists and bankers hand in hand promoting democratic reform against the aristocracy. But that alliance was needed in the early 19thcentury. Of course, democratic reform at that time extended only to the extent of unseating the landlord class, not protecting the interest of labor. The hollowness of the industrial and banking class’s democratic rhetoric became apparent in Europe’s 1848 revolutions, where the vested interests ganged up against extending democracy to the population at large, once the latter had helped end landlord protection of its rents.

Of course, it was socialists who picked up the political fight after 1848. Marx later reminded a correspondent that the first plank of the Communist Manifesto was to socialize land rent, but poked fun at the “free market” rent critics who refused to recognize that rentier-like exploitation existed in the industrial employment of wage labor. Just as landlords obtained land rent in excess of the cost of producing their crops (or renting out housing), so employers obtained profits by selling the products of wage-labor at a markup. To Marx, that made industrialists part of the rentier class in principle, although the overall economic system of industrial capitalism was much different from that of post-feudal rentiers, landlords and bankers.

The Alliance of Banking with Real Estate and Other Rent-Seeking Sectors

With this background of how industrial capitalism was evolving in Marx’s day, we can see how overly optimistic he was regarding the drive by industrialists to strip away all unnecessary costs of production – all charges that added to price without adding to value. In that sense he was fully in tune with the classical concept of free markets, as markets free from land rent and other forms of rentier income.

Today’s mainstream economics has reversed this concept. In an Orwellian doublethink twist, the vested interests today define a free market as one “free” forthe proliferation of various forms of land rent, even to the point of giving special tax advantages to absentee real estate investment, the oil and mining industries (natural-resource rent), and most of all to high finance (the accounting fiction of “carried interest,” an obscure term for short-term arbitrage speculation).

Today’s world has indeed freed economies from the burden of hereditary ground rent. Almost two-thirds of American families own their own homes (although the rate of homeownership has been falling steadily since the Great Obama Evictions that were a byproduct of the junk-mortgage crisis and Obama Bank Bailouts of 2009-16, which lowered homeowner rates from over 68% to 62%). In Europe, home ownership rates have reached 80% in Scandinavia, and high rates characterize the entire continent. Home ownership – and also the opportunity to purchase commercial real estate – has indeed become democratized.

But it has been democratized on credit. That is the only way for wage-earners to obtain housing, because otherwise they would have to spend their entire working life saving enough to buy a home. After World War II ended in 1945, banks provided the credit to purchase homes (and for speculators to buy commercial properties), by providing mortgage credit to be paid off over the course of 30 years, the likely working life of the young home buyer.

Real estate is by far the banking sector’s largest market. Mortgage lending accounts for about 80 percent of U.S. and British bank credit. It played only a minor role back in 1815, when banks focused on financing commerce and international trade. Today we can speak of the Finance, Insurance and Real Estate (FIRE) sector as the economy’s dominant rentier sector. This alliance of banking with real estate has led banks to become the major lobbyists protecting real estate owners by opposing the land tax that seemed to be the wave of the future in 1848 in the face of rising advocacy to tax away the land’s entire price gains and rent, to make land the tax base as Adam Smith had urged, instead of taxing labor and consumers or profits. Indeed, when the U.S. income tax began to be levied in 1914, it fell only on the wealthiest One Percent of Americans, whose taxable income consisted almost entirely of property and financial claims.

The past century has reversed that tax philosophy. On a national level, real estate has paid almost zero income tax since World War II, thanks to two giveaways. The first is “fictitious depreciation,” sometimes called over-depreciation. Landlords can pretend that their buildings are losing value by claiming that they are wearing out at fictitiously high rates. (That is why Donald Trump has said that he loves depreciation.) But by far the largest giveaway is that interest payments are tax deductible. Real estate is taxed locally, to be sure, but typically at only 1% of assessed valuation, which is less than 7 to 10 percent of the actual land rent.[1]

The basic reason why banks support tax favoritism for landlords is that whatever the tax collector relinquishes is available to be paid as interest. Mortgage bankers end up with the vast majority of land rent in the United States. When a property is put up for sale and homeowners bid against each other to buy it, the equilibrium point is where the winner is willing to pay the full rental value to the banker to obtain a mortgage. Commercial investors also are willing to pay the entire rental income to obtain a mortgage, because they are after the “capital” gain – that is, the rise in the land’s price.

The policy position of the so-called Ricardian socialists in Britain and their counterparts in France (Proudhon, et al.) was for the state to collect the land’s economic rent as its major source of revenue. But today’s “capital” gains occur primarily in real estate and finance, and are virtually tax-free for landlords. Owners pay no capital-gains tax as real estate prices rise, or even upon sale if they use their gains to buy another property. And when landlords die, all tax liability is wiped out.

The oil and mining industries likewise are notoriously exempt from income taxation on their natural-resource rents. For a long time the depletion allowance allowed them tax credit for the oil that was sold off, enabling them to buy new oil-producing properties (or whatever they wanted) with their supposed asset loss, defined as the value to recover whatever they had emptied out. There was no real loss, of course. Oil and minerals are provided by nature.

These sectors also make themselves tax exempt on their foreign profits and rents by using “flags of convenience” registered in offshore banking centers. This ploy enables them to claim to make all their profits in Panama, Liberia or other countries that do not charge an income tax or even have a currency of their own, but use the U.S. dollar so as to save American companies from any foreign-exchange risk.

In oil and mining, as with real estate, the banking system has become symbiotic with rent recipients, including companies extracting monopoly rent. Already in the late 19thcentury the banking and insurance sector was recognized as “the mother of trusts,” financing their creation to extract monopoly rents over and above normal profit rates.

These changes have made rent extraction much more remunerative than industrial profit-seeking – just the opposite of what classical economists urged and expected to be the most likely trajectory of capitalism. Marx expected the logic of industrial capitalism to free society from its rentier legacy and to create public infrastructure investment to lower the economy-wide cost of production. By minimizing labor’s expenses that employers had to cover, this public investment would put in place the organizational network that in due course (sometimes needing a revolution, to be sure) would become a socialist economy.

Although banking developed ostensibly to serve foreign trade by the industrial nations, it became a force-in-itself undermining industrial capitalism. In Marxist terms, instead of financing the M-C-M’ circulation (money invested in capital to produce a profit and hence yet more money), high finance has abbreviated the process to M-M’, making money purely from money and credit, without tangible capital investment.

The Rentier Squeeze on Budgets: Debt Deflation as a Byproduct of Asset-Price Inflation

Democratization of home ownership meant that housing no longer was owned primarily by absentee owners extracting rent, but by owner-occupants. As home ownership spread, new buyers came to support the rentier drives to block land taxation – not realizing that rent that was not taxed would be paid to the banks as interest to absorb the rent-of-location hitherto paid to absentee landlords.

Real estate has risen in price as a result of debt leveraging. The process makes investors, speculators and their bankers wealthy, but raises the cost of housing (and commercial property) for new buyers, who are obliged to take on more debt in order to obtain secure housing. That cost is also passed on to renters. And employers ultimately are obliged to pay their labor force enough to pay these financialized housing costs.

Debt deflation has become the distinguishing feature of today’s economies from North America to Europe, imposing austerity as debt service absorbs a rising share of personal and corporate income, leaving less to spend on goods and services. The economy’s indebted 90 percent find themselves obliged to pay more and more interest and financial fees. The corporate sector, and now also the state and local government sector, likewise are obliged to pay a rising share of their revenue to creditors.

Investors are willing to pay most of their rental income as interest to the banking sector because they hope to sell their property at some point for a “capital” gain. Modern finance capitalism focuses on “total returns,” defined as current income plusasset-price gains, above all for land and real estate. Inasmuch as a home or other property is worth however much banks will lend against it, wealth is created primarily by financial means, by banks lending a rising proportion of the value of assets pledged as collateral.

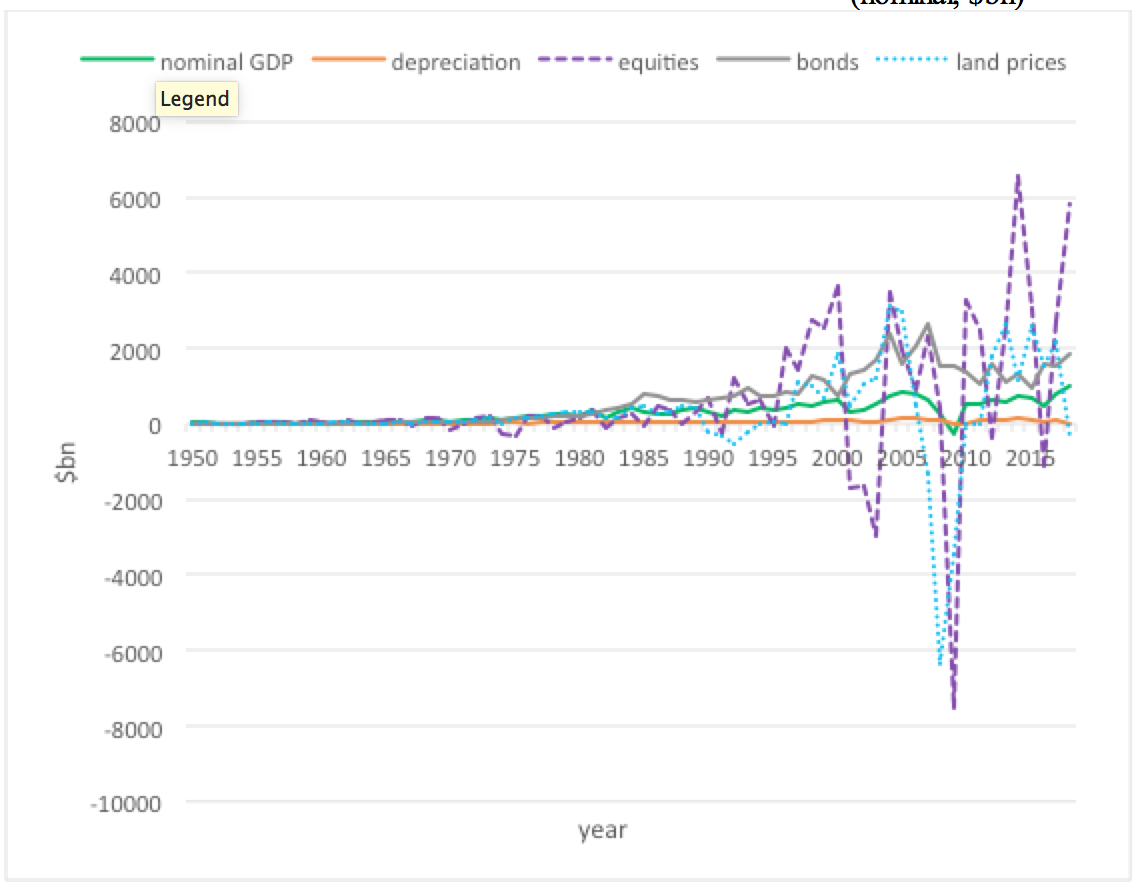

Chart 10.4: annual changes in GDP and the major components of asset price gains

(nominal, $bn)

The fact that asset-price gains are largely debt-financed explains why economic growth is slowing in the United States and Europe, even as stock market and real estate prices are inflated on credit. The result is a debt-leveraged economy.

Changes in the value of the economy’s land from year to year far exceeds the change in GDP. Wealth is obtained primarily by asset-price (“capital”) gains in the valuation of land and real estate, stocks, bonds and creditor loans (“virtual wealth”), not so much by saving income (wages, profits and rents).The magnitude of these asset-price gains tends to dwarf profits, rental income and wages.

The tendency has been to imagine that rising prices for real estate, stocks and bonds has been making homeowners richer. But this price rise is fueled by bank credit. A home or other property is worth however much a bank will lend against it – and banks have lent a larger and larger proportion of the home’s value since 1945. For U.S. real estate as a whole, debt has come to exceed equity for more than a decade now. Rising real estate prices have made banks and speculators rich, but have left homeowners and commercial real estate debt strapped.

The economy as a whole has suffered. Debt-fueled housing costs in the United States are so high that if all Americans were given their physical consumer goods for free – their food, clothing and so forth – they still could not compete with workers in China or most other countries. That is a major reason why the U.S. economy is de-industrializing. So this policy of “creating wealth” by financialization undercuts the logic of industrial capitalism.

Finance Capital’s Fight to Privatize and Monopolize Public Infrastructure

Another reason for deindustrialization is the rising cost of living stemming from conversion of public infrastructure into privatized monopolies. As the United States and Germany overtook British industrial capitalism, a major key to industrial advantage was recognized to be public investment in roads, railroads and other transportation, education, public health, communications and other basic infrastructure. Simon Patten, the first professor of economics at America’s first business school, the Wharton School at the University of Pennsylvania, defined public infrastructure as a “fourth factor of production,” in addition to labor, capital and land. But unlike capital, Patten explained, its aim was not to make a profit. It was to minimize the cost of living and doing business by providing low-price basic services to make the private sector more competitive.

Unlike the military levies that burdened taxpayers in pre-modern economies, “in an industrial society the object of taxation is to increase industrial prosperity”by creating infrastructure in the form of canals and railroads, a postal service and public education. This infrastructure was a “fourth” factor of production.Taxes would be “burdenless,” Patten explained, to the extent that they were invested in public internal improvements, headed by transportation such as the Erie Canal.[2]

The advantage of this public investment is tolower costs instead of letting privatizers impose monopoly rents in the form of access charges to basic infrastructure. Governments can price the services of these natural monopolies (including credit creation, as we are seeing today) at cost or offer them freely, helping labor and its employers undersell industrialists in countries lacking such public enterprise.

In the cities, Patten explained, public transport raises property prices (and hence economic rent) in the outlying periphery, as the Erie Canal had benefited western farms competing with upstate New York farmers.That principle is evident in today’s suburban neighborhoods relative to city centers.London’s Tube extension along the Jubilee Line, and New York City’s Second Avenue Subway, showed that underground and bus transport can be financed publicly by taxing the higher rental value created for sites along such routes. Paying for capital investment out of such tax levies can provide transportation at subsidized prices, minimizing the economy’s cost structure accordingly. What Joseph Stiglitz popularized as the “Henry George Law” thus more correctly should be known as “Patten’s Law” of burdenless taxation.[3]

Under a regime of “burdenless taxation” the return on public investment does not take the form of profit but aims at lowering the economy’s overall price structure to “promote general prosperity.” This means that governments should operate natural monopolies directly, or at least regulate them. “Parks, sewers and schools improve the health and intelligence of all classes of producers, and thus enable them to produce more cheaply, and to compete more successfully in other markets.”Patten concluded: “If the courts, post office, parks, gas and water works, street, river and harbor improvements, and other public works do not increase the prosperity of society they should not be conducted by the State.” But this prosperity for the overall economy was not obtained by treating public enterprises as what today is called a profit center.[4]

In one sense, this can be called “privatizing the profits and socializing the losses.” Advocating a mixed economy along these lines is part of the logic of industrial capitalism seeking to minimize private-sector production and employment costs in order to maximize profits. Basic social infrastructure is a subsidy to be supplied by the state.

Britain’s Conservative Prime Minister Benjamin Disraeli (1874-80) reflected this principle: “The health of the people is really the foundation upon which all their happiness and all their powers as a state depend.”[5]He sponsored the Public Health Act of 1875, followed by the Sale of Food and Drugs Act and, the next year, the Education Act. The government would provide these services, not private employers or private monopoly-seekers.

For a century, public investment helped the United States pursue an Economy of High Wages policy, providing education, food and health standards to make its labor more productive and thus able to undersell low-wage “pauper” labor. The aim wasto create a positive feedback between rising wages and increasing labor productivity.

That is in sharp contrast to today’s business plan of finance capitalism – to cut wages, and also cut back long-term capital investment, research and development while privatizing public infrastructure. The neoliberal onslaught by Ronald Reagan in the United States and Margaret Thatcher in Britain in the 1980s was backed by IMF demands that debtor economies balance their budgets by selling off such public enterprises and cutting back social spending. Infrastructure services were privatized as natural monopolies, sharply raising the cost structure of such economies, but creating enormous financial underwriting commissions and stock-market gains for Wall Street and London.

Privatizing hitherto public monopolies has become one of the most lucrative ways to gain wealth financially. But privatized health care and medical insurance is paid for by labor and its employers, not by the government as in industrial capitalism. And in the face of the privatized educational system’s rising cost, access to middle-class employment has been financed by student debt. These privatizations have not helped economies become more affluent or competitive. On an economy-wide level this business plan is a race to the bottom, but one that benefits financial wealth at the top.

Finance Capitalism Impoverishes Economies While Increasing Their Cost Structure

Classical economic rent is defined as the excess of price over intrinsic cost-value. Capitalizing this rent – whether land rent or monopoly rent from the privatization described above – into bonds, stocks and bank loans creates “virtual wealth.” Finance capitalism’s exponential credit creation increases “virtual” wealth – financial securities and property claims – by managing these securities and claims in a way that has made them worth more than tangible real wealth.

The major way to gain fortunes is to get asset-price gains (“capital gains”) on stocks, bonds and real estate.However, this exponentially growing debt-leveraged financial overhead polarizes the economy in ways that concentrates ownership of wealth in the hands of creditors, and owners of rental real estate, stocks and bonds, draining the “real” economy to pay the FIRE sector.

Post-classical economics depicts privatized infrastructure, natural resource development and banking as being part of the industrial economy, not superimposed on it by a rent-seeking class. But the dynamic of finance-capitalist economies is not for wealth to be gained mainly by investing in industrial means of production and saving up profits or wages, but by capital gains made primarily from rent-seeking. These gains are not “capital” as classically understood. They are “finance-capital gains,” because they result from asset-price inflation fueled by debt leveraging.

By inflating its housing prices and a stock market bubble on credit, America’s debt leveraging, along with its financializing and privatizing basic infrastructure, has priced it out of world markets. China and other non-financialized countries have avoided high health insurance costs, education costs and other services freely or at a low cost as a public utility. Public health and medical care costs much less abroad, but is attacked in the United States by neoliberals as “socialized medicine,” as if financialized health care would make the U.S. economy more efficient and competitive. Transportation likewise has been financialized and run for profit, not to lower the cost of living and doing business.

One must conclude that America has chosen to no longer industrialize, but to finance its economy by economic rent – monopoly rent, from information technology, banking and speculation, and leave industry, research and development to other countries. Even if China and other Asian countries didn’t exist, there is no way that America can regain its export markets or even its internal market with its current debt overhead and its privatized and financialized education, health care, transportation and other basic infrastructure.

The underlying problem is not competition from China, but neoliberal financialization. Finance-capitalism is not industrial capitalism. It is a lapse back into debt peonage and a rentier neo-feudalism. Bankers play the role today that landlords played up through the 19thcentury, making fortunes without corresponding value, by capital gains for real estate, stocks and bonds on credit, by debt leveraging whose carrying charges increase the economy’s cost of living and doing business.

Today’s New Cold War is a Fight by Finance Capitalism Against Industrial Capitalism

Today’s world is being fractured by an economic warfare over what kind of economic system it will have. Industrial capitalism is losing the fight to finance capitalism, which is turning to be its antithesis just as industrial capitalism was the antithesis to post-feudal landlordship and predatory banking houses.

In this respect today’s New Cold War is a conflict of economic systems. As such, it is being fought against the dynamic of U.S. industrial capitalism as well as that of China and other economies. Hence, the struggle also is domestic within the United States and Europe, as well as confrontational against China and Russia, Iran, Cuba, Venezuela and their moves to de-dollarize their economies and reject the Washington Consensus and its Dollar Diplomacy. It is a fight by U.S.-centered finance capital to promote neoliberal doctrine giving special tax privileges to rentier income, untaxing land rent, natural resource rent, monopoly rent and the financial sector. This aim includes privatizing and financializing basic infrastructure, maximizing its extraction of economic rent instead of minimizing the cost of living and doing business.

The result is a war to change the character of capitalism as well as that of social democracy. The British Labour Party, European Social Democrats and the U.S. Democratic Party all have jumped on the neoliberal bandwagon. They are all complicit in the austerity that has spread from the Mediterranean to America’s Midwestern rust belt.

Finance capitalism exploits labor, but via a rentier sector, which also ends up cannibalizing industrial capital. This drive has become internationalized into a fight against nations that restrict the predatory dynamics of finance capital seeking to privatize and dismantle government regulatory power. The New Cold War is not merely a war being waged by finance capitalism against socialism and public ownership of the means of production. In view of the inherent dynamics of industrial capitalism requiring strong state regulatory and taxing power to check the intrusiveness of finance capital, this post-industrial global conflict is between socialism evolving out of industrial capitalism, and fascism, defined as a rentier reaction to mobilize government to roll back social democracy and restore control to the rentier financial and monopoly classes.

The old Cold War was a fight against “Communism.” In addition to freeing itself from land rent, interest charges and privately appropriated industrial profits, socialism favors labor’s fight for better wages and working conditions, better public investment in schools, health care and other social welfare support, better job security, and unemployment insurance. All these reforms would cut into the profits of employers. Lower profits mean lower stock-market prices, and hence fewer finance-capital gains.

The aim of finance capitalism is not to become a more productive economy by producing goods and selling them at a lower cost than competitors. What might appear at first sight to be international economic rivalry and jealousy between the United States and China is thus best seen as a fight between economic systems: that of finance capitalism and that of civilization trying to free itself from rentier privileges and submission to creditors, with a more social philosophy of government empowered to check private interests when they act selfishly and injure society at large.

The enemy in this New Cold War is not merely socialist government but government itself, except to the extent that it can be brought under the control of high finance to promote the neoliberal rentier agenda. This reverses the democratic political revolution of the 19thcentury that replaced the House of Lords and other upper houses controlled by the hereditary aristocracy with more representative legislators. The aim is to create a corporate state, replacing elected houses of government by central banks – the U.S. Federal Reserve and the European Central Bank, along with external pressure from the International Monetary Fund and World Bank.

The result is a “deep state” supporting a cosmopolitan financial oligarchy. That is the definition of fascism, reversing democratic government to restore control to the rentier financial and monopoly classes. The beneficiary is the corporate sector, not labor, whose resentment is turned against foreigners and against designated enemies within.

Lacking foreign affluence, the U.S. corporate state promotes employment by a military buildup and public infrastructure spending, most of which is turned over to insiders to privatize into rent-seeking monopolies and sinecures. In the United States, the military is being privatized for fighting abroad (e.g., Blackwater USA/Academi), and jails are being turned into profit centers using inexpensive convict labor.

What is ironic is that although China is seeking to decouple from Western finance capitalism, it actually has been doing what the United States did in its industrial takeoff in the late 19thand early 20thcentury. As a socialist economy, China has aimed at what industrial capitalism was expected to achieve: freeing its economy from rentier income (landlordship and usurious banking), largely by a progressive income tax policy falling mainly on rentier income.

Above all, China has kept banking in the public domain. Keeping money and credit creation public instead of privatizing it is the most important step to keep down the cost of living and business. China has been able to avoid a debt crisis by forgiving debts instead of closing down indebted enterprises deemed to be in the public interest. In these respects it is socialist China that is achieving the fate that industrial capitalism initially was expected to achieve in the West.

Summary: Finance Capital as Rent-Seeking

The transformation of academic economic theory under today’s finance capitalism has reversed the progressive and indeed radical thrust of the classical political economy that evolved into Marxism. Post-classical theory depicts the financial and other rentier sectors as an intrinsic part of the industrial economy. Today’s national income and GDP accounting formats are compiled in keeping with this anti-classical reaction depicting the FIRE sector and its allied rent-seeking sectors as an addition to national income, not a subtrahend. Interest, rents and monopoly prices all are counted as “earnings” – as if all income is earned as intrinsic parts of industrial capitalism, not predatory extraction as overhead property and financial claims.

This is the opposite of classical economics. Finance capitalism is a drive to avoid what Marx and indeed the majority of his contemporaries expected: that industrial capitalism would evolve toward socialism, peacefully or otherwise.

Some Final Observations: Financial Takeover of Industry, Government and Ideology

Almost every economy is a mixed economy – public and private, financial, industrial and rent-seeking. Within these mixed economies the financial dynamics – debt growing by compound interest, attaching itself primarily to rent-extracting privileges, and therefore protecting them ideologically, politically and academically. These dynamics are different from those of industrial capitalism, and indeed undercut the industrial economy by diverting income from it to pay the financial sector and its rentier clients.

One expression of this inherent antagonism is the time frame. Industrial capitalism requires long-term planning to develop a product, make a marketing plan, and undertake research and development to keep undercutting competitors. The basic dynamic is M-C-M’: capital (money, M) is invested in building factories and other means of production, and employing labor to sell its products (commodities, C) at a profit (M’).

Finance capitalism abbreviates this to a M-M’, making money purely financially, by charging interest and making capital gains. The financial mode of “wealth creation” is measured by the valuations of real estate, stocks and bonds. This valuation was long based on capitalizing their flow of revenue (rents or profits) at the going rate of interest, but is now based almost entirely on capital gains as the major source of “total returns.”

In taking over industrial companies, financial managers focus on the short run, because their salary and bonuses are based on current year’s performance. The “performance” in question is stock market performance. Stock prices have largely become independent from sales volume and profits, now that they are enhanced by corporations typically paying out some 92 percent of their revenue in dividends and stock buybacks.[6]

Even more destructively, private capital has created a new process: M-debt-M’. One recent paper calculates that: “Over 40% of firms that make payouts also raise capital during the same year, resulting in 31% of aggregate share repurchases and dividends being externally financed, primarily with debt.”[7]This has made the corporate sector financially fragile, above all the airline industry in the wake of the COVID-19 crises.

Private equity has played a big role in increasing corporate leverage, both through their own actions and by disinhibiting large public companies in the use of debt. As Eileen Appelbaum and Rosemary Batt explained, the large buyout firms, following the playbook developed in the 1980s, produce their returns from financial engineering and cost cutting (smaller size deals target “growthier” companies, but while those private equity firms assert that they add value, it may just be that they are skilled at identifying promising companies and riding a performance wave). Contrary to their marketing, private equity fee structures mean they make money even when they bankrupt firms. And they have become so powerful that it’s hard to get political support to stop them when they hurt large numbers of citizens though exploitative practices like balance (“surprise”)billing. [8]

The classic description of this looting-for-profit practice process is the 1993 paper by George Akerloff and Paul Romer describing how “firms have an incentive to go broke for profit at society’s expense (to loot) instead of to go for broke (to gamble on success). Bankruptcy for profit will occur if poor accounting, lax regulation, or low penalties for abuse give owners an incentive to pay themselves more than their firms are worth and then default on their debt obligations.”[9]

The fact that “paper gains” from stock prices can be wiped out when financial storms occur, makes financial capitalism less resilient than the industrial base of tangible capital investment that remains in place. The United States has painted its economy into a corner by de-industrializing, replacing tangible capital formation with “virtual wealth,” that is, financial claims onincome and tangible assets. Since 2009, and especially since the Covid crisis of 2020, its economy has been suffering through what is called a K-shaped “recovery.” The stock and bond markets have reached all-time highs to benefit the wealthiest families, but the “real” economy of production and consumption, GDP and employment, has declined for the non-rentier sector, that is, the economy at large.

How do we explain this disparity, if not by recognizing that different dynamics and laws of motion are at work? Gains in wealth increasingly take the form of a rising valuation of rentier financial and property claims onthe real economy’s assets and income, headed by rent-extraction rights, not means of production.

Finance capitalism of this sort can survive only by drawing in exponentially increasing gains from outside the system., either by central bank money creation (Quantitative Easing) or by financializing foreign economies, privatizing them to replace low-priced public infrastructure services with rent-seeking monopolies issuing bonds and stocks, largely financed by dollar-based credit seeking capital gains. The problem with this financial imperialism is that it makes client host economies as high-cost as their U.S. and other sponsors in the world’s financial centers.

All economic systems seek to internationalize themselves and extend their rule throughout the world. Today’s revived Cold War should be understood as a fight between what kind of economic system the world will have. Finance capitalism is fighting against nations that restrict its intrusive dynamics and sponsorship of privatization and dismantling of public regulatory power. Unlike industrial capitalism, the rentier aim is not to become a more productive economy by producing goods and selling them at a lower cost than competitors. Finance capitalism’s dynamics are globalist, seeking to use international organizations (the IMF, NATO, the World Bank and U.S.-designed trade and investment sanctions.) to overrule national governments that are not controlled by the rentier classes. The aim is to make all economies into finance-capitalist layers of hereditary privilege, imposing austerity anti-labor policies to squeeze a dollarized surplus.

Industrial capitalism’s resistance to this international pressure is necessarily nationalist, because it needs state subsidy and laws to tax and regulate the FIRE sector. But it is losing the fight to finance capitalism, which is turning to be its nemesis just as industrial capitalism was the nemesis of post-feudal landlordship and predatory banking. Industrial capitalism requires state subsidy and infrastructure investment, along with regulatory and taxing power to check the incursion of finance capital. The resulting global conflict is between socialism (the natural evolution of industrial capitalism) and a pro-rentier fascism, a state-finance-capitalist reaction against socialism’s mobilization of state power to roll back the post-feudal rentier interests.

Underlying today’s rivalry felt by the United States against China is thus a clash of economic systems. The real conflict is not so much “America vs. China,” but finance capitalism vs. industrial “state” capitalism/socialism. At stake is whether “the state” will support financialization benefiting the rentier class or build up the industrial economy and overall prosperity.

Apart from their time frame, the other major contrast between finance capitalism and industrial capitalism is the role of government. Industrial capitalism wants government to help “socialize the costs” by subsidizing infrastructure services. By lowering the cost of living (and hence the minimum wage), this leaves more profits to be privatized. Finance capitalism wants to pry these public utilities away from the public domain and make them privatized rent-yielding assets. That raises the economy’s cost structure – and thus is self-defeating from the vantage point of international competition among industrialists.

That is why the lowest-cost and least financialized economies have overtaken the United States, headed by China. The way that Asia, Europe and the United States have reacted to the covid-19 crisis highlights the contrast. The pandemic has forced an estimated 70 percent of local neighborhood restaurants to close in the face of major rent and debt arrears. Renters, unemployed homeowners and commercial real estate investors, as well as numerous consumer sectors are also facing evictions and homelessness, insolvency and foreclosure or distress sales as economic activity plunges.

Less widely noted is how the pandemic has led the Federal Reserve to subsidize the polarization and monopolization of the U.S. economy by making credit available at only a fraction of 1 percent to banks, private equity funds and the nation’s largest corporations, helping them gobble up small and medium-sized businesses in distress.

For a decade after the Obama bank-fraud bailout in 2009, the Fed described its purpose as being to keep the banking system liquid and avoid damage to its bondholders, stockholders and large depositors. The Fed infused the commercial banking system with enough lending power to support stock and bond prices. Liquidity was injected into the banking system by buying government securities, as was normal. But after the covid virus hit in March 2020, the Fed began to buy corporate debt for the first time, including junk bonds. Former FDIC head Sheila Bair and Treasury economist Lawrence Goodman note, the Federal Reserve bought the bonds “of ‘fallen angels’ who sank to junk status during the pandemic” as a result of having indulged in over-leveraged borrowing to pay out dividends and buy their own shares.[10]

Congress considered limiting companies from using the proceeds of the bonds being bought “for outsize executive compensation or shareholder distributions” at the time it approved the facilities. but made no attempt to deter companies from doing this. Noting that “Sysco used the money to pay dividends to its shareholders while laying off a third of its workforce … a House committee report found that companies benefiting from the facilities laid off more than one million workers from March to September.” Bair and Goodman conclude that “there’s little evidence that the Fed’s corporate debt buy-up benefited society.” Just the opposite: The Fed’s actions “created a further unfair opportunity for large corporations to get even bigger by purchasing competitors with government-subsidized credit.”

The result, they accuse, is transforming the economy’s political shape. “The serial market bailouts by monetary authorities – first the banking system in 2008, and now the entire business world amid the pandemic” has been “a greater threat [to destroy capitalism] than Bernie Sanders.” The Fed’s “super-low interest rates have favored the equity of large companies over their smaller counterparts,” concentrating control of the economy in the hands of firms with the largest access to such credit.

Smaller companies are “the primary source of job creation and innovation,” but do not have access to the almost free credit enjoyed by banks and their largest customers. As a result, the financial sector remains the mother of trusts, concentrating financial and corporate wealth by financing a gobbling-up of smaller companies as giant companies to monopolize the debt and bailout market.

The result of this financialized “big fish eat little fish” concentration is a modern-day version of fascism’s Corporate State. Radhika Desai calls it “creditocracy,” rule by the institutions in control of credit.[11]It is an economic system in which central banks take over economic policy from elected political bodies and the Treasury, thereby completing the process of privatizing economy-wide control.

Industrial Capitalism’s aims Finance Capitalism’s aims

| Make profits by producing products | Extract economic rent and interest | |

| Minimize the cost of living and prices

|

Add land and monopoly rent to prices

|

|

| Favor industry and labor. | Give special tax favoritism to the finance, insurance and real estate (FIRE) sectors. | |

| Minimize land rent and housing costs by taxing land rent and other rent-yielding assets, not capital or wages | Shift taxes off land-rent taxation to leave it available to pay as interest to mortgage bankers | |

| Provide public infrastructure at low cost

|

Privatize infrastructure into monopolies to extract monopoly rent | |

| Reform parliaments to block rent-seeking

Avoid military spending and wars that require running into foreign debt |

Block democratic reform, by shifting control to non-elected officials

Use international organization (such as the IMF or NATO) to force neoliberal policy |

|

| Concentrate economic and social planning in the political capital. | Shift planning and resource allocation to the financial centers. | |

| Concentrate monetary policy in the national treasury | Shift monetary policy to central banks, representing private commercial banking interests. | |

| Bring prices in line with cost-value | Maximize opportunities for rent seeking via land ownership, credit and monopoly privileges | |

| Banking should be industrialized to finance tangible capital investment | Banks lend against collateral, bidding up asset prices, especially for rent-yielding assets | |

| Recycle corporate revenue is into capital investment in new means of production | Pay out revenue as dividends or use it for stock buybacks to increase stock price gains | |

| The time frame is long-term to develop products and marketing plans: M-C-M’ | The time frame is short-term, hit-and-run by financial speculation, M-M’. | |

| Industrial engineering to raise productivity by research and development and new capital investment. | Financial engineering to raise asset prices – by stock buybacks and higher dividend payouts. | |

| Focuses on long-term development of industrial capitalism as a broad economic system. | Short-term hit-and-run objectives, mainly by buying and selling assets. | |

| Economy of High Wages, recognizing that well fed, well-educated labor with leisure is more productive than low-priced “pauper” labor, and long-term employment | A race to the bottom, burning out employees and replacing them with new hires.

Mechanization of labor treats workers as easily replaceable and hence disposable. |

|

| M-C-M’ Profits are made by investing in means of production and hiring labor to produce commodities to sell at a higher price than what it costs to employ labor. | M-M’ “Capital” gains made directly by asset-price inflation | |

| Banking is industrialized, to provide credit mainly to invest in new capital formation. This increased credit tends to bid up commodity prices and hence the living wage. | Increased bank credit to finance the bidding up of housing, stocks and bonds raises the cost of housing and of buying pension income, leaving less to spend on goods and services. | |

| Supports democracy to the extent that the lower house will back industrial capital in its fight against the landlord class and other rentiers, whose revenue adds to prices without adding value. | Finance capital joins with “late” industrial capitalism to oppose pro-labor policies. It seeks to take over government, and especially central banks, to support prices for stocks, bonds, real estate and packaged bank loans gone bad and threatening banks with insolvency. | |

| Industrial capitalism is inherently nationalistic, requiring government protection and subsidy of industry. | Finance capital is cosmopolitan, seeking to prevent capital controls and impose free trade and libertarian anti-government policy. | |

| Supports a mixed economy, with government paying for infrastructure to subsidize private industry. Government works with industry and banking to create a long-term growth plan for prosperity. | Seeks to abolish government authority in all areas, so as to shift the center of planning to Wall Street and other financial centers.

The aim is to dismantle protection of labor and industry together. |

|

| Banking and credit are industrialized. | Industry is financialized, with profits used mainly to increase stock prices via stock buyback programs and dividend payouts, not new R&D or tangible investment. | |

| Favor industry and labor. | Give special tax favoritism to the finance, insurance and real estate (FIRE) sectors. | |

__________

[1]I provide the charts in The Bubble and Beyond(Dresden: 2012), Chapters 7 and 8, and Killing the Host(Dresden: 2015).

[2]“The Theory of Dynamic Economics,” Essays in Economic Theoryed. Rexford Guy Tugwell (New York: 1924), pp. 96 and 98, originally in The Publications of the University of Pennsylvania, Political Economy and Public Law Series 3:2 (whole No. 11), 1892, p. 96. Europe’s aristocratic governments developed their tax policy “at a time when the state was a mere military organization for the defense of society from foreign foes, or to gratify national feelings by aggressive wars.” Such states had a “passive” economic development policy, and their tax philosophy was not based on economic efficiency. I provide the details in “Simon Patten on Public Infrastructure and Economic Rent Capture,” American Journal of Economics and Sociology70(October 2011), pp. 873-903.

[3]George advocated a land tax, but his opposition to socialism led him to reject the value and price concepts necessary to define economic rent quantitatively. His defense of bankers and interest rendered his policy recommendations ineffective as he moved to the libertarian right wing of the political spectrum, opposing government investment but merely taxing the rent taken by privatizers – the reverse of what Patten and his pro-industrial school of economists were advocating, based on classical value and price theory.

[4]“The Theory of Dynamic Economics,” p. 98.

[5]Speech of June 24, 1877. He used Latin and said “Sanitas, Sanitatum” and translated it as “Sanitation, all is sanitation.” It was a pun on a more famous aphorism, “Vanitas, vanitatum,” “Vanity, all is vanity.”

[6]William Lazonick, “Profits Without Prosperity:Stock Buybacks Manipulate the Market and Leave Most Americans Worse Off,”Harvard Business Review, September 2014. And more recently, Lazonick and Jang-Sup Shin, Predatory Value Extraction: How the Looting of the Business Corporation Became the U.S. Norm and How Sustainable Prosperity Can Be Restored(Oxford: 2020).

[7]Joan Farre-Mensa, Roni Michaely, Martin Schmalz, “Financing Payouts,” Ross School of Business Paper No. 1263(December 1, 2020), quoted by Matt Stoller,”How to Get Rich Sabotaging Nuclear Weapons Facilities,” BIG, January 3, 2021.

[8] Eileen Appelbaum and Rosemary Batt, Private Equity at Work: When Wall Street Manages Main Street (Russell Sage: 2014). See also Eileen Appelbaum, Written Testimony before the U.S. House of RepresentativesCommittee on Financial Services, November 19, 2020.

[9]George Akerloff and Paul Romer, “Looting: The Economic Underworld of Bankruptcy for Profit,”https://www.brookings.edu/wp-content/uploads/1993/06/1993b_bpea_akerlof_romer_hall_mankiw.pdf

[10]Sheila Bair and Lawrence Goodman, “Corporate Debt ‘Relief’ Is an Economic Dud,” Wall Street Journal, January 7, 2021.

[11]Desai, Radhika. 2020.‘The Fate of Capitalism Hangs in the Balance of International Power’. Canadian Dimension, 12 October. https://canadiandimension.com/articles/view/the-fate-of-capitalism-hangs-in-the-balance-of-international-power. See also Geoffrey Gardiner, Towards True Monetarism(Dulwich: 1993) and The Evolution of Creditary Structure and Controls(London: Palgrave, 2006) and the post-Keynesian group Gang of 8 popularized the term “creditary economics” in the 1990s.

I don’t think I’m really on board with this strict separation between finance capital and industrial capital. Marx got a lot right, but one of many things he got wrong was actually buying into the emancipatory potential of capitalism. He mistakenly saw the market and its logic as some sort of quasi-autonomous, internally functioning thing with scientific laws which governed its motion (this is literal, hence he and Engels talking about “scientific socialism”). He missed that the capitalist marketplace and money itself were always already political, neither of which have any independent existence from the institutions which create them. I believe we have seen a rise in “rentier” capitalism less because it is fundamentally different than industrial capital and more because the rich and powerful long ago realized that there is no “free market” and that they could construct the market legally and politically in precisely the way which allows them to maintain and expand their wealth and power. Marx, for all his polemics against capitalism was actually too wrapped up in its logic to see this part of it. He didn’t really grasp that the supposed laws of the marketplace could be bent or broken at will be the people with the means to do so (hence, “too big to fail”), thought the laws of capitalism were something like laws of nature instead of pure fiat made by people.

That’s the mistake. At some point the elite just realized that the “free market,” far from threating them was the most effective way to maintain their control of society.

At least in Capital, I don’t see this as Marx’s mistake. It is not the dominance of Capital itself that he sees as potentially emancipatory, but the actual increase in the ability to generate surplus that it creates, which could be deployed to other ends if the system were surpassed. (And for Marx, it’s “progressive” function was already firmly in the past.)

The absolute Hellscape created for the working class, the degradation of the environment, and other disasters he saw as baked into the system. And this did not depend on whether industrial or finance capital predominated. He certainly would never have deluded himself with the belief that “the euthanasia of the rentiers” would fix things. That was left to a later economist.

I think that Marx regarded the “laws” of capitalism as different from what you seem to be calling laws.

He was of course in no position to observe the ever-accelerating tinkering with the supposed laws of the system that we’ve been witness to for many decades, but what he did see, and what he analyzed in the form of various proposals to eliminate the “bad” effects of the system while retaining it’s essential characteristics he saw as perhaps capable of altering the ways in which crises manifested but not of avoiding the crises.

This isn’t really adequately expressed, but I’m working from my little Lenovo touchscreen and am disinclined to do longer exposition until I have a keyboard available.

At the end of the 19th C. with capitalism exploiting the environment like never before the reaction in the art world was to romanticize nature. Dream-scapes of mystical nature. Followed soon by goofball tourism in model-Ts. The industrial revolution was the economic singularity at the beginning of automation. It gave us the ability to accumulate wealth in a whirlwind. But it lasted barely a century. At which point nature was no longer beautiful and mystical – it was completely trashed. So this went hand in glove with a population explosion and capitalism because it required both. Which is now totally counterproductive. In fact self-destructive. And instead of letting the whole thing implode, bringing essential resources and services to a screeching halt, we are (apparently) financializing the economy. M-C-M has become M-debt-M. At least this eliminates the ravaging of the environment at ever accelerated consumption. What we need, I submit, is M – environment – M. We need to increase our national and state legislatures by adding a new branch of lawmakers – scientists, now especially environmental scientists, but science in all its branches. And give science full political authority, along with vested financial interests. Balance sheets can be manipulated; money can be digitized; but the environment is the only thing that counts.

All this and not a word about the consequences for the world of ‘productive’ industrial capitalism. The need to produce so-called goods endlessly and in increasing quantities is destroying the planet yet the author seems to regard it as something to which a society should aspire. Capitalism itself, with its inherent drive for endless economic growth, is incompatible with a finite planet. Even some capitalists realise this and suggest, hopelessly, that we must immediately and seriously look for ways to expand beyond this planet. A piece elsewhere on this site today about Jeffrey Epstein labels him a ‘child rapist’ in a way that suggests his activities promoting capitalism were more respectable. ‘Capitalist’ should carry the same stigma. Or is the extinction of all complex life – as esteemed climate scientists are telling us we are headed for if we don’t stop this growth obsession – a less wicked end than a sex crime?

We could use more production of solar panels, wind turbines and electric transportation.

We could use an enriched working class with the wherewithal to replace their carbon sourced living standard with a green one.

This is a really good point. Just producing something doesn’t produce a net gain for society. I once had this idea that someone with a better background in economics than I have should write a long essay or a book about how the rise of advertising in the 1950s coincided with the need of industrial capitalists to create demand out of thin air for the products they were producing. When the actual need for your products doesn’t exist, we figured out how to manufacture demand as well. Up to that point, capitalism had mostly been concerned with the supply side of production but the advent of marketing, advertising, and PR was all about managing the demand/consumption side as well.

This is another way the rentier/industrial capitalist distinction breaks down. Both are beholden to the same interests.

There was a book called “from the wonderful folks who brought you pearl harbor”, which (in a light hearted way) dealt with madison ave (the series mad men was supposedly taken from this story line) and the creation of “consumers”…. in the fifties…

The real time version would be george seldes’ works… multiple books.. and he had a publication called “in fact” which dealt with the “association of national manufacturers” and how they were controlling the media of the day though advertising.

He was doing stories about the dangers of tobacco and the industry killing of all stories dealing with negative facts about tobacco, back in the forties and fifties..

A great book was “witness to a century”

It blows my mind that just about everything going on today, has been cooking for about a century… and we act like us “figuring it out” is a big deal…. we must be one smart species.

This theme gets a significant amount of space in Baran and Sweezy’s “Monopoly Capital (1966), in the chapter on the Sales Effort in particular, but also scattered elsewhere throughout the book.

au contraire. I say it’s described as part and parcel of finance capitalism. The extractive industries create a surplus of material that must then be sold (analogous is the need to have a war in order to create the need for more bullets), and the extractors get a massive land rent bonus as the resource is given to them free of charge, and they also benefit from tax advantages and land appreciation facilitated by the aforementioned finance capitalism…. How much of the bezos fortune has been acquired through selling counterfeit goods touted by fake reviews on the product quality? More junk, sold faster. delivered by an army of gig workers driving individual polluting cars and the notion that an electric or hybrid bus should be replaced by an army of uber drivers, until they don;)t need them anymore…

From the above…“The oil and mining industries likewise are notoriously exempt from income taxation on their natural-resource rents. For a long time the depletion allowance allowed them tax credit for the oil that was sold off, enabling them to buy new oil-producing properties (or whatever they wanted) with their supposed asset loss, defined as the value to recover whatever they had emptied out. There was no real loss, of course. Oil and minerals are provided by nature.”

From Buckminster Fuller’s last book ‘Critical Path’ –

“…approximately 60 percent of the employed in U.S. America are working at tasks that are not producing any life support….Which would cost society the least: to carry on as at present, trying politically to create more no-wealth producing jobs, or paying everybody handsome fellowships to stay at home and save all those million-dollar-each gallons of petroleum?”

Maybe it’s time to give the environment a breather from human ‘production’. Ecosystems have been loving COVID-19.

Excellent article!

Thank you.

It is time we boycott the FIRE sector.

I think their exists a confusion as to what constitutes- or is not included in the term – Productive industrial capitalism.

I think the term ‘Industrial’ evokes images of smoke stacks, endless pollution, misery and environmental degradation and excludes a positive side that includes polution elimination, contained systems, environmental resoration and blooming, happiness and mission, higher and more meaningfull fullfillment.

I think the term ‘Productive’ evokes images of so-called goods as being created endlessly while destroying the planet – whereas restoration of soils and environment on an industrial scale and the resultant beneficiary of goods produced for the enablement of biodiversity.

Further, a large component of the term ‘productive’ having negative connotations is a direct result of Financial capitalism’s take over and, deceptive use of terms and language – they were led by the computer revolutions use of terms and language taken from long used context and applied to their own narrow doings – See Michael Hudson’s -J is for Junk Economics.

This same de-focusing and sly re-working of definitions has left a majority of folks believing that banks use peoples savings to lend out to people trying to start a business, buy a home, or to business to increase production – and not the reality of most of it being to boost asset prices and de-regulate any type financial gambling and shicanery – . And what does it say about economics as science? where economics pretends that itself is self correcting and not entropic like about everything else, will take bad actors out of the equation of the free market, will produce good corporate citizens, and claims creative destruction without realizing that destruction applies to only those things previously created.

When has the production of good corporate citizens outweighed the destructive capacity of those produced bad corporate citizens.

There seems to be no distinction between the preditory, destructive and harmful capitalist corporation that only contributes to overhead, misery and deductive as opposed to productive – that and, those that are productive, useful and positive for all species and the planet.

Mother nature and this planet does not hold humans in as high esteem as we humans do – if you are religious – I don’t think god does either.

Sorry

For a critique of Hudson’s argument by a fellow marxist economist, JW Mason, to whom NC occasionally has linked, see:

http://jwmason.org/slackwire/has-finance-capitalism-destroyed-industrial-capitalism/

Mason is a careful and thoughtful economist, so his take is well worth reading. He points out that interest payments as a percent of GDP fluctuate with time and Fed-interest rate setting, and in fact are currently back down to roughly the same level as in 1975. I checked some FRED graphs, and this is true for both business interest payments and household interest payments.

He also points out that increases in relative financialization vs. industrialization have generally varied globally, with one area’s increase in one aspect balanced by another area’s increase in the other. And while US primary manufacturing has decreased, companies like Amazon, Walmart, and Google are still “industry”, as they produce usable consumer services (mainly logistical and distributional) that are not “financial”. Mason points out that most top fortunes in the US are still made in such “industrial” realms, not financial.

As Hudson agrees that Marx understood, Mason points out that industrial capitalists still extract “exploitative rent”, in the form of profit extracted from the labor power of workers, via the capitalists’ collective monopoly on the means of production. He feels that both industrial and financial capitalism are largely inseparable and essential (to the extractors) to the extraction of surplus value from workers.

Impressive article. Thanks for posting it, Yves.

I’m not sure I fully buy Mason’s argument in PB’s comment that Amazon, Walmart, et al are “industry”. Clearly, they’ve superseded Main St as agents to abet consumer culture, and may do so more efficiently (thus adding to GDP), but can this part of the service industry truly be labelled as “industrial”? It seems to me they’re old wine in new bottles, so isn’t it a zero sum, at least in the long run? They’ve really only made it easier for consumers to increase their indebtedness–it’s just a click away instead of a drive away–so are a more efficient way to abet the FIRE sector more than the industrial sector, especially since so much of what is on offer is now made offshore.

Further, as JS points out, we need to know how to get to some sort of sustainable economy before the whole thing collapses. Somehow the financial capitalism vs industrial capitalism conflict has to be replaced, which will require strong government and far-sighted leaders–both in short supply thanks to Neoliberalism. As many at NC have pointed out, we are now in a race between nuclear armageddon and climate armageddon. But it’s good to know where we are, and how we got here, if we are to find our way out of our present predicament.

Kilgore,

Good points. Re Walmart, etc., and the label “industrial”, Mason’s point is simply that those firms aren’t “financial”, i.e., not in the FIRE sector, and hence aren’t what Hudson says he’s upset with. Yet (claims Mason, I haven’t checked), they are the sort of firms, rather than FIRE, that comprise the dominant chunk of the wealthiest US firms, and of wealth generation in general.

Mason would agree that the problem isn’t about one type of capitalism vs. another, but about the whole inhuman, exploitative, unsustainable capitalist shebang.

One point re FIRE that neither Hudson nor Mason address is Dean Baker’s take: that much of what should rightfully be “labor’s” share of GDP doesn’t actually instead go to “capitalists” as “profit” OR to rentiers as interest or rent. It simply goes as wages/salaries to the very highest-paid (and increasingly so) laborers, as opposed to the bottom 90% of laborers. Most top professionals and managers of firms are not “owners”, hence they “work” for a living–but they get paid these days predominatly via wages and salaryies that have skyrocketed. And FIRE is indeed in this case a major offender, as Dean points out.

While one could argue that these are simply “profits by a different name”, the point is that such employees actually have no “owners” right to the salaries, unlike true owners’ rights to (all) profit. They do have a lot of cronyistic, informal power, however. Baker suggests several ways to regulate and lower their salaries, both for finance (a financial transactions tax), and for all corporations in general. This would free up money to go to the lower-paid workers and/or customers of these extractive firms.

Shareholders of public companies do not actually own the company [David Ciepley] and very few have a controlling stake either. Given the supine boards of most companies the CEOs have effectively complete control and should be considered functionally equivalent to the “capitalists” of lore. What with their options and so forth they are adept at joining the ranks of “owners” even if they started as “laborers”.

Baker has some good ideas, incremental style, but I don’t get a sense he has a big picture like Hudson. Mason quibbles over details just for the sake of it, it seems to me.

We’ve regularly referred to the landmark article by Amar Bhide, Efficient Markets, Deficient Governance, which lays out longer form how US regulations by preferring liquid markets, have created anonymous, transient, arms-length shareholders who do not exercise control over companies, and due to the need to keep strategically sensitive information confidential, are incapable of supervising them properly even if they had the power to do so.

https://hbr.org/1994/11/efficient-markets-deficient-governance