Yves here. Get a cup of coffee. This is a deep dive and does a thorough job of discussing what macroeconomic theory got wrong in the runup to the crisis, what elements deserve to be on the list of “things to be expunged” and the missing issues that deserve to be incorporated.

Marc Lavoie, Professor of Economics, University of Ottawa. Originally published at the Institute for New Economic Thinking website.

While many countries throughout the world have faced severe financial crises over the last decades, and while the Japanese stagnation and the 1997 Asian financial crisis did induce some additional interest for the introduction of banking and finance in macroeconomic theory, it is only with the advent of the US subprime financial crisis that macroeconomic and monetary theories put forward by mainstream economists have started to be questioned.

Still, there are at least two views about the role played by economic theory in generating the Global Financial Crisis, which, depending on one’s opinion, can be ascertained to having started at any of the three following times: when real estate prices in the US started to decline in the summer of 2006, when interbank money markets first froze in Europe during the summer of 2007, or when it was announced that the Lehman Brothers investment bank declared bankruptcy on the 15 th of September 2008. If we take the earlier date, then we can say that the financial crisis and its aftermath have been going on for nearly ten years.

In this essay I discuss how the end of the Great Moderation – this 15-year period of low inflation and low variance in real growth rates in the Western world — has been interpreted by the advocates of mainstream economics and what changes the subprime financial crisis has or may have entailed with respect to macroeconomic theory. I review of a number of key issues in macroeconomic theory, examining what seems to have been changed or been questioned as a consequence of what has happened during and after the financial crisis. The third section is devoted to the concept of hysteresis, which seems to have been resurrected by mainstream economists. The fourth section deals with a number of miscellaneous issues, in particular the shape of the aggregate demand curve and the lack of a relationship between interest rates and public debt or deficit ratios. I conclude with broad brushes about what ought to disappear and what might disappear from macroeconomic theory. Many others, such as Stiglitz (2014) and Mendoza (2013) have done an excellent job in pursuing this kind of exercise. Here I offer my idiosyncratic thoughts, starting with the reaction of economists to the crisis.

Reactions to the Crisis

It is well known that, just before the crisis, mainstream economists were bragging about how good their macroeconomic theories and policies had become. Just as the crisis was in the making, Olivier Blanchard (2008, pp. 2 and 26), the chief economist at the IMF, claimed that ‘the state of macro is good…. Macroeconomics is going through a period of great progress and excitement’. A few years before, Robert Lucas (2003, p. 1), the gravedigger of the Keynesian revolution and the advocate of the micro-foundations delusion, stated that supply-led economics was all that one should care for, with aggregate demand phenomena being well tamed: ‘Macroeconomics in this original sense has succeeded: Its central problem of depression prevention has been solved, for all practical purposes, and has in fact been solved for many decades…. The potential for welfare gains from better long-run, supply-side policies exceeds by far the potential from further improvements in short-run demand management’. Has anything changed since the advent of the crisis?

The first view about economic theory and the Global Financial Crisis is that economic theory has nothing to do with it. This view is most entertained by economists who believe that the government should refrain from intervening in the economy and who believe that unfettered markets remove any imbalances and will keep the economy at full-employment equilibrium. However, even among people who hold more reasonable views, there is a belief that very little in economic theory or in economic policy needs to be changed. This view has been propounded by Olivier Blanchard, when he argued that ‘the crisis was not triggered primarily by macroeconomic policy….. In many ways, the general policy framework should remain the same’ (Blanchard et al., 2010, p. 16). Similarly, the former Chairman of the Federal Reserve, Ben Bernanke (2010) argued that ‘calls for a radical reworking of the field go too far’ (p. 2), insisting that ‘the recent financial crisis was more a failure of economic engineering and economic management’ (p. 3) while shortcomings of ‘economic science, in contrast, were for the most part less central to the crisis’ (p. 4). Indeed several mainstream economists, as recalled by Mendoza (2013), believe that mainstream macroeconomics can be easily repaired from within, or that the required modifications already existed before the crisis but were ignored.

Several mainstream economists still believe that ‘any interesting model must be a dynamic stochastic general equilibrium model. From this perspective, there is no other game in town … If you have an interesting and coherent story to tell, you can tell it in a DSGE model. If you cannot, your story is incoherent’ (V.V. Chari, as quoted by Garcia Duarte, 2012, p. 220). [1] Similarly, not very long ago, Blanchard (2014, p. 31) was affirming that the solution to previous mistakes was that ‘DSGE models should be expanded to better recognize the role of the financial system.’ It is hard to see how conceiving of the financial system as frictions to the real economy can help in understanding macroeconomics. Simon Wren-Lewis (2016, p. 33) is adamant that the methodology proposed by what he calls the New Classical Counter Revolution, enclosed into DSGE and New Keynesian models, is a worthy one, and that as a consequence ‘the microfoundations methodology is entrenched … so it is unlikely that its practitioners will down tools and start afresh’. Wren-Lewis further claims says that ‘the methodology is progressive’, and like Blanchard he believes that ‘researchers are devoting a good deal of time to examining real/financial interactions’ (2016, p. 30), so that all is well as long as Keynesian results are not excluded by assumption and can be recovered from the simulations.

The second view about economic theory and the Global Financial Crisis is that economic theory was indeed a cause of the crisis. This view is very much entertained by left-wing heterodox economists in general, for instance Heinz Kurz (2010), but it can also be found among neo-Austrian economists and among orthodox economists, or at least among those that I like to characterize as dissident orthodox economists. Neo-Austrian economists, in particular those working at the Bank for International Settlements, were quite critical of the New Consensus among mainstream economists even before the advent of the subprime financial crisis. For instance Borio and White (2004) argued early on that the move towards more liberalized financial markets and the increased reliance on market evaluations have increased the inherent pro-cyclical tendencies of asset prices and of the banking system, making it more vulnerable to boom and bust cycles, thus contradicting the apparent success of inflation targeting policies and creating large imbalances and credit swings. After the crisis, White (2009, pp. 1-2) claimed that ‘the prevailing paradigm of macroeconomics allows no room for crises of the sort we are experiencing’, adding that ‘the recent crisis has demonstrated the inadequacy of models based on the assumption of rational expectations’, and concluding that ‘the crisis provides evidence that the simplifying assumptions on which much of modern macroeconomics is based were not useful in explaining real-world developments’.

The strongest indictment of orthodox theory from the orthodox side was perhaps made by Willem Buiter, a former member of the Monetary Policy Committee of the Bank of England, and admittedly an early critic of the hypothesis of rational expectations. In a now famous blog, Buiter (2009) wrote that ‘the typical graduate macroeconomics and monetary economics training received at Anglo-American universities during the past 30 years or so may have set back by decades serious investigations of aggregate economic behaviour and economic policy-relevant understanding’. Buiter (2009) referred to models based on New Classical and New Keynesian economics, and thus to DSGE-type models, as the kind of modelling that offers no clues as to ‘how the economy works – let alone how the economy works during times of stress and financial instability’. Robert Solow, who is sometimes considered as the father of DSGE models because of his famous 1956 neoclassical growth model, has also repudiated DSGE models, saying that its foundations were ‘dumb and dumber macroeconomics’ (Solow 2003), and that adding realistic frictions did not make these models any more plausible (Solow 2008, p. 244). [2] Not unexpectedly, Joseph Stiglitz (2014, p. 24) has also been an advocate of the second view, arguing that macroeconomics has done poorly over the years, as ‘the models/theories that guided policy were not just innocent bystanders in the crisis that unfolded beginning in 2008. They were critical in the creation of the crisis and in the inadequate responses to it’.

Critics of DSGE models do not only include heterodox economists and past recipients of the Nobel prize. Hope and Soskice (2016, p. 218) write that ‘despite its several associated Nobel prizewinners, and the fact that it is still staple teaching in many graduate schools, RBC [real-business cycle theory] —with its roots in Chicago and the Midwest—is regarded by many macroeconomists (including many of those in universities on the “two coasts” such as Harvard, Princeton, MIT, NYU, Berkeley, and Stanford) as esthetically beautiful but mad’ (emphasis added). Are New Keynesian DSGE models any better? Hope and Soskice give them high marks for taking on board what they think are sensible assumptions, that is, the assumption that ‘companies everywhere operate under conditions of imperfect competition’ and that they set prices at discrete intervals of time (the Calvo pricing hypothesis). But Hope and Soskice object to the rest of the New Keynesian assumptions, borrowed from the New Classical economists. As a consequence, ‘the result has increasingly been macro models of great complexity that bear little relation to reality’, Hope and Soskice (2016, p. 218-9) add that ‘the dysfunctional driver of evolutionary progress in New Keynesian economics has been the internal theoretical standards of the academic profession, rather than a concern to understand how the macroeconomy works’. They suggest as an alternative what they call realistic modern macroeconomics, which relies on what they consider to be the improvements provided by New Keynesian economics, stepping away however ‘from the (unrealistic) assumption that all actors are fully forward-looking and rational’ (p. 219). In effect, they reject rational expectations.[3]

The central line of defense of orthodox economists is that the criticisms of orthodox macroeconomic theory are misdirected because, as put forth by Thomas Sargent, its models ‘were designed to describe aggregate economic fluctuations during normal times … not during financial crises and market breakdowns’ (Rolnick, 2010). It is claimed that the main tool of central bankers, the DSGE model, was doing very well as long as the American or European economies were moving along the lines of the Great Moderation. There seems to be a consensus about the limited range of application of DSGE models. Charles Goodhart (2009, p. 352) writes that these models ‘were, by construction, fair weather models only’. Similarly, for Bernanke (2010, p. 17), ‘the standard models were designed for these non-crisis periods’. Blanchard (2014, p. 28) has blamed this on the kind of techniques that were used by mainstream economists, claiming that these ‘were best suited to a worldwide view in which economic fluctuations occurred but were regular, and essentially self-correcting’. Blanchard (2014, p. 29), has also claimed that everyone knew that these models were useless when the conditions of the Great Moderation did not hold: ‘we all knew that there were “dark corners” – situations in which the economy could badly malfunction. But we thought we were far away from those corners, and could for the most part ignore them’.[4] Blanchard (2014) still believed then that with improved models the economy will stay away from what he calls ‘the dark corners’, where mainstream models can provide no light. But this sounds like wishful thinking. There is a need for theories or models that take these dark corners as genuine components or likely possibilities.

Still it seems that some economists are saying tout et son contraire. Take for instance the case of David Colander, who is usually deemed to be a mainstream economist by heterodox authors while being perceived as a key voice of the heterodoxy by the mainstream. Colander has been a long-time advocate of what he called the post-Walrasian approach, also presented as the complexity approach to macroeconomics. In 2006 he published a book the subtitle of which was Beyond the DSGE Model. Nevertheless, in a paper presumably written before the Lehman Brothers default, he was telling us that the DGSE model ‘is well founded, scientific, and potentially more progressive’, highlighting the ‘intellectual coherence and mathematical elegance of DSGE models’, and concluding that ‘thanks to DSGE we know more than we used to about the economy’, all this despite having noted a page before that the DSGE standard ‘involves idealizing to a world we can fully understand in the hope that understanding this simplified world will help us better understand our own’ (Colander & Rothschild, 2009, p. 126−127). A year later, Colander (2010, p. 420) offered a rather different assessment of DSGE models, saying that the primary, and ‘highly problematic’, reason for its success was ‘that it was appropriately micro-founded’. The new Colander (2010, p. 424) added that before the financial crisis economists ‘were well aware of the model’s serious limitations in describing the real-world macro economy’ — a claim similar to that made by Blanchard, Bernanke and Sargent, as recalled earlier.

There has also been a reversal regarding the worthiness of some concepts. For instance, there is now a great deal of renewed interest for the notion of hysteresis, a concept that mainstream economists such as Blanchard and Summers introduced in discussions about unemployment in the early 1980s but that had nearly completely vanished with the apparent success of the Great Moderation, only to reappear with the prolonged aftermath of the 2008 financial crisis. Some could even say that Blanchard has recanted from his previous stand on the state of macroeconomics. In a recent interview in the IMF Survey Magazine, he made the following statement, that seems to open the door to alternative views and in particular to views endorsed by long-time advocates of post-Keynesian economics:

As a result of the crisis, a hundred intellectual flowers are blooming. Some are very old flowers: Hyman Minsky’s financial instability hypothesis. Kaldorian models of growth and inequality. Some propositions that would have been considered anathema in the past are being proposed by “serious” economists: For example, monetary financing of the fiscal deficit. Some fundamental assumptions are being challenged, for example the clean separation between cycles and trends: Hysteresis is making a comeback. This is all for the best.

In this interview Blanchard points out that the Global Financial Crisis has made a lot of people realize that what had become the established or fashionable theoretic approach in economics was not necessarily the best, and that it was time to go back to some of the ideas and models that had been set aside or abandoned in the past. Buiter (2009), in the article referred to earlier, had mentioned as possible alternatives the works of behavioral economists, as well as that of Hyman Minsky, Stiglitz and Tobin. Alan Blinder (2014, pp. 6-8), a former central banker, wrote that two of the lessons to be learned from the financial crisis were that ‘Minsky was basically right’ and ‘self-regulation is oxymoronic’. As to Paul Krugman, it is well known that he has repeatedly affirmed that the old IS/LM Keynesian model provided more insights than any of the fashionable macro models based on neoclassical micro-foundations and the rational expectations hypothesis to understand what has happened to major macro aggregates over the last seven years, although a return to the IS/LM model is probably not the direction that most heterodox economists would like to pursue.

The Reappearance of The Concept of Hysteresis

Mainstream Views

As noted by Blanchard in the previous indented quote, there is a return of the concept of hysteresis and the possible rejection of models based on the assumption of stationarity around a trend. As Blanchard (2014, p. 28) points out elsewhere, mainstream macroeconomists saw ‘the economy as roughly linear, constantly subject to different shocks, constantly fluctuating, but naturally returning to its steady state over time’, either through market self-correcting mechanisms or through the actions of an all-powerful central bank. In neoclassical CGE models, full employment is assumed, and the effects on output can only be achieved by efficiency or productivity gains that arise from specialization or the removal of what the modellers consider to be microeconomic distortions. In DSGE models, it is assumed that the economy will necessarily come back to its potential output, which is essentially determined by the supply of labour, set by demographics and the height of the real wage. If any change in the rate of employment occurs, it can only arise as a consequence of a short-term deviation that will be wiped out over the long run. In those models, just as in the neoclassical computable general equilibrium (CGE) models, output and employment can only be improved by the removal of rigidities and distortions, where relative prices play once again the essential role. Whether discussing neoclassical CGE or DSGE models, increases in employment will be driven through the labour supply function, with higher real wages inducing more consumers to drop their leisure time and increase the time they wish to devote to work.

In the DSGE model, the economy always goes back to its NAIRU (non-accelerating inflation rate of unemployment) or NAICU (non-accelerating inflation capacity utilization), which is entirely determined by supply-side factors. Whether we are talking of neoclassical CGE static models or of the dynamic stochastic equilibrium models does not matter: these mainstream models in general do not take into account that the new equilibrium resulting from some change or shock will be influenced by what occurs during the transition from one equilibrium to the next. In other words, these models assume away path-dependence and hysteresis. They assume away the possibility that demand-led factors will have an impact on the long-run equilibrium, for instance the long-run value of potential output or the long-run value of the natural rate of unemployment. They assume away the possibility that demand-led factors can change the slope of the trend growth rate of potential output over the long run.

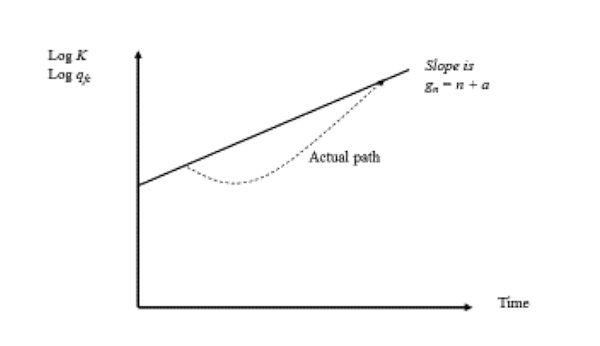

Laurence Ball (2014, p. 149) summarizes this feature of mainstream models in the following way: ‘A fall in aggregate demand causes a recession in which output drops below potential output – the normal level of production given the economy’s resources and technology. This effect is temporary, however. A recession is followed by a recovery period in which output returns to potential, and potential itself is not affected significantly by the recession’. This is illustrated with Figure 1. As recognized by Paul Krugman (2009), at least until the beginnings of the Global Financial Crisis, ‘self-described New Keynesian economists weren’t immune to the charms of rational individuals and perfect markets. They tried to keep their deviations from neoclassical orthodoxy as limited as possible’. The standard DSGE model, designed by New Keynesian economists, has illustrated ‘how Panglossian even New Keynesian economics had become’.

Figure 1: The Mainstream View (New Consensus, DSGE)

More recently, the Global Financial Crisis has clearly illustrated that quantity effects generated by demand-led factors have had a much greater role to play than price effects coming out from supply-side factors. This has been pointed out even by some authors, such as Lawrence Summers (2014), who in the past had succumbed to the sirens of supply-led models. Summers, as reported by Laurence Ball (2014, p. 149), went so far as to argue in a conference on full employment that ‘this financial crisis has confirmed the doctrine of hysteresis more strongly than anyone might have supposed’. [6] Ball (2014) has studied the impact on potential output of the Global Financial Crisis for a sample of 23 countries. His conclusion is that ‘most countries have experienced strong hysteresis effects: shortfalls of actual output from pre-recession trends have reduced potential output almost one-for one’ (Ball 2014, p. 149). This, he says, has occurred through a reduction in capital accumulation, a lower labour force participation rate, and a slowdown in the growth rate of productivity. I will briefly come back on this third cause in the text below.

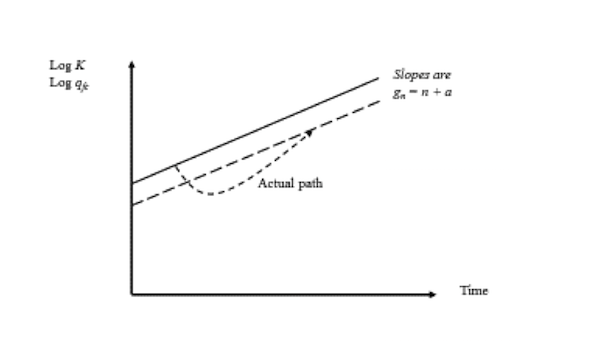

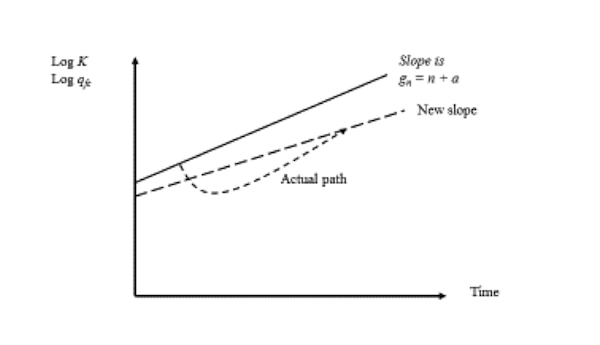

But these hysteresis effects have not only arisen as a consequence of the recent Global Financial Crisis. They have arisen in a majority of previous recessions. Blanchard, Ceretti and Summers (2015), in a study of over 120 recessions, assess that more than two-thirds of them have led to a permanent gap between the previously estimated potential output and the after-recession estimate. In one third of the recessions, this gap was actually increasing through time, meaning that the growth rate of potential output had actually declined – a result which is consistent with the earlier work of León-Ledesma and Thirlwall (2002) as we shall see below. Summers (2015, p. 8) has summarized this by saying that ‘reversion back to trend is actually less common than evidence that the recession not only reduced the level of GDP, but reduces the trend rate of growth of GDP, what Larry Ball has referred to as super hysteresis’. Hysteresis, as it used to be mostly understood by some eclectic New Keynesian authors, and super hysteresis, as it was mostly advocated by post-Keynesian authors, are illustrated with Figures 2 and 3 respectively. In Figure 2 the economy returns to its previous long-run growth rate, but the level of output does not go back to what it would have been without the recession. In Figure 3, the economy never goes back to its previous long-run growth rate – the case of super hysteresis.

Figure 2: Hysteresis

Figure 3: Super Hysteresis

In other words, as long as we accept that recessions are mostly caused by elements related to the demand side, and not to unexpected drops in productivity as argued by advocates of the real-business cycle theory, aggregate demand does have a feedback effect on the long-run supply side. As Stiglitz (2014, p. 16) forcefully argues, ‘the problem is lack of aggregate demand’. Thus, to provide a compelling analysis of what is going on, we need models that are demand-led, possibly with the incorporation of some supply-side elements that will allow us to assess the possible effects on potential output.

Post-Keynesian Views

There has always been a tradition in economics that kept rejecting the supply-led approach. It is well-known that the Keynesian tradition has put the emphasis on demand-led factors. This does not mean that supply factors are totally ignored. What it means instead, as implied by the following two statements from well-known Cambridge authors, is that the natural rate of growth is heavily influenced by the growth rate of demand.

But at the same time technical progress is being speeded up to keep up with accumulation. The rate of technical progress is not a natural phenomenon that falls like the gentle rain from heaven. When there is an economic motive for raising output per man the entrepreneurs seek out inventions and improvements. Even more important than speeding up discoveries is the speeding up of the rate at which innovations are diffused. When entrepreneurs find themselves in a situation where potential markets are expanding but labour hard to find, they have every motive to increase productivity.

The stronger the urge to expand … the greater are the stresses and strains to which the economy becomes exposed; and the greater are the incentives to overcome physical limitations on production by the introduction of new techniques. Technical progress is therefore likely to be greatest in those societies where the desired rate of expansion of productive capacity … tends to exceed most the expansion of the labour force (which, as we have seen, is itself stimulated, though only up to certain limits, by the growth in production). (Kaldor, 1960, p. 237)

For instance, before the subprime financial crisis, in an interesting empirical study Leon-Ledesma and Thirlwall (2002) have shown that the natural rate of growth, which is at the heart of supply-side analyses, is in fact endogenous to the growth rate of actual output, providing evidence that the natural rate of growth rises in booms and falls in recession. As they say, ‘growth creates its own resources in the form of increased labour force availability and higher productivity of the labour force’ (2002, p. 452). Their results, at which they arrive by finding the GDP growth rate that leaves constant the rate of unemployment, have been confirmed by a number of other empirical studies, using the same methodology, for other regions of the world. These studies have yielded similar results for North America, Latin America and Asia.

As an aside, it should be mentioned that most mainstream economists and policy makers interpret hysteresis as being something that only occurs on the downward side. A financial crisis or some other catastrophic shock is presumed to have bad hysteretic or super-hysteretic effects on the economy, essentially through the labour market, as unemployed workers are said to be losing their working skills. [7] But it is not contemplated that the phenomenon of hysteresis may also apply on the upward side, say because rising government expenditures or a credit boom generate an increase in the so-called natural rate of growth. This is to be contrasted to the post-Keynesian view, as presented in the above paragraphs, and as reflected in the numerous empirical works on the Kaldor-Verdoorn effect, whereby fast growth rates in manufacturing or more generally in GDP lead to an acceleration in the growth rate of labour productivity. For post-Keynesians, slower and faster growth in aggregate demand will induce effects on the possible growth rates of supply. In the mainstream view, these effects only occur on the downward side, if at all, since it is sometimes argued that it is a fall in the growth rate of potential output that has generated the observed fall in the growth rate of aggregate demand.

Fallouts

An interesting feature of the work of Blanchard et al. (2015, p. 14) is that they recover the same hysteresis and super-hysteresis effects when recessions are intended and induced by restrictive anti-inflation monetary policy – a clear case of recessions caused by reductions in aggregate demand. In other words, while an observer trained in New Classical economics could possibly argue that both the initial recession and the fall in future potential output had the same cause – a slowdown in productivity growth – the fact that recessions induced by restrictive monetary policy also lead to reductions in middle-run or long-run potential output shows that demand shocks also have a long-run negative impact. This has all kinds of interesting policy consequences.

First, obviously, if potential output depends on demand, then it must be that the NAIRU and the SIRCU (the steady-inflation rate of capacity utilization) are also influenced by demand factors. Before the crisis, several authors had provided empirical evidence that the NAIRU hypothesis had been falsified many times over and that it should be abandoned (Storm and Naastepad 2007; Vergeer and Kleinknecht 2010-2011; Mitchell and Muysken 2008). There were also some signs that institutions like the OECD – the champion of labour flexibility – was (sometimes) backtracking on its claims and on its systematic calls for labour market reforms. The crisis has provided more credence to these studies that reject the NAIRU. Before the crisis, it was believed that unemployment rates in the US were lower than elsewhere because their labour market was more flexible. When unemployment rates in the US started to exceed those of most European countries it became evident that unemployment rates were high because aggregate demand at the time was low. There is no such thing as a NAIRU, as became obvious even before the crisis. Indeed, this is the conclusion of Tom Stanley (2004, p. 65), who through two meta-regression studies concludes that the NAIRU hypothesis has been empirically and definitely refuted. Still, within the context of European policies, calls for labour reform – a euphemism for lower real wages and less job security – continue unabated.

A second consequence of the results obtained by Blanchard et al. (2015) is that recessions imposed on purpose by the monetary authorities in their attempt to reduce inflation rates or in pre-emptive strikes against inflation are likely to have long-run negative effects on economic activity. It was always claimed by central bankers that restrictive monetary policies were good for the economy because by producing short-term recessions they would generate lower inflation rates and more efficiency, thus achieving higher output per capita in the long run. Short-run pain was needed to achieve long-term bliss. The only question was whether the central bank could devise means, such as inflation targeting, by which the inflicted short-term pain could be reduced (how the sacrifice ratio could be somewhat reduced). It was always denied that short-term recessions engineered by central banks could generate lower long-run potential outputs. Central bankers now start to recognize that imposing low inflation may inflict long-run and permanent costs; in other words, they admit the possibility of hysteresis.

Furthermore, central bankers have been unable, after more than thirty years of intensive search, to provide any compelling evidence that low inflation is conducive to high productivity growth, in contrast to what was earlier asserted when anti-inflation policies were put in place as a follow-up to and replacement of monetarist policies. The assertion was based on the special case of the 1970s when high inflation rates were associated with a slowdown in productivity growth, but the negative relationship was never recovered afterwards. And of course, the subprime financial crisis has provided the clearest of demonstrations that low inflation rates could not guarantee financial stability, as it was once hoped.

An interesting fallout from this rediscovery of hysteresis effects is the controversy that arose following the estimated effects of the economic program of the 2016 Democrat presidential candidate Bernie Sanders, as they were computed by Gerald Friedman (2016a) – an economist from the University of Massachusetts in Amherst. Friedman found that Sanders’ program based on an expansionary fiscal policy could generate a real growth rate as high as 5 per cent, based on what he thought were standard assumptions of macro models. Following the critique of Romer and Romer (2016), he discovered to his dismay that the hysteresis and Kaldor-Verdoorn effects that he had assumed in his estimates were not part of standard modeling – that is, the kind of models that is used by the Council of Economic Advisers. His response to the critique illustrates well the importance of incorporating demand-led path dependence.

If the Romers were right that the economy is at full employment at capacity utilization, and capacity utilization grows independently of the level of output, then there cannot be a lasting stimulus effect at a fully employed economy. In the Romer case, a stimulus can raise output only temporarily because output depends on capacity and the economy is always at or moving towards capacity. But, if the economy can be stuck at an unemployment equilibrium, if it does not move to a full employment equilibrium, or if a higher employment and output level can trigger a higher growth rate, then a Keynesian-style government stimulus can have lasting effects…. We might call this, the Keynesian-Kaldor case with equilibrium unemployment and growth dependent on the level of the output gap. In the Keynesian-Kaldor case, a one year stimulus can lead to permanently higher output both by reducing unemployment and by raising the growth rate of capacity.

The Shape of The Aggregate Demand Curve and the Natural Rate of Interest

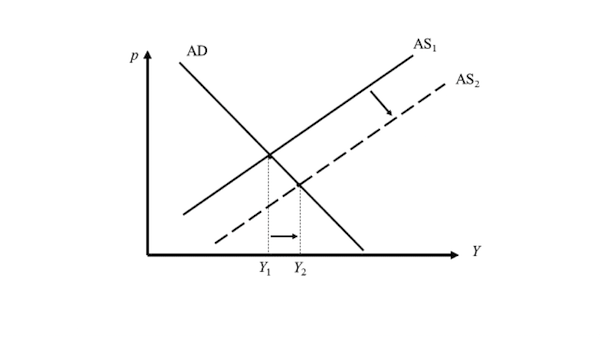

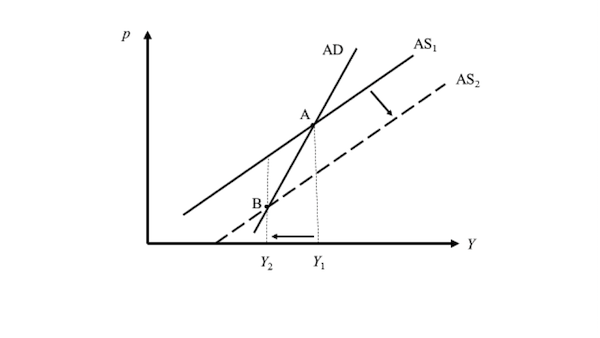

Several other beliefs, that one would have thought were well entrenched in mainstream macroeconomics, have been questioned as a consequence of the financial crisis and its aftermath. One of them is the belief that the aggregate demand curve has the standard negative slope. The desperate efforts of central bankers to stop prices from falling has clearly shown that central bankers for all practical purposes do not hold to the standard view that more flexibility in wages and prices is conducive to a better performance. The textbook view is illustrated with the help of Figure 4, where Pigou’s effects generate the downward slope of the aggregate demand curve. In as self-adjusting system, with no rigidities, a recession should induce a fall in wages and prices. A reduction in the wage rate leads to a rightward shift of the aggregate supply curve (from AS 1 to AS2), and thus, with the standard negatively-sloped aggregate demand curve, this ought to lead to an increase in real output, here from Y1 to Y2. Why then would central banks pursue all kinds of non-conventional measures to stop wages and prices from falling when a recession occurs?

Figure 4: The Effect of Falling Wages in the Mainstream View

Figure 5: The Effect of Falling Wages in the Fisher-Tobin-Minsky View

Obviously, as shown in Figure 5, if the aggregate demand curve is upward sloping instead of being downward sloping, then the actions of central bankers – putting aside the fact that several central banks are committed to inflation targeting and hence aim at low inflation rates – are much easier to understand. In this case, a fall in wages and prices also shifts the aggregate supply to the right, but this time the lower wages and prices induce a decrease in the level of real output, which falls from Y1 to Y2 in Figure 5, as the equilibrium point moves from A to B. This is what is called here the Fisher-Tobin-Minsky effect, in honour of these three economists who have emphasized the possibility of debt deflation – as did Kalecki when responding to the wealth effects proposed by Pigou as a response to Keynes’s unemployment equilibrium. The downward flexibility in wages and prices does not engineer a recovery of output. Instead, it engineers mounting problems for those households and firms who have large liabilities, it leads to debt defaults and bankruptcies, as well as the destruction of output capacity.

Modern macroeconomic theory, based on the New Consensus, relies on a presentation that highlights the rate of price inflation rather than the price level. In the not-so-distant past, the limits to monetary policy were being attributed to rigidities in real wages. If the rate of inflation got close to or reached zero, it was argued that there was no room for real wages to decline in a downturn, because nominal wages were downwardly rigid and were unlikely to fall. Inflation was needed to ‘grease’ the wheels of the labour market. With inflation at or close to zero, nominal wages and hence real wages would not fall when faced with a decline in nominal aggregate demand, and as a consequence firms would be forced to lay off workers, unemployment would rise, and real GDP would fall. The economy would need wage deflation to achieve potential output.

The downward rigidity in nominal wages close to zero price inflation has now been replaced by the downward rigidity of nominal interest rates in the pantheon of neoclassical explanations of unemployment and economic stagnation. This is the highly heralded zero-lower bound on nominal interest rates, or what Krugman has called, erroneously, the liquidity trap. The aggregate demand curve with the inflation rate on the vertical axis, or what some prefer to call the ‘inflation-output’ relationship, instead of being downward sloping could become upward sloping and hence generate perverse results. With nominal interest rates at their zero-lower bound and once more with inflation rates at or near zero, real interest rates cannot be made to be negative enough to achieve the real rate of interest that would be needed to bring back the economy to potential output or full employment. The nominal interest rate would need to be negative for the equilibrium real interest rate to be achieved. This New Consensus story put forward by New Keynesians and Krugman in particular is no different from the one told nearly 70 years ago by Don Patinkin (1948) in the American Economic Review: the investment and the full-employment saving functions were said to equate each other at a negative interest rate. As the French say, ‘plus ça change, plus c’est pareil’!

Normally, all else equal, the central bank would like to reduce the real rate of interest whenever the inflation rate and autonomous demand relative to potential output get lower. This generates the standard negative slope of the inflation-output curve. However, at some deflation rate, it is no longer possible to reduce real interest rates due to the fact that nominal interest rates cannot fall below zero (or so we all thought!). At that point, the inflation-output curve becomes positively sloped (as does the AD curve in Figure 5), as larger deflation rates (in absolute terms) lead to higher (rather than lower) real interest rates and hence to a decrease in the interest-elastic portion of spending.

This explains why New Keynesian economists advocate policies, such as quantitative easing, that could stop inflation expectations from falling below the inflation target, so as to avoid making things worse. And since these policies have proven to be largely ineffective, it explains why New Keynesians are once more considering the relevance of expansionary fiscal policies that would induce an increase in real demand. But why is the economy away from potential output in the first place? As recalled by Eckhard Hein (2016), the more eclectic mainstream authors invoke the long-term effects of the financial crisis on aggregate demand; the more mainstream ones blame long-term supply-side effects that have reduced potential output or the growth rate of potential output. Arguments invoking excess saving and deleveraging have also been put forward. Whatever is the case, there is now a near consensus among mainstream authors that the real natural rate of interest is lower than what it used to be, which makes it harder to achieve it and hence makes it harder to achieve potential output when the rate of inflation is around zero or negative. In the case where aggregate demand is below potential output, it is argued that the temporary neutral interest rate that is necessary to bring back the economy towards potential output is then below the long-term natural rate and hence is even harder to achieve through conventional monetary policies.

All this is rather confusing. Before the crisis, the long-term rate of interest on corporate bonds or on government bonds was deemed to be a good proxy of the (nominal) natural rate of interest. It was said that a central bank should align its administratively-determined short-term interest rate to this long-term rate. During the crisis, the long-term interest rate, for instance the Baa corporate rate, shot up as a consequence of uncertainty and risk premia; but at the same time a number of economists were arguing that the natural rate of interest had become negative. There was a contradiction. From a pedagogical point of view, it is clear that we can no longer speak of the rate of interest. Also, what is the meaning of the natural rate of interest in a world where the NAIRU and potential output are being determined by aggregate demand?

In the past, mainstream economists kept claiming the public deficits and public debts led to overly high interest rates, despite the fact that past econometric evidence relating public deficits or public debt to high interest rates had always been very weak. During the crisis, several countries have encountered large deficits and large public debt to GDP ratios while both their short-term and long-term interest rates have remained low and in fact have gone down, as was the case in Japan, the USA and the UK. The existence of a general positive relationship between public deficit or public debt to GDP ratios and nominal or real interest rates (found in the IS-LM model or in the New Consensus model) must thus be relegated to the dustbin.

Still, some countries (of the Eurozone) have suffered from high interest rates during the crisis while faced with rising debt and large current account deficits. These high interest rates arose mainly from the financial market fears of sovereign default. There is now a growing recognition that countries that have their own currency and their own central bank and that borrow in their own currency run no risk of insolvency and default. This has now been recognized by mainstream authors such as Krugman and Paul De Grauwe, who, prior to the crisis failed to understand the peculiar and faulty setup of the common currency Eurozone, whereas heterodox authors such as Godley, Kregel, Palley and Parguez predicted in the 1990s that the Eurozone countries would be at the mercy of the whims of financial markets. Indeed, ever since the ECB announced that it would do anything in its power to control interest rates, these interest rates have gone back down (except in Greece), and reached even lower levels.

The Eurozone crisis has also led to a reconsideration of a major tenet of mainstream economic policy, that is, the belief that as soon as some negative shock has induced the appearance of a fiscal deficit, the government should quickly engage into a consolidation program designed to remove the deficit and possibly to reduce the public debt to GDP ratio. Some researchers at the IMF now argue that while public debt imposes a dead-weight loss on the economy, when there is little risk of a speculative attack against sovereign bonds the costs of quickly proceeding to consolidation are likely to exceed their expected benefits, so that it is best to let future economic growth lead to a gradual reduction in the public debt to GDP ratio (Ostry et al. 2015). This change in attitude parallels the recognition by IMF officials that the public expenditure multiplier is much higher than previously thought, at least when measured in times of a slowdown (Blanchard and Leigh 2013). This means that fiscal austerity policies, in particular reductions in government expenditure, have a much greater negative impact on the economy than what was previously assessed. There has been a complete reappraisal of the values of these income multipliers, with the new measures being in line with those that used to be estimated by Keynesian models prior to the New Classical counter-revolution. This reinforces the irrelevance of the crowding-out effects mentioned earlier.

Conclusion

In this article, I have tried to stress that there is considerable dissatisfaction with the current state of mainstream macroeconomics and with the quasi-dictatorial directive that the only game to be played in town is the adoption of the DSGE model. This dissatisfaction arises from economists of all persuasions – heterodox, neo-Austrian and even a number of orthodox authors. The puzzle is why is it that DSGE models, which are based on calibration while their assumptions are contrary to factual evidence, are still being considered as the nec plus ultra of macroeconomics? The crisis has made a number of economists realize that one cannot adopt a model just because it provides formalized foundations that are consistent with neoclassical microeconomic theory and corresponds to the standards advocated by a small group of trend-setting academics, while this model describes an imaginary world. Such a reconsideration means that a number of components of the standard baggage of mainstream economists have to be questioned.

Without going into any detail, it seems clear to me, as Paul Krugman has argued several times, that New Classical economics or what has also come to be known as freshwater economics, just has not survived to the test of time. It must go away. The same applies to what many modern macroeconomists used to consider as compulsory components of any formal theory: the rational expectation hypothesis, the strong or semi-strong version of the efficient market hypothesis, the unbiased efficiency hypothesis in international finance, the assumption of perfect asset substitutability, the NAIRU, as a unique (or even time-varying) attractor of the actual rate of unemployment, Barro’s Ricardian equivalence theorem, and the idea of expansionary fiscal contractions based on the confidence fairy. The Global Financial Crisis has completely undermined those hypotheses or assumptions, because, as reported for a while on a sidebar of the website of the Financial Times, ‘the credit crunch has destroyed faith in the free market ideology that has dominated Western economic thinking for a generation’. Economics prides itself on being an empirical science. It cannot entertain these wild assumptions anymore. I just cannot see how models depicting imaginary economies (in contrast to models resulting from simplifications) have any usefulness.

Other mainstream concepts are under threat, in particular in monetary economics. Quickly once again, one can mention the quantity theory of money, the notion that excess reserves lead to inflation, the money multiplier story and its associated fractional-reserve banking system. Also under threat, in my opinion, is the belief in the usefulness of quantitative easing, the necessity of central bank independence and even inflation targeting. It is not clear anymore that some inflation rate is the true single target of several central banks; instead it seems that many central banks are as or more concerned with financial stability, the unemployment rate or the foreign exchange rate. It is difficult to claim that these central banks are still pursuing some kind of Taylor rule. The zero-lower bound story on nominal interest rates, although highly popular now, may also be a victim of winds of change.

Once again, heterodox economists are not the only ones who are appalled at the academic popularity of some mainstream models. Justin Wolfers (2016), who is a former graduate student of Blanchard, when presenting at a session honouring his former supervisor, has given a list of ‘things that probably aren’t true’. The list resembles the one I had independently compiled a year before, as found above. He lists the following concepts that almost certainly are false: rational expectations, DSGE models, consumption Euler equations, Calvo pricing, New Keynesian Phillips curves, the classical dichotomy. Whereas we were told that DSGE models based on sound micro-foundations were good at predictions, Wolfers shows instead that the workhorse of DSGE models has a dismal performance when it comes to one-quarter or four-quarter ahead forecasts of inflation rates and growth rates. There isn’t much left to justify the quasi-exclusive use of these models.

Orthodox authors such as Krugman or Wren-Lewis like to claim that the New Keynesian approach, which they often present as the realistic alternative to the hard-core New Classical model, has successfully internalized the zero-lower bound and has given space to counter-cyclical fiscal policy, thus implying that there is no need for heterodox alternatives since there is a sufficient amount of pluralism within neoclassical theory. But if we are to believe Wolfers, there isn’t much left of all strands of mainstream macroeconomics, be it freshwater or saltwater macroeconomics. Indeed, checking his list of things that are unlikely to be true, one can only conclude that Wolfers rejects all the essential constructs of the New Keynesian approach. One cannot claim that mainstream economics needs a bit of repair at the seams. New Keynesians claim that they are making reasonable modifications to the New Classical model; but the latter model, which acts as the base of the New Keynesian model, is pure madness, as claimed by Hope and Soskice (2016). If the foundations are not solid, nor will be the building.

Again using broad brushes, it is clear that some concepts have to be brought back from the limbo in which they had been since the Monetarist and Lucasian theoretical counter-revolution threw away from the mid-1970s to the early 1980s the little that was left of the Keynesian revolution. In my opinion, with depression economics being back, as Krugman would say, the following ideas are back into view: the crucial positive role of expansionary fiscal policy and the importance and relevance of fiscal policy at large; the possibility and even necessity of credit controls by the monetary and regulatory authorities – something that used to be supported by post-Keynesian monetary economists and which now seems to be advocated by some neo-Austrian economists [8]; the need to integrate into a single model the real economy and the financial side, by going beyond the introduction of the target rate of interest, for instance by considering the effects of the stocks of both corporate and household debt, as well as the immediate effects of the additions to these stocks. Two other claims, long made by heterodox authors, are now getting more attention from some international organizations: the favourable effects of controls over foreign capital flows, in particular short-term flows (Gallagher 2014); and the need to consider income distribution as a key component of aggregate demand – a long-time claim of post-Keynesian economists – as well as the realization that there is no necessary trade-off between income equality and growth.

The crisis has led to the reconsideration of many dogma in macroeconomic and monetary theory. Perhaps more importantly it has led some researchers at large international organizations to question their entire philosophical stance. Ostry et al. (2016), in an IMF journal with a large readership, wonder whether neoliberal policies have been oversold. They examine two standard neoliberal policies geared to promote long-term growth: first, fiscal austerity, namely the attempt to reduce fiscal deficits and public debt, notably by reducing the size of government expenditures (the so-called ‘expansionary’ fiscal consolidation); and second, the removal of restrictions on the mobility of capital across countries. Their argument is that these two policies did not increase economic growth, and that furthermore it did lead to more income and wealth inequality. The reason is that both of these policies reduce the bargaining power of labour and increase that of the rich and wealthy (Ostry 2015). But there is an additional twist to this story: ‘Increased inequality in turn hurts the level and sustainability of growth’ (Ostry et al. 2016, p. 39). In particular, free capital mobility increases the probability of a financial crisis and of large output declines, and these in turn are associated with increased income inequality. Thus, these authors conclude that ‘instead of delivering growth, some neoliberal policies have increased inequality, in turn jeopardizing durable expansion, (ibid, p. 38). [9]

On another front, there always was the feeling among heterodox economists that grants agencies were heavily biased towards orthodox economics. This also seems to be changing, at least in the UK, with a call by the Economic and Social Research Council (ESRC) for the creation of a new network devoted to an alternative understanding of macroeconomics. [10] The call is quite explicit about the criticisms that have been targeted at DSGE modelling and the insularity of mainstream macroeconomics. The call wishes to promote other approaches, such as agent-based modeling or alternatives incorporating other disciplines or other schools of economic thought.

Some orthodox economists believe that mainstream economics holds under normal conditions (Richard Koo’s yang phase), but that it needs to be modified under zero-lower bound conditions or during balance sheet recessions (Koo’s yin phase). Macroeconomic theory needs to be revised both for the yang and the yin phases. Providing new clothes to the Naked Emperor of mainstream economics won’t do; the Emperor needs to be dethroned.

Footnotes

[1] I heard Michael Kumhoff, from the IMF, make a very similar statement at the ‘State of economics after the crisis’ FMM Berlin conference in October 2012, despite the fact that obviously he is ready to entertain some eclectic views. Thus, if even dissident orthodox economists argue that the DSGE model is a must, there isn’t much room left for alternatives!

[2] This critique from Solow is ironically very similar to that made by Kaldor in 1966 and 1972 when he was arguing that neoclassical economics was based on unrealistic foundations and that removing the scaffolding of unrealistic assumptions with bits of realism would not make the theory any more solid. Goodhart (2009: 353) makes an assessment of the DSGE approach which is similar to Solow’s when he says that ‘like astronomers seeking to maintain the Ptolomaic system, they are trying to add refinements to make it consistent with the data’.

[3] Hope and Soskice (2016) present Carlin and Soskice (2015) as the textbook exemplar of this realistic modern macroeconomics. See Lavoie (2015) for a less enthusiastic assessment of their book.

[4] This is reminiscent of Lucas (1981, p. 224) who, when asked about how fundamental or radical uncertainty, by contrast with risk, could be taken into account, wrote that radical uncertainty had to be assumed away because ‘in cases of uncertainty, economic reasoning will be of no value’.

[5] Similarly, Bill White (2009), the former chief economist at the BIS, and currently the chairman of the Economic Development and Review Committee at the OECD in Paris, refers his readers to the works of Fisher, Minsky, Foley, Akerlof and Soros.

[6] As an example of this, Vítor Constâncio (2015), from the ECB, has recently pointed out that: ‘At the aggregate level, the euro area output is now 20 percent below the level it would have achieved had the trend growth in the previous 15 years continued after 2007….The crisis left a permanent economic loss with broad scars in our societies’.

[7] As a deputy-governor at the Bank of Canada says: ‘The decline in the participation rate of young and prime age workers reflects the cyclical effects of a weak job market. But these cyclical effects could become structural. After a long search, if you don’t think you are going to find a job, at some point, you become discouraged and you stop looking. The longer you stay out of the labour force, the more likely it is that your skills have deteriorated and your attachment to the job market has weakened. This is what economists mean when we talk about hysteresis’ (Wilkins 2014, p. 3).

[8] The ECB Targeted Long-Term Refinancing Operations (TLTRO) may be perceived as some sort selective credit control, in this case selective credit inducement.

[9] If capital mobility reduces the bargaining power of labour, then surely it is likely that free trade agreements have the same negative effect on the capacity of labour organizations to negotiate wages. Thus free trade is also likely to have detrimental effects on income equality and long-term growth. This was recognized by Jonathan Ostry during the question period in a seminar held at the University of Ottawa in the spring of 2016.

[10] See : http://www.esrc.ac.uk/funding/funding-opportunities/understanding-the-macroeconomy-network-plus/.

See original post for references.

I was recently in the BoE museum because I wanted to see how they explain what they do to the public, and they literally use a fair-weather model — the UK is a sailing boat, sailing an endless expanse. The parameters fed into the model were the amount of sail you carried on the mail sail, opening/closing a second, smaller sail, “wind speed”, and whether there were other ships passing you (and blocking/stealing your wind).

Foppe

September 26, 2016 at 10:33 am

Taking your analogy, did the Titanic sink because it was poorly designed or was it poorly sailed???

Answer: Both

(Wikipedia: Titanic’s high speed in waters where ice had been reported was later criticized as reckless, but it reflected -standard maritime-* practice at the time. According to Fifth Officer Harold Lowe, the custom was “to go ahead and depend upon the lookouts in the crow’s nest and the watch on the bridge to pick up the ice in time to avoid hitting it.” – – well, with hindsight, that sure looks reckless)

*standard maritime practice – Apparently: 1st consideration; profit – – 2nd consideration; passengers lives

It is hard to respect a profession that seriously puts forth the proposition that when the economy is calm we know how to describe that (normal!), but in a financial crisis we have no idea of how to predict that, what causes it, or how to fix it….

Titanic was both faster and less maneuverable than prior ships, so the standard practice ran into a practical limit.

They think in yachting terms. Their job is to make sailing for the wealthy as pleasurable as possible. They probably cannot imagine what it is like not to have a yacht. Actually, they probably believe that not having a yacht is the free market signalling what a loser one is.

Just a quick thought that kind of bugged me right from the get-go. It’s partly an issue of a sentence that lacks a subject, as in, who has questioned, and who is it that is being referred to now as asking questions :

“it is only with the advent of the US subprime financial crisis that macroeconomic and monetary theories put forward by mainstream economists have started to be questioned.”

The thing is, this isnt remotely true in a sense. When I went through the graduate economics curriculum in the mid 90s, there were some people that questioned things. Much as in the case of the WFC debacle, the same methods (and outcomes) are employed against those that question authority.

1) the questioners quit the program in disgust (WFC not fraud underlings quit their job)

2) the questioners persist and are failed out of the program (WFC little people fired for other causes)

3) the questioners push the claim via some internal channel and are asked politely to leave (WFC whistleblower policy, then firing)

Anyway, on with the show.

Well said, that is consistent with my experience as well.

I don’t think it’s just poor sentence construction. I have been disappointed for some time in INET and similar supposedly leftist/critical groups’ astounding lack of interest in actually applying human agency to the course of public policy over the past few decades. It’s as if they buy the fundamental premise that things just happen naturally and nobody saw it differently or bothered questioning what was happening.

Between your comment and JEHR below, the NC commentariat assembled a much more insightful critique in a lot fewer words.

I looked for the word “fraud” and it is not in the article. How can one describe an economic system and not include the word fraud to describe some of its aspects?

Nor “fraud”, or “theft”, or “national interest”, or “monopoly”, or any of those other things they assume could/will never happen.

Having a cartel control the world price of a commodity essential to the function of any economy out of the horse and buggy-whip stage, makes any economic arguments about “free market” pointless, IMO.

Economists are innocent puppies, just like Greenscam in front of Congress, rubbing his eyes in disbelief at the discovery that his bankster buddies are hardened unrepentant criminals only looking out for their interests.

Or lazyness, accomodation, lack of rigor, selfish indulgence. Mainstream economics or popular economics looks like anything but science. At least it shows that few economists, like Blanchard were able to change their mind but unable to figth the powers that be. That’s ocurring in China apparently. The Premier knows what should be done but he is not able to do it.

Interesting scoring analysis of Trump’s trade plan by Peter Navarro of UCIrvine here:

https://assets.donaldjtrump.com/Trump_Economic_Plan.pdf

canonicalthoughts.blogspot.com

I believe as suggested in several of the comments above the underlying structure of the economy has changed since the days of Keynes. Many of the assumptions current economic theories were built on no longer hold — if they ever did. Entrepreneurs are rarer than unicorns. The Captains of Industry care little about growing their businesses but to the contrary focus their efforts on ways to loot as much wealth as possible before their firms collapse. Corporations operate without constraints writing their own laws and use the government regulatory authorities they’ve captured to increase their monopoly profits and constrain or drive out smaller competitors. The Government sector which macro theory models as a controlling factor using fiscal and monetary policy to moderate the inherent instability of the market has turned into a Corporate piggy bank and the purveyor of policies driving instabilities.

Asserting that Macroeconomic Theory needs some re-thinking is an extreme understatement.

“Entrepreneurs are rarer than unicorns?” Please don’t make stuff up. In my own family, more of us are running our own businesses than not, and ones started in the last ten years to boot.

Companies faced fewer constraints in Keynes day than now. No product safety rules, no securities laws, a toothless FDA (it didn’t become powerful until the horrific death of Eben Byers from radiation tonics), no truth in advertising laws, no restrictions on campaign finance.

No matter. It’s still the same ol’, same old sh*t.

Pardon me for the pushback but I find very little to argue with in Jeremy’s post. I agree that entrepreneurs are not rare, but all too many of them seem to be of the Martin Shkreli persuasion. Outside of that I think he’s spot on.

IIRC, in Keynes’ time some of the “Captains of Industry” were actually convicted of crimes resulting from the Depression. Today, corporations have most of the rights of citizens with few of the responsibilities. Now I don’t argue that there aren’t any good corporations out there, but the biggest and most important seem bent on controlling our lives for their own perceived benefit. For the last 40+ years, we’ve been told that businesses are more important than people and the laws have progressively been passed to affirm that view.

Now you might be right about product safety rules (not sure about driverless cars) and the FDA, but as for the rest I beg to differ. Are there any effective securities laws in place now? And is there really any “truth” in advertising and what effective restrictions are there on campaign finance? Maybe ask the Clintons? Do you really believe that corporations today are more “constrained” than they were in the 30’s?

And I think his last sentence is an extreme understatement.

Martin Skreili is a hedgie, not an entrepreneur, and anecdote is not data. There has been a fall in new company formation, but that parallels the lack of new home formation. Both are results of the crappy recovery. People don’t start new businesses in a time of slack demand. That happens in recessions and is completely expected in conventional theory.

“Captains of Industry” were not convicted of crimes in the Great Depression. I have no idea how you dreamed that one up. The only person to go to jail as a result of securities fraud, despite the Pecora Hearings, was Richard Whitney, and that was for what amounted to old-fasioned embezzlement well after the Great Crash rather than any of the scams typical in the runup to the Great Crash.

I used Shkreli as an example that not all “entrepreneurs” are wonderful. Clearly there are some entrepreneurs like yourself that are worthy of emulation. But I believe there are plenty who are not. My question (which I maybe didn’t phrase correctly) was whether you rejected all of Jeremy’s post because of one or two minor problems. Because that’s the way it seemed to me – though I might be wrong about that.

I suspect you’re right about Whitney, it’s been a while since I read Galbraith’s book. But during FDR’s term Congress did pass Glass-Steagall which has since been repealed. Now maybe I’m wrong, but it seems to me that since the 30’s the laws have been changed to favor corporations in a big way. I’d add that since the great financial crash, nobody has been convicted of embezzlement or anything else to my knowledge.

You talk about “conventional theory”. I’d suggest that conventional economic theory has shown little ability to explain the economy and even less to predict the economy. I also think that these are unconventional times. When have we ever had ZIRP & NIRP & QE before? I know that economists are protective of their territory, but maybe it is time for them to rethink their assumptions.

As Jeremy put it: “Asserting that Macroeconomic Theory needs some re-thinking is an extreme understatement.”

I think the whole exercise is like trying to understand the flow of oceans when you don’t even know what water is, ask 90% of mainstream economists what money is and how it is created and they will not be able to say (no, it’s not when banks receive deposits and then loan out against them). And when the entire warp and woof of the economy is based on debt, then that, and the price (or lack thereof) of money is the only thing that matters. This then leads to the notion that endlessly issuing new debt to steal demand from the future can work for a very long time but it just may not work forever. Now we’re headed for NIRP, not just in 38% of sovereigns as we have today, but in 100%. Play that one out for a moment, when NIRP hits 5% what happens? 10%? 20%? The old saw “yes but a debt is somebody else’s asset” gets a very new twist to it.

So I predict collapse, read history sometime, there is nothing in the slightest that is new about all this. Debt-based money regimes collapse, not most of the time or 95% of the time, but 100.00% of the time.

debt-based as opposed to what?

I’ll admit to hyperbole but not to making stuff up. I sometimes browse in strange pastures: [https://www.newamerica.org/open-markets/in-the-news/declining-entrepreneurship-labor-mobility-and-business-dynamism-demand-side-approach/ — Barry C. Lynn — the site won’t play nice in my old browser — Lynn is the author of “Cornered”]

I have trouble equating the initiators of most small business startups I know of with what I would like to term an entrepreneur. I guess I’m guilty to over romanticizing entrepreneurs. After attending several presentations by the local branch of SCORE I left with the impression that many small business startups were selling services to the local big businesses. Often the presenters were selling a service they previously provided as employees before they were laid off. I don’t know many people who started their own businesses. I’ve watched many small businesses in the areas I where I’ve lived close. If anything replaced them it was usually a franchise.

I’m not sure what you’re by suggesting by pointing out the greater constraints on business now as opposed to Keynes day. I like the constraints you mentioned. I don’t know enough about the details of regulatory practice to provide examples for how big business uses those regulations to stifle competitors — but I believe it is done. I like to believe that the businessmen in Keynes day were running a business to grow the business — that the guy running General Motors came from the car making side of the business not the finance group. And in Keynes day a bump in Government spending would put Americans to work not man-up a factory in some other country or bring in more H1B workers.

I believe Macroeconomics needs to look deeper at the structure of the economy that lies below the aggregates they build into their models. I also believe international trade adds an external component to Macroeconomics which seems to get lost in a focus at the national level.

Supply side economics was always a scam, a belief, a fantasy. For those paying attention, even during this period of no demand businesses have been investing and generating tremendous returns on that investment. They have been paying lobbyists, doing inversions, rigging the markets, and committing fraud and other crimes with campaign donation immunity. That is how supply side works in the real world. It does nothing for the rest of us but it is the inevitable product of supply side economics. Demand side economic works very rationally and predictably. It benefits society at large, which is its problem.

“Demand side economic works very rationally and predictably.”

The Oracle has spoken. Demand side economics is the One.

So, no can opener?

Think of the hungry economist children.

All kidding aside, a fascinating article that may further more productive discussion.

Nice, but really…to quote the great Joan Robinson and say nothing of imperfect competition?!

Amends in advance… re-posting some stuff from a conversation with an AET sort….

Anywho…. money multiplier thingy….

In his book The Years of High Theory, GLS Shackle sums up the problem of the multiplier nicely and succinctly as such,

The Kahn Multiplier multiplies extra income not matched by extra consumable output, and it is of no consequence to the people of one country, seeking a means to increase their own employment, whether that original extra income is generated by the extra output of tools, or of goods for export uncompensated by extra imports, or whether it is a free gift of the government or private philanthropy. Kahn chose road-building as his example, doubtless because it is unnecessary to explain that roads cannot be sold to consumers. (p186)

This gets right to the heart of the matter and Shackle highlights precisely the sentence that is most important so that I don’t have to. When investment is increased new consumer goods do not become available immediately and thus the multiplier effects generate income and consumption that must be matched by the current output capacity of the economy or else they will cause inflation.

Now, here’s the problem for marginalist theory: if the economy is operating at full capacity, as is the typical case in a marginalist model, then how does an increase in investment not lead to inflation? The answer is familiar to any undergraduate who has done his homework: the new investment must be stimulated by a rise in savings. The process here is conceptualised as one in which the causality runs, not from investment to savings, but rather from savings to investment.

Now here is the rub… but since many variants of the quantity theory — like monetarism in particular — assume a constant velocity they have very little to say about the non linear dynamics. In other words this camp assumes conditions based on a preference regardless if is true or not and then extrapolates from that perspective.

Disheveled Marsupial…. is caveat emptor applicable to econ[n*]omics – ????? – faith based ™…

Part dux….

Marginalist economics tends to be characterised primarily by a couple of distinct axioms that operate ‘under the surface’ to produce its key results. these are simplistically characterise as: the axiom of methodological individualism; the axiom of methodological instrumentalism; and the axiom of methodological equilibration, where models derived from them have ex-ante predictive power.

This is historically Epicurean philosophy, example, Epicurus wrote,

“The magnitude of pleasure reaches its limit in the removal of all pain. When such pleasure is present, so long as it is uninterrupted, there is no pain either of body or of mind or of both together.”

Which is a reflection of its materialistic atomism which is basically identical with the marginalist focus on atomistic individuals and makes it an atomistic doctrine. Thorstein Veblen where he wrote in his Why is Economics Not an Evolutionary Science?:

“The hedonistic conception of man is that of a lightning calculator of pleasure and pains, who oscillates like a homogeneous globule of desire of happiness under the impulse of stimuli that shift him about the area, but leave him intact. He has neither antecedent nor consequent. He is an isolated definitive human datum.”

Which in turn is just Epicurean ontology where everything becomes objects and not subjects where Epicurean ethics involves individuals maximising pleasure and minimising pain — or, as the marginalists would put it, maximising utility and minimising disutility — it simply follows from the basic ontological position that is put forward.

Just to put a more modern perspective on it – see: Note that the patient suffering from schizophrenia tends not to answer the questions directed at him but rather responds with complete non-sequiturs.

“In his book, King lays out how economists have tried to establish supposedly disaggregated “microfoundations” with which to rest their macroeconomics upon. The idea here is that Keynesian macroeconomics generally deals with large aggregates of individuals – usually entire national economies – and draws conclusions from these while largely ignoring the actions of individual agents. As King shows in the book, however, the idea that a macro-level analysis requires such microfoundations is itself entirely without foundation. Unfortunately though, since mainstream economists are committed to methodological individualism – that is, they try to explain the world with reference to what they think to be the rules of individual behaviour – they tend to pursue this quest across the board and those who proclaim scepticism about the need for microfoundations can rarely articulate this scepticism as they too are generally wedded to the notion that aggregative behaviour can only be explained with reference to supposedly disaggregated behaviour.”

http://www.nakedcapitalism.com/2013/02/philip-pilkington-of-madness-and-microfoundationsm-rational-agents-schizophrenia-and-a-noble-attempt-by-one-noah-smith-to-break-through-the-mirror.html

You might also like – Le Bon, Gustave. The Crowd: A Study of the Popular Mind, you can get it free online.

Additionally – The Myth of the Rational Market: Wall Street’s Impossible Quest for Predictable Markets

by Justin Fox

Chronicling the rise and fall of the efficient market theory and the century-long making of the modern financial industry, Justin Fox’s “The Myth of the Rational Market” is as much an intellectual whodunit as a cultural history of the perils and possibilities of risk. The book brings to life the people and ideas that forged modern finance and investing, from the formative days of Wall Street through the Great Depression and into the financial calamity of today. It’s a tale that features professors who made and lost fortunes, battled fiercely over ideas, beat the house in blackjack, wrote bestselling books, and played major roles on the world stage. It’s also a tale of Wall Street’s evolution, the power of the market to generate wealth and wreak havoc, and free market capitalism’s war with itself.

The efficient market hypothesis–long part of academic folklore but codified in the 1960s at the University of Chicago–has evolved into a powerful myth. It has been the maker and loser of fortunes, the driver of trillions of dollars, the inspiration for index funds and vast new derivatives markets, and the guidepost for thousands of careers. The theory holds that the market is always right, and that the decisions of millions of rational investors, all acting on information to outsmart one another, always provide the best judge of a stock’s value. That myth is crumbling.

Disheveled Marsupial…. the reason I call it quasi religious at the end of the day it purports reality, then ascribes it and then codifies it as undeniable universal truth, that can not be undone or falsified, and makes no allowance for new information [inelastic at best] or the acknowledge its own failures. Imagine all life and potential on this orb strapped to an insane Moby Dick whale with the mental processes of the Dark Star bomb.

PS. this is your brain on….. https://www.youtube.com/watch?v=ub_a2t0ZfTs

During the 1930’s world depression Keynes viewed the policies of manipulating the interest rate as an ineffective tool. However, Conservatives and their economic guru, Milton Friedman, later sold monetary policy as less intrusive than Keynesian fiscal policy. John K. Galbraith describes the rise of monetary policy during the 1970’s as unfortunate. He writes, “Money: Whence It Came, Where It Went”(1975) the following early history of monetarism.

Unfortunately Ben Bernanke studied the Great Depression and not the events leading up to 1929.

What did the bankers do before 1929?

They made bad loans and bundled them up into securities to sell them on.

As they could get these bad loans off their books, they could carry on making more and more loans.

Most of this lending was margin lending into the US stock market.

What did Glass-Steagall stop bankers doing?

Making bad loans and bundling them up into securities to sell them on.

When investment and retail banks are separate, the retail banks have to take responsibility for the loans they make as they stay on their books.