Yves here. We had predicted that the sharp rise in mortgage rates precipitated by the Fed’s taper talk would put a damper on the housing “recovery” and could even send it into reverse if rates continued to increase. They’ve in fact fallen over the past few weeks but are still markedly higher than in the spring. The central bank has been sending mixed signals over the last week or so, on the one hand seeming more inclined to taper based on its cheery view of the fundamentals, but concerned over what a budget slugfest might do to the confidence fairy.

MacroBusiness provides a good overview of the latest releases. It’s important to notice its comments on consumer deleveraging. That’s a decided negative for growth, particularly in combination with the ongoing effects of the sequester.

As Wolf Richter pointed out:

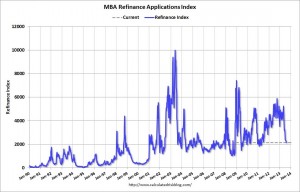

Mortgage applications have been on a brutal decline that started in early May. For the week ending August 9, the Mortgage Bankers Association’s Composite Index dropped 4.7%, with the Refinance Index down 4% and the Purchase Index down 5%. It isn’t a fluke. Mortgage applications have plunged 50% from early May and have hit a level not seen since April 2011.

Average interest rates for 30-year fixed-rate mortgages, at 4.56%, are nearly a full percentage point higher than in early May. These higher rates have been colliding with much higher home prices. Result: a dizzying jump in mortgage payments. Sticker shock for prospective buyers.

So first-time buyers now account for only 29% of total sales; prior to the housing crash, they accounted for up to half. The Fed’s “wealth effect” policies are pushing average Americans out of the housing market. Of course, they don’t have to be homeless. About half of the vacant single-family homes that these private equity firms and REITs have acquired are still vacant – maybe they’d cut some deals on rent.

By David Llewellyn-Smith, founding publisher and former editor-in-chief of The Diplomat magazine, now the Asia Pacific’s leading geo-politics website. Cross posted from MacroBusiness

Last night markets appeared to embrace more taper prospect. However the data was not favourable. It is now quite clear that the US mortgage market has turned sharply on the taper inspired spike in bond yields and hence mortgage rates. From the Mortgage Bankers Association:

Mortgage applications decreased 4.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 9, 2013. … The Refinance Index decreased 4 percent from the previous week. The seasonally adjusted Purchase Index decreased 5 percent from one week earlier. … The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,500 or less) decreased to 4.56 percent from 4.61 percent, with points decreasing to 0.39 from 0.42 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. … The average contract interest rate for 15-year fixed-rate mortgages decreased to 3.60 percent from 3.66 percent, with points decreasing to 0.35 from 0.43 (including the origination fee) for 80 percent LTV loans.

As usual, Calculated Risk has the charts:

Remember that US house prices actually track the refinancing index quite closely so I expect price gains are likely to slow sharply in the not too distant future, slowing consumption as well, although the new construction wave will proceed. Nonetheless, the 30 year bond is sitting right at the top of its recent range with yields at 3.75%.

Also weighing against any imminent taper were producer prices, which were unchanged on the month and sit at 2.1% year on year.

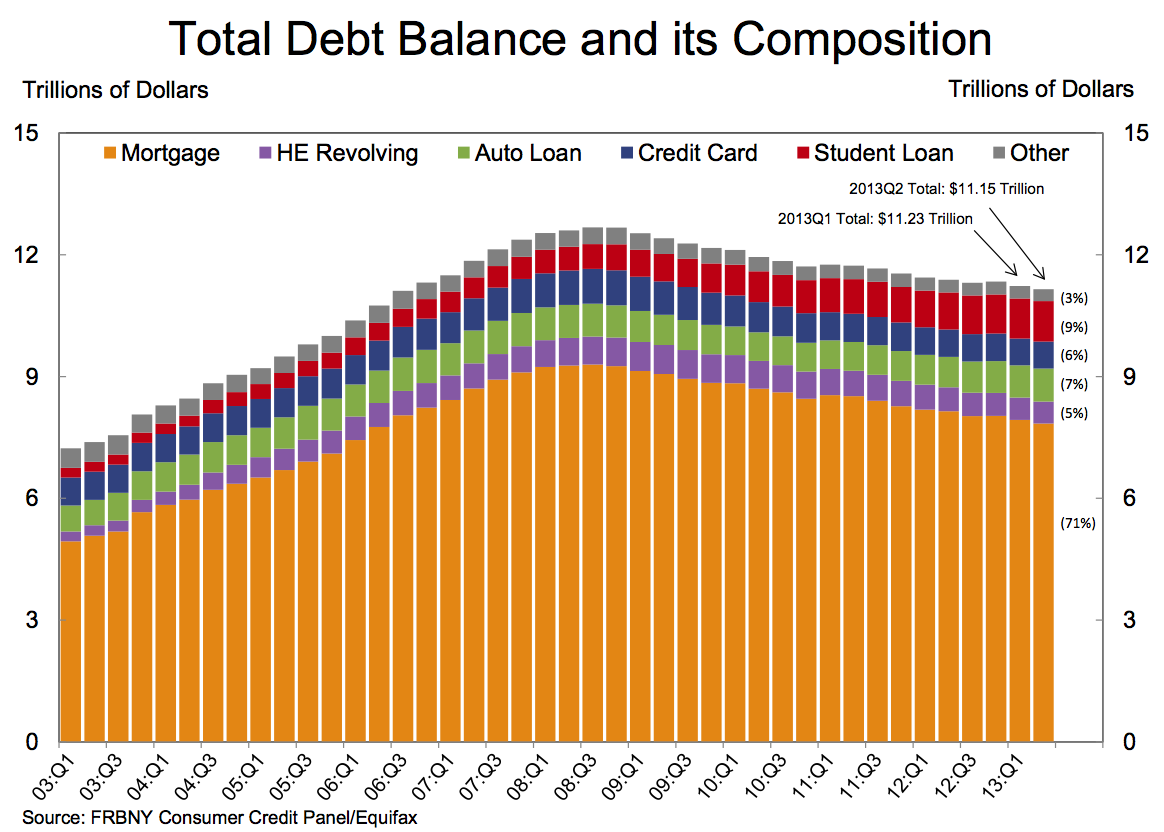

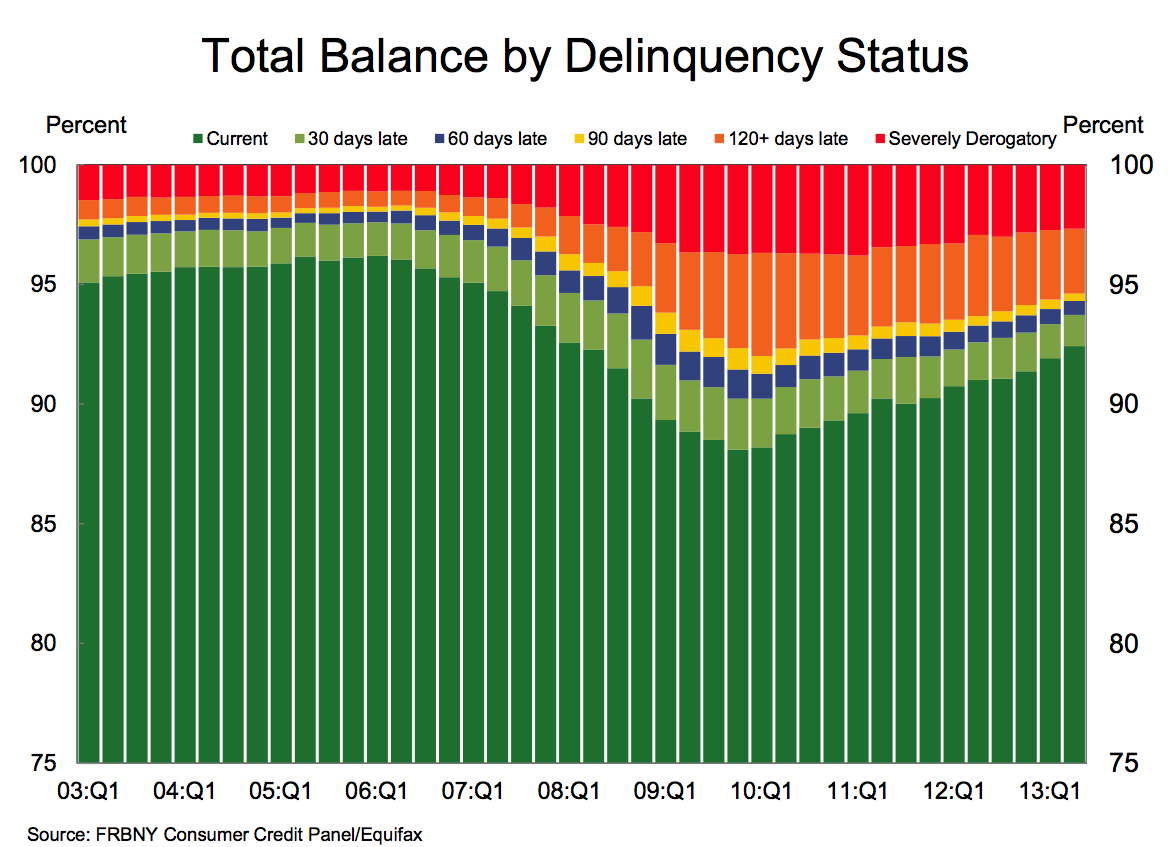

Rounding out our evening’s data, despite the recent surge in mortgage debt, US households continue to deleverage, according to the Fed:

The Fed told us it was going to taper to prevent excessive leverage building up as the cycle accelerated. It is succeeding but growth is not going to accelerate as a result.

it’s a three step process to navigate from the link above to the source of a larger version of NY Fed / Equifax charts posted at the end of the post above…

here’s a shortcut:

http://www.newyorkfed.org/research/national_economy/householdcredit/DistrictReport_Q22013.pdf

those charts are on pages 5 and 10; there are several others in that report you’ll all find interesting…hope to get to it this weekend..

here’s a direct link to the calculated risk post that will get you larger versions of those graphs:

http://www.calculatedriskblog.com/2013/08/mba-mortgage-applications-decrease-in.html

At that rate of deleveraging, and with almost no growth in the US economy, and certainly not in the productive sector as almost all the growth taking place is in the parsitic financial sector, how many decades is it going to take for the US to get back to a manageable Private Debt to GDP ratio?

The American people: debt slaves forever!

If that is of any comfort, the Americans are certainly not alone in that! It is a problem of virtually the entire world on a deeper scale.

Misery loves company, but it loves relief even more. Let’s hope that company breeds solidarity and solidarity leads to action, since relief is unlikely to come to us of its own accord.

Misery is the river of the world….. everybody row

@ f Mexico, Nice!

American people: “Doc, I’ve got a problem.”

Doc: “Take 2 Taperalls and call me later.”

American people: “You mean in a couple of decades?”

again, from Mejico,

Gore Vidal (RIP) stated after Wall $treet economic disaster-bailouts, that the U.S.

would now suffer at least 2 Japanese style “lost decades”…and economics would never be the same…

NC issues and visitors here take account of a variety of responses towards identifying this apparent reality…

We can study history, of which you are well aware…and great proponent of, in

identifying pertinent realities…

I often note 70’s-80’s Milton Friedman-“Chicago Boys” actions in South-Central

America…as intoned by Perkins’, “Confessions of An Economic Hit Man”, or Klein’s, “The Shock Doctrine-Rise of Disaster Capitalism”…

My own background being 70’s-80’s Poly-Sci, and living-instructing around the world, a variety of discipline…

(keep it up-you’re a treasure)

10 yr yield @ 2.8% as I type this. Yield now close to double where it was only a few short months back. And as Mexico accuratly said, deleveraging has a long way to go on the private debt side of the ledger. Given the 10 yr’s rise there sure doesn’t seem to be fear in the air either. I guess all the gamblers feel secure the Fed Put will ride to the rescue at a moment’s notice. With backing like that guess they feel just fine to party on while Rome burns and takes most of us with it.

NY Fed report says HH debt now down 12% from peak.

The deleveraging in the housing sector is heavy, especially considering the gains in auto loans and student loans recently. New high mortgage rates and the drip drip of foreclosures should continue that deleveraging for some time, I’d say.

P.S. with near 0% financing on new auto loans, it’s not surprising that auto loans are booming.

Continues to amaze me that the ‘rise in house values’ is somehow a wealth effect when the opposite is true.

Creation of wealth requires human labor. Rising house prices does not create wealth…it raises the cost of living and working and producing. It also increases the financing required (increases the interest stream to lenders in the form of economic rent. Along with this effect – the purchase of homes by institutional investors who are looking for a return in rent..raises rent costs – this again creates a situation where it costs more for most to live and work. The only times when housing (as opposed to land value) creates wealth is when human labor is employed to either build a new dwelling or upgrade an existing stock….with more money needed to purchase land on which to build or more money required to purchase an existing house…less is left over to employ labor to create wealth.

So, with stagnate wages – or even dropping wages – there is not enough money to afford the overpriced assets and economic rent extraction games or economic wizards say we must.

With millions of homes empty and millions of people needing shelter – something is fundamentally wrong.

To correct wrongs IMO taxation has always been a way to inhibit economically destructive activities. A free market means a market free of economic rent… thus, to achieve a free market… it should be obvious that the solution would be to tax (at a very high level) those economic rent seeking behaviours back into the common weal.

I dare say, tax those activities that are not wealth producing and, un-tax wealth producing activities. One step further… tax land values and de-tax the built part of land….Built—as in built using human labor and real capital not financial capital.

You’d love the UK. Our government is underwriting 20% on houses up to around $850K. Yes – apparently even people buying $850k homes need state help.

To be fair to the establishment it’s brilliant. Unhappy populace? Just add a zero to everyone’s house price. They love it!

One thing that policy seems to be achieving is to highlight the distinction between places that have a healthy base of worthwhile jobs, and places that don’t. I’ve been tracking prices in York for the past 9 months or so. Semis and detached houses in the 200-250 range stick around on the market for quite a while, and generally only move after an asking price decrease.

A mystery to me is why would you pay 550K for a semi in West London when you can get the same thing in York for 200K. It needs to be a hugely, stonkingly, remunerative job for you to be able to afford to finance the difference.

I conclude that people in decent housing in York are either working in Leeds and commuting, or retired and can live where they please.

TomDor makes some really good points.

It has always been a mystery to me why the elite doesn’t acknowledge what makes labor in the developed world so expensive. It is not unions or regulations but the high cost of living relative to the developing world.

If the elite of the developed world wants to make labor “competitive”, isn’t it a logical first step to make the cost of living cheaper so that people could live on lower income?

Here here. Here is a typical set of UK headlines:

* price of petrol goes up – bad!

* we need to devalue GBP to make our exports more competative

* house prices are up – hooray!

The big problem is the population lap it up. Our education system ensures they cannot join the dots.

As your brilliant compatriot George Orwell had said, it takes great courage to acknowledge what is right in front of your nose.

Truest words on the Internet… ever.

Are the values for ‘Total Debt Balance’ inflation adjusted? I don’t think it is. If you adjust the peak level to current dollars, you get $13.8T. So today’s level of $11.15T is nearly 20% down.

good point…

a bit of high inflation would go a long way in wiping out that debt in real terms…

but it would also reduce the real value of it to the rentier class, which is why they’ll never let it happen..

I wish the terms ‘rent’ and ‘rentier’ would be used more in economic discussion. They figure prominently in the Capitalist Bible (The Wealth of Nations), but it is a concept many conservatives would be wholly unfamiliar with. They seem to believe that any means to making money is OK and the all impact the economy similarly. Rent seeking is truly just grabbing a bigger share of the pie, whether the pie is getting smaller or not.

Since the 1980s, mortgage originations have gone through boom/bust cycles based on interest rates (i.e. Fed policy), which have a huge impact on the volume of refinancings, less so on home purchase mortgage volume.

This is the sort of slowdown we should have seen in 2004-2005, but for Greenspan telling the public to use ARMs and affordability products.

ugh…greenspan-“Certainly the most influential voice on DEregulation”:

http://www.youtube.com/watch?v=PWen53eqmJo

Homes are moving again in my upper middle class area of San Diego where people typically stretch to buy.

But home prices have most definitely stopped appreciating. They are now selling for about 5 percent less actually. It’s like somebody reboot the computer, the market has changed seemingly overnight.

If rates make another big jump I expect this to happen all over again. However, things just got interesting in the markets today with a key intraday reversal. This could be a top in rates for a while.

Susan, is the purchase index seasonally adjusted? If it is not then I would take that graph with a grain of salt. As far as refis-that cannot go on forever, and unless the gov’t is going to guarantee mortgages and hold them at 2% there’s no more refi demand, unless you start lowering standards such as LTV, DTI etc, and I don’t think we ought to there.

If the gov’t wants to see a better housing picture, it needs to focus on improving borrower income levels and stop propping up home prices which only limit affordability.

from the press release, linked above:

The Market Composite Index, a measure of mortgage loan application volume, decreased 4.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 5 percent compared with the previous week. The Refinance Index decreased 4 percent from the previous week. The seasonally adjusted Purchase Index decreased 5 percent from one week earlier. The unadjusted Purchase Index decreased 6 percent compared with the previous week and was 4 percent higher than the same week one year ago.

another piece of the puzzle:

Report: Half of All Homes Are Being Purchased With Cash — WSJ:

More than half of all homes sold last year and so far in 2013 have been financed without a mortgage, according to an analysis by economists at Goldman Sachs Group.

That is an astonishing datapoint. For speculation, or for habitation?

for both.. and you can include money laundering

A must read… with ominous undertones from the O=bot-orator.

President Obama gave a speech on winding down Freddie Mac and Fannie Mae, the GSEs often blamed for the housing crisis and a darling of conservative ire. Government sponsored enterprises, or GSEs buy up mortgages from private lenders and the theory is to loosen up funds to stir additional lending. Right now, GSEs have guaranteed 87% of all mortgages. Yet, the President’s speech was spattered with lies, spin and blame. Here are some lowlights.

Did you know homeowners were reckless with no mention of the derivatives, those mortgage backed securities now being bought up by the Federal Reserve, that fueled the housing bubble?

Over time, responsibility too often gave way to recklessness – on the part of lenders who sold loans to people who couldn’t afford them, and buyers who knew they couldn’t afford them.

We’ve made it harder for reckless buyers to buy homes they can’t afford

Foreclosure statistics are amazingly tricky with little accuracy. Completed foreclosures estimates range from 4.5 million from January 2008 to over 20 million, counting the years of the start of the housing bubble collapse, 2006 and 2007. Right now there are 3.1 million foreclosed homes listed in police auction sites and a new book claims over 10 million families have been displaced. Regardless, blaming homeowners when jobs are low paying, non-existent, temporary and cannot pay for the rent of a cardboard box is unbelievably callous and just plain wrong. People lost their homes primarily because they lost their income and ability to earn, not because they were reckless. People were hoodwinked, lied to, given the runaround and sold a bill of goods, all the while getting their property and livelihoods sucked out right from under them. – snip

Obama also seems to be killing the American dream of owning property entirely.

Step five: we should make sure families that don’t want to buy a home, or can’t yet afford to buy one, have a decent place to rent. In the run-up to the crisis, banks and the government too often made everyone feel like they had to own a home, even if they weren’t ready. That’s a mistake we shouldn’t repeat. Instead, let’s invest in affordable rental housing. And let’s bring together cities and states to address local barriers that drive up rent for working families – snip

Go to links on right margine @ economicpopulist privatizer-chief-obama-blames-reckless-homeowners

skippy… got that… get in the pit… non-weatlhy consumers slaves…

When the comments submitted past through the gastrointestinal spamorator… please delete all save the last one, umk Lambert.

skippy… wow how are Americas going to mentally deal with 3rd world economics being shoved down their gob… its breath taking.

How are Americans taking it?

Many are fighting their better off “neighbors” for scraps as they have been brainwashed to do instead of focusing their angst on the plutocrats that own our current Western Bloc world.

There will never be “jobs” for all and contribution to and responsibility to society needs to be redefined. At least into something that no longer reinforces inherited accumulation of money and social control into few hands over long periods of history.

We suffer under a class system that many are brainwashed to believe doesn’t exist.

I’m calling it… aMEirca is a fully fledged theocracy which foundation is egregious privileged wealth… en fin~

skippy… every political act is guided by servitude, preservation, continuance, to maintaining this theocracy… no matter the future consequences.

A very bad post. Mortgage lending already tumbled. MBA is a waste of a index because it doesn’t take into account cash and non-mortgage lending. When you are buying home without mortgage lending, that is a good sign. A real good sign.

If first time buyers were 50% prior to the crash, what were they prior to the boom? Most homeowners own more than two houses during their lifetimes so to me, 50% first time buyers looks likely to represent a bubble percentage caused by an influx of under qualified purchasers driven by the fear that they would be “priced out forever.” We shouldn’t use the bubble build up period as a yardstick to judge “normal.” Today’s distressed young homeowners and foreclosees might well have been getting ready to buy now if they hadn’t overleveraged themselves with the excessivly free lending of the bubble.