Yves here. Even if you don’t agree with Bob Hertz’s prescription for medical debt, his typology of various types of debtors and the political and practical problems they pose provides a good foundation for further analysis.

By Bob Hertz, a health care essayist

The recent proposal by Sen. Bernie Sanders to cancel $81 billion of medical debt is a very good start – but it is only a start.

The RIP Medical Debt group–which buys old medical debts ,and then forgives them– is absolutely in the right spirit. Its founders Craig Antico and Jerry Ashton deserve great credit for keeping the issue of forgiveness alive.

Unfortunately, over $88 billion in new medical debt is created each year – most of it still held by providers, or sold to collectors, or embedded in credit card balances.

Tragically, none of this has to happen! In France, a visit to the doctor typically costs the equivalent of $1.12 . A night in a German hospital costs a patient roughly $11. German co-pays for the year in-total cannot exceed 2% of income, Even in Switzerland, the average deductible is $300.

U.S. patients face cost-sharing that would never be tolerated in Germany, says Dr. Markus Frick, a senior official . “If any German politician proposed high deductibles, he or she would be run out of town.”

In Australia, a recent proposal to establish the equivalent of a $5 co-pay for primary care visits fueled such an outcry that the federal government was forced to withdraw the idea.

Americans may be forced to take second jobs just to pay medical debt; meanwhile, the highly-taxed Europeans get free medical care and are counting their weeks of paid vacation. What is wrong with this picture?

These nations have shown that cost sharing is not necessary to keep health care spending at a level well below that of the United States. They rely on higher taxes and price controls…..and yet, are those really worse than widespread patient debt?

- US Medical debt comes primarily from these sources:

- the uninsured

- high deductibles

- out-of-network bills

- claim denials

- specialty drugs

- emergency room care

- ‘zombie debts’ purchased by collectors

In this essay, we will show that a substantial number of these debts can be cancelled or greatly reduced.

Today, these groups run up the most medical debts:

Group No. 1. The poor and the uninsured, including those who still do not get Medicaid in red states.

A Tennessee couple earning $13,000 annually gets no help whatsoever on medical bills. They can barely afford food or rent; so of course they incur medical debt every time they are sick.

Over 20% of these families do not have a checking or savings account. Over 30% are not working at all. If they do work, they cannot afford to join the employer’s plan.

Six full years after the ACA, there are still close to 30 million adults in the US who are uninsured. About seven million are undocumented immigrants. Another seven million are actually eligible for Medicaid, if they do get sick.

About four million could benefit from the ACA, but are unaware of the benefits. Up to five million are kept out of both Medicaid and the ACA in the red states described above. Another two to three million make too much for ACA subsidies.

This is a hard group to help. No states besides California want the undocumented to get help. No cities outside liberal enclaves like Seattle and New York care about health insurance for restaurant and service workers.

The poor rarely vote, so ignoring them does not trouble conservatives. Politics are often dominated by seniors -who will approve a conservative message about ‘getting rid of socialized medicine’, while they themselves enjoy the federal socialism of Medicare.

(Not to mention Social Security, electricity, phone infrastructure, and the defense spending that comes to red state residents from the federal government.)

Group No. 2. The under-insured , who have high deductible insurance and no savings;

Why are they walking around with deductibles they cannot afford?

At some employers, this is the only health insurance which is offered.

Even where there is a choice of plans, people with smaller incomes often select the cheaper high-deductible coverage.

If you are healthy, a high deductible plan to save money on insurance premiums may be a decent gamble at first.. But if you have a chronic illness, you will pay the entire deductible each year, and will probably build up debt. Only a minority of employers offer assistance to pay the deductibles.

Sometimes this group pays $500 a month or more for a porous health plan, which then leaves them with thousands in debt if they are hospitalized.

Many families are living right on the edge financially, and they have trouble with all their debts, not just medical. Default rates are growing on car loans and credit cards as well. They often face utility shutoffs and repossessions.

A recent study of insurance claims showed that 49% of patient out-of-pocket costs per healthcare incident were below $500; 39% were $501-$1,000; and 12% were more than $1,000. That generates an enormous amount of medical debt.

Group No. 3. The well-insured, who may still get huge out-of-network bills.

Some of their debts are out-and-out fraud. If a hospital says they are in-network, then all their contractors should be in-network – or else we have an illegal bait-and-switch. These surprise bills should be cancelled (details to follow).

- In 2011, (9 years ago) New York studied more than 2,000 complaints involving surprise medical bills, and found the average out-of-network emergency bill was $7,006. Insurers paid an average of $3,228 leaving consumers, on average, “to pay $3,778 for an emergency in which they had no choice.”

- Out-of-network assistant surgeons, who often were called in without the patient’s knowledge, on average billed $13,914, while insurers paid $1,794 on average. Surprise bills by out-of-network radiologists averaged $5,406, of which insurers paid $2,497 on average.

Medical debt can be cruel and dispiriting – and It is also incredibly inefficient! The cost of creating a bill, sending a bill, following up, negotiating a settlement, paperwork for charity care, financial counseling, a possible lawsuit, and (rarely) getting repayments over years– the sheer administrative expense is enormous.

The average recovery on hospital bills sent to individuals is 15.3%. Non-hospital providers recover an average of 21.8% of each bill. No wonder some providers prefer Medicaid – it only pays about 50% or less of their normal charges, but that is far more than they will get in actual collections.

There are two overarching models for financing health care ;

One is the Bernie Sanders model:

- Paternalistic– you get insurance whether you choose it or not

- Sympathy for the poor, minorities, and migrants (you never know when you might be among them)

- Collectively bargained – usually with large payroll taxes

- No pre-existing conditions clauses

- Hospitals are financed mainly by taxes, not user fees

- Patients are not in debt (though governments often are)

- Cost control through price controls and rationing

The Sanders model accepts the use of coercion to pay for health care. (For that matter, the Singapore health model that is praised by conservatives is filled with coercion, including public hospitals, forced savings for HSA’s and taxes forcatastrophic insurance.) At some point we are all going to get sick, so letting us decide when to buy insurance is somewhat of a fool’s paradise. Millions will always make bad choices and be left to suffer; we need to be protected against our own stupidity. Coercion is needed –the only real issue is when and where. Even wealthy societies can benefit from forced savings.– for example, a mandatory HSA deposit of 3% of income would eliminate most of the medical debts discussed in this essay.

The other is the Paul Ryan-Newt Gingrich model:

- Based on Individual choice

- No mandates on employers to provide quality coverage

- No mandates on individuals to buy quality coverage; if they want to gamble going uninsured in order to save money, that is their call.

- Hospitals financed by user fees, insurance premiums and private savings

- No interference with anyone making money on health care -even those who prey on medical debtors

- Medical bankruptcy is OK, because the fear of it motivates the purchase of health insurance.

- Cost control (theoretically) through competition – faith in free markets

- Taxes on workers are lower – although the savings seem to be siphoned off in premiums, co-pays, and deductibles.

The Ryan model is frankly Darwinian when you get close to it. The uninsured, frankly, are usually people who make mistakes – like poor budgeting, failing in school, losing their jobs, or being born to non-rich parents. Persons with no money get much less care, and will die sooner. Those who do not buy insurance when they are healthy will suffer later on. Eventually it all starts to sounds like “culling the herd.”

The Ryan model therefore expects a lot from private charity. (Begging is preferable to new taxes.) Democratic legislators have also established Medicare, Medicaid, and SCHIP to smooth out the inevitable rough edges.

Medical debt is an obvious consequence of the libertarian model. It can only be reformed by importing controls and rules from the Sanders model.

The ideal image of high-deductible insurance features a judicious patient with at least $10,000 in HSA savings, getting bids on each procedure and therefore driving down costs. They might even have non-urgent care done abroad, which would force American hospitals to compete on price. They might decline an unnecessary treatment or diagnostic test, to save money.

Even If hospitalized , they can say to the provider, “I am paying cash, what is your best offer?” The Amish – who do not buy insurance, but save prodigiously – actually use this method.

This has some basis in fact. Cash for medicine.

However, millions of Americans have no cash, and no bargaining skills. Some diseases may not wait for patient ‘shopping.’ A desperate patient goes to the nearest hospital and then juggles utility bills and high-interest charge cards to pay down medical bills, and then begs for help from relatives or (even sadder) from GoFundMe.

The average holder of an HSA account is under age 45, healthy, and with an average income of $75,000. Whereas In low-wage America, a ‘consumer-driven’ health plan is a ‘consumer-indebted’ reality.

Financial casualties among patients do not seem to lead to lower health care prices. Providers are just as likely to raise their prices, in order to cover the bad debt they are taking on. (Drug companies certainly do not lower their prices when their customers suffer.)

Doctors may want to forgive some patient debts, but there is a limit how often they can do this and still cover the expenses of their practice. In some cases, it is actually (and idiotically) illegal for physicians to waIve the deductibles.

Therefore I advocate the following attacks on medical debt:

Phase One

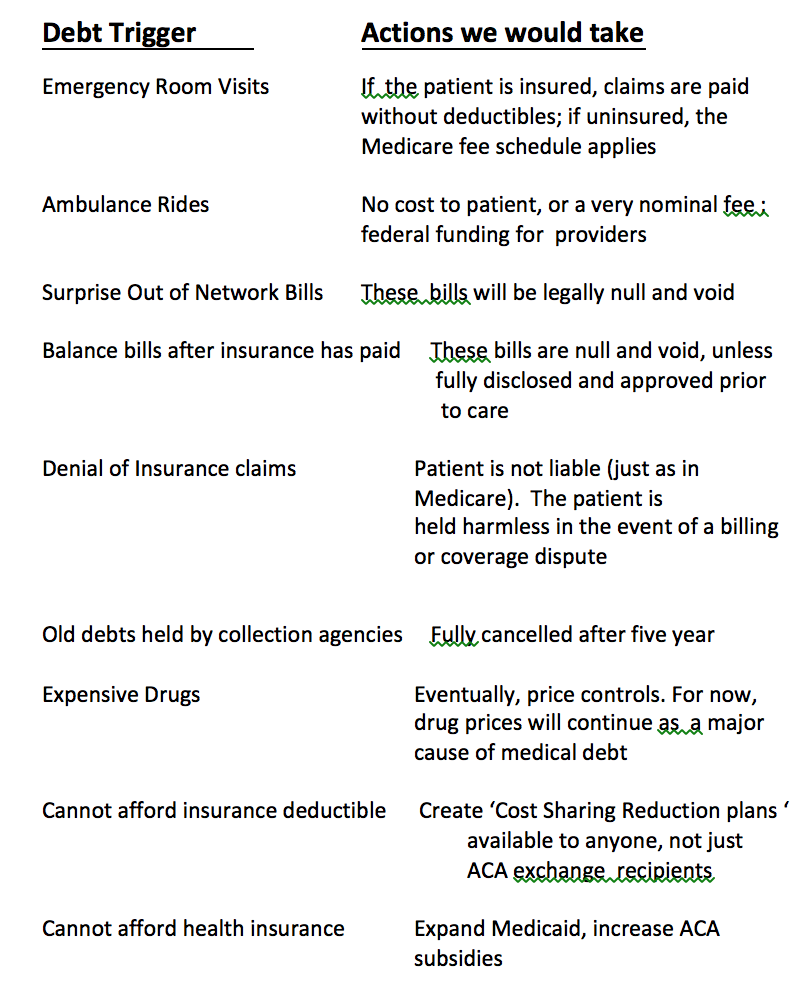

We must cancel balance bills and surprise bills if there was no prior disclosure.

In most cases, providers will not have the right to collect anything more than what the insurers pay them.

Phase Two

We must cancel the older, inactive “zombie debts “ that are being purchased by collection agencies.

This line of business must terminate. Providers throughout the country are selling uncollected medical debt for pennies on the dollarto collection agencies, who aggressively attempt to force patients to pay the full amount due. These debt collectors harass patients at work and at home, deploying unscrupulous tactics even after the statute of limitations on the debt has expired.

Debt collection lawyers can file hundreds of suits a day, often with little evidence that the alleged debt is actually owed. Once a lawsuit is filed, the process is stacked against defendants, the overwhelming majority of whom are not represented by an attorney. And collectors have a big advantage in small claims courts, which provide very limited due process protections to debtors.

The Debt Buyer Industry has a bad reputation and for good reason. They are typically far more aggressive than the original creditors or their hired debt collectors. There is nothing redeemable about the junk debt buying business.

Per Senator Sanders: “Forcing additional stress and hardship on someone for the ‘crime’ of getting sick is immoral, unconscionable, and un-American. We will eliminate past-due medical debt.”

Of course, all cancellations of unconscionable debt must be income-tax free.

Phase Three

Debts can also be reduced, by expanding the Affordable Care Act:

– Subsidies should be tied to low-deductible gold plans

– Subsidies should be available at all income levels – not just stopping at 400% of poverty

– We can let families join the ACA exchanges if their workplace

– Plans do not cover spouses and children (i.e. solving the ‘family glitch’)

Phase Four

We must create a subsidized, guarantee-issue “Cost Sharing Reduction Insurance” that would be available to any American – not just those who have low incomes and a Silver plan under the ACA.

This policy would cost about $125 a month and it would pay your deductibles – similar to the Medicare Supplement plans that seniors can purchase. Rates can be kept stable by government reinsurance – again, just like Medicare. The cost of reinsurance might be $50 billion a year…..but we spend that much and more to lower the cost of Supplements and Drug Plans for seniors.

Low-deductible health plans have just become too expensive for many American businesses and consumers. Adding on a separate policy to pay deductibles is not a perfect solution, but it is a workable one.

Here are specific regulations to continue the assault on debt:

RULE #1 No balance bills or out-of-network charges will be valid without arm’s length prior disclosure.

If a procedure can be scheduled, it can be quoted. Every other industry gives price quotes that are the basis of a valid contract – with fees and charges spelled out, and remedies if unavoidable extra costs appear.

A medical provider who does not offer a quote when requested will not be able to enforce payment. No prior disclosure means no patient liability, for scheduled procedures. Of course this solves the surprise bill problem: if extra fees are not disclosed in advance, then the patient may not be billed extra.

Also– If an insurance claim is denied, the patient is not liable.

The provider and the insurer can fight it out

For emergencies – when no contract is possible – providers can only charge an average of what they actually collect from all insurers. Networks are completely irrelevant.

I would call this “statutory protection.” You shouldn’t need to buy expensive insurance, just to be protected from price gouging.

These laws must be national and they must be enforced. Some hospitals will continue to send balance bills even if they are illegal. Therefore, we must

have a “Patient Financial Protection Bureau”with the power to nulllfy price-gouging. We need officials who are willing to assess fines, harassment, audits, bad publicity and even federal takeovers if needed.

(Price gouging happens much less to persons over age 65, incidentally. Medicare Advantage (MA) patients are not responsible for out-of-network charges in emergency care settings. Federal law also limits how much providers can bill the patients in traditional Medicare, in most medical situations– although specialty drugs create their own bankruptcy issues. )

RULE #2. Emergency care must not be subject to insurance deductibles.

Co-pays such as $250 for ER care would be acceptable, but nothing more.In other words, even if you have a plan deductible of $4000 or more, any emergency will be covered at 100%.

Otherwise we get awful scenes such as occurred on the Boston subway. A woman’s leg got stuck in the gap between the train and the platform. It was twisted and bloody. She was in agony and weeping, but she begged that no one call an ambulance. “It’s $3000,” she wailed. “I can’t afford that, I have terrible insurance.”

RULE #3. The uninsured will be charged Medicare rates for hospital care.

. All existing “chargemaster” bills must be cancelled, never to return.

The largest bills are almost never collected anyways. Wage garnishment generally doesn’t bring in very much for hospitals either. In a recent study of Virginia hospitals, the average total revenue from garnishment was 0.1% of the hospital’s annual cash flow. The average “award” for hospitals that won lawsuits against patients was just $1,400.

Hospitals who serve the poor and uninsured do have a legitimate problem, however. Hospital bad debts are running over $50 billion per year. Some hospitals do offer 70% discounts to the uninsured, and they still must deal with bad debt

The solution is not meaner collections–– it is more help from government. Medicare’s current aid to hospitals for patient bad debt are stingy and insufficient. (I would favor a small tax on the uninsured . The ACA mandate was not a bad idea, but the money that is raised should go toward hospital care.. A person who has money but stays uninsured will still receive emergency care, and a tax to pay for this is not out of place.)

RULE #5 Limits must be placed on debt collectors:

Some non-profitand “public”hospitals aggressively sue low-income patients for medical bills .(At least until the media catches them doing it.) They sue people who would actually be exempt under their own charitable guidelines. Some have evenfiled lawsuitsagainst their own employees to collect unpaid medical bills.

Charity care guidelines should be national, universal, and generous, with harsh punishments given to hospitals that ignore them.

The National Consumer Loan Center has made a good start in their proposed Model Medical Debt Protection Act, which would ban the following:

(1) Any action causing an individual’s arrest;

(2) Causing an individual to be subject to a writ of body attachment [or similar term such as “capias”];

(3) Setting a lien, or ever foreclosing on an individual’s real property;

(4) Garnishing the wages or state income tax refund(s) of a patient who is eligible for financial assistance.

Lawsuits for medical debt must disappear. No more attorney fees would be allowed, and no interest charged either.

Under our new laws and regulations, here is a sample of what will happen to individual medical debtors

#1 – The debtor brought their child to the Emergency Room, and was billed $25,000.

Hospitals use a complex, confusing chargemaster-based billing system to get more money from insurers. The list price is set unreasonably high; then the insurers negotiate a discount up tp 80%. (Some insurers even bill for this ‘re-pricing’ – which is pure financial waste.)

In any event, when some hospitals see a chance to collect their invented “rack rates” from the uninsured, they go for it aggressively.

It is true that a stubborn patient can sometimes reduce their debt through negotiation….. but no one has to negotiate with the fire department. Americans are used to posted prices, not haggling, and especially not haggling in medicine.

This bill for $25,000 should be denied at the state health agency. The hospital can collect on the Medicare fee schedule.

#2 – The patient had to use an out-of-network hospital due to complications after surgery, and was billed $50,000 extra.

This event could not have been scheduled in advance. The patient had no choice in the matter –

Therefore no extra fees are due. The out of network provider must accept the standard insurance reimbursement as payment in full.

The out-of-network providers – especially the ones owned by Wall Street – use a predatory price-gouging business model .The medical profession itself should have cracked down on them long ago.

#3 – The debtor is being harassed by debt collectors over a $40,000 hospital bill from six years ago

There will be a firm statute of limitations on medical debt. After a fixed period of perhaps five years the debt must be legally cancelled, so it can never be sold or re-sold to anyone. All interest and legal fees will also be cancelled. Lawyers who enforce medical debts can find honest work instead.

#4 – The debtor put $100,000 on high-interest credit cards to pay for cancer drugs, and now cannot cover the charge card payments.

They will probably have to declare bankruptcy. The pricing practices of Big Pharma unfortunately needs a more complex reform –and not a moment too soon. Very high drug costs are a major reason for the rising premiums (and resulting high deductibles ) in comprehensive health insurance.

However, bankruptcy only works well for one-time high medical expenses. If you have a chronic illness that will cost $1,000 a month for the rest of your life, bankruptcy is only a temporary reprieve.

#5 – The patient received a hospital bill for $50,000 –after their insurance company already paid the hospital $100,000

The hospital cannot bill extra, if they did not allow the insured to approve the extra fee in an arm’s length quote and transaction. No extra payment need be made here.

.#7 – The patient had a battery of tests of investigate his dizziness, and now faces a hospital bill of $15,000.

These tests could have been performed in a much cheaper location. The hospital should only be allowed to recover what an outside clinic would charge. We can go much further toward ‘site-neutral’ reimbursement., which hospitals violently resist.

#8- The patient had a successful surgery, but the insurance claim was denied due to coverage issues. The hospital is now pursuing them for $35,000.

If a claim is denied, and the patient could not have known this was likely, the patient will not be liable. (This has been true in Medicare for decades.)

Right now, patients are often asked to pay disputed medical bills while insurers and providers attempt to resolve the dispute. If an individual does not pay the bill during this time, it can be turned over to collections. Before receiving medical care, most consumers sign consent forms agreeing that they are responsible for any medical bills their insurance company does not cover in full – this must end!

#8 – The patient needed an ambulance after a stroke, and was billed $2800 for a 10 minute ride.

Ambulance service should be a government function, paid for by taxes, no different than fire or police. This applies to air-ambulances also.

The taxes required would be about $15 billion a year, which is a rounding error in federal health spending.

Ambulance fees must be capped at the standard Medicare amount of $450, perhaps with an increase of about 30%, all of which should be paid by government.

#9– The debtor did not pay a $600 medical bill while they were unemployed. They were sued for the debt but did not make a court appearance. Next time they got a traffic ticket, they were put in jail until they paid the medical bill.

No lawsuits should ever occur on small medical debt, and no arrests either.

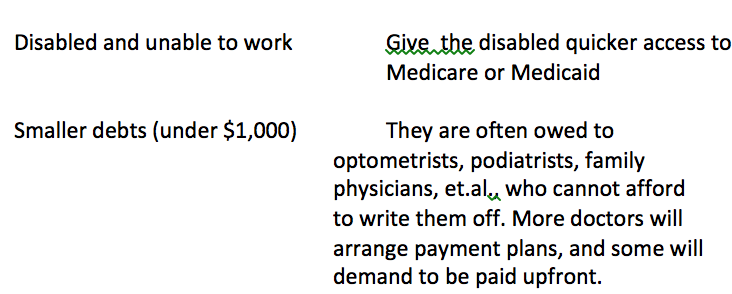

#10 – The patient owes their dentist $2,500 for past treatments, and needs addition dental care that they cannot pay for at this time (or ever).

This is a major area of medical debt – at least 12% of overdue bills — but unfortunately we do not have a quick solution. The patient must look to the following safety nets:

Dental schools-Most of these teaching facilities have clinics that allow dental students to gain experience treating patients, while providing care at a reduced cost.

Dental hygiene schools may also offer supervised, low-cost preventive dental care as part of the training experience for dental hygienists.

CONCLUSION

The only way to fully eliminate medical debt would be a comprehensive single payer plan, which allowed no fees at the point of service.

However – such a plan would require setting all prices for all doctors, hospitals, labs, and drug companies. All providers would have to be satisfied – in advance – with what the government is going to pay them on each procedure.

Countries like Germany accomplish this through collective bargaining. Japan, France, Taiwan, Israel and Scandinavia also have national fee schedules. However, I do not think you could get all the providers in Toledo to agree on one schedule, much less every provider group in America.

Single payer would also require new income and payroll taxes of at least ten per cent more than we pay now, if we want first-dollar coverage.

Most single payer countries have a 10%-20% sales tax as well. The Europeans are not shy about taxing the middle class for health care.

Based on consumer surveys, there are between seven and ten million households with over $10,000 in medical debt. However, there are about 20 million households who earn over $200,000 a year and would have to pay higher taxes to solve this problem.

It took a historic financial crisis, plus a fair amount of Democratic self-delusion, just to get Obamacare passed. One Congress after another has refused to impose relatively tiny cuts in Medicare reimbursements.

Therefore……….the best we can do for now is to

- Cancel the unconscionable debts

- Provide more federal funding for emergency care

- Create supplemental insurance that will pay the deductibles

A SUMMARY OF OUR ‘FULL-SCALE ASSAULT’:

Recycled back to the US via Richard Murphy

https://www.taxresearch.org.uk/Blog/2020/02/16/the-us-does-not-have-a-model-for-a-successful-health-service/

An American with cancer has nearly a 90% chance of surviving for 5 years. If they survive for 5 years they have a 40% chance of bankruptcy.

We look forward to the same in the UK

Somebody please verify: is that about a 4% chance, if getting treatment, that your families generational wealth will be wiped out, they will be destitute, and you won’t be around to help/protect them?

That’ll affect decision outcomes…

I don’t think your question can be answered from what is on the blog. Maybe it can be answered from analysis of the underlying scholarship, which a slide reproduced on the linked blog cites: https://ascopubs.org/doi/full/10.1200/JCO.2015.64.6620 . Sample excerpts: “Between 1995 and 2009, 231,596 persons were diagnosed with cancer. Patients who filed for bankruptcy (n = 4,728) were more likely to be younger, female, and nonwhite, to have local- or regional- (v distant-) stage disease at diagnosis, and have received treatment.” and “The term financial toxicity has been coined in reference to the growing recognition that high out-of-pocket expenditures during cancer treatment are putting many families into severe financial distress and, in some cases, leading to refusal of treatment or nonadherence to recommended treatments.” Also, from the Discussion section: “By linking the Western Washington SEER Cancer Registry and federal bankruptcy records over 15 years, we were able to explore the question of whether those who filed for bankruptcy after a cancer diagnosis had a higher risk for death from any cause. We found a consistent, positive association between filing for bankruptcy and earlier mortality, suggesting that those who reach the point of financial insolvency after a cancer diagnosis have significantly poorer outcomes than those who do not.” The last two sentences specifically address the relationship between cost of treatment and financial distress: “Finally, the rapid rise in the cost of individual cancer therapies is raising out-of-pocket costs for patients with cancer, even in the face of expanding insurance coverage. Policies aimed at reducing financial exposure of patients, such as caps on patient out-of-pocket costs, expanding access to patient assistance programs, or limits on rate of rise in the price of treatments may be necessary to mitigate the negative health consequences that stem from the rapidly rising cost of cancer care.” That last sentence stands out as the only one in the entire article that uses the word ‘price’ instead of ‘cost’. Some of the references (notably 2 and 3) seem to report very disturbing correlations indeed of incurred treatment cost to financial distress. My personal take-away is that, while American _medical science_ is succeeding remarkably well at extending the lives of people diagnosed with cancer, the American _medical system_ is even more remarkably failing them.

I stopped reading after this:

“higher taxes” = “cost sharing” and is how any number of countries with low to no out-of-pocket medical cost pay for their healthcare. In this case, it is a form of insurance. Insurance is a social construct after all. “Price controls” could also be argued to be “cost sharing”.

I think you miss the point that cost sharing by the patient is supposed to make them have a healthier lifestyle, avoid frivolous visits to the doctor, unnecessary use of prescription drugs, etc – otherwise known as “having skin in the game.” Apparently this rationale is not justified by the experience of other countries. Also, fear of personal medical expense could easily be counterproductive for society as a whole – that’s why flu shots are free or low cost.

My point exactly.

Hello!!! We *already* have quite literal skin in the game!!! The very few people who visit doctors for ‘frivolous reasons’ usually have some underlying, undiagnosed, unfrivolous problem. Eg, my ex-MIL, who visited doctor after doctor, was written off as a hypochondriac and sent to a psychologist. She succumbed to a never-diagnosed progressive cognitive disability, her last years full of fears, including fear of food. She finally starved to death. Just as her mother had. And just like her daughter, my BFF, is doing now (minus the doctor-visiting — she *hates* them as a class, except for her own physician of many years who retired two years ago…).

We manage the anorexia by giving her small amounts of food frequently, but she boggles at the sight of more than three food items at a time, only wants small bowls and small spoons. We put food on her desk b/c she panics at the sight of a refrigerator or panty full of food. Most the the diagnoses she has had over the years have turned out to be wrong, or at least were changed, sometimes three-four times (same symptoms got similar treatment with her mother) and no treatment has seemed to help except for *one* naturopath decades ago, a true healer. But he is now head of is own fancy-schmantcy clinic and you only ever see his disciples, who aren’t a patch on the old man.

Oh dear, that’s pantry full of food, not panty! BTW, back in the day, this woman was a specialist in ancient near eastern languages back in the day, a martial artist, a long-distance cyclist, and an excellent, if rather fast, driver of her little Karmann Ghia. She has agoraphobia as well, come on with the anorexia, has slowly progressed to where she hasn’t voluntarily been outside in two yrs.

I’m sad to hear all this because I have a (very nice) niece who is afflicted by real (or imagined) parasites.

Me? I’m so stupid as to believe that God, through doctors or not, will keep me healthy enough for my own good – and so far so good.

But I do sympathize and I’m NOT arguing for “skin in the game” but rather that we admit we have an unjust system and that we apply as much socialism as is necessary until it’s fixed and as much socialism thereafter as is needed too.

Billing someone “by surprise” is felony criminal fraud. You can’t consent because there is no offer, acceptance, consideration and performance. There is thus no contract. You cannot have a meeting of the minds — offer and acceptance — when you are intentionally deceived. The hospital in the case of the out-of-network “assistant surgeon” knows the “assistant” is out of network and deliberately does not tell you before putting you under anesthesia.

Been there done that. What the hospital will tell you is that the surgeons do not work for them and your complaint is with the doctors.

Here’s the BTDT: In California the state medical board recommends three surgeons in the operating room when performing open heart surgery. One as an “assistant surgeon” (scavenging femoral artery for transplant, etc.) and another in case the primary surgeon is “unable to proceed”, for some reason. The patient only has personal interaction with the primary surgeon. The other two surgeons will likely be unknown to the patient.

So the primary surgeon may be selected for “in-network” status. But the other two surgeons may not be. And when the assistant surgeons send you a bill for their “work”, you will not only be surprised by the amount their billing. You will be surprised by their identity and presence in the operating room.

You may ask your primary surgeon about these assistants bills. He will tell you the three physicians in the OR is state law. It’s NOT! The CA legislature allows the state medical board to set “policy” for medical procedures; but that is never discussed with the patient. (In my case the OR report indicated that only two surgeons were actively involved, but all three sent me bills of near equal amount.) Surprised to say the least!

When you are in a hospital the nurses may see you as a patient. The administrators and doctors see you as a mark.

Good for you. So many medical bills are based on what would be called fraud in most other commercial environments.

The Federal Trade Commission should be all over the surgical profession.

Most countries in the industrialized world achieve universal care with less than 10% of GDP–close to what the U.S. gov’t entities spend on healthcare. Total spending in the U.S. is closer to 18% of GDP or approx. twice what other countries spend.

The U.S. can properly regulate a private market with public or private payors to get savings in excess of $1trillion per year (>$10t over 10 years)–enough to payoff all existing medical debt, fund massive infrastructure and increase universal educational attainment to 16th grade plus pay for free medical school.

Corruption is the only thing that stands in the way of stopping this criminal behavior in the healthcare industry. An aggressive DOJ could likely have immediate and massive impact on costs by going after anti-trust and fraud via RICO in the healthcare industry.

You are half right. Higher taxes are indeed a form of cost sharing.

But there is one big difference.

with higher taxes, the rich pay more.

with higher cost sharing the American way, the sick pay more.

When my car isn’t running my mechanic does a good job fixing it. He is competent. When he tells me that it time for a new car or you will be throwing good money at bad, I buy a new car.

Our politicians are not good mechanics, they remind me of Click and Clacks joke about the mechanic looking over your car and thinking about that new boat he wants.

They were elected to fix problems, they don’t, time for a new mechanic that writes legislation for people and not fictive creatures invented in the United case.

I’ll second what Denninger has said this morning and forever. Where are the monopoly breakups, mandatory up front disclosures, and criminal prosecutions?

Now off to my personal healthcare regimen: Church Of The Sunday Long Run, then Bob Evans sausage for breakfast!

so…balance on one toe, stick your tongue out to the right(not the left…ever!) and whistle the battle hymn of the former republic through your ears while juggling pennies with one hand and pointing at a bird with the other.

simple.

surprised we haven’t done this yet.

in between 8th and ninth grade, i was allowed a party(one person came,lol) and i was tasked with cleaning up beforehand. bored, i tossed the machete i was using to trim the vines around the deck, and cut my thumb. 4 stitches.

soon after, went to canada with my grandparents.

stitches needed removing, so we entered the nearest ER(Montreal).

waited for 20 minutes while they triaged a bunch of people from a car wreck(socialist lines!)…then they came and removed my stitches.

granddad ran around with his wallet open like a tiny bird, trying to pay somebody…”sir, it’s paid for…”

gas was an extra quarter per gallon, and a washing machine cost a bit extra…but when you needed healthcare, no one even asked about money.

that experience has stayed with me ever since.

we’re stupid, as a nation, for continuing to allow the wanton cruelty and profiteering off suffering….and to niggle over obfuscatory nonsense, like people loving their insurance plans,lol.

and to shamelessly pit the socialised elderly against their capitalised children…or the minority unionised against the majority non-unionised…is just as heartless and mean.

shame on us.

The issue of Health Care drives me nuts. Some very good points are raised here, but it’s part of the approach to the issue and discussion that makes me batty. Band-aids, not root-cause.

“In France, a visit to the doctor typically costs the equivalent of $1.12 . A night in a German hospital costs a patient roughly $11. German co-pays for the year in-total cannot exceed 2% of income, Even in Switzerland, the average deductible is $300.”

“These nations have shown that cost sharing is not necessary to keep health care spending at a level well below that of the United States. They rely on higher taxes and price controls”.

To me, the first problem is a lack of price discovery, accurate cost-accounting, and disclosure.

A visit to the doctor does NOT cost $1.12, anywhere. What does it actually cost, anywhere?

How much, beyond the actual cost, do we as a society concede to the care provider as a reasonable profit level?

Due to the very basic primal need of good health, for our loved ones, and then ourselves, we are vulnerable to abuse of that need by profiteers.

The moral component, the existence of a collective mentality and spirit, born of compassion and social justice, is lacking in many systems in varying depth and degree; it is as hard to locate in Amerika as actual cost/ price discovery in the health care arena.

So, as a nation of Christian compassion and business ‘markets’ orientation, lets agree that health care is a right and necessity for all. Then, lets recognize it as a Utility, and institute heavy regulation, price-controls, a proscribed but stated profit margin, and streamline to eliminate overhead and redundancy.

Folks sound the alarm– government-run?! Guaranteed fustercluck and disaster!!!

Outsourced, like the M I C— guaranteed $700 tongue depressors.

That fear is an opportunity.

If care is for all of us, funded by US, does it necessarily mean it has to be a crapified system?

Can’t we all work together to get everyone access to the existing pretty good care facilities, providers, and meds that are presently in existence, and get those providers a reasonable remuneration and benefits for their employees?

The system would higrade to people who want to be in it for the care, the interesting work, the compassion, and weed out Shkrelli-like profiteers— not welcome- go elsewhere.

No more Billion with a B united Healthcare executive retirement packages.

No more byzantine hoop jump, navigation, gappy-holey capitalist dream S L I C C ‘systems’.

KIS,S. We could do this.

Amfortas nailed it— gas is more expensive in Canada, and tax rates are higher. But there aren’t that much higher, and one looks around that wonderful nation to the North, there is a high-thread-count safety net, and all have access to care, parks, athletic facilities, public ‘goods’.

Seems like the time is well–past-nigh for the collective US to grow up and Go Forward.

lack of price discovery in every corner of the healthcare system is the tack that makes the suits in the elevator stammer the most.

no price discovery? then it ain’t a “market”.

wife and i have spent a lot of time in the hospital in the last year and almost a half…and the ONLY price tags are in the gift shop(“grift shop”?)

and the little starbucks wannabe in the lobby.

no one in the whole place knows what anything costs(I asked).

and since apparently no one, from the cleaning lady to the surgeon, actually works FOR the hospital(do the suits, themselves, actually work FOR the hospital? I’ll ask one next time i have him cornered), you get 20 bills, when there should be one…and they all may as well be written in sanskrit. how is that representative of “rational actors, using perfect information, to maximise utility”?

at the oncology clinic, the “financial advisor” person assigned to us(cute redhead arkansas chick) admits that she hates the Machine…but didn’t know it was this bad until she was already schooled and well into that career track.

so now she helps people as best she can.

she turned off her phone, closed the door, and turned her large screen to me…”here’s what everything costs…”…depending on insurance, medicaid, cash, etc….and it’s remarkable.

the avarice needed to design such a blatant sham is breathtaking, once you get your head around it.

Shorter the above: take capitalism out of medicine. It doesn’t make any sense and it never did. And this

explains the true intent of the ACA which was to guarantee the Medical Industrial Complex revenue stream by forcing people to take out insurance and getting government to supply extra subsidies. It was all those uninsured failing to pay that was the industry view of the crisis, not their outrageous compensation.

Unfortunately dismantling this money pit will likely prove just as difficult as tackling the Military Industrial Complex and doubtless the health care industry will be one of the leading groups fighting any Sanders’ candidacy.

It sounds like the healthcare denial cartel is taking the Sanders campaign seriously enough that they are now in the Bargaining phase. The brilliance of creating a new class of insurance for ‘cost sharing reduction’ as a solution to the existing insurance scams is a tribute to the vision and brazen arrogance of the neoliberal market-fetishists posing as policy wonks.

Zingo, SI. The “typology” of debtors is useful to total newbies. I started skimming this “healthcare essay” about one third through… ridiculous amount of complexity, enough to make me wonder what’s being hidden (and who exactly is Bob Hertz?).

Let’s do the Sanders/Jayapal proposals and negotiate only about how long to phase in various age groups, not to exceed three years.

Bob Hertz (me) is a retired health insurance agent, who you might say was able to watch the sausage being made and is now proposing reforms.

Thank you Bob

” … they can say to the provider, “I am paying cash, what is your best offer?” The Amish – who do not buy insurance, but save prodigiously – actually use this method.”

This method works, up to a point, for the Amish. Mainly because they practice a form of socialism, or communalism, within their tightly knit communities. In cases of need, the community kicks in. If not with actual cash, then with meals, child care, farm and household chores.

OTOH, their overall health is not the best, with high rates of metabolic syndrome. Dental care is positively 19th century. I know young women in their mid-twenties who have total dentures, and certainly almost everyone has them by the time they are in their mid-forties. Admittedly my first hand knowledge is limited to communities in western New York and Pennsylvania.

What about the other half of this scenario – the “supply” side, with regard to the supply of “providers” (i.e. physicians)? Many more young people, I believe, would attempt to make it through medical school if they did not have to face such incredibly daunting debt. And for many who did take on this debt, I’m hearing stories (from a physician) about physician suicides because the debts from medical school keep growing, and thus the physicians see no way out. I think a full-scale plan must also address these matters: no one should face such debt because they wish to become a physician of any kind.

I support M4A and totally agree the system is running amok – BUT – if we cancel medical debt, and student debt, what’s next? Do we forgive the debt owed by tax payers who have cheated the IRS, or are they less deserving of our largess? And since taxes have to go up to offset the costs of health insurance premiums, do we also create a class of citizens who get free health care? And, critically, do they get to vote in this arrangement since they are the primary beneficiary? What, link voting to getting free stuff? Yes, I wonder about this because it strikes me there is a parallel to the bread and circuses situation today where CEOs stack the board with those who approve their pay.

Do we really want Medicare for All, or do we want Universal health Care?

We all must be very careful in accurate diction and semantics.

Health Insurance is NOT Health Care.

Medicare for all is Not Universal Health Care.

There are a LOT of problems with Medicare— starting with Complexity, loopholes, gaps (the intrusion of for-profit Capitalism).

Might be time to start with a fresh build, purloining the best parts, and scrapping the crap.

Might be time to start with a fresh build, purloining the best parts, and scrapping the crap.

That’s what needs to happen with virtually everything, but we simply don’t know how. I would obviously never root for a major collapse that would cause untold pain, misery, and death, but I do admit to a sometimes strong desire for a slow collapse wherein we can build many localized, humane societies.

How will that happen? I have no idea.

How will that happen? I have no idea. Dan

By rubbing the noses of purported Christians with the Old Testament wrt to social justice?

Then we should quickly eliminate privileges for usurers and also provide that every citizen own some land to live, work, and work on plus an equal Citizen’s Dividend to replace all fiat creation beyond that created by deficit spending for the general welfare.

Also, while the Bible extols mercy and kindness, it REQUIRES justice and the present system is certainly not just.

IIRC, tax debt has already been mostly forgiven for the big cheats and non payers.

It took a historic financial crisis, plus a fair amount of Democratic self-delusion, just to get Obamacare passed. One Congress after another has refused to impose relatively tiny cuts in Medicare reimbursements.

Up until this point, I felt the author had at least built up points for good intentions even if his plan is ridiculously complex and impossibly drawn out in phases. But saying that it took a historical crisis just to get Obamacare through is so obtuse, never mind just plain wrong, as to cast doubt on his whole scheme. All it took to get Obama care through was a bait and switch which guaranteed the insurance industry that shooting fish in a barrel would be easier and more lucrative than ever and that they could get around most of the less profitable aspects of the scam fairly easily. True, Obama had a historical crisis, but he never had any intention of using it to the advantage of a real health care plan that would benefit his constituents rather than the insurance companies.

If Bernie can’t get the core of single payer through via overwhelming public support, it’s not worth doing as it would simply be another failure, this time proving, so the bobble heads would wail endlessly, that socialism, no matter what kind, is pure evil.

this time proving, so the bobble heads would wail endlessly, that socialism, no matter what kind, is pure evil. Brooklin Bridge

In that case let’s eliminate socialism for the banks and the rich – the reason so many are desperate to begin with.

Indeed. Perhaps I managed, as usual, to mangle what I was trying to say which was simply that our kennel of howling pundits would take any excuse to rip apart Sander’s gentle form of “democratic socialism” as more horrible by far than Dante’s ninth circle of hell.

My point is that if Sanders can not get the core of M4A passed into law, he should avoid and not embrace compromise. He could continue to make his case that we need to shift our attitudes more toward a government of, by and for the people rather than the banks and the rich and he would have the megaphone of the bully pulpit and the power of executive directives to do so. Given what he has already done, just the job of making the public more fully aware of what’s happening – such as your suggestion – would be an invaluable contribution to turning things around.

I was in DC at the time ObamaCare was being negotiated. My buddy worked for AHIP (as lobbying VP) which I know for a fact wrote the first 900 pages or so of the 1300+ pages that eventually became the law. AHIP is the national lobbying organization for America’s Health Insurance Plans. The intent was to head off at the pass anything that was not favorable to the insurance companies which they for the most part achieved. When it is by the insurance companies for the insurance companies, you get the result that we have. Most Congress critters never even read the bill

The financial crisis gave Obama the democratic majorities in the House and Senate, without which even the very imperfect ACA law would not have passed. That is all I was trying to say.

The same could be said about the 1930’s. That financial crisis temporarily destroyed the Republican ideology, and the Republican party was down to about 25% of the House and Senate. That enabled Roosevelt to pass Social Security, the SEC, the Fair Labor Standards Act , et al.b

I sometimes get the feeling, especially when it comes to profiting from health care, that neoliberalism thinks there is something hypnotizing us all like the 5 stages of impoverishment. They leave out the 6th stage which is rage. What on earth could happen then?

Yesterday commenter RWood mentioned that John Pilger’s “The Dirty War on the National Health Service” was going to play on TV here. Well it was as bad as you would expect. But there was one thing that really impressed me was some of the people that were pushing for privitising the NHS. The were right on the front line and knew that what they were doing was killing people but they did it anyway to secure themselves a comfortable living.

The push is coming from the American healthcare companies but the British politicians, bureaucrats and the media (I’m looking at you BBC) were all making it a reality no matter how financially idiotic it was. Example – £11 billion has been borrowed from private interest for the NHS over the years but they have had to pay back over £80 billion back. If the NHS had gotten the money from the government, they would have saved themselves £70 billion.

One Wall Street operator named Ali Parsi led the charge to have the UK’s Hinchingbrooke Hospital turned over to a private company for a ten-year contract but the effects were so catastrophic that the contract was terminated after only three years. But Ali had already walked away with a coupla hundred million. Remarkably there is no mention of this hospital on his Wikipedia page. Now he has helped develop an app that will replace visits to a GP. It is people like that who leave a body count behind him in exchange for more money for himself and he is typical. It’s just “business.”

What a load of crap! Insurance has no place in healthcare because their prime objective is money and how to prevent it from being spent. The answer is not to come up with ways to “fix” it, but to ban it entirely in healthcare and pharma. By arguing ways to make things better for people, all you are really doing is incentivizing insurance companies to come up with new ways to game the system and take their pound of flesh from those who can least afford it. Anyone who argues for these fixes might as well tell people who need help that they should go ahead and die quicker since they will anyway from not being able to afford care in the first place.

As for medical debt, all debt should be immediately cancelled – not just medical – and debt buying as a whole made illegal!

Thank you! My thoughts exactly.

No insurance at all!

I also think a complete debt jubilee is long overdue. People who posit “moral hazard” or “slippery slope” arguments against debt cancellation always have low and moderate income people in mind. Corporations and wealthy individuals constantly restructure

canceltheir debts legally and with no public drama.Transformation of the entire medical/financial system is long overdue.

The Debt Buyer Industry has a bad reputation and for good reason. They are typically far more aggressive than the original creditors or their hired debt collectors. There is nothing redeemable about the junk debt buying business.

I received a surprise bill and I asked my insurance company why they hadn’t paid it. They told me that it was fraudulent because they had not gotten their permission for the the doctor who supposedly joined the team. I ignored it too but the doctor’s practice turned it over to a collection agency who kept harassing me. I got my lawyer to call them and they refused to speak to him. I never paid the bill and they reported it as a delinquent. I wrote to the credit agencies and eventually got it removed from my credit report.

The hospitals, doctors (some of them), insurance companies and collection agencies are all vultures preying on the sick.

Here’s a link to an LATimes opinion piece that is related to this post:

https://www.latimes.com/opinion/story/2020-02-16/doctor-patients-send-home-to-die

Exploitation is now part and parcel of life in the United States. Everything is defined by money and transferring it to the 0.1%; the Forever Wars, Casinos, Outsourcing, Just in Time Supply Chain, Drugs, Credit Cards, Subprime Financialization, Housing Rentals or Health Care. The right to life, liberty and the pursuit of happiness was sold down the drain. Once their wealth is extracted, patients are sent home to die. If the contagious Wuhan Coronavirus does not mutate to a less deadly form, neoliberalism will crash along with trade, society and politics in the coming months. A pandemic can only be overcome if everyone works together, greed is banished and society practices sound science.

The costs for “undocumenteds”? Easily dealt with.

First, terminology; they ARE “documented” — in their home countries, where they belong. To GET them documented, send them home where they ARE documented.

Second, if while here they incur medical costs, bill their country’s embassy. No pay, confiscate the place, sending all its occupants home.

Third, we need taxes on remittances, charity, and foreign aid at whatever percentage level it takes to cover illegal aliens’ medical and welfare costs while they’re illegally visiting. If it takes 100%, so be it.

==========================================

I do like the idea of buying up all zombie medical debt at its going very low price, so as to cancel it. This needs doing.

Your comment upsets my stomach.

Sj, that’s not a rebuttal. It’s not even an argument nor remotely relevant to the discussion. Why did you take up space to say that?