By Lambert Strether of Corrente.

As ObamaCare’s death spiral intensifies, with more and more edge cases demanding special treatment, the whole process reminds me of one of those black-and-white silent film comedies on airplane #FAILs, with bits of machinery flying through the air after the crash or explosion:

The only thing missing is the piano soundtrack, but of course we have the 2016 election. So there’s that.

For anybody who came in late, I’ll review the concept of a death spiral. Then I’ll briefly look at (and dismiss) the headline story, which is price rises. Then I’ll look the edge cases where a county has zero insurance carriers, or one, as well as the differing approaches to avoid getting sucked into the black hole of the death spiral taken by Minnesota, and the Federal government. Spoiler alert: I’m going to be using the word “insane” a lot. I think for good reason, and not Bill Clinton’s reasons, either. Oh, and “open enrollment” begins on November 1, just a week before Election Day! (It ends on January 31, 2017).

The ObamaCare Death Spiral

Let’s review. As we wrote earlier this year:

Economist Robert Frank explains how an unregulated health insurance market with such asymmetries would play out in the New York Times (2013):

The crux of the matter is what economists call the adverse-selection problem. Uninsured people with pre-existing conditions often face tens or even hundreds of thousands of dollars in out-of-pocket medical costs annually. If insurers charged everyone the same rate, buying coverage would be far more attractive financially for people with chronic illnesses than for healthy people. And as healthy policyholders began dropping out of the insured pool, it would become increasingly composed of sick people, forcing insurers to raise their rates. …. But higher rates make insurance even less attractive for healthy people, causing even more of them to drop out. Before long, coverage would become too expensive for almost everyone.

We then gave evidence that what Frank described was happening.[1] And the evidence for a death spiral has continued to mount all this year:

Insurers are pulling out, premiums are rising, and many customers are being left with little or no choice of insurance plans. When it was passed in 2010, President Obama and congressional Democrats hoped the Affordable Care Act would provide uninsured Americans with private health-care coverage similar to employer-sponsored plans, with federal subsidies making premiums affordable for nearly everyone. But many of the biggest providers — including Aetna, UnitedHealth, and Humana — started out with low premiums to attract customers, and have lost so much money on the program that they’re pulling out of most of the state health-care exchanges.

And as carriers pull out, we see all sorts of effects in the health insurance markets, to which we now turn.

Random Prices, Churning Markets, and More Shopping

The usual and easy narrative is that ObamaCare prices are rising dramatically; here’s a typical headline: “Obamacare premiums skyrocketing in Minnesota.” While this is true in some jurisdictions, it’s not true uniformly. The Urban Institute did a recent study seeking the average ObamaCare price increase, and concluded that was a foolish quest:

Increases in 2016 Marketplace Nongroup Premiums: There is No Meaningful National Average

With data available for all states, we find that the average change in premiums for the lowest-cost silver plan across all rating areas in all states increased a weighted average of 8.3 percent between 2015 and 2016. However, further exploration reveals that the rates of increase vary tremendously across states and across rating areas within states, with statewide averages as high as 41.8 percent in Oklahoma and as low as -12.1 percent in Indiana. We conclude that a national average rate of premium increase is a fairly meaningless statistic since different markets are having very different experiences.

In other words, our consistent contention (in “ObamaCare’s Relentless Creation of Second Class Citizens here, here, here, here, here, and here) that your ObamaCare coverage was random with respect to jurisdiction has been proven correct, empirically. If you live in County A, you go to HappyVille with a low price. If you live in County B, you go to Pain City with a high one. Allow me to deploy, for the first time, the word “insane.”

So prices are varying wildly all over the place.[2] So are policies. And as we have seen, carriers are leaving (and sometimes being replaced by others). So we expect considerable churn. In other words, just because you found a plan you could like or at least accept last year, doesn’t mean that a rational actor would choose the same plan this year. McKinsey (“2017 exchange market: Emerging pricing trends”) provides the following table:

In other words, your chance of having to do last year’s research all over again is a little bit better or worse than a coin toss. But that’s OK, because that means you can go shopping, and according to neoliberal ideology — did I mention the word “insane”? — more shopping is always good! From Time:

Even if you enrolled in 2016, you should shop around for a better program, as many are expected to change. According to an analysis by the McKinsey Center for U.S. Health System Reform, plans in the popular “silver” category that were least expensive this year will not be the most cost-effective in 2017.

But don’t worry. Shopping for health insurance takes hardly any time at all! Time (2015):

How to Pick a Health Plan in 15 Minutes or Less

And beneath the cheery headline, the following helpful advice:

Choosing a plan that your doctor accepts is a must. From there, if you’re relatively healthy and you have enough savings to cover a health care emergency, a high-deductible plan often makes sense, especially if your employer adds cash to your HSA. But if you tend to have high health care costs, you’re short on savings, or your employer isn’t adding to your HSA as an incentive, take a careful look at your potential outlay—it may be worth paying more upfront for better coverage later.

Of course, that’s insane. It shows a Versailles-level disconnect. It’s a steaming load of crap. Of course, readers know this, but for the record, Health Affairs:

Taxpayers who are on the fence about enrolling in health insurance face a complex calculation. They must weigh the cost of paying premiums to enroll in a plan against the tax they would pay for going uninsured, plus the risk that someone in their family might need medical treatment for which they could be fully liable.

The decision for those with very low incomes is likely to be easy. They are eligible for generous federal subsidies, substantially reducing the premium — in some cases, the net premium could be zero. Cost-sharing subsidies further reduce the cost of health care. That explains why most of the enrollment in insurance plans offered on the exchanges is concentrated among those with incomes just above the level of eligibility for Medicaid.

For those with higher incomes, however, it is a more difficult choice. They are often eligible for some subsidies but are still required to pay substantial premiums themselves. According to Bob Laszewski, a family of four living in Roanoke, Virginia with an income of $60,000 in 2016 would have a premium payment of $4,980 for the year for the second lowest-cost silver plan. That plan has a $5,000 deductible. That means the family could spend almost one-sixth of their pre-tax income on health costs before they received any insurance payment.

In contrast, the tax for going uninsured would be about $725. Of course, an uninsured household would face the risk of paying entirely for major medical expenses out of pocket. But that risk is limited. The ACA allows individuals to purchase insurance at least once a year without paying a premium penalty—even if they have incurred very expensive medical bills and regardless of whether they had previous coverage.

(And for those of us in System D, or who work as contractors or consultants, there’s the added stress of predicting a year’s income in advance, as well as whether we expect to be well, or sick. Insane or what?[3])

As carriers increasingly attempt to escape unprofitable markets, it’s only natural that some jurisdictions (for example, Pain City) will be left with one, or zero carriers. Now let’s look at those two edge cases.

The Case of Zero Carriers

Earlier this year, we heard about the case of Pinal County AZ (population 375,770 as of 2010), where earlier in the year zero (0) carriers had agreed to offer plans (here is a good review of the history). Apparently after some jawboning by the administration, Blue Cross/Blue Shield agreed to enter the Pinal County Market. However, zero carriers is an interesting edge case, and here’s why. From (conservative) Michael Cannon of King v. Burwell fame writing in Forbes:

[T]he ACA penalizes people if they fail to purchase insurance, unless they qualify for an exemption. The unaffordability exemption applies only if “the annual premium for the lowest cost bronze plan available in the individual market through the Exchange” in Pinal County, minus “the amount of the credit allowable under section 36B,” whether the individual enrolls in Exchange coverage or not, exceeds 8.13 percent of the individual’s household income.

You can’t do that calculation in Pinal County. The premium for the lowest-cost bronze plan in Pinal County is not $0.00. It’s not even a number. It’s the empty set.

Everybody remembers from math class that the empty set is not a number?

The “credit allowable under section 36B” is likewise the empty set. Section 36B “allow[s] as a credit…an amount equal to the premium assistance credit amount for the taxpayer.” To calculate the premium-assistance credit amount, you need to know either the premium for the health plan the taxpayer “enrolled in through an Exchange established by the State under [section] 1311,” or the premium for the “the second lowest cost silver plan” available to the taxpayer “through the same Exchange.” It would be awesome if all those premiums were $0.00. (Free health care!) But it’s not. Instead, no such premiums exist. Since there are no such premiums, there is no “required contribution.” Since there is no “required contribution,” there is no unaffordability exemption in Pinal County. Where there are no Exchange plans, there is no unaffordability exemption from the individual mandate

So, carrying the logic through to its insane conclusion, people could be penalized for not buying insurance where there is no insurance to be bought. It is true that making this argument — zero and the empty set are not both numbers! — looks, well… insane. But I prefer to think of it as insanity brought about by an insane situation (that is, by the The Patient Protection and Affordable Care Act as written. It is what it is and we are where we are).

Now, Cannon got into a beef on this point with ObamaCare supporters. Once they understand that the empty set is not a number, they urged that (a) thousands of individuals in Pinal Count could apply for a hardship exemption using a six-page form (clearly insane) and that (b) what should really happen is that the Secretary of Health and Human Services could issue a blanket exemption[4]. So, instead of thousands of Josef K’s sending in their individual six-page forms to the Castle, the Castle can issue a universal dispensation. At this point, we remember that ObamaCare is sold as a universal program. Franz Kafka would be proud.

The Case of One Carrier

Now let’s turn to the case of counties with one carrier. There are rather a lot of them, and more of them each year. From Kaiser:

We estimate that 2.3 million marketplace enrollees, or 19% of all enrollees, could have a choice of a single insurer in 2017, which is an increase of 2 million people compared to 2016. Going into marketplace open enrollment in 2016, about 303,000 enrollees (2%) had a single insurer option.

Similarly, we estimate that the number of counties with a single marketplace insurer is likely to increase, from 225 (7% of counties) in 2016 to 974 (31% of counties) in 2017.

At this point, we remember that ObamaCare was supposed to be universal (except for the counties with no insurer, but that’s OK, they can get a hardship exemption), and that neoliberal fairy dust competition was supposed to insure quality coverage at reasonable cost. Of course, when there’s only a single carrier there’s no competition (this is called giving the carrier “pricing flexibility”), so that theory goes by the boards. Here, as it turns out, there is — by which I mean “ought to be, but isn’t” — a solution, which would work for the counties with zero plans, too. From the invaluable Sarah Kliff:

There’s a section in the health care law — Sec. 1334, to be exact — that does look like the exact type of program that could help in this situation.

Sec. 1334 requires the federal government to contract with two multi-state plans, or MSPs. These MSPs would, in theory, provide coverage in all 50 states. And that would mean every Obamacare enrollee would get some choice of plan.

Building a national plan can be difficult. It means contracting with doctors all across the country. So the law intended for the MSPs to scale up over their first four years. They would have to sell in at least 60 percent of all states in their first year, 70 percent in their second year, 85 percent in the third, and 100 percent in the fourth year.

However, the Obama administration butchered its MSP implementation (assuming the MSP to be implementable), and then watered down its requirements to make it not universal:

From the get-go, the federal government only found one insurer willing to participate in the MSP program, Blue Cross Blue Shield.

And BCBS hasn’t been able to scale up its nationwide coverage as quickly as the law envisioned. In 2016, it sold MSP coverage in 32 states — fewer than half of what the law had envisioned at that point in time.

“The experience of the first three years of the program has demonstrated that providing nationwide coverage for any issuer or group of issuers is difficult to achieve,” a January 2016 memo from the Office of Personnel Management observed.

That same memo officially relaxed the rules for the MSP program: It announced that plans would not have to cover all states in 2017, as the law had envisioned. And it encouraged other health plans to apply to join the program, “whether or not they can commit to a four-year schedule for nationwide coverage.”

Insane or no? Now let’s turn to the state level.

The Case of Minnesota

Here’s how the state of Minnesota is coping with the ObamaCare death spiral:

Most of the insurers in Minnesota’s individual market also plan to limit enrollment, to avoid taking on too many customers from Blue Cross and Blue Shield of Minnesota, which is leaving the exchanges after financial losses, the state said. Taking on too many new customers could harm insurers’ finances or overwhelm the doctors and hospitals that they contract with.

Wait, what? Limit enrollment? I thought ObamaCare was supposed to be universal! And worse, who is going to set the limits? Why, the insurance companies! Does anybody really believe they won’t game the system and return to underwriting? What’s that saying: “Doing the same thing and expecting a different result”?

The Case of the Federal Government and “Discontinued Consumers”

Finally, let’s look at the Federal level. This story appeared, very briefly, and then promptly dropped off everybody’s radar screen[5]. Here we have a different use case: Customers who have been dropped because their carrier left the marketplace as a result of ObamaCare’s death spiral. And here is the administration’s plan:

Feds to pick new insurance plans for Obamacare customers losing coverage

You read that right: The Feds are going to pick a plan for you. On the bright side, you don’t have to shop (I mean, unless you actually want to know what’s in the plan):

Worried that insurers bailing out of the health law’s markets may prompt their customers to drop out, too, the Obama administration plans to steer affected policyholders to remaining insurance companies. But those consumers could get an unwelcome surprise if their new government-recommended plan isn’t what they’re used to.

The backstop was outlined in an administration document circulating among insurers and state regulators. It also calls for reaching those “discontinued consumers” with a constant stream of reminders as the health law’s 2017 sign-up season goes into full swing. Open enrollment for HealthCare.gov starts Nov. 1 and ends Jan. 31. A copy of the strategy was provided to The Associated Press.

I love “discontinued citizens consumers.” So would Franz Kafka, not to mention George Orwell. How many of The Discontinued will there be?

[Unsurprisingly –lambert] the Obama administration said it isn’t able to provide an estimate of the number of people who’ll get the notices, but independent experts say it could range from several hundred thousand to 1 million or more.

And:

Christen Linke Young, a senior administration official overseeing the health care markets, stressed that consumers are under no obligation to accept the new plan.

But this is Cass Sunstein’s “nudge theory” in action. What the administration is doing is replacing a discontinued plan, with a new default plan, and hoping that people simply accept it. The proof of that is that the scheme is opt-out, not opt in:

The federal government will choose health plans for hundreds of thousands of consumers whose insurers have left the Affordable Care Act marketplace unless those people opt out of the law’s exchanges or select plans on their own, under a new policy to make sure consumers maintain coverage in 2017.

Now, as the administration struggles to adjust to those changes, consumers may be surprised to learn that they have been placed in a health plan offered by a different insurance company, which is likely to have different doctors, benefits and drugs that are covered.

Ben Wakana, a spokesman for the Department of Health and Human Services, said consumers would not be enrolled in any plans without their consent since they would generally have to pay the first month’s premium to activate coverage.

So violating ObamaCare’s mandate to purchase a plan is the how the administration says people can opt out of the plan that was selected for them? Are they insane?

Conclusion

Recall that ObamaCare is putatively universal and depends for its success on [genuflects] competition. We’ve seen that ObamaCare is not universal for people who, because of ObamaCare’s death spiral, have the misfortune to live in Pain City, with zero carriers (and a resulting insane arithmetical calculation, topped off with an insane bureaucratic process). We’ve seen that it should be possible to create competition through the MSP program — accepting for the sake of the argument that the neoliberal faith in markets is sane — in counties with one carrier, but that the administration butchered the MSP implementation. Meanwhile, in Minnesota, we see one state propose to allow insurers to limit enrollments, which threatens a reversion to pre-ObamaCare underwriting practices, also insane. Finally, we see that the brainiacs in the administration propose to nudge — by which I mean shove — a million or so people into new plans not of their choosing when their old plans are cancelled.

Wouldn’t it make a lot more sense to move to simple, rugged, and proven single payer? I mean, if our elites were sane?

NOTES

[1] ObamaCare did provide various kludges mechanisms to mitigate against a death spiral –reinsurance, risk adjustment, and “risk corridors” — but “while these measures have funneled billions to insurers that have taken on losses to enter the market, risk corridors and reinsurance will be phased out in 2017, and risk corridors have been so far behind on payments that insurers launched a class-action lawsuit in February to seek compensation.

[2] The Urban Institute also points out, as befits its conservative heritage, that prices are lower were there are more market participants, although “causation cannot be determined.”

[3] Sarah Kliff points out that similarly complex calculations are required from individuals buying non-subsdized insurance.

[4] There seems to have been a Twitter war on this as well. So far as I can tell, the state of play is as I have described.

[5] “Everybody” including the Trump campaign, if indeed they even noticed, proving, if it needed proving, that an upraised middle finger, however ginormous, is not enough to slay.

That was a long and in-depth analysis, Lambert.

What else do you need to know?

Well Mrs. Clinton has proposed (promised? voiced support for? said words that focus-groups liked?) a medicare buy-in for people 55+. It seems to me that this is a good first step in a universal single-payer plan. Shouldn’t this also be available on the exchanges?

Medicare has been crappified by a neoliberal infestation. Also too, recall that the deal struck with big Pharma bars the government from negotiating drug prices for Part D.

The more members it has the more voters with an interest in improving it.

Don’t hold your breath on that one. I recall the term “public option” being bandied about back when Obama was campaigning for president.

Obama also campaigned that health care negotiations would be transparent…..bwahahahaha….

The only way we are getting a public option is if Democrats get control of congress while winning the presidency. A Clinton victory is very likely, a Senate victory is likely, and the last I have seen there is a 23% probability of the Dems taking the house. If Democrats do win everything, I would be willing to bet that Hillary will pass some form of single-payer healthcare. She lobbied for this over 20 years ago with universal healthcare and the majority of Americans want single-payer such as Medicare for all. Remember, that she has both a public and private opinion on certain matters like all politicians do. What is she thinking privately on this issue? My guess is a single-payer plan.

The cause of Obama not passing his original healthcare plan was due to Republicans controlling congress. Those shackles might be getting removed in a few months if there is a Democratic sweep. It is still a low probability event of happening, but who knows how it will end with the crazy election cycle we have had. We still need to tackle about 1 trillion dollars of waste in healthcare, even with a single-payer plan lowering administrative costs.

There is a reason for healthcare taking it on the chin recently, and as the chances of a democratic sweep rise, they will be under pressure. If there is a sweep, the Democrats will change Medicare Part D so they can negotiate on drugs prices. Hillary also wants us to be able to import drugs. Single-payer would decimate health insurance companies. There will be a lot of change coming if the Democrats sweep this election, so keeping a close eye on it will be prudent. Usually, any party controlling all of Washington never ends up well due to passing stupid laws so keep this in mind too.

> I would be willing to bet that Hillary will pass some form of single-payer healthcare

She disagrees, in public:

True, her private views may never be known. Also, magic sparkle ponies.

> The cause of Obama not passing his original healthcare plan was due to Republicans controlling congress

Bullshit.

> sweep

The Democrats squandered control of the Senate, the House, and the Presidency in 2009 (“squandered,” that is, for the country, not themselves). If there’s a landslide in 2016, they will squander that opportunity again; after all, just as with the banks, the same people are still in charge. As usual, policies that are good for the oligarchs but not a priority for voters — trade deals, Grand Bargain, war — will do well. Nothing else will.

What Lambert said. But also, she did not ever in her life advocate for or work towards universal or single payer healthcare. Hillarycare was another tangled, over complicated public private partnership with the insurance companies fed and groomed, just like the ACA. That’s why she froze Bernie out back then, and ever after. He met with her to try to move her towards single payer. He failed then. He failed this year. She has never been in favor of any version of socialism, and she still isn’t.

She’s a Goldwater Girl. She really is. She said as much as First Lady. (Yes, there’s an actual published quote of her reminiscing about how Goldwater still shaped her values in middle age.) She tried to get Barry Goldwater to come to dinner at the White House. She keeps showing us who she is. I don’t really understand why people are having such a hard time seeing it.

Consumer ! The board of directors of this your regional market have determined you will be discontinued , done this day October 13 2019. May Rand have mercy on your soul

Here is an article that shows exactly why health care has become so problematic in the United States:

http://2016/05/pfizer-and-its-role-in-americas.html

The pathological need for growing profits by Big Pharma at the expense of its customers is what is driving America’s health care crisis.

Stop blog-whoring. Thank you!

here are some real articles Lambert, they speak to the heart of the ‘crisis in representation” and the nature of the beast: :

http://www.truth-out.org/opinion/item/19692-obamacare-the-biggest-insurance-scam-in-history

Obamacare: The Biggest Insurance Scam in History

Wednesday, 30 October 2013 10:21 By Kevin Zeese and Margaret Flowers, Truthout | Op-Ed

(2)

And supporting this “discovery” material for the scam is some earlier original “foundation” from

Glenn Greenwald:

Published on

Friday, March 12, 2010

by Salon (common dreams)

The ‘Public Option’: Democrats’ Scam Becomes More Transparent

http://www.commondreams.org/news/2010/03/12/public-option-democrats-scam-becomes-more-transparent

(3)

And to bring it all up to date: “Congress showed health carriers the money”

“… most of us will be paying even more for health care than we do today. Profits come first in our health care system.”

Published on

Wednesday, October 12, 2016

by

HealthInsurance.org

History (of Health Insurance Greed) Repeats Itself

It doesn’t take a psychic to predict that health insurance carriers will return to the Obamacare fold in 2017 with dollar signs in their eyes.

byWendell Potter

http://www.commondreams.org/views/2016/10/12/history-health-insurance-greed-repeats-itself

“No discussion of the public option is complete without noting how

much the private health insurance industry despises it; the last thing

they want, of course, is the beginning of real competition and choice.”

Glenn Greenwald:

http://www.commondreams.org/news/2010/03/12/public-option-democrats-scam-becomes-more-transparent

You’ve done this twice now despite having been warned. One more time and we will rip out every one of you past comments. That takes less than a minute. In the meantime, I’m mangling your URLs so I don’t have to mess with this thread.

Is this to me or to Sally Snyder. Why is in reply to me?

To see who replied to who, just follow the left margins of the posts. (Yves replied to Sally Snyder)

Thank you!

The Discontinued, meet the Deplorables.

If you’re not in fact the same folks.

Pinal County, AZ, is just 25 miles away from where I sit. It’s a very Republican place, not very well off, and I guess that makes it a hotbed of, well, Deplorables.

It’s called a “basket” of deplorables, not a hotbed.

I believe there are many such basket cases throughout the US.

Yes, and they are certainly irredeemable.

Just curious: has anyone done the complex math that might show how much wealth has been transferred from ordinary people to the Medical UNsurace scammers as a result of Obamacare? That might at least inform some speculation on the outer bound of his payday after he hands the Greatest Empire off to his successor.

+10!

The winners are the PBMs (pharmacy benefits managers) and hospitals and providers (getting claims payments within 45 days of dates of service). Insurance companies are generally losing because they can no longer underwrite the rIsk. Many may appear to be “winning” but get revenues from other money making wholly owned subsidiaries. The tax payers are the biggest losers of all.

Recently has an adult child move between states. Shopping was a nightmare.

End result is we decided to go for an expensive non-marketplace policy that we are familiar with,

because better the devil that you know.

Paid for by the First National Bank of Mom and Dad.

Needless to say, our consumer spending will be subdued going forward.

Yes but your higher health care costs will be added to the country’s GDP numbers anyway. Forward Soviet!

And I guess you have to ask which geniuses who had even a passing knowledge of how insurance works designed this thing. Let’s see, we have 40 million people who have never had insurance and health care, for decades they left that growing lump untreated…um I wonder what they’ll do now that they’re covered?

And the Federal subsidy at the low end…isn’t that just the worst and most expensive possible way to nationalize health care? With none of the efficiency of actually providing a full government national health system.

England managed to put in national health in 1948 when they were absolutely flat broke, whatever else you’d say about it, it beats the pants off our system with similar outcomes for a much lower overall cost.

And if you absolutely HAD to keep private health insurers in the loop then the Netherlands approach would be better: make them offer standardized services at the same cost, which makes them compete in other ways like service, coverage, etc.

Like Churchill said “Americans can be counted on to do the right thing…after they have exhausted all of the other options”.

I beg to differ:

England managed to put in national health in 1948 when they were absolutely flat broke, whatever else you’d say about it, it beats the pants off our system with

similaroutcomes for a much lower overall cost.

1. No medical bankruptcies

2. Both infant mortality and longevity are better that the US.

3. Medics, doctors, become doctors to cure the sick. Not become wealthy, and o not have humongous student loans (until Tony Blair, the Tory).

Chronic conditions have more waiting time. Acute conditions are seen quickly.

Yep, much better than our current system. Here are the rankings:

http://www.commonwealthfund.org/publications/press-releases/2014/jun/us-health-system-ranks-last

I think this post gave me heart disease.

The Discontinued. Sounds like a Wes Craven classic, only infinitely scarier.

I have been fortunate enough to dodge this and other bullets often discussed at this site. I became Medicare eligible some years ago and my former employer, at least so far, provides a retiree Medicare supplement that caps my annual copay to an amount that wouldn’t wipe me out financially. Also, I came close but did not lose my home, no thanks not to the fraud that was HAMP. Decades ago I went to the University of California for almost no cost, which was good because my parents didn’t have much. If I thought more about it the list could go on. But the casualty rate among my fellow citizens who cannot dodge these bullets, rather like the kids I knew who went to Vietnam and came back broken or not at all, is indeed indicative of a system gone mad.

Thank you for this island of sanity.

“there’s the added stress of predicting a year’s income in advance”

Ugh, I ran into that. What a pain.

Thanks for this, Lambert. As an independent contractor who does not qualify for subsidies I am constantly revisiting the decision to leave my young family uninsured. This synopsis of where things stand allows me to better orient myself. This really is a valuable overview.

One anecdote: After having our first child a couple of weeks ago (which at $12,000 was STILL less expensive than ensuring the family for the year would have been, out of pocket costs we would have incurred included) I called my local agent to see about getting insurance. He says he is no longer writing health insurance policies. He said many others in his industry in our area are doing the same. (We live in Northeastern Louisiana).

For a bit of comic relief, the “rocket mail” crash at 0:46 in the early flight vintage films YouTube link is from Greenwood Lake, NY on Feb 23, 1936.

After the first rocket plane crashed, a second one stumbled and bounced a hundred yards or so across the state line that bisects Greenwood Lake. Then they hand-carried the letters to Hewitt NJ post office, to complete the interstate rocket mail flight.

An 0bamacare analogy would be that they just abandoned the wrecked rocket plane — mail and all — to sink to the bottom when the ice melted. And had no backup plane. “There is no Plan B.“

And the tragic aspect of the current mess is represented by the deadly crash at the 1:21 mark of the embedded video. (That clip was from the 1928 Pathé News reel of the Bonney Gull crash). All taken together, the whole current policy picture is quite the tragicomedy.

And don’t forget, those “low-income” luckies could still owe deductibles of $300-700 monthly after subsidies, because age, or smoking or because pre-existing conditions (read USING healthcare) requires a plan that starts paying costs, not a catastrophic plan.

Annnd, since low-incomers often juggle 2-3 part time incomes, they are most likely to have to report an income change to the marketplace, and risk getting their plan cancelled entirely, which has been happening since day 1 of the ACA. So enroll in a “new” plan, even if it’s the same plan, and your deductible starts all over again!

Add a generous helping of pharmacy back-billing, missing and erroneous diagnosis and treatment codes and insurance refusal for meds and procedures…with crap like this, who has time to see doctors?

There’s your goddamn consumer choice.

We live in one of those non-competitive counties in rural northern California, where it was Blue Cross or bust. At first the fiasco was stylistically complete: the two hospitals in the county willing to take county Obamacare were the free clinic in the county seat, and the rural hippie clinic that despised money. In other words, my wife and I were paying $5000 a year for admission to the only hospitals in the county that didn’t want our money!

But wait, there’s more. Because their scam was so brazen, Blue Cross was forced to negotiate with actual non-metropolitan hospitals. Then we learned that our Obamacare Blue Cross wasn’t actual Blue Cross, and that many to most decent care providers on the North Coast (except the truly decent ones who despise money) still opted out of taking Obamacare, because reimbursements are lower than from traditional Blue Cross. Now when I get a referral, the clinic sets me up with a specialist appointment, which I’ve learned to promptly call the front office of, and ask if they take Obamacare. They don’t. So I call my referring clinic, explain why I need another referral, ask if they can screen for specialists who accept mandated coverage, and of course they say of course, and the next two referrals don’t take Obamacare either–and it’s my job, of course, to de-select them. Life was so much simpler when they just threw me out of operating rooms for not having insurance, and billed me for getting ‘stabilized’, (though getting thrown out in one’s underwear is, in my experience, destabilizing) because throwing me out would be illegal . . .

I left my job this year to start my own business in Maricopa County, Arizona. I have an 18 month COBRA coverage period to figure this out.

I tried to start looking at available plans last month, but there is apparently no way to find out what next year’s plans will look like until open enrollment begins in November. From what I can tell based on last year’s plans, the networks are narrow and the coverage is terrible. Even the supposedly good plans have things like $300 per day hospital co-pays.

I see no reason to give any Democrat credit for good faith in passing this monstrosity. The Democrats are both stupid and evil, just like the Republicans.

Plan premiums going up nearly 40% between 2016 and 2017. Deductible also going up. Out of pocket max also going up. So far, not sure about anything else but nothing ever goes down.

I hate, hate, hate American health care. I treat the entire industry as if it were a criminal enterprise always trying to pick my pocket while not caring about the product or services it provides. If it wasn’t for the fear of malpractice suits, I doubt anyone in health care would care about health at all.

I am disgusted with the entire thing. If we do not get single payer to crack apart this criminal enterprise and reduce costs to what they are in other countries (about half), we are toast.

In this litany of complaints about insurance and government, there is too little talk about the price gouging from providers. That is where, in their secretive (prices? where?) and complicated and protected enclave they dream up how to charge $150 for something you can buy at Walgreens for $1.

Insurance companies are not good actors but providers are much, much worse.

I generally vote straight Dem ticket even though I am an independent but I can understand the anger of the Trumpettes. The future doesn’t look particularly good.

Couple of thoughts: the problem isn’t (just) with the cost increases — the plans were all unaffordable to begin with. Bronze plans had $6,000+ deductibles from day one.

And the random nature of happyville/pain city dispersion is a great divide-and-conquer tactic. Get the people who’ve benefited from the program to fight with the people who’ve been screwed by it.

HealthCare for all, health insurance is the problem.

Health insurance isn’t the only problem. Doctors, hospitals and Big Pharma set their own prices without constraints. A National Health Program needs to control costs along with designing means to pay them.

But doctors are typically graduating with $200 thousand-plus in debt. Often more. How can they afford to not set their prices high?

Which in turn means that if you want to fix the U.S. medical-industrial complex you’d have to simultaneously fix the U.S. academic-industrial complex.

And so on. To be sure, nobody in positions of power does currently want to fix anything; anybody who seriously tries will likely get crushed. But really the whole U.S. system is one big growing web of unsustainable neoliberal rapacity.

So finally, whether those in the top 10 percent admit it to themselves or not, they’re functioning on the same IBGYBG basis as Wall Street — except inasmuch as things will not end well within their working lifetimes, they’ll have nowhere to run when the failure cascade really hits.

Exactly! And you forgot to mention how the medical guild works to limit how many practitioners there are and limits the practice of pharmacists and nurses who might perform — probably better perform many of the treatments and diagnostics medical doctors by law withhold to their own practice. And much much more which drives up costs and lessens the health of our country.

Doctors are slowly but surely losing the war on exclusivity of treatment. One can go to CVS to deal with minor maladies and actually get scripts from a Nurse Practioner/Physicians assistant. Physicians are being outflanked by organized money and the only well paid positions left will soon be surgery and other highly specialized fields. Heaven help you if you’re just a GP.

Right.

Not to mention the big scam thanks to Rockefeller et al that created the modern medical industry. Great documentary (about oil but also about medicine, education, etc.) by James Corbett.

“…unaffordable to begin with” Exactly.

The decision to automatically enroll individuals in another plan is absolutely ridiculous. It’s hard to even comprehend how the federal government could conclude that this was either a valuable use of government time, or permitted based on the existing statute. I think this must have been a plan developed by the Trial Lawyers Association of America.

Ask Wells CEO Stumpf where this leads to.

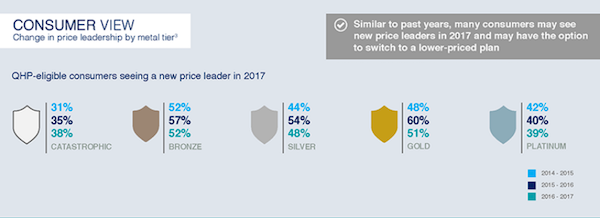

The consumer’s view: Platinum, Gold, Silver, Bronze, Lead

You might want to add a “Radioactive Wastes” plan after Lead.

It’s alchemy come true: the insurance industry turns lead into gold.

And, with a $0 deductible*, the Emanuel Plan.

* If you choose the Potter’s Field option.

Lambert and all, I am so sorry to read these stories. I live in Canada. We have real single-payer, administered through our provinces (similar to states) to Federally-mandated standards. I won’t say it couldn’t be improved. Prescriptions, dental, much ophthalmology, most chiro and naturo are not covered in my province, but true story (stop me if you’ve heard this before…)

I broke my 5th metatarsal in 1983 — approx, was running for a bus, fell off my platform shoe, so that era. I limped into the hospital, they Xrayed me, put on a cast and sent me home, with dates for follow-up. No charge for anything. I called my mom in the US, “Funniest thing happened to me today, Mom…” and told her the story. Concerned mom, “Do you need money?” Perplexed me, “What for?”

People, this is medical care in a civilized country. If you ski, scuba dive, go-kart or jump out of airplanes for fun, do BMX, fall of a fashion object, nobody cares — you are covered. Diabetes in family? Nobody here cares. Alcoholic? Nobody here cares. History of cardiac, insanity, drug use, incarceration, any damn thing? Nobody here cares, except for *medical* purposes, as in helping get your treatment right.

US-ians keep acting like single-payer is uncharted territory. Well, we in Canada are used to being considered America’s attic, but really, it works well. Oh, and insurance companies are doing just fine here too — they cover the things that our provincial health care programs do not, such as life, dental, long and short term disability, difference betw ward and semi-private (not much diff these days, std ‘wards’ are 4 in a room), prescriptions, psychotherapists, therapeutic massage, eyeglasses — hey, all those things that are really nice to have but don’t ever cost megabucks like ‘real’ medical coverage can. So InsCo’s say, what’s not to like?

My wife’s Obamacare costs us $800/month.

What’s to like is the nearly $10,000/year the insurance companies take.

My Medicare is $142/month.

Trump finally jumped the shark when he called Canadian healthcare a disaster. Clinton and Trump. What’s your flavor of neoliberal?

Removing state boundaries to stimulate competition as a solution demonstrates no comprehension of the reality.

It reminds me of previous primary repub presidental candidate Herman Cain’s (pizza restaurant CEO) solution that when one is sick/injured requiring hospitalization they should ‘shop around’ create competition and, while likely undiagnosed and impaired, get hospitals to quote the cost of proceedures.

Breathtaking absurdity…..

Funny question. I wonder what healthcare costs will be when we’re all dealing with the nuclear fallout we got from electing Hillary.

Go long on potassium iodide futures.

Re your medicare current payment, don’t worry — Hillary’s People will “fix” that, along with your Social Security…

prescriptions are not covered in your province? not a big deal, right, because prescription prices are controlled and kept not significant enough to break one’s personal bank?

here, a drug can cost more than a person’s annual salary.

Not sure how much Canada can escape the gouging on the newest drugs. However, in Australia, the Therapeutic Goods Administration would make a really rigorous review of the various drugs based on research data. They regularly limited their buying to older versions/treatments because the newer ones had vastly higher prices with little or even no improvement in efficacy. Many “new drugs” in the US are merely minor reformulations like extended release (so you take one pill a day rather than one three time a day) but those allow the drug makers to extend their patent lives and increase prices.

NC had a bit recently on how the “Miracle Cure” antivirals for “treating and curing” Hepatitis C apparently do nothing of the sort. (“Virus not findable in blood” is not “free of the disease.”) For the ordinary mope, the medication is (maybe fortuitously?) unavailable, unless they’ve got “UNsurance” or a spare $80k in the piggy bank. And if they don’t fit the narrow patient profile which the drug is marketed to.

However, if one is a veteran entitled to VA health care (note: this is not “medical UNsurance” but, God help us, Socialized Medicine) who happens to have acquired Hep C somehow, often by exposure in some foreign land, one gets the $80,000 course of “new, Magical” antiviral treatment for either $0 or $8 or $9 a month. http://www.baypines.va.gov/features/20161012.asp This is how “socialized medicine” ought to work, with the caveat that for-profit Blockbuster, Wallet-Buster drugs that are marketed based on essentially fraudulent “evidence,” with supine complicity by the “regulatory agencies,” ought to be excluded and stamped out. Along with the rest of the neoliberal terrorism.

Because it would be nice if people got in the habit of calling the Bezzle what it is: UNsurance. As a nurse, I spent a quarter or more of my work day trying to overcome the “presumption against coverage” and “denial of service” front-offices of the UNsurance companies that under ACA and other privatized medical treatment entities are “providing access to health (sic, should be “medical treatment”) UNsurance.”

UNsurance, because the “policyholder” is UNsure if their needed medications will be “on formulary” and in the same “tier” from this week to next. UNsurance because they are UNsure whether their accustomed provider will be “in network” or “on plan” this week or next, or whether the massive crushing bureaucracy that privatizing all this entails, coupled with the transfer of wealth inward and upward to corporate rulers and interests, has just driven their doctors and nurses out of the professions altogether. In the same vein, UNsure whether their providers have declined to sign on to the ‘adhesion contracts’ that privatized UNsurance corps present them with. UNsure where their “individually identifiable personal private medical information” that goes inexorably into all those Electronic Medical Records that turn out to be about LOOTING, not improving care, is collected, and who it is sold to, as part of “big data” that also enriches the few at the expense of the many. UNsure whether the treatments and procedures and specialists they need, NEED, not “want,” access to, are covered now, or will be next week. UNsure what their “deductibles” and “co-pays” and clawbacks and reverse subsidies and other surprises will be, today or going forward. PRETTY SURE that “medical bankruptcy” is still a very serious likelihood in the event of any serious medical problem. And now, after all the BS about “choice” and “competition,” UNsure why they are forced into a contractual relationship with an “UNsurance provider” most definitely not of their choosing.

From Wiki, a snippet: “Bruce Vladeck, director of the Health Care Financing Administration in the Clinton administration, has argued that lobbyists have changed the Medicare program “from one that provides a legal entitlement to beneficiaries to one that provides a de facto political entitlement to providers.” https://en.wikipedia.org/wiki/Medicare_%28United_States%29

My wife recently had the $80K Hep C treatment, had tested positive for about 20 years. Her Medicare coverage through Cigna found two different organizations that paid about $60K off the top, Cigna the balance. Out of pocket for her $0.00. Tested clear at 8 weeks into the 12 week protocol. I think the foundations were linked to the drug manufacturers, the little feel good part of their raping the rest of us.

I live in San Jose, CA and just received my Covered California renewal yesterday. My Blue Shield monthly premium is going from $707 to $909 – a 29% increase. From 2014 to 2016, my premium rose by 35%, although part of this was due to an age bracket change. I would love to switch insurers, but the large system where I get my fine medical care only accepts Blue Shield under Covered California. Also, as of last year, I can no longer use Stanford Medical Center and must instead go to UCSF in San Francisco, which is 50 miles from here!

Awful. Just awful.

I too have had some bad luck. Most recently, a call from my 24 year old son, on my work policy, thanks Obama, saying he did not have time to explain and that the EMT’s needed to know which hospital to take him to. My mind explodes. I stifle my need to understand what the hell is going on, and in just an instant I focus on his question, realize my company had recently changed coverage, realize I have no f-ing idea what hospitals may or may not be in my network, get pissed I don’t know the answer he needs, get pissed I am even having to f-ing think about it, and after that instant my son says: never mind, the EMT says it’s a level 1 trauma and there is only one hospital they can take me to (gives name) and he hangs up.

No where else on the planet do parents have to be subjected to this, and worse. The American system is barbaric. It is designed to inflict emotional and financial pain on all of us just to maximize profits of those at the top of this industry.

From just the few poster’s stories here, realize how many hours and how much stress our current system inflicts on the people in this country. Someone needs to put a price on that. The millions and millions of hours wasted trying to navigate the worst system on the planet, and the diminishing of the quality of life for hundreds of millions of people for the sole purpose of directing more money to the men who control for profit medicine. What is the value of our lost time, the cost of the emotional pain and suffering inflicted on all of us, in total? Now realize that Obama doesn’t speak about this, and neither does anyone else it seems.

Our stress, emotional pain, wasted time, abuse suffered, fear, confusion and helplessness is inflicted solely to increase the creature comforts of those at the top. So when your wife breaks down after spending a day she had to take off work trying to reconcile dozens of bills from a multitude of sources, trying to figure out what is covered and what we should pay for each, spending hours on the phone trying to understand what exactly their service codes are for and why none of the numbers they ask her for appear anywhere on our paperwork, tries to figure out what it is going to cost us and can we afford it, and then breaks down in tears because she doesn’t know a damn thing more than when she started the day, so when that happens remind yourself that everything she is being put through is being done so someone somewhere can enjoy a bottle of fine wine, add to their art collection or travel on their private jet to a destination of their choosing, all without ever having to give cost a thought.

And while I appreciate the fine work Lambert has done here, on this article, my God, at what point will this country rise up and say enough. F*cking enough. This is insane. The toll they are taking in our time and lives is not even in their equations. THEY. DO. NOT. CARE. Well, my time is worth something to me. Peace of mind is worth something to me. Less stress is worth something to me. And if you add up what I think all that is worth and multiply it by over a couple hundred million you would think that someone in charge would care.

Please Lambert, we already know the United States has the most complex health care system in the world, and we know it is the most expensive in terms of dollars, but why is there no measure of the loss and harm it inflicts on our society, something that does not exist anywhere else in the world. If we are to be able able to make a true comparison of cost, the full cost, apples to apples, shouldn’t there also be some quantitative expense for what we sacrifice and endure that no other country does? Our leaders have proven they do not care about our time wasted or anything else the systems does to our lives, only money. Isn’t there some way to put a price tag on the toll we pay in our lives so at least the actual financial cost of our shitty system is on the table?

Absolutely agree.

Hope you don’t mind a little dark humor.

I can hear the health care insurance companies’ new pitch for new products and services now.

Insurer advert:

For the low monthly rate of $150.00 you can have peace of mind knowing that we will make all your health insurance choices for you. No longer will you have to worry about making the rite choice…..we will make a choice for you. THAT’S RITE…no more messy websites, documents, contracts, exclusions and choice to worry about.

Just pay us $150.00 per month after signing our liability waiver and power of attorney affidavit and we will choose for you. To maintain this service ensure that you pay any expenses and bills from our selected carrier.

WE GUARANTEE THAT WE WILL SAVE YOU $150.00 a month by the choice in plans we provide you as compared to the most expensive plans provided in the market or by us.

Call know for peace of mind.

We earn money the old fashioned way so you can save …..we work hard at every swindle we do!!

Now that’s a value you can open your bank vaulet for us with.

if one actually added up the cost in stress alone (not even including time spent or other factors), which causes, exacerbates, and prolongs health problems across the board, it could be a figure beyond the estimated costs IN HEALTH CARE of mass tobacco and sugar consumption combined.

I hope your son was OK.

I’ll add to your chorus about cruel health care. My mother was babysitting my 2 year old daughter, and called me at work to tell me that my daughter hurt her arm. My mom’s got her crying in the backseat, but wants to confirm which urgent care to take her to as we had switched health insurance companies that month. I get off the phone with her and call the insurance company to figure it out. Turns out the clinic we used to go to is no longer covered. I call my mom back and tell her that she needs to take her to a different urgent care center. Meanwhile, my mom has been telling my 2 year old that they’re going to the doctor and the doctor will make it all better. Mom finds out she can’t use that clinic, and gets my daughter back in the car to go to the clinic on the other side of town. And now my daughter’s screaming, “no, want doctor, want doctor.” Turns out she had a dislocated elbow, and it was fixed very quickly once she actually got to see a doctor.

One more story…a friend’s 6 year old daughter was visiting and got bitten in the face by a dog near her eye. We took her to the ER, and the insurance refused to pay anything because they said she should have gone to the urgent care clinic in their home state 4 hours away. So again, they’re supposed to take a screaming and hysterical kid for a 4 hour car ride at 8 o’clock at night so the “right” doctor can fix it.

And even if you get to the right place, there’s no deciphering the bills, even if you call for an explanation. I got dinged on my credit report because I didn’t pay a bill that was for the exact same amount, for the same day, three different times (i.e. $94.27, $94.27, $94.27). I called the collection people back to say that it’s a mistake, I already paid it. They say they don’t have any details about the bill, can’t do anything, and to call the clinic. I call the clinic, and they say that can’t tell me what it’s for because it was sent to collections. I ended up paying the bill yet again. And…I got a refund check from the clinic almost 2 years after my daughter was born, saying that it had accidentally over billed me and had recently discovered the error. They can’t tell me why or how it happened, of course, but how much do you want to bet it’s wrapped up with the bill that I eventually gave up and paid, and is now listed on my credit report?

It all makes me livid. This health “care” system is a total sham.

Sue in small claims court. If enough people do this, things might improve. Also, what about a class action against the insurer on a contingency basis? Sic hungry lawyers on the insurance companies.

So well said. Our so-called “leaders” really don’t care about the rest of us at all. They are a bunch of sociopathic narcissists who seriously believe that their credentials make them special. The suffering of others is invisible to a person who never developed empathy.

I live in Cali. The Medicaid expansion literally saved my life. Everyone should have the same access to high-quality health care from committed practitioners that I did when I needed it most.

#SinglePayerNow

Another year, another signup. I wonder if the brokers’ hearts are in it anymore, faced with this downpour of health companies looking out for their profits/shareholders first and not people. Has there been any word on the status of what I’m beginning to call the “Pain City Panini Press” where those folks who have employer-based plans start to suffer due to the Cadillac Tax?

Other than a piece from early this year/late last year, everything has been quiet. I think that part of it is because of the election, which makes me wish for an election every year, but we can’t be so lucky.

your analysis and comments on this subject are spot as they have been since you started covering this topic. One of the only sources of accurate information I know of on this topic. I can speak to this because I have been in the individual insurance market since 2009 and Obamacare has been a disaster from my point of view. I can’t even think about it without my blood boiling over.

There is one escape. File an “exemption from withholding”. This means you think that your pay will be so low that you won’t owe any federal taxes. Not farfetched for people in Pinal County. Nothing but Social Security and disability is withheld from hourly pay.

At the end of the year the taxpayer then sends in whatever they owe to the IRS, if anything, instead of begging to get back their own money withheld through withholding back, after taxes are collected.

AFAIK, withholding refunds to taxpayers is the only way that the IRS can penalize people who refuse to buy a defective product: forced payments to private insurance corporations in exchange for a lousy product.

Let the government declare that forced extortionate payments to private companies is a “tax” and go after people to collect. That will help debunk the idea that Obamacareless is “health insurance.”

“Buyers Strike Until After The Election”

Praise Lambert for continually hammering on this injustice.

Insurance Is Insane.

Why haven’t those managers of ObamaCare just copied the system installed by the Pinochet dictatorship in Chile? It has been working uninterrupted for more than, what, 30 yrs? It’s based on the same concept of private insurers and competition, metal-named plans and contracts with doctors.

The system is supplemented with a public, cheaper (to the consumer) option of longer waiting times for the lower deciles of the income distribution, and some technicians in government offices calculate how much unfunded the public option needs to be in order to keep the higher deciles in the private system, otherwise they would move en masse to the public option.

When I left that country many years ago private insurers were among the most profitable businesses in the country, and poor people were starting to have dental coverage in the public option and did not have to wait more than a few months for, say, a glaucoma operation, and when the operation actually happened the medical service was good. This is what they told me.

There were other issues in the private system, such as doctors increasing the number of unnecessary examinations and delaying operations to the night time so they could charge more to the insurers and the customer, but I considered those just annoying frictions.

When Obamacare started and was described in this blog I thought this is just the Chilean system plus a website, but now I can see that it is less stable, less efficient, less sustainable than the Chilean system.

the goal is collapse and it can be done everywhere so as to force on US single payer whatever that means since insurance means shared risk to mitigate individual losses.

+1 “the goal is collapse … so as to force … single payer… ”

This has been fairly obvious from the get. Obamacare as currently constituted was never meant to endure. It’s a stop-gap at best.

We have several putative single payer systems already, each tailored to specific patient constituencies, and they provide relatively low cost, relatively accessible health care to their constituencies with relatively little hassle. Any of them or all of them could be expanded to provide essentially universal coverage in a relatively short time.

I think that’s been the goal all along, but in the meantime the insurance cartel was given a license to print money for themselves — perhaps as a bribe to get them out of the picture in the by and bye.

Transition away from private insurance to some variety of single payer basically requires the collapse of the for-profit private insurance model. That seems to be nigh.

The for-profit model of medicine and medical insurance is too-big-to-fail. The Fed will simply print more quatloos to protect the GDP and the politicians. Banks are not the only too-big-to-fail.

People want free and effective medical care, not free and effective medical insurance … though the second would accomplish the first. This is the death spiral of America, not just the medical business.

Thanks again for the excellent coverage of our crapified sickcare system.

A couple of things puzzled me:

First, I think the sentence that starts “Once they understand that zero is not a number” should be “Once they understand that the empty set is not a number” — unless I misunderstood something.

Also, I’m probably misunderstanding something in this quote from the Sarah Kliff article: “In 2016, it sold MSP coverage in 32 states — fewer than half of what the law had envisioned at that point in time.” Wouldn’t that imply that there are more than 64 states?

Re: “Mrs. Clinton has proposed…a medicare buy-in for people 55+.”

Not a good idea. Generally, only poor risk (high medical cost) folks would opt for this. Healthy patients would stick with lower cost private insurance. A high risk, high cost pool would be created within Medicare blunting universality and eventually raising Medicare costs for all.

Thanks for this post. It was informative and your snarkyness is very funny. Maybe one day people will gravitate to single payer.