Confidentiality ain’t all it’s cracked up to be, at least when it gets in the way of prospecting for new business.

This is the first of two posts on a confidential document we’ve obtained and embedded at the end of this post. It shows, and not in a good way, the sort of work that so-called forensic consultants perform on behalf of clients. It also demonstrates how investigative reporters use technology to unearth sensitive information.

This case study is of FTI Consulting, a large, publicly-traded professional services firm. It also involves our friends and frequent topic of discussion on the blog, some of the California public pension funds. The other main character is Apollo, one of the largest firms in private equity, another favorite topic.

FTI provided the super-secret document, a written proposal, to the Los Angeles County Employees Retirement Association (LACERA) in response to a request for proposal to examine private equity fees and costs.1 As we will discuss in our second post, as part of its proposal, FTI provided an example of its work, a confidential, attorney-client privileged draft report prepared for another client, CalPERS.

On its face, FTI’s provision of the document to LACERA breached both FTI’s confidentiality and attorney-client privilege obligations to CalPERS. FTI attempted to legitimate breaching its confidentiality duties by heavily redacting both all references to CalPERS in the report and also all of its findings. However, the report was improperly redacted, andin a technology conjurer’s trick, we were able to remove all of the black squares on top of the text, thus exposing private equity firm information which CalPERS believes to be highly confidential.

But today we will focus on the way FTI did a disservice to yet another client, Apollo, in making its pitch to LACERA. As we’ll discuss in more detail, the pitch contains both descriptions of relevant client projects, most of which are confidential, and then a list of clients for who FTI did relevant work. A reader looking at both sections of the proposal, which are right next to each other, would be likely to connect a project discussing a serious failure in internal controls that led to $50 million of excessive compensation being paid out, to Apollo. Needless to say, Apollo would not be happy to learn it’s been made to look guilty, particularly by a firm Apollo presumably paid well

And if we have two improprieties of this magnitude in a single proposal, how much supposedly privileged information is FTI casually tossing over the wall in its efforts to get new business?

Background on Forensic Consultants

Companies in hot water regularly engage consultants and law firms to perform independent investigations when the matter has or has the potential to become a public embarrassment. As we’ve discussed, if a company really wants to come clean, it will hire a consultant because it is giving up the ability to keep the investigation attorney-client privileged and then decide what if anything it will share with employees and outside parties. One of the reasons Gene Ludwig was able to build Promontory Group into a shadow financial services regulator is that he quickly staked out the niche of doing rogue trader investigations, where boards were eager to demonstrate that they were being open about what had gone wrong.

Headquartered in Washington, FTI Consulting, is a public company with roughly 4600 employees. Firms like FTI can be engaged directly by the client, or they can be brought in as subcontractors to law firms, which means their work product would also be subject to attorney-client privilege.

How Did FTI Embarrass Its Client, Apollo?

We’ve attached the FTI proposal, which includes the supposedly redacted version of the client report. We’re also including the version of the client report with the faulty redaction removed via our parlor trick to show that it was performed for CalPERS.

The first section of the proposal answers LACERA’s questions. Question 3, starting on numbered page 6, “Describe similar consulting engagements that your firm has performed within the past five years.” Question 4, on numbered page 8, is “List institutional clients (public and private pension funds, endowments, and foundations) served by your firm relating to this type of consulting service including…Dates of consulting service”

Further keep in mind that the incentives of anyone who is responding to a request for proposal is to appear as experienced as possible, meaning to list as many engagements as possible.

What we see is that FTI is not terribly careful in letting readers of the document puzzle out for whom it did various forms of confidential work. In question 3, FTI tries to hide the identity of the clients for whom it is describing the assignments, such as “Large public pension fund” and “Privately‐owned private equity investment firm.” But in its braggadocio, it give so much detail that readers would surmise that FTI has let the cat out of the bag regarding for whom it has done what work. For instance, about “Large public pension fund,” it says, “FTI is currently retained by the manager of one of the largest pension funds in the United States…Between 2011 and 2014, FTI was engaged by the same pension fund….”

If you look at the clients named in Question 4, FTI lists CalPERS and CalSTRS, both of which are “one of the largest pension funds in the United States”. But it shows CalPERS as having “Multiple engagements from 2011-present” while CalSTRS is “October ’15-present”. So “Large public pension fund” looks like CalPERS.

FTI also appears to do a lot of outsourced accounting work in the real estate space. The only named client in the Assignments section is The Praedium Group, and FTI describes the work it has done for them in some detail. In that section, it also says it has been engaged by but has not yet started a similar relationship with “Asset Manager that is the sponsor of over $76 billion of open and closed end funds”. Since that project hasn’t started, FTI would not be able to use that firm as a referrer or include it in a list with service dates.

In the client list, in addition to CalPERS, CalSTRS, and the Praedum Group, FTI also lists Western Asset Mortgage Capital Corp and Invesco Real Estate Advisors and under “Client Mandate” says for both, “FTI acts as outsourced corporate accounting group for this externally managed mortgage REIT.” So we know what FTI has done for those named client.

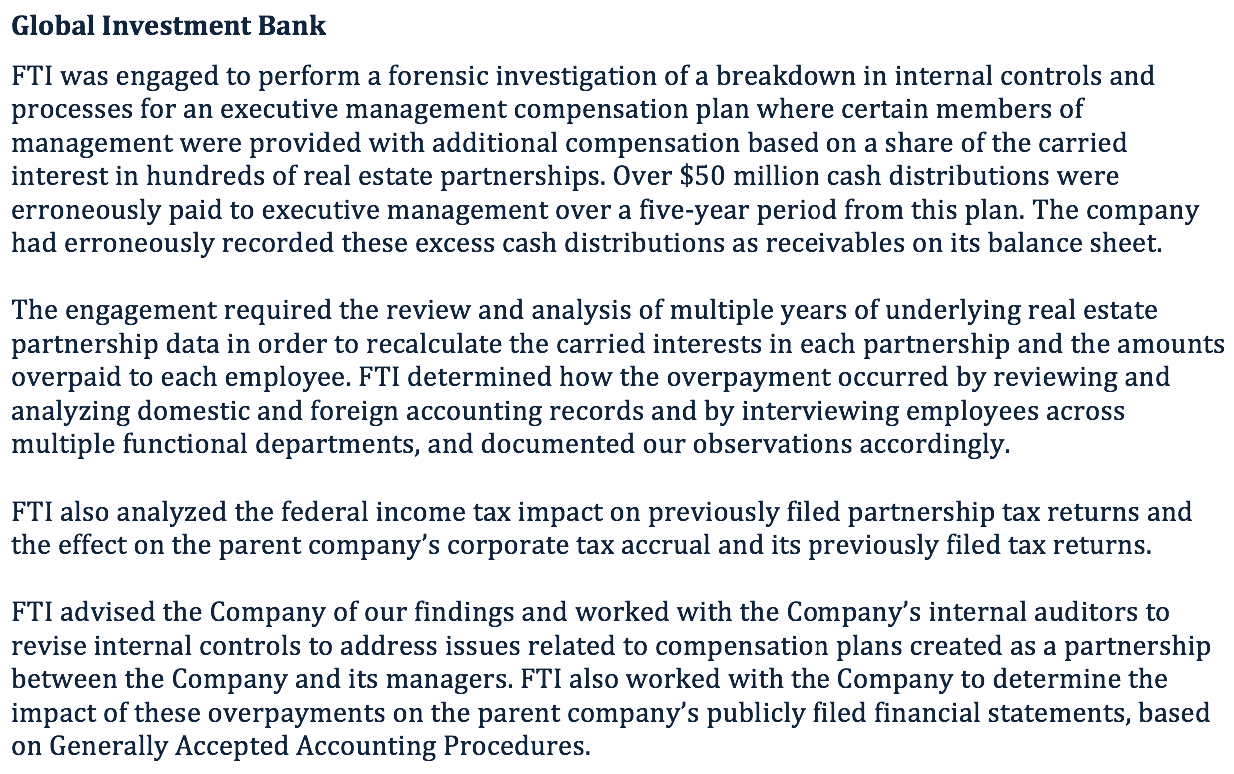

Thus we have only two remaining clients listed in response to Question 4, CalSTRS and Apollo, where the “Client Mandate” is “Confidential” where we have yet to determine if there might be a match from the assignments described in response to Question 3. There are also two matched assignments. One is for the aforementioned “Privately‐owned private equity investment firm.” That can’t be CalSTRS or Apollo, since Apollo is a public company and CalSTRS is a government pension fund. The other assignment was for “Global Investment Bank.” However, if you read the entry, the assignment was not done for a “global investment bank” but the real estate fund group (which may or may not be global) that is part of a bigger financial firm that is public. Note that under the answer to another question that is also confusingly numbered 4, on text page 10, to provide references, Apollo is listed, with the contact as Stuart Rothstein, Partner and COO of Apollo Global Real Estate Management. And when you read the dollar amounts at stake in the assignment, the project would have to have been performed for a very large fund management group.

Regardless of who the client actually was, FTI’s assignment description does not put that company in a very good light:

Some of the troubling elements:

Foxes running the henhouse. The text above effectively says that FTI was working for the management of the very same entity that received the $50 million of overpayments. FTI depicts the breakdown as taking place at the company level and says it gave advice only to “the Company” and worked with its internal auditors.

For this sort of review to be credible, the client needs to be independent of the people who benefitted from the control failure and may well have been aware of what was happening but chose to remain silent. Here, there was no apparent involvement of parent company internal or external auditors, management, legal team, or compliance. Reading this in isolation, a savvy reader would infer that FTI’s job was to help keep top management and parent company compliance officers out of the mix by papering up a solution at the subsidiary level.

No indication that the $50 million was to be paid back or credited against future compensation. If correct, this would be a windfall to the executives of the unit. The narrative discusses only determining who got what overpayment and assessing tax and accounting impacts at the company and parent level.

Possible SEC violation. While the amounts at issue are presumably too small from an accounting perspective for the parent company to refile its financial statements, even FTI depicts the large overpayment to executives as “a breakdown in controls.” This violation is very similar to the sort that the SEC repeatedly used as a basis for charging fines and ordering disgorgements in private equity exams. The text above makes it seem as if it was the public shareholders rather than real estate limited partners that lost out as a result of this overpayment which appears still to be outstanding. But the underlying issue that the SEC uses to assess fines is failure to disclose and that appears to be operative here.

Francine McKenna, who has worked at major accounting firms and now writes on accounting and compliance matters, confirmed our take: “As a public company the amount would probably not be material but as a lack of disclosure item the SEC would likely consider it material. ”

Incorrect terminology. The description says FTI worked with internal auditors to assess the impact on parent company public financials, “based on Generally Accepted Accounting Procedures”. The term of art is “generally accepted accounting principles”. This level of sloppiness in a presentation to a prospective client does not speak well regarding FTI’s professionalism.

And we have additional issues that relates to the proposed LACERA work and potentially the “Global Investment Bank” assignment:

Possible exaggeration of CPA credentials. In the bios presented, FTI has four individuals who present themselves as CPAs Scott D. Friedland and Clara Chin in New York and Scott W. Carnahan and Michael Garibaldi in California. You can input the names as I did in the New York and the California Board of Accountancy as appropriate. Clara Chin came up with no results.2 Perhaps she is licensed in another state, but she is located in New York and one would expect her to be licensed in the state in which she performs most of her work.

Now it may be that FTI has given a misleading picture in its LACERA. But if I were Apollo, I would be plenty unhappy, particularly since LACERA is a regular investor in the sort of funds that Apollo manages.

___

1 Perversely, LACERA’s Public Records Act log shows the records being provided to Gretchen Morgenson of the New York Times in 2016, but not from the source that obtained them earlier and provided them to Gretchen and us around the same time. We thought it was better for Gretchen to run the story, and then let it slip when she didn’t. We have the complete record of the source’s e-mail exchanges with LACERA, which included the provision of the FTI proposal with its CalPERS report, from March 3, 2017 to March 17, 2017. We obtained the documents again directly from LACERA to make sure that the agency was still handing out the version it had been provided by FTI, as in an improperly-redacted document. Why we are being so nit-picky about the document’s provenance will become clear when we discuss its significance for CalPERS in a later post.

2 “Clara Chin” is no longer listed in FTI’s directory on the “C” last name page of its FTI Consulting – All Professionals directory. Nor does a listing for her come up if you search the FTI site using her name. Nevertheless, at LinkedIn, she depicts herself as “Clara Chin, CPA, CFE…Greater New York City Area” and the most recent bio entry is “Senior Director, Forensic and Litigation Consulting,FTI Consulting, Jun 2005 – Present, 11 yrs 10 mos”

FTI Proposal_5_10_9_2015_RedactedCalPERS FTI Report

Let me guess, they slapped some black boxes on the redacted bits in acrobat but instead of “printing” it as a flat PDF it was saved layered, and the black box layer was removed?

It’s probably best if we don’t guess at such things. Wouldn’t want the criminals in question to get better at hiding their crimes, would we?

I seem to recall another instance of someone doing the black-box on a PDF thing and getting busted for it, but I don’t recall where. Anyone else have a better memory?

FTI did the whitewash report for MassBay Transit after Harry Markopolus proved all the hedge fund fraud.

How does one ‘erroneously report’ a $50 million cash distribution as a receivable on the balance sheet?!?! Wouldn’t that pretty much have to be deliberate?

Far from an expert on balance sheet accounting so maybe there is legit reason why one would do so but from where I’m sitting it certianly sounds like deliberate fraud.

If it was recorded as a receivable that would mean that the intention of both parties was that the $50M would be repaid. Ultimately it’s hard to conceive of a valid business purpose for a pension fund to advance $50M to an outside contractor. Smells like another case of the foxes raiding the hen house and trying to obscure the fact. Also, the $50M need not be repaid in cash. More than likely it will be repaid in future services instead. Stuff like this never happens in arms length transactions between unrelated parties.

Chin comes up at maine.gov.

Thanks a lot. However, if you read the NASBA, CPAs are supposed to be licensed in the state which is their primary place of business, which is not the case with Chin. See the end of the first para here: “may be granted a privilege to practice in another jurisdiction that is not the CPA’s principal place of business.”

https://www.nasba.org/licensure/substantialequivalency/

Well first FTI is not considered an “accounting firm.” It is a consulting firm. Once you move away from the attestation function and the tax return preparation function licensing requirements become a little more hazy. This work is performed by CPA’s but it could be just as easily performed by non-licensed individuals. In addition, any findings are generated in letters between private parties and no “opinions” are given. I would call this more of agreed upon procedures which once again could be performed by non-licensed personnel. I am sure if you looked at the job arrangement letter you would not see anything specifying that the work will be performed by licensed CPA’s. Besides, the letter could be signed by some one licensed in the state where the letter was given and that would meet the adequately supervised requirement.

I do some sub-contracting consulting work where the firm I do the work for go out of their way to indicate that they are not a “CPA firm” even though much of their work is internal control related. Once again no opinion is expressed on anything and usually the engagement letters indicates that we are working at the direction of the client ie there is no independence. With that said I am licensed in the states where I do the work and I make sure that I perform the standards within AICPA and state board standards.

Personally it would be great if the state boards would require CPA’s to be the only people who are allowed to do this type of work. Greatly reduce the bodies practicing in this area and get the hourly billing rate up. By the way lots of the firms staff this work with H-1-b’s which allows them to greatly improve their gross margin on these engagements. Needless to say, I believe the work is greatly sub-par.

You are missing the point. FTI actually markets itself as being a better choice because it does kinda-sorta audit type work but is not held to the independence standards of an accounting firm. What does that tell you about their work product? They are essentially marketing themselves as fixers.

And as indicated in the post, they have a big business in outsourced accounting for REITs. I am a pokey one employee company and I’d never consider having my accounting done by anyone other than a CPA for audit risk reason alone.

The state licensing boards appear to have allowed themselves to be muscled in a big way. The normal standards for being a CPA were that you worked for a public accounting firm, in that you needed to do a certain numbers of actual audit work a year to force you to keep current, as well as keep up with continuing education requirements. The fact that the four individuals I checked are CPAs while not working for a public accounting firm speaks volumes about how professional standards have changed, and not in a good way.

Excellent point. There is no doubt that the market pressure created by the infusion of Wall Street money into and around the accounting profession has greatly eroded professional standards. Audit and attestation work used to have a much more prominent position in the accounting profession. That changed greatly in the 1980’s and 1990’s, when tax, consulting and advisory services catapulted way ahead, and traditional A&A work came to be viewed as low profit and low growth. There are still throwbacks like Ishmael who do the job right, but that is not where the big money goes. Money gets what money wants.

Yep! Completely down with the article’s argument and the valence/implications that she is licensed somewhere else. Thank you for writing about these opaque organizations.

That lack of independence with the consulting firm is no different than the lack of independence that exists between an external CPA firm and the company that hires them to audit their books. Ultimately the company is the customer and the CPA firm the service provider who must please the customer in order to get paid and get future work. The accounting profession has a zillion rules on independence to mask the fact that real independence is not possible.

Generally I would take issue with this comment. Now trust me I know a number of firms do not have independence (even the large ones) but many do. I usually insist on payment up front and return excess fees afterwards. I have walked on several engagements. One time the general counsel (Stanford Law) gave me we are the customer routine with the CFO standing there. He quickly pushed the general counsel out of the room, gave him the lay of the land and the GC returned and said he now understood the relationship. I had been packing up getting ready to leave. Basically I do not look good in an orange jump suit and do not want to be roommates with bubba. When things start going south the first thing clients yell was that is what my outside accountants told me to do.

There are pressure points all over that compromise independence. The biggest of these is that the company that you must maintain your independence from is the company that is paying you. Of course the consequences of a lack of independence can be minimized, but you need to be forever on guard. Your example shows that company’s will push on those pressure points. Not everybody resists. Not everybody is in position to resist. To walk away from a job is to walk away from client revenue. And that can be a big problem, whether you are an independent contractor making that decision for yourself, or a partner of a large CPA firm making that decision on behalf of the firm. The world can be a cold and cruel place for that individual who resists temptation on ethical grounds.

Are these the same “experts” who vetted the Oroville dam?