It’s déjà vu all over again.

I’m only starting to dig into the AIG bailout trial by reading the transcripts and related exhibits. That means I am behind where the trial is now. However, that gives me the advantage of contrasting what is in the documents with the media reporting to date. And what is really striking is the near silence on the core argument in this case.

The Starr International v. the United States of America suit is, at its core, about whether an insolvent borrower still has the right to the protection of law. It’s thus a high-end, big-ticket replay of the same form of arguments that homeowners fighting foreclosure often tried in court to obtain a mortgage modification: we don’t dispute that we aren’t able to meet our obligations, but the party foreclosing on us needs to go through the proper steps to take possession of our house. In the mortgage borrower’s case, that meant establishing standing, as in proving that they really were the proper party to initiate the foreclosure. In the case of Starr, the AIG executive enrichment vehicle controlled by former CEO Hank Greenberg, the argument is that even though AIG was insolvent, the bailout, which included through a series of maneuvers getting control of 79.9% of AIG stock, was impermissible.

Let me stress I’m no fan of Greenberg. But you can’t ask for the rule of law to operate in one place and not another. We’ve seen the administration repeatedly bend over backwards to give banks all sorts of free or super cheap waivers for bad conduct and not enforce regulations against them, yet borrowers are held in court to strict terms of their agreements and face unreasonably high hurdles when they try to fight abusive conduct.

Despite his considerable warts, Greenberg is unearthing information that shows how one-sided and high-handed the Fed’s conduct during the crisis was. Yet people who claim to be on the side of curbing bank power are instead rallying to support the bank-cronyistic Administration:

We’ve embedded the transcript from the first day of the trial at the end of the post, which included both sides’ opening arguments, along with the testimony of the first witness, Fed Board of Governors general counsel Scott Alvarez, along with the sides each side presented.

The specific legal arguments from the Greenberg camp, represented by uber lawyer David Boies, are that the manner in which the government took control of AIG’s common stock involved a taking (a violation of the 5th Amendment requirement of offering adequate consideration for government seizure of property) and an illegal exactment (more on that shortly). Note that Greenberg can prevail on either contention.

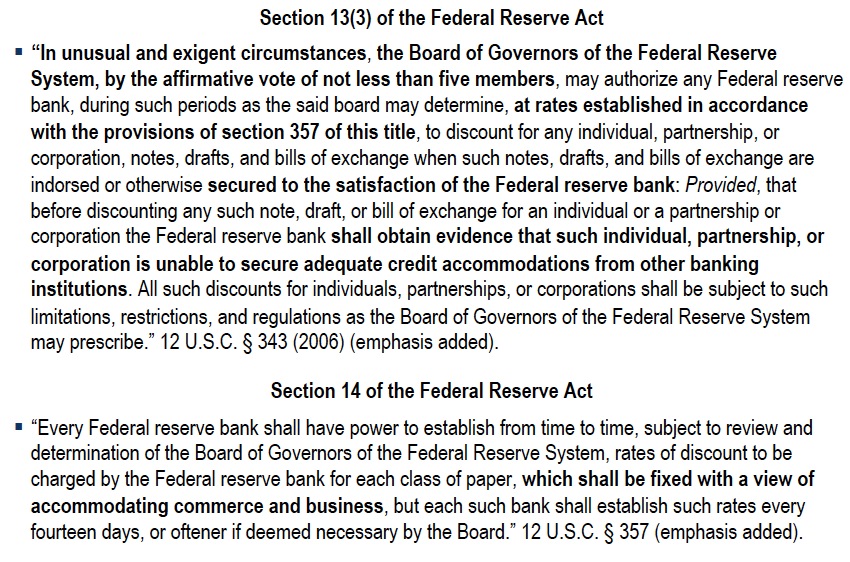

A key issue is whether the Fed exceeded its legal powers in how it structured the bailout and coerced AIG’s board into taking it. The rescue was done as a Section 13(3) loan, which is often referred to as the Fed’s “unusual and exigent circumstances” authority. While that allows the central bank to take pretty much anything it wants to as collateral for a loan and make that loan to pretty much any party it chooses to, Greenberg’s attorneys argue there are still limits on how the Fed can conduct itself. Consider this slide from the Boies’ presentation (click to enlarge):

Again, we’ll go into more detail in future posts, but some of the major Greenberg camp positions include:

1. The interest rate set can’t be punitive, which is something government officials have repeatedly stated in public and acknowledged in trial testimony. The rate is to be set “with a view of accommodating commerce and business.”

2. The central bank does not have the authority to demand the surrender of equity to make a Section 13(3) loan, which is effectively what happened here. The Fed had already obtained equity in the subs as collateral for demand notes that the board agreed to on September 16, and the 10-Q filing announcing that deal made clear that the board though it had also agreed to give equity warrants for 79.9% of the company.

But the Fed apparently determined in the following week that it would be vulnerable even with a demand note secured by all the equity in all the subs if AIG were to file for bankruptcy. The Fed had had enough direct dealings with the board and the company to have become an insider, which would lead its claims against AIG to become subordinated in the event of a bankruptcy filing.* So it wanted voting control to prevent that from happening.

This is one of the ways the illegal exactment argument comes into play. There is case precedent that supports the notion that the government can’t demand the surrender of a right as a condition of granting another. The government already had its normal condition for the granting of a Section 13(3) loan: sufficient collateral. Even though the government’s opening statement discusses the riskiness of taking equity as collateral (true), the Fed’s internal analyses already allowed for that by taking a 25% haircut and still found that the Fed had plenty of excess value.** To ask for equity on top of getting collateral for the loan is thus asking for the surrender of an additional right.

By contrast, the government’s case is almost a straight replay of the deadbeat borrower meme. AIG was toast with no bailout. The authorities could not let AIG’s ginormous liquidity problem lead to a bankruptcy filing that would bring down the financial system. So they were justified in putting in place a punitive rescue. AIG shareholders should be grateful that they got anything.

To put this even more simply, this contest is over whether the government should be allowed to run roughshod over the rule of law in the face of a potential national (actually international) emergency.

What is intriguing about the trial is how wildly divergent the approaches of the two sides are, not simply in their framing of the case, but in their approach to the trial itself. If you read Boies’ opening statement, he is clearly talking to the judge and only the judge. There is no effort to make his arguments more accessible to the media. He walks through what he contends are the thresholds he needs to meet on the two prongs of his argument and how he believes he will be able to satisfy them. The Greenberg side thus has no interest in waging a media war at this juncture. Their assumption appears to be if they win the case, the media will be forced to acknowledge the legitimacy of their position.

By contrast, the government approach to the trial, at least as demonstrated in their opening statement by Kenneth Dintzer, is classic Obama administration “any problem can be solved by better PR.” I’m not exaggerating by much. The opening statement included howlers that would not pass muster with anyone who has a passing knowledge of finance or corporate governance.

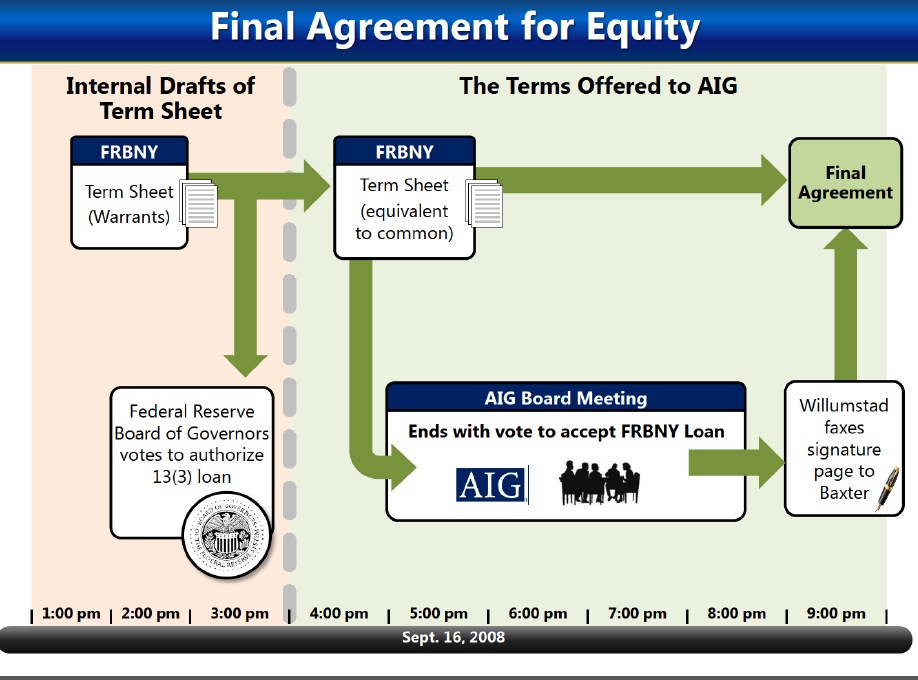

To illustrate: one issue the Greenberg camp has made centerpiece of their case is the way the board was muscled into agreeing to the Sept. 16 and Sept. 22 loans (see this post for more detail). For the Sept. 16 loan, only the CEO Robert Willumstad was ever show a term sheet, which he said was so amateurish that his children could have done a better job. The board was merely given a verbal description of terms. Willumstad, on behalf of the board, sent the government a signed blank signature page with no term sheet attached, a literal blank check.

Oh, and here is the priceless part: the government has failed to turn over this term sheet in discovery. Yet, even with this being a contested issue (and prominent enough that the judge almost certainly would remember it), get a load of this visual from the government (click to enlarge):

Do you see the misrepresentation in the slide? It show pages being presented to the board. The board never saw any documents. This is what I mean by playing to the media. The judge knows, or through his review of all the materials later, will be aware of the missing term sheet issue if it proves to be germane. But the press in the room has been given the impression the process was the board was given information they could inspect.

With that as background, Dintzer finesses the issue of whether Willumstad ever saw a term sheet (it only acknowledges that he asked for one) and claims the only one that was presented was given to AIG’s attorney. Oh, that’s Rodgin Cohen, who also happens to be Goldman’s attorney.

This is the government’s contention in the absence of coughing up any documents:

So, instead of identifying a specific form, the term sheet will indicate that the form will equal 79.9 percent of common stock but will not identify a specific type of equity….there is no ambiguity, no confusion regarding the terms of the agreement, and indeed, the parties issue press releases showing that they had the same view of the agreed-upon terms.

Our archives on Sept. 16 show both the pre-announcement leaks and news reports after the deal was done describing the equity component as warrants. AIG was directed by the government to correct its 10-Q, which described the equity component as warrants.

Here is another insulting-to-the-finance-literate discussion:

And, Your Honor, DX 161 is a memorandum written in March of 2008 that addresses just this issue, and it was sent to President Geithner of the New York Fed. The memo states: “This memo discusses whether a Reserve Bank is empowered to take ‘equity kickers’ in discount window lending under Sections 10B or 13(3) of the Federal Reserve Act.” It then goes on to state: “We believe that there are many different permissible routes to a finding that a Reserve Bank is empowered to take an equity kicker…”

An “equity kicker” in the lexicon refers to warrants or other contingent forms of equity. The government needs to provide stronger language than that to prove its claim.

And we have this cute bit that probably went over the heads of the crowd:

Moreover, the illegal exaction argument, Your Honor, it’s a red herring. The credit agreement expressly required that if one form of consideration under the agreement turns out to be illegal, AIG would have to provide an equivalent substitute.

Huh? This is circular. You can’t cure an illegal exaction by substitution.

Oh, and if you read to the end of Dintzer’s opening remarks, you’ll see he states that both the general counsel of the Fed Board of Governors, Scott Alvarez and the general counsel of the New York Fed, Tom Baxter, advised that the loan was legal.

Boies jumped on that right after the opening remarks. The government has just waived attorney client privilege, while the trial is in progress, after discovery is supposed to be finished. This is astonishing. You don’t do this sort of thing casually, if at all, and opening remarks is not the time to do it. The judge agreed to let the Boies perform discovery on this issue while the trial is in progress.

Now I’m picking particulars to demonstrate that the judge can’t have been the intended audience, that indeed, running these sloppy and dubious arguments run the risk of losing credibility with Judge Wheeler, who seems very sharp and sympathetic to the Starr arguments. But you get that impression even more strongly if you skim the government’s opening statement. It’s a dumbed down, low information density exercise in storytelling, not what you’d expect in a case like this.

Even though Boies has gotten off to what looks like a good start, it’s surprising to see him fail to take more aggressive positions on key issues. The government’s statement that an AIG failure would take the financial system down is a damaging admission. The government tries to depict that the tsunami would wash over the banks as a result of an AIG implosion, via the damage to the repo market and the impact on the insurance industry (which is dubious since the insurance subs weren’t part of the problem. The insolvency was at the parent company level).

But it is incorrect to regard the bank balance sheets as separate from AIG’s. The AIG credit default swaps reduced the risk weighting of assets at banks, allowing them to carry less equity. Or to put it in another way, AIG was effectively providing synthetic equity. So a failure of AIG would impact the banks directly as a result of their economic interdependence. I’m not sure why Boies didn’t include this in his line of argument; perhaps to get into how the use of AIG’s credit default swaps allowed banks to lever up more would be too complicated to go into, given that the regulatory treatment was different for the three major types of counterparties: US investment banks, US commercial banks, and European banks. But it seems like a lost opportunity.

The overall impression from the opening day is that the government is so confident of its position that it feels it can play to the gallery. Its assumption seems to be that it deems odds of loss at trial as low, and even if that were to happen, it will beat Starr on appeal. But as Gene Ludwig told me when he was my attorney, litigation is a crapshoot. And I wouldn’t overestimate my odds when playing craps with David Boies.

_____

* Even this seems like a stretch; Bernanke, Paulson, and Geithner all said they would not let AIG file for bankruptcy. So was the concern that AIG would somehow take advantage of the Fed later and threaten a bankruptcy filing to retrade the deal? That seems implausible given that top financial services regulatory lawyer Rodgin Cohen told the AIG board on September 22. Then, the board was expecting the Fed to offer a longer-term credit facility on the same terms as the demand note it had agreed to on September 16. Instead, the board was told that AIG would have to accept a much higher interest rate and give control of the company to the government. Rather than take 79.9% of the equity of AIG in warrants, the government now wanted to have control now by getting voting preferred stock tantamount to a 79.9% interest.

Cohen, who had told the board on September 16 that he would be willing to give an opinion letter supporting the board if they were to file for bankruptcy then, told the board on September 22 he could not provide the same legal cover if they decided to defy the government. I have been told that the reason for the change in Cohen’s views is that on Sept. 22, AIG was encumbered by the Fed’s demand note, which was then $37 billion. On Sept. 16, if AIG had filed for bankruptcy, it could have obtained debtor-in-possession financing. With the Fed demand note in place, that looked a ton more dicey.

** Even if you don’t deem 25% to be high enough, that was the level the Fed used, so they can’t have it both ways.

BSF_Opening-v2.5-with-slidenumbers

BSF_Opening-v2.5 with slidenumbers

Starr-US-Opening-Demonstratives

Starr US Opening Demonstratives

2014.09.29-Day-1-Full

2014.09.29 Day 1 Full

“Let me stress I’m no fan of Greenberg. But you can’t ask for the rule of law to operate in one place and not another.”

I think you just provided a pretty good real-world example of what’s wrong with the bourgeois conception of “the rule of law.”

I agree 1000% – how many examples do we need that the law is a chimera. Maybe it was ever thus, but it seems like they are not even trying to pretend that the law is enforced in an even handed manor…

The whole point of the rule of law is for courts to protect the weaker party. You are seriously willing to throw that out of cynicism? Are you insane?

There were borrowers who used the chain of title defense successfully. In New York State, judges imposed a requirement after the robosigning scandal that lawyers initiating foreclosures certify that the documents they submitted in court were valid. In theory, they had that duty all the time but from a procedural standpoint, the certification requirement lowered the bar for counsel for the borrower to seek sanctions.

As we documented, foreclosures came to a screeching halt. It appears that lawyers who couldn’t prove that their client had the standing to foreclose weren’t willing to risk getting whacked by the judge. So the system did work to protect the little guy. Similarly, with debt collectors, when borrowers go to court, even pro se, they can almost always beat them because they debt collector doesn’t have the original documents with the borrowerr’s signature proving that the debt was owed, along with the records showing why they owe what they owe.

We need to press for much better funding for legal services so more low income people have access to counsel, and not throw up our hands and say “the system sucks”.

Based on the 9th Court of Appeals ruling in 1982, in the Lewis case, the plaintiff was not permitted to sue the Federal government for the behavior of the Fed. Greenberg should sue the Fed separate from the US government.

The Fed and Treasury worked in tandem on the bailouts, and the Fed has delivered documents in discovery, so they are accepting inclusion.

Thanks for your continuing work on this. Loved the use of the word really. (“And what is really striking is the near silence on the core argument in this case.”)

It’s a little unfortunate Warren went for the simplistic badgering rather than highlighting the more nuanced aspects of the conduct. Thanks to the intertubes, we were all there. Everyone knew, in basically real-time, that this was a disaster by the government and a blatant bailout of Goldman.

AIG should also argue that the contracts that they insured were fraudulent, so their value was $0, and they owed nothing to Goldman, etc.

I am not certain if my previous comment posted? Apologies, if it has posted.

Based on their capital, AIG also entered into the contracts fraudulently. They knew full well they did not have the capital to make good on the contracts given normal market movements. They choose to speculate in excess of their capital to make good on the contracts, due to the lure of the out-sized income they could generate. That is deemed contract fraud.

The US Taxpayer deserves an investigation. Why did the Federal Reserve make US taxpayer payments under contracts that were entered into fraudulently? These were not “insurance contracts”. They were ISDA financial contracts and both parties had the responsibility to enter into the contracts with knowledge of the financial capability of their respective counterparty.

There is sufficient evidence to support the fact that both AIG and Goldman were aware the underlying asset had questionable value and AIG did not have the capital to support the speculative trades they made on these securities. Goldman was also well aware of the ability of AIG to make good on the contracts based on their published financial statements. This issue must be investigated thoroughly for every US taxpayer.

AIG also entered into the contracts fraudulently. They knew full well they did not have the capital to back them up. That is by definition contract fraud. Based on AIG’s published financials, Goldman was also well aware of this fact.

The head of their unit was an experienced swaps trader. The US Taxpayer deserves an investigation as to why the Federal Reserve used US taxpayer dollars to pay off counter parties under financial contracts that were entered into fraudulently by both parties. They could have been nullified, saving taxpayers billions of dollars, without a collapse of the US financial system.

There is sufficient evidence to launch this investigation, in fact in should become part of the current trial.

Yves, it’s unfortunate that you had to include “deadbeat” with the word “borrower” in your title. Why continue to repeat the lies of the bankers? It really pisses me off.

Come on. You can’t refer to a meme without using the words without looking silly and precious. Yves also talks about ideas like free trade and free markets even though she’s said those expressions are business propaganda too.

I would agree with Fawkes. The cause of the toxic lending was the financial system, and globalists to be more specific.

Can’t we just pretend that the assets of AIG were needed to build a huge football stadium for a rich team owner and call it a day?

You joke.

Stowe, wholly owned by AIG, was building out a TON during the crash. They never lost a day. In the middle of a finance crash, building a castle in their own resort fiefdom.

http://www.stowe.com/about/about/spruce-peak-development/

Lots of collateral in a bid-up-by-employees town couldn’t go down in value. “systemically important assets”

Good luck trying to find anything about stowe in an AIG report. They, and their employees(Starr and AIG), literally own the entire town. They have what amounts a zero cost lease in perpetuity for the entire east side of mt mansfield, from the state of VT.

http://en.wikipedia.org/wiki/Stowe_Mountain_Resort

Lake Champlain must be Jason’s eternal home. The stuff that comes out of around there is best describe as the “Things”, offspring are a hoot too…

In the USA, if you are an aggrieved white male loaded to the gills with bucks you can get your day in court even when facing down the government. Others, that are less fortunate and undoubtedly more numerous, who may be put in a similar situation must take their lumps and move on to endure their pain in silence.

That’s why the Homeowners Super PAC needs all your support!

http://www.HomeownersSuperPAC.com

Find us on Twitter and Facebook!

Going live soon.

Logical fallacy. The fact that others are wronged does not make Greenberg’s case less valid. And see above: http://www.nakedcapitalism.com/wp-admin/comment.php?action=editcomment&c=2331378. Some judges did change their stance towards banks once the robosigning scandal broke. There have been nationally important decisions in favor of borrowers, such as Ibanez by the Massachusetts Supreme Judicial Court, as well as decisions against MERS.

One of the biggest sources of harm to borrowers was the Obama Administration, in negotiating the second bank bailout of the 2012 National Mortgage Settlement, which was a get out of jail almost free card on chain of title issues. Several state attorneys general had been pursuing that issue seriously, and the Administration made sure to get them out of action. Had they continued with their cases, the facts they had gotten in the record would have been leveraged by private attorneys, both borrower and investor attorneys, and greatly increased the odds of homeowners defending themselves against wrongful foreclosures. The system was working, albeit slowly, until the Administration derailed it.

but where are the damages? if not for the bailout, AIG shareholders would have had nothing. In this case the flawed process is irrelevant. (so maybe there is a judgment in favor of AIG but an award of $1?) with the foreclosure problems (robosignings, failure/refusal to provide payoff figures), the ‘process’ failure was fundamental, e.g. many banks/mortgage companies trying to foreclose couldn’t even prove that they held the underlying note/mortgage.

Some of the biggest wrongs that have happened to the Homeowners fighting foreclosure is that these federal and State Attorneys General lawsuits have not moved forward into discovery stage and provided the Homeowners with real help. If these lawsuits would release the discovery, the Homeowners would be better armed with the discovery of these crimes. Taking monetary settlements rather than pushing these litigations to favorable Court decisions has really left Homeowners to struggle in their own private litigation.

My personal speculation is that the AIG suit is a shot across Obama’s bow, an early warning that when he leaves office his card goes out of the Rolodex.

After the trillions of taxpayer dollars, after the laws ignored to keep bankers out of prison, after all the hard words left unspoken, his reward is going to be a smile and a hardy handshake. If that. Unlike the Clinton Foundation, which has grown past $250 million, the Obama Foundation is never going to see a nickle from the financial industry. I mean, what has he done for them lately?

Per the University of Chicago, gratitude is measured in dollars. The financial MOTU probably consider they’ve paid for what they got, now it’s just business.

What have they got lately? Ummm, they did not receive 3 hots and a cot and Bubba as a roomie. Pretty huge pay out in my humble opinion.

The only reason Obama will be left off the bankster donation list is because he is not white.

Greenberg is rich but not politically connected. That is one of the reasons AIG was used to launder bailout money to the banks. Obama has gone to great lengths to curry favor with big swathes of Corporate America: banks, big Pharma and health insurers, the military industrial complex, the frackers, the list goes on.

One pissed off billionaire does not change that equation.

Well said, Yves.

“Greenberg is rich but not politically connected.”

woah. I might give you that he was insulated enough to not loose everything, therefore they took what they could, and he didn’t/couldn’t want to put up too much of a fight at the time. But greenberg not politically connected? YGBFKM.

On intel value alone, he’d probably rank in the top 50 nation states, as far as power goes. That’s about as politically connected as you can get. Having Boies repensent you is also a pretty good demonstration of “political connection”. Isn’t he the guy that argued in front of the supreme court over who the next president would be in 2000?

And really, how is his plan of not putting up much of a fight at the time going to work out? He’s doing pretty well, and he’s got a shot at a few hundred million dollar gamble(at least) within the courts, holding a pretty good hand. I’d call it a “synthetic t-bill”, a good claim on gov money.

Power is all about knowing when to use it. To claim he’s not politically connected is simply not true.

The whole point of the child’s term sheet may have been to give AIG recourse.

Once timmah and benny decided that they wern’t going to let AIG go BK there was a pretty simple choice. Let goldman et al take control, or let the gov borrow your company for a bit. You might be able to get it back from gov. Goldman, or rather, “the bond market”? No way in hell.

Put another way, AIG was going to have to make a loan. Who they made the loan to was up in the air. Are you going to ‘lend’ a bank money in a finance crash? Or, are you going to ‘lend’ it to the issuer of the reserve currency of the world? Who was the better credit risk at that time?

Boies is for hire. Look at his client list. You don’t need to be “politically connected” to hire an attorney. You need to have money and a minimally viable case, and an attorney who does not have an existing client conflict.

And I stand by my statement. All of Greenberg’s intel connections did him no good when AIG was floundering. He tried to gets meeting with Treasury and the Fed and no one would see him, while Goldman had ready access. He was not a big political donor and worked hard to have no real regulator, which also meant he had no defenders in court.

Interesting analysis, I hope you post the remaining transcripts! Also, I’m hoping someone calls the board members who voted to approve the bailout and asks them about the “voluntariness” of the board’s decision and the scope of what they understood they were approving. From what I’ve read so far (which isn’t much), it sounds like they aren’t going to be called…

My biggest problem with Greenberg’s suit is the blatant hypocrisy: On the one hand Greenberg blames the big bad Federal government for an illegal bailout which was allegedly forced upon the board, but on the other hand he also insist that some type of bailout was vitally necessary to save AIG. Although Greenberg asserts that certain provisions of the bailout were illegal under 13(3), he simultaneously claims the overall decision to “award” a bailout was perfectly legal and that bankruptcy was never a viable option.

As a result, Greenberg is asking a court to “re-write” the bailout documents by “severing” the unlawful provisions and thereby re-writing a different bailout package which the parties’ did NOT agree to and likely never would have. Even if Greenberg proves that certain provisions of the bailout were unlawful, I don’t see how a court could do anything other than rescind the ENTIRE transaction. In sum Greenberg has proved he loves big government bailouts, but he wants to quibble about the details…

You are misconstruing his arguments.

They are:

1. The government after they got the bride loan would not let them declare bankruptcy. This was a liquidity crisis, not a solvency crisis. Even the government’s own analysis showed that, even haircutting the value of the insurance subs from their crisis value and netting out the liabilities, there was still at least $30 billon in excess value. You can file for bankruptcy when you have positive net worth, which even the Fed’s own analysis says was the case with AIG. So had AIG filed for BK, in theory the shareholders would have been better off. There are plenty of cases where the creditors all get paid off in a BK and there is $ left over for the person who filed for BK precisely because it was a liquidity issue (this often happens with art dealers, for instance).

2. AIG had private sector offers, substantial ones, from the Chinese sovereign wealth fund, the Singapore sovereign wealth fund, and big Middle Eastern investors. Remember. Al Walled ALONE bailed out Citi in the early 1990s. Once the government had crossed the Rubicon of giving AIG a bridge loan, there was no reason not to play out these offers to minimize costs to the US taxpayer…unless other motives were at work.

3. Section 13 (3) loans by statute do not allow punitive rates to be charged. And contrary to the impression that the Treasury and Fed have given, Section 13 (3) loans were NEVER intended to be for banks only. The were to facilitate commerce in extreme times (for instance, although they have never been used that way, you could have 13 (3) loans supplement disaster relief).

No one except AIG was charged punitive rates Yet AIG was merely the dumb sucker that insured CDOs and bought subprime paper. They didn’t create toxic product, or entice/mislead unsophisticated borrowers into taking more in the way of loans than was sensible at their income level (or put them into loans with resets when the consumers though they were getting fixed rate, that has been documented to have happened too).

AIG was never sued or paid fines or engaged in settlement for bad conduct in the runup to the crisis. All they are guilty of is having a greedy, bullying ex-CEO who did less actual harm than all the other greedy, bullying CEOs of financial firms. So why are you so angry about this? Your ire is really misplaced.

1. Are you suggesting that AIG board members will testify that they were coercively pressured not to file bankruptcy, or that they wanted to file bankruptcy but were prevented from doing so because of government pressure? As I read the Plaintiff’s filings, they never argue that bankruptcy would have been a better option, that shareholders might have been better off in bankruptcy court, or that the board wanted to file bankruptcy but was coerced not to file. It appears the government is claiming the shareholders would definitely have been worse off in bankruptcy, and the Plaintiff’s don’t seem to dispute this. I’ll have to re-read the Plaintiff’s papers when I have a chance to verify this.

2-3. For the sake of argument, lets say that all complained-of bailout provisions were “unlawful” on constitutional and/or statutory grounds; given that, what are the “damages” and what is the proper remedy? You can’t be financially compensated for unlawful government conduct, if the unlawful conduct isn’t directly traceable to a legally cognizable injury.

You should’ve read Yves’ first piece on this trial. The fact is AIG had quite a few private parties willing to provide the money to keep them afloat, but the government nixed those offers on AIG’s behalf and then imposed a draconian, bank-favoring bailout. So no, its not so simple.

AIG alleges this, but it appears they will not be calling any witnesses to testify in support of these allegations. I guess we will have to see how the trial plays out…

The complexity of the two cases are of two completely different orders of magnitude. Valuing AIG during a time of extreme financial turmoil compared to verifying if a mortgage-debt was legally due and collectible.

The reason why a mortgage debt is not current might be very complex but verifying the size of the debt and whether or not it is due should not be a complex issue. US courts failed to deal with the mortgage debt. The system worked for lawyers – they got paid. Not sure if I’d say that it worked for anyone else.

What possible reasons are there for making something so basic as mortgage debt into something so complex that even judges apparently couldn’t follow the law?

I love the use of the term “synthetic equity”–that’s exactly what it was. However, keeping in mind that I’ve only read approximately half of Boies’ opening statement, what comes across to me is Boies arguing that no other institution that received 13(3) financing was required to give up equity. He repeatedly remarks that 200 institutions received similar financial help and that only AIG was treated differently by virtue of equity being taken . Seems to me he is pushing the fairness argument. If so, he would want to avoid pointing out that AIG played a different role in finance than other institutions receiving a bailout.

I suspect Boies’ biggest problem will be his need to intentionally avoid discussing the reasons behind AIG’s collapse, the conduct of the board of director’s and senior management, AIG’s own responsibilities for its “liquidity issues”, etc etc.

Boies’ conveniently omits the fact that during and immediately after the 13(3) bailouts were “awarded” to AIG, large numbers of commentators, angry voters and members of Congress questioned whether the Federal Reserve had ANY authority under 13(3) to bailout AIG in the manner they did. It is undisputed that the Federal Reserve determined, in it’s sound discretion, that 79.9% ownership was necessary to “adequately secure” the taxpayer-funded loans, and thereby assure Congress and the White House that the bailout properly complied with 13(3). If it was illegal to take the 79.9% ownership, it seems quite plausible the Federal Reserve would have simply rejected the bailout and directed AIG to bankruptcy court.

[Incidentally Boies’ is a brilliant lawyer and he is doing an excellent job advocating for his client, he clearly has a hard case]

13 (3) loans were never intended to be for banks only. The statue allows them to go to individuals and partnerships, basically anyone the Fed deems a valid target to help facilitate commerce in “unusual and exigent circumstances.”

Now the Fed makes a huge deal out of “oh we didn’t regulate these guys, we didn’t know them.” In fairness, AIG is a monstrously complex company. But everyone, and I mean everyone at that time, had no doubt about the solvency of all the insurance subs. The ONLY two parts of the company that were toast were the holding company (where the securities lending operation took place) and the Financial Products Group. They could, and effectively did, treat all the rest of AIG as a healthy black box.

The Fed also did not regulate Goldman or Morgan Stanley. The Fed gave up supervising primary dealers in 1992. And I guarantee they had no clue (because they lacked the competence) to asses their derivatives exposures. So was AIG really the bigger risk in September 2008? Even American Express got a 13 (3) loan!

Remember also that the banks got tons of additional goodies in the bailout that everyone has forgotten about. For instance, AIG was made to sign away its right to sue the banks over having insured toxic product. The FHFA just got about $20 billion in settlements for mis-sold RMBS, which were less toxic than CDOs, AND AIG would have contractually had at least as good rights to get to the loan files (the usual hurdle in proving fraud).

Liz Warren, useful idiot.

Hank Paulson and his $500 million tax free $$$, saved Goldman Sachs by laundering thru AIG at 100 cents….

Well it sounds like the Government lawyer is doing a great job; I love these quotes from the Government’s opening statement:

This is a falsehood. What benefit did the shareholders get when their ownership in the equity of the company went from 100% to 20.1%? Who pays Nate to post here?

20% of something is better than 100% of nothing, no?

“Plaintiffs quietly accepted this benefit until AIG had fully recovered”

This appears to be right to me.

Another HR. I’m still celebrating the SF Giants win… You break down all of the issues excellently. I am no fan of A.I.G. or Buffett’s reinsurance operation as I have dealt with both individuals.

Yves

Nice analysis.

Where are the transcripts found on-line? Ordinarily, in ECF, they are held for 90 days (open courts, correct!).

DJV

You drank the cool aid on this one!

Everyone has seriously confused AIG “The Insurance Company” Assets with AIG the Holding Company Assets!

The first had Reserves as required by law to pay (Insureds) claims.

The latter was legally insolvent as was every Major Wall Street Bank when a TARP was thrown over the systemic corruption!

The FED printed money and gave it to Wall Street to make them liquid!

None of the criminals trading the Junk the FED bought with public money have gone to jailL

A Public Fraud in the Trillion$!

FYI, the daily trial transcripts are all posted here at the very top:

CORRECTION: For some reason the link didn’t come through:

http://starrvstheus.com/filings.html

Nate:

Thank you. They have transcripts up to October 10, 2014.

djv

I always felt we needed a rich person who could afford the legal cost to give us a blueprint to challenge the Federal Government’s taking the properties of citizens as is the case of all the Ginnie Mae Mortgage Backed Securities (MBS) loans that were foreclosed without due process. In the case of Wells Fargo Bank’s handling the defunct Washington Mutual Bank (WaMu) issued MBS that the Notes were at the time of the creation of the MBS the Notes had to be endorsed in blank without a purchase occurring. Those Notes were relinquished and physically placed outside the hand of WaMu to Wells Fargo who was acting as the custodian of record.

Wells Fargo after WaMu was seized on Sept 25, 2008 kept a low profile as the WaMu loans were supposed to have been thought to have been purchase bu JPMorgan, however this was not the case as these loan were already involved in a post home loan closing transaction that did not involve the homeowners where the home loan payments were to pay the lender/issuer of the MBS.

Now as the WaMu is declared a “failed bank” by the FDIC who engineers the JPMorgan sale does not do anything to clear up the issue of what in fact JPM has purchase. So Wells Fargo is allowed to act as if they purchase the loan they been mortgage servicing starting in Jul 31, 2006 in the deal for the 1.3 million mostly government insured loans.

After Sept 25, 2008 any and all of the Ginnie Mae pooled loan of WaMu that were foreclosed using the non-judicial procedure were done with forgeries order by Wells Fargo from MERS and denied due process and the homeowner’s US Constitutional Rights were violated.

Wells Fargo so arrogant and ignorant that they allowed a situation that could have cost them at first a million dollar problem to billions of dollars, because full knowledge of their crime would not have been realized, because they could have simply agreed to a violation that was first realized. However as Wells thinks they are above the law, they continue abusing as if there is no punishment for what they do!

The man is Hank Greenberg who knew the government stole his property, just as they stolen government insured loan homeowners, and the same Three Stooges in Bernanke, Paulson and Geithner set out to punish these homeowners unfairly. They took what they could not take as they had “No Standing”. Thank Mr. Goldberg for the blueprint!