Yves here. It’s disheartening to see an abuse like payday loans back in the form of a cute app with a misleading name, early paycheck, that finesses that the user owes the party who advanced the dough, including a hefty premium. But the need it fills is the same.

By Jared Holst, the author at Brands Mean a Lot, a weekly commentary on the ways branding impacts our lives. Each week, he explores contradictions within the way politics, products, and pop-culture are branded for us, offering insight on what’s really being said. You can follow Jared on Twitter @jarholst. Originally published at Brands Mean a Lot

Most things are paid for right away, labor is not. This, plus stagnating wages and a lack of free, widely available banking options, has paved the way for re-skinned versions of payday loans.

Wages Are Built Different

Money doesn’t buy you love, and a love of Doritos doesn’t buy you Doritos. To walk out of the store with them, you need to exchange money for the chips in real time—this is how most day-to-day purchases are made.

Wages, the grease that lubricates these purchases, are built different. You exchange something of value in real-time, labor, and with some exceptions, that labor is compensated just twice a month. A person works for two weeks without pay, then receives income on the final day of the two-week pay period for the previous two weeks of work: employees provide an advance on their labor at 0% financing to their employer.

Cash Flow Feels Good

Not only is this a free loan for employers, it benefits employers’ cash flow at the expense of workers. In a business sense, positive cash flow—more liquid money coming in than going out—enhances a company’s growth through enabling it to buy raw materials, pay workers, conduct R&D, invest in new machinery to grow the business, etc. It’s crucial for everyday operating costs.

People eat, go places, buy stuff, and tend to their bodies constantly. This extension of credit for employers puts people in an adverse position to pay their operating costs. Going back to our Doritos-craver, there’s no way for that same person to get gas at 0% down, 0% for the first month. Conoco wants the money now.

The First Version Sucked Also

For people who are underbanked and low-income, a cash flow impediment presents a problem. This conundrum mostly used to be exacerbated (or solved, depending on whether or not you worked for a payday loan company) by payday loans. Ostensibly, payday loans are quick-cash solutions for people who may not have access to a bank or need cash before a paycheck arrives.

Payday loans’ prevalence declined the past couple of decades due to regulation and pressure from consumer advocates. Why regulation and pressure? The loans are obscene: a study by the Consumer Financial Protection Bureau revealed that most borrowers paid more in fees than the loan itself. Meaning, if you borrow $200 for medicine, you may owe more than $400 by the time you’re through fulfilling your loan obligation in much less than a year’s time.

What Is Old Is New Again

Despite payday loans evaporating, the addressable market isn’t:

- 18.7% of households are underbanked (“household had an account at an insured institution but also obtained financial products or services outside of the banking system”.)

- 5.4% of households are unbanked.

- 1 in 3 adults report “having difficulty covering basic expenses.”

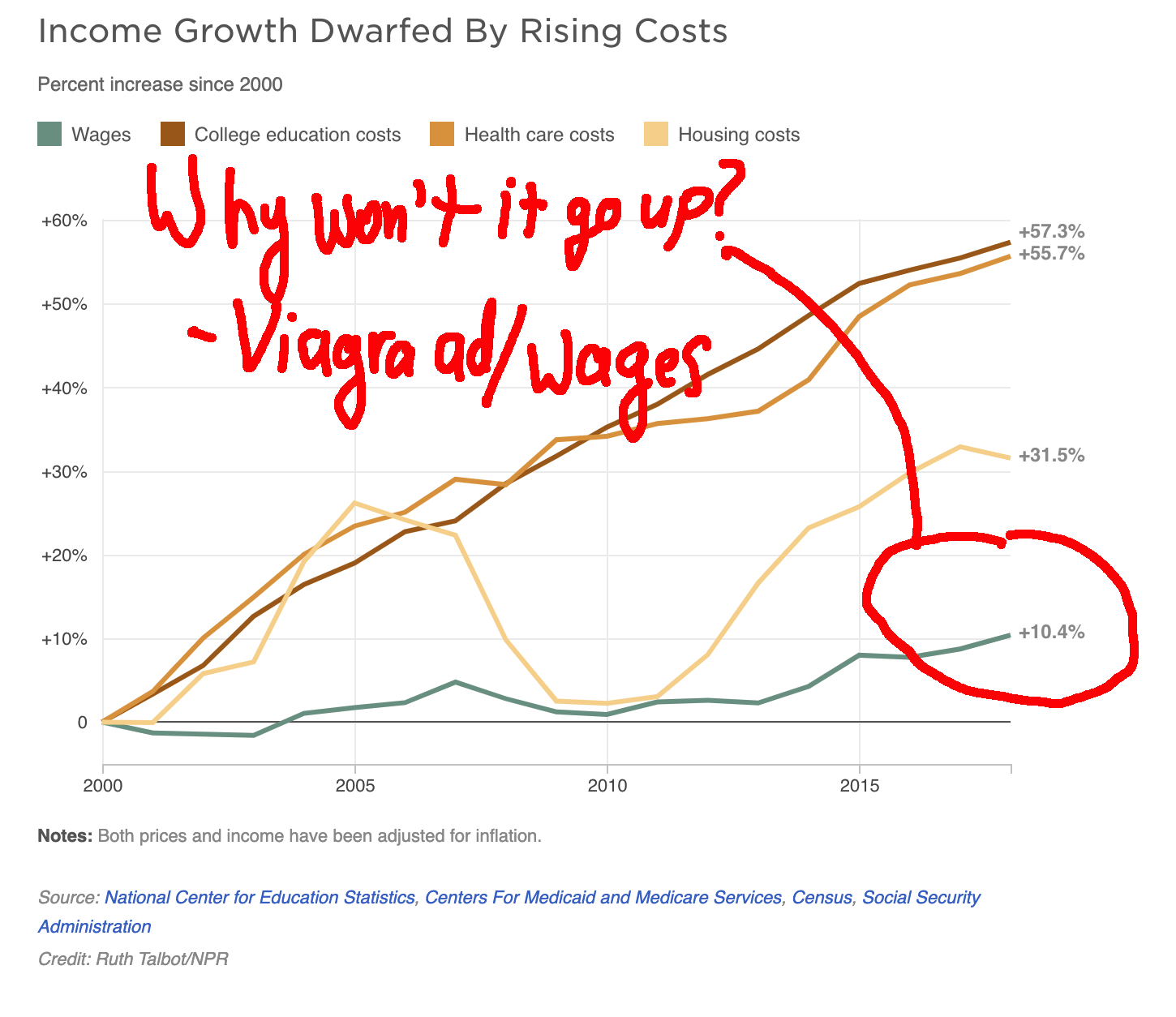

0% loans on labor, years of flat wage growth, and disproportionate costs in other major areas, has ensured the market has stayed ripe.

Source: National Center for Education Statistics, Centers For Medicaid and Medicare Services, Census, Social Security Administration Credit: Credit: Ruth Talbot/NPR

Notwithstanding their decline, the ethos of payday loans lives on in applications that allow people to access their paychecks in advance of payday: charge exorbitant amounts to those who can least afford it so that they may access their own wages in a timeframe that’s more reflective of reality. Apps such as Earnin, Dave, DailyPay, and many others give users access to their paychecks early. Each early-access app has its nuances around how paychecks are accessed and how each makes money; however, the effective interest rates charged by each mirror their payday loan forebears quite closely. Equally obscene APRs, repackaged in brightly-hued homescreen apps.

Earnin users, for instance, are prompted to pay a default 10% ‘tip’ on the amount of money they access. If they opt not to tip, they’re limited in the amount they’re able to withdraw. If a user tips $5 on a $100 advance, that comes out to a 130% APR. Earnin has received $190 million in VC funding. The ethos lives on.

Source: Nikocado Avocado

Dave gives its users access to payday advances up to $100 without interest or a credit check, provided the user agrees to the app’s terms. Similar to Earnin, users can tip to misleadingly inflate their APR. The app has additional financial features costing $1/month, which even without tipping, distend the effective APR to unreasonable levels. Dave also…

“…donates a percentage of tips to Trees for the Future, a non-profit which provides families in Sub-Saharan Africa with sustainable food sources, livestock feed, products to sell, and fuelwood through the planting of trees.”

Dave has $173 million in VC funding.

The existence of these apps isn’t any more sane than shoving a chicken bone down someone’s throat every couple of weeks, then gouging them for their CPR. They exist only because someone breathing is restricted by someone else.

From payday loans to early paycheck access applications, the wolf’s undergone an outfit change to be back en vogue. DailyPay, Earnin, and probably others are under investigation, but the circumstances that gave rise to their smorgasbord of customers persists.

I remembered Keynesian economics because that was relatively recent.

I forgot neoclassical economics was what we used before that.

Refresher course.

Mariner Eccles, FED chair 1934 – 48, observed what the capital accumulation of neoclassical economics did to the US economy in the 1920s.

“a giant suction pump had by 1929 to 1930 drawn into a few hands an increasing proportion of currently produced wealth. This served then as capital accumulations. But by taking purchasing power out of the hands of mass consumers, the savers denied themselves the kind of effective demand for their products which would justify reinvestment of the capital accumulation in new plants. In consequence as in a poker game where the chips were concentrated in fewer and fewer hands, the other fellows could stay in the game only by borrowing. When the credit ran out, the game stopped”

This is what it’s supposed to be like.

A few people have all the money and everyone else gets by on debt.

“The other fellows could stay in the game only by borrowing.” Mariner Eccles, FED chair 1934 – 48

Your wages aren’t high enough, have a Payday loan.

You need a house, have a sub-prime mortgage.

You need a car, have a sub-prime auto loan.

You need a good education, have a student loan.

Still not getting by?

Load up on credit cards.

“When the credit ran out, the game stopped” Mariner Eccles, FED chair 1934 – 48

What I have been curious about lately is the relationship between population growth and money supply.

It’s probably not economics but anthropology/sociology/psychology that underpin the fear over declining population growth, but at the same time there’s this burning desire to constrain the money supply and for austerity.

We worry about demographics, but do everything possible to exacerbate the problem.

1) Sky high housing costs

2) Student loans

3) Low wages and precarious part time jobs

4) A minimum wage specified at an hourly rate that won’t pay a living wage in a part time job

5) Both partners need to work to pay the bills

Hardly anyone should have the money to be able to start a family now.

There has been an ongoing battle between Government and the private sector.

After the 1930s, the old thinking had failed so badly that the majority were happy for Governments to take on a lot more active role.

By the 1970s, maybe things had gone a bit too far the other way.

We seem to be trying to go back to the way things used to be before WW2.

Austerity is just a way of cutting back on what the Government can do. Once those cuts are made, they hope they will be permanent.

Taking away benefits isn’t easy, they need a good reason.

“Your wages aren’t high enough, have a Payday loan.

You need a house, have a sub-prime mortgage.

You need a car, have a sub-prime auto loan.

You need a good education, have a student loan.

Still not getting by?

Load up on credit cards.”

Did you write this? I couldn’t agree more. Might use that Mariner Eccles quote to promote this piece on Twitter. Thanks for sharing!

I was just thinking of examples to use.

That’s what I came up with.

so just think, if we made credit a human right it would not carry interest… but that thought begs the question… So how does credit deserve interest now?

https://www.bankofengland.co.uk/-/media/boe/files/quarterly-bulletin/2014/money-creation-in-the-modern-economy.pdf

Money and debt come into existence together and disappear together like matter and anti-matter.

Bank loans create money and debt repayments to banks destroy money.

Bank loans create 97% of the money supply

The money supply ≈ public debt + private debt

Money and debt are like opposite sides of the same coin.

Borrowing from a bank is like borrowing your own money from the future to spend today, and the interest is the charge you pay for this service.

You spend the money today, and pay it back in the future with interest.

All the debt in the financial system, from bank credit, are claims on future spending power.

The money comes out of nothing, but does need to be repaid to balance the books at the banks.

The more risk, the higher the interest rates are to cover the risk.

With credit cards, the rates are high to cover all the defaults.

There is no collateral to repossess to cover the loss from default.

Interest is reasonable; the rate is a subject for debate.

Keeping everything running on credit can never work over the longer term.

You can’t keep shifting future spending power into today.

Another example of planned and managed equal protection abuse expressed by unequal access to the benefits of the money system.

Remember the Postal Banks? They might not have acted as loan originators, but they did help in that they provided low cost banking for the lower end of the socio-economic distribution. Taking the previous into consideration, it is no wonder the “financial elites” are trying to kill off the USPS entirely.

The schools should ideally be teaching ‘The Art of Living Well’ to the students. Instead, we get ‘How To Be a Better Cog in the Machine.’

Two things Predatory Capitalism is very good at producing are Hate and Fear.

Happily, as I have said recently on another thread, I have been seeing small Payday Loan and Title Loan storefronts closing. The ‘target population’ for these social parasites is falling below the income levels needed to support these malignant ‘service providers.’

When I was living in the Imperial Capital, I was helping an African-American woman (a highly accomplished and long-time labor lawyer) run for the City Council to represent her ward. As an economist, I was able to persuade her to include a plank of setting up neighborhood credit unions so that the poorest of the poor (who were primarily African-American themselves, with immigrants included as well) would not have to deal with the check-cashing places. In DC, the lowest form of government in terms of power – but actually thei highest form of government because of the much, much lower ratio of constituents to elected official – is the Advisory Neighborhood Commissions. So, the idea was that, as City Council Member, she would work to bring together the ANCs, the neighborhood churches, and the civic/citizens’ associations to build these neighborhood credit unions. The Democratic machine, including unions, in town did all it could to make sure that she didn’t get on to the city council.

One lesson I learned from this experience is that for people with good incomes, and that included many African-American residents of the ward, this matter was simply not important. And members of the press had their educations and jobs, so this matter was not important. And union members had their jobs, so this matter was not important. So, once again the poorest of the poor were left hanging out to dry. Is it really any wonder why people who are desperately poor and exploited then might have to turn to crime to keep a roof over their heads? Well, here’s one part of the “puzzle”.

I had to google “tipping” : “Tip yourself as a reward for working out or eating a healthy meal, by adding a few bucks to your Tip Jar. It’s Easy and Fun to Tip Yourself! Create and name a Tip Jar for your savings goal, such as new tires, a rainy day fund, or a vacation. Reward your everyday wins, like making it to the gym, by putting a few bucks in your Tip Jar.”

Tipping”dave” the loan app? There is no hope for this country.

Why am I not surprised that Andreessen/Horowitz are one of the five lead investors noted in that “$190 million” crunchbase™ link, and they look to be the largest of those lead investors. They are listed first, in non-alphabetical order, when the “Lead Investors 5” link is clicked, though I don’t have the time or internet access to absolutely verify that.

From 06/06/14 By Andrew Leonard Tech’s toxic political culture: The stealth libertarianism of Silicon Valley bigwigs – Who talks like FDR but acts like Ayn Rand? Easy: Silicon Valley’s wealthiest and most powerful people (emphasis mine):

see also, https://www.nakedcapitalism.com/2021/03/links-3-7-2021.html#comment-3518545

, for a bit more backdrop.

Absolutely revolting and amoral.

gotta run (Sandhill Road, Menlo Park, CA is not that far away from me)

Notice how whenever they put forth those thoughts, they don’t include a plan on how technological innovation will actually eradicate poverty instead of exacerbate it? Wonder why that is…

You use to have to see a real live, breathing human being at the pawn shop or the check cashing place, often behind wavy bullet proof glass. Now one can get financial ruined in the privacy of your(?) home/car/tent/sidewalk.

High tech all the way. Who says we don’t have progress anymore?

FinTech is immersed in payday lending. They give themselves clever names like “LendUP,” or “Dave,” etc., and have black and hispanic front people, but they are as predatory as any greedy institution you can imagine.

The issue of economic class is rarely discussed these days. It is thought to be less important than race. However, in modern America, economic class is the most damaging of the two.

Not surprisingly, our virtue signaling elites think a conversation that includes their wealth is uncomfortable.