We had hoped to leave CalPERS alone for a bit, but a new Wall Street Journal story confirms a post we published earlier this month. We discussed how the fees for its private equity scheme that CalPERS presented to the board as if it were a great deal are in fact so high as to amount to a roughly $80 million payday, per new fund, per year, for the fund owner(s).

It was alarming to see the architect of the private equity plan, John Cole, so badly mislead the CalPERS board. It says he is either utterly clueless or complicit in a plan to loot CalPERS.

Recall that the centerpiece of CalPERS’ plan is to set up two new fund management efforts, one of which would operate a “late stage venture capital” fund, the other which would run a “Warren Buffett style fund”. Buffett, if he had deigned to take notice, would vehemently disagree with the claim. This industry fad for marketing funds with longer holding periods bears virtually no resemblance to how Buffett invests. As his just-released annual shareholders’ letter makes clear, Buffett looks at taking 5-10% stakes in public companies along side evaluating acquisitions of entire companies. Buffett is also willing to sit pat if there are no investments at what he regards as good prices (and his black eye with Kraft shows he can get it wrong). He hasn’t bought a big company in the last few years and warned he might not this year either.

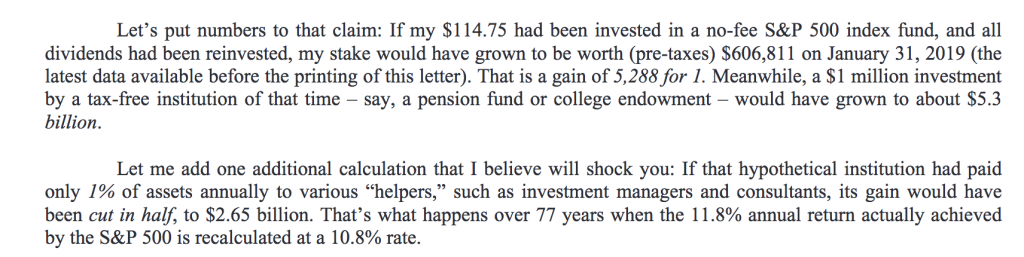

Most important, Buffett is allergic to paying fees:

Yet CalPERS being so willing to continue to overpay to invest in private equity, and on top of that, even when it admits that the “Warren Buffett strategy” fund will underperform conventional private equity funds. This makes no sense, yet staff keeps prattling on to the captured board that this sort of destruction of value is necessary and desirable.

The Journal’s story, BlackRock’s $12 Billion Bid to Become a Private-Equity Giant Is Behind Schedule, recounts how the giant fund manager has pinned its efforts on launching a mega “Warren Buffet style” fund as its apparent first major offering. Attentive readers will recall that BlackRock had been courting CalPERS hard. Bloomberg broke a story in September 2017 that CalPERS was in secret discussions with BlackRock about outsourcing their entire private equity program to BlackRock. Caught out, CalPERS tried putting lipstick on that pig via a sham beauty contest designed to favor BlackRock. The plan then was for CalPERS to put a big chuck of its monies in a private equity funds of fund program. That idea was indefensible by virtue of having CalPERS pay an unnecessary layer of fees, which as Buffett underscored above, takes a big bite out of returns over long periods of time. That plan fizzled out. CalPERS management quietly abandoned it; the scuttlebutt is that BlackRock sought fees so much higher than those of the other bidders as to make it impossible to go forward (raising the obvious question of why CalPERS didn’t proceed with one of the others on its overly short solicitation list if this was actually a good idea, as CalPERS staff had maintained to its board).

The Journal story by Dawn Lim is germane to CalPERS not just for showing how ludicrously rich the fees are for the deals CalPERS wants to strike for its new fund, but separately how other major investors are balking at the idea of committing large amounts to an untested private equity fund manager.

Bear in mind that new private equity funds housed in BlackRock would pose far less startup risk than the ones that CalPERS is trying to set up. BlackRock is providing lots of managerial support: accounting, compliance, office space rental, equipment purchasing, and so on. That means the professionals aren’t burdened down with administrativa that would distract the leaders of the CalPERS funds.

But even with the BlackRock imprimatur, the dogs don’t want to eat the dog food:

BlackRock Inc. in 2018 set a goal of raising at least $12 billion to buy and hold long-term stakes in companies, replicating the approach of Warren Buffett. The world’s biggest money manager is still waiting for its first check…

But an experiment with private equity is proving to be a tough sell for some investors. A major Chinese sovereign-wealth fund and the state investor for Alaska’s oil wealth passed on a new BlackRock fund known as Long Term Private Capital, according to people close to those organizations. Florida’s largest public pension fund and Minnesota State Board of Investment are in talks with BlackRock, but no deal is done, said people close to those institutions.

BlackRock officials now hope to secure initial funding later this quarter after missing internal deadlines in 2018. The architect of Long Term Private Capital said the launch has taken longer than expected partly because of the fund’s unusual approach. Its fees are cheaper than many in the industry, but it doesn’t have a deadline for returning money to investors.

Help me. Some big brand name private equity funds managers, such as KKR and Carlyle, have been able to cash in on the “Warren Buffett style” fad. But they didn’t refuse to give an expected fund horizon as BlackRock has, nor did they seek to raise such a presumptuously large amount of money. From the Financial Post in 2017:

A few years ago, private equity managers were growing tired of sitting on the sidelines, watching Warren Buffett’s Berkshire Hathaway make landmark investments in Kraft Heinz and BNSF Railway. They wanted to get in the game.

Stop here. The invocation of Kraft should serve as a big red flag. Back to the story:

So a few of the biggest names in the industry, Carlyle Group, Blackstone Group, and KKR, set about building their long-duration private equity businesses, hiring teams and raising multibillion-dollar funds (or forming long-life partnerships) to buy companies that are projected to perform well over a longer time frame than the short hold period of a standard buyout fund.

Let’s stop again. The difference between the target holding period for these newbie funds (the article cites ten years as a typical expectation) is actually not that much longer than that of a “standard buyout fund”. While the period of ownership once averaged four to five years, post-crisis, the norm is now six years. Back to the article:

In 2016, Carlyle raised $3.6 billion for its long-dated Carlyle Global Partners fund…Carlyle has so far struck six deals for the long-duration fund…

Blackstone Group LP has raised $4.8 billion to date for its long-term fund….

European firm CVC Capital Partners closed a $4.4 billion pool for a long-term strategy, with backing from the firm’s part owner, the Government of Singapore Investment Corp.

KKR & Co., whose co-founder Henry Kravis in 2009 described Berkshire Hathaway Inc.’s style as “the perfect private equity model,” is also dabbling….

The field is largely limited to these big players, the industry’s precious few household names with a track record and bench of players deep enough for investors to trust them with their cash for two decades. “I think it will be a very limited number of people who can raise a fund of this duration,” says Jim Treanor, head of North America advisory services for Pavilion Alternatives Group LLC.

Aside from the risks of being locked to a manager long-term, being held by a private equity firm for an extended period could also affect the portfolio company’s performance and investor returns, according to Treanor. “It’s hard for one GP to be able to continually add value at every stage of that development of the company,” he says. “It’s going to be the bigger GPs that have bigger networks and a variety of value-add” tools…..

And at a time when many investors like U.S. public pension systems are struggling to meet their expected rates of return, accepting lower returns — even in return for long duration and lower fees — isn’t appealing for everyone, he says.

Notice what is supposedly takes to succeed at this sort of investing (not that anyone has been at it long enough to be deemed a success): a big firms’ wide-ranging network and their extensive skills. There is no way that the small team that CalPERS plans to set up will have that.

And investors aren’t persuaded that even a mega-firm like BlackRock has the chops. The fact that it has been flogging this fund for so long and has not a single bite is damning. The target for fundraising for 2018 was $4 billion, and let us not forget that this is a white hot market for private equity. Nevertheless, BlackRock CEO Larry Fink says he’s not deterred and doesn’t see “the speed of a first close” as critical.

Notice that the Financial Post story pointed out that lower funds are a standard inducement for this strategy. It’s a sop to investors to compensate for the lower expected returns. But it still works for the fund professionals. By doing deals much less often and by begin spared raising funds every four or ive years, these long-term funds can operate with far fewer professionals than a similar-sized conventional fund. The Journal report seemed unaware of this design factor, and treated BlackRock’s fees as a special inducement, as opposed to a norm for this approach. From the story:

Long Term Private Capital is offering to charge clients a management fee below 1%, and 10% of profits, and its management fees would fall as the fund gets bigger. Private-equity funds across the industry charge clients a 2% management fee and 20% of profits, according to median figures from Preqin.

Lim is doing readers a huge disservice with this comparison. There are many very small private equity funds. The median size is on the order of $300 million, and for a fund of that size, a 2% management fee is reasonable because it corresponds well to how much it costs to run the business. But if you were to dollar weight the average, it’s way higher, and the corresponding typical fee levels would be lower. And that’s before you factor in that mid-sized to mega funds offer tiered pricing, with larger commitments getting lower fees.

With this long-winded introduction, let’s return to a February 5 post and see how the Journal has validated it:

Cole slipped his announcement about the crazy-high costs past the board using a tried-and-true tactic of investment managers when they are trying to obfuscate the fees, that of using percentages rather than mentioning any dollar amounts. Here is Cole’s response to a question from Steve Juarez, who was acting as the representative to Treasurer John Chiang. From the December transcript:

Investment Director John Cole: What that leads to is that in an early environment, or an early term of setting up the entity, when assets are relatively small, let’s say a billion or $2 billion, relatively small in CalPERS sense, that the percentage of that amount will be high. And that as that matures over the course of a few years, then it — that and that becomes a much lower percentage. So that by the time we get to, say, $5 billion, that the equivalent of that percentage to the 2 and 20 world is pretty close.

By the time you get to $10 billion, it’s about half — half of what we would be paying otherwise. And all of that is going to be subject to exactly how the calculation

Recall that the management fee is the biggest fee that private equity fund managers receive and that they get it regardless of how the fund does. It is prototypically described as 2% of the amount committed, but in reality, the level is much lower on large commitments, and the $5 billion per fund here is off the charts in terms of size.

Cole says that the applicable percentage varies with the size of the asset base but is 2% when the asset base is $5 billion dollars. Note that two percent of five billion dollars is $100 million, so Cole is saying that the management fee at that point will be $100 million. He then goes on to say that the management fee is roughly half the 2% at $10 billion dollars, which would be 1%. Again, 1% of $10 billion is $100 million. Note how Cole emphasizes the reduction in fee percentage as if these are actual cost savings, when the reality is that the formula will cause the total dollars paid by CalPERS to remain flat. And recall that Cole notes in passing that the percentage will be higher before the $5 billion level is reached, so the management fee in dollar terms may well be near or at $100 million from very early on.

The excessiveness of a two percent management fee on a single investor committing $5 billion dollars is obvious from the fact that, as we’ve already discussed, CalPERS’ peers (as well as CalPERS itself) routinely pays 1.0% to 1.25% management fees for much smaller commitments of around a billion dollars, and survey data supports that conclusion.

But showing either cheekiness or ignorance, Cole justified the absurd fee amount by claiming that, in essence, CalPERS had looked at a proposed firm operating budget of the investment managers and was satisfied that the $100 million was necessary to run the businesses on a lean basis:

Cole: In our construct, in our belief, we will be — go back to the original purpose [of a management fee] and provide the cost and expenses necessary to run the business on an agreed-upon operating budget. So that operating budget would be made up of compensation, that’s comp — this is salary-type compensation, or base compensation — and then as well as those costs associated with running the business – rent, travel, engagement of outside people to help in deal making. And that that number will be in place of a management fee.

This claim is laughable on multiple levels….

The post continued to debunk Cole in detail; please read the full treatment if you have time, since it gives a peek into private equity firm economics.

But all you need to remember is the bottom line.

BlackRock is offering a similar fund with management fees of less than 1% and they get even lower over time. By contrast, for a ginormously larger commitment, CalPERS is paying more than twice as much in the opening years and still more even at year 10.

CalPERS should be getting rock bottom fees, and that means lower than any in the marketplace, not just by virtue of its huge commitment but also by virtue of paying the startup costs

CalPERS’ teams won’t have the deal flow of a KKR or Blackstone, and it’s unlikely even to have the deal flow of a BlackRock, and they won’t have that level of institutional support either. That would argue for an even lower management fee and more in carry fees.

Of course, it’s possible that this whole cockamamie scheme is just a big show to give CalPERS an excuse to again try to hand its private equity business off to BlackRock.

Sigh. CalPERS really is the damaged Terminator of the Pension sector, isn’t it? By that I mean that ‘It can’t be bargained with. It can’t be reasoned with. It doesn’t feel pity, or remorse, or fear. And it absolutely will not stop, ever.’ Only thing is, it is damaged so it can never shoot straight either. Look, being a helpful sort of guy, I have decided to lend my expertise to them for their investment strategy and only charge a nominal fee. All they have to do is invest in the following corporations-

Lockheed Martin

Boeing

Raytheon

BAE Systems

Northrop Grumman

General Dynamics

Airbus Group

Thales

Leonardo

Almaz-Antey

Why them? Because they are the world’s 10 biggest defense contractors and I am sure that we can agree that weapon sales are not actually decreasing over time. For this advice I will only charge them my minimal one million dollar fee. In small, unmarked, used notes to be deposited into my Cayman Islands account please. I will even forgo the obligatory hookers and blow for this job. Actually, I can see that CalPERS made a standard rookie error in working out the terms of their investments. Fellas – the hookers and blow is for after the deal is finished, not while you are doing the actual work. Hmphh. Newbies!

Of course with this strategy they will have to do an Amazon and set up a second HQ in Virginia with an office in Washington DC and a house in the Hamptons for entertaining clients. The purpose of this office is of course to allocate, ahem, ‘resources’ to the right people in Washington for successful outcomes. Actually another office in New York City would not go astray ether. There! Now how hard was that! Glad to be of service.

I seem to remember Buffett giving some assistance to Goldman Sachs or one of the other big banks during the financial meltdown on terms that were extremely favorable to Warren Buffett, in sharp contrast to the terms these banks got from Uncle Sugar.

Thanks again for keeping the heat on CalPers.

Funny how WSJ failed to mention Calpers at all, did they fail to connect the dots?

I imagine Mr Cole will have splaining to do at the next board meeting, hopefully itll finally be apparent to all that he’s truly “ out of his lane”

I’m still wondering who the hell is benefiting from all this at CALPERS.

Someone is stuffing their mattress with this carp.

Not mutually exclusive!

We’ll never know the other bids submitted when former CIO Ted Eliopoulos (now evidently collecting a sinecure at Morgan Stanley) was forced to put this very BlackRock strategy, that he was apparently attempting to pitch to CalPERS, up for competitive bidding — but I must suspect that they were even lower than “1 and 10,” given how quickly Ted and since-defenestrated Board president Priya Mathur were saying “never mind” about it. The CalPERS Direct “2 and 20” nonsense is tantamount to a criminal misappropriation of public funds — and adopting it would be a violation of fiduciary duty through waste of assets per se.

Thanks for writing up this WSJ coverage!

Yes, the thought later occurred to me that the two options weren’t mutually exclusive, so thanks for highlighting that.

I went back and read the Forbes report about the Buenostro conviction; the gist of that particular story was CalPERS staff is paid too little in comparison to peers in the rest of big fund management world, so somehow ‘naturally’ the inclination to cheat will be almost irresistible, and therefore these problems could be eliminated if the pay was higher – a debatable position.

One thing I’ve noticed is that management at CalPERS has gotten worse under Dem control of the state govt. I’m not talking about the finances, subject to the swings in the market. I’m talking about the management. An odd situation, considering the Dems are supposed to care about working people having a decent retirement.

Thanks for your continued reporting on CalPERS, PE, and pensions.

Arnold Schwarzenegger was governor when Buenrostro was appointed CEO. Can’t blame that on Dems

Fred Buenrostro was appointed CEO of CalPERS during the administration of Democrat Gray Davis. Davis was Governor of California from January of 1999 until his recall in November of 2003. Buenrostro was appointed CalPERS CEO in December of 2002.

Buenrostro was pushed-out as CEO in 2008 during the governorship of Arnold Schwartzenegger, after staff complaints of “unprecedented levels of meddling in investment decisions.” The investigation of Buenrostro and Villalobos was conducted during Schwartzenegger’s administration, but then-Attorney General Jerry Brown only pursued civil violations until the SEC and the U.S. DOJ stepped in.

So we can blame that on the Dems.

I stand corrected. However, the truth is in neither case did the governor control the decision.

I dont like Comments fights, but I was a labor official lobbying CalPERS and Governor Davis during 2001-2003, and I personally knew him.

The governor directly appoints two board members, and controls two others — Dir of Dept of Human Resources and the rep from the State Personnel Board; the ex officio State Treasurer and State Controller usually defer to the governor. The governor wields quit a bit of influence over the CalPERS board’s decisions. I don’t personally know how much influence Davis had over Buenrostro’s appointment, but he had to have approved of it.

Sadly, Davis had much to do with how CalPERS lost its way when we all thought that the Tech-Bubble had “super-funded” the plan.

https://www.sfgate.com/politics/article/CalPERS-invested-700-million-with-Davis-donor-2817740.php

The problem was that the cheating was at the CEO level, and the CEO didn’t come out of the money management world. He was a political hack. So it’s hard to see how this squares. Buenrostro cheated because a big bribe was waved in his face.