JJ Jelincic has scored an important initial win in his Public Records Act suit against CalPERS. We’ve embedded the order from Judge Michael Markman below.1

Jelincic prevailed on the issue that had the potential to be most embarrassing to CalPERS, as well as the one that might pressure the giant fund to be a bit less flagrant about violating its confidentiality requirements.

As you’ll see on page 2, under “Orders and Writ,” Markman found that the CalPERS board had held an improper closed session on August 17, 2020, which was a “special” board meeting held in the wake of Ben Meng’s sudden exodus after we exposed that he had violated California conflict of interest laws by holding shares in Blackstone, and found that the only portions of the discussion that were bona fide closed session matters were two sections where California Government Code 11126 (g), which allow performance reviews, hiring and firing of CEOs and CIOs to be held in private. One has to presume these parts of the meeting related to hiring Meng’s replacement; Markman more or less says so in his analysis.

We are not going to analyze this ruling as closely as we normally might because as we’ll explain, some matters are still in play and CalPERS is just about guaranteed to appeal. Mind you, most observers expected CalPERS to appeal it if lost. Here, CalPERS lost on the most embarrassing issue, the abuse of closed session privilege, as in improperly relegating matters that are required by law to be deliberated in public to secret board discussions. Among other things, this finding is tantamount to ruling that Board President Henry Jones committed a crime, albeit one subject only to misdemeanor penalties. Since Jones no doubt relied on the guidance of supposedly trusted staff, this ruling should put Jones and the other members of the board on notice not to be so trusting.

Keep in mind that the incentive for CalPERS to appeal has almost nothing to do with its odds of prevailing. If it appeals, CalPERS can attempt to maintain that the matter is still not resolved and any nay-saying about their conduct is premature. CalPERS can also presumably stay the release of any additional portions of the closed session transcript that aren’t already public by virtue of CalPERS mistakenly posting the redacted transcript on a public section of the court’s site (see our copy of it here).

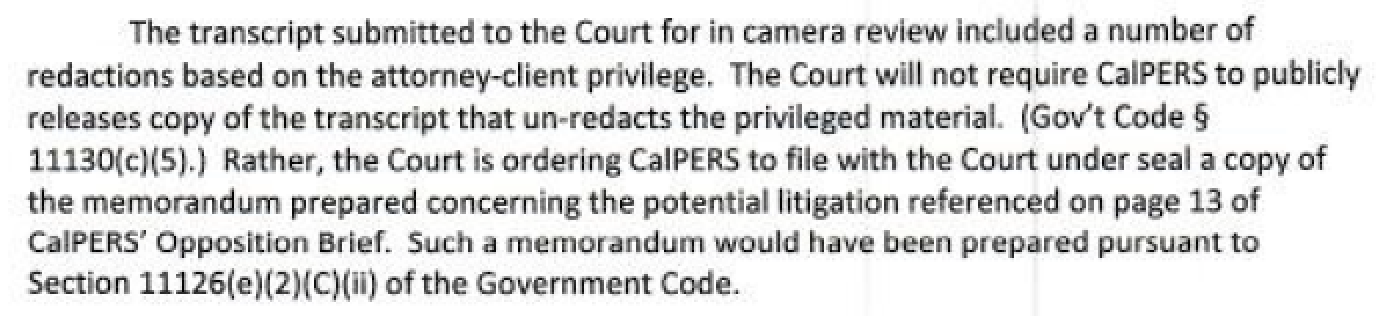

Now back to the order. It is clear that Markman still has not seen the entire closed session transcript. CalPERS has withheld some portions claiming they are attorney-client privileged. Apparently under California law, bona fide and sufficiently high stakes attorney-client privileged matters may be shielded even from in camera review.

Mind you, if there were any actual attorney-client privileged matter at issue, general counsel Matt Jacobs was required to submit a memorandum to the board as part of substantiating the basis for holding the discussion in secret. I am told that in the hearings, CalPERS has tried to maintain that such a document was created but now it can’t find it.

Markman looks like he is being awfully deferential in asking CalPERS one more time to unearth its supposedly wayward record:

Markman basically says CalPERS needs to cough up the document that has allegedly gone missing so he can assess its bona fides, or publish the entire transcript, or face sanctions. So this wrangling will continue into the new year.

Those of you who follow CalPERS might justifiably worry that this is an invitation for CalPERS to fabricate the missing memorandum. That would be risky since the document was never provided to the board and does not exist in the board’s records system, Diligent.

You will also see that Markman ruled that CalPERS did not have to disclose its writedowns of nearly $600 million in real estate assets because they fell under disclosure carveouts provided for the legislature for alternative investments (which are listed and do not include real estate) and alternative investment vehicles. Markman also accepts CalPERS keeping some supporting memoranda hidden by asserting trade secret status.

Unfortunately, this comes off as Markman falling, as judges sadly do, for assertions that saying too much about investment strategies or documents could expose the investor to harm, like an attack of evil shorts.

It’s also disconcerting to see Markman depict this ruling as the first time any court has considered the question of whether California public pension funds that invested in real estate via limited partnerships fell under the “alternative investments” confidentiality shield. A California court ruled against CalPERS on precisely this issue, in 2010, over CalPERS’ efforts to hide documents regarding a lossmaking real estate investment, Page Mill Properties. The judge ruled that real estate was a traditional investment and subject to disclosure.

The problem is that when these laws shielding private equity and closely related investments were put in place around the US in the early 2000s (ironically in response to a settlement of a CalPERS Public Records Act suit that required CalPERS to publish limited performance data about all of its private equity funds on a quarterly basis), the argument ran that companies were fragile things and too much harsh light of transparency could lead to adverse outcomes to both poor performers (they could collapse as customers and prospective employees shunned them) and high fliers (key staffers could be poached).

These concerns simply does not apply in commercial real estate. A building’s valuation is not going to suffer if its super or managing agent quits. And events that do impact value, like lease termination or tenants being evicted, become public pronto because the space is put back on the market. Similarly, sales prices are public so there’s no ability to make the private equity claim that they (somehow) need to hide their transaction prices. Buyers know, leasing agents know, lenders know, competitors know, all sorts of information: typical lease terms, who the tenants are (meaning also a good idea of how creditworthy they are), building construction type and condition. It’s a small world.

Put it another way: CalPERS and other investors were using limited partnerships and buying shares of REITs way back in the stone ages of the early 2000s. If the legislature had wanted investment in real estate to be included under alternative investments, one would have expected it to have been specifically stated, as the legislature did for private equity, venture, hedge funds, and absolute return funds. The other category is “alternative investment vehicles….through which the public investment fund invests in portfolio companies.” In the early 2000s and even now, industry professional would take “portfolio companies” to mean operating businesses. The only way a real-estate-related business might qualify is if it were a management company/service provider, say a major broker like Cushman Wakefield. But that does not appear to be the argument Markman relied upon. He bizarrely invokes the notion that the real estate fund manager CalPERS’ is deeply involved with, CIM, has set up and/or bought SPACS and then used them to acquire real estate. How does that make the real estate a “portfolio company”? And that’s before getting to the fact that it does not appear that CalPERS even claims that any of the written-down investments actually were or had been in a SPAC.

Let me briefly remind readers why the trade secret claim should have been a non-starter, and one is left wondering if Jelincic’s very competent lawyer Michael Risher spent so much time fighting the transcript/closed session issues that he didn’t brief the real estate matters as thoroughly. Markman does not seem to appreciate that nothing in private equity or real estate land could rise to the level of trade secret, which is a very high legal bar, on the level of the design of a proprietary Intel chip. The only possible type of investment in that arena that might warrant that treatment would be an exotic hedging or derivatives trading strategy that competitors had not yet emulated. Those sorts of strategies, even when successful, tend to have a very short shelf life. As we explained in 2014:

For decades, private equity (PE) firms have asserted that limited partnership agreements (LPAs), the contracts between themselves and investors, should be treated in their entirety as trade secrets, and therefore not subject to disclosure under Freedom of Information Act laws in any jurisdiction. These private equity general partners argued that the information in their contracts was so sensitive that it needed to be shielded from competitors’ eyes, otherwise their unique, critically important know-how would be appropriated and used against them. In particular, PE firms have made frequent, forceful claims that their limited partnership agreements provide valuable insight into their investment strategies. The industry took the position that these documents were as valuable to them as the formula for Coca-Cola or the schematics for Intel’s next microprocessor chip.

Now that we can look at the actual language in limited partnership agreements, we can see what any sophisticated user of legal instruments would guess: the PE firm lawyers describe the strategy in the broadest, most general terms to give the private equity fund as much latitude as possible…

When KKR claims the limited partnership agreement is a trade secret, it’s not hard to surmise that these tax games are a big part of what they are really trying to hide. But now that we can look across a series of limited partnership agreements, it’s clear that the tax strategies are highly parallel across funds. To the extent that there is anything distinctive, it’s in minor details relating to the implementation of the tax scheme, and not its objective or design…

We see more of the same, the absence of any specific or sensitive detail regarding investment strategies in this new round of limited partnership agreements. In fact, you’d expect, just like the “Use of Proceeds” section in a public securities offering, for the investment strategies to be described in the most vague and general terms possible so as to give the general partner maximum flexibility in executing his mandate.

Why don’t we toss this back to our sophisticated readers. How can anyone possibly have a real estate strategy that rose to the level of “trade secret,” save maybe the returns depending on unique illegal activity? There are no super duper confidential technical tricks for getting an information advantage.

The reason for belaboring this issue is that given the near-certainty that CalPERS’ will appeal, Jelincic and his attorney will have to respond. If they are put on the defense with respect to the finding of a closed session violation, they might as well go on the offense with respect to the real estate valuation, since the legal interpretation seems questionable. So if we are really lucky, CalPERS will wind up hoist on its appeals petard.

_____

1 The court posted 12 documents. This is the main ruling. We have not reviewed the other materials yet, another reason to stick to the big issues.

00 2021.12.20 JJJ v. CalPERS order granting in part petition for writ

The only reason I can think of why secrecy could be needed in real estate is when amassing land banks for amalgamation (i.e. when one very big site is worth more than the sum of the smaller sites) – you don’t want an existing landowner or competitor blackmailing you by purchasing blocking ownerships. I know of one major property company that got its start this way – it would buy small slivers of land off farmers, knowing the land was crucial for someone else land purchase strategy – that way they would bully their way into being partners in the project.

But I doubt this would apply to a pension fund unless they had a very specific land purchase strategy – this was not uncommon back in the 1960’s and 1970’s when big urban block redevelopments were the fashion, but I don’t think anyone does this now.

Oh, duh, you are right, an assembly could do that. But yes, that’s not the sort of thing that would be disclosed to a limited partner in location-specific detail in real time. And saying “We do assemblies” is hardly a trade secret. Every developer beyond Mom and Pop level in Manhattan tries to do that.

And not everybody bothers with secrecy! Steve Ross (my one time client) called his company The Related Companies, as in the dullest, most nondescript name possible so no one would think it was anybody. That helped in assemblies because being a nobody = lower price expectations. The guys at Related could not wrap their minds around how the Trump Organization would flounce in in its own name, assuring it would pay top dollar.

All I want for Christmas – is for CalPERS to totally blow of the judgement of that judge and then pretend that it is no big deal. And you know what? I wouldn’t put it past them.

This is good news. Kudos to Mr Jelencic for pursuing the matter.

Thanks for your continued reporting on CalPERS, PE, and pensions.

Yes! A crack in the Jacobs-Frost walking talking conspiracy at last. Kudos to JJ and NC, even as CalPERS uses our pension money to continue to block any sense of actual transparency to the beneficiaries they work against.

I’ll add my thanks to JJ and NC.

And as a no longer active Real Estate Broker I’ll state that treating any Real Estate strategy as a “Trade Secret” is a crock of fermenting crap.

Yes,there are times when you don’t want your plans to assemble certain parcels to become public knowledge, that’s been true for centuries.

Claiming that such a strategy amounts to a trade secret is laughable.

The most important factor in any Real Estate investment is timing, buy anywhere in the bottom 20% of the cycle and you are likely to do well (You can still screw up), buy within 20% of the cycle’s top and you are SOL.

Right now is,IMO, a good time to sell and a very risky time to buy.

A bit of context: CalPERS is the second-worst performing public pension fund in the entire country of the hundreds reviewed by Pensions and Investments. By a long shot.

They are now confirmed to be criminally secretive. If we ever find out what was in those blacked-out sections of the unlawful closed session, I have little doubt that it will be revealed that the CEO and Board President had been covering-up the CIO’s conflicts of interest with Blackstone (and others).

Why? Because it has become quite evident that their executives are facilitating the transfer of billions of dollars in trust fund assets to the worst players in our economy, cretins such as Trump-facilitator Stephen Schwarzman and Epstein-facilitator Leon Black. Conflicts of Interest are the most pernicious evil of our age — they are how corruption has taken-over our government from the bottom to the top.

This is far from over. Judge Markman is cueing-up to hold CalPERS and their counsel in Contempt of Court — this is the purpose of the final paragraph giving CalPERS one last chance to produce their “lost” contemporaneous legal justification for redaction or face an Order to Show Cause hearing. He has already set out the briefing schedule for February of 2022. CalPERS may attempt to seek an extraordinary writ to block him, but they would be unlikely to succeed given the blatant way they have violated the Open Meetings Law.

Pass the popcorn — and follow the money!

Parasites love legal privilege.

The local McDonalds has better management and is more competent than this group of clowns.