Yves here. Note how this article treats the idea that an overly large financial sector is bad for growth as widely accepted.

By Eilyn Yee Lin Chong, Graduate student; Ashoka Mody, Visiting Professor in International Economic Policy; and Francisco Varela Sandoval, Graduate student, all at the Woodrow Wilson School of Public and International Affairs, Princeton. Originally published at VoxEU

Recent research suggests a point beyond which the benefits of financial development diminish, and further development can even hurt growth. This column describes how a negative relationship between credit and growth emerged strongly after 1990 and was particularly pronounced in the Eurozone, consistent with the notion that an overgrown financial sector weakens economic growth potential. It also argues that slower growth leads to more rapid financial sector expansion. Policymakers need to be aware of the possibility that causality runs in both directions.

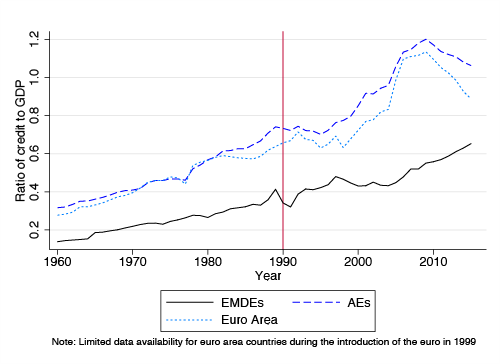

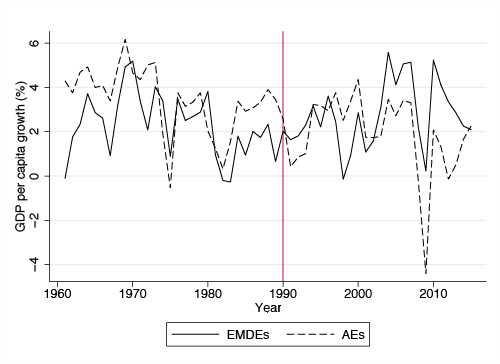

Average private credit-to-GDP – a commonly used measure of financial development – has increased steadily since 1960 (Figure 1). The credit-to-GDP ratio has been higher in advanced economies (AEs) than in emerging and developing economies (EMDEs), and the gap has increased since about 1990. Despite rapid financial sector growth in the advanced economies, GDP per capita growth remained almost unchanged (Figure 2). What role was rapid financial development playing if it did not help to raise growth in the advanced economies?

Figure 1. Average private credit-to-GDP by country group, 1960-2015

Figure 2 Average GDP per capita growth by country group, 1960-2015

Financial Development and Growth

The early empirical literature, starting with Goldsmith (1969), suggested that banks and financial markets allocate capital to the most productive endeavours; and the financial infrastructure accompanying credit reduces informational inefficiencies, such as moral hazard and adverse selection. Rajan and Zingales (1998) found that greater financial development promotes sectors that are not able to generate sufficient internal finance; Levine et al. (2000) went a step further and said that more finance increases an economy’s growth potential.

Recently, some scholars (e.g. Cecchetti and Kharroubi 2012) have told a more nuanced story. Financial development, they say, catalyses economic growth up to a point, beyond which more finance acts as a drag on growth. Several other authors have concluded that ‘too much finance’ can hurt growth (De Gregorio and Guidotti 1995, Gennaioli et al. 2012, Arcand et al. 2012, Dabla-Norris and Srivisal 2013). These authors argue that excessive finance sucks human capital away from the productive economy and, by creating macro and financial fragility, credit growth leads to bigger booms and busts, which leave countries ultimately worse off.

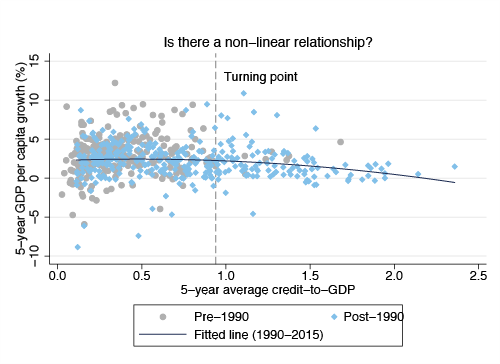

We take the Cecchetti and Kharroubi study as our starting point and ask: When and where did the adverse effect of finance on growth arise? And which way does the causality work? The simple scatter plots presented here tell the same story as the regressions they run with more control variables.

For 58 countries, from 1960 to 2015, Figure 3 plots five-year averages of credit-to-GDP and per capita GDP growth. As in Cecchetti and Kharroubi (2012), we observe some non-linearity. The turning point at which the marginal impact of finance on growth becomes negative – the so-called ‘too much finance’ effect – appears around a credit-to-GDP ratio of close to 95% (Chong and Varela Sandoval 2016).

Figure 3 Private credit-to-GDP ratio and growth

Figure 4 Private credit-to-GDP ratio and growth

Parsing the Non-Linearity

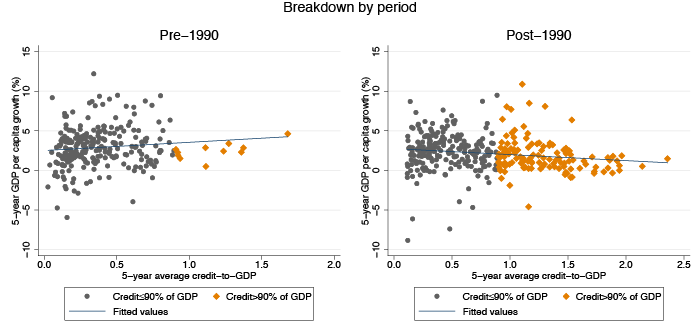

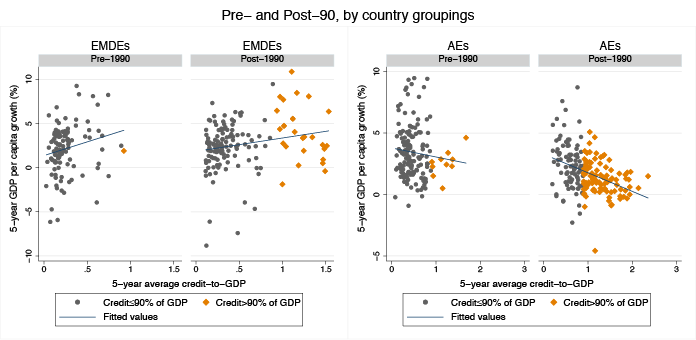

Figure 4 shows that when all countries are pooled by period, the finance-growth correlation is positive before 1990 and turns negative only after 1990. But this story hides a more complex reality. From Figure 5, we see a positive correlation between credit and growth for emerging and developing economies both before and after the 1990s; in contrast, the correlation is negative for the advanced economies even before 1990, but especially more negative after 1990. This suggests that two different sets of countries lie on either side of the non-linearity others have observed: emerging and developing economies with lower credit-to-GDP ratios benefit from more credit growth; advanced economies with higher credit-to-GDP ratios fare worse when credit increases, and this has been especially so since about 1990. But it is also the case that the negative relationship between credit and growth in the advanced economies begins even before the 90% credit-to-GDP threshold.

Figure 5 Private credit-to-GDP ratio and growth

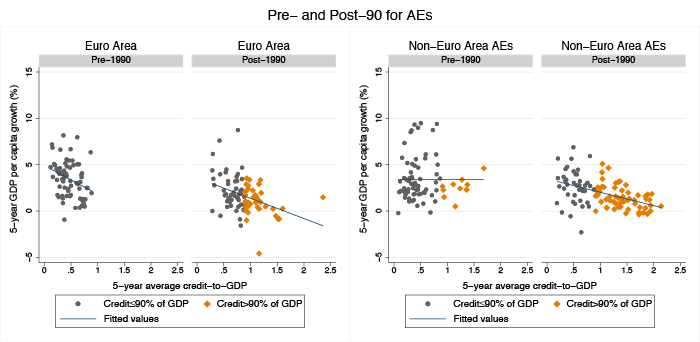

Digging deeper into the advanced economy experience, the negative correlation between financial development and growth before 1990 existed mainly in the Eurozone countries; the post-1990 negative relationship between credit and growth is somewhat steeper in the Eurozone than in other advanced economies (Figure 6). Again, the more pronounced negative relationship between credit and growth in the Eurozone is not necessarily the result of higher credit-to-GDP ratio in the Eurozone countries compared to other advanced economies.

Figure 6. Private credit-to-GDP ratio and growth

What Have We Learned?

One interpretation of the data is that beyond about 90% of GDP, additional credit is largely counterproductive. The evidence certainly supports that inference. Especially after 1990, many advanced economies exceeded the 90% of GDP credit threshold, and more credit beyond that level is associated with lower growth. Also, emerging and developing economies have credit-to-GDP ratios below 90% of GDP and in those countries, more credit has been associated with higher growth.

The data are, however, also consistent with an alternative interpretation, one in which the causality runs the other way. Emerging and developing economies start from relatively low incomes and have, on average, higher growth potential. As they grow to realise that potential, the demand for finance leads to greater financial development. This would be in line with Joan Robinson’s view that “finance follows enterprise”.

For advanced countries, especially for Eurozone countries, the data show that GDP growth has tended to decline even before the 90% threshold has been reached. This was evident in the years before 1990, when credit in Eurozone countries did not exceed 90% of GDP.

The possibility exists, therefore, that in advanced economies – and more so in Eurozone economies – growth potential has been low and even falling. The fall in growth potential has created greater demand for finance. One mechanism by which this demand could arise has been proposed by Gennaioli et al. (2014). Because savings rates do not typically fall with slower growth, accumulated savings grow faster than GDP; hence, the wealth-to-GDP ratio increases – a proposition that Piketty and Zucman (2014) have documented. But this increasing wealth-to-GDP ratio creates a demand for finance as households seek to preserve their wealth. Households use the financial system to park their savings and borrow for consumption and buying new homes. The financial system grows even as economic growth continues to decline.

The observation that the negative relationship between finance and growth is steeper for the Eurozone relative to other advanced economies lends further support for this opposite causation. The Eurozone had a sharper slowdown in productivity growth in the 1990s and its population growth has also been lower than in other advanced economies. This would imply, as Piketty and Zucman confirm, that wealth-to-GDP ratios have risen particularly fast in the Eurozone countries.

Policymakers need to be aware of the possibility that causality runs in both directions. Countries that pursue financial development – and many emerging and developing economies will certainly want to do so – need to also continue to pursue productivity-enhancing reforms. Finance could prove an illusory source of growth in the absence of real entrepreneurship. Where growth potential falls, the financial sector may continue to increase in size to play its wealth-preserving role. This is an important function, but it also creates the potential for financial instability.

Our findings also have an implication for the presumption after the start of the Great Recession that resuming credit flows was essential for economic recovery. In the Eurozone, where the recovery has lagged, efforts to create a greater supply of credit have been an important policy focus. Recapitalisation of banks, in particular, has been seen as crucial to the recovery of both the banking system and the economy. But where in the past the financial sector served a primarily wealth-preserving function, and where substantial wealth has now been destroyed, pushing more credit in the hope that this will generate growth could be counterproductive. This attempt to push more credit into the economy would be particularly harmful if growth potential is low. The risk is that zombie banks will be propped up, and the costs of cleaning them up and closing them down will only increase over time.

See original post for references

“Beyond about 90% of GDP, additional credit is largely counterproductive.”

Please don’t tell Bill Black, who would view this simple factual statement as smacking of austeritah.

A Government with fiat currency does not use credit. Can you not read, or do you have a comprehension disorder?

Bonds, TBills, are an interest bearing account. They are NOT debt.

“Bonds, TBills, are an interest bearing account.”

Yep. Income to the non-government, holders of the securities.

Functionally equivalent to a savings account…dollars are parked at a savings account at the Fed instead of a checking account at the Fed.

The only risk-free savings vehicle in existence for large sums of dollars.

Are you deliberately conflating private and public debt?

Anyway, For me, this fits in well with Prof. Steve Keen’s work.

“Are you deliberately conflating private and public debt?”

For him and his ilk, a distinction without a difference, or maybe, “private debt is OK, public debt is bad”.

On the contrary. Keen understands very well that “debt” is completely different for a currency creator (government) than for a currency user (households). His focus is on the latter for purposes of prediction. And “private debt is *not* OK” .. really … saying just the opposite doesn’t make it true.

Growth for whom? More Credit seems to work well for some.

Further, let’s ask: “growth toward what end, and at what external cost?”

Agreed.

The solution is to address the demand for credit. Again, higher taxes for the rich is the solution, provided enforcement was there to ensure tax dodging didn’t happens so that the “effective tax” of the rich was high.

With less money, they cannot speculate. That money could then be used for R&D, infrastructure, education, and other key investments. That would lead to real growth, rather than the financial sector.

Without as much demand for financial services, it would shrink, while demand for things like STEM jobs would go up. With that, there would be say, less demand for “Quants” on Wall Street and more job openings for places like Nasa.

NeoLib asshat tell: ” – need to also continue to pursue productivity-enhancing reforms.”

For investment to increase, “demand” expressed in money in a market somewhere will first need to present itself. “Productivity-enhancing reforms” have to date nearly made “demand” extinct.

“Just when I had that horse trained to eat nothing, it up and died!” I doubt the true believers in Market Theocracy can ever be reached, economic education appears to kill entire regions of the brain, I just hope they fade away before they kill the rest of us!

One can’t help but notice the first two names of the third author…hmmm.

Who? Francisco Varela, the late Chilean biologist, philosopher, and neuroscientist?

The graphed data generally looks like somebody is drawing a line through a Rorschach blot or shotgun target. The main thing I got out of the graphs was that advanced economies won’t grow faster than 2% or so above a credit/GDP ratio of 1.5. Beyond that, I failed to see anything particularly conclusive.

Less than credit/GDP of 1.0 seems to have a really big range of both high positive and negative values, possibly simply because more data points is more likely to produce “outlier” values in a typical distribution. As a result, the “good” ratio of less than 1.0 actual gives some points that are worse than above 1.5.

This appears to be a common problem in economics where data that does not appear to exhibit clear trends is massaged to come up with “clear” lessons instead of simply recognizing that it is very complex with many variables.

I’m glad someone noted this. In figure 3, the quadratic fit would be no better than a linear fit and both would be poor fits. Still, it is labeled a “turning point”. The data don’t warrant this conclusion.

If you connected all the dots in figure 4 to dots in figure 3 you’d come pretty close to a parallelogram.

Unseen patterns emerge from creative analysis.

That’s when the real analysis begins! What that means is you need a strong flat foundation for loading up people with debt. If you have a strong flat foundation, it can work. That’s called “cultural stability”. When they go broke you don’t want them to lose composure. It would be ideal if they can live with family and play video games or watch TV all day.

Reminds me of college when we had a perfeser that roundly criticized students for having flat brains. It’s clearly a 5 dimensional world – X,Y,Z,Time and Economics.

In a flat world, you would think like a cartoon – thinking off the edge of it, then, like Wiley E. Coyote, eventually realize it, and think in the Y direction. The Roadrunner, with the benefit of the Economic dimension, easily goes round and round in circles forever!

It still amazes me — just thinking about it — how close Professer Kelton came to getting her hands on the budget. Whoa. Can you imagine?

It seems like there’s still a possibility for 2020. Then every graph would be like a pinata bursting on Christmas day. hahahahah

You wonder what math to use if something like happened. It doesn’t seem like linear factor models would be enough. You’d almost need some kind of multi-dimensional harmonic analysis using Fourier series — or even something more complicated! Maybe tensors even. The more complicated the better, because the fewer people that understand, the better. It makes you look smart!

Making up a budget is easy. I do it all the time here. The problem is with spending. That’s when you discover the time domain and its corollaries “check clearing” and “credit card balance”. That screws everything up for ya.

Now, because I had mafe in colledge, I know what the answer is. Fourier Transforms – spending needs to be done in the frequency domain. Then you can write positive and negative checks and your checking account circles around zero. It’s sustainable! [that means it goes on for ever – kinda the opposite of “singularity”]

Except I can’t do that here. Ms Kelton would need to do that as Vice Congress. But as long as I get some, works for me.

Authors should have included confidence intervals.

Eyeballing is not the way though. Just stretch out the horizontal axis by using smaller unit lengths and you can have a much nicer looking eyeball fit, even though the numbers are identical.

That’s the right answer.

What Have We Learned?

. . . These authors argue that excessive finance sucks human capital away from the productive economy and, by creating macro and financial fragility, credit growth leads to bigger booms and busts, which leave countries ultimately worse off.

Finance is the unproductive economy, and the more banksters a society has, the worse off that society is. They are the wealth absorbers that suck the wealth created by the productive economy into their own pockets.

Bernie Sanders: The business of Wall Street is fraud and greed. Nothing has changed, with the Goldman Sachs banksters side by side with Trump, preparing for the grand loot, but I digress.

When one considers a “consumer” product such as a house, did the finance fuckers involved even hammer a nail? Lay a tile? Run some wire? Pour some concrete? Not ever. They weren’t part of the production, but make the most money off the transaction.

Policymakers need to be aware of the possibility that causality runs in both directions. Countries that pursue financial development – and many emerging and developing economies will certainly want to do so – need to also continue to pursue productivity-enhancing reforms. Finance could prove an illusory source of growth in the absence of real entrepreneurship. Where growth potential falls, the financial sector may continue to increase in size to play its wealth-preserving role. This is an important function, but it also creates the potential for financial instability.

This is trying to suck and blow at the same time. Pursuing productivity-enhancing reform is sabotaged by greater financial development. Emerging and developing economies ought to look at the bankster generated financial cancer running rampant in developed countries and get a clue. Don’t let it get started. Eventually banksters, a particularly stupid parasite, eats it’s host alive.

The fundamental difference between credit in the commercial banking sector (home loans, business loans, auto loans, etc.) and credit in the investment banking sector (the casino economy) can’t be ignored. That was the fundamental reason Glass-Steagall rules were implemented in the 1930s, see wikipedia:

Economic analysis of credit in the economy that treat these two sectors as indistinguishable should be discarded immediately.

It seems to me that the key variable is the transfer of wealth from the bottom tiers of wealth holders to the upper tiers. All this analysis of credit to gdp ratio, and advanced economies versus developing economies, and pre 1990 versus post 1990, all point to the the possibility that transfer of wealth is the issue. Measuring the growth of the financial sector as this article does, we see scatter plots with dots all over the place. That means that there are huge exceptions to the rules being gleaned. As an electrical engineer, I would call this a large noise to signal ratio. If we plotted all of the growth data against the axis of wealth disparity we would get smaller noise and larger signal. Then we could talk about large signal to noise ratios.

Debt can create growth when money is lent to productive business and industry; this is why banks tell us this is what they do.

80% of their lending actually goes into real estate which just inflates real estate prices and adds to the costs of mortgage payments and rents.

The bubble bursts and it all ends in tears.

Japan, UK 1989; US 2008; Spain and Ireland.

Financial speculation is easy, which is why they prefer it.

The Asian tigers, in their most stellar growth phases, limited bank money creation to lending into productive industry knowing the bankers will always engage in financial speculation in preference as it is less work.

I want to do an experiment, or find from FBO fuel sales internationally GDP PPP reality. US currency continues to be stronger and more trusted, even as reasons for that trust have been eroded since the destruction of Glass Steagall.

There are those who are trapped, in fact the majority who will need food clothing and shelter where they are, and those who can get whatever they want wherever they want.

How much does constant permanent war contribute to the US or Israel’s or Germany’s GDP PPP and substitute for civilian enterprises?

When do jet setters jets tanker fuel? When do Airlines determine the profitability of any particular routes respective of fuel prices?

What percentage of the GDP of a Nation is represented by asset capture as in the case of Greek or Puerto Rico and replicate asset capture that raised Germany’s GDP when they captured Belarus & Poland as explained in Chris Bellamy’s book Absolute War & Soviet Russia in the Second WW?

Is modern war more war by financial means, or war as a just war as a way to drive weapons sales?

Enough.

The GDP ratios of combatants Chapter 15.1 in Absolute War in Soviet Russia is worthwhile.