By Gaius Publius, a professional writer living on the West Coast of the United States and frequent contributor to DownWithTyranny, digby, Truthout, and Naked Capitalism. Follow him on Twitter @Gaius_Publius, Tumblr and Facebook. GP article archive here. Originally published at DownWithTyranny

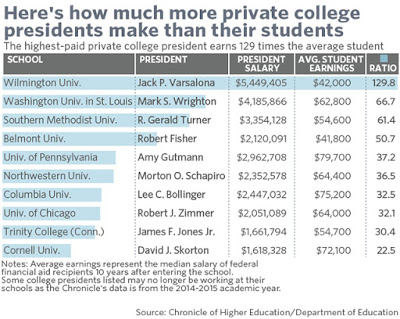

The other side of student debt: Salaries of some private college presidents according to the Chronicle of Higher Education (source). These numbers are deceptive. According to the Huffington Post, the president of the University of Chicago, for example, was paid $3.3 million in 2011 if you include deferred compensation.

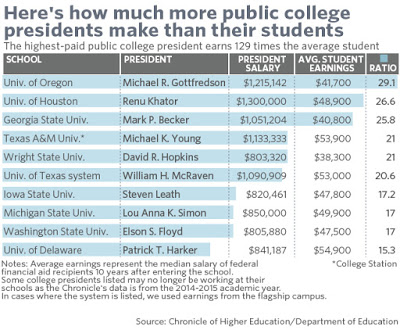

The other side of student debt: Salaries of presidents of some public (taxpayer-funded) colleges and universities according to the Chronicle of Higher Education (source), These numbers do not appear to include deferred compensation.

This is the second part in a short series, “Killing a Parasite — Canceling Student Debt.”

In Part 1, we made the case that the institutionalized and growing student debt crisis is not fed by predatory activity on creditors, but by parasitic activity. Predators kill, eat, and move on. Parasites disable, then live off the energy system of the disabled host for as long as they can keep the host alive. The argument there was simple: “Viruses are a form of parasite. So are credit card companies.”

An especially pernicious form of “loan parasite” includes institutions preying financially on students, who incur their debt without current income to pay it, yet need a college degree to effectively compete in the post-graduation job market. Because at one point the federal government guaranteed many or most student loans in the U.S., private lenders eagerly extended credit to anyone who asked for it. No-risk lending is a no-brainer in the financial world.

These practices put a flood of money into the higher education system, which continually drives up the price of higher education, even in public colleges and universities. Institutions charge what students can afford to pay, and since students were paying with government-backed loans — and today are paying with government-originated loans (see below) — they become a mere pass-through from lenders to college and university administrations.

Thus the more money this “program” makes available, the higher the tuitions charged by the receiving institutions. (It’s really a racket in the classic sense, since students are coerced by the ever-increasing need for “credentialization” in an ever-deteriorating full-time labor market. Again, see below.)

A great deal of the new money that colleges and universities acquire ends up in the hands of the administrators themselves via growth in their number and growth in their salaries. At the top, many college presidents are paid like corporate CEOs, whom they consider themselves to resemble.

Paul Campos, writing in the New York Times, first identifies the “cover story,” the comfortable myth, that’s used to explain the booming cost of college (my emphasis throughout):

Once upon a time in America, baby boomers paid for college with the money they made from their summer jobs. Then, over the course of the next few decades, public funding for higher education was slashed. These radical cuts forced universities to raise tuition year after year, which in turn forced the millennial generation to take on crushing educational debt loads, and everyone lived unhappily ever after.

This is the story college administrators like to tell when they’re asked to explain why, over the past 35 years, college tuition at public universities has nearly quadrupled, to $9,139 in 2014 dollars. It is a fairy tale in the worst sense, in that it is not merely false, but rather almost the inverse of the truth.

He then shows that the truth is almost exactly opposite:

In fact, public investment in higher education in America is vastly larger today, in inflation-adjusted dollars, than it was during the supposed golden age of public funding in the 1960s. Such spending has increased at a much faster rate than government spending in general. For example, the military’s budget is about 1.8 times higher today than it was in 1960, while legislative appropriations to higher education are more than 10 times higher.

In other words, far from being caused by funding cuts, the astonishing rise in college tuition correlates closely with a huge increase in public subsidies for higher education.

If car prices had gone up as fast as tuition over the same period, he writes, “the average new car would cost more than $80,000.”

Where is this money going? Among other places, into the pockets of the administrator class. Campos notes that “an analysis by a professor at California Polytechnic University, Pomona, found that, while the total number of full-time faculty members in the C.S.U. system grew from 11,614 to 12,019 between 1975 and 2008, the total number of administrators grew from 3,800 to 12,183 — a 221 percent increase.”

To see the effect on the salaries of college presidents, the industry’s CEO class, see the charts at the top.

Part 1 in this series looked at the Why question — Why should all student loans be canceled? — and answered it in economic terms, since ending student loan debt would benefit not just the students affected, but the economy as a whole. It also answered the Why question in moral terms: Ending the practice of parasitism, humans preying on humans, is a good thing in itself.

This piece looks at the How question — How should ending student loans be implemented? A future installment, the last, will address the What Next and What If We Don’t questions. (Hint: Extreme parasitism is not a stable system, and the social consequences of extreme human suffering aren’t limited to the ballot box.)

The Federal Government Is the Largest Lender of Student Loans

A little background before we get to the implementation. The largest originator and owner of student loans is now the U.S. government:

The Federal Student Aid (FSA) loan portfolio balances were $896 billion at the end of 2012. The FSA managed $473 billion under the Federal Direct Student Loan Program at the end of 2012. New loans originated under the program during 2012 totaled $106.7 billion. Loan portfolio balances managed by the FSA for the Federal Family Education Loan Program are slowly and steadily shrinking as new loans offered to students by the U.S. Department of Education originate under the FDSL program. Most of the growth in FDSL loan portfolio balances can be attributed to new loan originations, while being the sole government program for student loans. Another contributor to the rapid escalation in loan balances is due to the cost of higher education increasing rapidly, faster than inflation. Students are spending and borrowing more to finance their higher-priced, higher education.

As of the 2015 GAO audit, the total of the Federal Student Aid loan portfolio was one trillion dollars. [Footnotes removed]

By comparison, note that the aggregate national student loan total, including both public and privately originated loans, is close to $1.5 trillion.

The percentage of private loans is actually much smaller that these numbers imply. According to a new paper by Scott Fullwiler, Stephanie Kelton, Catherine Ruetschlin, and Marshall Steinbaum, “The vast majority of [student] debt originates from federal lending, with the private student loan market accounting for just 7.6 percent ($99.7 million) of all student debt.” (More from this paper below.)

Also note that the government-guaranteed loan program, in which private lenders were the source of the money, was eliminated only recently, in 2010:

Following the passage of the Health Care and Education Reconciliation Act of 2010, the Federal Direct Loan Program is the sole government-backed loan program in the United States. Guaranteed loans—loans originated and funded by private lenders but guaranteed by the government—were eliminated because of a perception that they benefited private student loan companies at the expense of taxpayers, but did not help reduce costs for students.

So the loan guarantee program became a loan origination program. This makes the U.S. government today the major parasite driving the student loan crisis, though $100 million in private student debt is still a sizable prize for private lenders.

This also puts the U.S. government in a unique and powerful position — it can, if it wishes, solve this problem by its own action alone.

How to End the Student Loan Crisis

Part 1 of this series argued the benefits of a “debt jubilee” on all student loans in the U.S. The paper cited above also argues those benefits (see the Executive Summary). The mechanics of this cancellation, ways it can be implemented, are as follows. Note in the second bulleted paragraph how private loan debt would be handled (emphasis mine):

• The current portfolio of student loans held by the ED would be cancelled or, equivalently, borrowers would simply be allowed to stop making payments and any principal due on a given date would be cancelled at that time (that is, the loan would effectively be cancelled in stages as payments come due). As of the second quarter of 2016, the ED’s outstanding loans totaled $986.19 billion.

• The federal government would either purchase and then cancel, or, equivalently, take over the payments on student debt currently held by the private sector. As with the ED’s loans, if the government purchases the privately held loans it can choose to cancel them immediately or as borrowers’ payments come due. The government-guaranteed loans are $266.69 billion, while nonguaranteed privately issued loans are $101.58 billion, both as of the second quarter of 2016. Having the government assume these payments or purchase and cancel the loans is preferable to cancellation by private investors. The latter would require the private sector to write down nearly $370 billion in both assets and equity, which could be highly destabilizing (or worse) for the affected sectors.

Section II of the paper works out the effects of the various choices presented above. Note again that the effect on the national debt derives solely from the loan servicing amounts (interest payments), which are either lost to the government in the case of canceled government loans, or paid by the government in the case of privately issued loans. Canceling the outstanding loans balances themselves has no effect at all on the amount of federal debt.

But Wouldn’t This Disproportionately Benefit the Rich?

One of the chief objections to this proposal is that it’s regressive, that it would disproportionately benefit the rich. The authors address this concern:

The Distributional Consequences of Student Debt, Student Debt Cancellation, and Debt-Free College

…[T]he main controversy over student debt generally and debt cancellation in particular has not been its macroeconomic impact, but rather the implications for people in different income and wealth quantiles and the impact on inequality. The controversy arises from the factual observation that among borrowers, those with the largest amount of debt outstanding tend to have the highest incomes, and those who spend the most on college (and who therefore—so the story goes—have the most to gain from the option of free college) come from the highest-earning families….

This objection, overly simple and therefore easy to “sell,” fails to take into account the wholesale changes that have occurred in both the student loan population and the U.S. labor market.

The widespread criticism of ambitious policies to address the student debt crisis, based on their supposedly regressive impact, is overdrawn. In some cases, it misinterprets the evidence about who is most burdened by student debt and who would benefit most from relief. In this section, we consider the evidence about the distribution of debt and debt burdens in the population and the evolution of those distributions over time. Our main point is that, while the largest loan balances are indeed held by comparatively high-earning households, the extent to which student debt is held by the rich has diminished significantly. Moreover, the argument that the distribution of the burden of student debt has not, in fact, changed very much, even as the total amount of debt outstanding has increased dramatically, fails to consider the significant changes in the population of people with any student debt at all. These issues of interpretation extend beyond accurately assessing the distributional impact of the policies we model—they point to larger problems with the assumptions behind existing higher education, student debt, and labor market policies. The student debt crisis is one of several linked manifestations of those problems. Others are wage stagnation, underemployment, and increasing inequality of household wealth.

Student debt was once disproportionately associated with graduate school and with relatively well-off households, in part because it was possible to graduate from community college or a four-year public institution with little or no debt, and in even larger part because many people did not need to obtain any higher education credentials in order to access the labor market. What has happened in recent decades, and especially since the mid-2000s, is a vast expansion of student borrowing, such that the preponderant share of younger cohorts newly entering the labor market carry student debt. This expansion is due in part to much higher tuition, mostly thanks to state-level cutbacks in funding for higher education, and in part because it is simply far more difficult to access the labor market now without higher education credentials. And that “credentialization,” in turn, is due to the underperformance of the labor market since 2000 and especially since the financial crisis and the Great Recession that began in 2008. Since 2000, the most important federal labor market policy has been the extension of student debt and the encouragement of a larger share of the population to obtain debt-financed higher education credentials, on the theory that underemployment and stagnant wages were caused by a “skills gap” that could be remedied through debt-financed higher education. The most obvious and acute effect of that policy was the growth of the high-priced for-profit higher education sector, but it was also evident in rising enrollment across all types of institutions, even as tuition rose. The “skills gap” was a false diagnosis of the labor market’s problems, and hence the prescription of more debt-financed credentials not only failed to solve the problem, it also created its own problem in the form of unsustainable debt.

The bottom line is this: Student debt today is killing a generation in a way it didn’t before. This is new and not a function of loans to students born of wealthy parents. It’s a societal and generational problem, actually a multi-generational one, that hurts us all. The economic harm done to an entire generation of Americans is not captured by the objection that this is somehow a “regressive” proposal.

As the authors note, there’s more in that section of the paper in support of these claims.

The Need for Debt-Free Public Higher Education

It’s clear that this proposal, in my view necessary, must also be accompanied by the Sanders campaign proposal of debt-free public colleges and universities. The arguments for Sanders’ proposal, on its own merits, were well explored during the campaign.

A major objection to Sanders’ idea was again that it would mainly benefit the rich — an argument that ignores, disingenuously I think, the fact that the very wealthy do not send their children to public colleges and universities. Harvard University would not become tuition-free under Sanders’ proposal.

But in the context of the current proposal for cancellation of all student debt, there’s another reason for instituting debt-free public colleges and universities: moral hazard. Briefly, canceling debt without removing the reasons debt is incurred in the first place encourages reckless borrowing in the expectation of future cancellation.

The authors address the problem this way:

The primary theoretical criticism of debt cancellation plans focuses on the reaccumulation of debt following the cancellation, in particular the potential for problems of moral hazard to arise. From this perspective, debt relief today could change the incentives of future student debtors who may increase borrowing with the expectation that the loans will be forgiven, causing an even faster accumulation of debt and increasing the negative consequences at the household, local, and macroeconomic levels. The perverse incentives for unsustainable borrowing in this scenario are the result of inappropriate policy institutions that absolve borrowers of their debts while perpetuating the necessity of increasing debt. In order to avoid problems of moral hazard, any restructuring of student debt—including our debt cancellation proposal—should be accompanied by strong and appropriate policies that enforce the consequences of borrowing and address the market failures that lead to undesirable social costs. In combination with debt cancellation, publicly funded free or debt-free college would provide the institutional reform.

In combination with a program like the one Sanders proposed during the campaign — free public colleges and universities — student debt cancellation would indeed and effectively address the current student debt crisis. The two proposals are a necessary pair and should be implemented together.

Finally, the “Fairness” Question

Which brings us to the last of the objections. In effect, it comes down to this: “I paid for my college degree with my hard work and sacrifice. I paid off all my loans, and believe me it was tough. But I did it. So why should others get a break that I didn’t get?”

The problem here is what one writer described as “status quo bias,” an emotional preference in which the “current baseline (or status quo) is taken as a reference point, and any change from that baseline is perceived as a loss.”

but there’s another bias as well, which could be called “retributional bias.” This situation is similar to any in which an originally beneficial policy was first rescinded and then reinstated. Public education was largely free prior to the Reagan era, and with the GI Bill, millions paid next to nothing to attend. As the paper’s authors point out, the largest loan balances were associated with post-graduate work.

But higher education policies changed under and after Reagan, reaching crisis proportions today. Should people trapped in debt by the blatant injustices of the post-Reagan world be allowed to veto, in the name of “fairness,” the repeal of those injustices?

The essence of this objection is, “It’s not fair that I was born at the wrong time.” This has been described as being “trapped by history.” Is it unfair that many be so trapped? Of course it is. But the perp in that unfairness is not the next generation to also be shackled, but the times themselves, the politicians who ruled them, and voters who kept them in power.

To therefore perpetuate that unfairness — to make, in effect, this generation suffer “because I had to” — is more than just unfair to them. It’s cruel.

Bravo!!!. I applaud this series of articles with the four hands god gave me!!! There is so much to comment, but just to bites that called my attention:

1. There is an internal “contradiction” in this article that I hope someone can clarify. At the beginning the author cites Paul Campos on the NYT writing:

Later on cites Fulwiller et al writing:

Is it that federal increases do not compensate state-level cutbacks?

2. Somehow the financialization scheme of higher education demonstrates how rigth are MMTers. The Federal Government can easily issue debt for 1 trillion dollars of student debt without any supporting collateral. (But weirdly cannot subsidize higher education?)

I like very much the term “credentialization” to explain the exploitation scheme created to squeeze the youngers before they start to produce as opposite to the “skills gap”, so many times invoked. It may be too long but I would consider the use of “over-credentialization”.

It’s possible that the “public investment” that Campos mentions includes the increases in debt taken on by public universities and other non-state (tuition, private, federal) funding sources that have ballooned budgets. Private / NGO funding is no longer trivial at public schools. Investments in higher education are “vastly larger” even as state support declined.

A related issues I would like to see some more discussion on is that University endowments pay out more in hedge fund and private equity fees than they pay out in scholarships

http://hedgeclippers.org/endangered-endowments/

Yes yes yes. It is the endowments who need to foot the bill for anything like this. They need to take the pain. Otherwise it becomes an issue of “MY TAX DOLLARS” and “BAILOUTS”.

I think many people fail to realize how almost obscenely wealthy some of these endowments are. In some cases they could fund university operations for centuries going forward!

Just allowing for a process where there is an actual negotiation on student debt repayment would be a huge plus. Right now there is no way to make a deal on unpayable debts, and the creditors know it.

1 – Totally agree this would be a great thing

2 – Will never, can never happen in this country ever.

Far too many way-too powerful constituencies with a finger in this pie. Both halves of the monoparty would find reasons to oppose it. You’d have the entirety of the higher ed sector throwing its billions at the blue Republicrats, the financial services sector throwing money at both the blue and red ones, and the easiest possible political message to sell to normies.

Red normie: well look at all those people who took student loans out with no intention of repayment who get a bailout from MY TAX DOLLARS (echoing exactly the common 10 y. ago nonsense about all those minorities taking out mortgages they can’t afford and never intending to repay them)

Blue normie: this is anti-education! Mean-spirited Ayn Raynd worshippers types wanting to take away access to EDUCATION from the disadvantaged! Who’s going to loan them money now? They don’t have rich parents who can just borrow money.

The contra argument being that so many of “the young” would be in favor. Well “the young” tend not to be in favor of endless permanent war and look how that has gone for more or less forever now.

Again, there is puzzlement about the federal role in funding higher education and in enforcing repayment of student debt. The whole system is as it is now because it does punish the young, shackling them to crushing debt. Please note that student loans are no longer dischargeble in bankruptcy court. This is not an accident. Students tend to vote Democratic and/or be more liberal than the general population. Hint, hint.

The student protests of the 1960’s have vanished, even though war atrocities abound. Add climate change and various other ecological disasters and there are even more reasons for students to be protesting the transformation of their futures into profits now, but … nothing. (Remember when students changed themselves to old-growth trees to stop their felling? Surely climate change is a more dire situation.) The reason is students have been defanged by their debts and their bleak job prospects.

This is why the current administration will take no action in this direction. They like things just the way they are.

Except that….it was Joe Biden who made student loans non-dischargable.

B Carson

I doubt that he did it alone, but he certainly led the charge (pun intended).

S Ruis

Change themselves in to old-growth trees? Zap. That’s a sappy thing to do in any era.

Your typing is like mind in that reegaard.

Some students are still not afraid to look at the world and express themselves through protest, but being frightened into blind obedience has unfortunately been so inculcated in the young (or distraction by the pleasure palaces in the cellphone) that obedience has become virtually an unwritten line on most university applications.

How to end student loans:

Make them subject to discharge through bankruptcy.

The end.

Are you suggesting that the US taxpayer should pick up the tab for the decades long spree of greed of:

1. Banks

2. Credit card companies

3. College and university administrators and trustees

4. Politicians who got re-elected promising college for all and easy loans

Jim, taxpayers don’t fund governments that can issue their own currency. Those governments are self-funding. (Money must be spent into existence before the first tax dollar can be collected.)

In these situations, taxes perform other functions. They:

1. Establish the government’s currency as the only one that most citizens will collect.

2. Remove money from the money supply when the economy heats up too much.

3. Balance social goals — for example, by feeding some parts of the economy and restricting funding to others. Other social goals can include enabling or preventing “rule by the rich,” etc.

GP

Gaius and others – I realize that this will seem heretical to the MMT true believers here, but historically, the “fiat currency means governments are self-funding” meme hasn’t worked out real well.

Once taxes no longer cover the bulk of expenditures, faith in the value of the currency is lost. Also, the excess expenditures lead to runaway inflation.

Politically, it’s inevitably too tempting to reach for the “free candy” spending option, rather than submit to the discipline of a balanced budget or the “punishment” required to raise taxes somewhere. Pension benefits are a particular example of subtle spending – easy to promise, hard to deliver.

One only has to look, globally, at the evolution of national/state/local government debt/GDP ratios since the end of the gold standard in the 1970s. To the best of my knowledge, the only time any nation ever came back from this level of excess debt/GDP (or “self-funding” / “actual economy”…) was Victorian England.

Municipalities rarely went bankrupt in the past, but it’s been abundantly clear for a decade that the path we are on ends only in tears, and the only question is how much longer the can can be kicked. Puerto Rico and a few cities in California ran off the rails already, and Illinois/Chicago are not far behind.

Worse, all that debt leads to over-financialization of everything in the economy, which is unhealthy in far too many ways, including the much-decried wealth inequality that is critiqued here often. By definition, one entities’ debt is another’s asset. When debts are issued and then owned (and interested collected) by a few centralized entities, cronyism and inequality are inevitable. Worse, the debt-holders need do no work whatsoever, forcing the rest to serve them despite their lack of productive labor.

In short, I think MMT is like Marxism – a fundamentally valuable critique of the prior system, and ideal in theory, but utterly hopeless in practice because it presumes too much goodness in human nature.

The human cost of the post-gold-standard financialization tragedy has yet to be established, but it will be tremendous.

With all due respect, I still think you have to fix the problem of the cost of higher education first, then forgive the student loans. Otherwise, you’ll end up with another $2Trillion in student loan by the end of a decade of the jubilee.

Exactly, ya beat me to it, here is comment I composed offline before seeing yours:

Making public colleges and universities free, as proposed above, fixes the cost of public education.

GP

Just as long as they adopt Sanders’ plan and not Clinton’s (that Sanders started promoting after his defeat). We don’t need to pit the haves vs. the have-nots. Free public college for all, just like we have free K-12 public education.

I have a quibble with this article (and many others that omit the same relevant info).

It states: “… over the past 35 years, college tuition at public universities has nearly quadrupled, to $9,139 in 2014 dollars.”

Is that tuition amount for a single semester, or for a full academic year (2 semesters) or for 4 years?

Semester: http://registrar.berkeley.edu/tuition-fees-residency/tuition-fees/fee-schedule

My God. I had no idea how crazy the tuition had become!

In state tuition and fees at the University of Colorado runs about $15,000 per year. And that doesn’t include room and board.

The instant any discussion begins of implementing a material benefit to the middle or working class, a horde of people crawls out of the woodwork protesting that they themselves will not benefit from it, with sotto voce complaints about “paying for” a benefit to others, and suggestions the money should be forwarded somewhere more deserving, presumably their own pockets.

I observed this phenomenon ad nauseam during the housing crisis whenever there was any mention of alleviating the fraudclosure epidemic. No wonder Obama did nothing for homeowners — he knew we’d be too busy ripping each other apart to come after him.

Heaven forbid anybody in the working class see a couple of pennies from a reform. Let’s all tear each other apart while the 1% swarm past us with wheelbarrows of loot.

great point, can’t be made too often

Obama did nothing for the homeowners because we didn’t have yachts and private islands he could play on when his little stint was over.

Student debt deserves a jubilee just as the homeowners deserved one.

The ultimate parasite, athletic coaches.

Look up what they are paid.

What do they offer in return? A chance for steroid monsters to better throw a ball back and forth and attract more donations to the school from sports bedazzled graduates?

Is that the mission of a university?