Yves here. Gillian Tett of the Financial Times has also been taking up the credit mania theme of late. For instance, from today’s newspaper:

A few short years ago, “subprime” was almost an expletive..

But the financial world has a short memory…In recent months subprime lending has quietly staged a surprisingly powerful return, not in relation to real estate, but another American passion – cars…

The historical echoes are uncanny. During most of the past decade the amount of car-related debt grew only modestly. Yet outstanding car loans, which totalled $700bn in 2010, have jumped by a quarter in the past three years…

Even more notable is that this has occurred amid a sharp deterioration in loan quality. Five years ago, subprime loans represented barely a 10th of the total; today they account for a third. A particularly high proportion of GM cars sales are financed by subprime loans. Meanwhile, a 10th of new loans are now going to so-called “deep subprime”, or consumers who would previously have had little chance of getting funding – particularly given that incomes for poorer households have stayed flat or declined, even as car prices jumped.

The problem is that the authorities’ solution to the credit bubble that led to the crisis was to reinflate it rather than restructure the debt (although they got more liquidations via foreclosures than they probably wanted as a result of the failure to rein in bank servicers). Unfortunately, it appears that they’ve succeeded all too well in this strategy.

By Wolf Richter, a San Francisco based executive, entrepreneur, start up specialist, and author, with extensive international work experience. Originally published at Testosterone Pit.

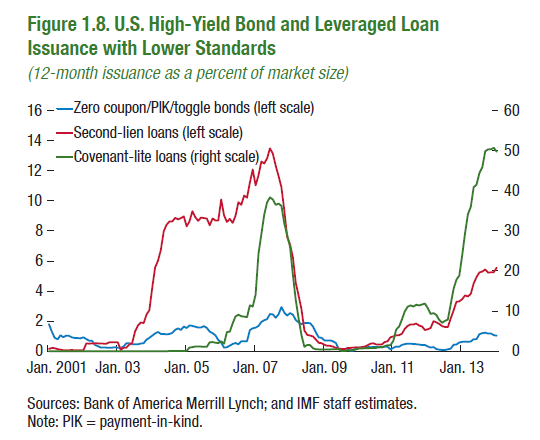

Hidden in the IMF’s just released 188-page Global Financial and Stability Report is a doozie of a chart that screams not only “credit bubble” but also flashes a red warning sign: “seek cover, implosion in sight.” It depicts US issuance of covenant-lite loans and second-lien loans since 2001, including their phenomenal bubble that so spectacularly collapsed in 2008, and the even greater bubble currently underway – with an equally spectacular future.

Covenant-lite loans, which eliminate many of the protections that lenders normally require, allow over-leveraged junk-rated companies to pile on even more debt when they would normally no longer be able to do so. A key benefit for the Private Equity firms that own them: PE firms make a big part of their profit by having their portfolio companies borrow money, but not for expansion purposes or other productive uses. Instead, PE firms suck that cash out the back door through special dividends, fees, and other devices. When the portfolio company pops, the PE firm conveniently has the cash, and the lenders eat the loss.

To protect themselves, lenders normally force borrowers into covenants that prevent these and other shenanigans. But not anymore. Lenders, driven to near insanity by the Fed’s interest rate repression, are caught up in an all-out chase for yield and don’t look at anything else, and to get that minuscule extra yield, they take on risks, any risks, no questions asked, and to heck with future losses, and they hold their noses and close their eyes and pick up the worst crap, and then find ways of stuffing those risks into your mutual fund.

It’s a Feeding Frenzy Out There.

The longer it goes on, and the more of this reeking debt with a high probability of default is piling up on the books of banks and other lenders, the more damaging the implosion will be. And so covenant-lite debt has become a flashing red light of a credit bubble in its final throes. A record $238 billion were issued in 2013, according to Thomson Reuters. Over 50% of the market, another hair-raising record.

The IMF chart shows the prior bubble as expressed in covenant-lite loans (green line, right scale) and second-lien loans (red line, left scale) and where it all ended so spectacularly – namely in the financial crisis. It also shows the current bubble through 2013. Covenant-lite loans started setting new records last year, but second-lien loans, a particularly nasty contraption for banks, haven’t quite caught up yet. Up to us to figure out where it ends:

This Year, It’s Even Worse

Through March, about $68 billion in covenant-lite loans have been issued, according to Thomson Reuters. Banks are making even more concessions and relax loan terms further, giving over-leveraged companies enormous flexibility in how they deal with their debt if they run into trouble and allow them to pile on yet more debt. These new loosey-goosey loans have lovingly been dubbed, “covenant-lite 2.0.”

Banks are lapping it up. Classic covenant-lite debt, of the type that helped blow up the banks in 2008, have maintenance covenants to give lenders at least a modicum of protection in case of default. But one of the many newfangled features – increasing the “restricted payments baskets” – permits companies to channel more borrowed money via dividends and other devices back to the PE firms that own them. The cash is gone. The debt is still there. The loan-to-value ratio deteriorates and wreaks havoc on recovery in case of default.

Covenants are supposed to protect banks from those shenanigans – but aren’t anymore. Leverage ratios have been rising for a couple of years and now exceed those of the white-hot bubble market of 2007. But these hyper-leveraged companies won’t pop right away, not as long as new covenant lite loans allow them to borrow even more, and not as long as they can bamboozle desperate banks into lending more. Yet piling on more debt to deal with old debt merely pushes the day of reckoning into the future and increases the loss for the banks.

Even the Fed, which never sees signs of a bubble, and denies the very existence of bubbles until long after they have imploded, is seeing the ballooning covenant-lite loans as a risk to the very banks it had so heroically bailed out during the financial crisis, and Fed heads have mentioned them as an item on their worry list, and as a reason for eliminating QE.

In the IMF chart, second-lien loans (red line, left scale) also bubbled and collapsed beautifully. These loans are secured by a second lien over assets that have already been pledged as lien for other loans. In case of default, holders of first-lien loans have first claim to the assets. Holders of second-lien loans get whatever is left, which is mostly nothing. These second-lien loans, a particularly nasty contraption for banks, are jumping again. The skyward angle of the slope continues beyond the IMF chart: in January and February, $7.4 billion in second-lien loans were issued, up from $4.5 billion during the same period in 2013.

Defaults are unlikely as long as the Fed shoves nearly free money out the front door into the hands of even over-leveraged junk-rated companies that would otherwise have trouble servicing their existing debt. But the Fed is cutting back on QE and is generating a deafening cacophony about raising interest rates. Watch out for falling debris.

Okay so what are we looking at here? 238 billion last year in crap loans in 2013 and about 7 billion more a month this year, but what is the default rate?

“What is the default rate?”. You now qualify to run JPM Chase or any other insolvent bank, or perhaps the Federal Reserve. The default rate IS of course, very low, just like it was in 2007. The correct question is: What will the default rate be when the collapse resumes? The answer is that all the companies that went down to $1.00 (hello Citi) to $5.00 in the Crash will now go to ZERO. The cleansing will begin.

I declare myself an Austerian on NC. Austerity for Bankrupt Banks, a broader safety net for the Citizen victims. The one thing the (at least) that the AUSTRIANS have right is the path of credit bubbles. Throw rotten tomatoes at me NC, call me a Melonite, but the fact is I stated 7 years ago that the Multi trillions in losses were ALREADY made, the only question was who would pay the price. Stupid question.

My Right Wing friends call the only ones to put their bodies on the line to be beaten by the fine NYPD- Occupy- lazy dirty scum. There will soon be no middle ground in the US.

The Depression that began in 2000 will soon resume. Europe is a goner. Money flows MIGHT propel the US Stock “Market” higher as the People starve (1932-1937).

Buffy Ste. Marie said it best: My Country ’tis of thee your people are dying”

“What will the default rate be when the collapse resumes? ….

The central tenet of the NC argument is that the U.S. economy (a proxy for the world economy) is on the cusp of another collapse because of insufficient employment and poor income distribution (purchasing power). Danger signals abound, true. The issue is when?

My guess is that there are enough economic drivers that will postpone the crisis for some time, for at least a couple years if not more. China is turning its economy inwards from exports-driven to domestic consumption, S.E. Asia is doing not too badly, Europe is humdrum but not dead. The Fed is pulling in its horns and plans to drive credit creation lower just like the moribund ECB, the price of oil will keep Russia and the Middle-East alive and pumping money into the U.K. Barring an accident from China (the Prime Minister wants to become “market oriented,” and squeeze credit) and/or high agricultural prices (The Western U.S. has become a desert due to lack of moisture this winter) the global economy will likely survive for another bout of growth.

I would discount Gillian Tet though. She does not know enough about the car business among others. Cars are very low priced compared to houses, are easily disposed off in the secondary market at close to fair value and hedge funds exposure to them is a drop in the bucket. The Fed is cognizant of covenant light loans I am informed and that is why it wants to raise the capital requirements from the Big Eight among other reasons. Bank profitability is declining because the banks are not doing too much new business: what does that say about “covenant-light”?.

We will have gotterdammerung some day, the causes at this juncture however, I believe, are not as certain or frightful as you make it sound.

Cars aside, your other assertions are simply that – and every one of them is suspect. I’ve been anticipating major trouble for the global economy by late 2014/early 2015 for 3 years now. You simply cannot make as many atrocious policy choices across so many areas as the US has made – and forced upon the world – and expect good results.

Europe may be “humdrum” from an investor’s point of view but persistently high unemployment particularly among the young, the rise of militancy on the right and left, repressive laws such as currently being proposed in Spain have the makings of some exciting times to come.

” Spain’s forthcoming Citizens’ Security Law. A decidedly Orwellian item, it proposes fines of up to 30,000 euros ($41,000) for “offensive” slogans against the country and up to 600,000 euros ($824,000) for unauthorized street protests…

…

The original draft of the law covers a lot of ground, including fines of up to 30,000 euros for “participating in the disruption of citizens’ security while using hoods, helmets, or any other article of clothing or object that covers the face, rendering identification difficult or impossible,” or for “disrupting citizens’ security at gatherings in front of the Congress of Deputies, the Senate, and regional legislative assemblies, even when these are not in session.” Fines of up to 1,000 euros ($1,400) are prescribed for hampering pedestrian traffic, losing one’s identity document more than three times in five years and circulating images of members of state security forces that might infringe upon their “right to honor.””

http://www.dailykos.com/story/2014/04/10/1291087/-Orwell-Returns-to-Spain

Timing is very hard to predict. However, companies whose business models consist almost entirely of defrauding their customers are not long for this world. (Monopolies like Comcast which provide a needed service can get away with a lot. But does anyone *really* need to deal with a megabank?)

Looking at matters from the vantage point of being in Hong Kong, and, minting close contact with my home nation, the UK; I’d have to say red warnings on “bubbles” have been flashing in many sectors globally since the commencement of QE, specifically: soft commodities, housing, student debt and now credit/debt for motor vehicles.

Anyone keeping an eye on the UK economy cannot be but amazed at the fact we have a “bubble economy” of epic proportions in London, whilst the rest of my beloved nation languishes in some kind of economic purgatory waiting for the supposed “green shoots” of recovery, which never seem to emerge.

In a nut shell, we have no recovery as such in the UK, the figures the IMF, Conservative Party and their LibDem henchmen are crowing about for GDP growth are all associated with private debt consumption, the very consumption that resulted in the 2007/08 implosion.

When will the buggers ever learn, and when will the voting electorate wake up and smell the coffee beans – its seems I’m in minority of maybe 3% at max of individuals who is aware what is going on in reality, and what I see scares the pants off me – thank god I’m poor and have nothing to lose – one things for sure, they can ram their cheap debt up their backsides.

TYPO ALERT

Should read” remaining in close contact with my home nation”

@Chris

The UK is not a nation

Its 19th century form was a banking union not unlike the Euro market state of today.

I have been crowing about the UK car bubble for some years now,

Its a obvious physical manifestation of the gross centralization of capital claims via the extraction of Londons chief hinterland – the EU entrepot via the forced extermination of all rational domestic exchange within EU vassal states.

Although this is now a grossly inefficient method of extraction as so much energy is lost via this long distance conduction of trade it is where the power / money resides so that is where the action (surplus transfer) happens regardless of its conseqiences to real production distribution and consumption chains.

The UK has been in the game of burning villages even before it was offically formed.

Now that UK roads are becoming saturated the banks are now looking to get a yield off of oil wastage elsewhere.

Ireland for example is at the start of yet another epic capital dumping event which they will call growth.

I advise people to retreat into their caves / run to the hills.

http://www.youtube.com/watch?v=W3zIfO-YOzg

We live a nightmare which people call the west.

@Dork of Cork,

Well, if by running for the hills, you mean economic independence from both the UK Westminster cabal and EU cabal, I’m all in favour of this, particularly given we can make localism work in Wales if left to our own devices – the same is true of Ireland – obviously, our “consumerist” way of life, underwritten by cheap credit – debt enslavement to give it its proper name, will be a thing of the past, the fact remains in my own Country, our destitute working class does not have a great deal of disposable income to begin with, it being the lowest in the UK.

I yearn to be free of neoliberalism and enslavement to England and its City of London, shame my fellow citizens don’t see it that way, so blinded are they to tribalism, a tribalism that results in the ridiculous situation whereby the son of Lord Kinnock can stand for election in one of the poorest seats in South Wales, whilst being part of the international kleptocrat himself – does not make sense to me – I’d hang the bugger and many others in my beloved Labour Party who have sold its core constituents out for mammon – they disgust me!

@Chris

What makes Al Murray / John Bull so funny is that he is now such a strange anachronism.

Now after serving a useful purpose as defined by bankers he can be safely chucked away and it is therefore now safe to laugh with him.

https://www.youtube.com/watch?v=GBVTDLtTLtE

He of course gets most of the euro crisis wrong – except for the last bit.

Listening to the man one would never think the UK was the greatest real goods deficit black hole that ever was………the very center of euro area rent extraction.

Car consumption is perhaps the easiest mean of controlling scarcity & thus profits.

A technology designed for Rockefeller type demand management.

Of course your resident bankers are making export noises so as to afford credit induced inputs.

This maintains the illusion of firecely competitive internaltional markets when in fact this is a bankers illusion.

It can seem a bit like me, you and a dozen others sometimes Christopher. I’m Scots by accident of birth and ancient family. I would vote to leave the Union. Our Labour Party is more or less in need of a new Declaration of Arbroath – ‘while 100 of us are left alive they will never rule us’ sort of stuff.

I suspect the next crash will come as a result of hybrid financial instruments. These are promoted as rather simple beasts, but they’ve been designed to carry plague. They have comforting names like CoCos. I’m sick of not being able to vote for a new honesty.

Well, if like me, you are confident that another “crisis” will emerge before this decade is out, the new honesty may be closer than we think. That said, its distressing that so many of my peers from whence I originated have failed to grasp the “new reality”, or embraced the illusion and crud we have all around us.

Thankfully, my bank balance kinda proves I remain true to a singular cause, ennobled by the fact that I fight not only for myself, but my offspring and my class to do otherwise would bring shame on my family and those I hold dear – we may be poor, but we don’t kowtow to anyone, particularly those who believe they can buy you off.

Here’s looking forward to the awakening once more, regrettably many will suffer further than they have already, and this hurts.

It will continue so long as:

1) bonuses are paid in cash rather than stocks that vest over, say, a 5-year period; and,

2) Governments act to make sure that top management is never punished for their actions.

Yes. They weren’t forced to be responsible for their actions, and then they did it worse the next time. Didn’t see that coming.

Remind me again what the low interest rates are supposed to achieve. All I see is the way they drive investors into dangerous investments in order to get the kind of returns I used to get from CDs.

http://www.levyinstitute.org/pubs/rpr_4_13.pdf

“”Before the first policy moves related to the current crisis in August 2007, the Fed’s reserve accounts were equal to about 5.5 percent of the monetary base. Today, the Fed’s reserve accounts—nearly all of which are in excess of the amounts required—are equal to about 60 percent of the monetary base. Required reserves are only three percent of the monetary base.””

“”Essentially, the new reserves provided by the purchases program enabled the banking system to fund the repayment of about $1 trillion of various forms of advances to financial institutions under the emergency lending program. The emergency lending program ended, but quantitative easing replaced it.””

“”Charging below-market subsidy rates violates the classical ideal of impartiality in LLR (lender of last resort) lending, and channels credit not to its highest and best uses as the market tends to do, but rather to politically favored recipients. The same inefficient and suboptimal allocation of credit occurs when the Fed purchases tarnished assets from selected preferred sellers.””

“”In retrospect, it is difficult to see how further expansion of the excess reserves pool by the quantitative easing programs once the initial round of emergency lending generally ceased in March 2009 assisted in the maintenance of sound economic conditions or helped lay the basis for a sustained recovery. Real rates of return have to become positive for borrowers to identify projects for which they wish to borrow and for lenders to prefer to lend.””

“”That is the lesson we can learn from Japan: if government does not ramp up the fiscal stimulus, and keep it ramped up until a full-blown recovery has occurred, the economy will remain trapped in recession””

———

This implies a combination of markets working together with government regulation and without favoritism..

One example of the Feds emergency programs…

TALF: The top three cumulative borrowers, Morgan Stanley, PIMCO, and California Public Employees’ Retirement System would borrow roughly $22 billion or 65 percent of the total borrowing. Together, they borrowed at a weighted average rate of 1.76 percent

Why did CALPERS have to take the Welfare? I never heard about that.

Yes, I thought that was an interesting trio..

The Fed did not give out this information willingly..

” In many respects, we found certain aspects of the Fed’s response troubling: size of the response; length of time required; which types of institutions received assistance; and most importantly, the veil of secrecy that surrounded Fed actions. Indeed, our detailed study would have been impossible without an Act of Congress and Bloomberg’s Freedom of Information Act lawsuit because until those actions, the Fed had refused to release the data.”

Just read on CALPERS website: “Calpers has a broadly diversified portfolio(paraphrasing) which means that losses in one area are made up for with gains in other areas”. #!. If they believe that they are more dangerous than we knew

#2. I believe this statement, made without caveats, should be sufficient grounds to call for the resignation of the entire Board of Administration of CALPERS, and possibly enough to charge them with mis-representation.

Aside from that, the corrallary(sp) to their statement would have to be “so any gains are offset by equal losses”.

CALPERS members, I would suggest you take a screenshot of the CALPERS “Investments” page with that statement. When it all implodes, you will be able to make the case that you based your decision to invest on that statement.

Most likely because the Fed wanted to do triage for the stock market asap.

Not a bug but a feature. It’s necessary to re-inflate those assets so they can finally be seized from deadbeats and sold off to fools.

My impression is that bubbles are seen by the oligarchs as a substitute for government spending. Without bubbles there is no growth. Is it really inevitable that these bubbles will crash? Can’t smoke, mirrors and misdirection work for a long time? Isn’t it a fact that the world economy has maintained itself rather well considering the astonishing disaster of the 2008 bubble collapse where most people here have been predicting disaster? Could it be that there is some principle we’re missing? Could it be that this chaotic system is displaying some kind of emergent “intelligence” we don’t yet understand? It certainly has become complex enough.

Banger said:

“Could it be that this chaotic system is displaying some kind of emergent “intelligence” we don’t yet understand?”

Banger you are on the right track. The issue is most people don’t realize that “says law” is not true!

Says law simply put says: The production output/capacity of the economy can be liquidated (used-up) by spending all wages and all profits of the (monetary) economy.

This is not true. We all implicitly believe it. And bankers and usurers encourage this false belief.

There remains plenty of capacity of a monetary economy to be used up by issuance to debt or just debt free money. The global usurious economic system worked ok because of economic growth. Now that economic growth is gone we need another model to distribute goods and services. I suggest $500 to $1000 per month social credit payment to each U.S.Citizen via FED printed new money.

Debt is real but it is accounting. We can have 100 times the debt we have now on books but that is just bookkeeping. It (level of debt) does not determine what is possible as far as capacity of the global economy is concerned.

http://aquinums-razor.blogspot.com/2013/02/the-banking-system-and-economic-growth.html

Mansoor H. Khan

But the word “debt” still carries a stigma.

Sadly, it ain’t this simple.

Just another “this time is different” argument. Debt brings demand from the future into the present. Eventually the future demand is all depleted but the debt service remains. You can fool the system for a while…in fact quite a while. The system was catastrophically “unfooled” in 2008…but then The Wizard of Ben conjured enough new balance sheet capacity to fool it back again. Can this work forever? Don’t think so.

Printing money works. And it isn’t debt. But nobody’s been willing to do it. The printed money has to be given to the poor people, of course…

You might take on the notion that there’s probably a 60/40 per cent working ratio of government and private banking created money which if varied in favor of more private bank created debt creates economic instability:-

https://dl.dropboxusercontent.com/u/33741/FGEXPND.png

http://mikenormaneconomics.blogspot.com/2013/11/mark-buchanan-actually-economists-can.html

http://economicsrantsnmusings.blogspot.com/2013/06/does-credit-drive-economy.html

Large parts of Europe are in Depression. The Stock market is not the Economy. “Without bubbles there is no growth”- can one say “crock of shit”? Name one bubble that has not collapsed. Bubbles do reflect the Publics’ often correct optimism over new technologies, but the bubble itself is discounting 10-30 years of the future into a far shorter time period and the result is ALWAYS a return to current reality and cash flows.

I think you may have misunderstood Banger. I believe his statement on bubbles was irony–the only way “growth” (or, opportunities for fleecing the 99%) has been achieved these days is via bubbles.

Thanks.

Bubbles are, in fact highly destructive to our society because they remove capital (social and financial) from productive activities.

In Bernanke’s last appearance before Congress he defended QE with the explicit reference to rising auto sales. Nevermind how destructive the entire auto industry is to the environment – that very destructiveness is evidence of how important it is to the “economy” and so Bernanke bragged it up. As if to say it wasn’t a credit bubble if grassroots America was the beneficiary. But again the Fed was doing triage for the stock market. Everything leads back to the stock market. Easy credit effectively lowered the price of a car in one last attempt to keep the economy from tanking. It is the opposite of the French Monarchy raising the price of flour to speculate away its debt only on the surface because both tactics shifted the burden of debt to the peasants. Sort of.

And remember, Bernanke explicitly cited the performance of Pink Sheet Stocks (o.k., not really- it was the Russell 2,000; close enough) during testimony a few years ago.

I believe the Japanese Central bank is openly buying equity ETFs.

“As if to say it wasn’t a credit bubble if grassroots America was the beneficiary.”

Beneficiary of what? Auto loan to get to their mandatory minimum wage job that doesn’t even pay the rent, until the day the roving bands of electronic bank spies seize the car?

“Automated license plate readers used by car repo companies, for example, collect billions of personal records per year, which contribute to vast databases that can be used by law enforcement, insurance companies, banks, and the like, with few limits…

The top commercial use of the devices falls into the auto finance and auto repossession industries, which both work closely with major banks to track down those who default on loans. Digital Recognition claims its clients include Bank of America Corp., JPMorgan Chase & Co., HSBC Holdings, and Citibank.

Banks strongly encourage its repo contractors to use plate scanners, based on their efficiency in tracking down loan defaulters.

“The banks want it,” said Liran Cohen, owner of repo company Massachusetts Recovery Bureau. “All of them make a big deal out of it, since it gives them so much value.” ”

http://rt.com/usa/license-scanners-private-database-046/

Who exactly are the recipients of these covenant lite loans? Companies owned by private equity firms?

For the most part, yes.

Does this mean that Wells Fargo’s earnings report is fictitious?

Wells Fargo’s earnings report is certainly ficttious. The company runs a large number of frauds and reports the illegally charged fees as “earnings”.

I don’t know if *this thing* means that it’s fictitious, though.

Wells Fargo is famous for aggressive games with their reserves and other aspects of their accounting. Why they aren’t dinged for it is beyond me.

CLL was usually seen as debt markets getting more liquid. The are now being issued in smaller packages well below $1 billion once seen. The companies issuing them have lower credit ratings than pre-crash. The lighter covenanting means collateralised loan obligation issuance will rise and at that point no one will know who is holding the bag with the dead donkey everyone was told would win the 3.30 pm at some future date.

Wells Fargo accounts have not been reliable since Dale Robertson worked for them.

Got a good chuckle out of that last reference.

“You can’t buy a toaster in America that has a one in five chance of exploding. But you can buy a mortgage that has a one in five chance of exploding.” Elizabeth Warren talking to Michael Moore in Capitalism: A Love Story.

That was 2009. Where’s the Consumer Finance Protection Board on this? Elizabeth Warren? I looked. Dday!

I am wondering if mortgage lending might be getting reckless. This is just a single anecdote but a good friend of mine just qualified for a mortgage where he only put down 3%. This person is making a pretty good living today, but he is self-employed and was reduced to near destitution for two years after the 2008 collapse. I simply can not see him being able to make payments if we go into another recession.

Hmmm. This goes a long way to explaining how a couple I know – who declared bankruptcy last year – recently qualified for a car loan for a new car. Couldn’t for the life of me figure out how.

:To protect themselves, lenders normally force borrowers into covenants that prevent these and other shenanigans.” That would be true if the money being lent is the money of the person making the decission to extend the load. Once this was the case, but for many, many decades now ” But not anymore.”

“Lenders, driven to near insanity by the Fed’s interest rate repression are caught up in an all-out chase for yield”. All low interest has done is increase the appetite for the loans themselves, it hasn’t done anything further the disconnect between the lending officers bonus in the short term and how these loans eventually perform in the long term.

The system of modern stock capitalism is broken because of it’s shear size necessitate using management who does not “own” the capital at risk. For example, It is impossible for any of the big banking corporation shareholders, the real owners of capital, to effectively unite get up enough votes to throw out the rot. Further, if the government bails out the losses, as long as the banks share ROI beats investment, they are not desperately motivated to do anything other that to shop around, which with the poor information flow, is hardly risk free.

Professional management has used corporate wealth to pay K-street to create a system where they can pick the pockets of both many shareholders and the tax payer with near impunity, behind a nearly impenetrable corporate shield. The regulators are in the capture of these professional managers so they go after the shareholders — which are mostly retirement funds — when public pressure must be met. Only in Sweden, Norway, and to a lesser extent, Germany does the old fable of the wisdom of PLC system still carry any water.

Even when these banks are hit with penalties, the shareholders, usually funds managed by other professional managers who have back scratching arrangements with their fellows in the banks & private equity funds, are hardly going to press the case of their investors in most cases because they know the market has very short memory.

http://www.scmp.com/business/article/1336788/public-suffers-most-big-bank-fines

Jake van der Kamp had retired and come back to writing editorials for the SCMP so many times that I’ve lost count. The temptation of pointing out stupidity in the world when it combines with the exasperation that the oligarchy isn’t interested in fixing it’s stupidity in many cases must take a toll when the deadline looms.