Yves here. Please welcome Jared Holst, who is graciously allowing us to syndicate some of the articles on his site. He’s started a new series on what he calls “The Bullshit Economy”: products and services that ought not exist because they are exploitative and in the end typically leave buyers worse off. His description is a tad more charitable than mine:

The series is an ongoing look at companies whose existence is predicated on poor policy and bad economics and not on solving a market need. Think payday loans, but newer.

We trust you’ll enjoy this and his future finds…well, the information and assessment, the actual products, not so much.

IBy Jared Holst, the author at Brands Mean a Lot, a weekly commentary on the ways branding impacts our lives. Each week, he explores contradictions within the way politics, products, and pop-culture are branded for us, offering insight on what’s really being said. You can follow Jared on Twitter @jarholst. Originally published at Brands Mean a Lot

For a variety of structural and political reasons, many people can’t afford to buy a home. In the first entry of The Bullshit Economy, we explore the companies which are attempting to fill the void.

The Avo Toast Cohort

We’ve touched on it before: when it comes to wealth, Millennials are nowhere close to where their Gen X or Baby Boomers parents were at their age. There are all sorts of side-effects from this dearth of wealth—lower social mobility, later retirement, higher odds of medical bankruptcy, etc. Today’s side-effect is millennials’ inability to purchase homes.

Millennials’ predicament is mostly out of their control. They face decades of flat wage growth (despite large gains in productivity), still struggle to find real work in the aftermath of the 2008 financial crisis, and relative to their predecessors, have earned more expensive college educations paid for with more expensive student debt. Because it’s easier to put avocado toast on layaway, millennials also have worse credit than older generations. Suffice to say, most millennials haven’t been able to save for a down payment on a house.

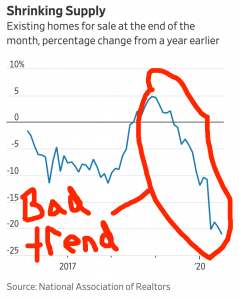

Houses are also more expensive. In Fall 2020, home price appreciation surpassed wage appreciation in 90% of national housing markets:

“The median home prices of single-family homes and condos in the third quarter are less affordable than historical averages in 63% of U.S. counties, up from 54% a year ago, according to Attom Data Solutions, a property data-base.” – Source

Yes, interest rates are low, but they’re negated by the high prices. Prices are waving goodbye to wage growth, but will millennials ever wave goodbye to their parents’ basements?

A Savior Comes Along?

There’s a gamut of structural issues preventing those living responsibly with full-time jobs from owning starter homes: lecherous student loans, stagnant wages, a paucity of savings, and poor credit. But since this is America, these policy issues are actually market opportunities.

As such, a slew of startups have found ways to lower the bar for entry into the housing market. Companies like Divvy, Flyhomes, and ZeroDown are attempting to encroach on the space traditionally held by mortgage lenders. Although each is slightly different, they have a shared goal: helping those, who by lack of funds or credit are excluded from the traditional home ownership model, own a home.

How do these companies see themselves? Let’s subject ourselves to some copy:

- Divvy: “We’re in the business of financial equality…Our team aims to break through traditional barriers to fight for the underdog.”

- Flyhomes: “Flyhomes is superpowering the way people buy homes.” (This one isn’t actually that bad).

- ZeroDown: “What used to be an integral part of the American Dream, or at least a check mark on the way to adulthood, is now well beyond reach for many of us.”

These are attempts to differentiate on nobility. Traditional mortgage lenders, real estate prices, the man, have all conspired to exclude millennials from the market. The new entrants are here to be allies.

Intuitively, if the people meant to be helped by these companies could get access to a mortgage, they would. They can’t get a mortgage because they don’t have the requisite wealth, income, credit profiles, or some combo therein.

From a lending perspective, this cohort is higher risk, which means high interest. Is it possible these startups are forgoing similar revenue to their mortgage providing forebears in pursuit of nobility? If payday lending, check cashing companies, and banks with overdraft fees and minimum deposits have taught us anything, it’s that it’s expensive to be poor. The answer is no: based on my bitter, qualitative math, whatever these companies end up charging their customers will be more expensive than a traditional mortgage.

What We Have is a Band-Aid

There are solutions to the issues preventing low-income, low-wealth buyers from home ownership which do not involve venture capital. For many small-dollar mortgages, the fixed costs of underwriting, risk assessment, and origination are greater than any potential profits, which eliminates any incentive for banks to provide them in the first place. This means low price homes go to cash buyers and investors. One remedy is the expansion of programs like the Micro Mortgage Marketplace, which:

“…will reduce fees and costs, simplify loan processing, offer underwriting flexibility, and support the purchase of affordable homes using a mortgage under $100,000.”

Other solutions are less direct. Some programs incentivize millennials to relocate to cheaper locales with more affordable homes. Tulsa Remote offers $10k in cash and free desk space for people to relocate. For many, the lower real estate prices, plus the one-time cash bonuses amount to greater purchasing power. Fueled by the pandemic-driven increase in WFH arrangements, programs such as Tulsa’s (there are several), have the potential to make home ownership more realistic for many.

These are a short term fixes. None solves the growing chasm between productivity and wages, nor ballooning inequality, nor the cost of a college education vis-à-vis inflation. Instead, all rely on a mix of private-public partnerships, charity, and the labor mobility of white-collar work, none of which is guaranteed to last.

Being for profit and funded by venture capital—which requires outsized growth by the startup for the venture investment to show a return—leaves little room for selflessness on behalf of millennials. The more the trends hindering millennials and others who cannot afford a home persist, the more people are left out of home ownership.

If payday lending, check cashing companies, and banks with overdraft fees and minimum deposits have taught us anything, it’s that it’s expensive to be poor. The answer is no: based on my

bittertruthy, anti-Panglossian, realistic, non-grifting, anti polyannish, qualitative math, whatever these companies end up charging their customers will be more expensive than a traditional mortgage.There, fixed it. Because now a days, there is no bitter math, because the whole economy is a scam. Carefully designed to perpetuate, and ever expand the great screwing. Less for more. Soylent green is just around the corner…

Sounds like a nice person…but giving bankers a hand wave on home loan lending… On affordable housing low balance loans: “the fixed costs…greater than any potential profits…eliminates any incentive to provide them”…ummm…well…moi has always been an advocate of yanking FDIC insurance for those who have a “problem” following the “law” as provided by the CRA (community reinvestment act)…not interested in stabilizing housing…no worries….just call your investor relations krewe and have them get your analysts on an earnings call and let the world know you will be all brave and stuff and will be dropping FDIC insurance as actually following that dreadful CRA thingee is just not worthy of the time and energy of the good folks on the top floor…

Or lack thereof.

https://www.cnbc.com/2019/08/31/6-us-cities-and-states-that-will-pay-you-to-move-there.html

Shelter is a basic human need. It always has been. Yet, like everything else in America, it’s distributed by a elaborate and confusing market where it becomes an “asset” that must always “appreciate.” Because that will never change, there is no solution to this problem, certainly not even more baffling and confusing methods of “financial engineering”.

I this just the new, kinder, gentler world of “sub-prime”?

The programmatic Google Ads served on this page were all for traditional home loans.

Why wouldn’t it? The general Psychographic and Demo traits of NC users is known. More interesting Neil, those traditional home loans may be following you, as you move around the internet.

I never see ads due to my ad blocker, but I disabled it just to see and my ads were all for cannabis and CBD. Which is a waste of money since I don’t use either ¯\_(ツ)_/¯

My ads are for short men’s boots, as in ankle-high boots for men, as opposed to boots for men of lesser stature.

Usually I get ads related to toys and collectibles, though its always toys and collectibles I have no interest in, but today I apparently have an ad for Goldbond. How I have been mistaken for some sort of Goldbug I truly have no idea.

https://www.thebalance.com/average-price-of-starter-home-4172916#:~:text=The%20National%20Association%20of%20Realtors,price%20of%20%24203%2C700

The National Association of Realtors (NAR) reported that the median price of homes purchased by first-time homebuyers was $215,000 in 2019. This is a 5.5% increase over the median price of $203,700 from 2018.</em

and

The median income for first-time homebuyers in 2018 was $79,400.

That’s about $1,500.00 gross weekly or $38.00 am hour.(individual or combined earnings)

Affordable entry products are a big issue–because everyone knows your home is your biggest asset and investment and a profit center and get your own boot straps…

Habitat has a model, of sorts, and there are also Land Trusts

https://www.charlotteobserver.com/news/politics-government/article237242624.html

Community land trusts promise “permanently affordable housing,” an alluring concept in cities like Seattle where rents and home prices are well above the national average. It separates ownership of the structure and land beneath it; residents purchase the home while the land trust owns the land and leases it back for a monthly fee.

https://www.deeds.com/articles/the-land-trust-approach-to-affordable-housing/

Land trusts first emerged as a form of home ownership in the United States during the civil rights movement. They were part of community-led efforts called New Communities, created by Black farmers in Georgia.

The land trust sounds a lot like the British freehold system, which they’re trying to get rid of. It may work (for some time) but I suspect some “structural flaws” will show that it’s just another knife wound to the home owner.

No one talks about the facts that you don’t need a realtor for transacting. You can deal directly with the owner, and of course you can have an attorney advise you on any points you wish. Creative solutions also might be encouraging self-financing from the owner, i.e. he’s your mortgage holder, doesn’t need a massive admin structure to pay for to service the loan. The lender gets a better rate of return than putting it in savings or carelessly managed Wall St. funds (a/k/a the Muppet Screwers). The buyer pays less and/or can pay it off sooner. More money circulating locally, which is why the FIRE sector would hate it and try to get it banned. But f— them, and do it while you can.

In other strange (and likely related news), I heard Jeff Bezos now owns 420,000 acres of land. Wonder why…

“I heard Jeff Bezos now owns 420,000 acres of land. Wonder why…”

Can a vast tract of land be treated as a depreciating asset? Maybe if it has a building on it somewhere?

If so, would be interesting to know if he has the ownership structured such that he can depreciate it down to near zero (residual value?), passing through the “losses”, at which point he flips a couple hundred thou acres with BillG, rinse and repeat.

Bezos’s is ranch land in west Texas. And I also found out that Bill Gates is the largest farm land owner now at over 200,000 acres. I know Ted Turner had owned some insane portion of Montana land.

I think the point is that they will have the area to raise animals or food to their liking and stuff everyone else. You can read F. William Engdahl’s Seeds of Destruction for all the skinny on GMOs. We already see small Indian farmholders committing suicide under crushing debt. I think they want to export that model to the rest of the world.

Is that picture of avocado toast trying to imply that Millennials themselves are toast? And after reading this, is there anybody else reminded of the mortgage brokers from “The Big Short”?

https://www.youtube.com/watch?v=PgGLgygsqus

And are NINJA loans back again?

I like the use of Gnarls Barkley’s “Crazy” in this scene. Works really well.

Our aunt and uncle used to make and eat avocado toast. They would give us some when we came on visits. And they were many decades older than the millenials.

The avocado toast is a bit of an inside (or not so inside) joke.

There was some pundit awhile back that basically said the reason Millenials can’t buy homes is because they spend all their money on much avocado toast.

Author here: it’s trying to imply that in media, millennials are scolded for spending money on Avocado toast instead of saving. Eg: https://money.cnn.com/2017/05/15/news/millennials-home-buying-avocado-toast/index.html

If only they stopped buying that, and lattes, they’d all have homes…

House prices are high BECAUSE rates are low. Asset prices are being defended to the hilt by the central banks. Financialization.

It’s difficult for first-time buyers to offer $200,000 – $300,000 for a house they don’t even like, and that will be gone in two weeks, so little comparison shopping is possible even when you can get a mortgage. At least in expensive cities this process feels like nothing but a form of high stakes gambling.

Most everybody’s wealth in the USA is the value of your real estate, which if you live outside the rust belt, has generally done well, or daresay great as an investment since anybody now alive can attest to.

If the almighty buck takes a tumble and becomes just another currency, we would see one hell of a bubble beyond imagine as people scramble to put their money in stocks or savings into something tangible with a track record.

You underestimate the rust best. Outside of super rural areas and the likes of Flint, real estate has still outpaced inflation. Combine this with the opportunity cost of forgoing rent (or receiving rent if your an investor) and the rust belt has actually done better then many places as one could buy 5 or more houses for the price of 1 on the coasts

False. My brother’s house appreciation in a mill town in Michigan has been 1.4% compounded. CPI appreciation over the same period is over 50% higher. And that’s before you include his maintenance expenses and property taxes in his cost base.

Here in Mountain Brook, the most affluent community in Alabama, with the best public schools in the state, the appreciation of my mother’s home on a .9 acre plot with excellent views, has similarly greatly lagged inflation. If you use Zillow, which is probably an over-estimate in her case (the house is a fixer-upper and I doubt it allows for that), it’s 30% below CPI inflation. If you use a more realistic valuation, it’s more like 69% less that what they would have gotten if they had invested in anything that tracked inflation.

And like the graph above shows.. there is little inventory. My county had 60% less sales in Nov 2020 compared to Nov 2019. People are bidding up whatever they see.

From Harper’s Index from the Dec 2020 issue –

Very few people young people live with their parents voluntarily so that is one hell of a lot of pissed off young people.

Then there are young people living in houses bought for them by their parents. The houses on both sides and behind mine are occupied by young unmarried males with children and the mothers of their children that were bought by their parents.

A few streets over from my street is an area of high priced houses in the low 7 figure range I call Richistan. The occupants of these houses are young couples in their late thirties and early forties often with three children that appear to be two years apart which they ferry around in six figure, six thousand pound SUVs. I have a friend who lives in the area that says most have received financial help from the parents. He lives next to one of these couples that have a pet miniature horse for the children.

pet miniature horse

Its cheaper than buying a high end breed dog. And they live 25 years. I don’t know about care costs, but you know its not unreasonable if you are already sinking money into a big enough yard.

I,ve been watching the Real Estate market in Sonoma County for 15 years and I do not see any economic basis for today’s prices.

I’m not the one who sees it, the only question most of us in the Biz have is how soon the crash will come and how fast and hard it will be.

And it isn’t just RE, it’s all of the markets.

When thing are this unstable an otherwise minor exogenous event can have major consequences.

Timing it is not easy, late summer this year?

Last time around in 2006 we held off buying a house under the same logic. But when the crash finally came, at least in our area it was just a leveling off – no substantial price cuts. People lost their homes but somehow this did not translate into lower prices since supply seems to have been controlled. So I’m not counting on a crash this time even though I think that’s what should happen. Will the govt stand by idly when the asset values of the donor class are threatened?

Around here, after the last crash, if the mortgage was held by a local or regional bank (lots are) they would use their connections to flip the house to some local rental property owner they had done business with before. Some of these guys would take the bank’s house sight unseen for more than what was owed on the mortgage by the previous owner. House next to mine was like that. So those properties never made it to market.

Inasmuch as this article is the first I’ve seen from the “Bullshit Economy”, I’d like to call people’s attention to a great book that might prove related: Bullshit Jobs, by the late [great] David Graeber. [Now you can understand that kind of research I used to like to do as an analyst in a Federal statistical agency, and why my career prospects were anything but rosy.] I believe that a principal reason why Mr. Graeber could write such a brilliant book on a key aspect of “the economy” (i.e. employment) was that he approached the study of the economy as an anthropologist would – much as Institutionalist economists do. Consequently, there’s lot of good insight into today’s Bullshit Economy in Mr. Graeber’s book.

Hi, author here. Thanks for reading! It’s funny you mention that, Graeber was a professor of mine in college and a major inspiration. The book you mention, in addition to being illuminating, has served as a platform for understanding all the needless ways companies have sought profits.

I second your opinion that it’s got great insight.

Thanks much, and I look forward to reading more of your posts. And if economics does interest you, please do check out books by John Kenneth Galbraith, the Journal of Economic Issues (the journal for Institutionalist Economists), and of course the writings of the late, great Thostein Veblen.

Which Galbraith and Veblen would you recommend for a first-timer?

The Affluent Society by Galbraith.

I’d also suggest The Original Affluent Society by Marshall Sahlins as well as Limited Wants, Unlimited Means: A Reader on Hunter-Gatherer Economics and the Environment by John Gowdy, Professor and Chair of the Department of Economics at Rensselaer Polytechnic Institute.

These will give you a much broader perspective to work from. Thinking in geologic time scales – well beyond the exceedingly narrow academic discipline of economics – is vital.

Me thinks the elephant in the room is Michael Hudson

I got the impression from the article you were picking up the gauntlet from Graeber.

Good for you.

His contributions are missed!

Jared! I appreciate you touching on real estate. For many the system feels opaque and since the revenue generated from each sale/move is massive (Brokers, Bankers, Attys, Title, Inspectors, Movers, Contractors) it makes sense that so many ‘startups’ are focused on ‘solving’ this. If any are successful they can establishing a network and then cross sell accross verticals in the transaction. Ultimately I think technology will help streamline the process and reduce overall costs but will likely lead to single industry leaders in each space that dominate the transactions and can support lower costs.

I am also wary for any companies that are looking to increase debt/leverage for any transaction. The cheap credit party will eventually have a reckoning and if history repeats itself the consumers will be on the hook.

Hi, I didn’t see any sample numbers in the article that illustrate the distance between the reality and the hype these companies publish – or what their business model is.

So I looked up Zerodown — ahh they have a rent-to(if_you_wish)-own. I had the misfortune, in terms of my financial circumstances – young just out of uni- , race-discrimination to only be able to get a rental place via a scheme like this in the late 70s. Run by the infamous slum landlords L.I. Rubin in Liverpool, UK. Doing it this way got them out of all sort of rental-laws – that was their win.

Interesting read – looking forward to seeing more of this in the near future!

My impression is there is much housing waste in the United States. Cities have abandoned houses.

Houses, warehouses, and factories…

Loving these lo-fi charts and annotations over the images. Softens the blow of the message, which is I’m fucked.

I’d like to know to what extent the venture capital behind these companies is sourced from the very industries that form the “wall of injustice” these companies purport to rectify. For the reasons stated in the article, it’s going to get tougher and tougher to keep the housing market party going, right? This could be a way for lenders, brokers, servicers, etc. to help ensure a future supply of mortgage slaves. If they can enforce more onerous and crippling terms over the life of the loan, while squeezing more actual equity from the “homeowners”, so much the better. That’s how I see this. It would be too transparent if the financial backing were the same companies that form the traditional mortgage industrial complex, with no attempt to obscure that. So what are the venture vehicles involved and where do they get their money?

The ads don’t even bother to explain what the terms are. But imagining that cheap mortgages can be had, they will have to be on cheap housing. A $100,000 house in Tulsa Oklahoma? Where there are no jobs? Right in the middle of Tornado Alley. If a good deal is ever construed to help the millennials get out of mom and dad’s basement it will have to be mutually beneficial. Venture Capital does not know the meaning of “mutually beneficial.” So there’s a bad start. But just imagining if this idea could be coordinated in a world that has reason to decentralize finance, get money back out into the greater economy, create some sort of commerce from our national corpse, and provide either a guaranteed job or income to those participating in a housing program. One where they can expect to earn a certain amount of equity and move on. It could fly if the vultures wings are clipped. That won’t be the choice of the Biden administration. I’d guess widespread cynicism and distrust will prevent this one from getting off the ground.

Leave it to startups to solve a problem by actually exacerbating it! Excellent read.

If you contract to buy a home that will have a mortgage on it, that is Home Debtorship, you are a Home Debtor. When you have paid off the mortgage, you are finally a Home Owner. For many if not most Home Debtors this never happens. (Keep in mind that the Home is still subject to being taxed, so that it is not completely and freely “owned”.)

Just another example of the language used being inadequate for the task.

Another bullshit economy created by the UK: IR35 rules are funneling contractors into umbrella companies and recruitment agencies like Hays (who got done for operating a cartel in said industry not too long ago…), who get to extract rent from contractors wages in return for nothing.

Being screwed by this myself, it looks like. Company will ’employ’ me as a contractor through an umbrella, working remotely – but won’t offer direct employment with same flexibility. I’ve a good relationship with this company and am getting help looking for other solutions, but you never know what’s going on with legal/HR departments and the politics within them – it pays to keep in mind that the employers best interests are different and often antagonistic to the best interests of those who work for them.

Feels like I’ve been caught in an inconsistent bind on the companies behalf, where the company doesn’t want to let the cat out of the bag of giving employees increased work flexibility and the opportunity for permanent work from home after the coronavirus, yet wants to have their cake and eat it with contractors who were a sort of exception to this, but now they have to indirectly employ them as second-class employees due to IR35 – exposing the inconsistency and the power they exert over workers and work conditions.

Sort of wish (but not really…) that I could be ignorant to all of the ins and outs of this, so I could just get on with it without being very annoyed and feeling screwed around. It is a very good job regardless.

What the heck is a “lecherous student loan”?

lech•er•ous:

1. given to or characterized by lechery; lustful.

2. erotically suggestive; inciting to lust.

I mean, [family-blog] student loans, sure, but I don’t think that’s quite what you meant?

Perhaps it’s more spot-on than first glance suggests given that the number of college students entering soft prostitution (i.e. sugar babies, onlyfans, etc.) to pay the bills.

I have no idea if sugar daddies and whatever the term is for women who are associated with said daddies are any more common than they used to be, but the amount of women using OnlyFans and similar sites is getting out of hand. Its obvious many of these women are not doing it for fun. And the competition is incredibly fierce, many new users end up making fairly little despite attractiveness. Often women using these services have to specialize in servicing some kind of niche fetish in order to siphon viewers away from more mainstream semi-celebrity types like Belle Delphine or whoever.

A little real estate MMT: Rethinking the Economics of Land and Housing by Josh Ryan-Collins, Toby Lloyd and Laurie Macfarlane

This is euro-centric, but it recognizes that 80% of house price inflation is based on the land price.

See also RealEstate4Ransom (Michael Hudson).

Land speculation has been an American Tradition since Washington and Jefferson.

let me argue with this bit:

Houses are also more expensive. In Fall 2020, home price appreciation surpassed wage appreciation in 90% of national housing markets:

“The median home prices of single-family homes and condos in the third quarter are less affordable than historical averages in 63% of U.S. counties, up from 54% a year ago, according to Attom Data Solutions, a property data-base.”

people don’t pay what the median price of a home is; they make monthly payments…as of November, the median monthly payment was down 10 months in a row…

caveat: i haven’t seen data since..

There’s overproduction of money, while real investments (factories, infrastructure etc.) are few (most of them are in Asia). So the overproduced money goes to inflate house prices.