The ten year-old CalPERS CEO bribery scandal has abruptly resurfaced in an ugly fashion, as the Wall Street Journal indicates that one of the investment firms tainted by the scandal did not pay the full restitution promised to CalPERS

CalPERS’ former CEO, Fred Buenrostro, is now in Federal prison serving a four-and-a-half year sentence for taking bribes from a placement agent and former board member, Al Villalobos, who received a mind-boggling $58 million in fees from Apollo, CIM, and three other investment managers close to Apollo. Villalobos killed himself rather than face trial.

Buenrostro and Villalobos paid for their crimes. But it looks like the firms that greased their palms came out ahead. Not only did they not return the placement agent fees as CalPERS had demanded, but CalPERS didn’t even put them in the penalty box and refuse to do business with them for a set period of time as punishment.1

Instead, CalPERS entered into agreements with each of the five firms stipulating that they’d make it up to CalPERS…..by giving them future fee breaks. Not only did that have the effect of inducing CalPERS to do more business with firms that abused them, but the agreements shown to the public were mere napkin doodles. If this was all CalPERS got in the way of formal commitments, they were obviously setting themselves up to be cheated, as we pointed out when we first looked at the pay-to-play scandal in 2014. And as we’ll discuss, even better documentation wouldn’t save CalPERS from being fleeced via the ruse used to short change them, one used pervasively in the private equity industry.

A Wall Street Journal story published earlier this week, on CalPERS firing CIM as the manager of a major Sacramento development project, 301 Capitol Mall, explains that among CIM’s sins were that it still owed $41 million on a $50 million agreement from 2010. The Journal authors Heather Gillers and Dawn Lim missed the significance of their find. The amount due clearly came out of CIM’s pay-to-play settlement, a fact we subsequently confirmed.

This revelation also raises red flags as to whether the other four firms wound up giving CalPERS anything close to the amount they’d promised. As we wrote in August, there’s good reason to think the biggest abuser, Apollo, also paid CalPERS less than it promised.

This embarrassment illustrates how powerful and in the case of CalPERS, supposedly sophisticated private equity investors aren’t willing to be hard nosed when in any other area of finance, it’s the money that calls the shots.

Background: The Pay-to-Play Scandal and New Information About CalPERS’ Settlements

…placement agents had to get written acknowledgments from fiduciaries like CalPERS of the fees paid by general partners. Indeed, many GPs insist on having the documentation in hand before paying the fees.

Villalobos used his personal relationships with Buenrostro and a CalPERS board member, Charles Valdes, who got improper political donations from Villalobos’ firm, to get them to lean on the investment team on behalf of his clients. It was also Buenrostro who signed the waivers without notifying the board as required. In two cases, the waivers were on crudely doctored-up CalPERS letterhead and dated after Buenrostro was no longer with the giant pension fund. There were other sordid chapters, like improper gifts and flights on private jets, but the real juice was in the coverup of the massive fees paid to Villalobos.

When the scandal broke in late 2009, CalPERS hired a Los Angeles law firm, Steptoe & Johnson, to investigate…. Philip Khinda was the Steptoe partner that ran the investigation and prepared the report.

Insiders who participated in the investigation said that Khinda was calling the shots. He insisted that CalPERS get all the placement agent fees back from the Apollo and the four other fund managers so as to avoid any implication that CalPERS had supplied the funds used to bribe its CEO.

The private equity staff called Leon Black at Apollo and told him that it was very important to the relationship that Apollo return the placement agent fee.2 Black said no. Khinda then told the Chief Investment Officer Joe Dear to call Black and tell him he needed to give the money back. Black again said no.

Khinda and CalPERS General Counsel Peter Mixon then flew to New York to meet with Leon Black. They were again rebuffed on their demand for a cash payment. Black countered with a proposal to rebate a bigger headline number than the amount CalPERS sought out of fees on future funds.

Of course, this sounds too good to be true because it was. If you think Leon Black ever gave someone he owed $100 twice as much for the hell of it, you probably think used car dealers are your friends too. The offer of more in face value in on the come fee breaks was a de facto admission that these future rebates are worth less that cold hard cash.

Moreover, Black’s response was a bog standard ploy in private equity for general partners to escape paying money to limited partners when the money is contractually owed. For instance, fund agreements often provide for clawbacks, such as when the private equity firm collects carry fees on early deals that do well, but the later sales are such dogs that the total carry fees are an overpayment.

Of course, private equity firms just about never send money back. But if an alert limited partner notices they’ve been shortchanged, the general partner offers to make it up on the fees on a future fund. Stay tuned, we’ll explain the three card monte shortly.

CalPERS Admits It Was Short-Changed by CIM

From the Wall Street Journal article Calpers Switches Developers for Sacramento Project:

Sacramento officials cheered its decision last year to move forward with a plan by real-estate developer CIM Group for an office-condominium-retail complex that would have been Sacramento’s tallest tower.

But an outside consultant recently expressed concerns about CIM’s performance for the California Public Employees’ Retirement System in a review, said people familiar with the matter. The real-estate developer has failed to deliver as much as $41 million in rebates that were negotiated as part of a nine-year-old agreement.

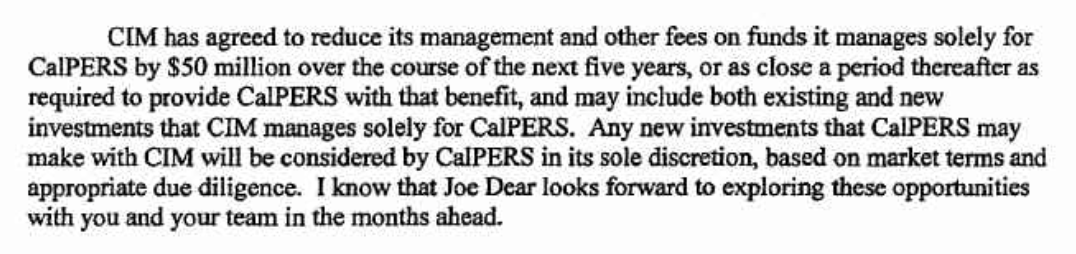

CIM maintains it gave CalPERS every break it was owed. That is hard to square with this section of what might charitably be called a letter of intent between CIM and CalPERS (see pages 74 and 74 of the document embedded at the end of this post):

One might reasonably wonder why an agreement that structured to give CalPERS $50 million in rebates in five years could possible have been adhered to, as CIM claims, yet come up so short.

The Management Fee Offset Three-Card Monte

CIM was managing real estate funds, not private equity funds, for CalPERS, but the practices are likely to be similar. The extract above makes clear that only funds that CIM manages solely for CalPERS are eligible.

Confusingly, there are quite a few types of fees in private equity and real estate funds. The fees in question are management fees, which are the biggest single income stream for private equity and other alternative investment managers. “Carry fees” are a distribution, not a fee, and thus not part of this equation.3 Another type of fee, and the one that is most opaque, is the money paid portfolio companies, or in this case, by particular real estate projects to CIM, Apollo, or other investment managers. These fees are pocketed by the investment managers and the managers are supposed to then turn around and reduce the management fees paid by the investors commensurate with what they collect. Because the private equity general partner cleverly defines the rebates as applying only to fees at the fund level, and these fees occur at the company/project level, they would not be eligible for rebates even though they too come out of the investors’ pockets.

So what’s wrong with this picture?

The original sin of private equity is investors agreeing to funny money credits for activities that that they have no ability even to monitor rather than cash payments or prohibitions of managers sucking money out of portfolio companies or real estate projects in this fashion. This leeching provides no benefit to the investors, since the money could otherwise be distributed to the investors as dividends or invested in company operations.

At some point in the dim recesses of history, private equity limited partners woke up an realized that even though they were paying “management fees” for the privilege of having the general partner take their money, as in buy, supervise, and sell companies, those sneaky general partners, who controlled those portfolio companies, were also paying themselves more fees directly from the companies.

In recent years, it’s become an open secret that despite the promise to rebate these portfolio company fees to investors, they are a scam. Even Bloomberg’s Matt Levine, who generally depicts financial services industry abuses as “nothing to see here, move along,” acknowledges these fees aren’t legit:

The basic idea is that private-equity firms charge their portfolio companies a “monitoring fee” for … monitoring them? It seems silly to insist on a reason. They charge the monitoring fee to get more money. They could charge portfolio companies a Fee For Being Nice Guys, and the portfolio companies would cheerfully pay up. The way private-equity firms work is that they buy portfolio companies with money provided by their limited partners (pensions and other big institutional investors), and then run those companies on behalf of the limited partners. So the private-equity firms are the (effective) owners and managers of their portfolio companies. They can send a portfolio company a bill, and then send themselves back some money. The guy sending the bill is also the one paying it, but with the limited partners’ money. You can monitor, or you can not monitor, but either way you charge a monitoring fee, because the emphasis in “monitoring fee” is solidly on the word “fee,” not the word “monitoring.”…

This all sounds like a racket, and it is a racket, but to be fair it is a well-known racket of private-equity investing, which is that the private-equity firms keep dreaming up amusing fees to charge to their investors and portfolio companies, and the investors keep discovering those fees….

When investor found out about this embezzlement, they didn’t do what most functioning adults would do, which was insist the private equity firms cut it out. No, they let the private equity firms talk them into….drumroll…rebating those portfolio company fees against the management fee. 4

Thus is seems probable that CIM reduced its management fee greatly by taking more in fees from projects that were then offset against the management fee than CalPERS anticipated. In other words, the general partner took more fees out of a pocket where the fee rebate would not apply and would reduce the fees that were eligible for rebates. 5

If CalPERS did enter into detailed agreements stipulating how the fee rebates worked, it’s possible that they were subject to an additional type of bait and switch. Private equity firms have devised fiendishly formulas for crediting the rebates that result in many such credits never being applied. An analogy from everyday life would be receiving a coupon for a ten dollar discount on a product. The ten dollars is a “fee offset,” but it will expire useless if you never buy the product. Similarly in private equity and real estate, the fund managers have crafted ways to implement fee credits (the “coupons”) only after investors permanently cease paying management fees, which is the equivalent of not buying the product. In other words, CIM may have promised fee credits to CalPERS but were careful to time them so that they appeared at times and in investment vehicles where no management fee would ever again be paid by CalPERS, thus causing CalPERS to receive the equivalent of mostly worthless coupons.

It Looks Like Apollo Shortchanged CalPERS Too

In our August post, CalPERS in Bed With Jeffrey Epstein Client and Co-Investor, Apollo’s Leon Black Even After Apollo Pay-to-Play Scandal Led to Conviction and Jail Term for Former CalPERS CEO, we wondered why CalPERS was still so loyal to Apollo after it looked like they’d been had by Apollo twice, once in the pay-to-play scandal and second by Apollo likely not making good on its promise to make up for it.

A CalPERS insider later confirmed what we’d inferred from the text of the Apollo settlement letter and CalPERS quarterly private equity fund performance reports: that the dedicated fund that Apollo hoped to get CalPERS to commit to never came together.5 That meant Apollo was managing less CalPERS funds than both parties had anticipated. That alone meant CalPERS would get its rebate funny money, which for Apollo was $125 million, more slowly than the five year contemplated in the settlement agreement.6

But our back-of-the-envelope guesstimate came up with CalPERS being way short, even nine years out. From the August post:

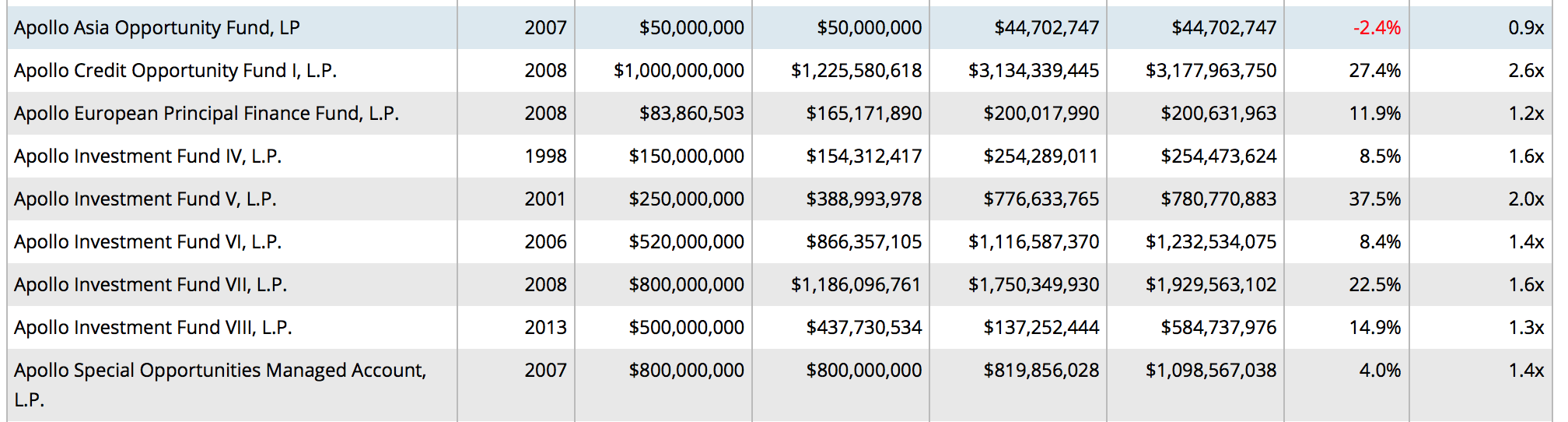

If you look at the list of CalPERS’ current Apollo investments, you’ll see only one that looks like a separately managed account, the 2007 “Apollo Special Opportunities Managed Account.”

In theory, there might have been other separately managed accounts in 2010 that were liquidated since then, but the fact that Apollo hasn’t wound up 1998 and 2001 funds makes that seem unlikely….

So CalPERS had $800 million of committed capital that was eligible to have its management fee waived until the $125 million was exhausted. Recall that management fees usually step down after the fifth year and are usually based on the amount of capital then deployed, and not the committed amount.

Some simplifying assumptions:

1. CalPERS was already a full three years into its 2007 fund by the time its fee reduction agreement with Apollo was effective. So it would have only two years of fee reductions at the full management fee rate

2. Due to the size of the commitment, the management fee was 1.75% (this if anything is conservative)

3. It effectively dropped to half that after the investment period of five years, meaning after the two years left at full rate on this fund.

2 x $800 million x 1.75% = $28 million

7 x $800 million x (.5 x 1.75%) = $49 million

Total = $77 million

So a reasonable guesstimate is that CalPERS got less than 2/3 of the face amount that CalPERS was supposed to receive from Apollo as compensation for the harm suffered by CalPERS, when CalPERS expected to get it all back in five years or so. And that’s before recognizing that letting Apollo and its fellow bad boys pay not a dime in cash was a ginormous concession. Black is worth nearly $7 billion. His worst take-home pay in recent year was $142 million and it’s been as high as in excess of $400 million. But CalPERS is too cowardly to demand that Apollo, which in this case would have been Apollo principals, to be personally responsible for their bad acts.

Now this analysis was generous in a way I neglected to unpack at the time. I calculated the stepped-down management fee as if it were on the total commitment amount. In fact, not only does the percentage charged fall, but it is also applied to a lower amount: the limited partner funds actually invested at the time, and not the commitment amount. Typically general partners start selling companies at the four or five year mark, reducing the amount of monies outstanding, so using the full commitment amount for the last seven years is generous.

The estimate is also generous virtue of making no allowance whatsoever for the management fee offsets discussed above.

Now perhaps we have some Apollo-favoring facts missing. After all, Apollo’s flack called us to chide us for not reviewing our “facts” with him, but he didn’t ask for a correction,as you’d expect if we’d gotten something wrong.

But unless there is another Apollo fund that is eligible for the fee rebate (or perhaps CalPERS has failed to disclose one despite the terms of its 2002 settlement with the Mercury News), the gap between what CalPERS should have gotten and what a reasonable guesstimate of what it received is so large that it’s hard to imagine that CalPERS wasn’t snookered by Apollo.

Our interest in CalPERS came about by virtue of its long-standing position as one of the biggest private equity investors which also was required to conduct its business in a pretty transparent manner. CalPERS’ intense efforts to go dark rather than correct mistakes come from learning all the wrong lessons from private equity secrecy, and from having failed to do much soul-searching and house-cleaning in the wake of its corruption scandal.

____

1 This is standard practice with defense contractors who’ve behaved badly.

2 Starting with Apollo was a bad move. Khinda should have gone to the weakest, not the strongest, party first.

3 The profit share called a “carry fee” is not a fee as defined in limited partnership agreements. For instance, in the Apollo VIII limited partnership agreement, pages 37 through 39 set forth “Portfolio Investment Distribution,” known in the trade the “waterfall.” And the 20% cut of the gains that goes to the general partner is repeatedly called a distribution, not a fee.

4 We have discussed this in excruciating detail in older posts. Some of the common tricks include dreaming up new fees (the limited partnership agreements require only that specifically enumerated fees be offset against the management fee, and paying fees to affiliates.

5 So maybe CalPERS was not so dumb, as in they didn’t take the bait of “get your rebates back sooner if you give us a lot more dough.”

6 It is hard to square Apollo committing to $125 million in fee rebates versus $50 million for CIM, when Apollo paid roughly $48 million of the total of $58 million in pay-to-play fees.

.

You really need to listen to this interview with Catherine Austin Fitts, which mentions CalPERS. She was Assistant Secretary of Housing — Federal Housing Commissioner at the US Dept of Housing and Urban Development under President George H. W. Bush. I have not been able to find any reference to FASAB 56 on your blog, which is disappointing to say the least, and is hugely relevant to this topic.

*Sigh*

FASAB 56 has nothing to do with CalPERS. CalPERS is an agency of the state of California. FASAB 56 applies to Federal government accounting only. CalPERS is subject to GASB. Link-whoring, which is using our site to elevate the Google ranking of a post or site (I note your link is to a fresh article, and it looks like you wandered around to sites to link to it with any thin excuse), is a violation of our written site as well as thread-jacking and assignments.

In addition, we have regularly mentioned the magnitude of the Pentagon’s black budget regularly, as well as its supposedly missing funds.

Update: Out of curiosity, I started listening to the podcast. In a bit over five minutes, Fitts established that she is an uninformed hysteric. Even if one accepts her claims about the significance of FASAB 56 in terms of Federal budgetary transparency, no way, no how does this even come close to “taking the majority of the US securities market dark.” Anyone with a Bloomberg terminal would laugh this out of the room.

She then proceeds to demonstrate that she doesn’t understand how the Federal government funds itself either (it’s a currency issuer and does not need to tax to spend, as the fact that we never worried about how to fund the next bombing run in Iraq attests).

While there are good reasons to be concerned about and upset with FASAB 56, Fitts discredits critics by grotesquely exaggerating her claims and repeatedly demonstrating her ignorance of finance and economics. I have accordingly removed the link (which I should have done regardless since our policy is either to delete comments that engage in link whoring or remove the offending link).

Link Whoring

Thread-Jacking

Vocabulary expands when I take the time to read your articles and comments.

Keep up the focus on CalPERS. If the largest pension fund in the US has this many controversies and bad actors, I can only imagine what’s going on with the smaller funds where no one is looking?

This is now Gavin Newsom’s baby.

The fact that California Republicans haven’t jumped all over this shows just how deep the corruption runs.

Since CalPERS stays in bed with PE it must like getting ****ed over, and over. imo.

Thanks for your continued reporting on CalPERS, PE, and pensions.

Love starting a day with coffee and CalPERS. About the Phillip Khinda link, though, I get this from the CalPERS website:

I searched on “Steptoe and Johnson” but a whole lot of stuff came up. Which one should I be reading?

Thanks again for your keeping all this delicious slime under your microscope.

Thanks for your interest!

The 2014 post we excerpted and linked to in this one discussed the Steptoe report long form and includes an embed of the full document:

https://www.nakedcapitalism.com/2014/03/calpers-private-equity-scandals-steptoe-johnson-report-whitewash.html

This is so embarrassing to read. All that money on the table and CalPERS has forgotten how to play hardball to claw it back again. Seems like the takeaway lesson is that if you have a scandal in your company, you really have to go into it root and branch and clear it out while wrapping up the loose ends. When you do that you get to draw a line under the whole thing and move on. If you don’t, the same issues will crop up, the same people will re-offend, and past misdeeds refuse to go away but will come back to haunt you.

The story of the original scandal is remarkable, particularly the role of that guy Villalobos-

https://www.latimes.com/business/la-fi-villalobos-suicide-20150115-story.html

https://fortune.com/2013/05/06/where-is-calperss-governance-when-you-need-it/

I sometimes wonder if the State of California needs to step in and take over CalPERs for awhile to try to straighten out their governance problems but a few minutes reflection shows that the State government is actually an enabler of CalPERS’s behavior so that would not work.

Another excellent,relevent,competent,material response…thank you

robert

I am always amazed when corporations that abuse those they do business with, or who committed crimes without having to admit or deny them, are allowed to make restitution over time, with only the slightest assurances that they will make good. (And, in other circumstances, are required to make no changes in their executive ranks or business model).

What part of, “Fool me once….” does CalPERS not understand? Or should I not ask that of a board and management team that thinks a high school graduate is the ideal person to run one of the world’s largest pension funds?

One would think that being forced to do more business with a vendor, which has already screwed you out of tens of millions – and whose management seems ready to do it again – in order to recoup prior losses, would be a non-starter.

Accepting repayment via rebates against future fees would seem to be an invitation to perform creative accounting. Among other vulnerabilities, it seems to allow a wrongdoer to claim credit at retail for something they buy at wholesale. It also ignores how lowering one set of fees via the rebate might lead to another set of fees going up by the same amount. Whatever happened to cash on the nail head?

For some reason, this mess reminds me of an employer’s union negotiator, who once claimed that slicing the compensation pizza twelve times, rather than ten, gave the union a twenty percent raise.