Yves here. VoxEU has come to serve as a wonky alternative to the Financial Times comments section, which is Brit-speak for op-eds. While most FT comments are at least interesting and timely, now and again the pink paper serves as a venue where real policy players put a stake in the ground, sometimes in exclusive interviews but also in opinion pieces.

This article by David Miles of the Bank of England is clearly intended to reach a wider audience than the normal VoxEU piece. In it, he calmly and methodically tries to tell finance people that what they want from central bank forward guidance is tantamount to having their cake and eating it. Admittedly, the unreasonable expectations for what forward guidance can accomplish is partly central bankers’ own creation. In keeping, this piece suggests that a retreat from efforts at precision in forward guidance would probably be a plus.

By David Miles, Monetary Policy Committee Member, Bank of England. Originally published at VoxEU

Many central banks embrace forward guidance by announcing expected interest rate paths. But how likely it is that actual rates will be close to expected ones? This column argues that quantifying such uncertainty poses great difficulties. Precise probability statements in a world of uncertainty (not just risk) can be misleading. It might be better to rely on qualitative guidance such as: “Interest rate rises will probably be gradual and likely to be to a level below the old normal”.

“Mensch tracht, und Gott lacht” is a Yiddish proverb – men plan and God laughs. Woody Allen puts the same thought this way: “If you want to make God laugh tell him about your plans”. Some people might see these words as a fitting epitaph for forward guidance on monetary policy. The Bank of England has certainly faced a good deal of criticism for the guidance that it has recently been giving, as has the Federal Reserve in the US. In both cases the nature of the guidance has evolved, though I think it is rather harsh to assume that God has been laughing at how things have gone; anyway it is hard to know. Yet there is a real question here that is worth thinking about: What is the most useful way for a central bank to provide information about the way in which it will set monetary policy?

Consider a spectrum of choices a central bank might face about what it says about its future policies. At the minimalist end of the spectrum (which we might associate with Montagu Norman)1 is just a statement that the central bank will continue to do what it sees as most appropriate over time. At the other end of the spectrum is an explicit commitment that policy will be set in a specific way at each point in the future – not just a rule that might be followed but a commitment to a particular policy setting. Between these two are a great many intermediate points. Nearer the vague end is a statement of the goal of policy (e.g. an inflation target) but little beyond that. Further along again might be an assessment of how the policy set by the central bank might evolve for different outcomes of some of the main forces driving the economy. That would tell you something about the central bank’s reaction function. Or the central bank could give an explicit forecast of what it thinks its most likely future policy will be.

I think it is helpful to think about forward guidance as being a choice about which point to settle on along the spectrum I have described.

There is not a lot of generally agreed-upon and directly applicable economic theory to help with this. To a large extent this is because in many standard economic models this is a bit of a non-question. If everyone in an economy is completely rational, has unlimited computational powers, has the same information, and understands the processes driving the economic outcomes, then so long as the central bank tells people what its goals are then there is not much more to be said. People outside the central bank will work out what the optimal policy will be for the central bank to follow given how the economy seems to be evolving. Everyone will form the same expectations about the course of future policy.

There are a few wrinkles to this. Under some circumstances optimal policy might be time inconsistent – that is a situation when the central bank plan which is optimal today is no longer optimal at some point in the future simply because of the (entirely predictable) passage of time and not because of some news. But time inconsistency is a slightly tangential issue.2

The main point is that when everyone shares common information and understanding (and that is the default assumption in many economic models) the central bank just needs to say what its aims are. Of course this is very unrealistic. So it is not a very good guide to the practical policy issue about what guidance the central bank should give.

Give Us More Certainty

Much of the most vocal recent criticism of guidance given by central banks really reflects a seeming preference to take one of the extreme ends of my spectrum. The Bank of England is very often criticised for ‘flip-flopping’ – for giving different signals about policy at different times, for seeming to change its mind on the right path for policy – in short, for not providing certainty about policy. I think in many cases this boils down to the criticism that while the Bank of England now claims to be giving guidance on policy, it is not saying what policy will be – it is not giving a specific path for interest rates, and not even saying when it is going to start raising rates.

And it is true that the Monetary Policy Committee (MPC) could commit to a certain path for future interest rates, and stick to it whatever economic circumstances materialise. Indeed the more uncertain the economic environment, the more valuable might people find it to have certainty about where interest rates are heading. Yet the greater the uncertainty, the greater are the chances that the economic environment will turn out to be very different from what the MPC expected at the time they committed to an interest rate path. And this means that sticking to that path can be very costly.

To explore this issue of the effects of committing to a specific path for interest rates, I have used a simple model of the economy which accounts for several types of uncertainty and their effects on monetary policy. (For details see Miles 2014.)

My aim is to assess how much of a difference it would make if the central bank fixed the path for policy over the next few years rather than making it conditional upon the way the economy actually pans out. I calibrate the uncertainty about the size of the output gap, the impact of monetary policy, the growth momentum in the economy, and the path of productivity. I also specify the aim of the central bank as being to try to keep inflation close to a target and output close to its estimate of the supply capacity of the economy. I then compute an optimal policy rule showing how the interest rate should respond to the (uncertain) evolution of actual inflation and output so as to best achieve the aims of policy.

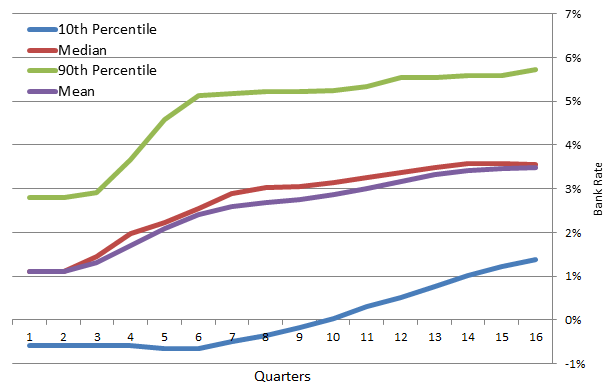

Figure 1 shows the resulting probability distributions for the path of Bank Rate. Along the central path (that is the median where 50% of the outcomes are with lower interest rates and 50% have higher rates) the level of Bank Rate rises gradually. But it remains materially below its pre-Crisis average of around 5% even after four years. Figure 1 also shows that things may turn out quite differently from the central path. This simple model suggests that there is a 10% chance that the appropriate level of Bank Rate increases to above 5% within 18 months (the line labelled ‘90th percentile’). It also shows that there is a 10% chance that the appropriate level of Bank Rate is around zero for two years to come and is only just over 1% even four years ahead (the line labelled ‘10th percentile’).

Figure 1. Optimal Bank Rate, simulation

How does a policy of fixing the interest rate for a three- or four-year horizon look in the light of this model? Not very attractive I should say. Suppose that interest rates are set at the outset so that they follow the central (median) path. On average this is an appropriate policy – but in the light of how things actually evolve it could be very different from the interest rate that would be appropriate based on what actually happens to inflation and output. How wrong could it be? Well, four years ahead the interest rate to which the central bank commits at the outset if it fixes policy at what is (ex ante) the average outcome could, with about 10% probability, be at least 2.5 percentage points too low, and with 10% probability it could be at least 2 percentage points too high. Having interest rates that far from the right level, and for an extended period, seems to me a very high price to pay for the certainty of following a given path for interest rates. It would probably generate outcomes that were wildly unstable.

Suppose instead that the central bank accepts that it must respond to events as they unfold. Suppose in fact that the central bank calculates what the appropriate response is given the uncertainties and sees that the fan chart for interest rates is as in Figure 1. How might it then give guidance on policy? A natural response might be to say it should just publish Figure 1. I want to consider some practical issues with that in a moment. But setting those to one side for now, how might you describe in everyday language the message that Figure 1 conveys? (And using everyday language is absolutely central to effective communication. The amount of training and time needed to really understand what Figure 1 means is surprisingly large). One might try the following as guidance:

“Interest rates are likely to rise gradually from their current exceptionally low point, but probably to a level that is meaningfully short of the level of around 5% that used to be thought normal. But the exact path that interest rates should follow cannot be known for certain since how the economy will evolve is not known in advance.”

I don’t think that is a bad summary – in everyday language – of what Figure 1 shows. It is also pretty much the message on policy that the MPC at the Bank of England have been giving for some months.

Whether or not something more precise and quantified than this broad description is useful is the issue I want to turn to next.

Are Precise Probability Statements Good Guidance?

One type of guidance is for the central bank to provide an expected path for the policy rate (for example the median path shown in Figure 1 above). But without giving some idea about how likely it is that policy will be close to this path, this may not be particularly useful – and it could be seen as more of a commitment than an expectation. Quantifying that uncertainty is tricky. One might just draw on the volatility of past interest rates (around some previously expected path) as a guide to uncertainty in the future. Or a stochastic simulation using a monetary policy rule could be used to derive fan charts for the policy rate. The policy rule could be (an approximation) to an optimal rule – which is one way to interpret Figure 1 above.

So the MPC could use a mechanical procedure that is some sort of very rough approximation to its decision-making so as to produce a fan chart for interest rates. But there is no getting around the fact that constructing fan charts of interest rates that represent the MPC’s view of the probability of different paths presents many problems. It involves, for example, the quantification of the chances of various events happening which may go beyond what can meaningfully be done. The apparent precision of probability statements in a world of uncertainty (not just risk) can be misleading.

Currently, it might be just as useful – and probably less misleading and possibly even more accurate – to give forms of guidance which are more qualitative, such as: “Interest rate rises will probably be gradual and likely to be to a level below the old normal”.

That says something substantive; and most people can understand it.

Disclaimer: This is the view of David Miles and not that of the Monetary Policy Committee at the Bank of England of which he is a member.

Footnotes

1 In recognition of his reputed dictum “never apologise, never explain”.

2 Woodford (2013) has an extensive discussion of the conditions under which the optimal monetary policy of a central bank might be time inconsistent. This depends upon the nature of the goals of the central bank, which need to be precise enough to determine a policy path. The key condition is that “…the sequence of target criteria for different horizons are of the same form (i.e., if the target criterion is independent of the horizon)… then the forecast-targeting procedure will be inter-temporally consistent.” I believe that the way the MPC at the Bank of England interprets its goals satisfies this condition.

See original post for references

the entire forward guidance things as clearly just another BS program to allow banks/ finance to make excess profits. It was based on assumptions never tested or proven. The wonder is how people buy into it at all. I Can’t begin to say how many times I questioned the rationale in the ft while they were pushing it. The idea that people make purchasing decisions based upon what central bankers say was just silly. When you start to realize the majority doesn’t even know what QE is. Yet these people are going to decide to purschase on credit based upon their knowledge of forward guidance. it was all about allowing the bankster class to sell at the top before interest rat3e rises. The implication is that it should then increase speculation and instability. The instability then used to justify more asset price support beyond fundamentals, and more money flowing directly into the pockets of the rich/ wealthy. I just can’t believe the masses fall for this crap. They say they have learned from insky, then effectively do exactly what he is saying causes instability

I think Mr. Miles is too modest about the effects of central bank policy. One of the few rules of thumb that almost always apply in financial markets is the relationship of interest rates to stock and bond prices. By manipulating that number, the CB creates an outcome rather than simply discovers it. With QE operating another rule of thumb, that of supply and demand, the effect is more certainty rather than more surprises.

Whether plans for future actions create informational asymmetry for insiders to profit from isn’t provable with publicly available information. It’s a pretty safe bet, but it couldn’t be proved in a court of law. It’s like a conspiracy theory or the theory of gravity; we see the effects but no one has the information for a definitive answer of causation. Operating in the real world, there’s more success in operating on the conspiracy theory.

By observation, the CBs have followed a policy that’s enriched the rich, mostly in the financial industry, and impoverished the rest of us, here in the real economy. Mr. Miles might be agnostic about why that all worked out, and continues to work out, but the rest of us know there’s cowboys and cattle, and we haven’t got a hat.

Oddly, the “uncertainty” (i.e. distance from median to 10/90) is not really very different at quarter 16 from where it is at quarter 1. On day 1 it looks like you could be mis-set by up to almost 2 points, too. It looks like it goes from about 1.8 points to about 2.2 points over four years.

So from that perspective, the “cost” of publishing a 4-year curve is more like 0.4 points.

Put another way, by this figure banks aren’t even very good at getting it right today.

“Interest rates are likely to rise gradually from their current exceptionally low point, but probably to a level that is meaningfully short of the level of around 5% that used to be thought normal. But the exact path that interest rates should follow cannot be known for certain since how the economy will evolve is not known in advance.”

I would take some comfort if the above statement were ever pronounced if the amount of shadow banking were taken into account and if I knew that the banks would not become insolvent when the interest rate does rise and if the bankers were not also “investment” mechanisms which work against the welfare of anyone not in finance. It is alchemy–all alchemy!

This one never got much traction at all, did it? Fair to say NC readers may not be big supporters of either central banks or their forward guidance? Count me in.

Speaking of human plans, this, the last paragraph from The Archdruid’s latest missive:

In the real world, in the course of ordinary history, these things happen. So does the decline and fall of civilizations that deplete their resource bases and wreck the ecological cycles that support them. As I noted above, I’m aware that true believers in progress insist that this can’t happen to us, but a growing number of people have noticed that the Progress Fairy got her pink slip some time ago, and ordinary history has taken her place as the arbiter of human affairs. That being the case, getting used to what ordinary history brings may be a highly useful habit to cultivate just now.

Indeed!