This month has seen the antipodean central banks both cut rates, with almost no flow through to mortgages to relieve consumer debt and an appreciation in their respective currencies, in perfect opposition to their stated goals.

This is not a new trend – far from it. What’s supposed to happen when the local economy slows is you pull the lever, Kronk, lower interest rates stimulate consumer spending, reducing savings rate as a deluge of money floods the economy, inflation goes up, wages go up, more spending and whoosh, in come the accolades from the captured business media elites.

Now levers are pulled left right and centre and nothing seems to happen, further hindered by a lack of communication from both monetary and fiscal authorities into the truth of the matter at hand – that a lack of confidence in the direction of the economy is what is holding back consumer spending, not lower rates.

Furthermore, communicating and smoothing the confidence game that is the market is now becoming more of a parasite/host relationship, instead of a divorced, clinical approach in the past.

At Forexlive they put it a little less eloquently:

Back in the day a central bank would move rates when they saw fit and certainly didn’t massively advertise the fact. Traders and the population were left to infer expected action from what the economy was doing. If inflation was high then you’d get ready for hikes. If the economy was wobbling, you’d get prepared for cuts. Forward guidance was minimum but everyone knew where they stood on it. It made for some hairy monetary policy decisions but that’s what traders thrived on.

Nowadays no one should be expecting a big downside move on a cut, nor big upside move on a hike, unless it comes out of the blue. Forward guidance brings the move a rate cut would bring forward so when we get the actual rate cut, we’re expecting it. All that’s happened is the move has shifted forward in time.

As far as the currency is concerned, this rate cut has been a waste of time and now they may be forced into intervention to get it lower. We know how that’s worked out for them previously.

Forward guidance can work but it depends on who’s doing it. Look at Draghi back in 2014 when the euro was at 1.40. Remember Trichet and his vigilance/strong vigilance clues? The difference is that the ECB and the euro is huge, and with all due respect, the RBNZ and NZD isn’t. Draghi can utter a word and the market can move a thousand pips. Wheeler can utter the same word and the market can go “meh”.

You can’t stop change but I wish central banks would kick forward guidance out the window. They need to get shot of fan charts, dot plots, guessing games projections and just concentrate on what they should be doing, not on what the market may think or do if they act. If they did that then monetary policy would have a greater, and most probably a more positive, effect on their economies.

But would it really? Pushing on a string is what is really happening as this post-GFC global economy continues to mature, where rate cuts seem to be having the opposite effect.

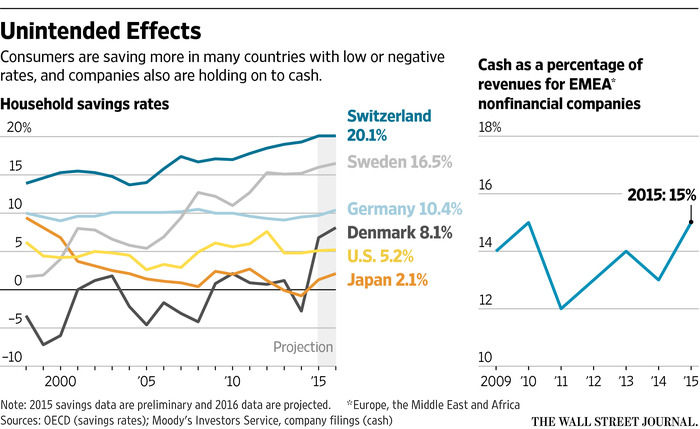

According to a recent Wall Street Journal article based on data from the Organisation for Economic Co-operation and Development, Moody’s and corporate regulatory filings consumers in countries with negative rates are actually saving more now than in 1995.

And a measure of corporate cash coffers compared to revenues for Europe and neighbouring countries has been climbing over the past 5 years. At the end of 2015 the ratio was at a level not seen since 2010, representing almost 1 trillion Euros in corporate bank accounts.

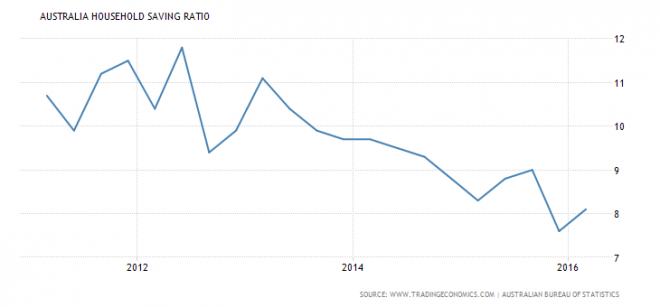

Interestingly, the Australian household savings rate is in decline:

But retail sales growth is tapering:

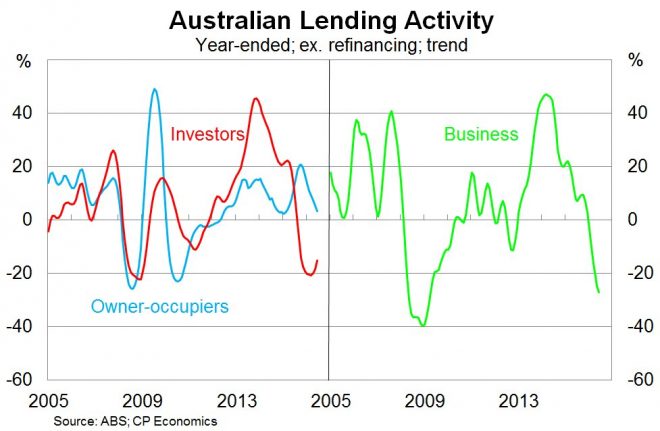

While corporate bank accounts burgeon, with surplus funds only used to buyback shares, not for investment, with more than 25% of assets being cash at hand – the second biggest in the world. So cutting interest rates to stimulate business investment wouldn’t work because why borrow money at record lows when you’re sitting on a mountain of it like Scrooge McDuck?

And indeed the latest figures bear this out, with business lending at record lows:

More:

Workers are faced with the same problem, yet it is compounded by the slow state of the current and projected economic environments. When central banks, government officials and the financial community have low expectations for economic prosperity, the confidence of businesses and consumers is also sure to fall. Confidence in the economy is a necessary condition for spending, and today’s lack of confidence means more saving.

Unfortunately for central bankers hoping to boost spending by offering cheap loans, they may have only boosted the incentive to squirrel away even more money. Counterintuitively, higher rather than lower interest rates may be the key to stimulating these economies. But that has a whole other set of issues to deal with.

First of which, particularly here in Australian and New Zealand is an enormous mountain of debt that needs to be serviced. Raising interest rates may stimulate one third of the economy that owns its house outright and has no debt, but for the rest, only runaway inflation can solve their debt binge problem. And no central bank governor wants that millstone around their neck, as they cling mightily to the 2-3% theoretical zone.

One hopes that a new Captain at the helm of the RBA when Glenn Stevens steps down can be a little more willing to admit defeat in the rates war and get more proactive and honest with both the FX market and the households of Australia.

OK, the CBs don’t know what the hell they’re doing. We get that. But what is the “ultimate outcome” of their foibles: INflation, DEflation, or perhaps the dreaded STAGflation?

oho

” But what is the “ultimate outcome” of their foibles”

the ‘good news’ is that since currencies are all about relative value, I’d bet that Japan and Euro-land blow up before the US does and that the US Dollar will rise before the real endgame.

but of course 2016 is Trump v. Clinton and I can see both of them doing something dumb that stumbles the world into a meltdown.

As for how to prepare for the future: save, save, save in assets appropriate for your age….and stay as healthy as you can as for the bottom 92% your biggest asset is your labor.

JustAnObserver

Ultimate outcome ? All economies will export more, have their currencies fall, have their sov. debt reduce, their inflation in the Goldilocks range, etc…

In short all economies will become above average in our Wobegone future.

Fiver

Doing God’s Work I presume?

zapster

“Expectations” again? Really? How is it that financial writers are terminally unable to breathe the words “low wages”?

Arizona Slim

Because they are well paid. The lower classes don’t matter to them.

jsn

The bizarre idea that purchaser “demand” could be more important than business “confidence” is the basis of Communism, Satan worship and moral turpitude of every kind! If CEOs don’t expect to get ALL the money, what hope is there for the economy? How will they be incentivized?

samhill

The managers must be paid as much as possible otherwise they won’t be incentivized. The workers must be paid as little as possible otherwise they won’t be incentivized.

Some Guy

+1

Had the exact same thought.

Basically the problem is that all the money is in the hands of people who have so much money that they sit around considering their expectations before deciding how to allocate their pile of money, and then they generalize their own position to the economy as a whole. Put it in the hands of people who are desperate to buy a car to relieve their 2 hour transit commute (or a million other examples) and watch the magic happen – but the folks sitting on their piles of money can’t see far enough down the chain of consequences to support a policy of giving money to anyone but themselves.

Low wages is the main thing, the other thing which the authors do capture is the inverse effect of low rates. I remember reading studies of cab drivers in some city – the expectation of the economists doing the study was that cab drivers would spend more time driving when fare conditions were good and less on days when they were bad. But in fact, the cab drivers had a daily quota to meet, so they spent *less* time driving on good days and *more* on bad days.

Similarly, if people have a quota in mind that they need to accumulate to safely retire, then lower interest rates will make them save more to meet quota, and that is exactly what we see happening. It is human nature (sadly, outside the scope of most of the field of economics).

sunny129

Capital has become more important and valued, progressively more than the LABOR all over the world. Financial Economy grew at a cost to productive Economy thanks to CBers.

Globalization made it worse, with capital ‘mobile’ and labor arbitrage Further robotization of the Economy doesn’t help either! How & when this loop end, is any one’s guess!

Lord Koos

“…a lack of confidence in the direction of the economy…”

Nope — it’s a lack of money.

WanderingMind

This is more of a question than a comment.

Raising interest rates may stimulate one third of the economy that owns its house outright and has no debt, but for the rest, only runaway inflation can solve their debt binge problem.

Warren Mosler has pointed out that interest paid on outstanding government debt and other interest paying instruments exceeds the amount paid on indebtedness.

So, if the central bank pushes up rates, doesn’t this result in net additions to the economy? If so, doesn’t that provide a stimulus similar to a fiscal stimulus?

What is the flaw in that analysis?

Steven Greenberg

At this point, pushing up interest rates would cause deflation, not runaway inflation. Usually raising interest rates is meant to cut inflation, but we don’t have CPI inflation now.

So raising the interest rates is very likely to kill the economy. Mosler may be talking about second order effects while ignoring the first order effect. Never a good idea when trying to figure out what will actually happen.

There are many forces acting on the economy from all directions. Unless you actually measure each force and its direction and sum them all up, you don’t know the net force. Saying a force exists or doesn’t exist is not enough to get the force balance.

Jim Thomson

The interest paid on gov’t debt does add to reserves and the accounts of the debt holders. But I suspect most of the debt is held by wealthier individuals and corporations, with a lower propensity to consume, so it is not spent. It is spending that drives the economy.

Actually, the main use of Treasuries is to secure derivatives positions, but the same general point holds.

Jim Thomson

Thank you, Yves. Still learning.

WanderingMind

So, Warren Mosler’s point comes with a caveat.

reslez

> So, if the central bank pushes up rates, doesn’t this result in net additions to the economy? If so, doesn’t that provide a stimulus similar to a fiscal stimulus?

It does. And that is part of the reason why low and negative interest rates are causing so much harm to the economy. Of course actual fiscal stimulus however can be targeted and much more effective than blanket rise in interest rates. A rise in interest rates would affect more than just what the government pays out on its Treasuries, people who take out private loans also end up paying more. The current environment is certainly painful for retirees and pension funds, however. Clearly the policy is not working — Wall Street speculators may not want interest rates to rise but they will have to eventually.

Steven Greenberg

I’d like to throw out the following challenge to conventional economic theory.

Does even a fiscal stimulus of a budget deficit always stimulate the economy?

I have been thinking that with our current system, the federal government finances deficits by selling bonds. So whatever liquidity they push into the system is offset by taking it right back out in the form of bonds sold.

What deficits really do to stimulate the economy is to redistribute a fixed amount of liquidity in the private sector. When this entails taking money from the wealthy who do not recirculate it, and putting it in the hands of working people who do circulate it, then we get stimulus.

When deficits don’t stimulate the economy is when the deficit is the result of tax cuts that leave the liquidity in the hands of the wealthy by taking it from the hands of the workers when we shift the tax burden from the wealthy to the workers.

I’d love to see some research done on this idea and some article published.

Jim Thomson

Steven:

There has been much written about this topic. Yves book, Econned discusses the issue as well as texts by Randall Wray, Modern Money Theory: A Primer on Macroeconomics for Sovereign Monetary Systems.

A place to start is with Bill Mitchells blogs, this one is a good introduction: http://bilbo.economicoutlook.net/blog/?p=8117. It references earlier articles he has written on Deficit Spending.

Actually your statements are more in line with conventional economic thinking, that there is a fixed amount of liquidity which is only redistributed by government deficit spending. The reality is that deficit spending increases the financial assets of the private sector, specifically the accounts of the target of the spending. The subsequent bond sales just convert reserves into securities, with no further change in net assets. So the bond sales do not remove the financial assets from the system.

jsn

In addition to Jim Thompson’s recommendations, the “required readings” at Mosler’s site “Center of the Universe” cover this ground also. Per the reply to Wandering Mind, Mosler has been pointing out that while Central Banks think QE is stimulative, for small bond holders, retirees in particular, ZIRP has been deflationary requiring consumption of principal to offset lost incomes. So while it may well be a tertiary effect from a financial market perspective, it is a primary one from the point of view of affected individuals.

Chauncey Gardiner

It seems to me that given the failure for the vast majority of the neoliberal policies of private sector debt growth, austerity, manipulated markets, wage suppression, privatization of public assets and services, etc. it has become increasingly difficult to ascribe the actions of central bankers and their fellow travelers to good faith.

Given a choice between stupidity or duplicity, one must attach some probability to the latter based on the evidence. Regardless of which applies, however, at what point does a society pull the plug on their failed policies rather than passively continuing to accept the argument that “You simply haven’t done enough. We will make you again double down on our policies”? After all, they’ve had decades to work their magic and all we’ve gotten is repeated financial and real estate asset bubbles and crashes, record economic inequality, and military-geopolitical disarray and tragedy.

Sovereign positive money, coupled with increased domestic fiscal spending on infrastructure and public assets and services make policy sense to me.

OpenThePodBayDoorsHAL

It’s about dogma.

We kill a million and spend 2 trillion with just a harvest of chaos in Iraq…but since the dogma says that’s what we do, we’ll elect someone who will double down.

Similarly the neo-Keynesian dogma at the heart of every single CB says the business cycle and creative destruction must be subverted at all costs.

So even in the face of utter failure they double down. It’s what they do.

So now we have NIRP, which instead of spurring credit and spending growth is increasing the savings rate. At the other end of course income from bonds or bank CDs is also zero so it’s a pincer movement. And velocity is dropping like a rock.

The only transmission channel left unblocked is the stock market, so they take the completely bizarre step of amassing equities. Since when does a central bank own a boatload of equities?

As a FT commenter said “Thank you for your description, I now know what QE is. The problem is I no longer understand what money is”.

Sound of the Suburbs

Central Banks have lost control and I think that is becoming pretty obvious to everyone.

The control they used to exert:

1) Raising interest rates to reduce borrowing

2) Lowering interest rates to increase borrowing

We put our faith in bankers and they saturated the world with their debt products, everyone just wants to pay off debt and not take on new debt, the Central Banks interest rate control mechanism has stopped working.

Bad news for Australians I am afraid, but you may not have noticed what happens after a housing boom.

The bubble pops and it gets pretty bad.

Japan 1989, US 2008, Ireland, Spain ……..

Japan was the first to get into a balance sheet recession when their real estate bubble burst in 1989. The private sector was saturated in debt and no one wanted to take on more debt, they just wanted to repay the existing debt. It’s been going on for 25 years (they were just recovering when the 2008 crisis hit).

They learnt the Central Bank’s interest rate policy and QE does nothing and only fiscal stimulus works.

When Australia’s housing bubble pops you can find out what to do from Japan:

Why has no one noticed the dangers of housing bubbles?

Fiver

And certainly include Canada as an exceedingly likely candidate for an attack on its enormous and vulnerable sovereign housing market – prices in Canada’s two prime destinations for foreign money, Vancouver and Toronto, have left orbit. Some secondary cities as well (Ottawa) – that should it fail, beget a national bankruptcy of a State – as what is being discussed re some European and other nations. These are true bubbles by anyone’s standard and thus misrepresent the real worth of a huge portion of Canada’s homeowners’ total assets.

gordon

In fairness to the retiring Governor of the Australian Reserve Bank, Glenn Stevens, we should note that he is aware of the limitations of central bank action (quote from his farewell speech as Governor):

“As would be clear from my utterances over the past couple of years, I have serious reservations about the extent of reliance on monetary policy around the world. It isn’t that the central banks were wrong to do what they could, it is that what they could do was not enough, and never could be enough, fully to restore demand after a period of recession associated with a very substantial debt build-up”.

If the arm muscles have been thus taxed the arm drops as if paralyzed and can no more be forced to do work in chronic fatigue than we can push on a string. “Pushing on a string” is particularly used to illustrate limitations of monetary policy , particularly that the money multiplier is an

Supply side won!

There is no demand.

OK, the CBs don’t know what the hell they’re doing. We get that. But what is the “ultimate outcome” of their foibles: INflation, DEflation, or perhaps the dreaded STAGflation?

” But what is the “ultimate outcome” of their foibles”

the ‘good news’ is that since currencies are all about relative value, I’d bet that Japan and Euro-land blow up before the US does and that the US Dollar will rise before the real endgame.

but of course 2016 is Trump v. Clinton and I can see both of them doing something dumb that stumbles the world into a meltdown.

As for how to prepare for the future: save, save, save in assets appropriate for your age….and stay as healthy as you can as for the bottom 92% your biggest asset is your labor.

Ultimate outcome ? All economies will export more, have their currencies fall, have their sov. debt reduce, their inflation in the Goldilocks range, etc…

In short all economies will become above average in our Wobegone future.

Doing God’s Work I presume?

“Expectations” again? Really? How is it that financial writers are terminally unable to breathe the words “low wages”?

Because they are well paid. The lower classes don’t matter to them.

The bizarre idea that purchaser “demand” could be more important than business “confidence” is the basis of Communism, Satan worship and moral turpitude of every kind! If CEOs don’t expect to get ALL the money, what hope is there for the economy? How will they be incentivized?

The managers must be paid as much as possible otherwise they won’t be incentivized. The workers must be paid as little as possible otherwise they won’t be incentivized.

+1

Had the exact same thought.

Basically the problem is that all the money is in the hands of people who have so much money that they sit around considering their expectations before deciding how to allocate their pile of money, and then they generalize their own position to the economy as a whole. Put it in the hands of people who are desperate to buy a car to relieve their 2 hour transit commute (or a million other examples) and watch the magic happen – but the folks sitting on their piles of money can’t see far enough down the chain of consequences to support a policy of giving money to anyone but themselves.

Low wages is the main thing, the other thing which the authors do capture is the inverse effect of low rates. I remember reading studies of cab drivers in some city – the expectation of the economists doing the study was that cab drivers would spend more time driving when fare conditions were good and less on days when they were bad. But in fact, the cab drivers had a daily quota to meet, so they spent *less* time driving on good days and *more* on bad days.

Similarly, if people have a quota in mind that they need to accumulate to safely retire, then lower interest rates will make them save more to meet quota, and that is exactly what we see happening. It is human nature (sadly, outside the scope of most of the field of economics).

Capital has become more important and valued, progressively more than the LABOR all over the world. Financial Economy grew at a cost to productive Economy thanks to CBers.

Globalization made it worse, with capital ‘mobile’ and labor arbitrage Further robotization of the Economy doesn’t help either! How & when this loop end, is any one’s guess!

“…a lack of confidence in the direction of the economy…”

Nope — it’s a lack of money.

This is more of a question than a comment.

Warren Mosler has pointed out that interest paid on outstanding government debt and other interest paying instruments exceeds the amount paid on indebtedness.

So, if the central bank pushes up rates, doesn’t this result in net additions to the economy? If so, doesn’t that provide a stimulus similar to a fiscal stimulus?

What is the flaw in that analysis?

At this point, pushing up interest rates would cause deflation, not runaway inflation. Usually raising interest rates is meant to cut inflation, but we don’t have CPI inflation now.

So raising the interest rates is very likely to kill the economy. Mosler may be talking about second order effects while ignoring the first order effect. Never a good idea when trying to figure out what will actually happen.

There are many forces acting on the economy from all directions. Unless you actually measure each force and its direction and sum them all up, you don’t know the net force. Saying a force exists or doesn’t exist is not enough to get the force balance.

The interest paid on gov’t debt does add to reserves and the accounts of the debt holders. But I suspect most of the debt is held by wealthier individuals and corporations, with a lower propensity to consume, so it is not spent. It is spending that drives the economy.

Actually, the main use of Treasuries is to secure derivatives positions, but the same general point holds.

Thank you, Yves. Still learning.

So, Warren Mosler’s point comes with a caveat.

> So, if the central bank pushes up rates, doesn’t this result in net additions to the economy? If so, doesn’t that provide a stimulus similar to a fiscal stimulus?

It does. And that is part of the reason why low and negative interest rates are causing so much harm to the economy. Of course actual fiscal stimulus however can be targeted and much more effective than blanket rise in interest rates. A rise in interest rates would affect more than just what the government pays out on its Treasuries, people who take out private loans also end up paying more. The current environment is certainly painful for retirees and pension funds, however. Clearly the policy is not working — Wall Street speculators may not want interest rates to rise but they will have to eventually.

I’d like to throw out the following challenge to conventional economic theory.

Does even a fiscal stimulus of a budget deficit always stimulate the economy?

I have been thinking that with our current system, the federal government finances deficits by selling bonds. So whatever liquidity they push into the system is offset by taking it right back out in the form of bonds sold.

What deficits really do to stimulate the economy is to redistribute a fixed amount of liquidity in the private sector. When this entails taking money from the wealthy who do not recirculate it, and putting it in the hands of working people who do circulate it, then we get stimulus.

When deficits don’t stimulate the economy is when the deficit is the result of tax cuts that leave the liquidity in the hands of the wealthy by taking it from the hands of the workers when we shift the tax burden from the wealthy to the workers.

I’d love to see some research done on this idea and some article published.

Steven:

There has been much written about this topic. Yves book, Econned discusses the issue as well as texts by Randall Wray, Modern Money Theory: A Primer on Macroeconomics for Sovereign Monetary Systems.

A place to start is with Bill Mitchells blogs, this one is a good introduction: http://bilbo.economicoutlook.net/blog/?p=8117. It references earlier articles he has written on Deficit Spending.

Actually your statements are more in line with conventional economic thinking, that there is a fixed amount of liquidity which is only redistributed by government deficit spending. The reality is that deficit spending increases the financial assets of the private sector, specifically the accounts of the target of the spending. The subsequent bond sales just convert reserves into securities, with no further change in net assets. So the bond sales do not remove the financial assets from the system.

In addition to Jim Thompson’s recommendations, the “required readings” at Mosler’s site “Center of the Universe” cover this ground also. Per the reply to Wandering Mind, Mosler has been pointing out that while Central Banks think QE is stimulative, for small bond holders, retirees in particular, ZIRP has been deflationary requiring consumption of principal to offset lost incomes. So while it may well be a tertiary effect from a financial market perspective, it is a primary one from the point of view of affected individuals.

It seems to me that given the failure for the vast majority of the neoliberal policies of private sector debt growth, austerity, manipulated markets, wage suppression, privatization of public assets and services, etc. it has become increasingly difficult to ascribe the actions of central bankers and their fellow travelers to good faith.

Given a choice between stupidity or duplicity, one must attach some probability to the latter based on the evidence. Regardless of which applies, however, at what point does a society pull the plug on their failed policies rather than passively continuing to accept the argument that “You simply haven’t done enough. We will make you again double down on our policies”? After all, they’ve had decades to work their magic and all we’ve gotten is repeated financial and real estate asset bubbles and crashes, record economic inequality, and military-geopolitical disarray and tragedy.

Sovereign positive money, coupled with increased domestic fiscal spending on infrastructure and public assets and services make policy sense to me.

It’s about dogma.

We kill a million and spend 2 trillion with just a harvest of chaos in Iraq…but since the dogma says that’s what we do, we’ll elect someone who will double down.

Similarly the neo-Keynesian dogma at the heart of every single CB says the business cycle and creative destruction must be subverted at all costs.

So even in the face of utter failure they double down. It’s what they do.

So now we have NIRP, which instead of spurring credit and spending growth is increasing the savings rate. At the other end of course income from bonds or bank CDs is also zero so it’s a pincer movement. And velocity is dropping like a rock.

The only transmission channel left unblocked is the stock market, so they take the completely bizarre step of amassing equities. Since when does a central bank own a boatload of equities?

As a FT commenter said “Thank you for your description, I now know what QE is. The problem is I no longer understand what money is”.

Central Banks have lost control and I think that is becoming pretty obvious to everyone.

The control they used to exert:

1) Raising interest rates to reduce borrowing

2) Lowering interest rates to increase borrowing

We put our faith in bankers and they saturated the world with their debt products, everyone just wants to pay off debt and not take on new debt, the Central Banks interest rate control mechanism has stopped working.

Bad news for Australians I am afraid, but you may not have noticed what happens after a housing boom.

The bubble pops and it gets pretty bad.

Japan 1989, US 2008, Ireland, Spain ……..

Japan was the first to get into a balance sheet recession when their real estate bubble burst in 1989. The private sector was saturated in debt and no one wanted to take on more debt, they just wanted to repay the existing debt. It’s been going on for 25 years (they were just recovering when the 2008 crisis hit).

They learnt the Central Bank’s interest rate policy and QE does nothing and only fiscal stimulus works.

When Australia’s housing bubble pops you can find out what to do from Japan:

https://www.youtube.com/watch?v=8YTyJzmiHGk

Why has no one noticed the dangers of housing bubbles?

And certainly include Canada as an exceedingly likely candidate for an attack on its enormous and vulnerable sovereign housing market – prices in Canada’s two prime destinations for foreign money, Vancouver and Toronto, have left orbit. Some secondary cities as well (Ottawa) – that should it fail, beget a national bankruptcy of a State – as what is being discussed re some European and other nations. These are true bubbles by anyone’s standard and thus misrepresent the real worth of a huge portion of Canada’s homeowners’ total assets.

In fairness to the retiring Governor of the Australian Reserve Bank, Glenn Stevens, we should note that he is aware of the limitations of central bank action (quote from his farewell speech as Governor):

“As would be clear from my utterances over the past couple of years, I have serious reservations about the extent of reliance on monetary policy around the world. It isn’t that the central banks were wrong to do what they could, it is that what they could do was not enough, and never could be enough, fully to restore demand after a period of recession associated with a very substantial debt build-up”.

http://www.rba.gov.au/speeches/2016/sp-gov-2016-08-10.html

The whole speech is worth reading.

If the arm muscles have been thus taxed the arm drops as if paralyzed and can no more be forced to do work in chronic fatigue than we can push on a string. “Pushing on a string” is particularly used to illustrate limitations of monetary policy , particularly that the money multiplier is an