Yves here. With this the last week of Bernanke’s tenure as Fed chairman, it will be necessary to brace yourself for a barrage of unwarranted encomiums. Steve Keen provides a useful counterpoint, that Bernanke failed even in his own terms.

By Steve Keen, a professional economist, long time critic of conventional economic thought, and author of Debunking Economics. Originally published at Steve Keen’s Debtwatch

On January 31, we will bid goodbye to chairman Ben Bernanke and say hello to chairman Janet Yellen. Most commentary has focused on what Yellen’s ascendancy might mean for the Federal Reserve and the US economy, but today I’d like to consider how Bernanke’s legacy might he be regarded in future years — say, 70 years after the crisis we’re in now.

It certainly won’t be as he expected it to be before he took on the job of Fed chairman in February 2006. In the worst case scenario, he will be blamed for causing the ‘Great Recession’, just as he blamed his predecessors for causing the Great Depression.

His finger-pointing doesn’t get any more blatant than his closing remarks in his speech in praise of Milton Friedman at the latter’s 90th birthday gabfest back in 2002:

“Let me end my talk by abusing slightly my status as an official representative of the Federal Reserve. I would like to say to Milton and Anna: Regarding the Great Depression. You’re right, we did it. We’re very sorry. But thanks to you, we won’t do it again.”

Of course, Bernanke got the job he’ll soon vacate because he was perceived as the Hercule Poirot of economics, whose brilliant sleuthing solved the ‘Whodunnit?’ of the Great Depression. But a closer look (both at his sleuthing and his performance in office) reveals him to have been more of an Inspector Clouseau, whose successes, as Wikipedia notes, emanated from “frequently pursuing an idiotic theory and solving the case only by sheer, improbable luck”.

That of course is unfair, but then so too was Bernanke’s treatment of his predecessors.

Bernanke took them to task for letting the growth of the money supply (specifically, the level of M1, which largely consists of currency held by the public plus cheque accounts) fall to zero prior to the Great Depression, and then allowing it to go negative during the Great Depression itself:

“The monetary data for the United States are quite remarkable, and tend to underscore the stinging critique of the Fed’s policy choices by [Milton] Friedman and [Anna] Schwartz… US nominal money growth was precisely zero between 1928:IV and 1929:IV…

“The year 1930 was even worse in this respect: between 1929:IV and 1930:IV, nominal money in the United States fell by almost 6 [per cent].. The proximate cause of this decline in M1 was continued contraction in the ratio of base to reserves, which reinforced rather than offset declines in the money multiplier. This … locates much of the blame for the early (pre-1931) slowdown in world monetary aggregates with the Federal Reserve.”

That’s the Poirot-sounding expose of the culprit, but how does the evidence stack up?

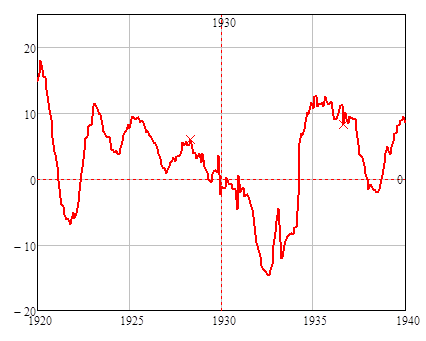

Well, yes there was indeed zero growth of M1 (in nominal terms) in 1930, and an extended period where it fell during the Great Depression itself (see Figure 1). So there’s smoke emanating from the gun.

Figure 1: Change in M1 from 1920 to 1940

But there are two flaws in this sleuthing:

Firstly, if Ben had truly learned from both his analysis of the data and ‘Milton and Anna’, then you’d think that surely he would have ensured that the rate of growth of M1 never dropped to or below zero, wouldn’t you?

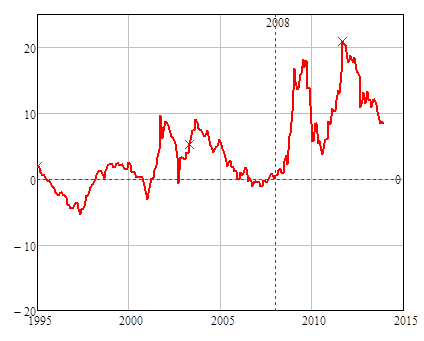

Whoops: what the data actually shows is a Clouseau-like stuff-up, with the rate of growth of M1 actually turning slightly negative after Bernanke took the helm at the Fed, and before the crisis began in 2008 (see Figure 2).

Figure 2: Change in M1 from 1995 to now

He does better in the aftermath of the crisis, when M1 explodes rather than implodes as it did in the 1930s. But there’s another, more important, problem with Bernanke’s sleuthing: to whit, who owns the M1 (and M2) ‘gun’? Bernanke argues as if the Fed has easy and direct control of the money supply, and he famously once referred to this power as its “printing press”:

“The US government has a technology, called a printing press (or, today, its electronic equivalent), that allows it to produce as many U.S. dollars as it wishes at essentially no cost… We conclude that, under a paper-money system, a determined government can always generate higher spending and hence positive inflation.” (See Deflation: Making Sure “It” Doesn’t Happen Here.)

But that simply isn’t true of M1 and M2. Those guns belong to the private banks, since M1 consists mainly of cheque accounts (and M2 adds savings accounts, time deposits and money market funds), and the change in M1 and M2 therefore depend on the willingness of private banks to make loans.

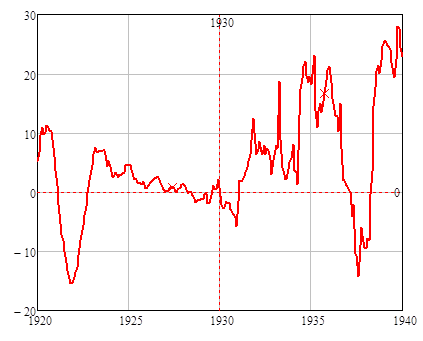

The gun that the Fed actually does control can change the level of M0, or so-called base money, which consists of currency in circulation – the stuff in your wallets – and the reserve assets of private banks. Economic textbooks – like Ben Bernanke’s – teach that bank lending is actually controlled by the Fed using two controls (the volume of base money and the “money multiplier”), but the Fed knows this a fantasy. The only gun with the Fed’s finger undeniably on the trigger is base money.

So how about that gun? Well, it remains true that the 1930s Fed let this fire negative bullets just before the Depression began, and for a while after (see Figure 3). But whereas M1 fell for four straight years from 1930 on, base money fell for only one year: from then on, the Fed was pulling on the only trigger it directly controls. It was clearly trying to revive the economy by increasing base money.

Figure 3: Change in Base Money from 1920 till 1940

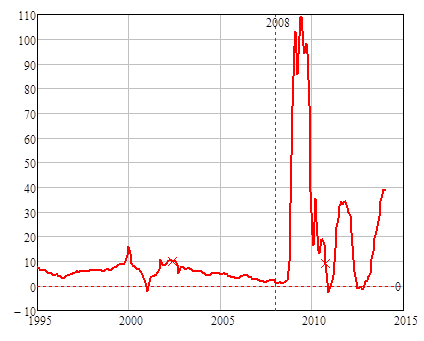

Ben also let the rate of growth of base money drop to extremely low levels before the crisis began (see Figure 4). But he pulled the trigger much more vigorously than his predecessors, once it became obvious that this was no ordinary recession.

Figure 4: Change in Base Money from 1995 till now

So on Ben’s own theory of what caused the Great Depression, he could quite easily be found guilty – by a future Ben Bernanke – of causing the Great Recession. The only saving grace would be that once he had made the mistake, he fought to reduce the size of the crisis. But the crisis still occurred, on his watch, and when his Fed did the very things he said the Fed got wrong in the late 1920s.

I like Keen. But I doubt very much that his analysis will trouble Bernanke.

In fact, most economists are so model-driven and compromised that Clouseau-like bumbling is an occupational hazard. Keen’s investigation, while couched in terms of economics and monetary therory, is really a murder investigation. (People have died in this Recession) . Keen (rightfully!) concludes that fiat gravity was the “cause of death” so he ignores eyewitness accounts that the economy was pushed.

For an economist, cronyism and collusion are idiosyncrasies that defy modeling. Monetary aggregates – are what’s REALLY important (to an economist).

But the fact is, Bernanke is a crony. As such, he made good on the Greenspan put. In a sense, he drove the getaway car. He made foolish statements like “subprime is contained”, that QE’s magic was stock not flow, and that he could end QE any time of his choosing. He repeatedly talked of the need for the Fed to communicate and then lied about the taper (to whose benefit? ZH said Goldman made a bundle).

He insisted that QE was the answer for unemployment and that the Fed would employ its considerable resources to help the unemployed but that was all talk. QE benefits were dispersed far and wide via portfolio diversification so only a fraction made its way to Main Street. Thus, his QE experiment failed to re-inflate the housing bubble. But what his faux attack on unemployment DID do, coupled with BLS’s flawed headline unemployment measure, was provide political cover for tax breaks for his cronys and other rich people.

Bernanke COULD have spoken out about important issues like: inequality; the revolving door; the carried interest tax deduction; record bank bonuses; the need for Banks to return to mark to market accounting; the failure of Dodd Frank reform; corporate governance (in light of JPM’s record losses and legal bills); and much more. He didn’t.

Bernanke disgraced the profession, as much as Wall Street disgraced capitalism, though very few seem willing to recognize this today. Perhaps because he didn’t do it alone. He was one of many cronys that pushed our economy off the balcony. And these cronys WELCOME the Clouseau economists and pressittute reporters that examine and report on minutiae but never effectively connect the dots. Nothing to see here.

This has long been my view. I used to travel to international conferences armed with papers written by a postmodern text-engine to see if anyone could tell (a bit like Alan Sokal’s scam). Somehow, everybody knows meaningless drivel is in play and no one is dumb enough to call the Emperor naked. Most of the dullards equated positivism with fact-based analysis and the real clowns spoke on reviving transitional economies based on the number of new vehicle registrations whilst ever increasing numbers of homeless were totting on garbage tips round the corner.

Much of what Steve says is very 70’s to an oldie like me and his scientific smell test type-stuff would have been derided as positivism by the social constructionists and others attracted to solipsist gravity. His work seems trapped in the Academy in the sense Jack says. In the UK we have public inquiries/inquests that whitewash everything – several into Iraq without Blair swinging from a lamp-post and farcical stuff on cop/care blunders that demonstrate little beyond it being a bad thing to let people investigate themselves. We knew back in 1910 (whenever) that the problems were imperialism, lack of democratic foreign policy, extremely biased and poor education and media and vast corruption. The Academy generally fails to teach investigation and has found many ways to kill off the critical eye.

Having conducted some serious investigations, I found social sciences generally pathetic distraction from practical inquiry to find out what was going on. Access to the very material I’d have wanted as a cop or scientist was denied. Academics are too feeble-minded to work out proper suspicion techniques (despite ‘suspicion of suspicion’), lying and why it is we think we are teaching accounting when we can’t tell a good company from a bad one on the basis of our teaching. Convincing the Establishment by a scientific economics is a non-starter.

I wouldn’t be surprised if your text engine could win a Nobel Prize in Economics. Could you use the $10 million?

Bernanke was no Poirot, looking for clues to the Great Depression. He took his analysis directly from Friedman and Schwartz. His achievement was to translate from Friedman’s rather simple-minded quantity theory of money into a credit creation framework. Friedman and Schwartz were not detectives, either; theirs was a counterfactual argument, a kind alternative history — not an explanation of why the Great Depression happened, or how it happened, but, rather, an explanation of how “it” might have been avoided, where “it” deserves some explication.

What Bernanke thinks could have been avoided in the Great Depression is a bit vague in his writing, but, in general, it — the “it” to be avoided — seems to be a large part of the New Deal, which could be avoided if the runaway deflation and financial system collapse could be avoided. If the financial collapse could be avoided, the plutocracy and its political domination would remain intact, unchallenged by the institutional reforms of the New Deal.

We don’t do ourselves any favors when we speak so vaguely about success and failure, what “works” pragmatically and what doesn’t, that we cannot discern when a leading figure simply does not share anything like our values and goals.

I think Bernanke’s original rise to Fed Chairman, which was planned well in advance, is, itself, strong evidence that the economy was pushed off the cliff. Some powerful people could see that a crisis was coming, and they knew from his resume that Bernanke would be prepared to handle that crisis is the way they desired. I don’t put that thesis forward as a conspiracy theory, but as a simple hypothesis about the reasoning of those in power, as they shepherded Bernanke’s career through the Bush Administration to his appointment to succeed Greenspan.

I would think Bernanke is well-satisfied, in the main, with the results of his policy. He did what he thought would have been best in the original Great Depression: he preserved the banking and financial system intact, and expanded markedly the volume and value of financial securities and credit instruments in the economy. The most salient institutional change — the marked increase in industrial concentration and domination by the largest, most diversified giants — is something I imagine he thinks is an improvement. And, the dog that did not bark — the absence of major institutional reforms in the economy inside or outside the financial sector — is a big win.

John Taylor’s Comment on Bernanke

Translation from ultra-polite economist-speak: Bernanke screwed up royally: he helped cause the problem (GFC) and then compounded it with QE.

I imagine much more $ M0 found its way into Europe this time around the depression sun.

I still hold a few notes just in case America gets to eat all the (energy) pies.

PS , the depression is not over , its just beginning.

We are possibly seeing oil sloshing around and maybe moving back into Europe but for that to happen countries such as Morocco and Turkey need to be drained as if they were $ swamps.

The best gift of the USA to the world in the 21st century is crony Central banking. It has ALWAYS been a feature of the American system but it is only with the advent of Robert Rubin and the decimation of Glass-Steagall that crony Central Banking has been exported to other places. Hitherto, the machinations that brought about the Fed, the gyrations of the House of Morgan and other Fat Cat Bankers have all been minutiae of economic history which only the very careful history reader abroad would have known. Today, there is rapid education in all corners of the world of how Central Banking can be subverted to the greed of the private banking sector. We will soon be witness to the dethroning of independent and truly autonomous Central banking nations like India and Canada pretty soon. The vehicle for this – AS ALWAYS – will be through the political sphere. Politicians in India and Canada are already railing against the autonomy of Central bankers. England saw its Central Banking apparatus made toothless in the last decade. The very successful modus operandi of private banker empowerment in the USA which started with the advent of Walter Wriston and Sandy Weill is sure to be repeated in capitals ALL over the world soon. This country has already succeeded in exporting the ‘money buys the best politics’ to other nations. Money bag politics was a corollary to crony capitalism and Central Banker cronyism. Can any nation that worships greed come to any good? Can it’s vaunted ‘Super Power’ status do the rest of the World any good?

I like Steve Keen’s work but discussions like this one fall into the obscurantist trap that divorces economics from politics. All Bernanke did was save insolvent banks, fuel an asset bubble, enable continued looting by the very people who caused the ’08 crisis, while punishing all honest savers, stimulating unemployment, and stealth (unmeasured) inflation. He was an establishment creep, toadying to elite masters, and Yellen will be another one. These people cannot help themselves, and if they tried to act in the public interest they would not last two hours of their terms, although exactly how they would be eliminated is far from clear.

Bernanke simply did not understand his own monetary operations. He clung to an outdated 19th century banking model which proved useless for dealing with a massive demand shock and spent the next five years trying one variation of the theme after another, each failing in turn. For many reasons (peer pressure, a lifetime of work he couldn’t bring himself to jettison, fear of consequences for leaving the reservation) he was unable to veer from the path he’d followed his whole life and so let down the entire world.

The lesson is our elites are as much prisoners of their ideology as we are.

Post was mine, autocorrect ate my surname.

Ah, never mind. I don’t understand how my Nexus interacts with blog commenting, but weird stuff happens sometimes.

Ben – “Bernanke simply did not understand his own monetary operations.” I suggest he understood very well what he was doing. Proof? Who is raking in the money? Yes, you got that right, his banker friends. He did what he was told.

“Of course, Bernanke got the job he’ll soon vacate because he was perceived as the Hercule Poirot of economics, whose brilliant sleuthing solved the ‘Whodunnit?’ of the Great Depression.”

That seems to be the point of contention between the ‘we have an economic problem’ view and the ‘you cannot separate economics from politics’ view. I would posit that there is no evidence to support the claim that Bernanke got the job because of his work on the Great Depression.

Rather, I would contend that Bernanke got the job because he agreed to continue doing what Greenspan was doing (namely, helping to keep the facade of the system intact for a few more years’ worth of looting – a task at which Bernanke excelled, not failed).

I tend to favor any explanation which favors the lowest common denominator. One Bernanke looks like a goofy professor and was a Republican when first appointed by W. Obama besides being in the thrall of bankers is also not an activist President. Someone other than Bernanke might not make it past the 60% threshhold, and the GOP was at nadir with the current Democrats as opposition.

Bernanke’s chief qualification in Obama’s mind was that he would be an easy and bipartisan pick. Other than that,Obama expected to just be praised just like his cultists do.

ugh, I’m glad he is gone.

For starters, Bernanke had no tools to turn this new depression around. The only tools he had were setting interest rates and some he kinda made up as he went along like the money shuffle with repos and MBS and treasuries back and forth between the Fed and the banks. Then there was the most irresponsible congress in the history of the United States who refused to give Bernanke any effective means of changing social structure by directing credit toward main street instead of Wall Street. And the parallel refusal of congress to create jobs because they were dedicated to the idea that it would just rob the wealth of the future. And then there was the civil war within congress creating a stalemate of government itself on every level except military funding. And of course military funding meant our treasury would be squandered all over the planet and never be accounted for but it was vaguely hoped that this would stimulate enough demand that the whole capitalist system would not implode. And there was also a certain self-interests among senators and representatives to get re-elected by scapegoating Bernanke. And then we learn something we instinctively knew via another of Greenspan’s confessions: interest rates are useless for turning a dead economy around – proving that the Fed Chairman is the Big Nothing.

Don’t forget Obama, Holder and the DoJ. They not only didn’t prosecute anyone for banking malfeasance they didn’t even investigate blatant instances thereof that we’re right before their eyes. As documented exhaustively here at NC over the past five plus years.

Where was our Ferdinand Pecora?

Bernanke was determined to avoid deflation. He failed in a telling way: his efforts to quietly flood the financial and credit markets with precautionary liquidity in 2007 set off a runaway boom in commodity speculation, which set off the recession and set up the brief deflation, which precipitated the acute moment of crisis.

Failing to notice the resource ceiling on the global economy revealed in that episode, along side the pernicious role an easy money policy can play as we approach that ceiling, is a huge handicap in forming a progressive view of feasible policy.