By Lambert Strether of Corrente.

This year’s ObamaCare open (mandated) erollment period begins on November 1, 2015 and ends January 31, 2016[1]. Plans and prices will be available “by late October.” Skipping over the repellently self-congratulatory material on how the totally-not-a-laughingstock-by-civilized-standards ObamaCare has managed to deliver a non-universal[2] national health insurance program, everybody admits that this enrollment period is going to be a tough one[3]:

HHS Secretary Says Coming Sign-up Season Will Be Toughest Yet Under Health Law

[Official] are eyeing about 10.5 million people who could buy coverage through HealthCare.gov or state sites, often with federal subsidies to offset premiums, but who have resisted signing up as the law rolled out.

“Those who are still uninsured are going to be a bigger challenge,” said Health and Human Services Secretary Sylvia Mathews Burwell in a speech at the Howard University College of Medicine, after praising the law for pushing the rate of Americans without coverage to historic lows.

“Overall, this open enrollment is going to be tougher than last year,” she said. “But while our goals may be harder to reach, we’re working smarter to reach them,” she said. “We know Americans are depending on us and we’re doing everything we can to help them find the coverage they need.”

Let’s skip over the question of why “doing everything we can to help,” for this Democratic administration, and for the currently leading Democratic candidate, never includes even a smidgeon of consideration for the simple, rugged, and proven single payer solution. And for now, let’s skip over the question of why Burwell thinks Americans are “depending” on HHS but at the same time “resist” enrolling. When Burwell says “working smarter,” what does she mean, and what are her goals? Kaiser Health News:

Burwell said the agency’s goals for the upcoming enrollment season, which ends Jan. 31, 2016, are to “improve the consumer experience, retain our current customers and increase our enrollment.” By the end of this year, HHS expects 9.1 million individuals will have coverage through the federal and state health insurance exchanges, or marketplaces, she said. HHS officials have yet to announce an enrollment goal for 2016.

OK, Burwell hasn’t actually set any goals. To be fair, that actually could be “working smarter,” given the givens. Moving on:

To reach the approximately 10.5 million uninsured, agency officials plan to use data accumulated over the last two health law enrollment campaigns, such as information about where the uninsured live and what sorts of messages might convince them to purchase coverage, senior HHS officials said Tuesday. Email and social media campaigns that encourage people who have started their applications to finish them, or to promote awareness about the law’s financial assistance that is available to help people purchase coverage and pay out-of-pocket costs, will be key. While there’s ‘no silver bullet’ to increasing enrollment, ‘we have to keep chipping away at it,’ a senior agency official said.

Again, let’s skip over the fact that there is a “silver bullet”: Junk the Rube Goldberg device that is ObamaCare, and adopt a single payer system instead. And let’s skip over the bathetic collapse from “we were able to deliver on universal health care” (Obama, November 6, 2013) to this year’s “we have to keep chipping away at it” (with lethal effects for those “depending on us”). Where is the chipping away to be done?

Outreach and enrollment efforts will be focused on five targeted areas — Dallas, Houston, Northern New Jersey, Chicago and Miami — where there are large numbers of uninsured who qualify for the law’s financial assistance.

And again, let’s skip over the fact that consumers’s citizens’ access to life-saving health care under ObamaCare is random with respect to jurisdiction (as we showed here, here, here, here, here, and here, in “Obama’s Relentless Creation of Second Class Citizens”). I mean, if you don’t live in one of those five urban areas, you’re out of luck, right? But so what, because markets [4]. Rather, let’s ask the question:

Why would people “resist” signing up for ObamaCare?

The punditry really can’t explain. For example, FiveThirtyEight does the math. There are 33 million uninsured, of whom 7 million are non-citizen immigrants, 3.8 million are in states that did not expand Medicaid, 7.7 are between 19 and 14 (that is, on their parents policies or so-called “young invincibles“), leaving about 14 million.

It’s hard to say why these 14 million people weren’t insured, but the administration will have to figure that out if it wants to come close to the universal coverage the law intended [snort].

Six years after ObamaCare was passed, and it’s “hard to say” why everybody wouldn’t already have leaped to sign up for it. Alrighty then. Bloomberg is just as vague:

[T]he uninsured rate needs to be pushed even lower. The people who’ve signed up for Medicaid or exchange coverage are those who have most wanted insurance; the challenge remains to persuade those who are less motivated or don’t understand their options.

Or, perhaps, are highly “motivated,” and “understand their options” all too well? Burwell:

Almost 40 percent of the uninsured who qualify for marketplace coverage earn between 139 and 250 percent of the poverty level, about $30,000 to $60,000 a year for a family of four, Burwell said. Nearly 60 percent of the uninsured are either confused about how the tax credits work or don’t know that they are available, and about half of the uninsured have less than $100 in savings, Burwell said.

Or, perhaps, are not “confused” at all?

Could it be that ObamaCare just isn’t that good a deal? Could that be why people resist enrolling? Interestingly, that’s what HHS’s internal studies are telling them, even if word hasn’t percolated out to the pundits just yet. From a June 2015 study outsourced to the Robert Wood Johnson Foundation:

Cost remains the main barrier to insurance. Those who have looked made a calculated decision based on more than just the premium. They also consider out-of-pocket expenses, deductibles, co-pays and other factors in their decision.

Imagine that! Working people making “calculated decisions”! Who would have thought? RWJF goes on to mention factors that might change those calcuations:

Even after two enrollment periods, many uninsured individuals lack knowledge about tax credits, special enrollment periods and the fine. Providing ongoing and straightforward information on these issues could move more uninsured towards enrolling in insurance. Also, the survey found that most uninsured would like to talk with someone when signing up for insurance.

Let’s skip over the fact that six years into the program, nobody’s been able to figure out how to provide “straightforward information” about how ObamaCare works, and let’s skip over the question of whether Rube Goldberg devices are ever hard to explain.

Rather, let’s ask ourselves: Even taking the tax credits, the special enrollment periods, and the fines into account, is ObamaCare a good deal? A new study from the NBER suggests no. From Mark Pauly, Adam Leive, Scott Harrington, NBER working paper number 21565[5], quoting the abstract in full:

This paper estimates the change in net (of subsidy) financial burden (“the price of responsibility”) and in welfare that would be experienced by a large nationally representative sample of the “non-poor” uninsured if they were to purchase Silver or Bronze plans on the ACA exchanges. The sample is the set of full-year uninsured persons represented in the Current Population Survey for the pre-ACA period with incomes above 138 percent of the federal poverty level. The estimated change in financial burden compares out-of-pocket payments by income stratum in the pre-ACA period with the sum of premiums (net of subsidy) and expected cost sharing (net of subsidy) for benchmark Silver and Bronze plans, under various assumptions about the extent of increased spending associated with obtaining coverage. In addition to changes in the financial burden, our welfare estimates incorporate the value of additional care consumed and the change in risk premiums for changes in exposure to out-of-pocket payments associated with coverage, under various assumptions about risk aversion. We find that the average financial burden will increase for all income levels once insured. Subsidy-eligible persons with incomes below 250 percent of the poverty threshold likely experience welfare improvements that offset the higher financial burden, depending on assumptions about risk aversion and the value of additional consumption of medical care. However, even under the most optimistic assumptions, close to half of the formerly uninsured (especially those with higher incomes) experience both higher financial burden and lower estimated welfare; indicating a positive “price of responsibility” for complying with the individual mandate. The percentage of the sample with estimated welfare increases is close to matching observed take-up rates by the previously uninsured in the exchanges.

Let me just emphasize the key sentence once again:

[E]ven under the most optimistic assumptions, close to half of the formerly uninsured (especially those with higher incomes) experience both higher financial burden and lower estimated welfare

So, ObamaCare’s not a crapshoot after all; it’s a coin toss! That means that the uninsured are entirely rational to resist it. They did the math! And in the marketplace, we’re all rational actors, right? The Street summarizes the report as follows:

The group of people whom the authors highlight are the non-poor, or those ineligible for Medicaid but who maybe eligible for various subsidies for premiums or cost-sharing, depending on their income level. It turns out that the more someone earns the worse off they’ll be.

“At higher income levels, small or zero subsidies and currently modest penalties will not be enough to affect the large welfare losses that the middle class uninsured experience were they to buy coverage,” the report says. Those in good health were “consistently worse off from purchasing coverage regardless of the assumptions made,” according to estimates calculated by the researchers.

“Most uninsured will lose and, according to our estimates, will prefer to remain uninsured at the current penalty levels for violating the individual mandate,” the report continues.

Conclusion

ObamaCare has always had a contradiction at its heart: It’s a marketplace that people are forced to enter (and I’ve always felt that this should have been the principled[6] conservative objection to it. And now it turns out, that for some large proportion of the uninsured, the only way to get them to buy a product they view as defective — because otherwise they would already have purchased it — is to ratchet up the fines until they see reason. The beatings will continue until morale improves.

NOTES

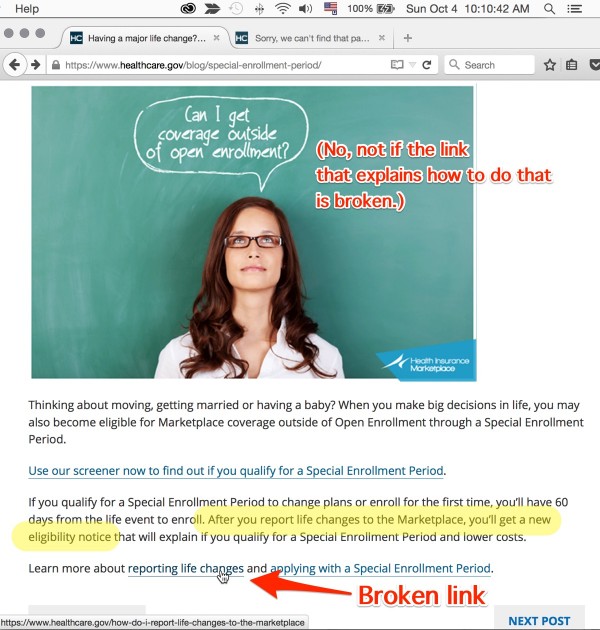

[1] If you can’t, won’t, or don’t make the January date, you may be able to qualify for a “Special Enrollment Period” by reporting “major life change” to the marketplace. I would explain how, but sadly — by which I mean hilariously, because who would have expected such a thing from Obama’s HHS? — the link to “learn more” is broken (as of Sunday, October 4 at 10:10AM EST):

To be fair, we can remind ourselves of the programming pearl: “the cheapest, fastest, and most reliable components are those that aren’t there.” In a single payer “everybody in, nobody out” system, this nonsensical eligibility test would never exist in the first place, and so there would be no link that the farcially bad quality assurance program of whatever HHS vendor built this page could fail to check. (I’m also showing the whole page to contrast the nauseatingly patronizing and over-familiar marketroid prose with the broken delivery of critical information.) Secretary B-u-u-u-r-r-r-well! Could you fix this, please?

[2] Here are the latest enrollment figures from HHS:

In March 2015, ASPE estimated that 16.4 million uninsured people had gained health insurance coverage as several of the Affordable Care Act’s coverage provisions took effect. Using updated data, ASPE now estimates that 17.6 million uninsured people have gained health insurance coverage. Coverage gains refer to different sources of coverage, including Medicaid, the Health Insurance Marketplace, and individual market coverage; therefore, gains are not limited to Marketplace-eligible individuals.

Notice how, with “different sources of coverage,” HHS is managing to take credit for all gains in health insurance coverage, including however many people purchased individual coverage in the post-2009 recovery, such as it was. Notice further HHS’s methodology:

[W]e use the most recent data available on health insurance coverage from the Gallup-Healthways Well-Being Index Survey, which are collected daily and become available soon after data collection. The data in this brief reflect interviews through September 12, 2015. Analyses to date suggest the Gallup-Healthways Well-Being Index survey’s national uninsured estimates track the NHIS national estimates quite closely (see http://aspe.hhs.gov/health/reports/2014/InsuranceEstimates/ib_InsuranceEstimates.pdf). (There is a review of a number of nonfederal surveys from the Urban Institute at: http://www.urban.org/UploadedPDF/2000146-Nonfederal-Surveys-Fill-a-Gap-in-Data-on-ACA.pdf).

We determined the change in uninsured rates for the nation, states with and without the Medicaid expansion, and persons with different demographic characteristics. We computed these uninsured rates by updating the methodology used in the ASPE issue brief “Health Insurance Coverage and the Affordable Care Act”, published in March 2015, which adjusted for demographic and economic covariates: age, race, household income, ethnic group, sex, employment status, and state of residence. The current methodology also adjusts for marital status and rural residence. These covarietes are aimed to control for changes in the economy, population composition, and non-policy factors affecting health insurance coverage.

In other words, HHS has outsourced the enrollment figures to Gallup. One thing I don’t understand: Why can’t HHS use its own hard numbers for enrollment through the marketplace? Can it possibly be that the ObamaCare backend is so flaky that it can’t deliver this data? Or that HHS specified the system such that the total number of enrollees can’t be queried? Or is HHS so captured by the ideology of the market state that the most basic of functions — in this case, what one would think would be a count of records in their database — can’t be provisioned without paying some third party a fee?

[3] Assuming Matthews isn’t lowballing the numbers to make a mediocre effort appear superior at some later date, of course.

[4] Have HHS officials been so deeply captured by neoliberal ideology that they literally cannot conceive of universal coverage for all citizens as an achievable objective?

[5] I’m deliberately not quoting the title of the paper, which is: “The Price of Responsibility: The Impact of Health Reform on Non-Poor Uninsureds.” ObamaCare’s architecture is one of putatively shared responsibility between “the federal government, state governments, insurers, employers, and individuals.” However, since the insurers are parasitical and should not exist, there’s no reason to share responsibility with them, so I don’t accept the language.

[6] I know, I know.

[7] Of course, insurance companies can violate the law and not get fined, because they have impunity and you don’t.

“Most uninsured will lose and, according to our estimates, will prefer to remain uninsured at the current penalty levels for violating the individual mandate.”

Aint dat da troof. If Obamacare were really such a great deal, it would be like selling $30 cases of beer for $10: they’d have to beat back the unruly mob of applicants with a stick.

So of course, with its ‘punishments instead of incentives’ mindset, government resorts to fining those who don’t sign up for its sh*tty deal (which is so complicated that you’d be best advised to obtain degrees in accounting, taxation, pharmacy and health care administration before attempting to parse it).

Earth to gov: when folks are Tasered into compliance, they aren’t ‘customers.’

Which means that anyone who knows what a deductible is will look at the Bronze plans and quickly intuit that they’re damned if they do and damned if they don’t, since they won’t see any benefit from paying premiums (at whatever price) unless they can magic another $6,000 into existence.

Are these clowns who can’t figure out why we’re not buying being purposefully obtuse, of do they really just not understand what poverty means (and entails)?

The eternal question: Are the elites stupid and/or evil?

Uncaring is probably better than stupid. Back during the website fiasco, Obama noted how “we” are just learning buying Health insurance is complex. Obama cared so little, he didn’t even bother of understand issues around his signature achievement.

“What we’re discovering, is that you know, health insurance is complicated to buy.” Barack Obama November 14, 2013. ACA is the closest thing to an achievement Obama has.

Evil doesn’t care and won’t work to address issues until it affects a perpetrator directly. A week before the Web site’s launch Obama compared the website to kayak .Com which is just a search engine. I think they just redirect traffic.

I’m sure there is a good deal of stupid too.

As today will apparently be TPP-day, I’m gonna go with evil.

Obama has been working toward the TPP since the beginning of his administration. The ACA was a holding action – keeping, enhancing, and entrenching privatized healthcare and predatory drug prices until “free trade” makes anything from HR 676 to the most pitiful sliver of a public option or drug re-importation, or the reversal of additional privatization facilitated by the ACA even more impossible in the US, and puts public-oriented programs in other countries in jeopardy.

Thank you for continuing coverage of this topic.

This is one way to show MSF, the highly visible organization opposing the TPP, how 21st Century class warfare is waged.

Air Strikes On Doctors Without Borders Hospital In Afghanistan ‘Possibly Criminal’: UN Rights Chief

Doctors Without Borders said in a statement: “All indications currently point to the bombing being carried out by international Coalition forces.”

The White House issued a statement from President Obama, in which he expressed his “deepest condolences,” to those killed and injured in the incident. It added the the U.S. Department of Defense had launched an investigation and the White House would wait for its results before making a definitive judgment on the incident.

Doctors Without Borders had angrily reacted to news of the bombing on Saturday, saying that they had repeatedly informed all parties to the conflict of the hospital’s location, and that “sustained bombing,” of the facility continued for 30 minutes after the organization notified U.S. and Afghan military officials that a medical facility was being struck.

During the strikes, the hospital was repeatedly hit during each raid, while surrounding buildings were left mostly untouched, according to a BBC report.

That $6,000 deductible is at most a best-case scenario, too. What with small networks on most plans, this can quickly turn into many times that.

As for the craptacular website and bureaucracy of 0Care, this is what I posted on the 9/30 Water Cooler: “0bamacare is great! /sarc. It’s an enormous time drain. Just got an 0Care notice for my mother’s coverage. Apparently they STILL have a data verification issue concerning her citizenship and threaten subsidy recovery. Mind, I submitted the copies of the US passport and Naturalization Certificate BOTH electronically AND through the mail last December. How much more ridiculous can this BS get?! As I type this I have been on the phone with 0Care marketplace for 40 minutes and no one can get to the bottom if this, except to suggest that I mail copies, AGAIN. Thanks 0bama!”

That phone call ended up lasting a bit over an hour, and ended with the promise that the issue was being “escalated” and someone will call in the next 30 days. Holding my breath I’m not.

Have you tried finding out the name for the boss or the boss above of the person you have talked to? These are government employees they are listed. You could just try calling directly. My guess is your lower state legislator has a staffer with nothing better to do than help you hound people. So few people vote, helping you is a big deal to state legislators.

Not Timothy G: That is exactly what we did for my mom last year. She and I collected all the papers we thought we would possibly need according to the awful care website and went to our local congressional representative’s office and said- HELP.

We ended up with an excellent staffer ( who knew because our representative is a filthy republican Ted Cruz loving tool and a half) who had us make an appt for two days hence. We did and he had three plans that fit our stringent criteria ( she has six doctors that she would die before changing!!) and budget. My mom was over the moon and much relieved. I cannot speak to other people’s experiences but I am glad we went directly to our congressional reps office. I still won’t vote for him but if his staffer runs( thanks Ethan Faulkner!) for any office from any party he has my vote… Competence and caring count I found out!!

Well that’s a positive, keeping them busy navigating the labyrinths of 0Care might prevent them from engaging in more nefarious activities!

I believe the waste of time and energy you describe was deliberately engineered into the system on purpose. The purpose is to wear millions of people out so completely that they have no time and energy left to think about “larger issues” or “social agitation” with.

I suspect a fair number of them think that anybody living above the Medicaid cutoff really has the cash to spare. They neither know nor want to know the real cost of living, or why bringing those costs down might be pound foolish.

I.e., the Joneses could spend less on groceries — but then they’d be more susceptible to “lifestyle illnesses.” The Smiths could move to a cheaper residence — but their kids would go to a crappier school, or the savings would get eaten up in transportation costs. The McDonalds can put off getting a new roof until their salaries go up relative to inflation, right? Except that hasn’t happened in ever. And so on.

To answer Lambert’s question: the elites are not necessarily stupid, but they are willfully and happily ignorant. Likewise, they may not be evil exactly, but they cannot or will not extend their compassion and understanding very far beyond the people they personally know.

But “stupid and evil” makes a perfectly acceptable shorthand.

Does the author have a plan for getting this solution through a Congress that would shut down the government rather than fund women’s health care?

Wouldn’t the first step be to replace the clowns who ran the party into the ground? When Bernie Sanders has to explain to the DNC that people want to vote for issues matter to them, you have to look at the Team Blue establishment. For example, many people in these parts were opponents of the Iraq War. Nominating a Hillary Clinton type isn’t exactly a motivator, and let’s be honest, she isn’t going to win the votes of women because she is a woman because that kind of person is to shallow to care.

In 2006 and 2008, the Democrats had a clear, progressive platform which own despite computerized gerrymandering which is named after a signer of the Declaration of Independence. The GOP didn’t invent it 2010, and the world wide Web went live In 91.

You have to two battles. The enemy from within and the enemy from without, and it’s unfortunate any Team blue voters wanted to cheer on their team instead of demanding results.

A good starting point would be firing anyone in the Congressional leadership, closing OFA, purging the DN, and begging Howard Dean to take over the DNC.

My money’s on the enemies from within. Always a sure bet.

Hope and change, baby! :)

What, exactly, is it that prevented the democrat party from passing single payer the same way it passed 0Care: through budged reconciliation? Dembots and obots are so damn willfully forgetful.

I think it’s time for this classic:

What’s willfully forgetful is to hand-wave the fact that conservative Democrats in the Senate at the time – Nelson, Pryor, Lincoln – would not have supported single-payer either way. But go ahead and reassure yourself that everyone willing to point out the impracticability of a plan you support is ideologically impure.

Wait a minute here, your original comment implies that it is the republicans who were the impediment. Matter of fact that’s dembots and obots favorite talking point. You are bit slicker than average, but nonetheless thanks for pointing out the ridiculousness of the “democrat party stands for the little people” talking point. Both parties are corporate shills, which invalidates the implied “0Care was the best that could be done” BS. Best for whom? Surely not for the regular people.

I miss the Obots. Y’all used to be so good. Now it’s just sad.

I suppose Barry was for spending on reproductive healthcare before he was against it? He super secretly supports women’s health but has to publicly oppose icky things like emergency contraception and abortion to keep from blowing his cover?

First, this should have been done in 2009. Second, I would examine the platforms of the various candidates, and consider voting for one that at least advocates the right policy. The first step to solving a problem is admitting you have one.

Ahistoric, much? When Ocare passed, without one single Republican vote, the Democrats completely controlled congress. If they passed that, they could have passed anything.

Furthermore: their loss of control of Congress – again, a historic defeat – was at least in part directly BECAUSE of their non-performance on health care. They are presently paying the price of their malfeasance. Unfortunately, so are the rest of us – except those lucky enough to have gotten through to Medicare, an actually decent plan which could use considerable improvement.

And finally: you’re just parroting Dem propaganda, so it’s probably a mistake to take you so seriously.

Yes, ObamaCare was passed via “reconciliation,” so no Republican votes whatever were required, as you point out.

The second way to pass ObamaCare despite Republican opposition would have been to abolish the filibuster. Reid actually abolished the filibuster in 2012 IIRC, but only to get some appointments through the Senate. Apparently, though, it’s entirely impossible to abolish the filibuster to save thousands of lives and billions of dollars with single payer.

So, ahistoric a lot.

The Affordable Care Act (Obamacare) should be renamed to more accurately describe the program. I suggest the Unaffordable Care & Forced Bankruptcy Act.

Regarding dead links, my own experience in Washington state is that dead links abound within the state government websites, the insurance company websites and the medical network websites. Also, the latter two websites contain misinformation about which doctors will accept the insurance product.

I had to make a rare trip to the doctor recently. As I was checking in, the receptionist informed me that I have a $6,000 deductable, of which five thousand blah blah blah was still left. I knew this of course, but just hearing someone else say it out loud made me want to laugh/cry.

A sick, very sick system.

In fact TINA.

There is no alternative to single-payer that does what needs to be done. But there are infinite ways to gum up single-payer systems to defeat them. Even there, the simple idea: you get health care; the government pays the bill; taxpayers collectively pay the bill pooling the money as a risk fund. Where the complexity enters are the providers (and some patients) who will play financial games with the system. The years of pushing managed care with professional MBA-trained managers has created a large provider culture of gaming the system. That will not go away easily even under a single-payer system. The current bunch of politicians likely to get into power would even then eff up a single-payer system with deductibles, co-pays, and all sorts of rules to “ensure that the money is spent properly” and involve lots of accountants and billing specialists, and …because the health care industry (including insurance) is 1/6 of the jobs in the economy.

Even with that reality TINA to single payer. Just get ready to criticize what you get even then. Or find better politicians.

Here’s my idea to make their heads explode if you have money. Set up your stash so you’re generating tax free income only to live off. Take the federal subsidy and buy a platinum plan with it on the exchanges. I get so tickled thinking about gaming the system that way.

I’ve always suspected there was a reason why tax free income has it’s very own line item on the 1040. That’s probably it right there.

If that works, there are yet MORE serious glitches in the bill.

The tax free income (though not used in calculating the tax) is on page 1 which totals up at the bottom as one’s AGI – the number used to calculate income for Obamacare (before taxes).

Except, (U.S. Code § 5000A – Requirement to maintain minimum essential coverage)

You’re right! I wrote in haste. (And isn’t it amazing that there’s been no tax resistance from Republicans, since there’s no cost to it? And I made that point so many times, so 50 slaps with a wet noodle to me!)

Is it possible that a person who fails to pay the penalties can have his or her wages garnished? Or perhaps future Social Security payments could be seized? These would not be criminal penalties. I’m not asking rhetorical questions: I really don’t know.

No, it really isn’t. As David points out, the law doesn’t permit that. OTOH, I imagine you’d go on some sort of list….

They take it out of your tax refund, so it’s better not to have one. Might be able to go on for a long time that way.

It’s one of many very odd features of of the bill.

iirc Yves posted about this topic.

iirc the IRS would not garnish wages, but it would garnish a future refund, with interest that is higher than CPI inflation rate. This IRS interest rate was ~3.3% at the time of that Yves article.

For example,

1 assume John Doe was uninsured & subject to the ACA Individual Mandate in 2014, but owed money in John’s 2014 tax return.

2 Then in years 2015-2022 John IS INSURED, but owes money on each of his 2015-2022 returns.

3 Then in 2023 John continues being INSURED, but “screws up” by not withholding “enough”, so that on his 2023 return he would receive a refund of $1000. However, now that ancient 2014 ACA Individual Mandate Penalty is compounded at the high IRS rate, and that amount is extorted off of the refund. Thanks 0bama TM!

I would submit that the Time Tax TM idea would apply here. Even if John was “responsible” to insufficiently withhold in 2023 and thus “got away” without paying the ancient 2014 Individual Mandate Penalty, the time/effort/stress tax of micromanaging his withholding, & possible having more complex annual tax return paperwork, for 10 years, probably exceeds the ~$100-500 that the actual 2014 Individual Mandate Penalty Tax would’ve been.

If the situation has changed, &/or my understanding is incorrect, I would love to read your correction. It seems that with the ACA, specific aspects are changed frequently at random by the Exec branch with no/little notice or attention

BTW, whatever TF happened to the Employer Mandate? Last I heard, it was Indefinitely Suspended, and that a Wack Arnolds hack lobbyist had cried to 0bama that it was “too burdensome” to comply with currently, so 0bama of course suspended it. So the mandate is “too burdensome” to MegaCorps with historically high cash reserves, & armies of employee & elite BigName consultant accountants, but is “not burdensome” to Individuals, many of who have low savings, all of which self-file via tax software, or pay an non-CPA tax preparer at the retail H&R Block store. Thanks 0bama TM! Oh also thanks economist & 0bama water-boy Paul Krugman, who IIRC defending this Satan Samwich TM of enforcing the Individual Mandate while suspending the Employer Mandate.

Yes. Since I never get a refund, it didn’t occur to me to add this. Thank you.

I don’t think so…

From the link above.

From the IRS,

Note the “may” and no mention of future returns.

Yet another reason to always owe tax in April.

Forget what I wrote, I’ve seen some other sources that agree with you.

Unfortunately, this time of the year is not just for the latest O-care circus. Yesterday I received my 1/4 thick Medicare & You 2016 booklet along with my Express Scripts 1/4″ thick booklet on changes to the various Part D Rx plans they offer.

Time to find out which of my minimal number of drugs will still be covered, what new co-pays and deductibles will be, etc. And of course, if I’m lucky, the same AARP Medi-Gap policy that I have this year will be available in 2016.

Seems like you guys are placed in a position something like not only are you being forced to buy an automobile, you have to buy either a Ford Edsel, a Pinto or an AMC Pacer. If you’re prepared to splash the cash and go for the fancy option, then you can have a carb fed Chevvy Camaro from the 1980 model year complete with first generation emissions control device.

Or you can pay a fine.

The fine would appear to be cheap at twice the money in that case.

The real joke is that squillionaires can buy a DeLorean and think that they’re getting something utterly totally fabulous compared to what the plebs can afford to buy.

They should at least have the decency to offer all a TESLA with a tax credit!

Recently helping a just-turned-26 child shop on a state exchange drove home the insanity of the ACA, which until now had been an abstraction. Unless you have years of experience dealing with insurance companies and understand all the gotchas they are constantly coming up with, it would be impossible to really know how flawed many of the policies are. (For that matter, the Navigators don’t seem to know much either, but that’s probably a feature not a bug.) The idea that un-insured, many of whom leading struggling and stressed lives, will be able to choose a plan that’s good for them is something only Heritage could have dreamed up. I’m duly impressed that so many people are choosing `none of the above’.

The TPP is getting close:

Senior officials meeting in Atlanta had sought to wrap up in just two days of high-level talks, but a final deal was delayed by a fight over intellectual-property protection for biologic drugs between the U.S., which has argued for longer protections …

http://www.wsj.com/articles/countries-inch-toward-trans-pacific-partnership-trade-deal-1443974873

Any single payer country that signs on to TPPA including pharma needs to understand what Obamacare has done in America in the article below and understand how drug development has gone from research laboratories and science to Wall Street and financial engineering:

Valeant’s Drug Price Strategy Enriches It, but Infuriates Patients and Lawmakers

http://www.nytimes.com/2015/10/05/business/valeants-drug-price-strategy-enriches-it-but-infuriates-patients-and-lawmakers.html

I and my demotivated, willfully-options-‘ignorant’ self elect to once again pass on the current enrollment period and continue to simply pay cash for services rendered. It is stunning how much provider-selection and price-negotiating power (and incentive!) paying cash gives one. Of course the elites are all too aware of this ‘secret’ to actually making medical care affordable, which is why they continue to do everything in their power to make it illegal to opt out of the ever-more-rapacious medical-industrial-insurance-complex clusterfvck.

Well, up to a point. Your GP may love getting paid cash for a physical, but if you ever need hospital care — hospitals actually charge the uninsured more for the same procedures (unless that has changed, and I doubt it has).

Hospitals typically charge the payor the lesser of list price or whatever any preexisting agreements dictate, and the payor typically bargains down from there. Because insurers, who are typically on net whenever-we-feel-like-it terms, tend to pay more slowly than individuals that do pay, most hospitals will offer a substantial discount to self-payors to encourage them not to blow off the bill.

It’s a marketplace that people are forced to enter (and I’ve always felt that this should have been the principled[6] conservative objection to it.

There is a larger principle at play here, regarding the legitimacy that governments have to create and enforce markets. I believe that in attempting to create this ACA insurance market/racket by forcing people into something they don’t want to be in, the government has sacrificed a good portion of its moral authority to enforce the existence of its other markets. Well it’s no mystery where this is headed. Governments that do enough stupid things simply go away after a while.

A highly anticipated purpose of the ACA is to habituate people to self destructive mandated relationships (wrapped in marketing double-speak) with private enterprise. This is not the last such disaster, but rather one the first.

That might work on the drawing board of some thinktank in DC. In the real world though a formerly complacent population starts weighing the pros and cons of breaking out the guillotines after a while of that. The sudden popularity of Trump and Sanders is a sign that things are already heading that way.

The question is, have the masses noticed that Trump’s proposed tax plan is a huge cut for the wealthiest?

I wonder if Trump has. This does answer my question about how populist he really is, though.

Answer: until his own ox is gored.

From my perspective, that’s irrelevant. The important thing about Trump is that he appears to be crazy and a megalomaniac, and therefore he has the greatest chance of wrecking the applecart.

If it were Trump v. Biden, I’d have to give it some thought.

What if it were Trump versus Clinton?

I’d have to give that some thought, too.

“Trump versus Clinton?”

Either way you give validity to neoliberalism…. its just the Ghost Busters question of – what form will the destructor take – its up to you too choose bit…

Skippy…. Sci Fi triumphs again – !!!!!! – marsh mellow man brand identifier or lusty feral interdimensional canine…. absurdly delicious…

I am in healthcare and I am opting out. The fine and paying cash is a better option for me. I travel and use various agencies, this healthcare law is useless. Better to see the dentist and fill my regular scripts in cash with an APRN at a pharmacy. Most regular care that is recommended is a waste. My PCP gets furious because I am a noncompliant patient, oh well. Next stop the bitter cold of Maine. Need to stock up on respiratory meds!

What is going up faster the fine or general cost of policy (narrow network/copays/deductables/policy/narrow formulary)?

Years ago, I knew of a woman who called her vet for a urinary tract infection. Does anyone else feel like it’s 1972 again?

Did the vet help her? I’ve long thought vets, who are taught to work on multiple animals, are better qualified to work on people than doctors are to work on animals.

Cranberry juice helps; so does baking soda treatments. (My wife’s pretty doctor-phobic.)

These plans are only good for a serious trauma or illness. Most scripts can be filled at chains for $4, just don’t get the new fancy stuff. Actually bad teeth can cause a lot of problems. APRNs also spend a lot more time with you than an MD. If you get one with a lot of experience can be just as good as an MD with chronic issues. They all follow the same algorithms given to them by insurance companies & committees.

thanks for sharing your story.

It is sad that USian healthcare workers exist, where their job does not provide employer-provided health insurance.

I would love for someone like yourself on a debate show against an ACApologist like the HHS Sec Burwell. Burwell’s head might explode from the ACApologist bias incorrect notion that only “uniformed” people opt out of the ACA, although said head explotion probably wouldn’t be covered by an ACA policy.

There are policies available, but they are garbage.

Odd, the ‘economic man’ and his ‘rational profit maximizing actions’ ideology that undergirds neoliberalism isn’t seen as a valid response by plebs to the ACA, even by this neoliberal Dem administraton. “Working people making “calculated decisions”! “

The whole marketing portion reminds me of businesses that will not stop sending solicitations through the mail; whose marketers seem to believe that a different envelope design or a different phrasing of the same offer will somehow magically change their targets’ minds.

If the item in question is a chicken parm sandwich, that might be the case. Insurance that someone can’t afford is — well, I’m sure there’s some Econ term for it, “inelastic individual demand,” or some other obfuscatory malarkey, but it boils down to people not buying what they manifestly cannot begin to afford.

I might want a Tesla, for example, but I’m not going to get one — and the reason isn’t Tesla’s marketing.

choose to remain uninsured. to oversimplify—

If I get hit by a bus and have Obamacare, I’d be bankrupt from the coinsurance and the deductible.

If I get hit by a bus without Obamacare, I’d be bankrupt from the ER bills but would have lived a bit more comfortable life in the interim.

glad to read that i’m not alone in my thinking.

Perfect comment. Sums it up in a few sentences. Wonder if anyone from HHS reads this.

A question that bothered me from the start is how deductibles and co-pays are categorized. The law still provides that for medical expenses, you can write off the outstanding debts without having to liquidate your home and other necessities.

But the ACA never changed the designation of the deductibles or co-pays. I suspect that it will be a lot harder to discharge these expenses under ACA and would possibly lose your home in the process.

Odd though, I have seen no data regarding medical bankruptcies. It’s as if they stopped tracking this data. I haven’t heard of any antidotal bankruptcies either. Something particularly scary when you don’t have any data at all to work with.

After Romneycare was passed there were studies done and they showed there was no real change in the medical bankruptcy rate. I have since tried to find these studies and I am unable. They were done by people at Harvard & other Mass based universities, good luck.

Re: Fines.

If you don’t pay your utility bill and get a disconnect notice, you can get a waiver for the fine (with the correct form, of course).

IRS may have the best ACA stats. Through April 30th:

2.6M returns with a Premium Tax Credit form

10.7M returns with at least one exemption

6.6M returns with a penalty (aka Shared Responsibility Payment)

Kind of interesting how penalty returns and exemptions dwarf the number of returns reconciling their Premium Tax Credits. Also, the stats above are returns, not individuals. The count of individuals would be higher.

Stats listed in:

http://www.taxpayeradvocate.irs.gov/Media/Default/Documents/2016-JRC/Volume_1.pdf

Speaking for the other end of the spectrum I am an early victim of the Cadillac Tax. Our union just negotiated a new contract where the company told our negotiators that there was no way they would pay the extra tax for our insurance so they had to figure out how to crapify it enough to be under the cap. The result is this January our co-pays for visits, prescriptions, surgeries and basically anything that we can be charged for will go up and then in 2 years they’ll go up some more for a total increase between 150-250%.

According to economists this isn’t supposed to happen. The company should either a) pay the tax to help subsidize those on the exchanges or b) reduce the cost of the offered plan and give the workers the difference. Our company chose c) reduce the plan and pocket the difference.

The rank and file are upset because while our wages were cut a long time ago the positive was we had better health insurance than anybody around. Now we don’t even have that. It’s so strange how only a handful of us understand how Obamacare gave leverage to the company to cut our health benefits.

In exactly the same week late in Summer last I had friends or family at 3 separate companies in 3 separate states tell me that their companies announced that because 2016 Cadillac Tax they would now have crapified healthcare coverage. In all three cases company HR reps carefully explained that it was not the company but rather Obamacare that was “to blame.” In one SFBay area case the new narrow network excluded the Stanford health system because (the HR peeps openly said this at the meeting, I was told) a handful of employees — or their children — had serious health care issues and were going to Stanford– and driving up the overall cost of care. So you just can’t see those providers any more. Problem solved from HR’s point of view, I guess.

Barry taking one for the team. No doubt his post-presidential bank account will be richly renumerated for his selfless service.

Your union should have tried to negotiate for option b) and got some wage increases for the concession. I don’t think anyone with no union representation is likely to get b).

Did Obamacare “give leverage to” the company to cut your healthcare benefits? Or did Obamacare “torture the company into” cutting your healthcare benefits? It seems to me that Obamacare was designed to FORCE companies to crapify their benefits. That was an Obama goal, not a company desire.

Or am I wrong?

You keep knocking ’em out of the park Lambert. Great work!

Oh but we did negotiate for a raise… and got a whopping 50 cent per hour increase with no COLA going forward because our future raises will be used to keep our health insurance costs down.

Why does the website eat my posts

Exactly when did it become possible to get single payer past the Republicans?

The same day the democrats used reconciliation to get 0Care past the republicans. All that lacked was any actual intention to implement single payer, soaring speechifyin’ notwithstanding.

As pointed out elsewhere on the thread, when ObamaCare was passed through the reconciliation process, and/or the Democrats controlled the Senate? For now, we’ll have to try to focus on electing a Presidential candidate who supports the policy.

But you weren’t really asking a serious question, were you?