By Lambert Strether of Corrente.

I feel a little bit like a Beltway operative whose ricebowl has been smashed; after three years of writing post after post about ObamaCare (“The History of ObamaCare, 2013-2016”), ObamaCare is going to be “repealed” and “replaced”, although citizens consumers won’t have any idea how the changes will net out for them until the actual replacement has at least been proposed.[1] And I’m not the only one who thinks that “nobody knows anything”; all the coverage is massively caveated, so I selected two of the caveats, which also apply to this post. From HealthBlawg:

Some MSM outlets reported last week — as if it were news — the President-elect’s support for some key components of Obamacare. While the man seems to be heavily influenced by the last person he spoke with, and he was interviewed shortly after his initial transition meeting with the outgoing president, it is impossible to predict with certainty what the future holds, in the health care realm as in many others. Despite the campaign rhetoric, the president-elect is a political naïf, a policy tabula rasa, and until we have a clearer picture of who his key appointees and advisors will be, and of whether, and to what extent, he is likely to actually follow their counsel — or simply allow them free rein — there’s no way of knowing exactly what to expect.

And this headline from Vox:

Will Obamacare be repealed? Replaced? Amended? We have lots of clues, but they all point in different directions.

At this point, I’ll have to introduce new vocabulary: I’m going to call whatever system replaces ObamaCare TrumpCare. And I do think we can know something about “what the future holds”:

- TrumpCare will be a neoliberal, market-based solution

- Trump has said he wants to retain coverage of pre-existing conditions, may want to abolish the individual mandate, and wants to allow insurance to be sold against state lines to cut costs

- If selling insurance across state lines is TrumpCare’s policy nostrum, TrumpCare will fail as badly as ObamaCare

Before I turn to the future, which lies ahead, some brief notes about the politics of TrumpCare. One theory is that Trump must deliver on repealing (and replacing) ObamaCare, because that’s what his voters demand. Bob Laszewski, who made a lot of good calls about ObamaCare, especially during the rollout:

Obamacare will effectively be repealed. No ifs, ands, or buts about it. The Trump voters voted for him expecting that he and the Republicans would do it and there is no turning back. This will be the first if not one of the first agenda items. Speaker Ryan, at his press conference this morning, reaffirmed that.

(Of course, Democrat voters thought they would be getting “hope and change” with Obama. Perhaps Republican leaders will be luckier in their candidate.) And here’s the “fear the base” rationale:

Don’t forget the point I have been beating the drum on for the last three years––half of those with Obamacare compliant individual health policies do not get a subsidy. I expect the vast majority of these people, hit with the big premiums and deductibles, voted for Trump and the Republicans.

(And the ObamaCare price hike the week before the election can’t have helped with those voters. There seems to be no exit polling on this.) A second theory is that Trump will not be able to repeal (and replace) ObamaCare because ObamaCare is too complicated and too interlaced with too many interests (including citizens consumers, to change rapidly. Modern Health Care:

Some Republicans are worried about moving too fast and too far on healthcare changes, risking blowback from the public and stakeholder groups and potentially hurting their party in the 2018 congressional elections. The CBO concluded that the GOP repeal bill vetoed in January would add 22 million Americans to the ranks of the uninsured. Modern Healthcare’s second-quarter CEO Power Panel survey of healthcare executives found that more than two-thirds of 86 chief executives opposed repealing and replacing the ACA.

In fairness, a survey of Republican health care plans put coverage losses at far less than 22 million, so, again, we can’t know how TrumpCare nets out until… we know what it is. And Republicans may fall to fighting among themselves. There are also Inside Baseball issues of how the Republicans will use reconciliation in the Senate to do whatever is that they will do.

So having said what we don’t know, let’s look at what we do know.

TrumpCare Will Be A Neoliberal “Solution”

ObamaCare is a neoliberal, markets-first plan, and if or when it is repealed, it will be replaced by a neoliberal, markets-first plan. In fact, in one of life’s little ironies, ObamaCare is a Republican neoliberal program. For our newer readers:

Make no doubt. Romneycare was the model for Obamacare.

And Brad DeLong writes in 2010:

The conservative DNA of ObamaCare is hardly a secret. “The Obama plan has a broad family resemblance to Mitt Romney’s Massachusetts plan,” Frum wrote. “It builds on ideas developed at the Heritage Foundation in the early 1990s that formed the basis for Republican counter-proposals to ClintonCare in 1993-1994.”

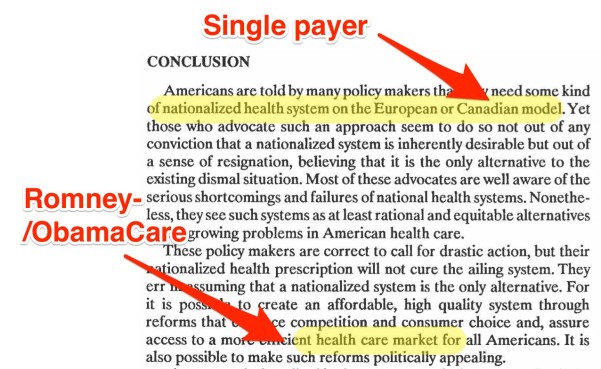

Now let’s consider those Heritage “ideas,” because they ended up setting the boundaries for acceptable discourse in the policy debates that followed. In a 1989 Heritage Foundation brief, Assuring Affordable Health Care for All Americans, Heritage Foundation’s director of domestic policy strategies, Stuart M. Butler, Peter J. Ferrara (George Mason), Edmund F. Haislmaier (Heritage), and Terree P. Wasley (U.S. Chamber of Commerce) proposed the essence of ObamaCare: “[E]very resident of the U.S. must, by law, be enrolled in an adequate health care plan to cover major health care costs.” However, from the “political advantage” standpoint, the key goal of the Heritage plan was to fend off single payer. From the conclusion:

The mandate made its political début in a 1989 Heritage Foundation brief titled “Assuring Affordable Health Care for All Americans,” as a counterpoint to the single-payer system and the employer mandate, which were favored in Democratic circles.

So, reminding ourselves of Jeff Sessions’ strictures on “anything goes” post-modernism, we have Democrats (Obama + Gruber) adopting a Heritage-inspired plan pioneered by Republicans (Romney + Gruber), whereupon the Republicans turn around and fight their own plan tooth and nail, while the Democrats, fighting back furiously, never mention they adopted the Republican plan. However, we also find Democrats, Republicans, Heritage, and Gruber in simultaneous agreement that “single payer” is verboten, taboo, unmentionable, “off the table,” and not politically feasible. So all parties noisily and venomously seek “political advantage” at a level of mind-boggling illogic and contradiction, but the real policy conflict — the policy both parties and the political class seek to avoid — is buried, and never mentioned at all.

TrumpCare operates in the same policy space, because markets. On TrumpCare, I’ll quote the putatively wonkish Paul Ryan, since Lazsweski highlights Ryan’s work, considering it “as detailed as the plan Bill Clinton or Barack Obama had the morning after they were elected.” Ryan’s impressive-looking site, A Better Way, has several PDFs on health care. From the policy paper:

Americans deserve a competitive insurance marketplace that provides quality care at an affordable cost. But, this does not mean returning to the pre-Obamacare status quo. Our health care system has been broken for decades because people lack the most basic tools they need to make decisions that are right for them. Red tape hides information on prices and quality, bureaucrats in Washington put themselves between doctors and their patients, and choice and competition take a back seat to federal mandates and coercive taxes.

(I like “Americans deserve.” Because, as we know, “you can’t always get what you want.”) The “big gummint” rhetoric is different from Democrat’s, but the concept — If only people had better information! — is identical. And then there’s this:

Unleashing the power of choice and competition is the best way to lower health care costs and improve quality. One way to immediately empower Americans and put them in the driver’s seat of their health care decisions is to expand consumer-driven health care. Consumer-driven health care allows individuals and families to control their utilization of health care by providing incentives to shop around. This ultimately lowers costs and increases quality.

Again, I can’t imagine Obama using rhetoric like “unleashing the power of choice and competition.” Obama says buying health insurance will be like buying a flat-screen TV. But the concept — go shopping! — is identical. That doesn’t mean that TrumpCare won’t further crapify what you’re shopping for. Health Affairs surveyed eight Republican health care plans offered between 2012 and 2015:

Regarding guaranteed issue, medical underwriting, and pre-existing condition exclusions in health insurance policy rating, while all plans endorse the principle of guaranteed issue, all but one require that individuals have at least 12-18 months of continuous coverage to avoid medical underwriting. Though two plans preserve the ACA’s ban on lifetime benefit limits in insurance, six do not, and all but one (Roy) eliminate the ACA’s ban on annual benefit limits.

In summary, the plans demonstrate a clear intent to deregulate most consumer protections established in the ACA, and to eliminate the individual and employer mandates. More limited tax-based assistance would be available to fewer consumers and that assistance would not vary by income. Guaranteed issue and the elimination of pre-existing condition exclusions would apply only to individuals who can maintain continuous coverage.

Of course, ObamaCare being in a death spiral of rising rates, crapifying policies, and falling enrollment, there’s no telling what the Democrats would have picked from this laundry list.

Trump, Preexisting Conditions, the Mandate, and Selling Insurance Across State Lines

Here’s what Trump had to say in the CNN-Telemundo Republican debate:

MODERATOR: Mr. Trump, Senator Rubio just said that you support the individual mandate. Would you respond?

TRUMP: I just want to say, I agree with that 100 percent, except pre-existing conditions, I would absolutely get rid of Obamacare. We’re going to have something much better, but pre-existing conditions, when I’m referring to that, and I was referring to that very strongly on the show with Anderson Cooper, I want to keep pre- existing conditions.

I think we need it. I think it’s a modern age. And I think we have to have it.

MODERATOR: OK, so let’s talk about pre-existing conditions. What the insurance companies say is that the only way that they can cover people is to have a mandate requiring everybody purchase health insurance. Are they wrong?

TRUMP: I think they’re wrong 100 percent. What we need — look, the insurance companies take care of the politicians. The insurance companies get what they want. We should have gotten rid of the lines around each state so we can have real competition.

Parsing Trump, which is not easy, we see:

1. Clear: “I want to keep pre-existing conditions.”

2. Clear: “We should have gotten rid of the lines around each state so we can have real competition.”

3. Not clear: “I agree with that 100 percent, except pre-existing conditions, I would absolutely get rid of Obamacare.” Since Trump is asked “you support the individual mandate. Would you respond?” Trump seems to be saying (“I agree with that”) that he supports (!) the mandate. But he also says that he would “get rid of ObamaCare,” with the only exception being preexisting conditions. My interpretation is that Trump would abolish the mandate. His campaign site says he will:

Completely repeal Obamacare. Our elected representatives must eliminate the individual mandate. No person should be required to buy insurance unless he or she wants to.

However, the Trump transition site page on health care is silent on this topic. Trump doesn’t mention the mandate in a recent interview with the Wall Street Journal. Ryan is equivocal, at least on his own site[2]. The survey of other Republican plans is from 2015, and so does not include Ryan’s plan, but most of those plans do abolish the mandate.

I’m going to assume that Trump misspoke in debate and wants to abolish the mandate. Of course, if Trump’s replacement plan includes a mandate, he’ll be following in Obama’s footsteps: Obama slammed Clinton in 2008 for having a mandate for her plan; then he incorporated a mandate in his own plan when he was elected. And I’m further going to assume that Trump’s solution to rising health insurance premiums is selling health insurance across state lines; certainly they are juxtaposed in his own mind.

Selling Insurance Across State Lines is Snake Oil

Unfortunately, selling health insurance across state lines is a seemingly reasonable policy proposal that has lousy results. Michael Hiltzik has an excellent takedown in the Los Angeles Times. He points out two problems. First, the proposal encourages a regulatory race to the bottom:

On the face of it, lowering state-level barriers to health insurance sales would launch a race to the bottom akin to what happened with credit-card regulations after 1978. That’s when the Supreme Court ruled that credit card regulations could be exported by banks located in one state to customers located anywhere else. (This was no reactionary ruling, by the way; it was a unanimous opinion, written by arch-liberal William Brennan.) The result was that credit card-issuing banks set up shop in places like South Dakota and Delaware, which had virtually no usury laws, effectively nullifying other states’ limits on credit card fees and interest rates. One can envision a similar reaction in health insurance.

The second problem is more subtle:

The key is that healthcare is almost always delivered locally. Even if a Southern Californian’s insurer is located in, say, Idaho, his or doctors and hospitals are almost certain to be nearby. To provide coverage, Joe’s Insurance would have to make deals with local providers in its new markets, creating its own local networks and agreeing on fees.

The typical tradeoff is that Big Insurer A promises Hospital B access to its thousands of local enrollees, if Hospital B agrees to treat them at a preferential rate. [Richard] Mayhew, who does this stuff for a living, tells us: “Insurers have leverage against providers when the insurer can credibly promise to direct a large number of covered lives to or from a particular provider. Providers have leverage when they don’t think that the insurer is bringing a lot of members.”

Insurers entering a new state from far away will have no leverage because they’ll be building their customer base from scratch and therefore will have only minimal business to offer hospitals or doctors in their new state. They’ll have to pay premium rates to attract these providers, at least at first; and to attract more customers they’ll have to offer competitive premiums.

Multi-state networks work under limited conditions, chiefly in metropolitan areas that span several states; an insurer in the Washington, D.C., market needs to offer a network of doctors and hospitals in the District, Maryland and northern Virginia, for example.

Everywhere else, this is a formula for big losses in the first few years of expansion, at least. One could argue that such a loss-leader strategy might work in the long run, but the big U.S. insurers such as Aetna and United Health have shunned the loss-leader game under Obamacare — they’ve pulled out of the market because they’re unwilling to sustain losses until it stabilizes. What makes anyone think they’d jump back in?

We know the answer: They won’t. We know because the ACA allows states to reach compacts with other states to allow cross-border insurance sales (compacts are essentially interstate treaties). Georgia, Maine and Wyoming have passed laws enabling such compacts.

So, another case of the dogs not eating the dog food. We could, of course, subsidize the insurance companies as they seek to stand up their markets. But that would be expensive, complicated, unwieldy, and would give big gummint a leading role…

Conclusion

What we do know is that TrumpCare, like ObamaCare, will be a neoliberal, markets-first solution. So the country will have oscillated from the left side of the Overton Window to the right, and simple, rugged, and proven single payer will still be unmentionable in polite company; it will be interesting to watch liberals squirm to avoid discussing it. Since we can cross selling insurance across state lines off as any kind of solution, I’d be surprised if TrumpCare didn’t end up looking like a crapified version of the already crapified ObamaCare.[3] For pre-existing conditions in particular, the Republican plans from 2015 all crapify the coverage (with, for example “at least 12-18 months of continuous coverage” being required). Too bad the Democrat victory in 2008 was such a squandered opportunity.

NOTES

[1] There are also the actuarial issues of selling a product in a marketplace that is be about to be abolished. How does that work?

[2] Coverage of Ryan’s policy paper says that it will abolish the individual mandate. The policy paper itself is more equivocal; it inveighs against mandates, plural, but nowhere does explicitly say that the individual mandate will be abolished. The same is true of the “Snapshot,” a short version of the policy paper. The same is true of the FAQ, which uses verbiage like “ending expensive mandates,” but nowhere mentions the individual mandate. Perhaps that’s because the Republican hive mind hasn’t figured out how to square the circle of having enough healthy people in the pool for the insurance companies to make a profit without a mandate.

[3] Perhaps they’ll make the Exchanges go away? Or privatize them? Throw Jeff Bezos a bone and sell health insurance on Amazon? With customer reviews turned off, of course.

Yes it would be and Bezos hates trump and might leave comments on …he can put I am just the middleman in big letters.

also a back door to dismantling Medicare, which works so well, and bury it as a model.

Paul Ryan is said to want to use Obamacare repeal to dismantle Medicare.

Yes. This.

Ryan and Trump discussed it during the long slog election process. Trump told Ryan that while he was telling his fans that he (Trump) would “protect Medicare & SS,” that actually he (Trump) was on board with Ryan for cutting and gutting both. That’s why Ryan finally gave a low-level endorsement of Trump.

So get ready for Medicare to come under the knife. Hope Trump supporters enjoy that.

The report I saw was that Trump told Ryan he personally wished it was possible to get rid of Medicare but he couldn’t do it because too many people needed it. So Ryan felt Trump was on board personally but Trump would not support getting rid of it.

But this could be one more of those Rorschach ink blots where Trump says something and you can take away any of three different interpretations. And who knows what will happen once Trump is in office with a R Congress supposedly eager to gut all these important programs that voters love (seriously, people who actually vote and do so consistently). Maybe this Congress will have to relearn what it did in 86: you do not mess with Medicare.

>was that Trump told Ryan he personally wished it was possible to get rid of Medicare but he couldn’t do it because too many people needed it

Haha so what does that even mean? More to the point, who the heck would be privy to (and leak) this kind of conversation. I;m beginning to wonder if Donald Trump even exists, or if this is a mass – but also weirdly individualized – hallucination brought on by our Alien Overlords.

For some reason, people think that commercial (or frankly, any kind of) success requires considerable competence (which is then extrapolated towards some kind of absolute like “perfection”), permitting them to see more “there” to Trump than is actually there.

Not just Trump, of course. “Experts”. “Professionals”. Perceived elites of all kinds.

But for the most part, aggressive behavior is sufficient. Trump certainly has that. Combine it with the diffuse half-statements and history rewriting, and a desire to please either the person he’s conversing with, or an audience, and there’s the “there”.

Exactly. Combine that with an inheritance that buffered early small failures and a narcissistic tendency to not hold loyalty to any person or position.

I keep coming back to this and I wish the press would report more on it: Trump is a PURE clinical narcissist, with some co-morbidities. Narcissists are *always* looking for narcissistic supply; they can’t help themselves; thus, *whatever action appears to result in the enhancement of narcissistic supply* will be the direction taken.

It’s very difficult to predict future actions with a narcissist, because many factors come into play; there is very little in the way of “what is good for the nation” in Trump’s psychic makeup; it’s more about “what things can I do for that nation (my voters) to increase the adulation that IS my identity”. It’s not a conscious process, in Trump’s case.

Every individual – including Trump – has many competing psychic variables. What does Trump consider the most valuable kind of praise; the kind of praise that makes him feel best? Is it the crowd; his immediate family; being deferred to; “winning”? It’s all too complex to figure out. We are not Trump.

Also, remember, at bottom, narcissists are *incredibly * insecure; this is why Trump needs counsel from his family, from people he trusts and whom he knows would never betray him under any circumstance.

Personally, I think his daughter and her husband have figured out how to get to Trump; it’s not a cynical kind of manipulation, but a way towards keeping him aloft. Look to the people closest to Trump (his family) to get a clue as to how he will behave. Look at their preferences and inclinations. Ivanka appears to be the person he trusts the most.

Until we actually start to see how all the political variables play out – mixed with the psycho-dynamic variables of Trump’s various pathologies – it’s going to be hard to know what to expect.

Trump has already been attempting to insulate himself from public exposure; he’s hanging out in his gilded womb in Trump Tower. His new gig is not about putting your head down and figuring out how to overcome or outsmart the planning commission in NYC and elsewhere, so a building can be built; it’s way more complex than that.

Trump is not stupid; he sees that there are so many MORE things that can go wrong than in his business; so many MORE things that can cause his image to falter. Trump *cannot*;*must not* lose narcissistic supply. I can’t even begin to describe the panic that Trump is probably feeling at this moment; thus, the bravado and continued behaviors that brought approval during the campaign. ANYTHING to keep narcissistic supply flowing. THAT is what his term – if he lasts – is going to be more about than any policy decision. Trump is not aware of this; and thus, the danger.

Hard to believe; attacking Medicare is political suicide. Old people aren’t real big on rioting, but that might do the job.

Well, this old person is down for a riot. I signed up for Medicare Part B in October, having lived in the warm and fuzzy cocoon of a platinum employer-provided health plan for the last ten years since I turned 65. (My husband finally retired.) Here’s what I learned.

The Medicare market has been captured by for-profit health ‘insurance’ corporations. I signed up for Traditional Medicare for the remainder of 2016, at a monthly premium, which has been adjusted upwards from the base amount of because our 2014 income was on the high side, from $105 to $170. (I don’t have a problem with that; those who can afford to pay more, should.)

This monthly payment is automatically deducted from my social security benefit.

Next, Medicare Plans A and B do NOT cover the cost of prescription drugs. I take only one, very cheap generic for mild hypertension, which would cost only a few dollars per month. BUT, if I do not enroll in a Plan D prescription program within 60 days after enrolling in Medicare Part B, the system imposes a financial penalty on me. So, turns out all these drug plans are administered by for-profit insurance companies. I look for a plan with the least expensive monthly premium … which comes out to $18 … and enroll. (I will not torment you with the tales of my hours spent on the phone with this for-profit company when they decided my on-line enrollment through the government medicare site, which was quick and easy, BTW, was not valid.) Goddess help me if I then need a prescription drug which is not on that plan’s formulary. My crystal ball has been a bit foggy these days. They finally accept my application and send me a bill. Yea!

But, for 2017 I face a bewildering array of choices. I can stick with the Traditional Medicare, and face possible rejection from health care providers who object to not being paid for months. Or, I can chose from a bewildering variety of Medicare Advantage Plans, sold by for-profit companies. Literally, hundreds of options that only a retired person (with no plans for a life after work) has the time to research thoroughly. And, that’s just for Colorado. Because these Advantage Plans are tied to a locality, only certain health care providers are available. I must be sure that any specialists I might need in the future are on that list of providers. I blow on my crystal ball to warm it up. Medicare sends my monthly premium to the the for-profit company. If I want ‘extra’ coverage, I can pay an additional monthly fee directly to the for-profit corporation. How much extra coverage and what does it actually cover and exclude? Goddess knows!

So, for 2017 I decide to stick with Traditional Medicare, which gives me access to all doctors in the U.S., if they will take Medicare patients, that is. I then have the option to buy a Medicare Supplemental, from a for-profit insurance company. I have not yet had the courage, or the time, to research available Supplemental Plans. But a friend, who is in much the same situation as I am, tells me she is paying $300 per month for Supplemental coverage through Anthem BC/BS.

Still no dental or eye exam coverage. Like teeth and eyes are not a part of one’s body.

So, from my frantic scrabblings through the Medicare morass the last month, my conclusion: Medicare has been already been ‘crapified.’ The for-profit companies have a stranglehold on the system and impose, as Lambert has pointed out, immeasurable costs on seniors in the form of time and uncertainty.

So, yeah, on second thought, I just don’t have time to riot. Gotta spend the next month reading through all the fine print on the available Medicare Supplemental Plans.

Well, this old person is down for a riot. I signed up for Medicare Part B in October, having lived in the warm and fuzzy cocoon of a platinum employer-provided health plan for the last ten years since I turned 65. (My husband finally retired.) Here’s what I learned.

The Medicare market has been captured by for-profit health ‘insurance’ corporations.

I signed up for Traditional Medicare for the remainder of 2016, at a monthly premium, which has been adjusted upwards from the base amount of because our 2014 income was on the high side, from $105 to $170. (I don’t have a problem with that; those who can afford to pay more, should.)

This monthly payment is automatically deducted from my social security benefit.

Next, Medicare Plans A and B do NOT cover the cost of prescription drugs. I take only one, very cheap generic for mild hypertension, which would cost only a few dollars per month. BUT, if I do not enroll in a Plan D prescription program within 60 days after enrolling in Medicare Part B, the system imposes a financial penalty on me. So, turns out all these drug plans are administered by for-profit insurance companies. I look for a plan with the least expensive monthly premium … which comes out to $18 … and enroll. (I will not torment you with the tales of my hours spent on the phone with this for-profit company when they decided my on-line enrollment through the government medicare site, which was quick and easy, BTW, was not valid.) Goddess help me if I then need a prescription drug which is not on that plan’s formulary. My crystal ball has been a bit foggy these days. They finally accept my application and send me a bill. Yea!

But, for 2017 I face a bewildering array of choices. I can stick with the Traditional Medicare, and face possible rejection from health care providers who object to not being paid for months. Or, I can chose from a bewildering variety of Medicare Advantage Plans, sold by for-profit companies. Literally, hundreds of options that only a retired person (with no plans for a life after work) has the time to research thoroughly. And, that’s just for Colorado. Because these Advantage Plans are tied to a locality, only certain health care providers are available. I must be sure that any specialists I might need in the future are on that list of providers. I blow on my crystal ball to warm it up. Medicare sends my monthly premium to the the for-profit company. If I want ‘extra’ coverage, I can pay an additional monthly fee directly to the for-profit corporation. How much extra coverage and what does it actually cover and exclude? Goddess knows!

So, for 2017 I decide to stick with Traditional Medicare, which gives me access to all doctors in the U.S., if they will take Medicare patients, that is. I then have the option to buy a Medicare Supplemental, from a for-profit insurance company. I have not yet had the courage, or the time, to research available Supplemental Plans. But a friend, who is in much the same situation as I am, tells me she is paying $300 per month for Supplemental coverage through Anthem BC/BS.

Still no dental or eye exam coverage. Like teeth and eyes are not a part of one’s body.

So, from my frantic scrabblings through the Medicare morass the last month, my conclusion: Medicare has been already been ‘crapified.’ The for-profit companies have a stranglehold on the system and impose, as Lambert has pointed out, immeasurable costs on seniors in the form of time and uncertainty.

So, yeah, on second thought, I just don’t have time to riot. Gotta spend the next month reading through all the fine print on the available Medicare Supplemental Plans.

Whoops, sorry for the double post. The later one has been edited, slightly. Put it down to suppressed rage that is the result of dealing with multiple for profit insurance companies.

Éclair:

Why are you whining??? Your income is > than 90% of the people still working and exceeds $170,000 annually as a retired person. Some people will not see $170,000 during the time when they retire till the time they are dead. You are crying while running to the bank with two loaves of bread under each arm (not just one).

Just to make this clear, I am on Medicare. Most doctors and hospitals accept Medicare as it is one of the biggest games in town. Say not to Medicare, and you restrict yourself t the wealthy and they are a fussy clientele. Since you are an old f*rt like me, things get worst so not enrolling in Part D will cost you money at 1% increments per year forever.

You are ridiculous as people on the PPACA would love to pay what you pay for Medicare. $170 per month for Part B plus supplemetal at another amount exceeding $110/month and the ~$20/month for Part D for one person? I would shut up and pay it. You, you have nothing to complain about. Geez . . .

Wouldn’t be to sure about that, some of us are children of the 60’s.

Twas ever thus.

“Markets first plan”?

Isn’t Obamacare a testament to the fact that market approaches – especially those rigged in the direction of healthcare companies – don’t work?

Isn’t that the most parsimonious analysis?

Did I say that health care markets worked, or weren’t rigged?

It doesn’t matter if they work. It matters if they continue to shovel money into the bloated gullets of giant health care corporations.

It’s like asking why our Middle East policy doesn’t work.

It doesn’t have to work for you or me. It only has to work for the people who actually matter.

“Americans Will Always Do the Right Thing — After Exhausting All the Alternatives”

So here comes the next alternative. I wish I could buy futures in socialized health care. Like I said somewhere a long time ago, once we finally do go to it, it will be so expansive it will embarrass the French. Sad about everybody who will get screwed in the meantime.

The college tuition problem is also pretty awful, but at least it’s a burden carried mostly on the shoulders of healthy and young people. I can’t imagine sitting in a hospital, being able to do nothing but think about the unpayable bills piling up and wonder how long that may continue. Wondering if it would be better or worse to die, as that would leave my loved ones with a known* burden, or keep racking it up and hope I can rise out of bed and somehow work it off?

*actually not really known, since is is f’ing impossible to figure out your medical costs for months after the incident is behind you, let alone in real-time.

Not sure a federal law is needed for selling insurance across state lines.

And selling insurance across state lines has already been tried:

http://wendellpotter.com/2012/10/romneys-phony-answers-to-tough-health-care-questions/

In fact, as Hiltzik points out, interstate compacts are permitted under ObamaCare. And that hasn’t worked either. It’s snake oil.

Yes. This is what Trump’s supporters didn’t realize. Most of what Trump is suggesting now has already been tried and failed.

Ooopsie. But someone today at my Dentist’s office was snarling that, as much he disliked Trump, at least he wasn’t a socialist and would not “inflict” socialist health care on us.

Okay then. Ya got yer wish. Hope yer happy with that.

re: “If selling insurance across state lines is TrumpCare’s policy nostrum, TrumpCare will fail as badly as ObamaCare”

yes. on point.

Actually, I think we’ve discovered a real, concrete difference between the parties, here.

Democrats: Let’s try something that will almost definitely fail (Dodd-Frank, HAMP/mortgage mods, Obamacare)

Republicans: No, let’s try something that has already been a PROVEN failure (trickle-down tax cuts, Trumpcare)

Republicans: No, let’s try something that has already been a proven disaster for the country while massively benefiting the only people who count — us and our cronies.

And they’ll continue to “fail” over and over again, because their definition of success is very much narrower than yours and mine.

“while massively benefiting the only people who count — us and our cronies.”

Like JohnnyGL said, we’re looking for differences, not commonalities.

‘states already have full authority to decide whether or not to allow sales across state lines’

Of course they do. But that means an insurance company based in one state has to apply to 49 other state insurance commissioners to sell coverage nationwide.

Attempting to federally pre-empt state insurance commissioners’ turf will provoke a revolt, even though Republicans control more states than Democrats.

And you certainly wouldn’t expect to get good people to work on stuff like that for a piddly 49 million/yr.

… the stuff I was referring to is working with a whopping 49 new state insurance commissioners if that wasn’t clear… interestingly that Jim’s mind first went to pre-empting them with the feds, that does sound more like the path the “small government” Rethugs would take I gotta admit…

So much for states’ rights. As someone in a state with an elected insurance commissioner, I certainly don’t want the feds swooping in and making his job obsolete.

Both Republicans and Democrats only care about states’ rights when it suits them.

No exit-polling data for Obamacare / Exchange “consumers”? Why am I not surprised.

Shouldn’t we now be able to phrase the question as:

Do we want Medicare to be more like Obamacare (private for-profit insurance; varying subsidies/vouchers; increasing high out-of-pocket costs; narrow networks; no controls on drug prices;)

or do we want Obamacare to be more like expanded and improved Medicare (public not-for-profit insurance; funded by taxes on [Wall Street, other progressive elements]; no out-of-pocket costs; everybody in/nobody out; negotiated drug prices)

Has *anyone* here looked carefully at what Medicare actually covers now? In many ways it’s more of a minefield than most ACA style plans. High deductibles, coinsurance, exclusions. Private supplemental or replacement insurance is available for those who can afford it, but those plans are also a morass. Definitely not socialized medicine on either the British or Canadian models.

Yes, that’s why the alternative to further privatization of Medicare or to Obamacare “replacement” is Expanded and Imroved Medicare for All (HR 676), not expanded access to current Medicare.

no reason to believe trump will do it this way. he will look at the problem, and figure out how to solve it. this is lefty wishful thinking. they hate that they will have to like trump.

Hey, all I can do is look at the evidence, which I did. I’m not really a fan of the logic that the “great man” (or “great woman”) is going to work everything out. After all, how did “I trust Obama” work out? If not being an authoritarian follower makes me a lefty, I plead guilty.

Regarding selling across state lines: I’m pretty sure insurance companies could do this now if they wanted to meet the individual requirements of the states as to incorporation and minimum policy requirements. One of the few decent things Obamacare provides is that regardless of which state you are located in, if a policy is sold on the Exchange, you know that it must contain certain coverage, depending on the plan level.

Regarding competition: See Aetna (trying to purchase every competing insurer). See also all the bankrupt Exchange co-ops. If anything, we are seeing less competition. Unless Trump wants to become a trust-buster, competition is a non-starter.

Other issues to consider if Obamacare goes the way of the Dodo bird: women being charged more for policies, no contraception coverage, individuals over 50 being charged sky high premiums.

The GOP/Mercatus take on this is that

Concentration in an Industry Does Not Mean It Lacks Competition

The inmates have truly taken over the asylum.

It turns out that the inmate’s research is G**gle-supported.

Don’t be evil until it’s strictly necessary.

Sex has been considered an accepted underwriting input in other insurance markets. Not sure why it should seem an outrage in this one, but a simple remedy would be to ban the practice for all types of insurance. Hard to argue against the data that says that women file lower collision claims in the auto market but equally hard to look at the data and not conclude that being a woman costs more in healthcare claims. To me it seems like the compromise here is to just disallow the practice entirely.

Maybe because auto collisions typically don’t drive people into bankruptcy but health conditions can and frequently do. The cost is different by an order of magnitude.

Medicare and Medicaid don’t charge women more. Why should we allow private health insurers to profit off someone based on what sex they were born into? Should we also let them charge more to Latinos or the poor, because their health outcomes are worse and their care costs more?

Health insurance should have greater scrutiny and less tolerance for discrimination.

Good reply, better if we all just start refusing to use the word “insurance”. Insurance is for backstopping against the unexpected. We want Health Care Coverage and then nobody has to make excuses – unbelievably enough – for pregnant women.

Yes!

Public health is a public good that should be publicly provided: there is no sane reason middle men need to be empowered to profit from provision of public health.

That they should is pure ideology.

Hmm… agreeing on the misuse/abuse of the term “insurance”, I don’t want “coverage” either, beyond catastrophic insurance coverage.

http://www.kevinmd.com/blog/2016/11/youre-obeying-law-youre-contributing-ceos-astronomical-salaries.html

I want access, and the economic means to afford treatment. Oh and more consistent quality would be nice too.

The problem with “coverage”, as I see it, is that there is still a middle layer. That layer inevitably wants/gets to decide on suitability of treatments, etc. which may not fit my needs or decisions. For example, to get treatment B you must accept treatment A, and treatment C is not covered at all.

Like welfare, which should be a safety net for unusual distress, but has been distorted to be a permanent supplement replacing fair wages, the current concept of insurance as a payment model for coverage is a distortion of the insurance model (hedge against unlikely events, not against certain events). That distortion takes us further away from a discussion of how health and health care actually work.

I’m not trying to engage that final discussion right now either, just want to point out it’s not a one size fits all scenario. I’ve gone without health insurance for ~50 years, so this is not abstract to me.

Great point about Medicare not differentiating between men and women in terms of rates. As to ethnic minorities, that’s just redlining, and should be as illegal in insurance as it is in mortgage lending.

And lifetime caps on benefits, which no one ever mentions.

What difference does it make what happens with Trumpcare? Paul Ryan has made it explicit that he (and presumably his GOP led government in lockstep) wants to dismantle Medicare and Medicaid and will probably start right in on this Day 1. Pretty much no matter what Trump says or “thinks”.

So in the end, we’ll be right back where we started, only much, much worse: no Medicare to buy into (esp for people in my 45-55 age group! Thanks, Trump Voters!), a bunch of ridiculous private insurance plans that cost whatever they want to charge, and tens of millions left with nothing as their GOP Governers take the Medicaid block grant money and spend it on private prisons or whatever they desire.

This is where Trump can use the “Bully Pulpit,” wield the veto pen, and do a United Front with both “Moderate Republicans” and “Progressive Democrats.” Paul Ryan has always exuded the miasmic stench of a superiority complex. I’ll admit that how he handles Ryan will tell us a lot about the character of Trump. I’m crossing my fingers and toes and hoping for “Mr. Big Shot” to make an appearance and slap Ryan down just like he manhandled Pence.

I wish I were more optimistic, but Trump’s performance over the past year and a half doesn’t lead me to believe that he cares about anything but himself – certainly not “policy”. If Ryan can suck up to him enough, (and he appears to be very good at this), T will agree to whatever is put in front of him. He is woefully unprepared for the task at hand, (didn’t even appear to have a transition plan in place) so the politicos on the inside will be happy to fill in the blanks.

And I have zero hope that Trump’s supporters or voters will get out there and insist that he fulfill his promises. (Too much work.) They couldn’t have cared less when Bush let them down until eight years in. This will be the same.

yeah i’m sure if he passes TPP they’ll (trump supporters) all just go along with it because they’re such morans. re ryan you make trump sound like play doh, wonder what pence and christie think about that. If all he cares about is himself he will want to leave an imprint through policy. That too much work comment makes you sound pretty meritocratic. I’ve got a rock you can carry if you can get up from your ergonomic chair. Obama let his supporters down, what did they do? Sent hillary packing, that’s what

The point being that the Republicans will finally be held accountable for their idiocy in service to their pay masters. When so called progressives enact regressive Republican policies to please their paymasters, progressives take the blame, hence the election results 2010 and currently. Please let the Republicans privatize and gut Medicare before the 2018 midterms, the sooner the better. Progressives should stand back and let them do their worst and when the typical Trump voter yells, “Don’t let the gumment touch my Medicare” the progressives should let them know precisely who that government is being run by. A key political strategy mastered by the Republicans and dismally ignored by progressives is timing your backlashes. For instance the Republican practice of deficit spending to juice the economy with massive deficits and then taking credit for the booming economy, “…see trickle down works”; and when the Democrats take power blaming them for the deficits and promoting a rigorous policy of cutting government spending and then blaming the Democrats for the poor economy, “see what over regulation does”. Moral rectitude is not always enough, there needs to be strategy and proper accountability.

The problem with progressives allowing Medicare or Medicaid to be gutted is that there are millions of people whose lives depend on medicine. If a person is healthy, I can see why some people want Republicans to screw up so badly that progressives could take the reigns in 2018. The problem with that thinking is progressives need to fight right now to not lose health insurance due to the catastrophic consequences of being ill. Fight for the sick now while working towards “Medicare for all” or something similar.

The Democrats need to get a spine and start using all the dirty tricks Republicans use. We have the most obstructionist congress in American history which hinders any progress at all. Democrats were even blamed for government being dysfunctional. Start fighting fire with fire since it turns out that voters cheer their party blocking any progress. Democrats need to quit being beholden to big money, and it looks like that is already changing with the shakeup of Democratic leadership. Progressives will be the new Democratic party with Sanders, Warren, etc. leading the charge.

Trump has at various times in past years praised single-payer health care. So — who knows? From Independent Journal Review earlier this year:

“In 2000, Trump wrote a book called The America We Deserve, in which he praised universal healthcare systems:

“We must have universal healthcare…I’m a conservative on most issues but a liberal on this one. We should not hear so many stories of families ruined by healthcare expenses…

Doctors might be paid less than they are now, as is the case in Canada, but they would be able to treat more patients because of the reduction in their paperwork..

The Canadian plan also helps Canadians live longer and healthier than Americans. There are fewer medical lawsuits, less loss of labor to sickness, and lower costs to companies paying for the medical care of their employees. If the program were in place in Massachusetts in 1999 it would have reduced administrative costs by $2.5 million. We need, as a nation, to reexamine the single-payer plan, as many individual states are doing.”

http://ijr.com/2016/02/537107-5-times-donald-trump-praised-socialized-healthcare/

Since no less than two of Trump’s biographers came out publicly during the election to say that he barely even participated in the writing of his biographies as far as the actual writing goes, I will be astounded if this statement actually came from T himself. Even more astounded if he has anything even in this zip code as President, since he will be surrounded by the GOP.

No he actually said that financially the better option was a Canadian style healthcare, then later he started state border thing. This was early on in primaries.

Well just give up, then, you know? Quit. Tune in, turn on, drop out. Why not, it’s obviously all gone to sh*t permanently.

Lordy.

You misunderstand completely. But I think hoping for purchase via Trumps potential reasonable ness is a fool’s errand. I hope to be proven wrong.

I noticed the other day when I looked at my travel insurance policy document it had introduced a new clause specifically for the USA:

In other words, the costs of hospital care in the US is so exorbitant and, when purchased at rack rate, so outrageously profiteering that any sane insurer outside the US simply refuses cover it apart from Medicare+a little bit. I wonder how many tourists who are unfortunately admitted to a US hospital, don’t realize they’ve ended up in some gangster-like HMO place and get a nasty shock when they end up having to foot the bill for The Mother of All Co-Pays.

Suffice to say, only the US is subject to this policy exemption. Power of choice and competition, my arse.

Interesting follow up question would be: What travel insurance premium would one have to pay to get around this clause ? Assuming the the insurance outfit will even allow you to do it. That would give a real measure of how bad non-US insurance companies think US healthcare gouging actually is.

Maybe a question for one of the LLoyds `we’ll insure anything at a price’ syndicates … anyone on NC know a LLoyds broker/underwriter ?

I’ve checked and it’s an uninsurable risk for a retail customer. Known in the trade as “wide of scheme” — it needs bespoke underwriting. No off-the-shelf reinsurance will touch it. Of course everything can be fixed (or bought) for a price but it shows you how bad US healthcare costs are out of control.

Out of control costs will not be addressed by keeping insurance companies in the drivers seat, presiding over an opaque medical pricing system which enjoys de facto antitrust immunity for its flagrant price discrimination and anticompetitive behaviour by hospitals.

Since health care providers compensate for Medicare’s relatively low reimbursements by charging higher rates to private payers, a piecemeal, private sector-only solution cannot control costs.

Linking health coverage to employment — an accidental legacy of WW II, when employers facing a wartime wage freeze expanded fringe benefits instead — is another lousy policy that’s deeply entrenched.

Only a total rethink will do. But no such breakthrough is on tap, to serve as an overnight miracle in the first 100 days.

You’d think that after repealing Obamacare 45 times or so in the past six years, the R party leadership would have a Plan B in the top drawer. Sadly, they aren’t paid to think. Their job is to swing from tree to tree, to keep onlookers entertained.

> Plan B in the top drawer

Leszewski points out, I think correctly, that Ryan’s material is equivalent to whatever Obama or Bill Clinton had in the top drawer when they were elected, and I link to a summary of the main points of eight pieces of Republican legislation throught 2015 that seek to replace ObamaCare. It isn’t that isn’t a Plan B, it’s that there are too many Plan Bs. Do consider reading the post.

Now, that doesn’t mean that the Republican plans are any good. But there are plans.

“Since health care providers compensate for Medicare’s relatively low reimbursements by charging higher rates to private payers”

This is complete “heathcare provider” BS.

Most “heathcare providers”, especially at the specilast level, are doing up to and over 50% of their biz with medicare.

If it’s so bad, why are they doing it?

Now, point out some family practice doctor who got rid of medicare. They’re like black swans, the press loves the story, but they can only find a few.

Why is that Jim? What business, pardon, “heathcare provider”, would willingly cut 50% off the top line?

Yes, and maybe that bears some more specific examination, where does all the money go?

– actual cost of treatment/medication

– provider markup (if anyone is entitled to some slice of markup, it’s the direct provider)

– insurer markup (mostly through coverage premiums, also through deductible and co-payment)

– payment processor fees

– product manufacturer markup over cost (entitled to some but we see this going off the rails too)

Note that the payment processor is not the insurance company. This largely hidden layer of the cake is not often discussed, but they take a pretty big bite. Payment processors also produce much of the software used by providers and insurers, and it ain’t free (anymore).

I am not a researcher of this, I’ve just been sick, and also done some work (software, data) in the medical billing and payment processing fields. If insurers are a blood-sucking leech on the necks of

patientsconsumers and providers, then payment processors and an even bigger leech on the necks of all three.I don’t know about travel insurance, but in 2012-2013 I lived in Singapore and investigated health insurance. Most plans aimed at expats were global ex-US, global+US plans cost about twice as much.

A virtually intractable problem, because (1), the inherent, baked-in failure of (solely) profit-based healthcare (zero cost-containing incentives and perverse coverage flaws) , and (2), so obvious a solution, the single-payer approach, is eternally damned because of crackpot ideology. How anyone at this late juncture can even postulate a Trump do-over based upon identical “private” i.e., neoliberal premises could even begin to “fix” ACA is smoking stuff I would pay my next SS check to score! The consequences of what we all expect will happen are continued marginal healthcare delivery at ever-increasing costs, and more people opting out of the system, leaving themselves prey to medical catastrophes. Even employer-based healthcare schemes are inexorably pushing costs onto employees, and the more dependents an employee claims, the sharper the self-borne costs rise. Having been in a decent health plan most of my working life, at a reasonable cost to me – all of this pre-2000 – I am truly stunned at the headlong degradation of so-called pay-to-play healthcare, and the fumbling attempts at establishing a national, equitable policy.

IMHO, the basic issue is and always has been: is decent, reliable healthcare a “right” or a “privilege”? Until our political masters buy into the notion that healthcare is indeed a fundamental right for all residents of the US, what you see is what you get, for years out, I’m afraid.

“If I am sanguine on this point, it is because of a conviction that men and nations do behave wisely once they have exhausted all other alternatives.”

Abba Eban

Wow.

Toning down war with Russia whilst actually not arming training al Qaeda…. maybe even helping ol Russia whack ’em.

Possibly eliminating the Obamney mandate.

If they include in their infrastructure establishing fiber internet to all us wayward rural citizens in flyover country.

Trifecta… the poor decent populist isolationist mans ten bagger. And Trumppublicans could reign for a decade.

Wonder if those slim DT/HRC margins were smaller than the numbers of citizens who remain in Section D or paid the penalty on Obamney, not care?

If Trump’s dumb enough to hitch his wagon to Paul Ryan, he’s going to get what he deserves.

My guess is that he takes a look at whatever legislation comes out of Ryan’s staff (written by lobbyists) or gets picked up off the shelf (written by lobbyists awhile back) and realizes it’s an albatross that will sink his presidency, and scuttles it, or even actively opposes it with a veto threat. Trump clearly doesn’t understand health care policy, but he’s got good political instincts and he will probably realize there’s no good answer on this one.

Yet another reason why the Bernie-crats need to get a hold of the levers of power in the Democratic Party. They’ve got to be ready for when Trump and the Repubs flop. It’s probably going to come pretty quickly.

I expect single-payer to find its way back into the Overton Window because there is NO other option left. The public won’t support the subsidies necessary to persuade Aetna and Cigna back into the marketplace and get it to function sustainably.

My prediction goes like this:

Scene in the Oval Office, late spring 2017.

By all accounts, Donald Trump is ill-prepared for the presidency and is unable to handle the responsibilities that come with the job. The Washington Post has been editorializing in favor of his resignation. As have The New York Times and the major TV networks.

So, a meeting is convened in the Oval.

The meeting is brought to order by former President George W. Bush. He gets right to the point:

“Donald, I’m gonna make this simple and easy as possible.

“Y’know, I tried to tell you about all the complexity that goes with this thing. Hell, it took me a long time to get up to speed. And you were reading the news just like I was. Quite a few people think that I never got up to speed.”

Paul Ryan suppresses a smirk and Bush shoots him a dirty look. Bush continues:

“Donald, it’s becoming pretty obvious that you aren’t cut out for the presidency.”

Trump squirms in the President’s leather chair by the fireplace.

Ryan, Carson, Cruz, Priebus, Gingrich, McConnell, and Rubio, who’ve been sitting on the couches on either side of the President, glance at each other. Cruz silently wonders if Trump is about to burst into tears. Pence stares straight ahead.

Bush, who is seated to the left of Trump, continues:

“Donald, it’s time. For the good of the country, it’s time to resign.”

Trump suddenly takes an enormous interest in the pattern of the Oval Office carpet. Bush notices a tear rolling down Trump’s left cheek.

“Yeah, okay,” Trump says.

Pence continues staring straight ahead.

I don’t agree. For one thing, Pence is terrific impeachment insurance. The Republicans do not want to put evangelicals again in a position of power. That was a big part of the mess they got themselves in.

Second, Trump will not be pushed out short of impeachment or an equivalent scandal (blue state major indictment on state-level matters that would produce an uncontainable furor that would make it hard for him to govern). He might make up a loony-tunes excuse on his own to quit if he gets sick of being President, but that’s a completely different scenario. The guy loves to fight. He took on the entire Republican party and then the Democrats, against one current and three former Presidents, the entire media and credentialed classes, all pounding him for months. He took quite a lot of pain to get where he is and he has an ego like the outdoors. He’s not quitting easily and sure as hell not in a mere quarter.

If the establishment wants him out fast, it’s going to be via an assassination, not a nice chat.

In my opinion, medical care and insurance are like oil and water. They will never mix well together. If your home insurer knew that the odds were that your home would have a major catastrophe, do you think it would even be interested in pursuing the business? They might, if they could charge enough to insure that the business would be profitable. We need to take a different approach to medical care entirely.

The rest of the developed world has made it work so far at a fraction of our cost. The key is that they view universal health care as not only a right, but is also the cost saving key by bringing everybody into the fold, spreading the costs out across the entire population, and making sure that the people get reasonable healthcare to prevent more major costs down the road.

Insurance doesn’t work if it is only focused on covering people who have already had a disaster. It is why I don’t support much federal aid for people who live in floodplains. In many cases, people elected to have no or inadequate flood coverage because it is “unaffordable” but then I am expected to help pick up their tab after a predictable flood event occurs. We already provide some subsidies for the FEMA flood insurance, but they want the whole cost defrayed. That is not how insurance works.

With respect to the “what the future holds” bullet points, the author omitted the 4th leg of the stool: malpractice reform, aka, caps on jury awards.

… which is yet another thing single-payer would render obsolete.

Single-payer systems do not automatically change tort law statutes. The providers are still liable for malpractice. However, many of those countries do have mechanisms for limiting tort awards, but they also usually have much stronger consumer protection regulations overall which reduces the need for tort suits.

Complete BS talking point, which also takes away the few rights you may have left.

It’s not capping the jury. It’s capping you, you fucking moron.

A beloved neo-conservative talking point, but is only a small percentage of the excess costs.

Surely the problem with the US is population growth: less than 100 million Americans in 1946, 200 million in 1976, now in 2016 well over 300 million of you. That many cannot live the rich lives previous US citizens enjoyed.

That’s a fallacious argument, given that US profit share is at an unheard of level of GDP. The US does not have a shortage of land, agricultural produce (the US remains a huge exporter) or raw materials. We have rentier capitalism which steers wealth into the hands of the few and encourages investment in unproductive sectors, like our outsized financial services industry.

Malthus made those arguments a couple of centuries ago. He was wrong.

MIT published “The Limits to Growth” almost 50 years ago on the same theme. They have been wrong so far.

Never underestimate what human ingenuity can accomplish. That doesn’t mean there aren’t serious problems, but they can be resolved if we want to.

I am still baffled about how an administration and Congress run by people who continuously spout off against the intrusion of the federal government in areas that are the states’ prerogative propose to remove the state insurance regulators from the equation. Insurance is one of the areas that has been most clearly regulated by the states over the past century. The ACA simply said that the states could work together, kind of like having free trade agreements for insurance between states but it didn’t over-ride state regulation of insurance.

On the economic side, two of the most powerful state insurance regulators are California and New York State. These states have a lot of people with high median incomes, and will be primary targets for the insurance industry. Its going to be very tough for insurance carriers to sell insurance from many other states in those two states unless Trump and Ryan take the state insurance regulators out of the equation.

In a market, you shop for what you want.

You get band-aids, but just because you bought some does not automatically mean that I also got a box.

But if I get influenza, you might get it as well.

Illness — particularly communicable diseases — do not belong in a market paradigm.

They are fundamentally ill-suited to the idea that people have ‘choice’ or can ‘select among options’.

They’ll cut the CDC too.

They’re like a death cult.

Strange effect of knocking down state borders: localized diseases like Lyme will now be that much harder to chase down because of insurance billing and the administrative nightmare when you get a disease that doesn’t exist on the other coast.

Your work on healthcare is always awesome, Lambert, thanks for this great read.

Neither party have proposed any serious concepts on how to tackle the big nut that needs to be cracked in US healthcare, namely that it cost roughly twice as much per capita as any other developed country, despite most of the countries having near-universal coverage, including the poor who have health problems and should be driving costs higher. The high costs constrain policy decisions. Instead of focusing on ideological approaches, there needs to be a real focus on executing continuous improvement to get cost-effectiveness. The rest of the world has shown us benchmarks of where we can reasonably get to.

Instead, we just keep getting different Rube Goldberg machines that don’t significantly change the endpoint. The concept that “consumerism” is driving costs down is laughable. All you have to do is look at the randomness of doctor and hospital bills that make cell phone bills a model of clarity.

Ultimately, one of the big things that the single payer systems are using to control costs is the access to population-wide big data on medical histories and outcomes that are used to tailor and optimize policies and procedures. Since many countries (like Canada) have had people in single-payer system for decades now, they are really starting to understand what works and what doesn’t work. US health insurers have almost random population groups that are constantly switching carriers (job changes, employers bidding out insurance to get lower pricing, etc.) , so it is tough for them to track what is effective care.

Visual Capitalist – US healthcare system a global outlier and not in a good way

All the insurance companies wanted out of the ACA was the mandate. Dumb suckers in this country!!!!

They’ll offer insurance to those with pre-existing conditions, but it won’t be affordable…for anybody.

We should all welcome Ryan and Trump’s plan to expunge Medicare and Medicaid. There are two major obstacles to Single Payer in this country and they are the employer subsidized health plans and Medicare/Medicaid. Note that it mentions somewhere in the article that 60% of the population is covered by employer subsidized healthcare. If we are to have any chance of getting to critical mass of support for Single Payer then we should abolish these special subsidies for large sections of the population. It is only when everyone is truly in the ‘Free’ market that they will realize how crappy it is and start demanding Single Payer.

oh boy another the worse the better, bring on the revolution, heightening the contradictions argument. While I’m not a fan of specialized benefits, this has a great chance of just leaving everyone worse off. You can demand whatever you want, but have you noticed there are many ways they don’t listen to demands.

There are many ways we haven’t tried to tell them lately, too.

Nice show of solidarity with the oligarchs, btw.

Shorter version:

If we destroy everything, a magic pony will appear to save us.

How can you argue with that? It’s common knowledge. Worse leads to better.

yin and yang bro.

Just like economics. The is always a mean reversion.

Except, it almost never happens.

And what happens to the people that are currently sick? I am guessing you are relatively healthy to make a statement like that. I get that you want a single-payer system, but we should try to get there using the smoothest path possible. I am not a fan of fire and brimstone, but I am chronically ill so I have a different viewpoint than you. Please fight for the sick and ill while spreading a better way through single-payer, multi-payer, “Medicare for all,” etc.

If you want to fix the problem it’s simple since the government wants to interfere you give each American a 50k deductible and take away the ability to claim bankruptcy on medical underneath. A company can buy a plan to cover it’s employee’s for 50k each or self fund an individual can do the same.

The savings on the company side will increase taxes becaus a 2k premium per mont tax free will be replaced by a 200 premium tax free because they will have lower costs because of huge competition.

What do we know at Claimlinx only wrote two books and save people millions. Check us out at http://www.claimlinx.com.

Firstly, I am an old and retired general pediatrician (a dying breed), and as a retired Kaiser-Pemanente

physician, get free healthcare for the rest of my life, along with my wife. I have no skin in this game, but

I know what’s best overall. Secondly, Medicare apparently works well and efficiently. Don’t ever allow

its removal. Making healthcare Medicare For All, single payer is the best solution I can imagine, and I

lived in Germany for six years long ago, and admired their medical care system. It was better and less

expensive than what we have in the US. Healthcare Insurance CEO’s with their lobbyists and vulnerable

professional politicians are the last people in the world to deal with a problem well beyond their ability

and background. QED

“How does that work?”

There’s a 1-year cycle anyway. The government can’t reverse contracts that were legal when made, and a policy is a contract, so any changes wouldn’t affect policies issued this year until a year out.

(Haven’t read the comments yet, so this may be redundant.)

A consideration, FWIW:

Trump favored single-payer before he ran for the Republican nomination, and continued to say things advocating universal coverage for some time after. This reflects his business interests: he has a LOT of employees, mostly hotel help.

Granted, that would be impossible to get through Congress, but popular to advocate. OTOH, at this stage he’s coming across a fairly standard conservative Republican.

From a deep strategy view, Obamacare was not a well-intentioned mishap, but a devastatingly effective parasite that will not stop until it has hollowed out and destroyed the entirety of the New Deal/Great Society.

I’m in my 50’s and I don’t see any reason to hope that anything will be left for me.

You thank Obama for that and the Democrats for that, not Trump and the Evil Republicans.

FFS, Democrats are supposed the opposing Republican policy – not implementing it.

Once Obamacare/Romnneycare was rammed down our throats it was inevitable what was coming next.

Trump is mob.

Insurance is dominated by the mob.

It ain’t going anywhere. Only the price floor was set, and that’s already taken off running. Next, and ongoing, less and less and less benefit.

Expect legislation that will limit the benefits that can be collected by those losers.

IMO, parsing Trump’s words is futile. He says what needs to be said to get what he wants. He understands how to use the media.

He is a case of only look at what he’s done and what he is doing. Forget the words.

My take on this for now is that we of the 80%-or-so are not “collateral damage” in the

USG healthcare debacle, we are the target, and the system is working more or less as

designed: individual mandates to buy virtually worthless coverage as we die of

diseases cause by “safe” pesticides, eg Atrazine, Glyphosate, Dicamba, Naled; drinking

polluted water.. make your own list.

So our friends at the top make money off of us and our “insurance” as we conveniently, um, pass on. What’s not to like? /S