By Houses and Holes, the founding publisher and former editor-in-chief of The Diplomat, a regular contributor at The Sydney Morning Herald, The Age and The Drum, and a former commentator at Business Spectator. He is also the co-author of The Great Crash of 2008 with Ross Garnaut. He edits MacroBusiness. Originally published at Macrobusiness.

Excessive indebtedness has been one of the root causes of financial crises and the ensuing deep recessions. In recent years, the focus has been on household debt, as excessive leverage by the household sector was at the heart of the Great Financial Crisis.

It is well recognised that household borrowing is an important aspect of financial inclusion and can play useful economic roles, including smoothing consumption over time. At the same time, rapid household credit growth has featured prominently in financial cycle booms and busts. For one, household debt – or debt more generally – outpacing GDP growth over prolonged periods is a robust early warning indicator of financial stress.

Furthermore, there is growing evidence that household indebtedness affects not only the depth of recessions but growth more generally. In an influential paper, Mian et al (forthcoming) find that an increase in the household debt-to-GDP ratio acts as a drag on consumption with a lag of several years.

BIS research reinforces this conclusion. For instance, based on a panel of 54 advanced and emerging market economies over the period 1990–2015, Lombardi et al (2017) find that rising household indebtedness boosts consumption and GDP growth in the short run, but not in the longer run. Specifically, a 1 percentage point increase in the household debt-to-GDP ratio is associated with growth that is 0.1 percentage point lower in the long run.

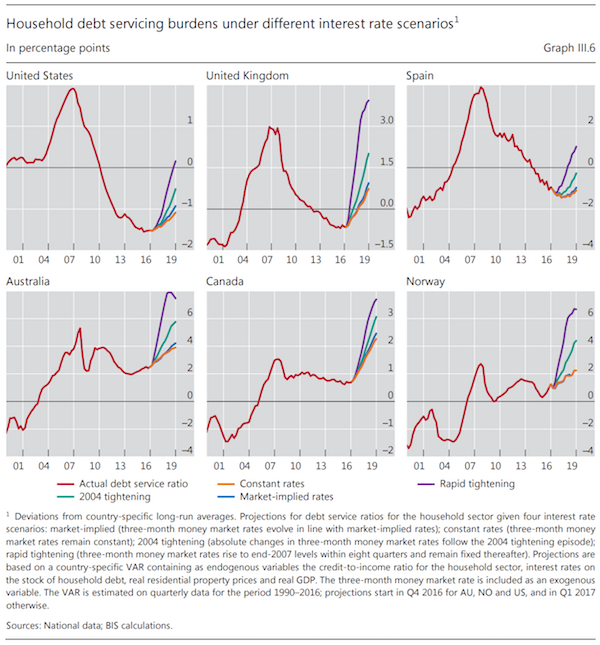

Drehmann et al (forthcoming) shed light on a possible mechanism behind these empirical regularities. When households take on long-term debt, they increase current spending power but commit to a pre-specified path of future debt service (interest payments and amortisations).

A simple framework captures this accounting relationship. It highlights two key features. First, if borrowing rises persistently over several years and debt is longterm, as is typically the case, the debt service burden reaches its maximum only after the peak in new borrowing. The lag can be of several years and increase with the maturity of debt and the degree of persistence in borrowing. Second, cash flows from lenders to borrowers reach their maximum before new borrowing peaks. They turn negative before the end of a credit boom, since the positive cash flow from new borrowing is increasingly offset by the negative cash flow from rising debt service. Empirically, these simple accounting relationships suggest a transmission channel whereby excessive credit expansions lead to future output losses. In particular, using a panel of 17 mainly advanced economies from 1980 to 2016, Drehmann et al (forthcoming) show that an increase in new debt relative to GDP beyond historical norms provides on average a boost to GDP growth in the short run but depresses output growth in the medium term (Graph III.A, left-hand panel and black line in the right-hand panel). As the accounting framework suggests, the increase in new debt feeds into higher debt service burdens. As higher debt service burdens have a strong negative effect on output going forward, this channel explains almost fully the medium-term growth decline (blue bars, right-hand panel). However, the negative effects of high credit growth in the medium term are not unconditional. If households initially have low debt service burdens, additional borrowing continues to be beneficial in the short run without significant adverse effects later on. This suggests, for instance, that there can be room for benign financial deepening in countries where households are not yet constrained.

The adverse effects of excessive credit growth can also be magnified by the economy’s supply side response. For example, banks’ stronger willingness to extend mortgages may feed an unsustainable housing boom and overinvestment in the construction sector, which may crowd out investment opportunities in higher-productivity sectors. Borio et al (2016), for example, report evidence that credit booms tend to go hand in hand with a misallocation of resources – most notably towards the construction sector – and a slowdown in productivity growth, with long-lasting adverse effects on the real economy.

Wow! and do you really need a ivy league phd to see that? I would never have thought that excessive debt burden shrink markets and growth…

“Drehmann et al (forthcoming) shed light on a possible mechanism behind these empirical regularities. When households take on long-term debt, they increase current spending power but commit to a pre-specified path of future debt service”

What a surprise. I am at a loss for words. Nobody could have foreseen that.

And they even add “possible mechanism”. Like, hey dudes, we are not sure but it is a remote possibility. I would laugh my ass off but then I remember that these charlatans are in control of our lives.

Rocket science.

jerry

You even need ivy league PhD’s to come up with the wrong conclusions as well, see Rogoff and Reinhart. But it’s not like their research influenced government policy for years and helped promote austerity which has and continues to ruin the lives of millions around the world.. oh wait..

Agreed, the fact that this serves as some sort of discovery is comical. Mainstream economists are joke, a dangerous joke, because they have a major role in public policy. Great interview with Steven Keen on Macrovoices last month and I loved his discussion of mainstream economics and his argument that you have to go to second or third tier school to get a proper eduction in the subject.

Kuhio Kane

Absolutely. See Keen for additional information regarding the bigger picture. Another liquidity trap with all the assets moving to the rentier banking class.

Susan the other

Ann Pettifor has become so disgusted with all of this “gee, we didn’t know” and other incompetencies that she has written a piece demanding that the government take a hard look at the economics profession in a first step to making it responsive and responsible to the people. This is the UK, and we should definitely do it here, US, too.

DanB

From a class conflict perspective, the economics field is responsive to its constituency: the 1%. As Marx and others have pointed out, the ideological necessity of making what is unjust appear as “There Is No Alternative” is the unstated core mandate of the economists. Therefore, despite the ludicrousness of this analysis, I find it another chink in the armor of the dominant ideology that the obvious is now being so gingerly discussed by mainstream economists, the chief ideological propagandists of the 1%.

WobblyTelomeres

What Minsky called “court economists”?

cocomaan

When households take on long-term debt, they increase current spending power but commit to a pre-specified path of future debt service (interest payments and amortisations).

How much are these people paid to come up with these thrilling and original conclusions?

Ignacio

Economists struggling with the obvious because it does not fit their models, I guess. For instance models that say “someone’s debt is just the asset of other”, hence debt doesn’t matter

Kuhio Kane

Because the mainstream model is still delusionally basing macroeconomics on microeconomics.

TomDority

The research is being published. Although the outcome is obvious…it appears these obvious tidbits never saw the light of day because they did not fit the fantasies of the gnats of finance and ‘industry’…err giants

Moneta

For some reason, many economists still don’t see it!

Now the general meme is that after 10 years, balance sheets have slowly been repared as if these household would be about to remake the same debt mistakes.

Most of the debt before the crisis was taken on by the 45+. They are 10 years older now and not about to releverage themselves.

The growth will have to come from the younger group… but they are full of student and car debt. Will they be able to buy houses for which prices have returned to pre-crisis levels?

This leverage game depends on housing but it looks like we will be forced into a change of paradigm.

skippy

Wages and productivity divergence, crapifiction of long term credit risk, concentration of wealth and assets….

disheveled… and the sound track chorus – because markets – all sung by Milton, Rubin, Greenspan, et al… but yeah… the debt… sigh…

templar555510

Very well put. The ‘ leverage game ‘ comprises the whole neo-liberal paradigm which as you say depends on housing . Here in the UK until the last fifteen years or so, apart from a small number of very top end residential properties there was a ‘ property ladder ‘ we used to say . The meaning was that you could start at the bottom and if you chose to, could move up, and even though property prices moved up your wages were likely to increase, but your debt was being eroded bit by bit by inflation which kept the whole thing in sync. Those days are long gone and I think it is dawning on a lot of us that the game is finally up for this paradigm and there is no going back. Hence the certain air of melancholy which pervades the atmosphere . I went to a little drinks party on Saturday evening and it was interesting how the room of twenty or so people divided between those stuck in the status quo and those beginning to perceive of a future beyond the status quo .

abynormal

for shits n giggles

Forecasting thru 2024…they kinda get hung up on 2017

Oregoncharles

Link doesn’t work – “not found.”

Oregoncharles

for some reason, it works without the “http//” – then inserts it.

It’s the CBO projection from 2014, but I don’t see the issue with 2017.

Hope you’re doing well, aby.

Carla

So, the BIS is going to promote a Global Jubilee, right?

I would say that before the JG (Job Guarantee), we need a GJ (Global Jubilee).

After a GJ, we could afford nice things: world peace, health care, sustainable energy, universal public education at least through the B.A., publicly owned and operated utilities, including Internet and banks — you know, NICE things.

JEHR

I’m really pleased to see that none of the comments supports the ridiculous belief that “excessive leverage by the household sector was at the heart of the Great Financial Crisis.” What a load of crap! What about the financialization of “everything” that gives the financial sector huge amounts of revenue while the working stiffs gets stagnant wages and/or loss of jobs. Because of the financial crisis, people lost their houses, their jobs and their dignity.

The BIS has a lot to answer for because they seem incapable of doing their job for the whole economy and seem to concentrate on the stability of the financial sector without any regard for the people who are not in the financial sector but who are affected by the decisions of the financial sector. The BIS protects and coddles the cartel of banks in this world with little regard to their corruption and fraud, the two things that really brought about the Great Financial Crisis. Man, we are in for a rough ride for eons if these weirdly unpleasant persons stay in power at the BIS for very long.

“fostering discussion and facilitating collaboration among central banks;

supporting dialogue with other authorities that are responsible for promoting financial stability;

carrying out research and policy analysis on issues of relevance for monetary and financial stability;

acting as a prime counterparty for central banks in their financial transactions; and

serving as an agent or trustee in connection with international financial operations.”

Mark Carney, London

Agustín Carstens, Mexico City

Andreas Dombret, Frankfurt am Main Mario Draghi, Frankfurt am Main William C Dudley, New York

Ilan Goldfajn, Brasília

Stefan Ingves, Stockholm

Thomas Jordan, Zurich

Klaas Knot, Amsterdam

Haruhiko Kuroda, Tokyo

Anne Le Lorier, Paris

Fabio Panetta, Rome

Urjit R Patel, Mumbai Stephen S Poloz, Ottawa

Jan Smets, Brussels

François Villeroy de Galhau, Paris

Ignazio Visco, Rome

Pierre Wunsch, Brussels Janet L Yellen, Washington

Zhou Xiaochuan, Beijing”

We really must see these men as the power brokers of all time and our miserable existence is only going to get worse with these guys and gals in control.

polecat

How ’bout a commemorative lamp post ‘dedicated’ to each of the above ?

Maybe we could start a ‘kick@ss starter’ fundraiser !

Jim Haygood

Globally, household debt is the smallest of the four commonly used categories of Household, Corporate [non-financial], Government, and Financial. Chart:

In a recession, a debt-burdened corporate sector behaves much as households do, cutting back particularly on capital investment. Government goes the opposite way, hiking debt during a recession to fund automatic stabilizers. But heavy gov’t debt, like household debt, is a drag on consumption after a lag of several years.

Focusing on household debt alone is of questionable value, when much broader debt aggregates are available. What’s clear from the chart comparing household debt in six countries is that Canada and Australia are up to their necks in debt, largely owing to mortgage debt supported by their housing bubbles.

When these housing bubbles burst — as bubbles invariably do — these two resource-oriented economies are going to be sucking wind. Unfortunately, in 2014 USgov started applying US income taxation to Canadians who stay 182 days a year or more in the US. Refugees from the Great White North who flee south will face a whole new level of pain when the US IRS works them over with a rubber hose.

John k

Gov debt drags the economy…

True in non sovereign EU, not necessarily true here, granted reps trying to cut discretionary to ‘afford’ tax cuts to savers.

Fed Bought more treasuries than issued for years, so self funding, surprising some no inflation results. Instead of refunding interest to treasury, fed could just burn them; what’s the diff?

Result is savers can’t get the safe investment they want, so speculate on assets… won’t end well, maybe soon, bank credit crashing, savers worldwide continue to drain dollars from economy, fiscal deficit not compensating… and maybe auto stabilizers won’t kick in as much in next recession, Mosler thinks unemployment harder to get, maybe benefits exhausted, or a maybe because so many rep governors…

Oregoncharles

Restating the obvious, but I guess it has to be done.

I’m wondering about BIS; isn’t it essentially a co-op of banks, with the job of providing international clearing services? So why is it pointing out this particular obvious?

RBHoughton

I’m guessing the BIS saw it would have to take a position and thought it should have a bit of naff research to support it. Apparently, it takes experts to say household debt today reduces economic growth tomorrow (and they haven’t actually said it yet – its forthcoming)!

Wonder what that startlingly penetrative insight cost!

So that’s the cause, what’s the remedy?

Sound of the Suburbs

Financial stability has been a mystery in this era of boom/bust capitalism.

2008 – “How did that happen?”

The early 1980s see the beginnings of financial liberalisation and the late 1980s sees the following crises, e.g. US S&L crisis; UK, Japan, Australia, Canada and Scandinavia real estate busts.

More financial deregulation leads to 2008; the Euro-zone crisis; Irish, Greek and Spanish real estate crashes.

2008 is just another real estate bust, leveraged up and transmitted internationally by complex financial instruments. As the global bust hits the Euro-zone, it crumbles.

Australia, Canada and Scandinavia are queuing up for their second real estate bust.

Today’s neoclassical economics was around in the 1920s and it led to the roaring 20s and the Great Depression. The roaring 20s, roared because of debt based consumption and debt based speculation. All the debt built up in the boom led to the debt deflation of the Great Depression.

Neoclassical economics was revamped but it still has its old problems.

We have a problem, a real estate fuelled economy driven by unproductive lending that naturally leads to financial instability.

Neoclassical economics doesn’t consider private debt in the economy and naturally leads to boom/bust capitalism because of this over-sight. It doesn’t even consider debt and so can’t make the finer distinction between productive and unproductive lending.

If you want financial stability, don’t use neoclassical economics.

Sound of the Suburbs

The problem can only be understood by a thorough understanding of money and debt.

How money is created and destroyed on the balance sheets of private banks.

This is where financial crises come from.

“…banks make their profits by taking in deposits and lending the funds out at a higher rate of interest” Paul Krugman, 2015.

2008 – “How did that happen”

This is not how banks, money and debt work and make the financial system look much safer than it is to today’s economists.

The understanding of money and debt have been regressing for one hundred years.

Credit creation theory -> fractional reserve theory -> financial intermediation theory

“The movement from the accurate credit creation theory to the misleading, inconsistent and incorrect fractional reserve theory to today’s dominant, yet wholly implausible and blatantly wrong financial intermediation theory indicates that economists and finance researchers have not progressed, but instead regressed throughout the past century. That was already Schumpeter’s (1954) assessment, and things have since further moved away from the credit creation theory.”

“A lost century in economics: Three theories of banking and the conclusive evidence” Richard A. Werner

You need the “credit creation theory” of money to get a grip of financial crises and financial instability and today we don’t have that in the mainstream leading to boom/bust capitalism.

Sound of the Suburbs

The BIS catches up:

“Stocks have reached what looks like a permanently high plateau.” Irving Fisher 1929.

Irving Fisher looked into his mistakes and in the 1930s came up with a theory of debt deflation.

Hyman Minsky carried on with his work and came up with the “Financial Instability Hypothesis” in 1974.

Steve Keen carried on with their work and spotted 2008 coming in 2005.

All worked out after neoclassical economics 1930s apocalypse.

Sound of the Suburbs

The BIS have got it wrong they don’t know how money works.

They are trying to use “financial intermediation theory” rather than “credit creation theory”.

Pia Nielsen

Economists are like the priesthood in Middle Age church. Hocus Pocus. There´s no sense to it. They are there to uphold the hierarchical system of those who have and those who haven´t.

How do we disconnect? We can´t just sit and wait – The way we live is a social, cultural and environmental disaster. And they are not going to chance it anything. They are just looking for new ways to enslave people. They know there may be a breaking point soon to come – and usually that just lead to war.

Next week-end 100 people are joining together to widen the project and buy a piece of land ( it´s cheap because it is in the countryside where prices have decreased) and an old industrial building for those who want to start up business. The aim is to end up free of debt and waste. The houses are cheap made of materials recyclable. The houses will be off the grit and collect rainwater and recycling waste water. In short they aim to be self sufficient and near no production of waste. And debt free so you can have more spare time to do the things you really want in life.

Karl

One implication I take from this is that too-rapid debt expansion sows the seeds of the next downturn.The problem arises when debt and debt service climb too fast. As Minsky and Keen point out, if the expansion is too rapid, like a plane gaining altitude too fast on take-off, the expansion will stall. A more gradual rise in debt (altitude) will enable speed (GDP growth) and lift (more debt) to work together to keep the expansion going. Therefore, if there is a way to moderate debt expansion, this might keep growth sustainable. But that’s like asking capitalists to moderate their greed.

Wow! and do you really need a ivy league phd to see that? I would never have thought that excessive debt burden shrink markets and growth…

“Drehmann et al (forthcoming) shed light on a possible mechanism behind these empirical regularities. When households take on long-term debt, they increase current spending power but commit to a pre-specified path of future debt service”

What a surprise. I am at a loss for words. Nobody could have foreseen that.

And they even add “possible mechanism”. Like, hey dudes, we are not sure but it is a remote possibility. I would laugh my ass off but then I remember that these charlatans are in control of our lives.

Rocket science.

You even need ivy league PhD’s to come up with the wrong conclusions as well, see Rogoff and Reinhart. But it’s not like their research influenced government policy for years and helped promote austerity which has and continues to ruin the lives of millions around the world.. oh wait..

Speaking of Rogoff

https://www.project-syndicate.org/commentary/eurozone-reform-macron-merkel-by-kenneth-rogoff-2017-06

When you’ve lost Rogoff….

Agreed, the fact that this serves as some sort of discovery is comical. Mainstream economists are joke, a dangerous joke, because they have a major role in public policy. Great interview with Steven Keen on Macrovoices last month and I loved his discussion of mainstream economics and his argument that you have to go to second or third tier school to get a proper eduction in the subject.

Absolutely. See Keen for additional information regarding the bigger picture. Another liquidity trap with all the assets moving to the rentier banking class.

Ann Pettifor has become so disgusted with all of this “gee, we didn’t know” and other incompetencies that she has written a piece demanding that the government take a hard look at the economics profession in a first step to making it responsive and responsible to the people. This is the UK, and we should definitely do it here, US, too.

From a class conflict perspective, the economics field is responsive to its constituency: the 1%. As Marx and others have pointed out, the ideological necessity of making what is unjust appear as “There Is No Alternative” is the unstated core mandate of the economists. Therefore, despite the ludicrousness of this analysis, I find it another chink in the armor of the dominant ideology that the obvious is now being so gingerly discussed by mainstream economists, the chief ideological propagandists of the 1%.

What Minsky called “court economists”?

How much are these people paid to come up with these thrilling and original conclusions?

Economists struggling with the obvious because it does not fit their models, I guess. For instance models that say “someone’s debt is just the asset of other”, hence debt doesn’t matter

Because the mainstream model is still delusionally basing macroeconomics on microeconomics.

The research is being published. Although the outcome is obvious…it appears these obvious tidbits never saw the light of day because they did not fit the fantasies of the gnats of finance and ‘industry’…err giants

For some reason, many economists still don’t see it!

Now the general meme is that after 10 years, balance sheets have slowly been repared as if these household would be about to remake the same debt mistakes.

Most of the debt before the crisis was taken on by the 45+. They are 10 years older now and not about to releverage themselves.

The growth will have to come from the younger group… but they are full of student and car debt. Will they be able to buy houses for which prices have returned to pre-crisis levels?

This leverage game depends on housing but it looks like we will be forced into a change of paradigm.

Wages and productivity divergence, crapifiction of long term credit risk, concentration of wealth and assets….

disheveled… and the sound track chorus – because markets – all sung by Milton, Rubin, Greenspan, et al… but yeah… the debt… sigh…

Very well put. The ‘ leverage game ‘ comprises the whole neo-liberal paradigm which as you say depends on housing . Here in the UK until the last fifteen years or so, apart from a small number of very top end residential properties there was a ‘ property ladder ‘ we used to say . The meaning was that you could start at the bottom and if you chose to, could move up, and even though property prices moved up your wages were likely to increase, but your debt was being eroded bit by bit by inflation which kept the whole thing in sync. Those days are long gone and I think it is dawning on a lot of us that the game is finally up for this paradigm and there is no going back. Hence the certain air of melancholy which pervades the atmosphere . I went to a little drinks party on Saturday evening and it was interesting how the room of twenty or so people divided between those stuck in the status quo and those beginning to perceive of a future beyond the status quo .

for shits n giggles

Forecasting thru 2024…they kinda get hung up on 2017

Link doesn’t work – “not found.”

for some reason, it works without the “http//” – then inserts it.

It’s the CBO projection from 2014, but I don’t see the issue with 2017.

Hope you’re doing well, aby.

So, the BIS is going to promote a Global Jubilee, right?

I would say that before the JG (Job Guarantee), we need a GJ (Global Jubilee).

After a GJ, we could afford nice things: world peace, health care, sustainable energy, universal public education at least through the B.A., publicly owned and operated utilities, including Internet and banks — you know, NICE things.

I’m really pleased to see that none of the comments supports the ridiculous belief that “excessive leverage by the household sector was at the heart of the Great Financial Crisis.” What a load of crap! What about the financialization of “everything” that gives the financial sector huge amounts of revenue while the working stiffs gets stagnant wages and/or loss of jobs. Because of the financial crisis, people lost their houses, their jobs and their dignity.

The BIS has a lot to answer for because they seem incapable of doing their job for the whole economy and seem to concentrate on the stability of the financial sector without any regard for the people who are not in the financial sector but who are affected by the decisions of the financial sector. The BIS protects and coddles the cartel of banks in this world with little regard to their corruption and fraud, the two things that really brought about the Great Financial Crisis. Man, we are in for a rough ride for eons if these weirdly unpleasant persons stay in power at the BIS for very long.

We really must see these men as the power brokers of all time and our miserable existence is only going to get worse with these guys and gals in control.

How ’bout a commemorative lamp post ‘dedicated’ to each of the above ?

Maybe we could start a ‘kick@ss starter’ fundraiser !

Globally, household debt is the smallest of the four commonly used categories of Household, Corporate [non-financial], Government, and Financial. Chart:

In a recession, a debt-burdened corporate sector behaves much as households do, cutting back particularly on capital investment. Government goes the opposite way, hiking debt during a recession to fund automatic stabilizers. But heavy gov’t debt, like household debt, is a drag on consumption after a lag of several years.

Focusing on household debt alone is of questionable value, when much broader debt aggregates are available. What’s clear from the chart comparing household debt in six countries is that Canada and Australia are up to their necks in debt, largely owing to mortgage debt supported by their housing bubbles.

When these housing bubbles burst — as bubbles invariably do — these two resource-oriented economies are going to be sucking wind. Unfortunately, in 2014 USgov started applying US income taxation to Canadians who stay 182 days a year or more in the US. Refugees from the Great White North who flee south will face a whole new level of pain when the US IRS works them over with a rubber hose.

Gov debt drags the economy…

True in non sovereign EU, not necessarily true here, granted reps trying to cut discretionary to ‘afford’ tax cuts to savers.

Fed Bought more treasuries than issued for years, so self funding, surprising some no inflation results. Instead of refunding interest to treasury, fed could just burn them; what’s the diff?

Result is savers can’t get the safe investment they want, so speculate on assets… won’t end well, maybe soon, bank credit crashing, savers worldwide continue to drain dollars from economy, fiscal deficit not compensating… and maybe auto stabilizers won’t kick in as much in next recession, Mosler thinks unemployment harder to get, maybe benefits exhausted, or a maybe because so many rep governors…

Restating the obvious, but I guess it has to be done.

I’m wondering about BIS; isn’t it essentially a co-op of banks, with the job of providing international clearing services? So why is it pointing out this particular obvious?

I’m guessing the BIS saw it would have to take a position and thought it should have a bit of naff research to support it. Apparently, it takes experts to say household debt today reduces economic growth tomorrow (and they haven’t actually said it yet – its forthcoming)!

Wonder what that startlingly penetrative insight cost!

So that’s the cause, what’s the remedy?

Financial stability has been a mystery in this era of boom/bust capitalism.

2008 – “How did that happen?”

The early 1980s see the beginnings of financial liberalisation and the late 1980s sees the following crises, e.g. US S&L crisis; UK, Japan, Australia, Canada and Scandinavia real estate busts.

More financial deregulation leads to 2008; the Euro-zone crisis; Irish, Greek and Spanish real estate crashes.

2008 is just another real estate bust, leveraged up and transmitted internationally by complex financial instruments. As the global bust hits the Euro-zone, it crumbles.

Australia, Canada and Scandinavia are queuing up for their second real estate bust.

Today’s neoclassical economics was around in the 1920s and it led to the roaring 20s and the Great Depression. The roaring 20s, roared because of debt based consumption and debt based speculation. All the debt built up in the boom led to the debt deflation of the Great Depression.

Neoclassical economics was revamped but it still has its old problems.

https://cdn.opendemocracy.net/neweconomics/wp-content/uploads/sites/5/2017/04/Screen-Shot-2017-04-21-at-13.52.41.png

1929 and 2008 stick out like sore thumbs when you look in the right place.

The build up in the ratio of debt to GDP signals the build up of unproductive lending into the economy leading to a Minsky Moment (1929 and 2008).

Productive lending goes into business and industry.

Unproductive lending goes into real estate and financial speculation and it shows up in the graph above.

The UK:

https://cdn.opendemocracy.net/neweconomics/wp-content/uploads/sites/5/2017/04/Screen-Shot-2017-04-21-at-13.53.09.png

We have a problem, a real estate fuelled economy driven by unproductive lending that naturally leads to financial instability.

Neoclassical economics doesn’t consider private debt in the economy and naturally leads to boom/bust capitalism because of this over-sight. It doesn’t even consider debt and so can’t make the finer distinction between productive and unproductive lending.

If you want financial stability, don’t use neoclassical economics.

The problem can only be understood by a thorough understanding of money and debt.

How money is created and destroyed on the balance sheets of private banks.

This is where financial crises come from.

“…banks make their profits by taking in deposits and lending the funds out at a higher rate of interest” Paul Krugman, 2015.

2008 – “How did that happen”

This is not how banks, money and debt work and make the financial system look much safer than it is to today’s economists.

The understanding of money and debt have been regressing for one hundred years.

Credit creation theory -> fractional reserve theory -> financial intermediation theory

“The movement from the accurate credit creation theory to the misleading, inconsistent and incorrect fractional reserve theory to today’s dominant, yet wholly implausible and blatantly wrong financial intermediation theory indicates that economists and finance researchers have not progressed, but instead regressed throughout the past century. That was already Schumpeter’s (1954) assessment, and things have since further moved away from the credit creation theory.”

“A lost century in economics: Three theories of banking and the conclusive evidence” Richard A. Werner

http://www.sciencedirect.com/science/article/pii/S1057521915001477

You need the “credit creation theory” of money to get a grip of financial crises and financial instability and today we don’t have that in the mainstream leading to boom/bust capitalism.

The BIS catches up:

“Stocks have reached what looks like a permanently high plateau.” Irving Fisher 1929.

Irving Fisher looked into his mistakes and in the 1930s came up with a theory of debt deflation.

Hyman Minsky carried on with his work and came up with the “Financial Instability Hypothesis” in 1974.

Steve Keen carried on with their work and spotted 2008 coming in 2005.

All worked out after neoclassical economics 1930s apocalypse.

The BIS have got it wrong they don’t know how money works.

They are trying to use “financial intermediation theory” rather than “credit creation theory”.

Economists are like the priesthood in Middle Age church. Hocus Pocus. There´s no sense to it. They are there to uphold the hierarchical system of those who have and those who haven´t.

How do we disconnect? We can´t just sit and wait – The way we live is a social, cultural and environmental disaster. And they are not going to chance it anything. They are just looking for new ways to enslave people. They know there may be a breaking point soon to come – and usually that just lead to war.

Is it possible to live differently. This project started up with 13 families

friland http://www.denmark.net/friland/

Next week-end 100 people are joining together to widen the project and buy a piece of land ( it´s cheap because it is in the countryside where prices have decreased) and an old industrial building for those who want to start up business. The aim is to end up free of debt and waste. The houses are cheap made of materials recyclable. The houses will be off the grit and collect rainwater and recycling waste water. In short they aim to be self sufficient and near no production of waste. And debt free so you can have more spare time to do the things you really want in life.

One implication I take from this is that too-rapid debt expansion sows the seeds of the next downturn.The problem arises when debt and debt service climb too fast. As Minsky and Keen point out, if the expansion is too rapid, like a plane gaining altitude too fast on take-off, the expansion will stall. A more gradual rise in debt (altitude) will enable speed (GDP growth) and lift (more debt) to work together to keep the expansion going. Therefore, if there is a way to moderate debt expansion, this might keep growth sustainable. But that’s like asking capitalists to moderate their greed.