By Philip Pilkington, a writer and research assistant at Kingston University in London. You can follow him on Twitter @pilkingtonphil. Originally published at Fixing the Economists

Well, a team at the FT under Chris Giles has claimed to have discovered serious errors in the data spreadsheets underlying Thomas Piketty’s work. A few housekeeping issues before I proceed.

First of all, I do not have the time needed to go through the spreadsheets to confirm Giles’ findings; I am not being paid by the FT to do so (offers to do so will be seriously considered however!). I am taking Giles’ data at its word. This is because Giles’ does not strike me as a hit piece at all. I think that him and his team have genuinely found what they claim to find.

Secondly, I pointed out that Piketty’s use of data was suspect after reading just a few hundred pages of the book. I was less so referring to the data used than in the manner in which it was used. Something that often gets lost in these debates about the accuracy of data is that data means effectively nothing unless you are careful in the manner you interpret it. Reading Piketty’s book I found numerous highly contentious interpretations of the data. That said, I can appreciate that we will all have our own interpretations and that the first step is to all agree on the data we are using.

The first thing to note is that Giles is dealing with the data on wealth inequality and not income inequality. The former is, and Piketty stressed this both in his book and in his response to the FT, far more uncertain than the latter. The ability to get data on wealth inequality is thwarted by any number of facts; from the reluctance of the rich to talk about their wealth holdings, to the fact that much wealth is held in a ‘dark zone’ overseas outside of the reach of statistical agencies.

That said, some of the errors that Giles uncovers are pretty embarrassing. Take, for example, the issue of averaging in Europe. Giles writes,

Prof. Piketty constructs time-series of wealth inequality relative for three European countries: France, Sweden and the UK. He then combines them to obtain a single European estimate. To do so, he uses a simple average. This decision (shown in the screen grab below) is questionable, as it gives every Swedish person roughly seven times the weight of every French or British person. Using an average weighted by population appears more sensible.

I don’t know why on earth you would use a simple average in this regard. This does not strike me as being a simple ‘fat finger’ error. Piketty must have thought about what he was doing. He must have said to himself, “oh, I’ll just do a standard average of these very different countries”. That seems to me a very silly thing to do indeed.

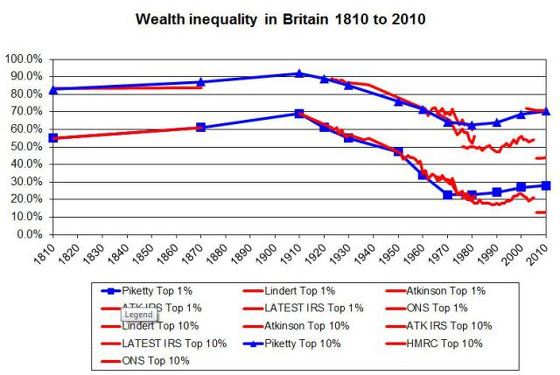

That said, the reconstructions that Giles puts forward seem to me completely out of whack. Here is the chart that he provides for wealth inequality in the UK. The blue lines are Piketty’s estimates, the red lines are Giles’.

From Giles’ reconstruction you would conclude that wealth inequality has not risen in the UK all that much since 1980. I have seen a lot of data related to this and I simply cannot believe this. It also does not really pass the ‘smell test’ — i.e. it does not really confirm with what we actually see day-to-day.

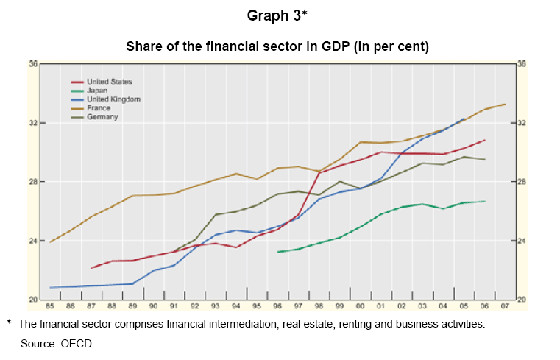

Consider the following graph from the BIS showing the evolution of the financial sectors in various countries from 1985-2006.

Since 1985 the size of the financial sector in the UK has increased by over 50% relative to GDP. It seems difficult to account for this rise of finance without assuming that there is far more idle wealth to be managed relative to GDP than there was in 1985. Since idle wealth disproportionately sits with the wealthy (otherwise they wouldn’t be called ‘the wealthy’, duh!) then we can only assume that wealth inequality has increased.

Since 1985 the size of the financial sector in the UK has increased by over 50% relative to GDP. It seems difficult to account for this rise of finance without assuming that there is far more idle wealth to be managed relative to GDP than there was in 1985. Since idle wealth disproportionately sits with the wealthy (otherwise they wouldn’t be called ‘the wealthy’, duh!) then we can only assume that wealth inequality has increased.

There are many, many ways of making this same argument in a roundabout way. All of the figures I have seen support the idea that wealth inequality has risen substantially in the UK. In fairness to Giles, he does admit this when he writes,

There is one important caveat. None of the source data at the basis of Piketty’s work is completely reliable. So while this post is clear about what is wrong with Piketty’s charts, it is much less certain about the truth.

Perhaps Piketty has mucked up some of the figures. But his is not the only study dealing with this issue. In that sense, I don’t think that this is a Reinhart and Rogoff moment that discredits the underlying thesis of Piketty’s book. Rather I think that it is just another lesson in data analysis for us all. Lies, lies and damned statistics, as they say.

If Piketty, in calculating a wealth inequality average for Europe, assigned a disproportionate weighting to Sweden & France, wouldn’t that mean that he probably underestimated wealth inequality?

As for Giles, if he thinks that wealth inequality hasn’t widened in Britain during the past 30 years, then I don’t see how we have much choice than to assume his criticisms of Piketty are malicious.

We have to assume malice, since nobody could possibly be stupid enough to be a wealth inequality denier in our time.

I don’t think you need to assume malice. Giles writes:

The data is what it is. The data could raise all sorts of issues (Giles points them out) and Piketty’s thesis still is true.

The really odd thing is that if Piketty’s formula is right, would that not imply that capitalism is stable? As opposed to prone to crisis? Is that really something that the left wants to be cheering about?

If a system that tends to produce high inequality, forces that undermine democracy and savage social injustice can be sustained over a long period of time without falling into a system-threatening crisis, then I think the consequence is that the system must be challenged and altered by political action. The fact that a form of barbarism is stable is no argument for barbarism.

I think Piketty’s main targets are two: liberal defenders of neoliberal market capitalism who have argued that there are forces within capitalism that well naturally tend to reduce inequality over time, and marxian defenders of one or another form of crisis theory who often seem to be arguing that we shouldn’t do anything politically about the way capitalism works, because capitalism has an inherent tendency to fall apart and collapse on its own as capitalist profits fall, and the worse it gets, the sooner the collapse will occur.

But what if capitalism is a system in which a few wealthy capitalist barons can sustain their rents and keep us all on the industrial and post-industrial plantation indefinitely if no political action is taken?

Well, what if that were so, *and* it were so that representative democracy were merely the tightly controlled means by which we are graciously permitted to peaceably petition for redress of grievances?

Then we have to find a new politics, don’t we? Perhaps one less inspired by a clique of white guys asserting some kind of social privilege in bloviating about pinheads and angels in Latin, the secret code and institutional idol of the privileged? At the very least, recognizing as much puts a few holes in the belief in the essential goodness of authority, which is a good start in any case.

Well, THE LEFT is not up to speed with Marx and Piketty. So much for a social science where nobody starts with the same premises for their arguments or the refutations. But for the sake of brevity, the constancy of Piketty’s “r” as the ever present state of affairs we all accommodate, hence not causing a disruptive crisis, because it’s a new IRON LAW, that makes the social order possible at all, even if the social order permanently relegates most people, most of the time to an economic inequality. David Harvey addresses this point in his May 17th commentary on Piketty.

http://davidharvey.org/2014/05/afterthoughts-pikettys-capital/

If inequality is being underestimated then it again calls into question the theoretical justifications for Piketty’s r>g assertion. He’s already made the claim that returns grow at a fairly consistent rate which he chose to put an actual number to; if that number is false then it’d back to the drawing board as he won’t get away with simply adjusting it upward to Y, not after 700 pages arguing why it is X. In the absence of more rigorous work by other economists we’re right back to knowing inequality exists but not why it exists.

The claim that r is exceeds g, usually by a wide margin, isn’t given a theoretical justification. It is an empirical claim based on actual measurements of r and g over time. The UK wealth inequality increase number doesn’t really have any direct bearing on it since no particular conclusion about wealth inequality follows from the values of r and g alone, but depends on such factors as the initial distribution of the capital stock, the rate at which the wealthy are able to save and the differences among the rates of return that different classes of wealth owners are able to achieve. r is not the rate at which returns “grow”, it is just the average rate of return. The rate at which total returns to capital grow is always far less than the rate r and depends on the capital-to income ratio, the savings rate and the rate of income growth.

Piketty doesn’t have a deterministic model of inequality growth. What he does in the part of the book devoted to the structure of inequality is identify five of six “forces for divergence” of incomes of wealth, and then builds up a cumulative case that in the 21st century those forces are likely to acquire new strength because of a combination of factors including demographics, globalized competition for capital, the long-term rebuilding of capital stocks, and the political decisions that have increased the post-tax rate of return to wealth-owners. The demographic factors are the most important. Low rates of population growth result in lower national income growth rates, and one of Piketty’s main arguments is that low growth provides an environment propitious to the growth of inequality.

The fact that r > g and the magnitude of the difference between r and g are a kind of precondition for those forces for divergence to operate. The greater the magnitude of r-g, the stronger those forces will be.

Any explanation for observed phenomena is by definition a hypothetical. Empiricism provides a What, not a How.

The how is debt created currency.

Again, I’m just saying that the UK wealth numbers are no part of any “theoretical justification for Piketty’s r>g assertion.”

How does one write about “capitalism” when one only has a system of “crony capitalism?”

I have already made a critique of the critiques of Piketty, but I’ll say it yet again. Why are we so focused on metrics that are only concerned about the flow of Capital? It is splitting hairs. Again, where are the economists that are sociologists first and foremost? As the profession should have always been. I keep hoping that academics working in the field of economics begin to understand that the discipline is not a hard science. These models are not natural law. Often they do not even well reflect the material reality of economy, as all the models hinge on ideological assumptions. A good critique of PIketty would follow in these lines rather than focusing on certain poorly driven nails in the framework of historical British GDP.

That is the truth.

I don’t know why on earth you would use a simple average in this regard.

I can think of many cases in which a country average rather than a population average seems like the more relevant number.

For example, suppose one country wants to compare the efficiency of its health care system to the systems in a group of 20 peer countries in the sense that all of those countries have roughly equivalent outcomes in measures such as longevity, infant mortality, disease levels, etc.

Suppose 19 of those countries have 20 million people and the other country contains a billion people. Suppose the country with a billion people spends 5000 per capita on health care and the other 19 spend 1000 per capita. How is that big country doing. If you take a population average of all 20 countries, you come up with $3899 in per capita expenditure. By that measure the people of the large country might say that the answer to how well they are doing in delivering health care efficiently is “not bad – only 28% above the average.”

But if you take a country average instead, you come up with $1200 in per capita expenditure, and by that measure the larger country is doing much worse, spending 317% above average.

In this case, I think the second measure is the more meaningful one, because what we are trying to do is compare alternative systems, not just regional variations within a single system. One could make the same case when it comes to comparing inequality.

In any case, as Roland has already pointed out, by giving Sweden and the other relatively egalitarian Scandinavian countries equal weight in measuring trends in European inequality, that means that he has made Europe come out less unequal than it would be if he had taken a population average.

I’ve heard this defense. Doesn’t make sense. He aggregates the states into an entity called “Europe”. If he was trying to make a state-by-state comparison he would not have done this. In your example, if he had wanted to determine the quality of healthcare in an aggregate entity called “Europe” you would obviously use population-weights. Ditto for a “European wealth inequality” measure.

Also even if he does provide a salient reason he did not do so in his source data. That’s an awful idea if you’re going to make the data public.

Whenever I hear of an economist doing a cross-national, multi decade or multi century economic study, I automatically assume he is trying to make cherry pie from apple and oranges ingredients.

Unlike everyone else, I’m never surprised someone can find fault with it. So I propose that authors release their first version of publications in a E-Book Version 1.0 format. Then after crowd sourcing the study, he can edit his work and release hardcopy 2.0. The econ book industry can learn something from the software industry.

Until then, I fear nothing will come of wealth or income inequality studies, and Royal Bloodlines shall re-inherit the Earth.

It is my understanding that Piketty’s book was based on research stretching back a decade or more and that interim papers and results were circulated. Was his underlying data made available during that period? Was there any criticism of his methodology during that period? These are genuine questions.

I will add another question: Were there no economics grad students in need of topics or publications? I know many years ago when I was a grad student in a field far, far away from economics i read the literature with an eye to spotting errors or problems.

In software we keep a “changes log” when going from version 1.0 to version 2.0. I guess they don’t do that in economics.

But in spite of the prime software vendor doing his best (?) to eventually work towards a release fit for human consumption, gaps and shortfalls still remain. This presents an opportunity for 3rd party software vendors to fill in the shortfall with supporting software products. Econ grad students will have much to do, IMO, and you can eventually get a paid job as Court Jester, too!

Piketty uses data going back several hundred years.

In his (very gracious) intro, he acknowledges the assistance of quite a few grad students who helped over the years.

Also, all his data is online – google for more details.

In Theory

There was a guy on TV a long time ago named Jed Clampett. he lived in a cabin in Kentucky, I think it was Kentucky, and went out hunting one day and shot at a raccoon and missed, and the bullet went into the ground and up from the ground came bubbling crude oil.

Evidently, he lived on top of an oil field. That made him rich even though he didn’t have capital C or income (I). So he moved to Beverly Hills and bought a mansion and hired a banker to help him manage all his money, which now was Capital.

it’s no wonder r > g. Since you have to work to get “g” but you don’t have to do anything to get C except shoot at a raccoon and miss. “Wait minute!”, the thoughtful critic interrupts. “You said he shot at a raccoon and the bullet went into the ground and up came bubbling crude oil. That’s not a return on capital, that’s just good luck with a bad shot!” Well, it was nature first, then it became capital instantaneously when somebody bought his land and put oil wells on it and then it became r when the oil was sold. So you can call it Nature or you can call it Capital, but it’s the same thing. Of course if somebody hadn’t invented oil wells and engines it would have stayed N and not transformed into C.

That’s why r > g, because to get g requires labor and that N be transformed into C, but to get r only requires that N–>C, and wealth at time n+1 is C + C’ and (C+C’)/C .> g when N–>C since N = O until it’s transformed into C, which is a infinite return on C at time t-1.

However, you could say this doesn’t work unless they paid him for the land rather than just took it. But If they took it, then it’s still N–>C and it just makes r even more bigger than g since Jed Clampett didn’t get any of the C. That happens a lot too, which no doubt is part of the problem

A minor quibble

Texas, not Kentucky. Note the reference to “Texas tea..” in the intro song. I believe you may have confused Elly May for Dolly Parton – an understandable error – they do look and sound alike… but Texas, not Kentucky.

Eastern Kentucky or Tennessee are the best guesses. Milton Friedman analyzed this in his undergraduate thesis. The Clampett legend goes back to the 1910’s.

hmm. You may be correct, considering the 1910 time frame. I thought “who ever heard of oil in Kentucky?” But we’ve also heard Jed is a poor mountaineer, and one may counter “Who ever heard of mountains in Texas?”

Actually, I have. They have some in the Austin area, albeit small ones.

But this does highlight the need for more research in this area.

And the theme rolled on when the Clintons left the White House and grossed $109 million in the decade that followed:

Well, first thang ya know ol’ Hill’s a millionaire

The kinfolks said, Hill, move away from there!

They said, Old New Yorky is the place you oughta be

So they loaded up the truck, and they crossed the Tappan Zee …

To Westchester, that is: swimmin’ pools, movie stars!

Am I alone is being surprised that it is FT that has printed the most negative commentary on Piketty’s book rather that WSJ, Fortune, Bloomberg or the NYT?

I’ve actually wondered that myself. The FT is very liberal and critical until it comes to the ‘I’ word, maybe?

Someone should do an article count on LexisNexis. I’d be fascinated to hear the result.

Wow, have you not been watching. The FT has become very neoliberal in the last two years.

My hunch is that Piketty’s work is bad for their very high-end advertising clients.

People like to think they’ve ‘earned’ that tax haven in the Caymans and the condo in Vail and the car elevator (a la Romney): to have to admit that they only have those things because their money made more money — and has zilch to do with their own efforts or entreprenurial chutzpah — is nasty for the ol’ egos.

Hence, any hope of diminishing Piketty is good for the caviar crowd.

Pity, really.

they produce some absurd magazine insert in their newspaper called “How to Spend It”. I don’t know why but it ocassionally sits on a table in the cafeteria where I work — and I assure you neither me nor anyone I work with is in that financial demographic, to be interested in How To Spend It. None of us have “It” — which I guess is like a bonus of half a million or more that gets handed to you for being there where they leverage beta, for leveraging beta, for using the right jargon and slang, and when the sh8t hits the fan for keeping your head down and the right determined and grim expression on your face while you get bailed out. In church they pace the collection plate, where you work they pass out the cash collected. Then you spend it on things like special architecturally desinnged guest houses and private jets and cameras that cost $7000. Why buy a camera like that? if you knew how to take a picture you’d realize you don’t need it, and if you do need it, if you really need it, it’s because you know exactly what you’re doing and that doesn’t ccome ffrom leveraging beta, it comes from leverraaging imagination. And it’s very precise. The ads look glamorous in that quietly gaudy and sick way, You’d think the products were weapons in some war that you’d use in forms of violent self-defense, products gauranteed to maim and kill, even the fashionable items seem intent on being accessories to a sort of murder, a sort of anonymous murder of a nameless victim and a placeless location where any relationship, any connection between action and result is so burdened by confusions that one can consider the purchase an acti of both style and virtue. That’s not to say there really ARE connections, in real life, but it is to say the evocation is one that you’d construe easily in that regard. The publication seems a form of darkness, the way a painting is keyed to a low value and even the brightest brights are dim and the darks are nearly impenetrable. That’s the way it seems to me, something so full of irrelevance to anything human as to be not so much a magazine but a hood which is placed over the head of the reader so they see only what’s in their mind and not what’s really there ouside in the sun and under the trees and the sky. Why this is in the office I work in is a mystery. And why they’d publish it, at FT, is a mystery and why anyone would read it is a mystery and why anyone who thinks they need an 7000 dollar camera when they don’t know the first thing about light and line and color and shape and composition and gesture and form and metaphor and the craft of it all, that’s a mystery to me too. The whole thing is a mystery, but it’s one that one ceases to have any interest in over time, it’s one whose solution becomes less and less interesting because it requires time to contemplate and the reasons one can think of seem less interesting than what one can do instead of think of them, which is look at a tree or out a window and imagine what you could to with a 50 camera while wearing a plain T-shirt driving a cheap car. It’s so much more than you’d ever read about in a magazine like that. It sort of discredits the FT as an institution. but who cares, it’s just a passing thought before looking oout the window again and really wondering

Indeed, the act of buying is made to seem a statement of style and virtue.

I think you’ve nailed it.

Again ;)

Piketty has some refutation for the FT:

http://www.theguardian.com/business/2014/may/26/thomas-piketty-financial-times-dishonest-criticism-economics-book-inequality

In reading that the FT’s greatest concern was with the UK numbers about wealth inequality growing more recently. The UK is a monarchy which still holds a large percentage of the land, and much real estate, along with the Church Of England, the Duke of Windsor and a small percentage of the population consisting of nobles going back over a century. They could not be rolling up even more land by foreclosures since they already dispossessed the land and own Allodial Property rights which legally is absolute, not subject to any superior claim, not even the state. But then, it is called the united KINGDOM, and are not states as such. Our property rights can be relinquished for the greater good of the public at large via Eminent Domain. The Allodial system precludes such quaint notions for the Nobility and Royalty of England.

If the English presents a problem for showing recent concentration of wealth it simply because they concentrated the wealth for themselves a long time ago. The French on the hand got rid of the titles and much of the land was redistributed and consequently held by small family farmers, to this day. The comparison of English wealth derived from rent payments for land rests on a tightly held and secretly maintained record for title to ownership, unwilling given up.

—————————————–

More than a third of Britain’s land is still in the hands of a tiny group of aristocrats, according to the most extensive ownership survey in nearly 140 years.

In a shock to those who believed the landed gentry were a dying breed, blue-blooded owners still control vast swathes of the country within their inherited estates.

A group of 36,000 individuals – only 0.6 per cent of the population – own 50 per cent of rural land

Read more: http://www.dailymail.co.uk/news/article-1328270/A-Britain-STILL-belongs-aristocracy.html#ixzz32sXNsRV7

Lambert:

If one wants to dispute the findings of a particular report, then one nitpicks the way the writer/creator got there. There are enough other studies with the same findings and other than transfers in the US, Median Income has decreased. Income is typically the presage to the accumulation of wealth.

Már Gudmundsson BIS Report “How might the current financial crisis shape financial sector regulation and structure?” which you reference in your showing of the graph 3/4s of the way down his report certainly gives an indicator of how the wealth was accumulated by the few and numbering 1 million in the US. Just before the graph this explanation appears:

“From 1990 to 2006, the GDP share of the financial sector in the broad sense increased in the United States from 23% to 31%, or by 8 percentage points. During the same period, the increase in the GDP share was in excess of 10 percentage points in the United Kingdom but significantly less – around 6 percentage points – in both France and Germany. Graph 3 shows the development of the share of the financial sector in GDP for selected major advanced economies since the middle of the 1980s. The figures on profits are even more striking. For example, the financial services industry’s share of corporate profits in the United States was around 10% in the early 1980s but peaked at 40% last year.”

Since this is a report on a broken global Financial System, one could wonder how the wealth was accumulated. Már certainly was not giving his speech about the good old days when Wall Street was “making its money the old fashion way” as John Houseman so aptly put it. We are looking at the accumulation of wealth and income through the use of CDS, MBS, CDO, false rating none of which were invested heavily in Labor creation. To grow to be 10% of GDP in England and 8% in the US, the growth had to outstrip normal growth by leaps and bounds. 40% of the corporate profits in the US were attributed to “financial services industry’s share of corporate profits .” This wasn’t the result of hiring bank tellers.

To me , the attack is a “red herring” and meant to sway people from the overall validity of the findings. England was at the top of the ratings for Gini with the US close behind it.