Yves here. We’re a little EU-centric tonight as a result of a wealth of particularly good material, which is often a sign that stresses are rising (there was tons of good material in the runup to the crisis as well).

These analyses of the state of play come as the pushback against Germany’s vision of strict adherence to austerity is increasing. As Ambrose Evans-Pritchard writes today, the new Italian premier Enrico Letta (and remember, Italy can credibly leave the eurozone) has declared himself to arresting “death by austerity.” France’s Hollande had a speech leaked that lambasted austerity as well as “egoistic intransigence of Mrs Merkel”. And EU Social Affairs Commissioner László Andor is pushing for another change in German policies, that of higher wages.

The wee problem with all of this is that German elections are in September, which is an eternity in political terms. The German electorate has been conditioned by the media to see the citizens in periphery countries as lazy profligates and/or tax evaders, so calls for relaxation of austerity are likely to be seen as malingering, despite incontrovertible evidence that the wearing of hair shirts is only making matters worse. And on top of that, the German parliament has to approve lending to Italy under the OMT, and hectoring by various foreign officials is not likely to improve their mood.

In other words, the sort of playing to prejudice that has served German leaders so well is now restricting their ability to moderate course (and that’s even charitably assuming Merkel understands that persisting in a failed strategy will only compound the costs and increases the risk of a eurozone breakup).

I’ve been saying for months that the current configuration has a 2008 feel about it, in that the incumbents want to paper things over at least until an election has passed, but it looks like events won’t cooperate.

By Jesús Fernández-Villaverde, Professor of Economics, University of Pennsylvania and Luis Garicano, Research Fellow with the Productivity and Innovation Programme, Centre for Economic Performance; Professor of Economics and Strategy, Departments of Management and of Economics. Cross posted from VoxEU

By the end of the 1990s, under the incentive of Eurozone entry, most peripheral European countries were busy undertaking structural reforms and putting their fiscal houses in order. This column argues that the arrival of the euro, and the subsequent interest-rate convergence, loosened a tide of cheap money that reversed the incentives for further reforms. As a result, by the end of the euro’s first decade, the institutions and governance in the Eurozone periphery were in worse shape than they were at the start of the decade.

The conventional wisdom before the creation of the euro was that the monetary union would force its least productive members to undertake the structural reforms needed to modernise their economies. In the past, the peripheral European countries had used devaluations to recover from adverse business-cycle shocks, but without correcting the underlying imbalances of their economies. The euro was expected to eliminate the bias of their monetary policy toward inflation, force sound fiscal policy and encourage widespread liberalisation.

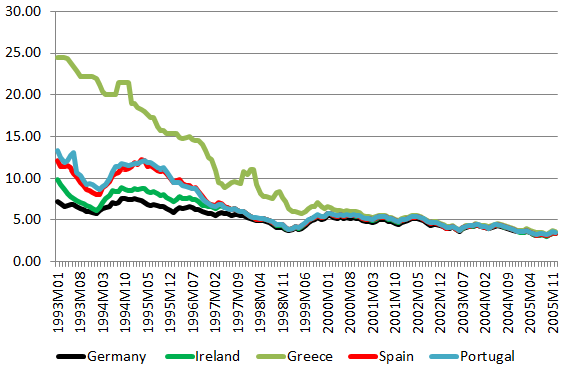

By the end of the 1990s, under the incentive of Eurozone-entry, most peripheral European countries were busy undertaking structural reforms and putting their fiscal houses in order. However, the arrival of the euro, and the subsequent interest-rate convergence (see Figure 1), loosened a tide of cheap money that reversed the incentives for further reforms. As a result, by the end of the euro’s first decade, the institutions and governance in the Eurozone periphery were in worse shape than they were at the start of the decade. The credit bubbles unleashed by the euro not only undermined competitiveness and increased indebtedness, but they also undermined the institutional basis of these economies.

Figure 1. Government bonds, ten-year yields

Source: Eurostat.

There were two main channels through which these large inflows of capital led to the abandonment of economic reforms. First, they relaxed the constraints under which agents were acting, thus reducing the pressure for reforms. Second, they made it harder for principals in both the public and private sectors to extract signals about who was performing well or poorly. When banks are delivering great profits, all managers look competent; when countries are delivering the public goods demanded by voters, all governments look efficient. As a consequence, bad agents were not fired, incompetent managers kept their jobs and inefficient governments were re-elected. The efforts to reform key institutions that burden long-run growth, such as rigid labour markets, monopolised product markets, failed educational systems, or hugely distortionary tax systems plagued by tax evasion, were abandoned and often revoked.

New Research

In Fernández-Villaverde, Garicano and Santos (2013) we examine this mechanism, develop a framework to understand it and apply it to the experience of Spain, Ireland, Greece and Portugal. We then argue that the same circumstances that allowed delays in the periphery actually forced reform on a reluctant Germany.

Spain

In Spain, the years before the euro were auspicious for reform. In particular, Spain’s fiscal position was consolidated and several strong multinationals appeared as a result of a wave of privatisations. But Spain’s real-estate bubble turned the clock backward. Meagre attempts at reforming the malfunctioning labour market in 2002 were not completed, the educational system suffered an increase in the dropout rate, and local governments and a large segment of the financial system were infected by the pervasive corruption engendered by the real estate boom.

Ireland

Similarly, Ireland had introduced important economic-policy reforms since the second half of the 1980s, including labour-market reforms, and had liberalised strategic sectors of the economy such as air transport and the telecommunication system. These reforms helped to deliver real annual output growth that averaged more than 6% from 1987 to 2000. However, as real interest rates dropped, Ireland became the country with the highest share of housing investment in gross capital formation in the EU. Rather than seeking to counterbalance the bubble, governmental policy accentuated it through regulatory and tax changes – such as reductions in stamp duties or increases in the ceiling on income-tax deductibility of mortgage interest – that made real-estate development even more attractive. Moreover, several major legislative changes worsened financial supervision. Probably not unrelatedly, from 1997 to 2007, 49% of disclosed donations to Fianna Fáil – the party in government- were from property developers and the construction industry (Byrne 2012). Thus, Ireland, instead of transitioning toward a lower, more sustainable rate of growth based on productivity gains, went from growth based on increases in the employment ratio to a speculative cycle.

Greece

Greece is the poster child for postponed adjustment. Greece’s curse, more than any of the other peripheral countries, was an unreformed economy. Although the examples of arrested reforms are many, one of the clearest is the pension system, where reform has been considered imminent at least since 1990 as the system faced both a dramatically rising dependency ratio and an overly generous replacement ratio (OECD 2009). Furthermore, the system was extremely fragmented, with 236 separate funds in 2003 (O’Donnell and Tinios 2003) that caused inefficiencies and duplications and yet left many pensioners at risk of poverty. There had been sporadic attempts at reforming this defective system. Some changes had taken place in 1992 when the budget was under serious strain, but they did not tackle the long-term imbalances. The year 2001 saw the defeat of a reform package of the pension system that had first been proposed in 1958 and was already considered extremely urgent (Borsh-Supan and Tinios 2001). A new reform package, characterised by creative accounting and little real reform, sailed through parliament in 2002. The government of Greece had been under some pressure during the negotiations about joining the Eurozone. But once Greece had entered the Eurozone, the pressure was off, pension and other economic reforms were abandoned and not taken up again until Greece was already in the midst of the worst of the economic crisis.

Portugal

Finally, after 15 years of economic growth that followed its accession to the EU, Portugal’s economy stagnated around 2000. Shockingly, in 2012, Portugal’s output was lower than in 2001. The headline government budget deficit never fell below 2.9% of GDP and the primary balance was constantly in deficit, even after controlling for the effects of the business cycle and one-off and temporary adjustments (Marinheiro 2006, updated 2011). The parade of deficits led public debt to accumulate from 51.2% of output in 2001 to 92.4% in 2010. The private sector responded to the stagnant economic outlook by reducing its saving rate and heavily borrowing from abroad to finance current consumption, while investment fell as a percentage of national demand. In short, the behaviour of both the public and the private sector was unsustainable in the medium run. However, accession to the euro allowed both the public and the private sector to postpone the day of reckoning by taking advantage of the historically low interest rates. For example, while government debt as a share of GDP rose by 41 percentage points, interest paid on the debt barely budged; it was 2.9% of GDP in 2000 and 3% of GDP in 2010. Thus, the euro allowed Portugal’s political-economic equilibrium to be sustained in the medium run by the large capital inflows from the rest of the world, even if a correction was eventually unavoidable.

Germany

On the other hand, in the years after the introduction of the euro, Germany undertook painful reforms of its welfare state and labour market (particularly those known as Hartz IV). Germany’s poor economic performance in the late 1990s, the accumulated costs of reunification and the adverse demographic trends had placed the welfare system under severe strain. Why did the euro not have the same effect in Germany as in the peripheral countries like Spain, Ireland, Greece and Portugal – namely, to postpone reforms? In our view, and consistent with our hypothesis, the answer lies in the paths of interest rates shown in Figure 1. For Germany, the euro meant tighter budgetary and fiscal constraints but not looser financial conditions. Absent the leeway provided by a financial boom, politicians had no choice but to act.

In summary, while observers had expected the arrival of the euro to lead to a modernisation of the peripheral European economies, the steep financial boom derived from the drop in exchange-rate risk and from the Eurozone-wide financial bubble meant that the budget constraints that these countries faced were loosened, rather than tightened. Countries that could cheaply borrow delayed painful reforms. Moreover, accountability was lost during the bubble as bad decisions had no negative short-run consequences, since rising asset prices hid all mistakes.

Avenues for Future Research

Our work suggests several avenues for future research. First, while case studies are ideal for providing a careful analysis of the mechanisms at play, a more systematic empirical analysis of public and private governance in bubbles is necessary to test our theory. Second, as our work is currently in progress, our hypothesis on signal extraction in bubbles needs to be formalised. Third, our theory suggests that there may be differences between how damaging private and public bubbles are. Private bubbles appear to be more damaging, since they not only affect the sustainability of public finances but also damage governance in the private sector. A final issue concerns the broader applicability of our analysis. Are all situations in which financing is plentiful and cheap conducive to the deterioration of governance and the abandonment of economic reforms? If so, this situation is currently the one the US, at the zero lower bound, is facing, in which case our analysis suggests that a similar deterioration of public and private governance may occur.

See original post for references

A really insightful post.

We know that The First Commandment of Neoliberalism is: Thou shalt not place any restrictions on the blowing of debt bubbles. In practice, this means the abandonment of any and all macro- and micro-prudential banking regulation.

The Second Commandment of Neoliberalism is: Thou shalt not place any restrictions on free trade.

The Third Commandment of Neoliberalism is: Thou shalt not place any restrictions on free capital flows.

The Fourth Commandment of Neoliberalism is: Thou shalt peg thy currency to that of a more industrialized economy.

Religious adhereance to the first four Commandments of Neoliberalism (engraved in stone, of course, in the book of Genesis of the IMF/World Bank bible) is guaranteed to produce the same result every time, everywhere. No exceptions.

Nice commandments. However I always thougth that inflation was the unforgivable sin that had to be mentioned in the First Comamndment.

Yep. We gotta fit this Commandment in somewhere:

We could call that the Paul Volcker Commandment, since that was the one he invoked in his jihad on labor.

THIS SITE IS UNDER SUSTAINED LIBERTARD TROLL ATTACK!!!

DO NOT RE-BOOT YOUR COMPUTER, OR RUN SAFETY SOFTWARE. UNFORTUNATELY, LAMBERT IS TEMPORARILY MULCHING. NORMAL SERVICE WILL RESUME SHORTLY.

Lambert Mulching …knee slappin

i should know better than to eat while reading this site…what a mess

Volker’s high interest rates killed the inflation caused by the hot money created by the increases in the price oil and the cost of the Vietnam War. It was Reagan’s killing of the flight controllers union that sent the signal to business that the consent of the Unions needed for the Cold War was over. Nixon had opened up China. Soon the marching of the factories to the non-union south onto Mexico could jump the Pacific.

Now the wage price spiral stagflation of the 70s could be headed off at the pass. After the Cold War ended the gains in productivity from the computer didn’t need to be shared. Instead increased credit was given. Even with gas and food costing more than any wage increases, there are no stikes getting commensurate wage increases. Globalization has killed the wage price inflation. The Fed can give trillions to finance and it doesn’t show up in the CPI. Trillions of dollars going to money heaven from bad loans also helps.

The Federal Reserve’s strategy only worked in the short-term. By continuing to crush wages while productivity and economic growth were on the rise they ensured that we’d enter into an era of debt bubbles that remarkably resembles the 1920s era. Even with political considerations aside, (ie; Mellon/Bush tax cuts, military spending, shifting the tax burden) the distribution of wealth massively skewed towards the top income levels.

This ensures that the Fed cannot stop the current economic paradigm from unraveling. Bernanke gave it his best shot. In the end all he did was kick the can a few times. Ultimately they’re powerless as long as any of the economic gains they generate end up in the hands of the few. This realization is why the Fed took the backseat with regards to the Treasury during the Great Depression.

Globalization finished off what was going to be the end of an era of labor power in the United States. The labor unions had already begun to turn their back on the New Deal coalition before Reagan. This reached it’s apex during the Carter Administration. Without their political patrons in the Democratic party they plunged themselves into the abyss of their own irrelevancy. Instead of forging ahead they eventually crawled back to their Democrats. Only now the Democrats no longer needed the backing of labor. So they took labor union support for granted. Which they still do as a matter of fact.

We’d probably all be in a better economic position if the remains of the New Deal coalition hadn’t died. Still the odds that liberal idealists and labor unions could hold together during the economic and social upheaval of the 1960s and 70s was slim. Which ushered us into another era of laissez-faire capitalism and heralded the rise of the neoliberals and the neoconservatives alike.

As long as the economic interests of the labor unions clash with the social crusade of the liberal classes over issues like immigration any partnership will not endure for long. This represents one of the greatest challenges that any new political coalition faces.

Liberals may lament the passing of the New Deal era but they sure don’t seem intent on preserving it’s political basis. They are what Reinhold Niebuhr called the foolish children of light.

from Mexico: I really must register a protest here. Inflation certainly rates a higher category than venial, mortal at very least if not all the way to the completely unforgivable sin-against-the holy-Troika.

I think you have 2 and 3 confused between the kabuki theater and the actual policy.

Neocons/libs hate average citizens engaging in consensual trade. They prefer tightly regulated fiefdoms where people, goods, services, money, ideas, and everything else have to filter through the sieve of the state.

That’s true.

There’s a very large difference between the way neoliberalism works in theory, and the way it works in practice. You gotta watch what these guys do, and not what they say.

Insightful comment. Thank you.

Interesting paper. Nevertheless, when explaining the differences amongst Germany and europeriphery nations, I prefer Pettis’ way to explain it. What happened in Germany was the mirror image of what happened in periphery nations. Tightening fiscal policy in Germany increased savings in Germany and caused huge capital flows to periphery nations whose leaders were unable or unwilling to control/manage properly.

For me, the most interesting paragraph in this paper is when it explains the effects of capital inflows in the governance in periphery countries:

“Second, they made it harder for principals in both the public and private sectors to extract signals about who was performing well or poorly. When banks are delivering great profits, all managers look competent; when countries are delivering the public goods demanded by voters, all governments look efficient. As a consequence, bad agents were not fired, incompetent managers kept their jobs and inefficient governments were re-elected.”

I 100% agree with this view. Mr, Aznar, who governed Spain between 1997-2004, is a perfect example of incompetency that appeared great by the time (no one was able to critisize the economic performance then). Yet, this guy proudly says even these days that “he was the one who brought the AAA to Spain” when in fact his government paved the way for the housing bubble and associated corruption. Now we are having a hint of how his party was corrupted with illegal private donations mainly from the residential construction sector.

Exactly. But Thou Shalt not negate the perfect information and equilibrium of the Market as it is ALWAYS correct and has the perfect knowledge of past, present and future.

Ignacio says:

I like that.

Essentially what the German government did was to murder German labor in favor of the German oligarchs. This meant that German workers were no longer paid enough to consume the goods they produced. Credit was tightly controlled in Germany, however, so the goods ended up being exported to the perifery, where they were sold on credit. The German oligarchs thus became the owners of vast quantitites of paper, loans, debt, or whatever you want to call it, owed by the perifery countries. The German oligarchs are now hell bent on collecting on that paper. All the contortions and backflips the Troika is currently going through are attempts to make that paper good.

The only problem is that, as Michael Hudson is fond of saying: “Debt that cannot be paid, won’t be paid.”

Had they consumed their own production, they would have become net energy importers… that is an unsustainable proposition.

They need to sell added value stuff to get to consume energy… like most of Europe… the financialization of the markets is closely tied to our consumption of energy.

Now, look at Japan… a looming disaster.

• Moneta says:

It’s sustainable if there’s balance of trade. Unsustainablility is caused by debt-trap dynamics, which are caused by cronic trade and current account deficits.

• Moneta says:

I have not the foggiest notion what you’ve talking about. Energy products are traded just like any other commodity.

I don’t agree. Imbalances can be caused by differences in natural riches.

Imbalances are a fact of life. Everyone wants waterfront property but not everyone can get it. That’s why we fight. And after thousands of years, we still have not found a solution for this natural unfair distribution of natural resources. And more than ever, we pretend it does not exist!

The UK was a successful colonizer because it was constrained by the island. It knew it had to exploit foreign land to stay wealthy.

France colonized because it was greedy and did not want its rivals to gain a competitive advantage… every time it ran into trouble, it would navel gaze and focus inwardly. France is probably the most advantaged European country in terms of riches, geography and climate.

So if the countries with less natural bounty want to consume more than what nature has given them and the countries with the bounty don’t want to give it away… we’re got a problem…. that’s what history is made of!

Two questions:

1. Who are these German oligarchs?

2. How to do get from “tightening fiscal policy in Germany increased savings in Germany” to “German workers were no longer paid enough to consume the goods they produced”?

I also believe that the issue of German wage depression is being somewhat exaggerated here on Naked Capitalism. While realy wages in Germany declined by 4% between 2000 and 2010, unit labour costs remain comparably high in Germany compared to other EU countries.

Germany’s continuing economic success in regard exports has more to do with what the German export industry specializes in (high quality consumer durables and high-tech capital goods) than with low labour unit costs.

So what do we have here, another neoliberal apologist living in his defactualized world?

I’m sorry, but rambling about “oligarchs” and quoting other people’s thoughts without being able to tie it into some form of coherent argument makes you look like an idiot. Coupled with your completely uncalled for ad hominem it tells me that you’re not actually interested in debate, you merely want to rant.

You “repsonse” neither addresses my point, nor does it answer my questions.

Here’s a chart of international labour unit costs:

http://www.iwkoeln.de/_storage/asset/97356/storage/iwm:image-zoom/file/2306513/01282077.jpg

Enjoy.

Um, Max, this is Naked Capitalism. Ranting about oligarchs is what they do around here, and if you present counterfactuals, they accuse you of being a paid troll.

@ Max Laue

Like all true believers, I see that you just don’t do factuality. And when presented with facts that counter your deeply held beliefs, you get all emotional and go ballistic.

The facts are, however, that German workers have lost much of the comparative advantage in pay they once enjoyed over workers in the perifery.

For instance, by 2011 German manufacturing workers had lost 28% of the pay advantage, relative to the perifiery countries, that they had enjoyed only 15 years earlier.

In 1996 a German manufacturing worker made 450 percent times as much as a Portuguese worker. In 2011 he made only 358% times as much.

He made 263% times as much as a Greek worker. In 2011 he made only 222% times as much.

He made 220% times as much as a Spanish worker. In 2011 he made only 175% times as much.

He made 182% times as much as an Italian worker. In 2011 he made only 144% times as much.

He made 174% times as much as an Irish worker. In 2011 he made only 111% times as much.

ftp://ftp.bls.gov/pub/suppl/ichcc.ichccaesuppt2_2.txt

@ Sid_Finster

I see the neoliberal true believers are out in force today.

And just like Max Laue, I see you’re short on facts and long on rhetoric.

[ad hominem –ls]

1. I do not subscribe to the ideology of neo-liberal economics. I have no idea where you even got the idea. Challenging you on your bullshit does not make me a neo-liberal “true believer”.

2. I merely pointed out that, even after a real wage contraction of 4% between 2001 and 2010, and even though other Eurozone countries saw strong wage increases, Germany still has some of the highest unit labour costs in the world.

3. The numbers you just quoted don’t contradict anything I have written. Yes, the gap between Germany and a lot of other EU countries has become narrower in terms of unit labour costs, but most periphery countries still enjoy a competitve advantage in this particular area.

5. The gap becoming narrower hardly supports your borderline retarded claim that “German workers were no longer paid enough to consume the goods they produced”. This is hyperbole, to put it fucking mildly.

4. This also means that the continuing German economic success cannot be explained by low unit labour costs in its entirety. Neither is periphery weakness merely a result of a comparative increase in unit labour costs. It’s more complex than that.

5. Even though unit labour costs in Germany are still the highest in the world, the German economy does extremely well, while ohter EU countries don’t, even if they have lower unit labour costs. Again, this makes it highly improbably that Germany wage contraction is the core problem. It’s a contribting factor, nothing more, nothing less.

6. You still haven’t explainedHow you got from “tightening fiscal policy in Germany increased savings in Germany” to “German workers were no longer paid enough to consume the goods they produced”.

7. Considering the unit labour costs, it stands to reason that Germany’s competitive advantage is not one of lower wages alone. One competitve advantage lies in the types of products the German economy has specialized in. I don’t see how that simple observation is even controversial.

[assignment –ls]

Max

From Mexico is quite diffcult to discuss. He just can’t take an argument without challange even if you 75% agree with his views and challange just 25%. Its my personal opinion based on reading this site for 2 years.

Your statement about Germany is probably correct as the highest value add that Germany has is not labour costs but the type of industries it has focused on and grew a comparative advantage.

German economy to a PIGS economy in terms of say ease of competition/emulation is same as Phd physicist to a shopkeeper. It will take shopkeeper 15-20 years to become PhD physicist, while it will take him only a 1 year to become a barber.

This is the prevailing strenght of German economy which has maybe 2-3 countries globally (US, JPN – springs to mind) who can directly challange German economy based on cost, since ONLY they can provide the same level of service and quality.

Having said that I think Germany does not have the highest labour cost around the world. You need to look a bit North to find those.

@ Max Laue

[ad hominem.–ls]

The German oligarchs (or the “super-rich class of cosmopolitan transnationals” as you called them on another of today’s threads) put the screws to German labor. German workers produce far more than they consume, and the German oligarchs, because of Germany’s current unequal and maldistribution of income, are the beneficiaries of this supurfluous production . The German oligrchs export and sell this superfluous production in the European perifiery countries, as is explained here:

Up until 2008, this huge trade surplus with the European perifiery was financed by the German oligarchs. The result is the curve which can be seen here:

The value for Net foreign assets (current LCU) owned by Germans reached €1.57 trillion as of 2008.

As can be seen from the graph, the value of net foreign assets owned by Germans began shooting skyward into the blue empyrean in 2000. That was also the year that the German oligarchs began putting the screws to German labor and that German labor’s share of German national income and GDP began sinking. It plummeted from 68% in 2000 to 62% in 2008. http://www.diw.de/documents/publikationen/73/diw_01.c.342371.de/diw_wr_2009-28.pdf

The money that German oligarchs screwed German workers out of is the same money it loaned the European perifiery nations.

coobek says:

Max and I agree on nothing. It would not be possible to stake out a position any further from mine than what he does. So please, don’t insult me by saying I agree with Max’s evasions, distractions and distortions.

Here is what Max is attempting to distract attention from:

• For employers, wages—or, more precisely, compensation of employees—represent a cost.

• [R]eal compensation of employees on a per employee basis fell by 9% in Germany in 2000-2008. No other EU-15 member state experienced worse wage declines over this period (see Figure 9).

Look at the population vs. the resources of a country.

Those countries in which the population has ballooned, with a history of famine should be very nervous.

They need some added value business to keep on going… in Germany, it’s the cars. In the UK, the banking…

In India, family farms have been divided so much that most can’t even live on their piece of land anymore.

Energy use will get redistributed but no one will see it… just like no one sees the link between Cyprus and Greece and the energy situation.

Over the last few decades, we have gone from 3.5 billion to 7 billion, forever increasing our consumption of energy per capita. But the gig is up. We need to reduce our energy consumption but we are still deluded thinking we can just print more money, distribute it to the 99% so they can spend it more efficiently than the 1%.

Since we can’t share to save our souls, Mother Nature will twist our arm.

Again, Moneta, I don’t have the slightest clue what you’re going on about here.

If you’re trying to float your neoliberal apologia under the banner of conservationsism or saving the planet, you’re not doing a very good job of it.

Our lifestyles consume too much energy which is mispriced.

Energy is currently in the process of getting repriced.

Our lifestyles must become less energy consuming however, all our efforts to restimulate the economy revolve around solutions that increase our energy dependency.

Since our energy consumption is unsustainable, our efforts guarantee that countries will continue to implode one after the other.

From what I can tell, Mexico, Moneta thinks everyone should have austerity because that will lower energy consumption. Or something.

Im not actually sure that makes sense or not, seeing as how the wealthy use a large part of energy and austerity hasnt done much to hurt them.

Maybe im just misunderstanding him somehow? Im not actually sure.

No. I am against austerity.

I think we should print but in a way that redistributes wealth and reduces our enery and resource consumption per capita.

The thing is that I am a realist… this will happen the day the UK gets off financialization and gets to live within its means.

IMO, we will suffer the effects of the Anglo-Saxon economic model until we have deforesteed the whole planet… just like the UK did to its own island in the 1700-1800s.

But because in the Western world we value materialism, my vision of growth based on services and community is viewed as austerity because it calls for less material goods.

In my perfect world, I have much less stuff but of much better quality.

Massinissa:

For things to get better, we would need to reduce our per capita consumption of energy… but this has never happened historically.

Countries will run themselves to the ground before cutting their energy consumption.

IMO, the Euro was the natural evolution of a population consuming too much energy and looking for a free lunch.

We in the Western world are still clinging to our high energy consuming lifestyles and many more countries will implode over the next decade.

So even if the 1% decided to share, chances are we would just burn the energy to maintain our overindulgent material lifestyles.. which will just accelerate the downfall of many more countries.

Moneta: Your statement missed one period of history:

“For things to get better, we would need to reduce our per capita consumption of energy… but this has never happened historically”.

At one point in English history – (probably between the time they had cut down all the trees and the time that coal production was increased) English royalty declared that all loyal subjects would give up bathing and laundry to save desparately needed energy.

They did so to the extent that much of the aristocray exhibited filthy linen as a sign of their loyalty amd cooperation, and the censer became a part of church ceremonies because the congregation smelled so bad that incense was a necessity of life.

Gerard:

But they were probably already starting to get imports from the Americas… so they might have stopped burning energy on the island but they were burning it somewhere else to feed their consumer needs. Therefore, probably never really reducing their energetic consumption as a country on the whole.

“At one point in English history – (probably between the time they had cut down all the trees and the time that coal production was increased) English royalty declared that all loyal subjects would give up bathing and laundry to save desparately needed energy.”

I call bullsh*t on this story.

If the authors’ hypothesis is correct, then one possibly interesting question is:

Why the market of money to gov’ts eased (lower rates) to the peripheral countries once the euro was introduced if at that time the undergoing reform was far from complete? Why the cheap funding that only led to arrested development instead of solid growth?

If the market had correctly interpreted the data, the rates in Figure 1 shouldn’t have converged so fast, in spite of monetary union. These rates should have stayed put for some time before converging.

The market for funds to gov’ts grossly mis-estimated the effect of monetary union at the precise time it occurred.

One very large and sophisticated market took a wrong turn.

Interesting.

I don’t buy it.

Irish Euro entry started in 1979.

The domestic (agrarian & simple industrial economy) was crushed beginning in 1980.

Spain stopped its Nuclear programme in 1986 at Euro entry……

The objective from the start was to turn these economies into Imperial markets for the cores goods.

Now that the European entrepot economy imploded in 2007/8 , the new objective of the core was to make a smaller core entrepot economy with Spain , Ireland ,Greece etc as their new current account surplus hinterland.

Italy of the late 1990s was the model for these corporate operations.

Yves,

is there an e-mail address by which I might e-mail you something?

thanks,

nonclassical

The post 1987 boom in Ireland was not sustainable….

How absurd.

It was dependent on huge external capital flows from the very start.

In 1980 the older rust belt industries died in Cork Harbour.

Apple computers came to town that year.

The fiscal austerity post 1980 was used to crush domestic demand & thus domestic industry.

http://www.youtube.com/watch?v=8o28aWtm-3M

This could then free up oil to be burned by free banks creating “assets” such as cars (post 1987) as wages as a % of GDP began to dive after 1980.

The European experiment is a expression of pure evil.

Its a madhouse filled with health % safety police wishing to tell us how we live our lives.

Anti-austerity is best for the people however…

A large percentage of the anti-austerity crowd just wants government to print money for the sake of printing money, thinking that if you give the 99% some money, they will know best how to use it. I am part of 99% and want some money but I do not believe we will save ourselves. We need a change in paradigm before this ever happens.

Every time we try to stimulate, we start with huge energy intensive infra projects… which will probably keep us car dependant and guarantee many country’s future demise.

Our monetary system is mostly based on collateral. You need hard assets to get a loan. And government has fallen prey to that ideology. Over the last couple of decades, our governments have been forced to turn into make believe profit centres… and then we wonder why they are so screwed up.

All countries keep on increasing their energy requirements to sustain their growth. Look at what we have done to our planet over the last 4 decades as we went from 3.5 billion to 7. Imagine what we will do to it over the next few as we keep on increasing our consumption of energy and we go from 7 to 9 billion.

Countries with huge entropy, limited resources, energy and lack of added value production should be very careful. That includes most countries.

On collateral.exactly.

Instead it should be based on us. It is we who are the wealth.

I support your view of energy dependence and it being misspriced. In fact the only good thing I see in crazy use of financialization and shadow banking is the effet it has on the price of energy. Price signals do create action, same as no price signals create inaction (as the above article shows for PIGS countries and the low capital cost from 2001).

I would like to thing that with such a unemployment state would use this opoortunity to employ for free (print) the idle resources (us) to produce things like basic research. Sine it is basic research for public money that gave us the best inventions of 20th century. Internet included.

I agree. Ironically, here in Canada, government has been cutting research and putting an increasing focus on resources and energy production.

@Moneta

You have not studied European countries energy systems closely.

The French and Germans created local scarcity in their home markets from the late 70s / early 80s…..

But their corporations needed to show profits.

Ireland , Spain etc became these strange fois gras economies.

Any major domestic effort (that could work) to increase local energy intensity such as peat stations in Ireland or Nuclear in Spain was shunned.

This fleeting surplus of capital was used to buy yet more cars which depreciate after 10 -or 15 years.

They just filled us with oil & gas which the UK , France and Germany did not now burn.

In a nutshell from 1980 on they prevented the Irish from drinking (domestic demand) so that we could buy more external cars………..this they called growth.

The above is the result – junk land

If the Irish kept drinking more land (the best land in the country) would not now be destroyed.

And its not just the Irish – French domestic wine consumption has tanked ,once upon a time they drank 2 or 3 bottles a day on average.

A general characteristic of the euro system has been a collapse of domestic demand via the destruction of manual labour as those are the guys who drink to subsidize the machines.

Now the machines have destroyed our culture , our way of life and for what ?

Nothing but junk.

Without oil, our global population would be MUCH smaller.

Most of us would not be here to complain.

Irish urban Junkland blight.

It started after 1957 & especially the 1970s but after 1990 it really took off

Y1990 : 1.5% of land cover.

Y2000 : 1.9% of land cover.

Y2006 : 2.3% of land cover.

I imagine few Bogs were built on…… by and large it was the better land.

What a waste.

4.4.3. Increase in Artificial Surfaces

There was almost a 15% increase in artificial surfaces between 2000 and 2006. Most of this increase is explained by the increases in the following (Table 18):

Infrastructure (roads and railways); increase of 23.5 km² or +126.43%

Industrial and Commercial; increase of 17.5 km² or + 21.91%

Mineral extraction sites (quarries and dumps); increase of 12.52 km² or +16.5%

Discontinuous urban (sub-urban housing); increase of 140.45 km² or +14.95%

http://www.epa.ie/…Final%20Report.pdf

The above discontinuous urban (140.5 km²) did the most damage to good agricultural land and also subtracted from the tourist potential of many areas as few people with wealth & taste will spend money in a sub-rural sub standard landscape.

If we could only turn the clock back………

http://www.youtube.com/watch?v=9TakfNbFuNA

This is an interesting piece, however, David McWilliams (“that red-headed eejit on the telly”) was making these same arguments as early as 2005 in his bestseller, The Pope’s Children. These same arguments were reiterated, post-crisis, in books like Follow the Money(2009) and The Good Room (2012). Still, I guess it’s good to see “real” economists copping on.

An interesting article.

One can read it as supporting the pov that cheap – easy money fueled and augmented corruption and encouraged the flowering of profiteering, quasi-criminal elements, in complicated private-corporate-Gvmt networks. Which certainly took place, to some degree. And, of course, continues.

E.g. This paper about Ireland by TASC, *Mapping the Golden Circle.* PDF, 75 pages. 2010.

http://www.tascnet.ie/upload/file/MtGC%20ISSU.pdf

One short paper can’t attack multiple angles. To quote only two others one might consider important:

1) Periphery EU countries quoted have high energy bills, higher than the core in per capita terms. The reasons are obscure, and vary from country to country…

See here e.g. (chart which lists imports of FF)

http://www.theoildrum.com/files/percent-of-energy-consumption-from-imported-oil-and-gas.png

from: http://www.theoildrum.com/node/8998

Yes, that is all extremely complex and few afaik are working it out. See some posts above, like by Dork of Cork.

2) The relationship between national ‘culture’, production, and easy money. Greece, for ex. was, and is, solidly built on family biz – that is so in all the spheres from the local grocer to the top Pol / Boss of Corp (excepting perhaps the Church?). Yes, that is a generalization, and relative, but in a short post one can’t say more. GR is the country in the EU that afforded the least oppos in terms of jobs (NOT education) to its young ppl. You join your tribe, work for Pa or the Uncle, Ma, or in a spot in that biz, entity, thru relations. So, decisions are taken in tiny circles. In contrast to Germany. So there is a clash of values, in the sense of creating differing reactions to new financial landscapes, and the imposition of a model that doesn’t suit everyone. So the periphery got screwed.

First!

The periphery got suckered into joining an energy intensive economic way of doing business which was mid to long-term unsustainable for them.

I would venture to say that estimates of US energy consumption are way too low… they never include all the oil that is burned in other countries to produce the imports and the shipping to get them there.

Great read.

For me, it really boils down to the observation that the big banks are a blend of recklessness, carelessness, and criminality. Everything that is happening is just them trying to get the citizenry to bail them out. Individual nations still have some sovereignty; Iceland has chosen to jump ship from the craziness of socializing losses, the other smaller nations have stuck around thus far.

What will be really interesting to see unfold is whether the US, UK, French, and German bankers manage to keep most of the other nations in line or not.

Or if one of the big 4 themselves has a domestic break in policy – such as the US shifting from bailouts to reform…(yeah, HA, I know – but it’s interesting to contemplate).

Well, if we are going to talk about criminality at banks, I will drop in the views of an old friend of mine I met a few days back after not seeing him for a few years. He is still in banking (I left the markets fifteen years ago before things got really bad). He ranked the banks in order of corruption:

1. Cypriots (he worked for a Cypriot bank for several years)

2. Chinese

3. Israelis (he added that there are a lot of honest Israeli bankers but the corrupt ones are really corrupt.

4. Americans

5. British

6. Japanese

Just one man’s opinion but I throw it in for what it is worth

That’s an interesting list – essentially China and the US, plus Cyprus. I definitely defer to others about trying to weigh relative corruption.

And I wish the people of Cyprus good luck as they figure out what to do about being #1 :)

Assets were leveraged through debt in the service of creating large economic rental streams – economic rent directly increases the cost of living and producing wealth – money is not wealth – the bust of the boom deflated asset prices (mainly property for human habitation and industry) but, the debt owed on the previously high asset prices did not come down. Governments and in the USA have been trying to keep prices inflated – this leads to the cost of real production to continue to be above what is needed to compete in the real economy – Financial capital is treated as more important than industrial capital. Financial capital gets the tax breaks and the financial predators use this to draw cash in.

To create wealth you need capital (tools, imagination, resources) Labor and property (rent lease, own). Raising the cost through a bubble in property prices will raise the cost of a widget produced or sold from a place (manufacturing housing) – Spending money to provide a roof over ones head or borrowing to purchase a facility….cost of a place being inflated leaves less money to purchase other things with. Since the volume of debt has not come down nearly as fast as the actual price of property and, wages have stagnated or fallen – then demand will be down due to servicing inflated asset prices. Since financial capital has become dislocated from industrial/business capital – it will chase returns elsewhere and is not stuck (like property) to location. The debt overhang…through the magic of compound interest inhabited its own place outside of the real economy.

Debt that can not be paid back…will not be paid.

Until pure gambling in the financial sector ceases or is reduced (taxed out from the predatory and into the real economy) things will not get better.

For years now I’ve been seeing article and columns stating that this country or that needs to “undertake structural reforms.” Everybody seems to know what that means. I don’t. I’ve seen “reform the labor market,” which seems to mean “make it easier to fire people and leave them to starve.” I’ve seen arguments to reduce regulation, which seems to make sense in light of the collapse of the factory in Bangladesh. Supposedly some licensing restrictions are supposed to be too strict, such as requiring a college degree to give manicures, or taking two months and hundreds of Euros to open a new business. But in general the term “structural reform” just seems to be a dog whistle for cutting the social safety net. Am I understanding correctly? Are there sources anyone can point be to which makes things clearer?

This paper is saying that too much cheap money flooded the PIGS. Instead of finding a useful, profitable enterprising set of investments, the money inflated the residential and commercial real estate markets. Germany, had cheap money all along, and also had institutional governing processes in place that would focus the cheap money into productive, profitable, use.

The Celtic Tiger narrative used to be high tech jobs for educated English speaking and free university trained Irish propelled the residential boom, due to higher wages and increased consumer demand for housing and shopping.

Spain was in the middle of building a national high speed rail system connecting the nation the same way in which the Interstate Highway system connected America post WWII. They also were the global wind power and solar electric panel leaders. So, it seemed that the capital was being absorbed in useful, productive ways. The narrative there was you could live in Barcelona and work in Madrid. Even Bilbao in the middle of no-where was closer to jobs due to the high speed trains.

Greece got the Olympics and Athens received infrastructure build out to make it a modern European capital with a modern airport etc. But not much more. It was a tourist haven, not an Aegean Tiger. So, capital there was absorbed by over construction and inflated assets in real estate.

Portugal is a basket case, with a poorly educated population, the Louisiana of Europe? Construction absorbed the cheap money there and little else productive was built. Sunny tourism and killer pastries.

So, these 4 countries are flooded with cheap money and the only thing they could figure out to do with all of that money was construction and inflation of real estate. That is where the surplus capital was absorbed because they did not have what Germany had.

If I recall the history of banking as explained on this site, German industrial banking operated upon completely different principles than Anglo-American banking. In this country, no one is getting a loan without collateral in the form of real estate. The capital markets are for extremely well heeled blue chip companies. All else were considered junk bond status borrowers. Or in household kitchen table terms, sub prime. But the Germans were different in their approach to finance. So, culturally, they would not have a real estate asset bubble because that was not how they preferred to do business to begin with. It was a lot more than cheap money.

Furthermore, the Germans did have that little thing, oh yea, unification. Berlin became not only the new capital but also the biggest construction site in the world for over a decade. That absorbed a lot of capital in the way Haussmann rebuilt Paris and remade it in the form of a modern business center, and not a narrow Mideval cobble stone sprawling mess.

http://www.foothill.fhda.edu/divisions/unification/econ.html

Here is a little background on the hundreds of billions poured into East Germany becoming a part of just Germany. A Dow chemical plant was reconstructed at the cost of $3.2Mil per job. That sounds like an inflated asset to me. I wonder what the cost per sq ft was? Nice contract. I am not sure if the Euro and the Germans institutional reforms and governing processes is the causal connection. The cheap money went into Berlin, East Germany and not the residential housing market. It was an anomalous situation, an adaptive response that helped them dodge a bullet maybe, but not a superior design in policy that kept them disciplined in the storied Prussian manner.