Yves here. It’s frustrating to watch Fed officials and pundits wring their hands about how all that super cheap money is not finding its way into the hands of small businessmen who are the engines of job creation in the US. One reason why is that businesses that in the real economy (and not in the business of goosing stock prices for the benefit of top executives) don’t borrow just because money is on sale but because they see an opportunity. In this spotty “recovery,” there are plenty of company owners who are not in the mood to stick their necks out by borrowing to try to expand.

But another big factor is that banks have exited small and medium sized business lending. Until sometime in the mid 1980s, banks had credit officer training programs that taught them how to lend to businesses large and small. The training was extensive and took two years at big banks like Chase Manhattan. The graduates went on to make big corporate loans or to get on track in retail branches to become branch managers, where they’d oversee loan approvals and get involved personally in assessing the larger or more complex loans in that branch. But as Wall Street kept encroaching on traditional bank lending, and more and more of the credit officers themselves got MBAs and often wound up in investment banks, commercial banks almost entirely abandoned credit assessment and embraced securitization.

A colleague, Amar Bhide at Tufts, argues that securitization requires standardized, low information content assets. That is one reason that collateralized loans are preferred for securitization: there’s a false sense of security in describing the value of the loan in various ways in relation to the value of the collateral (after all, if a market falls completely out of bed, as Texas did in the oil bust of the early 1980s, all those collateral “values” and income streams go poof).

Needless to say, as this VoxEU post alludes, the shift over time to prefer collateralized lending has the effect of channeling funds to less productive sectors of the economy, such as home and office building, over more productive investment. This echoes the findings of an important Bank of International Settlements paper by Stephen Cecchetti and Enisse Kharroubi which describes how financial services sectors become overgrown and drag down growth. From a summary in the Economist:

In short, the finance sector lures away high-skilled workers from other industries. The finance sector then lends the money to businesses, but tends to favour those firms that have collateral they can pledge against the loan. This usually means builders and property developers. Businessmen are lured into this sector rather than into riskier projects that require high R&D spending and have less collateral to pledge. On a related note, see our recent Free Exchange on how bank lending has become more focused on residential property.

A property boom then develops. But property is not a sector marked by high productivity growth; it can lead to the misallocation of capital in the form of empty Miami condos or Spanish apartments. In a sense, this echoes the research of Charles Kindleberger who showed that bubbles are formed in the wake of rapid credit expansion or Hyman Minsky who argued that economic stability can lead to financial instability as financiers take more risk.

By Clemens Jobst, Economist at the Oesterreichische Nationalbank, Research Affiliate at CEPR and Stefano Ugolini Assistant Professor of Economics, University of Toulouse. Originally published at VoxEU

Central banks today provide liquidity exclusively through purchases of (mostly) government bonds and through collateralised open-market operations. This column considers the evolution of liquidity provision by central banks over the past two centuries, and argues that there are alternative approaches to those that are focused on today. One such alternative is a revival of the 19th century practice of uncollateralised lending. This would discourage market participants from relying on informational shortcuts, and reduce the likelihood that informational shocks trigger collateral crises.

One of the most acute problems experienced by developed countries since 2008 is that the expansion of the monetary base has not been matched by an expansion of credit to economic activity. In January 2015 loans to the private sector were still contracting in the euro area, despite a steady increase in the money supply. The long-lasting contraction of credit has particularly hit small and medium-sised enterprises (SME), which have often found themselves exposed to rationing. The question of how to repair the transmission channel has therefore naturally emerged. Given the malfunctioning of bank lending channels, should central banks find alternative strategies for easing SMEs’ access to credit?

The Limits to Collateralised Lending

One possible solution involves designing better mechanisms for securitising small corporate debt – once turned into standardised collateral, SMEs’ highly idiosyncratic debt could thus be made eligible to central bank operations (e.g., see Brunnermeier and Sannikov 2014). By intervening directly on the asset-backed corporate securities market, central banks could in this way bypass the banking system. This would not actually imply any major change in monetary policymaking for major central banks, who engage exclusively in collateralised operations today. As recent experience and theoretical developments have shown, however, the big problem with standardised collateral is that it is constructed precisely in order to allow lenders to save on information-gathering costs. As a result, the price of standardised collateral tends to be prone to informational shocks, which can easily trigger money market freezes (Gorton and Ordoñez 2014). In such circumstances, the only way a central bank can prevent the freeze of a collateralised loan market is by transforming itself into a ‘market-maker of last resort’ – clearly a suboptimal outcome (Buiter and Sibert 2007). All this suggests that collateralised loan markets might not necessarily be an ideal intervention ground for central banks – especially when the risk of a ‘collateral shock’ is highest. An alternative might consist of going the opposite way – rather than operating on a standardised collateral debt market that incites participants not to collect information, the central bank could operate on an uncollateralised debt market that does incite participants to rely on valuable information.

Two Concepts of Liquidity

Uncollateralised and collateralised lending can be associated to two different concepts of liquidity, corresponding respectively to today’s definitions of liability-side (funding) liquidity, i.e. the ease with which funding can be obtained; and asset-side (market) liquidity, i.e. the ease with which a given asset can be sold (Holmström and Tirole 2010). In some scholars’ view, these two concepts of liquidity are but the two sides of the same coin (e.g., see Brunnermeier and Pedersen 2009) – but this applies only if liability-side liquidity can be exclusively obtained through collateralised loans, access to which is proportional to available collateral. This is not necessarily always the case, though – when uncollateralised transactions are easily available, funding and market liquidity are not bound to behave accordingly. The reason is that uncollateralised operations may involve other kinds of (moral) guarantee (Ghatak and Guinnane 1999). This suggests that the two concepts do not perfectly coincide. The fact that the central bank chiefly provides the one or the other type of liquidity will provide different incentives to information-gathering by money market participants.

Central Bank Liquidity Provision During the First Globalisation

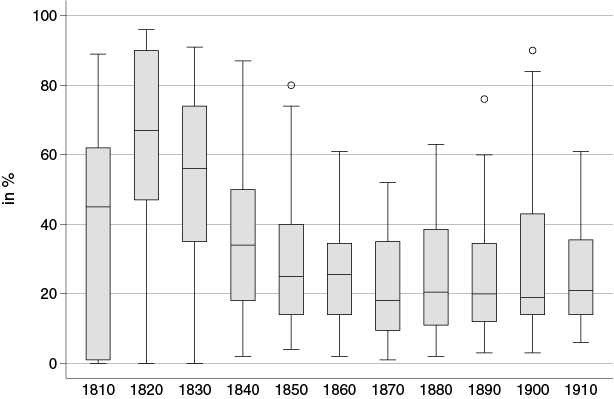

In a recent paper, we reconstruct the way central banks’ liquidity provision has evolved over the last two centuries (Jobst and Ugolini 2014). We find that uncollateralised operations were long-preferred to collateralised ones as a means for providing liquidity to the economy – the share of collateralised operations in total lending constantly declined from the end of the Napoleonic wars to the mid-19th century, and recovered substantially only in connection with the world wars. Although the situation differed from one country to the other, uncollateralised loans were thus predominant everywhere in the period between these two major geopolitical shocks (see figure 1). Therefore, during the first globalisation central bankers appeared to prefer uncollateralised over collateralised operations. Why was that the case?

Figure 1. Share of collateralised operations in total domestic lending (averages per decade)

Source: Jobst and Ugolini (2014). The database includes ten countries (Austria, Belgium, Switzerland, Germany, France, Italy, Netherlands, Norway, UK, and US). For individual country data, see table 2 in the paper.

Note: Each central bank is one observation. Boxes cover observations between the first and third quartile (inside line being the median), whiskers cover the remaining observations except outside values. Outside values (smaller/larger than the first/third quartile less/plus 1.5 times the interquartile range) are plotted individually.

19th century central bankers’ bias for uncollateralised operations

The extent to which central bankers engage in one of the two interventions may be related to the credit risk associated with each type of operations. In principle, thanks to the double guarantee provided by the borrower and by the collateral, secured transactions should be less risky – in particular if the collateral consists of easily marketable government securities and haircuts are significant. However, unsecured lending through the purchase of commercial bills (the standard 19th century discount operation) also benefitted from the additional safety feature provided by the joint moral guarantee of all persons (at least two) who had signed the bill. Unlike marketable securities, moreover, bills were subject to credit risk but not to market risk, as their price at maturity was not liable to vary. As a result, none of the two types of operations was necessarily superior to the other as far as risk is concerned.

Commentators unanimously report that discounting of uncollateralised (but jointly-guaranteed) commercial bills was clearly preferred in the 19th century:

• Discounting was deemed to provide more flexibility for the adjustment of overall liquidity. Continuous backflows from bills falling due could facilitate the granting of new loans to new counterparties, which was useful whenever money markets were not working perfectly. Central banks might have been forced to prolong collateralised loans, or face difficulties selling the collateral. Bills, on the other hand, were considered to be ‘self-liquidating’, a widespread notion in 19th-century banking (Plumptre 1940). The same concern about liquidity can also explain the preference of many central banks for real bills over finance bills, as finance bills (with their need to be rolled over at maturity) rather resemble collateralised loans in moments of financial stress.

* It was possible to derive valuable information on economic activity from the bills submitted to discount. Central banks were big players in the money market. For instance, around 1900 40% of all bills originated in France each year passed through the Banque de France’s discount window (Roulleau 1914). Central bankers were hence necessarily concerned about financial stability, and the discounting of bills was thought to provide the possibility to manage the extent of risk-taking in the economy, because the origination and distribution of bills were possible to track (Flandreau and Ugolini 2013). Moreover, by encouraging or discouraging the presentation of certain types of bills for discounting at its discount window, central banks could encourage or discourage particular activities or sectors (Allen 2014).

The 20th Century Change

Central bankers’ attitude seems to have changed following the crowding-out of the commercial bill market by the government debt market, engendered by the world wars. The costly information-gathering mechanisms put into place in order to monitor risk-taking in the bill market became less and less useful, and central bankers gradually started to dismiss them. This prompted a rethinking of the concept of liquidity, which became closer to the modern one – according to which asset- and liability-side liquidity are but two sides of the same coin (Plumptre 1940, Brunnermeier and Pedersen 2009). Today, central bankers no longer focus on the maturity of outright holdings (i.e., their being self-liquidating) but on the possibility to sell them on the market if need be (i.e., their ‘shiftability’). Shiftability, however, appears to be very sensitive to informational shocks (Gorton and Ordoñez 2014). As a result, central banks have increasingly found themselves exposed to collateral crises – and hence, to the risk of having to become market-makers of last resort.

Concluding Remarks

Unlike their 19th century predecessors, today’s central banks no longer try to have access to superior information than markets – as any other market participant, they rely on the informational shortcuts provided by collateralisation. As a result, central banks appear to be fatally doomed to become market-makers of last resort whenever informational shocks trigger the unravelling of collateral crises. An alternative might consist of reviving 19th century practice and reactivating uncollateralised lending, thus encouraging all market participants not to rely on informational shortcuts. This might perhaps provide a more efficient strategy in order to repair the transmission channel. Sure, the costs of rebuilding information-collection mechanisms might well be substantial; but economies of scope must exist between monetary policy implementation and the carrying-out of the financial stability mandate.

See original post for references

“An alternative might consist of reviving 19th century practice and reactivating uncollateralised lending, thus encouraging all market participants not to rely on informational shortcuts.”

Hence the rise of peer-to-peer lending? But even that is starting to be smothered by the Too Big To Jail banksters.

care to elaborate on the scond point?

I agree with the first one, btw, although I expect that more than one retail investor gets burned by P2P at some time…

We already know securitization rewards crappy underwriting because the banks make their money up front and have little risk in loan quality because the risk is sold off to “market participants”. Then this also encourages high loan volume, and the resultant decrease in loan quality. But you can be a growth bank because you are not capital constrained, until the world finally melts down under bad debt.

So what we really need is the Loanable Funds model back. Then banks can make any kind of loans they want, but knowledgeable credit mangers manage risk and the banks bears the risk because they keep the loans on their books. The “market participants” can be savers with bank accounts and bank CDs.

“The “market participants” can be savers with bank accounts and bank CDs.”

Physical cash and the mattress or a safety deposit box are not realistic alternatives to banks so, in the absence of a Postal Savings Service or equivalent, the “market participants” would be, in fact, forced investors, not voluntary depositors. So where would the “market discipline” come from?

The big flaw in the US Constitution seems to be the lack of a risk-free fiat storage and transaction service for ALL citizens; in effect leaving the citizens at the tender mercy of bankers.

There was a study that came out end of last year calculating that ZIRP, as of then, was a transfer of half a trillion dollars from savers to banks.

And with ZIRP, it’s savers that lose to inflation too.

by using novel securitization, central banks could quantitatively ease the junk bond markets… that’s certainly a modest proposal.

See The State of Small Business Lending:Credit Access during the Recovery and Hiw Technology May Change the Game by Karen Gordon Mikks and Brayden McCarthy. This is Working Paper 15-004 of the Harvard Business School.

It details the decline in bank lending if loans are less than $1 million. Bank lending still dwarfs online lending but is growing while charging 30% plus.

African American small businesses are out of luck at banks. They often need SBA guarantees and an average loan to an African American business with a 7a guarantee is under $300,000. SBA is working hard to find new distribution paths since the banks opted out.

No public pressure on banks since the lack of CRA enforcement.

But … but … GAAP is so … what? Arcane?

Information? Due diligence?

Actually doing something of value?

Why do anything when you can get something from nothing but smoke and mirror and position in the gravy train line?

IT has made it possible to standardise many things – including credit assessment. It is a long time since company loans were commonly approved by people outside of corporate HQ. Some might argue otherwise, their argument is that they do approve the loans locally. My counter-argument is that they’re approving or rejecting based on an IT-tool designed by corporate HQ and if the borrower falls afoul of the IT-systems then the loan will not be approved -> in effect they can approve as long as corporate HQ already has approved it….

Credit approval process at banks is nowadays very standardised and simple – enter in the financial data into the IT-tool then follow the tool’s recommendation. Go against the recommendation? Only for the ones willing to risk their jobs and who does that in the job-market of today?

The tool can be a help but blindly trusting the tool will lead to disaster, just look at how well the IT-tools used by credit-rating agencies worked out….

Only way forward is to break up the big banks. Anything else will just be an experiment in central planning under a thin disguise of the mythical efficient market. If the decisions are taken based on almost identical IT-tools/models by all the big players, is there really a difference between the oligopoly and the centrally planned?

Thanks for this article, Yves. As one of those “not expert enough to cogently comment,” I nonetheless appreciate becoming educated by its points. All items such at this increase our intelligence and ability to fight the banking monsters.

“… abandoned credit assessment and embraced securitization.”

Parasite Methodology and the Sequestration of Real Property

Blow a bubble which demands investment to remain competitive. Secure the property. Pop the bubble and own the property. Price becomes the means, not the ends.

Cases:

Great Depression: led to megafarms. Banks bankrolled industrialized farming. Supply booms, prices drop, positive feedback ensues. Dustbowl provides crisis shock to collapse the local system. Banks consolidate properties, use bigger machines (more efficient, cheap fossil fuel energy) to eliminate more pesky humans.

Civil War: “…many of their buyers believed that cotton prices would begin to climb again. They had no evidence to suggest a return to rising prices. Supply clearly exceeded demand.” “By the early 1840s, Wall Street and New York had emerged as the definitive victor. Slave owners continued to supply virtually all of the industrial world’s most important commodity, but the post-1837 inability of Southern planters to control their own financing or get the capital that would enable them to diversify led them to sacrifice massive skimmings of their profits to financial intermediaries and creditors. ”

//www.nakedcapitalism.com/2015/04/quick-note-slavery-finance-minsky-panic-1837.html

_ What this article doesn’t mention was that the cotton gin had already delivered a mortal blow to slave economics (hat-tip Heinrich). It wasn’t just about picking the cotton, it was plucking the seeds, and the cotton gin meant a positive feedback, labor-saving price drop. Invasion enforced the property transfer.

Crassus: have a fire brigade which demands pay from competitor landlords to put out the fire. If they don’t, it decreases your competition, and you can get the property at a discount. The Tammany corollary: fight other fightfighters. And if you start the fire, you control the system.

At this point, ZIRP is the spark that allows control of where the fires start / bubbles blow up. Michael Lind provided analysis of the split between local and national elites. //www.salon.com/2013/10/06/tea_party_radicalism_is_misunderstood_meet_the_newest_right/

Austerity programs bumped the context up another notch. Capture the national government, and grabs large swathes of public property. TPP cuts those elites who control at the national level out, and puts the power to control outcomes in the hands of international elites.

I admit this is a nonlinear analysis. It is meant to show the increasing intangibility of controlling the tangible. Crassus dealt with actual buildings, the Civil War and Depression levered technology, but today’s leverage requires nothing more than keyboard clicks and the magic of fiat. Who controls the money wand gets the goods. Collateral is the ends, not the means.

Businesses invest and expand when they see customers coming thru the door. So how about giving billions to customers in Main Street rather than to criminal banksters next time there’s a crisis? Those customers would then walk thru businesses doors.

I realize Harvard economics professors don’t understand that point, but everyone on Main Street understands it.

Excellent post, with a good insight as to the depth of the disease in our financial system. Posts like this are why I keep coming back.

To my knowledge I’ve never posted anything you needed to delete. I used to not be moderated. Now I am.

Seeing a post that I made hours later … no gratification there.

And … I’ve have reduced my posting down to a dribble. Now a dollop. Plop.

Been around since 2007 or so.

Loyalty … I guess it’s not worth a 1 or a 0

I hate to come down on you but your comment is out of line.

We have repeatedly explained that:

1. We have moderation tripwires

2. This site is run by all of 1.3 people. We prioritize writing new material over dealing with the mod queue and comments. Our Policies state that we will get to comments in moderation at least once every 24 hours. You are demanding a level of service well beyond what we have ever said we can or will provide. I work an absolutely punishing schedule, which these days with Greece means routinely staying up until 7 AM or later.

3. We have repeatedly told readers that if they want us to get to the mod queue faster, they need to write checks for this purpose. No one has, which indicates that they agree with our sense of priorities

You mistakenly assume your comment went into moderation because we moderated you. We haven’t. And given that this site is free to your, your complaint about loyalty is misplaced. I make considerable personal sacrifices to keep this site going at its level of quality and regularity of publication, as in having no personal life. For you to attack me personally is abusive and unwarranted.

A big win for American Small Business Job Creation(TM) around here is we have a new self service dog washing store at the strip mall. This has helped offset offshoring, a little bit.

The one I’m not so happy about is my favorite Chinese buffet went out of biz. After siting empty a couple of years, the building was finally leased to someone that made it a Wok & Roll Chinese buffet franchise. Maybe he got a good loan for the franchise fees, I dunno. The all you can eat lunch buffet went from $7 to $10.

But maybe my area is just weird, and small biz is winning the battle against offshoring. Maybe small biz, outside of Silicon Valley venture cap startups in tech and bio-tech, do something besides open restaurants and silly stores. Maybe.

In my neck of the woods (N. CA, but not Silicon V.), most of the small business start ups are restaurants or bars and small stores; typically, many don’t make it. There seems to be a regular round of clubs that open (for live music or dj music) with some fanfare and then close down about 9 months later.

I did hear about some construction companies regrouping recently. There’s still a ton of empty retail space around Sacramento with not much to fill the stores, apparently.

Many, if not most, of the traditionally small enterprises are obsolete due to technology, big box stores, and/or internet retailing.

Roughly 40 years ago, a strip mall (still in existence) opened near my home in suburban Philadelphia. As I remember, the businesses included:

Hobby Shop

Dairy Store

Leather goods/repair/hobby store

Vacuum cleaner store

Small greengrocer

Stationary Store

Ice Cream Store

Hallmark Store

Record Store

Travel Agency

plus some others I don’t remember.

Look at that list — the ONLY one left as an original tenant is the ice cream store (Baskin and Robbins) and the Dairy Store (same brand, but now a major regional chain that is really a full service deli).

Add asking rents – in NORCAL $2/3 sq ft. and there are very few small businesses ouside of restaurants that are possible for today’s entrepreneur.

This. People don’t seem to realize that capital funding models adapt and change according to the vicissitudes of economies and societies over time.

If your business idea — despite lacking available collateral — is so good, then find a VC to buy equity. Others…

There’s a multitude of factors that weigh down entrepreneurs (socioeconomic inequalities, regulatory/tax burdens, etc.), yet I find it hard to believe that someone who can lay out a definitive cash flow can’t find someone to give her a loan. This is America; creditors line up around the block, licking their lips.

In the past, money spent in a local restaurant would circulate through the local economy; but now even local restaurants source pre-prepped ingredients from Sysco.

In the words of Sysco – “heat, assemble, and serve.”

In the words of Sysco founder John Baugh: “frozen foods taste better than anything I could grow in my garden.”

– The training was extensive and took two years at big banks like Chase Manhattan.

I’ll soon have a post hit a little while ago. When it does, please know I welcome disproval of my less optimistic musings.

. . . An alternative might consist of going the opposite way – rather than operating on a standardised collateral debt market that incites participants not to collect information, . . .

Calling all economists, all banksters, go to the toilet right now, stick your head in there and flush.

every country is different

In the US of A, ERISA killed off industry by design it would appear. The Community Reinvestment Act was put in place to try balance out the capital diversion which ERISA(1974) was going to cause.

ERISA rules were put in place to make up for the lost captured revenue that was caused by the looming deregulation of fixed commission on May 1, 1975. The ERISA rules were “sold” to take away from local “corruptible” officials the power to invest pension funds and put it into the responsible hands of Standard & Poors and Moody’s, two fine upstanding organizations bestowed with the power of god by claiming American Industry is bad…and German Industry is good…so magically within 5 years, we had a rust belt…and Germany had its “economic miracle”…since German Unions are good, but American Unions are bad…

The Community Reinvestment Act allows ANYONE WHO CAN FOG UP A MIRROR to walk into an FDIC TAXPAYER FUNDED AND GUARANTEED deposit taking institution and be a part of the conversation…

But, the financial world has been able to twist the intent of the CRA by making sure most people do not understand its power…and to make sure only “certain” organizations are even aware that ANYONE can have a seat at the table..

Red Hat church ladies from ohio, retired librarian, local nobody…

anyone can walk in and say,

“I want to look at your public file and comments, and look at your previous three CRA reports and ratings from regulators”…

they will try to get cute…asking you who you represent, how did you even (dare to) hear about the CRA…you don’t have to represent anyone…but by looking at the public file and comments you will see who is the lapdog for the institution…you will find a bunch of local organizations that you have never heard of, have never seen and are filing wonderful letters claiming how wonderful the bank is with its lending practices…guess what, you can get to fill one of those letters to…and you can insist it be put in the “public file”..and that letter might say,

“I am confused how the regulators are insisting this bank has a wonderful record in lending, when everyone I know of has been refused a loan modification, and there are vacant or boarded up businesses within two miles of a local branch, yet upon review of the banks loan records, I see they are lending in areas outside their deposit taking area…and the map they use to claim their “service area” is not squared or circled, but seems to be twisting and seems to avoid obviously poorer parts of the immediate area…I would like you to properly classify this institution as a “failing institution” as there is very high unemployment in this area and the instability of their lack of aggressive lending in this area is only making matters worse. FDIC taxpayer subsidized insurance is available only to institutions who work for the benefit of the communities where they have taken deposits from. The economic imbalance and instability of this community is an obvious sign that this institution is not doing as required by the Community Reinvestment Act”

Then go out and start talking to businesses in your area…go to flea markets…go to business development centers…and ask them a simple question…if you had a line of credit available to you to grow your business, would you use it and could you create local jobs…???

I don’t buy the idea there are not americans with ideas in their back pocket or rattling inside their heads…

banks know how to argue for risk taking with credit cards and derivatives…the arguments for lending to start ups is basically the same logic…oh…and don’t let the banker get too cute…you do not have to be a finance genius to insist at a seat at the table…you just have to know the game they play…

Hitler was an economic rockstar before becoming a stooge too.

back to the N word

top three locations of white N’s

#3: Seattle

#2: Anywhere you find NASA

#1: Spokane

I love Spokane, one of the best places to eat breakfast in America, and some of the nicest people you will ever meet, but white Ns per capita, it’s #1.

It’s not the word that’s the problem.

Empire Economics

John steals product A from Paul, a catholic, and sells it to Peter, a muslim, and then steals product B from Peter, to sell to Paul. Peter and Paul buy a bridge from John when they realize that they can trade, who also offers money and accountant to keep the books, and charges a bridge toll that increases over time. Over time, Peter and Paul begin to understand the scam, but aspire to be John, so they bring in 4 more people, a republican, a democrat, a socialist and a communist. Betty and Sue, looking from the outside, demand equal rights and inclusion, aspiring to replace Peter and Paul. John hires a kid to write a few lines of code to manage the ponzi automatically, blows up his physical operation, and retires. Over time, all parties become specialists, in their own brand of stupidity, trading away what they need for what they want, a piece of crap SMARTphone that cannot feed, house or clothe them, wondering why their standard of living is crashing.

It’s noise.

I am looking at adding $150k/yr right now, surrounded by closed-system thinkers who are competing to stop me, who will immediately be at my door if I take it.

My wife, who has been calling the banks is amazed, at the ignorance on the other end of the line.

Poverty, regardless of brand, doesn’t make you a better person, regardless of what the pastor says. Spend some time in the event horizon to see what goes on there, and move on. And don’t be surprised when you find out that every floor on the hoarding skyscraper is pretty much the same, with a different dress.

not to mention the State of California on the bluff doing its Wyle E Coyote gyrations, thinking it is somehow going to transform my work into water and soil that isn’t polluted. Now the critters are stupid enough to think that reservoiring grey water is going to help the drought, looking into model homes from the outside, with plastic organic fruit on the table.

Solid review by Karen Mills on the state of bank small business lending at

She documents decline in commercial loans under $1 million on the one hand and continuing domination of small business loans by banks. (Online commercial lenders are growing fast but still relatively very small plus they charge 30% plus and only lend for up to 18 months or so.

African American small businesses tend to borrow smaller amounts ($300M on average on loans guaranteed by the SBA) so the trend in which banks have walked away from smaller commercial loans (under $1 million? $500M?) hurts them more than it hurts profitable larger businesses, usually not African American or Hispanic owned.

The SBA has taken several bold steps to invent use of its guarantee program for smaller loans (more delegation of approval authority, new certified lenders from the non profit small business loan industry) but it has not yet broadened access to commercial credit for African American businesses.

Every community needs economic activity. And entrepreneurship is one way for families to build their personal assets. Without personal assets, families are not stable and children do not have as many choices as they grow up.

There is no public policy push to re-inforce the fact that commercial banks get charters (and FDIC insurance) because of their role of financing the real economy. The Community Reinvestment Act was an effort in that direction but enforcement is now weak (and has been for some time.)

SBA, picking winners and losers for the chamber of commerce, maximizing rent/income, that’ll work.

exactly who are the recipients right now?

Among minorities, Asian businesses have gotten an increasing share of SBA loan guarantees. But relatively large loans to existing white owned businesses owned by men get most of the guarantees.